Key Takeaways

- Nigeria's principal corporate legislation, the Companies and Allied Matters Act (CAMA) 2020, governs all entity types and assigns registration authority to the Corporate Affairs Commission (CAC).

- The Private Limited Company (Ltd) is the most widely registered structure in Nigeria, preferred by both domestic and foreign businesses for its liability protection and operational flexibility under CAMA.

- Foreign businesses entering Nigeria may operate through a Branch Office, Representative Office, or Subsidiary, each carrying distinct regulatory and liability implications under Nigerian law.

- Incorporated Trustees constitute a separate legal category under CAMA, reserved specifically for NGOs, associations, and non-profit entities rather than commercial enterprises.

Introduction to Entity Types in Nigeria

Nigeria is a federal republic in West Africa, bordered by Benin, Niger, Chad, and Cameroon, and is the continent's most populous nation. Selecting among the available types of business entities in Nigeria requires an understanding of the legal framework that governs each structure, primarily the Companies and Allied Matters Act (CAMA) 2020, which is the principal legislation regulating corporate formation and conduct.

Company registration and ongoing compliance fall under the authority of the Corporate Affairs Commission (CAC), a federal body established under CAMA. The CAC maintains the official register of companies, business names, incorporated trustees, and partnerships.

Nigeria operates a residence-based tax system, with corporate income tax administered by the Federal Inland Revenue Service (FIRS). The entity types available under Nigerian law include the Public Limited Company, Private Limited Company, Limited Liability Partnership, General Partnership, Limited Partnership, Business Name, Branch Office, Representative Office, Subsidiary, and Incorporated Trustees. Each structure carries distinct registration requirements, liability implications, and tax treatment, all of which this article examines in detail.

