Key Takeaways

- The Aksjeselskap (AS) is the most widely registered entity type in Norway, offering limited liability and a structured governance framework under the aksjeloven for privately held companies.

- Public capital-raising in Norway requires the Allmennaksjeselskap (ASA) form, which carries more stringent regulatory obligations than the private limited company equivalent.

- Foreign businesses entering Norway without immediate need for a full subsidiary can operate through a Norsk Avdeling av Utenlandsk Foretak (NUF), a branch structure registered through the Foretaksregisteret.

- Beneficial ownership disclosure requirements under Norway's Money Laundering Act have tightened in recent years, increasing compliance obligations across all entity types regardless of size or structure.

Introduction to Entity Types in Norway

Situated in Northern Europe and sharing borders with Sweden, Finland, and Russia, Norway is an independent sovereign state governed under a constitutional monarchy. Companies seeking to establish a presence there register through Brønnøysund Register Centre (Registerenheten i Brønnøysund), the central government body responsible for business registration and public record-keeping.

Norway operates a standard corporate tax regime — not a zero-tax or offshore jurisdiction — with tax residency determined primarily by place of effective management and registration.

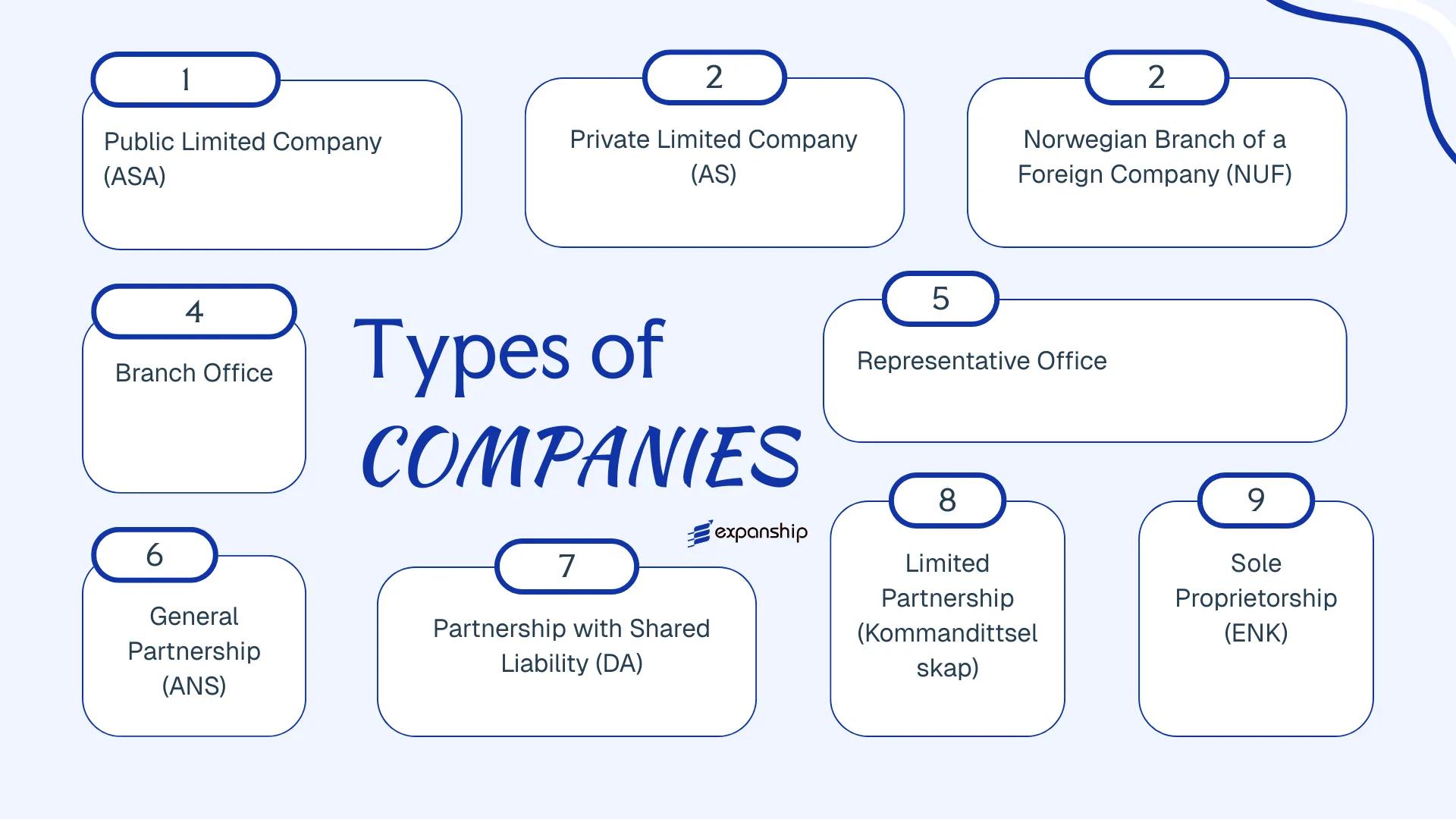

Several types of business entities in Norway are available to both domestic and foreign founders. These include:

- Aksjeselskap (AS)

- Allmennaksjeselskap (ASA)

- Enkeltpersonforetak (ENK)

- Ansvarlig Selskap (ANS)

- Selskap med Delt Ansvar (DA)

- Kommandittselskap (KS)

- Norsk Avdeling av Utenlandsk Foretak (NUF)

Each structure carries distinct requirements around capital, liability, governance, and reporting obligations under Norwegian company law, particularly the Private Limited Companies Act (aksjeloven) and the Public Limited Companies Act (allmennaksjeloven). This article examines each entity in detail to help your business identify the most appropriate structure for operating in Norway.

