Key Takeaways

- New Zealand's primary business structures — including the Limited Company, Limited Partnership, Co-operative Company, and Overseas Company Branch — are registered and overseen by the Companies Office, a unit of the Ministry of Business, Innovation and Employment (MBIE).

- The limited company (Ltd) is the most widely used incorporated structure in New Zealand, suitable across a broad range of commercial activities under the Companies Act 1993.

- Co-operative companies operate under a separate legislative framework, the Co-operative Companies Act 1996, distinguishing them from standard limited companies in both governance and member-based trading arrangements.

- Overseas entities can establish a legal presence in New Zealand without separate incorporation by registering either as an overseas company branch or as a New Zealand-registered foreign company.

Introduction to Entity Types in New Zealand

New Zealand is an independent sovereign nation located in the southwestern Pacific Ocean, situated approximately 2,000 kilometres southeast of Australia. The country operates under a parliamentary democracy with a well-established legal system derived from English common law.

Company registration and ongoing compliance are administered by the Companies Office, a business unit of the Ministry of Business, Innovation and Employment (MBIE). Businesses are also subject to oversight from the Inland Revenue Department (IRD) for tax purposes. New Zealand applies a residence-based tax system with a standard corporate tax rate and has an active network of double tax agreements.

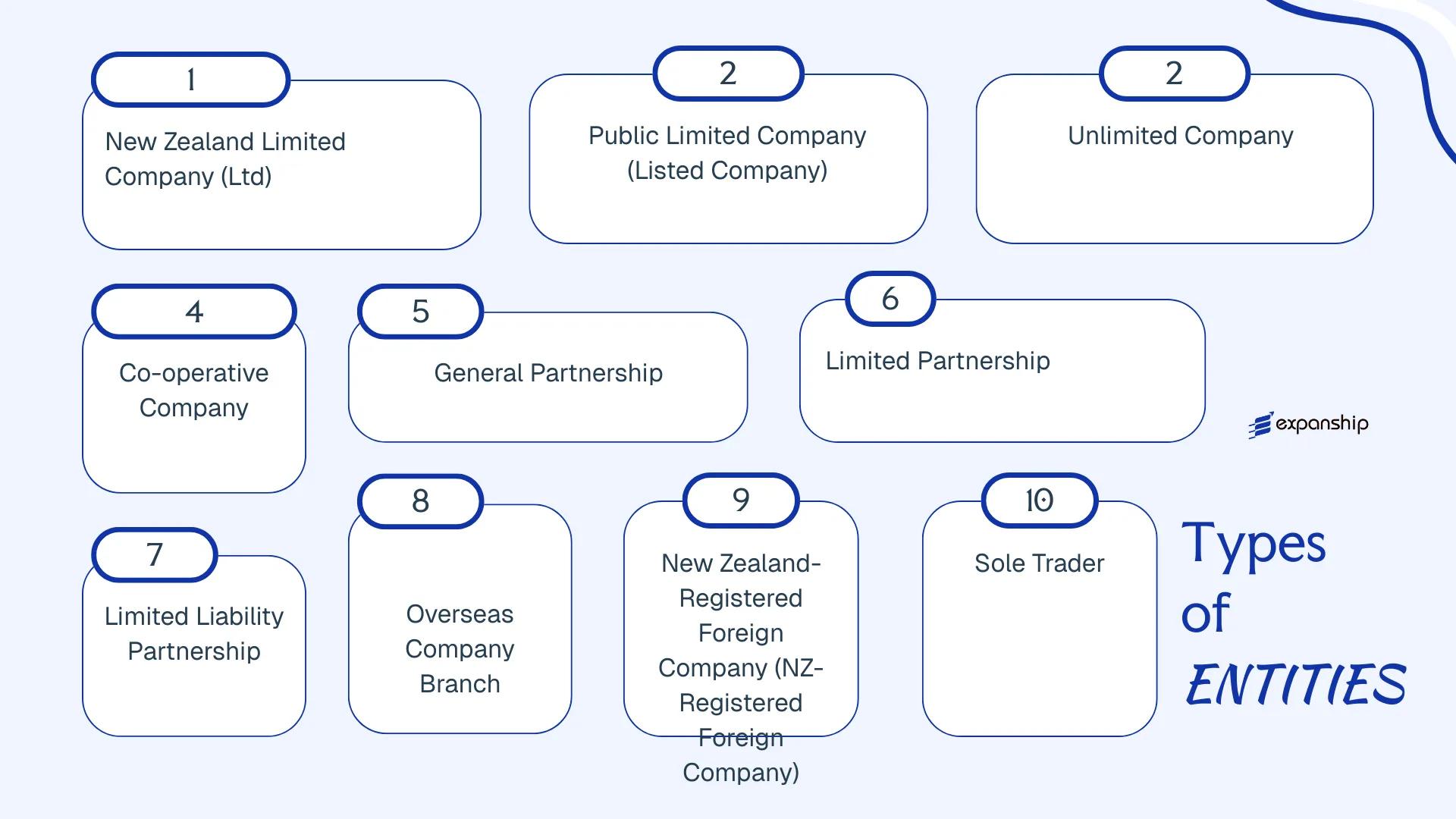

Several types of business entities in New Zealand are available to both resident and non-resident operators. These include the Limited Company, Listed Company, Unlimited Company, Co-operative Company, General Partnership, Limited Partnership, Limited Liability Partnership, Overseas Company Branch, New Zealand-Registered Foreign Company, and Sole Trader.