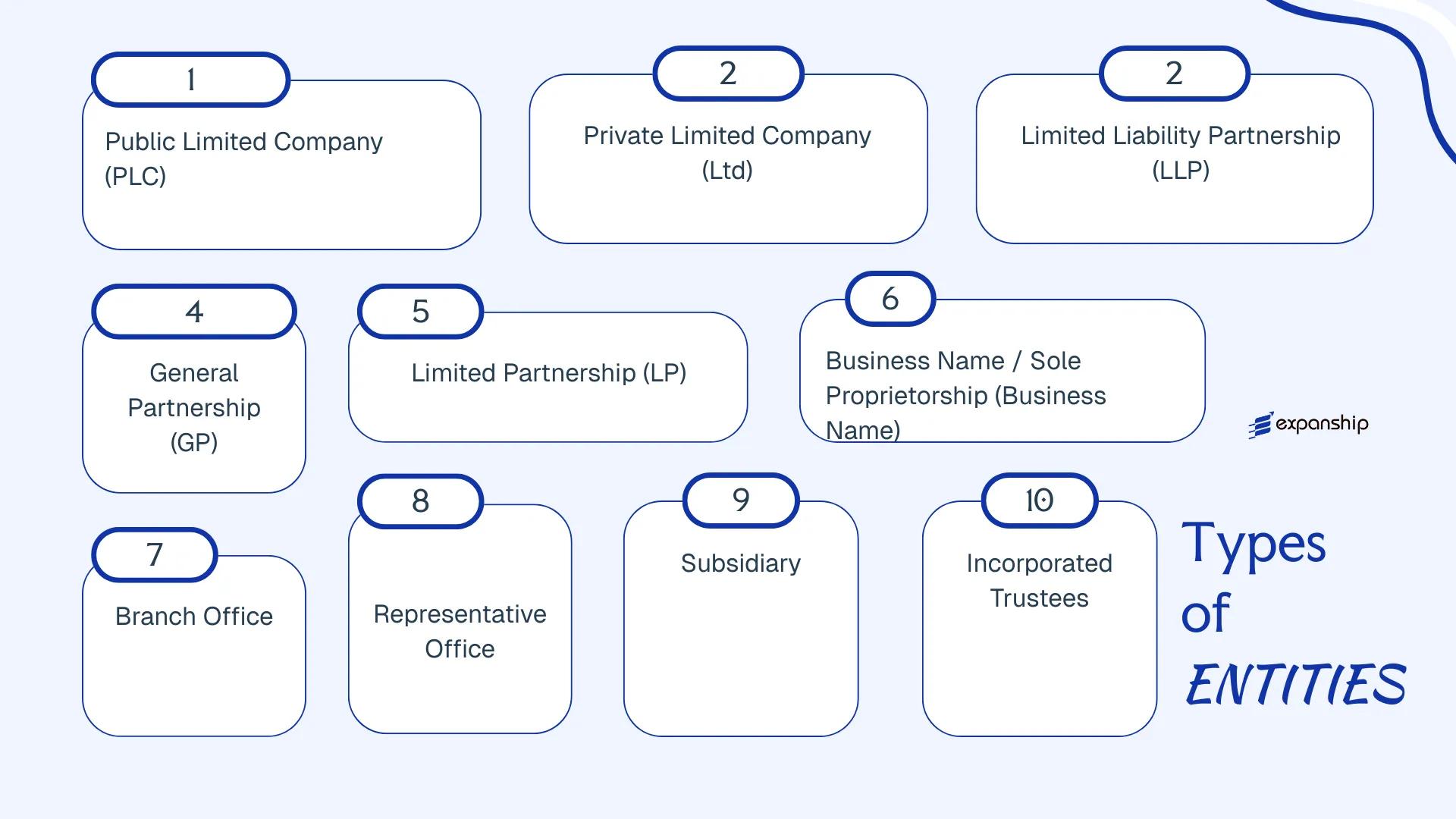

An Overview of Business Structures in Nigeria

Nigeria's company law framework provides several distinct entity types, each governed primarily by the Companies and Allied Matters Act (CAMA) 2020, administered by the Corporate Affairs Commission (CAC). Subsidiary legislation, including the Business Names Act (now consolidated under CAMA), further defines the conditions under which certain structures operate. Each entity type carries a different legal form, liability profile, and set of regulatory obligations suited to a different commercial purpose.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (PLC) | Incorporated company | Limited | Taxed | Yes | 2 shareholders | CAC | CAMA 2020 |

| Private Limited Company (Ltd) | Incorporated company | Limited | Taxed | Yes | 1 shareholder | CAC | CAMA 2020 |

| Limited Liability Partnership (LLP) | Registered partnership | Limited | Taxed | Yes | 2 partners | CAC | CAMA 2020 |

| General Partnership | Unincorporated firm | Unlimited | Taxed | Yes | 2 partners | CAC | CAMA 2020 |

| Limited Partnership | Registered partnership | Mixed | Taxed | Yes | 2 partners | CAC | CAMA 2020 |

| Business Name / Sole Proprietorship | Registered individual | Unlimited | Taxed | Yes | 1 owner | CAC | CAMA 2020 |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Restricted | N/A | CAC / NIPC | CAMA 2020 / NIPC Act |

| Representative Office | Foreign entity extension | Parent liable | Generally exempt | No | N/A | CAC / NIPC | CAMA 2020 / NIPC Act |

| Subsidiary | Incorporated company | Limited | Taxed | Yes | 1 shareholder | CAC | CAMA 2020 |

| Incorporated Trustees | Non-profit body | Limited | Exempt (conditions apply) | No | 2 trustees | CAC | CAMA 2020 |

Each of these structures is examined in full in the sections below.