An Overview of Business Structures in Norway

Norway's company law framework provides several distinct legal structures, governed primarily by the Aksjeloven (Private Limited Companies Act) of 1997 and the Allmennaksjeloven (Public Limited Companies Act) of 1997, alongside the Selskapsloven (Partnerships Act) of 1985 for partnership-based forms. Each structure carries different implications for liability, capital requirements, taxation, and ownership — the sections that follow examine each in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Aksjeselskap (AS) | Private limited company | Limited | Taxed | Yes | 1 shareholder | Foretaksregisteret | Aksjeloven 1997 |

| Allmennaksjeselskap (ASA) | Public limited company | Limited | Taxed | Yes | 1 shareholder | Foretaksregisteret | Allmennaksjeloven 1997 |

| NUF | Foreign branch | Parent liable | Taxed on local income | Yes | N/A (foreign entity) | Foretaksregisteret | Foretaksregisterloven 1985 |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | No | N/A | Foretaksregisteret | General registration rules |

| Ansvarlig Selskap (ANS) | General partnership | Unlimited / joint | Taxed at partner level | Yes | 2 partners | Foretaksregisteret | Selskapsloven 1985 |

| Selskap med Delt Ansvar (DA) | Divided-liability partnership | Pro-rata unlimited | Taxed at partner level | Yes | 2 partners | Foretaksregisteret | Selskapsloven 1985 |

| Kommandittselskap (KS) | Limited partnership | Mixed | Taxed at partner level | Yes | 1 GP + 1 LP | Foretaksregisteret | Selskapsloven 1985 |

| Enkeltpersonforetak (ENK) | Sole proprietorship | Unlimited personal | Taxed as personal income | Yes | 1 (owner) | Foretaksregisteret | Foretaksregisterloven 1985 |

Each of these structures is examined in full in the sections below.

