Key Takeaways

- New Zealand's 28% corporate tax rate applies to worldwide income under a residence-based system, meaning foreign-sourced profits remain taxable even when earned and reinvested entirely outside the country.

- Under the Companies Act 1993, director and shareholder information is recorded on a publicly searchable register, removing the layer of privacy that comparable offshore structures in other jurisdictions would typically provide.

- With a limited double tax treaty network, businesses operating across multiple jurisdictions face a higher risk of double taxation on cross-border income flows than they would under a broader treaty framework.

- Geographic isolation from major Northern Hemisphere markets adds logistical friction and operational cost that businesses headquartered in Singapore, Hong Kong, or Ireland do not face to the same degree.

New Zealand operates under a well-established, rules-based regulatory environment governed by legislation such as the Companies Act 1993. The framework is transparent and consistently enforced, placing it firmly among the more heavily regulated common law jurisdictions in the Asia-Pacific region.

The disadvantages of incorporating in New Zealand span several distinct categories, from tax structure and disclosure obligations to cost pressures and geographic constraints.

How significantly these factors affect your business depends on its structure, industry, and where it earns revenue. A holding entity with no active New Zealand operations faces a different risk profile than a trading company with local employees and customers.

This article is most relevant to foreign investors, non-resident directors, and internationally structured businesses considering the cons of New Zealand company formation — particularly those weighing it against lower-tax or more privacy-oriented jurisdictions.