Each structure carries distinct implications for liability, governance, and taxation. This article examines each entity in detail to help you determine which structure fits your commercial objectives.

An Overview of Business Structures in New Zealand

New Zealand's company law framework accommodates several distinct business structures, each governed primarily by the Companies Act 1993, with additional legislation applying to specific entity types. Structures range from private limited companies to co-operatives, partnerships, and registered foreign businesses. Each form carries different implications for liability, ownership, and tax treatment.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Limited Company (Ltd) | Separate legal entity | Limited to shares | Taxed | Yes | 1 shareholder | Companies Office | Companies Act 1993 |

| Listed Company | Separate legal entity | Limited to shares | Taxed | Yes | 1 shareholder | NZX / Companies Office | Companies Act 1993 |

| Unlimited Company | Separate legal entity | Unlimited | Taxed | Yes | 1 shareholder | Companies Office | Companies Act 1993 |

| Co-operative Company | Separate legal entity | Limited | Taxed | Yes | 5 shareholders | Companies Office | Co-operative Companies Act 1996 |

| General Partnership | Not separate | Unlimited | Pass-through | Yes | 2 partners | Inland Revenue / MBIE | Partnership Act 1908 |

| Limited Partnership | Partially separate | Mixed | Pass-through | Yes | 2 partners | Companies Office | Limited Partnerships Act 2008 |

| Overseas Company Branch | Extension of parent | Parent's liability | Taxed (NZ income) | Yes | N/A | Companies Office | Companies Act 1993 |

| Sole Trader | No separation | Unlimited | Pass-through | Yes | 1 person | Inland Revenue | Common law / IR |

Each of these structures is examined in full in the sections below.

New Zealand Limited Company (Ltd)

Governed by the Companies Act 1993, a New Zealand limited company Ltd registration creates a body corporate with a legal identity entirely separate from its shareholders. This structure is the most widely used commercial vehicle in the country, suitable for both domestic operations and foreign-owned trading or holding activities.

Shareholders' liability is confined to any amount unpaid on their shares. The entity can own assets, enter contracts, sue, and be sued in its own name, independent of the individuals behind it.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company (body corporate) | Incorporated under the Companies Act 1993 |

| Members | Shareholders (min. 1, no maximum) | Shareholders can be natural persons or legal entities, resident or non-resident |

| Directors | Min. 1 director; at least 1 must reside in NZ or Australia (if Australian, must be director of an Australian-registered company) | Directors are personally responsible for statutory obligations |

| Local Presence | Registered office in New Zealand (physical address, not a PO Box) | Required at all times; must be accessible during business hours |

| Share Capital | No minimum capital requirement; NZD is the standard currency | Shares can be of one or more classes with different rights |

| Privacy | Shareholder and director details filed with the Companies Office and publicly searchable on the Companies Register | Beneficial ownership disclosure requirements apply under AML/CFT rules |

Focus Points

- Taxation: Subject to corporate income tax at 28%; GST registration required if turnover exceeds NZD 60,000 annually; dividends may carry imputation credits; withholding tax applies to dividends, interest, and royalties paid to non-residents at rates varying by tax treaty.

- Annual Compliance: Annual return filed with the Companies Office; financial statements prepared in accordance with NZ GAAP (or IFRS for larger entities); audit thresholds apply based on size criteria.

- Treaty Access: New Zealand maintains an extensive double tax agreement network, making NZ Ltd companies eligible for reduced withholding rates on cross-border income flows.

- Economic Substance: No specific substance legislation equivalent to some offshore regimes; however, tax residency is determined by place of incorporation or central management and control.

- Conversion: A limited company may convert to an unlimited company or amalgamate with another company under Part 13 of the Companies Act 1993 without requiring a new registration.

Closing

A New Zealand Ltd suits trading businesses, holding structures, and IP ownership vehicles where limited liability and access to tax treaties are priorities. The director residency requirement is the most common structural hurdle for non-resident founders.

Foreign investors and domestic entrepreneurs seeking a tax-resident, treaty-eligible entity with straightforward incorporation and no minimum capital requirement.

Company Incorporation in New Zealand

Incorporate a New Zealand Limited Company with Expanship's end-to-end support, from registration to compliance setup.