Allmennaksjeselskap (ASA) — Public Limited Company

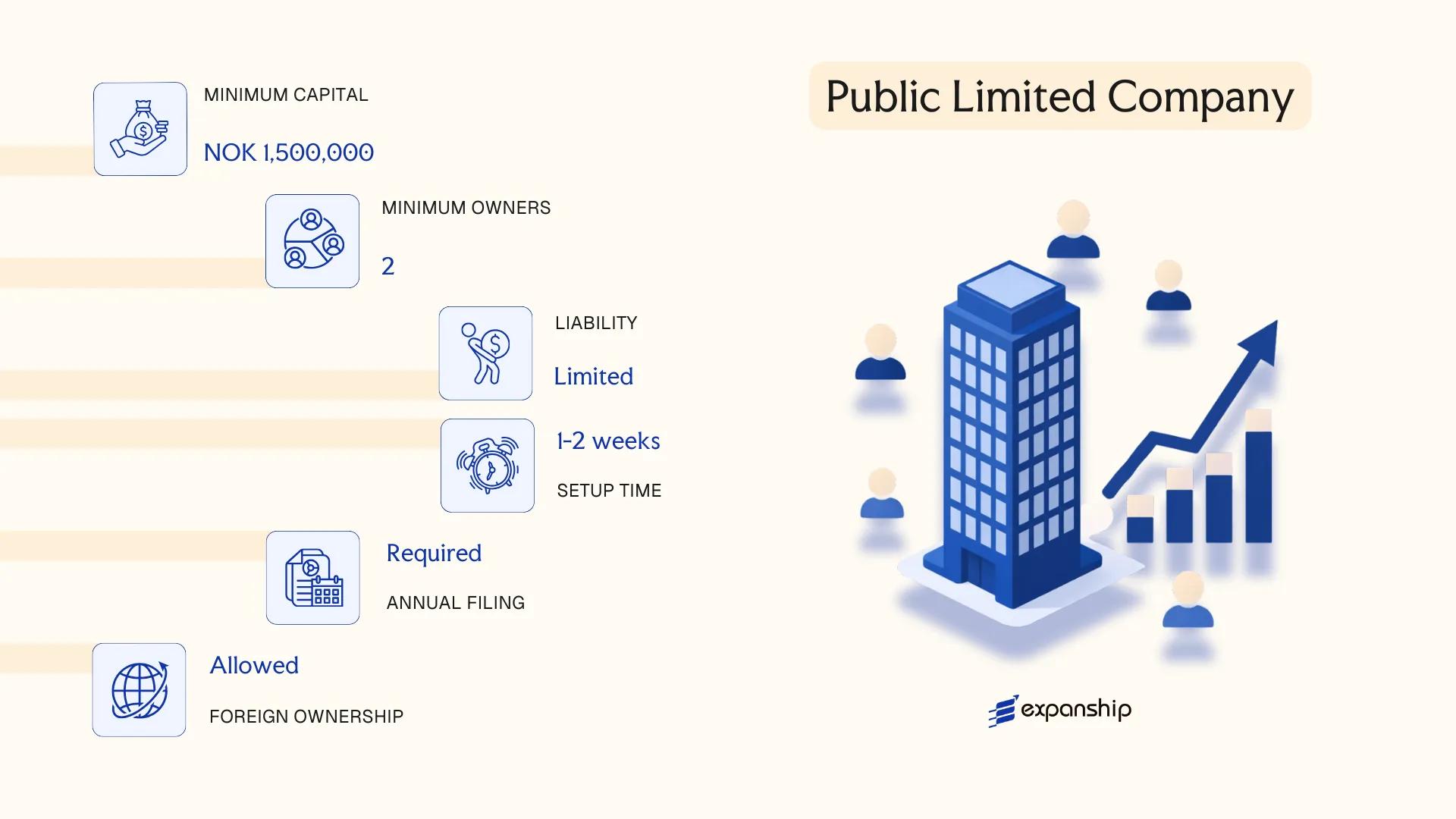

Governed by the Public Limited Liability Companies Act (allmennaksjeloven) of 1997, the Allmennaksjeselskap ASA Norway public company structure is designed for businesses that intend to offer shares to the general public or seek a listing on a regulated market such as Oslo Børs. As a separate legal entity, an ASA carries its own rights and obligations distinct from its shareholders, who bear no personal liability beyond their invested capital.

Registration is handled through the Foretaksregisteret (the Register of Business Enterprises), and the entity must be registered with Finanstilsynet (the Financial Supervisory Authority of Norway) if it conducts regulated financial activities. Shares in an ASA must be registered in the Verdipapirsentralen (VPS), the Norwegian Central Securities Depository.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company | Separate legal personality; governed by allmennaksjeloven 1997 |

| Members | Shareholders; Board of Directors (minimum 3 members); General Meeting | Board must include employee representatives if workforce exceeds 30 |

| Capital | NOK 1,000,000 minimum share capital | At least 50% must be paid up before registration; shares freely transferable |

| Local Presence | Registered office in Norway required | Must maintain a physical Norwegian address on public record |

| Auditor | Statutory audit mandatory | Must appoint a state-authorised public accountant (statsautorisert revisor) |

| Privacy | Shareholder register is publicly accessible via Foretaksregisteret | Beneficial ownership information reported to the BO register |

