Key Takeaways

- Niue's corporate framework is administered by the Niue Financial Services Commission (NFSC) and governed primarily by the Niue Act 2006, which underpins all entity formations in the jurisdiction.

- The International Business Company (IBC) is the dominant registered structure in Niue, suited to non-resident entrepreneurs seeking tax-neutral holding or trading arrangements under the jurisdiction's zero-tax regime.

- International Trusts in Niue are designed specifically for asset protection and estate planning purposes, making them a distinct instrument from the IBC rather than a general-purpose business vehicle.

- Ongoing alignment with FATF standards and international transparency expectations continues to shape how Niue's financial services registry and its licensed service providers operate.

Introduction to Entity Types in Niue

Niue is a self-governing island nation in the South Pacific Ocean, situated northeast of New Zealand and in free association with it. Despite its small size, the jurisdiction maintains a distinct legal framework for corporate formation, administered by the Niue Financial Services Commission (NFSC), which oversees company registration and regulatory compliance.

Understanding the available business entity types in Niue matters when selecting the right structure for your purposes. The jurisdiction operates a predominantly zero-tax regime for internationally focused entities, though the specifics vary by structure.

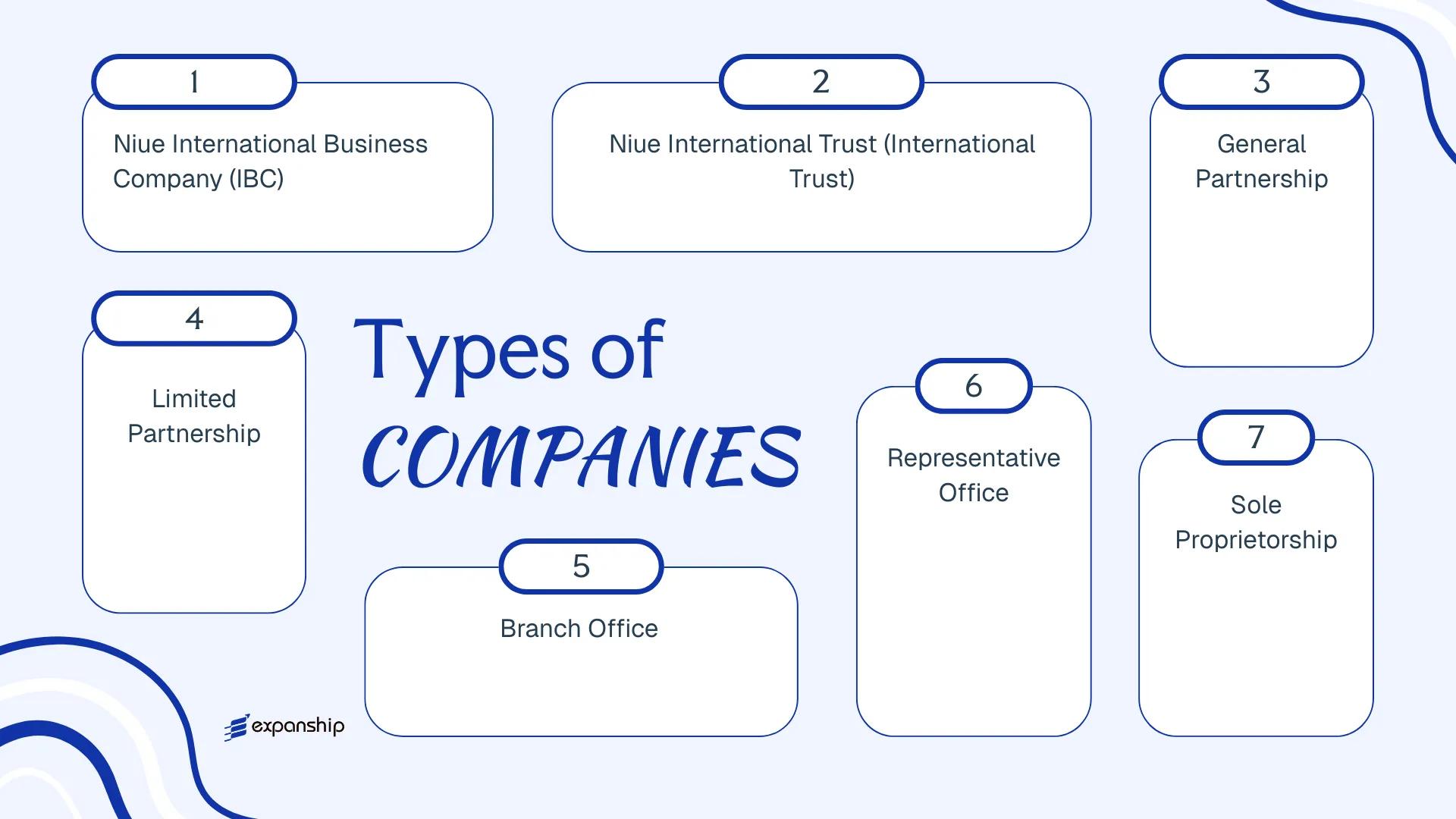

Businesses and individuals forming entities here can choose from the following structures:

- International Business Company (IBC)

- International Trust

- General Partnership

- Limited Partnership

- Branch Office

- Representative Office

- Sole Proprietorship

Each structure carries distinct formation requirements, liability implications, and operational constraints under Niue's corporate legislation. This article examines each option in detail — covering legal characteristics, regulatory obligations, and practical considerations relevant to your decision.

An Overview of Business Structures in Niue

Niue's company law framework provides several distinct entity types for international and domestic use, governed primarily by the Niue Act 1966 and supplemented by the International Business Companies Act 1994. Each structure carries different implications for liability, taxation, and permitted commercial activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| International Business Company (IBC) | Separate legal entity | Limited | Exempt | Not permitted | 1 shareholder | Niue Financial Services Commission | IBC Act 1994 |

| International Trust | Trust structure | Trustee liability | Exempt | Not applicable | 1 settlor, 1 trustee | Niue Financial Services Commission | Niue Trusts Act 1994 |

| General Partnership | Unincorporated body | Unlimited | Taxable | Permitted | 2 partners | Registrar of Companies | Niue Act 1966 |