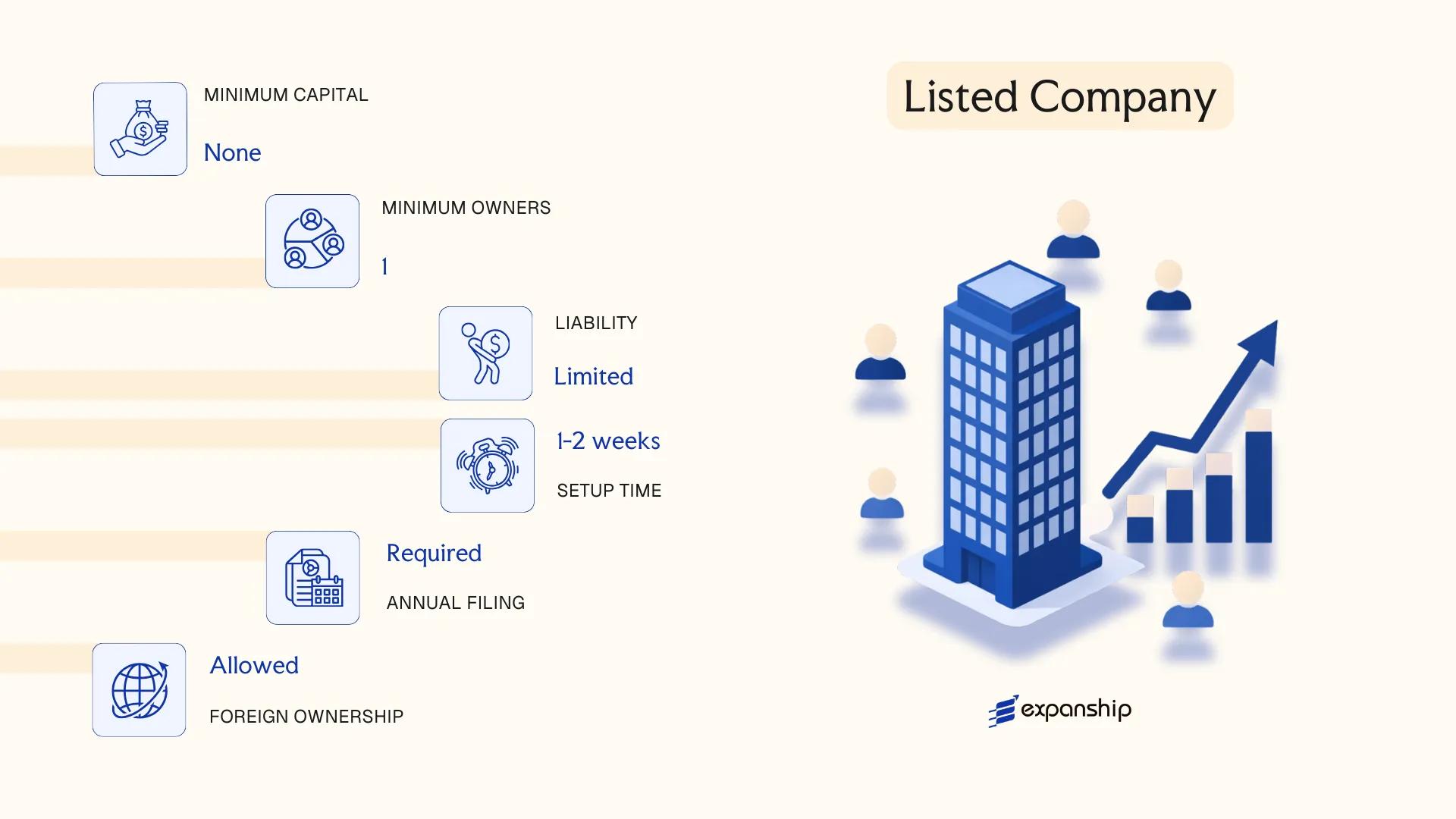

Listed Company (Public Limited Company)

A New Zealand listed public limited company is a company whose shares are quoted and traded on a recognised securities exchange, most commonly the New Zealand Exchange (NZX). Governed by the Companies Act 1993 alongside the Financial Markets Conduct Act 2013, this structure carries separate legal personality and limits shareholder liability to the amount unpaid on their shares.

Listing on the NZX subjects the entity to a dual regulatory layer: the Companies Office administers corporate law obligations, while the Financial Markets Authority (FMA) oversees securities law compliance. Continuous disclosure obligations, periodic financial reporting under NZ IFRS, and NZX Listing Rules collectively define the compliance burden for any publicly listed company.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by shares | Incorporated under the Companies Act 1993; listed on NZX or other recognised exchange |

| Members | Shareholders — minimum 1 director (NZ resident or an NZ-resident director required); no cap on shareholders | At least 1 director must be resident in NZ or Australia |

| Local Presence | Registered office in New Zealand required | Must maintain a physical address on the Companies Register |

| Capital | NZD; no statutory minimum, but NZX sets minimum spread and market capitalisation thresholds for listing | NZX Main Board requires minimum 500 shareholders and NZD 15M market cap (general guideline) |

| Disclosure | Continuous disclosure of material information to NZX and FMA | Non-compliance carries FMA enforcement action |

| Privacy | Low — accounts, shareholder registers, and director details are publicly available | Annual financial statements must be audited and filed |

Focus Points

- Taxation: Subject to 28% corporate income tax; GST at 15% applies to taxable supplies; dividends paid with imputation credits to avoid double taxation; withholding tax applies to unimputed dividends paid to non-residents.

- Annual Compliance: Mandatory audited financial statements under NZ IFRS, annual returns to the Companies Office, and continuous disclosure obligations to NZX and the FMA.

- Treaty Access: New Zealand's double tax agreement network is available to resident companies, reducing withholding tax on cross-border income flows.

- Conversion: A private company may convert to a listed structure through an initial public offering (IPO) process, subject to NZX admission requirements and FMA product disclosure statement obligations.

- Restrictions: Foreign ownership is not capped at the corporate law level, though investments above certain thresholds may require Overseas Investment Office (OIO) consent depending on the assets held.