Focus Points

- Taxation: Corporate income tax applies at 22% on worldwide profits for resident entities; VAT registration is required once turnover exceeds NOK 50,000; dividends paid to foreign shareholders are subject to withholding tax (generally 25%, reducible under applicable tax treaties); no stamp duty on share transfers. See Skatteetaten (Norwegian Tax Administration) for current rates.

- Annual Compliance: Annual accounts must be filed with Regnskapsregisteret; annual general meeting must be held within six months of the financial year-end.

- Treaty Access: Norway has an extensive double tax treaty network; ASA entities resident in Norway can access treaty benefits, subject to anti-abuse provisions.

- Listing Requirement: An ASA is a prerequisite for listing on Oslo Børs or Euronext Expand Oslo, though formation does not mandate a listing.

- Conversion: An ASA may be converted to a private limited company (AS) by shareholder resolution and re-registration, provided reduced capital requirements are met.

Established trading companies, financial institutions, and large enterprises requiring public capital use the ASA structure. Its primary advantage is unrestricted share transferability and access to public capital markets; the principal drawback is the comparatively high minimum share capital and the regulatory burden associated with Finanstilsynet oversight and mandatory VPS registration.

The ASA is most appropriate for large enterprises or businesses actively planning a public share offering or exchange listing in Norway.

Company Incorporation in Norway

Expanship assists with ASA and AS formation, registered office provision, and ongoing compliance in Norway.

Aksjeselskap (AS) — Private Limited Company

The Aksjeselskap (AS) is the standard private limited company structure in Norway, governed by the Private Limited Companies Act (Aksjeloven) of 1997. It carries separate legal personality, meaning the entity itself holds rights, enters contracts, and bears liabilities distinct from its shareholders.

Liability is confined to each shareholder's capital contribution. The AS structure suits a broad range of commercial purposes, from active trading businesses to holding arrangements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company | Shares cannot be offered to the public |

| Members | Shareholders (min. 1, no maximum) | A single individual or corporate entity may hold 100% |

| Management | Board of Directors (min. 1 member) + optional Managing Director | Companies with share capital above NOK 3 million must appoint a Managing Director |

| Local Presence | Registered office address in Norway required | Must be registered with the Brønnøysund Register Centre |

| Share Capital | Minimum NOK 30,000 | Must be fully subscribed at incorporation; no par value requirement |

| Privacy | Shareholder register is publicly accessible via Brønnøysund | Beneficial ownership is reported to the Beneficial Ownership Register |

Focus Points

- Taxation: Subject to 22% corporate income tax; VAT applies at 25% standard rate (registration threshold: NOK 50,000 turnover); withholding tax of 25% on dividends to non-resident shareholders, reducible under tax treaties; no stamp duty on share transfers.

- Annual Compliance: Must file annual accounts with the Regnskapsregisteret (Register of Accounts) and submit a tax return to Skatteetaten; audit obligation applies based on size thresholds.

- Treaty Access: Norway's tax treaty network covers 80+ countries, and an AS qualifies as a resident entity for treaty purposes.

- Conversion: An AS can be converted to an Allmennaksjeselskap (ASA) if public listing is intended, subject to increased capital and compliance requirements under Allmennaksjeloven.

- Restrictions: Share transfers are subject to pre-emption rights held by existing shareholders unless the articles of association expressly waive them.

Closing

The AS is the default choice for foreign investors establishing an operating subsidiary, joint venture, or holding structure in Norway. Its principal advantage is straightforward limited liability with a low capital threshold; the main drawback is the public availability of shareholder information, which limits structural privacy.

The AS is most appropriate for small to medium-sized enterprises, foreign subsidiaries, and entrepreneurs seeking limited liability without the regulatory burden of a publicly listed entity.