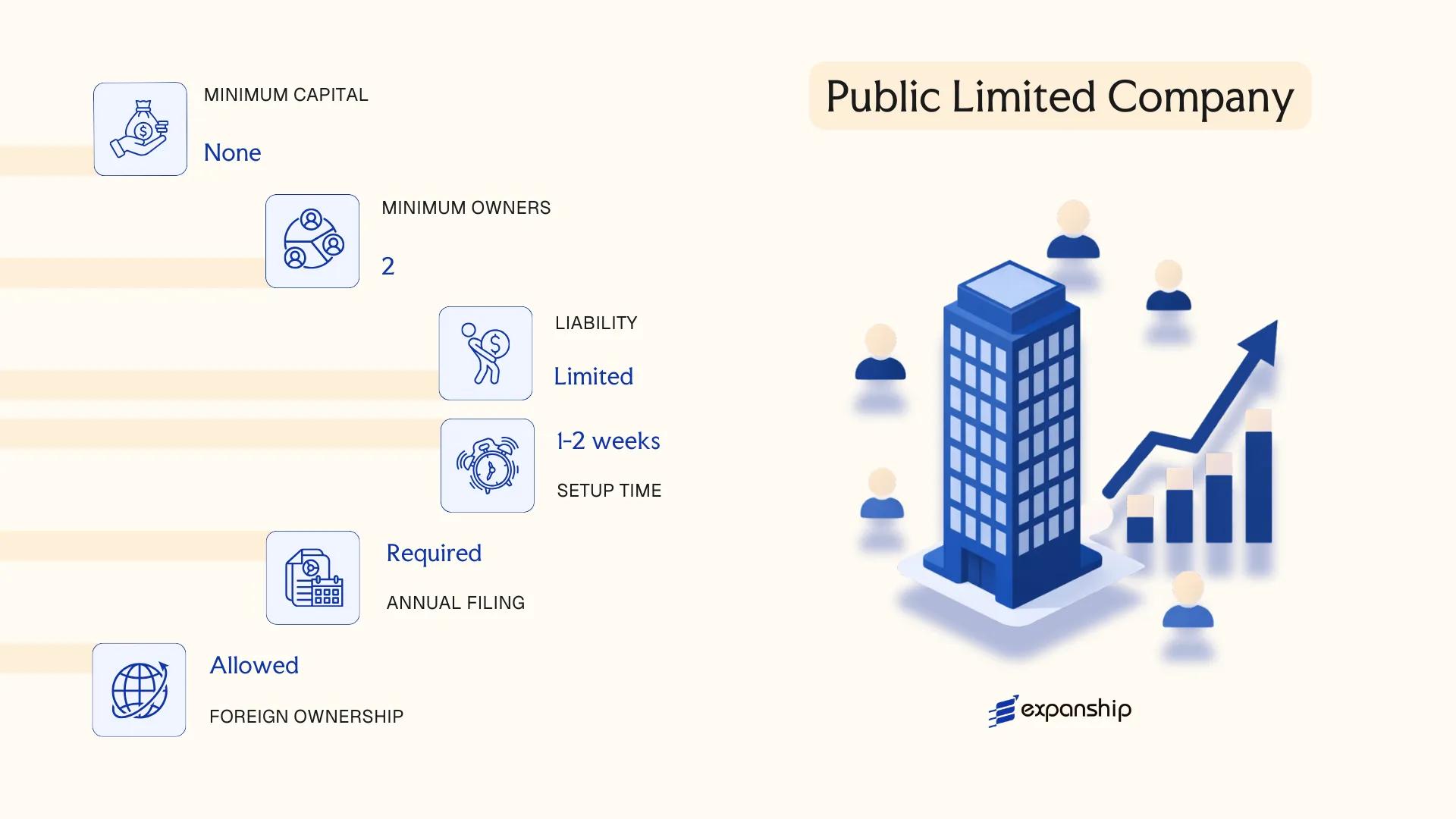

Public Limited Company (PLC) under the Companies and Allied Matters Act (CAMA)

A public limited company (PLC) in Nigeria is governed by the Companies and Allied Matters Act (CAMA) 2020, administered by the Corporate Affairs Commission (CAC). It exists as a separate legal entity from its shareholders, meaning the company can own property, enter contracts, and incur liabilities in its own name.

Shareholders' liability is capped at the value of their unpaid share capital. Because a PLC can offer shares to the general public and list on the Nigerian Exchange Group (NGX), it suits businesses seeking large-scale capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by shares | Separate legal personality; governed by CAMA 2020 |

| Members | Minimum 2 shareholders; no maximum | Directors: minimum 2; at least one must be resident in Nigeria |

| Share Capital | Minimum authorised share capital of ₦2,000,000 | Must include "PLC" in company name |

| Local Presence | Registered office address in Nigeria required | CAC-registered agent not mandatory, but a local director is |

| Public Offering | May offer shares to the public; listing on NGX permitted | SEC registration required for public offers |

| Privacy | Accounts and annual returns filed with CAC are publicly accessible | Beneficial ownership disclosure required under CAMA 2020 |

Focus Points

- Taxation: Subject to Companies Income Tax (CIT) at 30% of taxable profits (0% for companies with turnover under ₦25 million; 20% for medium-sized firms); VAT applies at 7.5%; withholding tax rates vary by transaction type; stamp duty applies on share transfers and certain instruments.

- Annual Compliance: Must file annual returns, audited financial statements, and hold an Annual General Meeting (AGM); listed PLCs face additional Securities and Exchange Commission (SEC) filing requirements.

- Economic Substance: No standalone economic substance regime equivalent to offshore jurisdictions, but corporate residence and effective management tests apply for treaty purposes.

- Treaty Access: Nigeria has Double Taxation Agreements (DTAs) with several countries; PLCs resident in Nigeria may access treaty benefits subject to beneficial ownership and substance conditions.

- Conversion: A PLC may convert to a private limited company by special resolution and CAC approval, provided public shareholding conditions are unwound.