Closing

A listed structure suits businesses seeking access to public capital markets, typically at an established stage of growth. The primary advantage is access to equity funding from a broad investor base; the corresponding limitation is the significant ongoing compliance cost and public disclosure of financial and operational information.

Best suited for large, established businesses or those seeking public capital raises that can absorb the ongoing regulatory and reporting costs associated with NZX listing requirements.

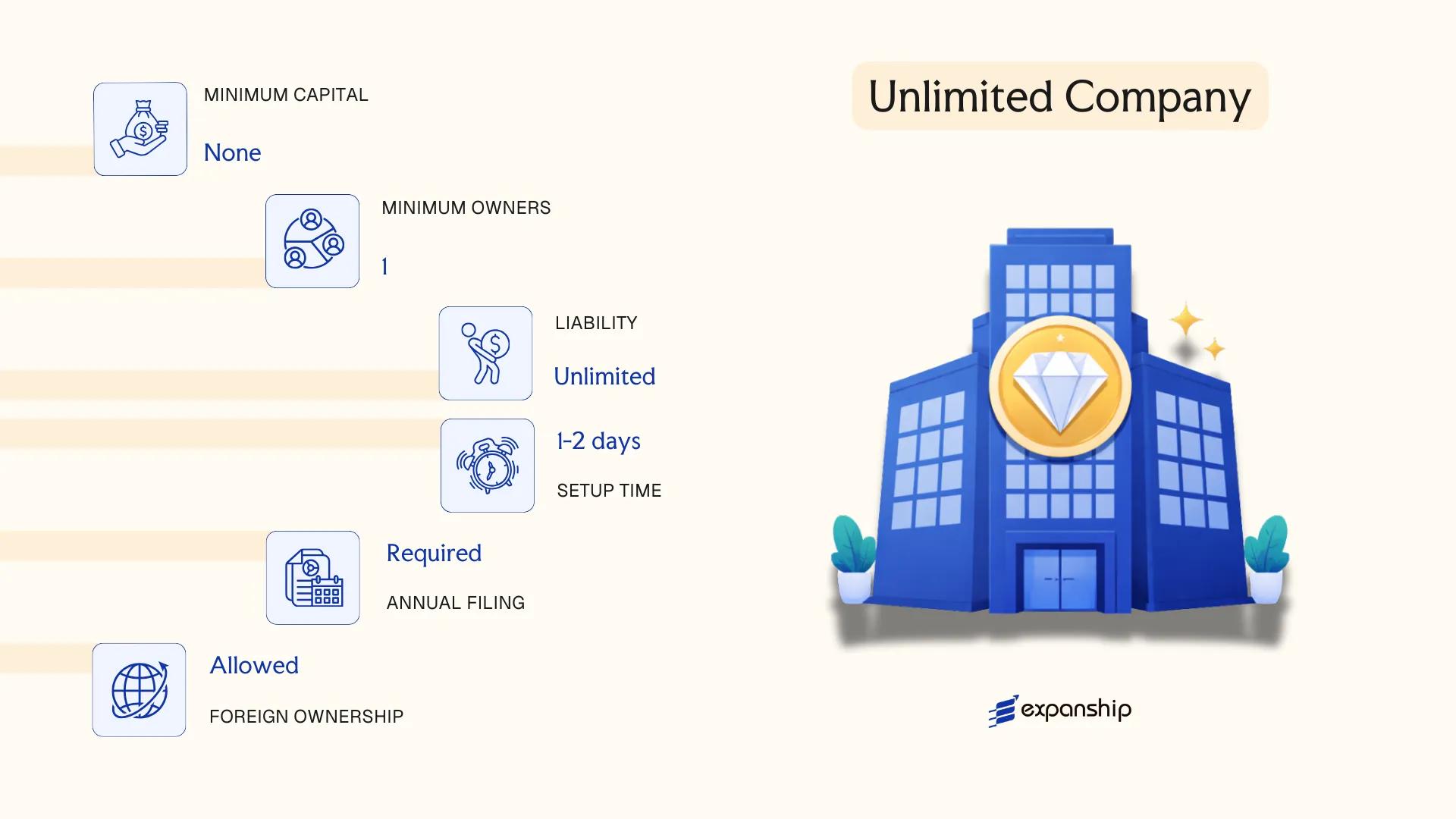

Unlimited Company

Registered under the Companies Act 1993, the New Zealand unlimited company structure is a distinct corporate form that carries separate legal personality while removing the liability shield ordinarily afforded to shareholders. Unlike a standard limited company, members bear personal, unlimited liability for the debts and obligations of the business should it be wound up with insufficient assets to meet its creditors.

This makes the unlimited liability company NZ variant relatively uncommon in practice. Its primary appeal lies in specific regulatory or structural contexts, such as group reorganisations or intra-group financing arrangements, where unlimited liability is deliberately accepted in exchange for certain accounting or disclosure advantages that may apply under applicable legislation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated company with separate legal personality | Registered under the Companies Act 1993; unlimited member liability on winding up |

| Members | Shareholders; minimum 1, no maximum | No distinction between share classes is mandated; structure is flexible |

| Directors | Minimum 1; at least 1 must be ordinarily resident in NZ or Australia | Residency requirement applies per Companies Act 1993 |

| Local Presence | Registered office in New Zealand required | Must be a physical address; cannot be a PO Box |

| Share Capital | No minimum capital requirement; NZD denominated | Shares may or may not have a par value |

| Privacy | Director and shareholder details are publicly available on the Companies Register | No option to suppress standard registration details |

Focus Points

- Taxation: Subject to standard corporate income tax at 28%, GST registration obligations apply where turnover thresholds are met, and withholding tax applies to dividends, interest, and royalties paid to non-residents; no separate tax treatment arises solely from the unlimited liability structure.