Norsk Avdeling av Utenlandsk Foretak (NUF) and Other Foreign Structures [Branch Office, Representative Office]

A NUF branch office Norway registration allows a foreign company to conduct business activities without incorporating a separate Norwegian legal entity. Governed by the Companies Act and administered through the Brønnøysund Register Centre, a NUF is not an independent legal person — the parent company bears full liability for its Norwegian operations.

Registration is mandatory before commencing activity, and the NUF must maintain a Norwegian-resident contact person. The foreign parent's legal form and home-country registration remain the controlling framework; Norwegian law governs only the local activities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch of a foreign legal entity | No separate legal personality; parent company is fully liable |

| Governing Body | Designated Norwegian contact person | Must be resident in Norway; not a director of a new entity |

| Local Presence | Registered business address in Norway | Required for Brønnøysund Register Centre filing |

| Capital Requirement | None | Parent company's capital structure applies |

| Privacy | Parent company's details are publicly registered | NUF registration is searchable in the Entity Register |

Focus Points

- Taxation: Subject to Norwegian corporate tax (22%) on Norway-sourced income; VAT registration required if turnover exceeds NOK 50,000; withholding tax may apply to payments to the parent depending on applicable tax treaty.

- Economic Substance: Activities must genuinely occur in Norway; purely passive registrations attract scrutiny from Skatteetaten (the Norwegian Tax Administration).

- Annual Compliance: Annual accounts must be filed if the NUF meets statutory thresholds under the Accounting Act; the parent's accounts may also require submission.

- Treaty Access: Access to Norway's tax treaty network depends on the parent entity's residence and treaty eligibility — not automatic.

- Restrictions: A NUF cannot hold equity in Norwegian entities in its own name; the parent company is the contracting and liable party throughout.

Sub-Types

Representative Office

A representative office carries out preparatory or auxiliary functions — market research, liaison, promotion — without generating direct revenue. It does not require VAT registration and has no tax liability in Norway, provided it does not constitute a permanent establishment under applicable treaty definitions.

Closing

A NUF suits foreign businesses testing the Norwegian market or fulfilling specific project-based contracts without committing to a permanent subsidiary structure. The primary limitation is unlimited parental liability for all Norwegian obligations.

Foreign companies with existing legal entities abroad that need a temporary or activity-specific presence in Norway without establishing an independent subsidiary.

Ansvarlig Selskap (ANS), Selskap med Delt Ansvar (DA), and Other Partnership Structures [General Partnership, Limited Partnership, Kommandittselskap]

Norwegian partnership structures are governed by the Selskapsloven (Partnership Act) of 1985. Unlike capital-based entities, these forms carry no separate limited liability by default — partners remain personally exposed to the firm's obligations.

The Ansvarlig Selskap ANS partnership Norway structure requires at least two partners, each bearing joint and unlimited personal liability. Its counterpart, the DA selskap Norway delt ansvar (Selskap med Delt Ansvar), allocates liability proportionally rather than jointly, which can affect creditor recovery.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated partnership | No separate legal personality |

| Members | Called "partners"; minimum 2, no statutory maximum | Individuals or legal entities permitted |

| Local Presence | Registered address in Norway required | No mandatory resident partner under all scenarios |

| Capital | No minimum capital requirement | Contributions defined by partnership agreement |

| Privacy | Partnership agreement not publicly filed | Partners' names appear in Foretaksregisteret |

Focus Points

- Taxation: Partners are taxed individually on their share of profits at personal income tax rates; the entity itself is not a separate tax subject; VAT registration applies if turnover thresholds are met.

- Annual Compliance: Annual accounts must be filed with Regnskapsregisteret if the business meets statutory thresholds under the Regnskapsloven.

- Liability Exposure: ANS partners face joint unlimited liability; DA partners face proportional unlimited liability — both structures expose personal assets.

- Conversion: A partnership may convert to an AS under the Aksjeloven, subject to meeting capital and procedural requirements.

- Treaty Access: These entities generally do not access tax treaty benefits as independent taxpayers; treaty entitlements flow through to individual partners.

Sub-Types

Ansvarlig Selskap (ANS)

All partners share joint and unlimited liability for the firm's total debt, meaning any single partner can be pursued for the full amount. This structure is common among professional service practices such as law or accounting firms.

Selskap med Delt Ansvar (DA)

Liability is divided proportionally among partners according to their agreed shares, rather than applied jointly. The DA selskap is preferred where partners want defined personal exposure.