| Limited Partnership | Hybrid structure | Mixed | Taxable | Permitted | 1 GP, 1 LP | Registrar of Companies | Niue Act 1966 |

| Branch Office | Extension of foreign entity | Parent liability | Taxable | Permitted | N/A | Registrar of Companies | Niue Act 1966 |

| Representative Office | Non-trading presence | Parent liability | Exempt | Not permitted | N/A | Registrar of Companies | Niue Act 1966 |

| Sole Proprietorship | Unincorporated individual | Unlimited | Taxable | Permitted | 1 individual | Registrar of Companies | Niue Act 1966 |

Each of these structures is examined in full in the sections below.

Niue International Business Company (IBC)

The Niue International Business Company (IBC) is governed by the Niue International Business Companies Act 1994, which established the framework for offshore corporate activity on the island. As a separate legal entity, an IBC carries its own rights and obligations distinct from its shareholders, with liability confined to the company's assets.

Incorporated under the oversight of the Niue International Trust and IBC Registry, the entity is designed primarily for cross-border commercial activity rather than domestic operations within Niue.

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | International Business Company (IBC) | Incorporated under the Niue IBC Act 1994 |

| Members | Directors (min. 1, no max); Shareholders (min. 1, no max) | Corporate directors and shareholders permitted |

| Local Presence | Registered Agent required; no requirement for a local office | Registered Agent must be Niue-licensed |

| Capital | No minimum share capital; USD is commonly used | Bearer shares are generally not permitted |

| Privacy | Shareholder and director details not publicly disclosed | Beneficial ownership held on file with the Registered Agent |

Focus Points

- Taxation: IBCs are exempt from Niue income tax, withholding tax, and stamp duty on income derived outside Niue; no VAT or corporate tax applies.

- Economic Substance: No economic substance requirements are currently imposed on Niue IBCs.

- Annual Compliance: Annual renewal fees apply; financial statements are not required to be filed publicly.

- Treaty Access: Niue has a limited tax treaty network, which restricts access to treaty benefits in most jurisdictions.

- Restrictions: IBCs cannot conduct business with Niue residents or own real property within Niue.

Closing

The IBC suits holding structures, IP ownership, and international trading operations where confidentiality and tax efficiency on foreign-sourced income are priorities. The absence of public disclosure requirements is a practical advantage, though the limited treaty network constrains its utility for income flows into treaty-dependent jurisdictions.

Niue IBCs are most appropriate for internationally active businesses or investors seeking a low-cost offshore vehicle for asset holding or cross-border trade, with no domestic revenue component.