- Annual Compliance: Annual return filing with the Companies Office and financial statement obligations under the Financial Reporting Act 2013 apply in the same manner as for a standard limited company.

- Conversion: An unlimited company may be re-registered as a limited liability company under the Companies Act 1993, subject to shareholder approval and filing with the Companies Office.

- Treaty Access: Access to New Zealand's double tax agreement network is determined by tax residency, not by liability structure; unlimited companies qualify on the same basis as other resident companies.

- Restrictions: No restriction on foreign ownership, but the unlimited liability exposure makes this structure unsuitable where personal asset protection is a priority.

Closing

An unlimited company is occasionally used within corporate groups where the parent entity is willing to absorb liability, or in structures where reduced disclosure obligations under financial reporting rules provide an operational rationale. The key advantage is structural flexibility within group arrangements; the significant drawback is that members have no cap on personal exposure to company debts.

Best suited for wholly-owned subsidiaries within established corporate groups where the parent accepts unlimited liability and the structure serves a specific intra-group or reporting purpose.

Co-operative Company (under the Co-operative Companies Act 1996)

Governed by the Co-operative Companies Act 1996, a co-operative company is a distinct corporate structure designed for groups of persons who transact business with the entity as members, rather than as external investors. New Zealand co-operative company registration produces a body corporate with separate legal personality and limited liability, placing it structurally closer to a standard limited company while preserving rules that prioritise member transactions over external shareholder returns.

At least 60% of the voting rights must be held by transacting shareholders — those who actively supply goods or services to, or acquire them from, the co-operative. This statutory threshold is what formally distinguishes the structure from a conventional company under the Companies Act 1993 and makes it eligible to use the "Co-operative" designation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate (separate legal personality) | Registered under the Co-operative Companies Act 1996 |

| Members Referred To As | Transacting shareholders and investor shareholders | Transacting shareholders must hold at least 60% of voting rights |

| Minimum Members | Minimum 2 shareholders | No statutory maximum |

| Local Presence | Registered office in New Zealand | Must maintain a registered office address at all times |

| Capital | NZD; no minimum share capital requirement | Shares may be redeemable; terms set in constitution |

| Privacy | Director and shareholder details on public register | Searchable via the Companies Office register |

Focus Points

- Taxation: Subject to standard corporate income tax at 28%; transacting rebates paid to members may be deductible for the co-operative; GST (15%) applies to taxable supplies; no special co-operative tax concessions exist at the entity level under the Income Tax Act 2007.

- Annual Compliance: Annual returns filed with the Companies Office; financial statements required; audit obligations depend on size thresholds.

- Conversion: A co-operative can convert to a standard company under the Companies Act 1993 if it ceases to meet the 60% transacting shareholder threshold or by shareholder resolution.

- Restrictions: Cannot hold the "Co-operative" name or designation unless the 60% transacting shareholder rule is maintained on an ongoing basis.

- Treaty Access: As a New Zealand tax resident, the entity can access double tax agreements, subject to standard residency and beneficial ownership conditions.

Closing

A co-operative company suits member-owned trading operations in sectors such as agriculture, dairy, or retail purchasing groups, where the primary benefit flows to those who transact with the business rather than passive investors. The structure formally limits external investor influence but creates ongoing compliance obligations around maintaining the 60% transacting shareholder threshold.

Producer groups, agricultural cooperatives, or member-owned trading businesses where ownership and commercial activity are intended to remain aligned within the same member base.

Partnerships in New Zealand [General Partnership, Limited Partnership, Limited Liability Partnership]

New Zealand partnership types — general, limited, and limited liability — are governed by distinct statutes. General partnerships fall under the Partnership Act 1908, while limited partnerships are governed by the Limited Partnerships Act 2008. Neither a general partnership nor a limited partnership carries separate legal personality under New Zealand law, though a limited partnership does offer liability separation between general and limited partners.

Registration requirements differ by structure. General partnerships do not require formal registration with the Companies Office, whereas NZ limited partnership registration is mandatory and must be completed through the Companies Office portal before the entity can operate.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (not a separate legal person) | Limited partnerships have registered status; general partnerships do not |

| Members | General Partnership: 2+ partners (no maximum); Limited Partnership: 1+ general partner, 1+ limited partner | General partners bear unlimited liability; limited partners' liability capped at their contribution |

| Local Presence | Limited Partnership: registered office in New Zealand; at least one general partner must be resident or a NZ-registered entity | General partnerships have no formal registration requirement |

| Capital | No minimum capital; contributions in any agreed form | NZ dollar denominated in practice |

| Privacy | Partner names disclosed on public register for limited partnerships | General partnership details not on public record |

Focus Points

- Taxation: Partnerships are fiscally transparent; income is attributed to and taxed at each partner's applicable rate. GST registration is required if turnover exceeds NZD 60,000 annually. No separate entity-level income tax applies.