Closing

A PLC suits businesses targeting public capital markets, large institutional investors, or cross-border listings. The structure's mandatory disclosure requirements and regulatory oversight under both CAC and SEC add compliance weight that smaller operations may find disproportionate.

A Nigerian PLC is most appropriate for large enterprises, financial institutions, or businesses seeking access to public equity capital through the Nigerian Exchange Group.

Company Incorporation in Nigeria

Incorporate your Nigerian entity with end-to-end support from CAC registration through post-incorporation compliance.

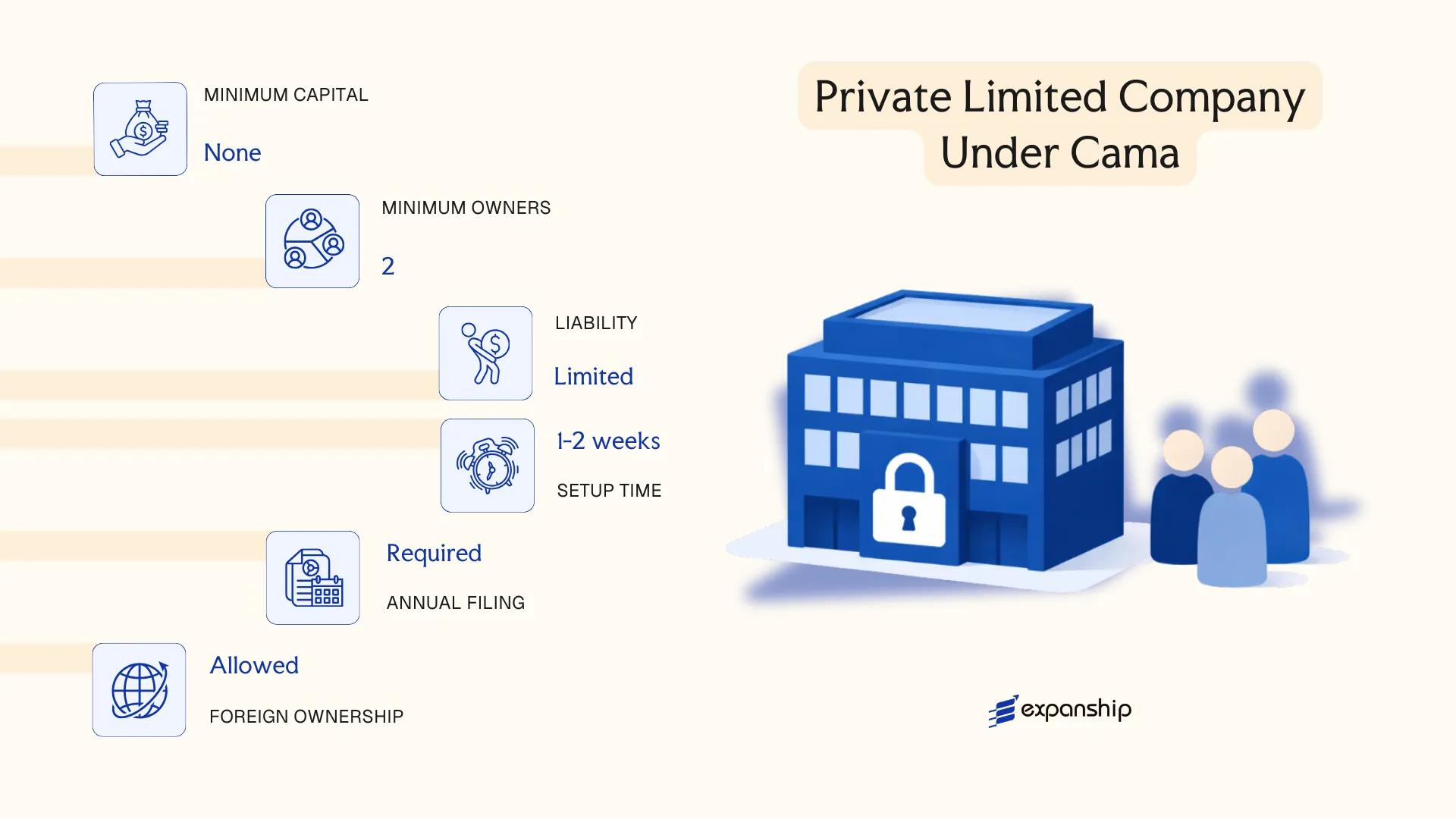

Private Limited Company (Ltd) under CAMA

A private limited company (Nigeria Ltd) is governed by the Companies and Allied Matters Act (CAMA), Cap C20, LFN 2004, as substantially amended by CAMA 2020. It exists as a separate legal entity distinct from its shareholders, meaning the company can own assets, enter contracts, and incur liabilities in its own name.