Kommandittselskap (KS)

The Kommandittselskap limited partnership Norway structure introduces at least one general partner (komplementar) with unlimited liability alongside one or more limited partners (kommandittister) whose exposure is capped at their capital contribution. This separation makes the KS suitable for investment vehicles and real estate structures.

Partnership forms suit businesses where shared professional expertise is the primary asset rather than capital. The absence of a minimum capital requirement lowers the formation barrier, though unlimited personal liability is a material structural constraint for most commercial activities.

ANS and DA structures are best suited for small professional practices or domestic joint ventures where the partners have an established relationship and are comfortable with personal liability exposure.

Enkeltpersonforetak (ENK) — Sole Proprietorship

The Enkeltpersonforetak Norway sole proprietorship is governed by the Act on Business Enterprise Registration (Foretaksregisterloven) of 1985, alongside general provisions under Norwegian commercial law. Unlike a limited company, an ENK carries no separate legal personality — the business and its owner are legally the same entity, meaning full personal liability attaches to all obligations.

Registration with the Brønnøysund Register Centre (Enhetsregisteret) is mandatory once annual turnover exceeds NOK 50,000, though voluntary registration is possible below this threshold. ENK registration in Norway is straightforward, with no minimum capital requirement.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole proprietorship (no separate legal personality) | Owner and business are legally indistinct |

| Members | Single proprietor only | No co-ownership permitted under this structure |

| Local Presence | No registered agent required; a Norwegian address is needed | The proprietor must have a Norwegian personal identification number (D-number or national ID) |

| Capital | No minimum capital | No paid-in capital obligation |

| Liability | Unlimited personal liability | All business debts extend to personal assets |

| Privacy | Proprietor's name and address appear in public register | Limited privacy; details are publicly searchable |

Focus Points

- Taxation: Business income is taxed as personal income under the trinnskatt (step tax) system, with rates reaching up to approximately 47.4%; no corporate income tax applies, and VAT registration is required once turnover exceeds NOK 50,000.

- Annual Compliance: Annual accounts must be filed with the Tax Administration (Skatteetaten); a separate audit requirement does not apply at this scale.

- Treaty Access: As a pass-through structure with no separate legal personality, treaty protection under Norway's tax treaties generally does not extend to the ENK itself.

- Conversion: An ENK can be converted into an AS (private limited company) under a tax-neutral transfer process, subject to the conditions of Section 11-20 of the Tax Act (Skatteloven).

- Restrictions: Only a single natural person who is resident or holds a Norwegian identification number may operate this structure; foreign nationals without a D-number face practical barriers to ENK registration in Norway.

Closing

A Norwegian sole trader setup suits freelancers, consultants, and small-scale traders who require a low-cost, simple operating structure with minimal administrative overhead. The absence of minimum capital and straightforward registration process are clear practical advantages, though unlimited personal liability makes this structure unsuitable for activities carrying significant financial or legal risk.

The ENK is best suited for individual entrepreneurs and sole operators running low-risk, small-scale commercial activities in Norway.

How to Choose the Right Entity Type in Norway

Selecting the correct structure at registration affects tax treatment, liability exposure, reporting obligations, and your ability to operate legally — getting it wrong has measurable consequences.

Why Your Entity Choice Matters

The structure you register shapes every compliance obligation your business carries. Selecting the wrong form can produce outcomes that are difficult and costly to unwind:

- Registering a NUF to conduct full trading activity in Norway while failing to meet the requirements of the Branch Offices Act can result in the Brønnøysund Register Centre striking the registration or imposing penalties.

- Choosing an entity form that does not qualify as a resident taxpayer under Norwegian law means you cannot access Norway's tax treaty network, blocking withholding tax reductions available to counterpart jurisdictions.

- An AS or ASA that cannot demonstrate genuine management and control in Norway may trigger substance-related reporting failures under the Norwegian Tax Administration Act.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or securities each point to a distinct entity form under Norwegian law.

- Liability Exposure: If personal assets must remain protected, structures without limited liability — such as ANS or ENK — are unsuitable regardless of other advantages.