Company Incorporation in Niue

Incorporate an IBC in Niue with end-to-end support from registered agent appointment to certificate of incorporation.

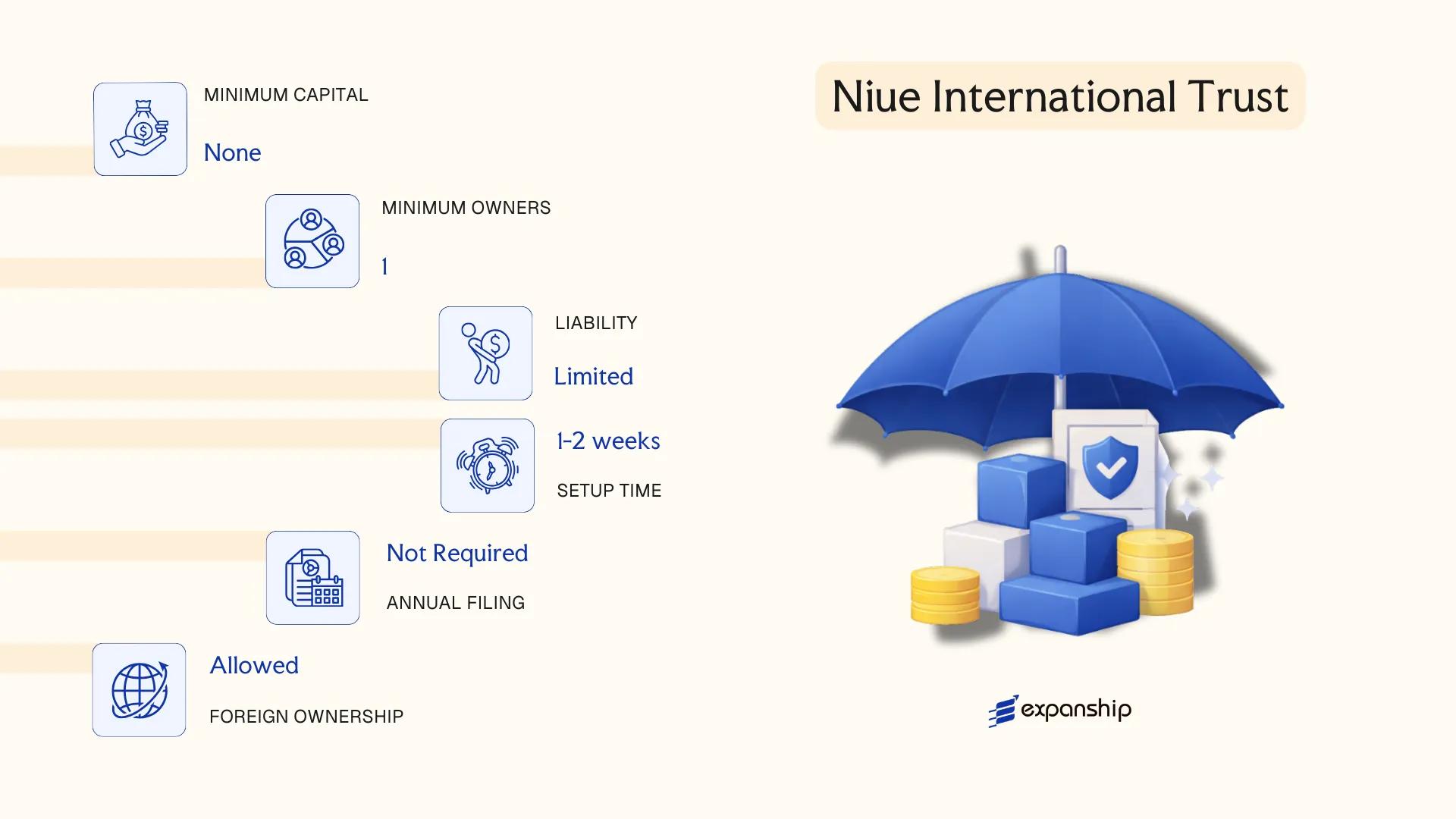

Niue International Trust

Governed by the Niue International Trusts Act 1994, the Niue international trust formation process creates a legal arrangement rather than a separate legal entity. The trust holds assets on behalf of beneficiaries, with a trustee assuming fiduciary responsibility under the terms of the trust deed.