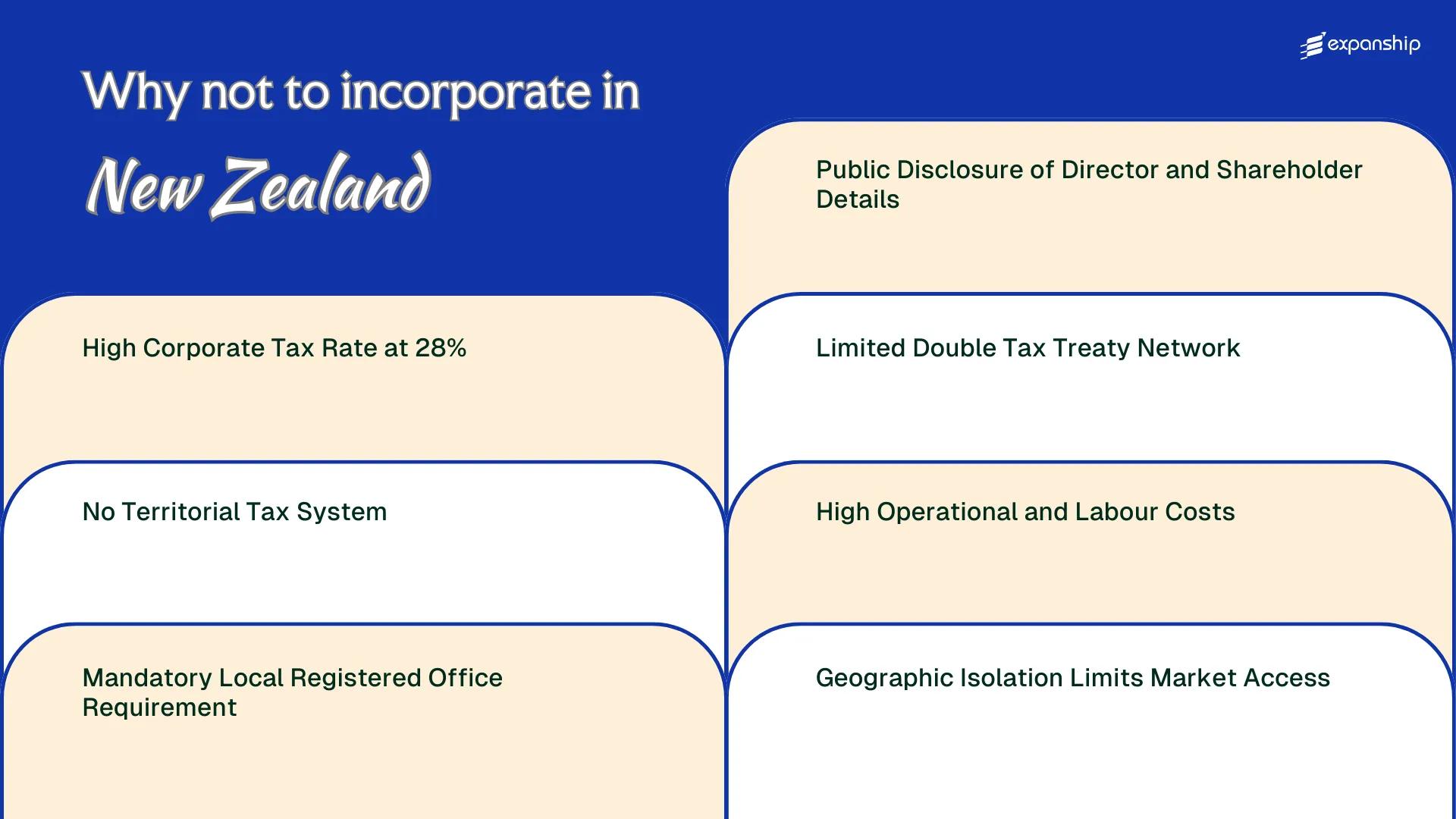

High Corporate Tax Rate at 28%

At 28%, the New Zealand corporate tax rate drawbacks are immediate and measurable for foreign-owned companies. Under the Income Tax Act 2007, this flat rate applies to all resident companies on their worldwide income, with no sliding scale or reduced rate for smaller profits.

How the Rate Stacks Up Against Competing Jurisdictions

Singapore taxes resident companies at 17%, and Ireland's standard rate sits at 12.5%. For a foreign business selecting a Pacific-region base, that gap in the 28% company tax rate New Zealand imposes directly reduces post-tax earnings available for reinvestment or repatriation.

Certain imputation credits tied to the dividend imputation system can offset some shareholder-level tax, but this mechanism primarily benefits resident shareholders rather than foreign investors receiving dividends abroad.

What This Means for Foreign-Owned Structures

The NZ corporate tax burden foreign companies face is compounded when profits cannot be sheltered through group structures, since the worldwide income basis leaves little structural room to reduce the effective rate through offshore arrangements.

A foreign business owner cannot reduce liability below 28% through internal restructuring alone, as the Income Tax Act 2007 taxes all resident company income at a flat rate with no preferential foreign investment tier.

No Territorial Tax System

New Zealand operates a worldwide tax system, meaning resident companies are taxed on income earned globally, not just domestically. For foreign business owners, this is one of the more consequential New Zealand worldwide tax system limitations: profits generated in lower-tax jurisdictions don't escape the reach of the Inland Revenue Department simply because they were earned offshore.

Under the Controlled Foreign Company (CFC) rules in the Income Tax Act 2007, if your company holds an interest in a foreign entity, attributable income may be taxed in New Zealand regardless of whether it was repatriated. This removes the deferral advantage that makes incorporation in pure territorial systems financially attractive.

The practical burden this creates for cross-border operators includes:

- Foreign branch profits are pulled into the New Zealand tax base, eliminating the structural benefit of holding low-tax offshore operations through a New Zealand entity

- CFC attribution rules require detailed calculation of attributable income across each foreign interest, generating significant compliance costs annually

- Passive income earned offshore, such as dividends and royalties, can trigger tax obligations that would not arise in territorial regimes like Singapore or Hong Kong

- Restructuring an existing international group to sit under a New Zealand holding company may inadvertently create tax exposure on income streams that were previously outside any high-tax net

A limited active business exemption exists under the CFC rules, but it applies narrowly and does not resolve the burden for businesses with mixed or passive income streams abroad.

Company Incorporation in New Zealand

Set up your New Zealand company with full compliance support, from entity selection to registration with the Companies Office.

Mandatory Local Registered Office Requirement

Under the Companies Act 1993, every company registered in New Zealand must maintain a registered office at a physical address within the country. This New Zealand registered office requirement restriction means a foreign business owner cannot simply list an overseas headquarters or use a virtual address without local substance. The registered office must be a genuine, accessible location where official documents and regulatory correspondence can be received.