- Ownership Structure: Multi-party ownership with defined profit-sharing obligations suits a DA, while a single shareholder can lawfully hold an AS.

- Tax Objectives: Your need for participation exemption eligibility, treaty access, or a specific withholding tax position should directly inform the structure you select.

- Substance Capacity: If you cannot maintain an office, staff, or board-level decision-making in Norway, certain structures will expose you to reclassification risk.

- Exit and Conversion: The Companies Act (aksjeloven) governs conversion and winding-up procedures; not all entity types permit straightforward redomiciliation or conversion.

Compliance Services for Companies in Norway

Ongoing compliance support for Norwegian entities, including annual reporting, board obligations, and registry maintenance.

Conclusion

Selecting the right structure is the first substantive decision in any Norway company incorporation, and this guide has outlined the practical distinctions between each form. The Aksjeselskap remains by far the most registered entity type, suited to privately held ventures seeking defined liability and a familiar governance framework. The Allmennaksjeselskap serves firms intending to raise capital from public markets. Enkeltpersonforetak suits sole operators prioritizing simplicity over liability protection. Partnerships under the ANS or DA structures are reserved for those prepared to accept personal exposure. The NUF provides foreign businesses with a lighter initial footprint.

Registration is administered through the Foretaksregisteret, and ongoing compliance obligations vary meaningfully across these forms. Regulatory requirements have tightened in recent years, particularly around beneficial ownership disclosure under the Money Laundering Act. Your choice of entity shapes not only liability but also tax treatment, reporting obligations, and long-term structuring options.

How Expanship Can Assist You

Expanship provides corporate services Norway company formation assistance across the full range of structures covered in this guide — from a single-member AS to a publicly listed ASA. Our team works directly with the Brønnøysund Register Centre, the central authority responsible for entity registration and ongoing filings, so your documents are prepared and submitted correctly the first time.

From initial structure selection through to post-incorporation obligations, our services include:

- Preparation and legalization of incorporation documents

- Registered address and local representative provision

- Government filing and liaison with the Foretaksregisteret

- Ongoing compliance management, including annual accounts and shareholder register maintenance

- Banking introduction assistance for new entities

Setting up a business in a foreign jurisdiction involves paperwork, deadlines, and regulatory requirements that vary by entity type. Expanship handles the specifics so your firm can focus on operations from day one.

Get in touch with Expanship Norway to discuss your requirements.

Frequently Asked Questions (FAQ)

The Aksjeselskap (AS) is by far the most widely registered entity, largely because it limits shareholder liability to the amount of capital contributed and does not require a public listing. Its NOK 30,000 minimum share capital threshold makes it accessible to a broad range of founders.

An AS is a locally incorporated entity subject to Norwegian corporate tax at 22% and full Brønnøysund Register Centre reporting obligations. A NUF is a registered branch of a foreign company, meaning the parent entity retains legal and tax exposure in its home jurisdiction, though the branch itself must still file accounts in Norway if it meets statutory thresholds.

Norway maintains a high level of beneficial ownership transparency under the Act on Register of Beneficial Owners. No entity type fully shields ownership from public disclosure. Nominee arrangements exist in practice but do not override the statutory obligation to register the ultimate beneficial owner.

An AS can be formed by a sole shareholder. An Ansvarlig Selskap (ANS) and Selskap med Delt Ansvar (DA), however, require at least two participants by definition, as both are structured around shared ownership. An Enkeltpersonforetak (ENK) is inherently a one-person structure.

Foreign nationals and non-resident companies may establish an AS, NUF, or ENK without a Norwegian citizenship requirement. However, under the Companies Act, at least half of an AS board must ordinarily be resident within the European Economic Area, unless an exemption is granted by the Norwegian government.

Conversion from an AS to an Allmennaksjeselskap (ASA) is expressly regulated under the Public Limited Companies Act and requires meeting the NOK 1,000,000 minimum share capital. Conversion from an ENK or ANS to an AS is also permitted through a formal transformation process involving registration with the Brønnøysund Register Centre.

An AS and ASA each hold full legal personality distinct from their shareholders. An ENK does not; the owner and the business are legally the same person, which means personal assets are exposed to business liabilities. An ANS also lacks separate legal personality in the same sense, with partners bearing joint unlimited liability.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.