Unlike corporate structures, a trust has no shareholders or directors. Control and benefit are separated between the trustee, who manages the assets, and the beneficiaries, who receive the economic benefit. At least one trustee must be a licensed Niue trustee company registered under local legislation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Trust (not a separate legal entity) | Assets held by trustee under deed |

| Parties | Settlor, Trustee(s), Beneficiaries, optional Protector | Settlor may not be sole beneficiary |

| Trustee Requirement | At least one licensed Niue trustee company | Must hold a valid licence under local law |

| Local Presence | Licensed trustee company mandatory; registered office required | No requirement for physical office beyond trustee |

| Settlor Restriction | Must be non-resident of Niue | Applies to both individuals and corporate settlors |

| Privacy | Trust deeds are not publicly registered | Beneficial ownership not publicly disclosed |

Focus Points

- Taxation: Niue international trusts are exempt from local income tax, withholding tax, and stamp duty on trust transactions, provided the settlor and beneficiaries are non-resident.

- Economic Substance: No economic substance obligations apply to trust structures under current Niue regulations.

- Annual Compliance: Annual renewal fees are payable; trusts must maintain a valid licensed trustee throughout their duration.

- Treaty Access: Niue has a limited tax treaty network, so trust structures generally cannot access double taxation agreements.

- Duration: The perpetuity period under the Act can extend significantly beyond common law limits, making long-term asset holding viable.

Sub-Types

Discretionary Trust

The trustee holds full discretion over how and when assets are distributed among beneficiaries. This structure is commonly used for succession planning and multi-generational wealth management.

Fixed Interest Trust

Beneficiaries hold defined, predetermined interests in trust assets. This removes trustee discretion over distribution and suits arrangements where clear entitlements must be documented.

Purpose Trust

A purpose trust is established for a specified non-charitable purpose rather than for identifiable beneficiaries. It is frequently used as an orphan structure in structured finance or securitisation transactions.

Closing

Setting up a trust in Niue suits those seeking long-term asset protection, estate planning, or holding arrangements for offshore assets, with privacy as a structural advantage. The key limitation is the absence of broad treaty access, which restricts tax planning strategies that depend on double taxation relief.

This structure is best suited for high-net-worth individuals and family offices seeking confidential, long-term asset protection outside their home jurisdiction.

Partnerships in Niue [General Partnership, Limited Partnership]

Partnership registration in Niue is governed by the Niue Act 1966, which provides the foundational legal framework for both general and limited partnership structures operating within the jurisdiction. Neither a general nor a limited partnership constitutes a separate legal entity under Niuean law — rights and obligations vest directly in the partners themselves.

Liability exposure differs significantly between the two structures. In a general partnership, each partner bears unlimited personal liability for the firm's debts and obligations. A limited partnership introduces a two-tier arrangement, where at least one general partner retains unlimited liability while limited partners are exposed only to the extent of their contributed capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated association | No separate legal personality |

| Members | General partners and/or limited partners | GP: minimum 2, no statutory maximum; LP: minimum 1 GP + 1 LP |

| Local Presence | Registered address in Niue | A local registered agent is typically required |

| Capital | No prescribed minimum; no specified currency requirement | Capital contributions defined by partnership agreement |

| Privacy | Partner details may appear in registration records | Limited public disclosure obligations |

Focus Points

- Taxation: Niue does not impose corporate income tax, withholding tax, or VAT on partnerships, though partners may carry personal tax obligations in their home jurisdictions.

- Economic Substance: Partnerships engaged in relevant activities may be subject to economic substance requirements under applicable Niuean regulations.

- Annual Compliance: Annual filing or renewal obligations apply; the partnership agreement governs internal compliance and governance matters.

- Treaty Access: Niue has a limited tax treaty network, which may restrict partners from accessing treaty benefits in their resident jurisdictions.

- Conversion: Conversion from a general to a limited partnership, or to another entity type, is subject to re-registration procedures under local law.

Sub-Types

General Partnership

All partners share management responsibilities and carry unlimited personal liability. This structure suits closely held business arrangements where partners maintain active operational involvement and accept proportional risk.

Limited Partnership

At least one general partner manages the business and assumes unlimited liability, while limited partners contribute capital without participating in management. This structure is commonly used for investment vehicles and fund arrangements where passive investors require defined liability exposure.

When to Use a Partnership Structure

Partnerships in Niue suit arrangements where two or more parties wish to conduct business under a shared agreement without the administrative requirements of an incorporated entity. The absence of minimum capital requirements offers structural flexibility, though the unlimited liability exposure of general partners remains a material constraint for many commercial applications.