The Companies Office, which administers the New Zealand Companies Register, requires this address to be publicly visible on the register at all times. If your business has no physical footprint locally, you must appoint a third-party registered office provider, which carries an ongoing annual fee.

| Requirement | Detail | Implication for Foreign Owner |

|---|---|---|

| Physical address | Must be within New Zealand | Overseas addresses not accepted |

| Address visibility | Publicly listed on Companies Register | No privacy for registered location |

| Update obligation | Changes must be filed promptly | Administrative cost and potential penalties for delay |

| Third-party provider cost | Typically NZD 150–400+ per year | Recurring overhead with no operational return |

Unlike some offshore jurisdictions that permit nominee or virtual arrangements with minimal oversight, the NZ Companies Act 1993 ties legal correspondence and service of process directly to this address. Missing a document because the address lapses or becomes invalid can result in default judgments or compliance failures without your knowledge.

There is no exemption from this requirement based on company size or foreign ownership structure.

Public Disclosure of Director and Shareholder Details

New Zealand director disclosure risks are a genuine structural concern for foreign founders. Under the Companies Act 1993, every company must file details of its directors and shareholders with the Companies Office, and that information is publicly searchable on the NZ Companies Register with no restriction on who can access it.

This means a competitor, a litigant, or any third party can identify the beneficial owners behind your entity within minutes. For founders who rely on structural privacy to manage commercial risk or personal security, this exposure is a material limitation of the jurisdiction.

Shareholder details, including names and the number of shares held, appear on the public register. Unlike some jurisdictions that allow nominee structures to remain off the public record entirely, New Zealand does not offer a mechanism to withhold this information from general public view.

- Director names and addresses are mandatory disclosures under the Companies Act 1993.

- Shareholder names and shareholding percentages are visible on the public register.

- No confidentiality exemption exists for foreign-owned entities operating locally.

- Any change in directors or shareholders must be filed within 20 working days.

New Zealand has no central beneficial ownership register separate from its public company registry, meaning the public register itself serves as the primary transparency mechanism — making it more exposed than jurisdictions that separate private beneficial ownership filings from public-facing records.

Limited Double Tax Treaty Network

New Zealand's double tax treaty (DTT) network is narrower than its economic profile might suggest, and that gap carries direct cost implications for foreign-owned businesses operating across borders.

Scope of the Treaty Network

New Zealand has concluded around 40 double tax agreements, covering major partners such as Australia, the United States, the United Kingdom, and China. For comparison, the Netherlands holds over 90 active treaties. Businesses with operations or investors in non-treaty jurisdictions, including many Southeast Asian and Middle Eastern markets, face withholding taxes on dividends, interest, and royalties at New Zealand's domestic rates, which can reach 15% to 33% depending on the payment type and recipient.

Practical Exposure for Foreign-Owned Entities

Where no NZ double tax agreement exists, cross-border profit extraction becomes materially more expensive, as withholding tax risks in New Zealand with no treaty cannot be offset by treaty-reduced rates or tax credits in the counterpart jurisdiction. A holding structure that functions efficiently within a treaty country may produce a significantly heavier tax burden when routed through a non-treaty partner. The Income Tax Act 2007 governs these withholding obligations, and the absence of a bilateral agreement leaves no statutory mechanism to reduce them.

Addressing Treaty Gaps in Your New Zealand Structure

Understand how New Zealand's limited treaty network affects your cross-border tax position and what structural considerations apply to your specific investor or partner jurisdictions.

High Operational and Labour Costs

New Zealand high business operating costs rank among the highest in the Asia-Pacific region, driven by statutory wage floors and a relatively small domestic labour pool. Foreign firms frequently underestimate the cost burden before incorporation.

- The adult minimum wage, set annually by the Minister for Workplace Relations and Safety, stood at NZD 23.15 per hour in 2024, and any business employing local staff is legally bound to meet this floor regardless of revenue or stage of growth.