- Annual Compliance: Limited partnerships must file an annual return with the Companies Office and notify changes to partners or constitution.

- Treaty Access: As flow-through structures, partnerships generally do not access double tax agreement benefits directly; treaty entitlement depends on the residency of individual partners.

- Restrictions: A general partner in a limited partnership cannot limit their personal liability; substituting or adding general partners requires amendment of the partnership's registration.

Sub-Types

General Partnership

Partners share management, profits, and unlimited personal liability equally unless a partnership agreement specifies otherwise. Commonly used by professionals and small trading businesses.

Limited Partnership

At least one general partner holds unlimited liability and manages the business, while limited partners contribute capital and are shielded from liability beyond their investment. Frequently used for private equity, venture capital, and investment fund structures.

Partnerships suit investment funds, joint ventures, and professional services arrangements where pass-through tax treatment is preferred over corporate structuring. The fiscal transparency is a clear advantage for multi-jurisdictional investors managing tax at the partner level, though the unlimited liability exposure of every general partner remains a material drawback.

Limited partnerships are best suited for investment fund managers and private equity sponsors who require capital pooling with liability separation for passive investors.

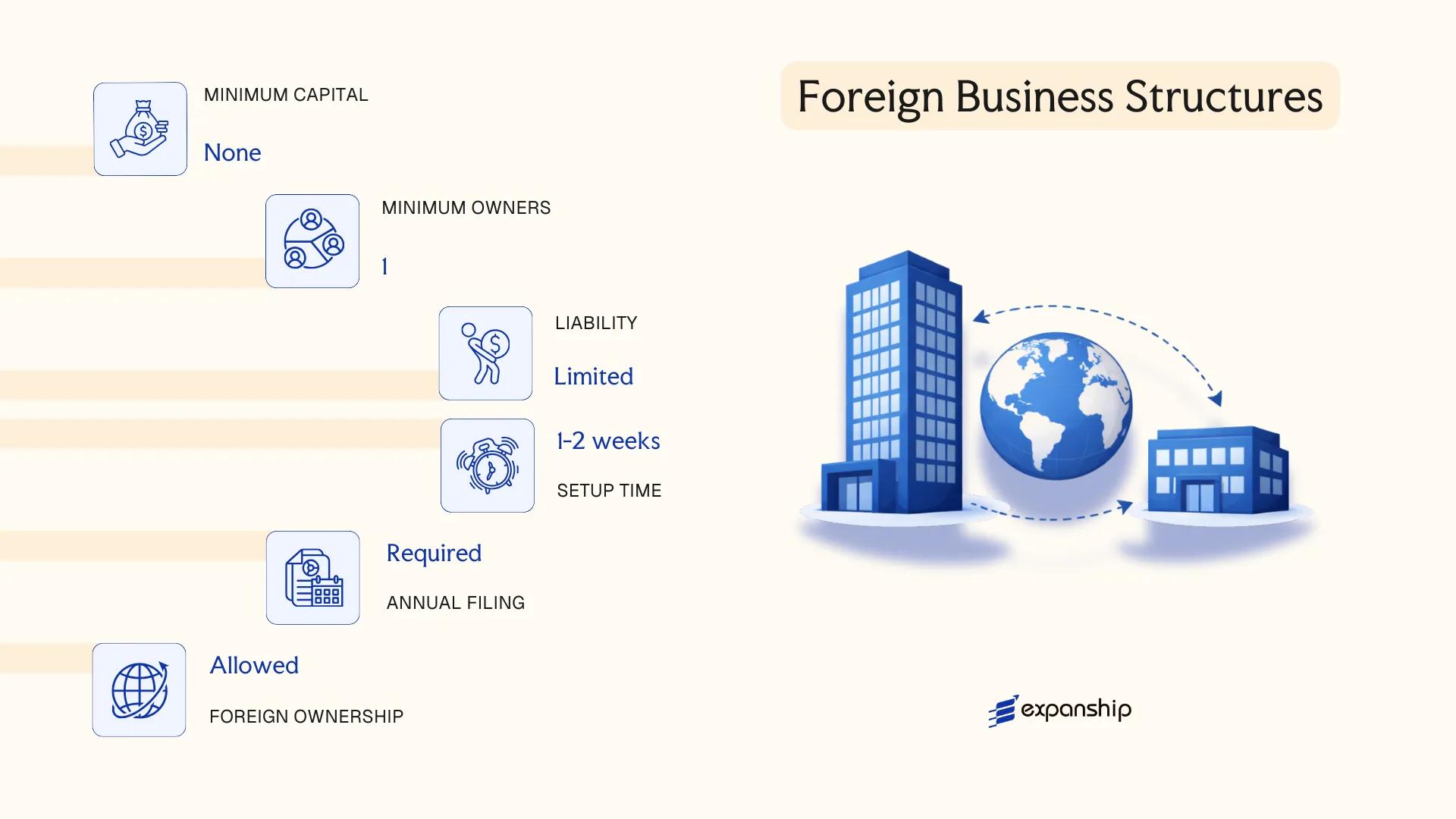

Foreign Business Structures in New Zealand [Overseas Company Branch, New Zealand-Registered Foreign Company]

Foreign entities seeking to operate in New Zealand without incorporating a local company have two primary options, both governed by the Companies Act 1993: registering an overseas company branch or establishing a New Zealand-registered foreign company. Registering an overseas company branch in New Zealand does not create a separate legal entity — the parent company remains directly liable for all obligations incurred through the branch.