This structure is best suited for small collaborative ventures or investment arrangements between parties who have an established trust relationship and a clear, documented partnership agreement.

Foreign Business Structures in Niue [Branch Office, Representative Office]

Establishing a foreign company branch office in Niue is governed primarily by the Niue Act 1966 and supplementary provisions under Niue's companies legislation, which requires foreign entities to register before conducting business locally. A branch does not constitute a separate legal entity — it remains an extension of the parent company, which retains full liability for the branch's obligations.

Representative offices occupy a more restricted position. Permitted only for liaison and promotional activities, they cannot generate revenue or enter into commercial contracts on behalf of the parent firm.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Non-trading liaison office; no separate legal personality |

| Liability | Parent company bears unlimited liability | Parent company bears full liability |

| Local Presence | Registered agent and local address required | Registered agent and local address required |

| Permitted Activities | Commercial and trading operations | Liaison, market research, promotional activities only |

| Capital Requirement | No statutory minimum prescribed | No statutory minimum prescribed |

| Privacy | Parent company details disclosed upon registration | Parent company details disclosed upon registration |

Focus Points

- Taxation: Niue does not levy corporate income tax, withholding tax, or VAT on offshore income; local-source income may attract obligations under domestic rules.

- Annual Compliance: Annual renewal filings are required to maintain active registration status with the relevant registry.

- Restrictions: Representative offices are prohibited from invoicing clients or executing revenue-generating contracts.

- Economic Substance: Neither structure carries formal substance requirements under current Niue legislation.

- Conversion: A branch may not convert directly into a locally incorporated entity without a separate incorporation process.

Closing

Branch structures suit foreign businesses with existing operations seeking a direct operational presence, while representative offices serve firms conducting preliminary market activity without commercial commitments. The primary advantage of a branch is operational continuity under the parent's existing legal framework; the key drawback is that the parent assumes unrestricted liability for all branch activities.

Best suited for established foreign companies that need an operational or liaison foothold without committing to a locally incorporated entity.

Sole Proprietorship in Niue

A sole proprietorship in Niue is the simplest form of business operation available to individuals. Unlike the IBC or trust structures governed by dedicated offshore legislation, sole traders operate under general business registration requirements administered by the Niue government.

There is no separate legal personality. The individual owner and the business are treated as one legal entity, meaning personal assets are exposed to business liabilities without limitation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole trader | No separate legal personality from the owner |

| Members | Single proprietor | No minimum capital, no co-owners permitted |

| Local Presence | Business registration with government authority | Physical or registered address in Niue required |

| Capital | No statutory minimum | Denominated in New Zealand Dollar (NZD) |

| Privacy | Owner's name linked to business registration | Limited privacy compared to incorporated structures |

Focus Points

- Taxation: No corporate income tax, capital gains tax, or withholding tax applies; business income is treated as personal income of the proprietor.

- Annual Compliance: Renewal of business registration is required; financial reporting obligations are minimal compared to incorporated entities.

- Treaty Access: No access to double tax treaties as an unincorporated individual business.

- Restrictions: Foreign nationals may face limitations on eligibility to register as sole traders under local business licensing rules.

- Conversion: Can be converted into a partnership or incorporated structure if the business grows.

Closing

Sole proprietorship suits small-scale local trading or service activities where simplicity of setup outweighs the need for liability protection. The absence of complex compliance requirements is an advantage, though unlimited personal liability remains a significant structural drawback.

Best suited for resident individuals operating small, low-risk local businesses who do not require liability separation or international tax structuring.

How to Choose the Right Entity Type in Niue

Choosing the right business entity in Niue is a structural decision with legal, tax, and operational consequences that compound over time.

Why Your Entity Choice Matters

- Registering an International Business Company and then conducting business with Niue residents breaches the Niue Amendment Act governing IBC restrictions on local trade, which can result in penalties or striking off.

- Selecting a tax-exempt IBC when your strategy requires treaty-based withholding tax reductions means the firm cannot access those reductions, since tax-exempt entities are typically excluded from treaty benefits.

- Forming a company structure when a Niue International Trust would better serve asset protection or succession planning locks your business into annual shareholder maintenance obligations that do not apply to trust arrangements.

- Choosing an entity without the capacity to meet any applicable substance requirements triggers compliance failures and potential regulatory sanctions under the relevant reporting framework.