- Employers must also fund Kiwisaver contributions of at least 3% of gross earnings per eligible employee under the Kiwisaver Act 2006, adding a mandatory payroll cost on top of base wages.

- The Employment Relations Act 2000 requires good faith obligations and formal processes for termination, making workforce adjustments slower and more expensive than in many competing jurisdictions.

- Skilled labour shortages in technical and professional fields push market salaries well above statutory minimums, compressing margins for foreign-owned entities that cannot yet access local networks.

Geographic Isolation Limits Market Access

New Zealand geographic isolation business limitations are structural, not incidental. Situated roughly 2,000 kilometres from Australia and over 10,000 kilometres from major Asian trade hubs, the country sits at the edge of global supply chains rather than within them.

For a foreign business owner, distance translates directly into cost. Freight times to Europe or North America can exceed three to four weeks by sea, and air freight rates from Auckland are among the higher in the Asia-Pacific region due to limited carrier competition on long-haul routes.

The domestic market compounds this further. With a population of approximately 5.1 million, NZ small market size restrictions mean your total addressable market is limited before you factor in any export ambition.

Scaling regionally requires separate market-entry strategies for Australia, Southeast Asia, or the Pacific, each carrying their own compliance and logistics overhead. Distance adds real cost to that expansion, not just inconvenience.

A hypothetical scenario: A firm exporting manufactured goods from Auckland to Rotterdam faces transit times of 25 to 30 days by sea freight, with costs per 20-foot container typically ranging between USD 2,000 and USD 4,500 depending on routing, compared to intra-European shipments often completed in two to five days at substantially lower per-unit logistics cost.

How to Navigate These Drawbacks

How to manage New Zealand incorporation drawbacks requires structural planning before the entity is registered, not after operational issues arise.

- Appoint a New Zealand-resident director to satisfy the Companies Act 1993 requirement for at least one locally resident director.

- Use a professional registered office address to meet the Companies Office address requirement without committing to a physical lease.

- Assess your group's treaty exposure early by reviewing NZ's tax treaties through Inland Revenue to identify withholding tax gaps on dividends, royalties, and interest.

- Structure offshore IP ownership or holding arrangements before incorporation, since post-registration restructuring triggers additional compliance under the Income Tax Act 2007.

- Account for the absence of a territorial tax system when modelling foreign income flows, as worldwide income is subject to New Zealand tax from day one.

- Factor ACC levies and minimum wage obligations into your labour cost projections before committing to local hiring.

These steps address the most structurally significant friction points within the framework administered by the Companies Office and Inland Revenue. Neither body offers exemptions from the obligations discussed in this blog, so mitigation depends on preparation rather than post-registration adjustments.

New Zealand Still Worth It

The drawbacks covered in this blog are real and, for certain business profiles, disqualifying. That said, New Zealand's incorporation framework, governed by the Companies Act 1993 and administered by the Companies Office, reflects a system built on legal stability, a clean regulatory environment, and genuine ease of registration. Whether those structural advantages outweigh the costs depends entirely on your commercial objectives.

| Pro | Con |

|---|---|

| Company registration through the Companies Office is straightforward and completed online | Corporate tax is fixed at 28%, with no participation exemption reducing dividend income |

| New Zealand operates a common law legal system with strong contract enforcement | No territorial tax system means foreign-sourced income remains within the tax net |

| The country holds a consistent record of regulatory transparency and low corruption | Director and shareholder details are publicly accessible on the Companies Register |

| No minimum share capital requirement for a limited liability company | A local registered office address is mandatory under the Companies Act 1993 |

| The double tax treaty network is narrower than comparable OECD incorporation destinations |

Geographic distance from major markets and above-average operating costs add further friction for businesses reliant on physical supply chains or local labour. These are structural conditions, not regulatory anomalies, and they do not diminish with time.

Compliance Services for Companies in New Zealand

Maintain good standing with the Companies Office and meet your ongoing statutory obligations under New Zealand law.