Registration is administered by the Companies Office (part of the Ministry of Business, Innovation and Employment) under Part 18 of the Companies Act 1993. The branch carries no independent legal personality, meaning creditors can pursue the foreign parent directly. An overseas company must register within 10 working days of beginning to carry on business in the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch of a foreign corporation | No separate legal personality; parent entity bears full liability |

| Governing Persons | Directors of the overseas parent; local director or agent required | At least one contact person resident in New Zealand must be appointed |

| Local Presence | Registered office address in New Zealand; designated contact person | Physical address required; P.O. Box not accepted |

| Capital | No minimum capital requirement | Governed by parent company's home jurisdiction capital structure |

| Disclosure | Parent company financials must be filed if not otherwise publicly available | Financial statements of the overseas company may be required under the Financial Reporting Act 2013 |

| Privacy | Directors and contact person details publicly searchable on the Companies Register | Parent company constitution or equivalent document must be submitted on registration |

Focus Points

- Taxation: The branch is taxed in New Zealand on NZ-sourced income at the standard corporate rate of 28%; no separate withholding tax applies to profit repatriation to the parent, though dividend and royalty payments may attract withholding tax under domestic rules or applicable double tax agreements (DTAs).

- Annual Compliance: Annual returns must be filed with the Companies Office; financial statements of the overseas parent may require separate filing depending on size thresholds under the Financial Reporting Act 2013.

- Treaty Access: New Zealand maintains an extensive DTA network; branch profits attributed to NZ operations are generally covered, but treaty access depends on the parent's country of residence and the applicable agreement.

- Restrictions: Branches cannot issue shares, hold assets independently of the parent, or enter contracts in their own name — all legal acts bind the overseas parent directly.

- Conversion: A branch cannot be converted directly into a local limited company; a new entity must be separately incorporated and assets transferred through a formal restructuring process.

Sub-Types

Overseas Company (Trading Branch)

The standard form used by foreign companies conducting active business operations — sales, services, or distribution — from a fixed presence. The overseas parent remains the contracting party for all commercial arrangements entered into through the branch.

Overseas Company (Non-Trading / Representative Office)

Used for liaison, market research, or promotional activities where no revenue-generating transactions occur locally. Regulatory obligations are reduced, though registration under the Companies Act 1993 is still required if the entity is deemed to be "carrying on business."

Closing

An overseas company branch suits foreign businesses seeking operational presence without committing to a separate local incorporation, though the absence of liability separation between the branch and its parent is a significant structural drawback for risk management purposes. Costs and timelines for registration are generally lower than full incorporation, but ongoing parent-level financial disclosure obligations can reduce confidentiality.

Best suited to established foreign companies entering the New Zealand market on a short-to-medium term basis, particularly where centralised control and consolidated group accounting are priorities.

Sole Trader

A sole trader is the simplest business structure available, and sole trader New Zealand setup requirements are minimal by design. There is no dedicated legislation governing sole traders as a distinct legal form; instead, the structure operates under general contract, tax, and property law. Registration with the Companies Office is not required, though you must register for a New Zealand Business Number (NZBN) if you intend to transact formally.

Critically, a sole trader has no separate legal personality. You and your business are the same legal entity, meaning personal assets are directly exposed to business liabilities with no liability shield of any kind.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business structure | Not a separate legal entity from the owner |

| Member Title | Proprietor | Single individual only; no co-owners |

| Local Presence | No registered office required | An NZBN is strongly advised for formal dealings |

| Capital | No minimum capital requirement | NZD; entirely at proprietor's discretion |

| Privacy | No public register filing | No financial disclosures required |

| Governing Framework | General law (contract, tax, property) | Inland Revenue Department oversees tax obligations |

Focus Points

- Taxation: Income is taxed at personal income tax rates (10.5%–39%) via Inland Revenue; GST registration is mandatory once turnover exceeds NZD 60,000; no separate corporate tax applies.

- Annual Compliance: No annual returns or financial statements are required to be filed publicly; provisional tax payments apply if tax liability exceeds NZD 5,000.

- Treaty Access: As an unincorporated individual, access to double tax agreement benefits depends on personal tax residency, not a corporate structure.

- Conversion: A sole trader can convert to a limited company by incorporating under the Companies Act 1992 and transferring business assets accordingly.

- Restrictions: Cannot raise equity capital; cannot bring on partners or shareholders without restructuring into a different legal form.

Recommendations

A sole trader structure suits self-employed individuals and freelancers operating domestically with low liability exposure and modest revenue. The primary advantage is the near-absence of administrative overhead; the significant limitation is unlimited personal liability for all business debts and obligations.

Resident individuals conducting low-risk, owner-operated activity who do not require liability protection or external investment.

How to Choose the Right Entity Type in New Zealand

Selecting how to structure your business in New Zealand has direct legal and financial consequences that persist long after registration.