Key Factors to Consider

- Business Activity: Passive asset-holding, active trading, and regulated activities such as insurance or fund management each point toward a different structure under Niuean law.

- Local vs. Offshore Operations: If your business will transact with Niue residents, an IBC is prohibited from doing so and you would need an alternative domestic structure.

- Ownership and Management: Single-owner operations and multi-party ventures have different governance needs, with partnerships offering flexible arrangements that companies do not.

- Tax Objectives: Full exemption, treaty access, and jurisdiction-specific tax regimes are not available across all entity types equally.

- Privacy Requirements: Public register disclosure requirements vary by entity; nominee structures may be available but carry their own compliance obligations.

- Exit Strategy: Your ability to redomicile, convert, or wind up the entity depends on which structure you form, and not all Niuean entity types permit all exit mechanisms.

Compliance Services for Companies in Niue

Maintain good standing and meet ongoing regulatory obligations for your Niue-registered entity.

Conclusion

Niue company formation concludes with a clear picture of a small but deliberately structured offshore environment governed primarily by the Niue Act 2006 and administered through the jurisdiction's financial services registry. The IBC remains the default structure for non-resident entrepreneurs seeking tax-neutral holding or trading arrangements. International trusts serve asset protection and estate planning purposes for high-net-worth individuals. Partnerships accommodate joint venture arrangements where pass-through treatment is the priority, while sole proprietorships and foreign branch registrations suit those with simpler operational footprints.

IBCs account for the overwhelming majority of registered entities, reflecting the jurisdiction's positioning as an offshore incorporation destination rather than an operational business hub.

Regulatory developments, including ongoing alignment with FATF standards and broader transparency expectations from international bodies, continue to shape how the registry and licensed service providers operate. Your choice of structure should account for this trajectory. Expanship's advisors are familiar with the current requirements and can guide the process from entity selection through to registration.

How Expanship Can Assist You

Expanship Niue company registration services cover the full process of forming and maintaining entities under Niuean law — from International Business Companies governed by the International Business Companies Act 1994 to international trusts and partnership structures. Every filing passes through the Niue Financial Services Commission (NFSC), and your registered agent must meet local licensing requirements. Expanship works within that framework directly.

From document preparation to long-term compliance management, the services available to you include:

- Document drafting, notarization, and apostille legalization

- Registered agent and registered office provision in Niue

- Filing and liaison with the Niue Financial Services Commission

- Post-incorporation compliance management (annual returns, renewals)

- Corporate secretarial support

- Banking introduction assistance for offshore entities

Ready to move forward? Contact Expanship Niue to discuss your structure.

Frequently Asked Questions (FAQ)

The International Business Company (IBC), governed by the Niue International Business Companies Act 1994, is by far the most frequently incorporated structure on the island. Its zero corporate tax on foreign-sourced income and minimal filing requirements make it the default choice for non-resident entrepreneurs and holding structures alike.

An IBC is a separate legal entity with limited liability, exempt from local taxation on offshore income under the 1994 Act, and carries no obligation to trade within Niue. A sole proprietorship carries unlimited personal liability, is not restricted from local trading, and involves considerably lighter registration formalities — though it also lacks the structural protections that foreign investors typically require.

The IBC offers the strongest confidentiality profile: beneficial ownership details, shareholder registers, and financial statements are not subject to public disclosure under Niuean law. Nominee director and shareholder arrangements are permitted, adding a further layer of separation between the underlying owner and the public record.

Not universally. An IBC can be formed by one director and one shareholder, both of whom may be the same individual. General and limited partnerships, however, require at least two partners by definition, making sole formation impossible under either partnership structure.

Foreign nationals may incorporate an IBC, settle a Niue International Trust, or register a branch of a foreign company without restriction on nationality. Sole proprietorships and partnerships are also technically open to non-residents, though these structures offer fewer advantages for cross-border planning than the offshore-specific vehicles the jurisdiction was designed to support.

The Niue International Business Companies Act 1994 provides for continuation — allowing a foreign company to re-domicile into Niue as an IBC and vice versa. Direct conversion between, for example, an IBC and a partnership is not a defined statutory process; restructuring in such cases would generally require dissolving one entity and forming another.

The IBC imposes the lightest ongoing burden: no annual accounts filing, no audit requirement for most structures, and no requirement to hold meetings in Niue. By comparison, a branch office must maintain accounts consistent with its parent company's obligations and file periodic reports with the relevant Niuean authority.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.