Conclusion

A New Zealand company formation drawbacks summary must account for a jurisdiction that is administratively efficient but carries real structural costs. The 28% corporate tax rate, combined with a worldwide income regime, creates an ongoing tax burden that grows with your firm's international activity. Public disclosure obligations under the Companies Act 1993 remove the privacy that some business structures depend on. Geographic distance from major markets remains a fixed constraint. These factors do not disappear with better planning; they require deliberate structural decisions before incorporation proceeds.

Expanship and Your New Zealand Expansion

Expanship New Zealand company registration support covers the specific compliance obligations that make operating through a New Zealand entity more demanding than many founders anticipate. From maintaining a registered office under the Companies Act 1993 to managing director disclosure requirements on the public Companies Register, your administrative exposure is real and ongoing. Expanship's role is to reduce the operational burden of meeting these obligations, not to change what New Zealand law requires of you.

Beyond incorporation, Expanship offers a practical range of corporate services to support your business at each stage:

- Your company is registered with documents prepared to meet the Companies Office requirements.

- A registered agent and local office address are provided to satisfy the resident director and registered office rules.

- Government filings are handled with direct liaison to relevant regulatory bodies on your behalf.

- Post-incorporation compliance is managed to keep your entity in good standing.

- Banking introductions are facilitated to help you establish a local financial presence.

- Tax registration and liaison with Inland Revenue is coordinated from the outset.

Reach out to Expanship New Zealand to discuss how we can support your expansion into this jurisdiction.

Frequently Asked Questions (FAQ)

New Zealand taxes resident companies on their worldwide income, not just income sourced domestically. If your New Zealand-incorporated entity earns revenue from clients or operations in Europe, Asia, or North America, that income is included in its New Zealand taxable base under the Income Tax Act 2007. Foreign tax credits may offset some liability, but the obligation to file and account for overseas earnings remains regardless.

New Zealand has double tax agreements with approximately 40 countries, which is narrower than the treaty networks maintained by the United Kingdom, the Netherlands, or Singapore. If your business operates in or derives income from a country outside that network, withholding taxes on dividends, royalties, and interest may apply at full domestic rates with no treaty reduction available. For businesses with supply chains or revenue streams across Southeast Asia or Africa, this gap creates measurable additional tax cost.

The Companies Office register, maintained under the Companies Act 1993, publicly discloses director names, residential addresses, and shareholder details for every New Zealand company. This information is freely searchable online without any access restriction. Unlike jurisdictions that permit nominee structures to shield beneficial ownership from public view, New Zealand does not provide a mechanism to suppress this data from public disclosure.

Under the Companies Act 1993, every New Zealand company must have at least one director who is either a New Zealand resident or a resident of Australia with a New Zealand-registered company as their qualifying entity. Failure to maintain this requirement puts the company in breach of its statutory obligations, and the Registrar of Companies has the authority to remove the entity from the register or take enforcement action. Ongoing non-compliance can also expose directors to personal liability for acts carried out while the company is in breach.

Yes. New Zealand's minimum wage, employer obligations under the Employment Relations Act 2000, and general cost of professional services place it among the more expensive jurisdictions in the Asia-Pacific region. Office space in Auckland, the primary commercial centre, carries costs comparable to mid-tier European cities, while access to a skilled talent pool is constrained by a national population of approximately five million. Businesses that require a physical workforce or local professional services will face a cost base that is difficult to offset through operational efficiencies.

Geographic distance from North America, Europe, and even the larger Asian economies creates tangible logistical and time-zone friction for businesses that depend on real-time client interaction or physical goods movement. New Zealand sits roughly 10 to 12 hours ahead of Western European time zones and more than 16 hours ahead of the US East Coast, which limits synchronous working hours with major trading partners. For service businesses requiring close client coordination, this isolation translates directly into staffing complexity and delayed response cycles.

It is more administratively complex for a foreigner because the Companies Act 1993 requires at least one director to be ordinarily resident in New Zealand or Australia. A non-resident founder must either relocate, appoint a nominee director who meets the residency test, or partner with a local individual willing to take on that statutory role. Each of these options carries cost, dependency risk, or ongoing management overhead that a local resident incorporator does not face.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.