Why Your Entity Choice Matters

The wrong structure can create compliance failures that are difficult and costly to unwind. Consider these concrete outcomes:

- Registering as an overseas company branch when you intend to trade locally as a resident business may result in the Companies Office treating the entity as non-compliant, risking deregistration under the Companies Act 1993.

- Forming a company when a trust or other vehicle would better serve asset protection locks you into annual shareholder obligations, director duties, and filing requirements that do not apply to those alternatives.

- Selecting an entity without the capacity to maintain genuine local substance, where substance is expected, can trigger reporting failures and associated penalties under relevant tax legislation.

- Choosing a structure that mandates audited financial statements when your firm is a single-person operation adds recurring costs with no corresponding compliance benefit.

Key Factors to Consider

- Business Activity: Whether the entity will trade actively, hold assets passively, or operate in a regulated sector each points toward a different registration category.

- Ownership and Management: A sole operator has little reason for a multi-shareholder company structure, whereas joint ventures typically require clearly defined ownership instruments.

- Tax Objectives: Your need for treaty access, look-through treatment, or a specific tax regime determines whether a company, partnership, or look-through company is appropriate.

- Liability Exposure: The degree of personal liability you are willing to accept directly affects whether a limited liability structure or unlimited company form is suitable.

- Exit Strategy: Not all structures permit straightforward redomiciliation or conversion, so anticipated changes in ownership or jurisdiction should factor into the initial choice.

- Privacy Requirements: Director and shareholder details are publicly accessible on the Companies Register, which may influence whether nominee arrangements are warranted.

Compliance Services for Companies in New Zealand

Ongoing compliance support for New Zealand entities, including annual return filing, director obligations, and regulatory reporting.

Conclusion

Each entity type registered under New Zealand law serves a distinct purpose. The limited company (Ltd) is the most commonly incorporated structure, suited to a wide range of commercial activity. Listed companies are reserved for businesses seeking public capital markets access. Unlimited companies address specific liability and reporting needs, while co-operative companies, governed by the Co-operative Companies Act 1996, serve member-based trading arrangements. General partnerships carry joint and several liability; limited partnerships separate it by partner class. Overseas company branches and registered foreign companies give offshore entities a local legal presence without separate incorporation.

This New Zealand company incorporation conclusion guide reflects a corporate structure summary shaped by Companies Office oversight and a legal framework that continues to align with OECD transparency standards. Your choice of entity ultimately determines tax treatment, liability exposure, and ongoing compliance obligations under the Companies Act 1993. Expanship's team works directly with these structures across the full registration and maintenance process.

How Expanship Can Assist You

Expanship's New Zealand company registration services cover the full spectrum of entity types available under New Zealand law — from registering a Limited Company (Ltd) with the Companies Office to establishing a Limited Partnership under the Limited Partnerships Act 2008. Whether your structure is straightforward or involves a foreign company registration under Part 18 of the Companies Act 1993, our team handles the process from start to finish.

Our corporate services span every stage of formation and ongoing compliance:

- Document preparation and notarisation

- Registered office and agent provision in New Zealand

- Filing and liaison with the Companies Office (MBIE)

- Post-incorporation compliance management

- Banking introduction assistance

Each engagement is handled by specialists familiar with New Zealand's regulatory requirements, so your entity is set up correctly from day one.

Reach out to Expanship New Zealand to discuss your incorporation or compliance needs.

Frequently Asked Questions (FAQ)

The limited liability company (Ltd) is the most frequently incorporated entity, registered under the Companies Act 1993. Its combination of liability protection, a single-shareholder minimum, and no residency requirement for shareholders makes it the default choice for both resident and foreign operators.

A branch registered under Part 18 of the Companies Act 1993 is an extension of its foreign parent and does not create a separate legal entity in New Zealand. A locally incorporated Ltd, by contrast, holds independent legal personality, meaning its liabilities are distinct from those of its shareholders. Compliance obligations also differ: a branch must file the parent company's financial statements with the Companies Office, while an Ltd files its own.

New Zealand maintains a public register, so director and shareholder details for companies incorporated under the Companies Act 1993 are publicly accessible. No entity type in this jurisdiction is exempt from disclosure on the register, though nominee director and shareholder arrangements are legally permissible and commonly used to add a layer of separation between beneficial owners and public records.

A limited liability company requires only one director and one shareholder, so a sole individual can incorporate one. General partnerships and limited partnerships each require a minimum of two partners under the Partnership Act 1908 and the Limited Partnerships Act 2008 respectively. A sole trader, by definition, involves only one person and carries no formal registration requirement beyond an IRD number for tax purposes.

Foreign individuals and corporations may register a limited liability company, a limited partnership, or an unlimited company without holding New Zealand residency. A foreign company may also register as an overseas company under Part 18 of the Companies Act 1993. The sole trader structure is generally limited to individuals with the legal right to work in New Zealand, making it less accessible to non-residents operating from abroad.

The Companies Act 1993 allows a company to re-register in a different form, for instance converting between a limited and an unlimited company. However, converting a company into a partnership or a co-operative company is not a straightforward re-registration process and typically requires dissolution and fresh incorporation under the relevant Act.

Not all structures confer separate legal personality. A limited liability company, a limited partnership, and a co-operative company registered under the Co-operative Companies Act 1996 each hold independent legal status. A general partnership and a sole trader do not; in both cases, the individual partners or sole trader remain personally exposed to business liabilities.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.