Liability exposure for each shareholder is confined to the amount unpaid on their shares. This structure makes the private limited company the most widely used vehicle for both domestic and foreign-owned businesses registered with the Corporate Affairs Commission (CAC).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by shares | Separate legal personality; distinct from shareholders |

| Members | Minimum 1 shareholder, maximum 50 | Shareholders cannot transfer shares freely; transfer requires board approval |

| Management | Minimum 1 director; at least one must be ordinarily resident in Nigeria | Directors manage day-to-day operations; a company secretary is required |

| Local Presence | Registered office address in Nigeria | Must be a physical address; CAC correspondence is sent here |

| Share Capital | No statutory minimum under CAMA 2020; denominated in Nigerian Naira (NGN) | Sector-specific regulators (e.g., CBN, SEC) may impose minimum capital thresholds |

| Privacy | Shareholder and director details filed with CAC; public search is possible | Financial statements are not publicly listed, unlike PLCs |

Focus Points

- Taxation: Subject to Companies Income Tax (CIT) at 30% for large companies (turnover above NGN 100 million), 20% for medium-sized companies, and 0% for small companies (turnover below NGN 25 million); VAT applies at 7.5%; withholding tax rates vary by transaction type; stamp duty applies on share capital and certain instruments.

- Annual Compliance: Annual returns must be filed with the CAC within 42 days of each annual general meeting; audited financial statements are required unless exempt as a small company.

- Restrictions: Prohibited from offering shares to the general public or listing on the Nigerian Exchange Group (NGX); share transfers require compliance with the company's articles of association.

- Treaty Access: May access Nigeria's double taxation agreements (DTAs) as a tax resident entity, subject to beneficial ownership and substance considerations.

- Conversion: Can be converted to a public limited company (PLC) under CAMA by special resolution, provided it meets PLC requirements including minimum share capital thresholds set by relevant regulators.

A private limited company suits trading operations, subsidiaries of foreign groups, and holding structures within Nigeria. The liability protection and separate legal personality are clear operational advantages; however, the restriction on public share offerings limits capital-raising options compared to a PLC.

Foreign investors establishing a locally registered operating subsidiary and domestic entrepreneurs seeking formal limited liability without the compliance burden of a publicly listed company.

Limited Liability Partnership (LLP)

Introduced under Part C of the Limited Liability Partnership Act 2022, the limited liability partnership Nigeria LLP framework established a distinct hybrid business structure in Nigerian law. It combines the operational flexibility of a partnership with the protection of limited liability, and the entity holds separate legal personality from its members.

Unlike a general partnership, each partner's financial exposure is capped at their agreed contribution. The LLP itself can own property, enter contracts, and sue or be sued in its own name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate with separate legal personality | Distinct from both partnerships and limited companies |

| Members | Minimum 2 partners; no statutory maximum | At least 2 designated partners required at all times |

| Member Titles | Partners / Designated Partners | Designated partners bear specific compliance responsibilities |

| Registered Office | Physical address in Nigeria required | Must be maintained for official correspondence |

| Capital | No minimum capital prescribed | Contributions defined by the LLP agreement |

| Privacy | LLP agreement not publicly filed | Names of partners are on public record |

Focus Points

- Taxation: LLPs are generally taxed on a pass-through basis; partners are individually liable for income tax on their share of profits, though VAT and withholding tax obligations still apply at the entity level where relevant.

- Annual Compliance: Annual returns must be filed with the Corporate Affairs Commission (CAC); designated partners are personally responsible for filing obligations.

- Conversion: An existing partnership or company may convert to an LLP under the Act, subject to CAC approval and applicable procedural requirements.

- Restrictions: LLPs cannot issue shares or raise capital from the public, which limits their utility for equity-based fundraising.

- Treaty Access: As a relatively new structure, treaty access and international recognition may vary; professional advice is warranted before using an LLP for cross-border arrangements.

Closing

The LLP suits professional service firms, joint ventures, and fund management arrangements where partners want liability protection without the formality of a corporate board structure. Its primary limitation is the inability to issue shares, which makes equity investment structuring more complex.

Best suited for professional practices (legal, consulting, accounting) and two-party joint ventures where partners require liability protection but prefer contractual governance over a corporate constitution.

Partnerships (General Partnership, Limited Partnership)

Under Nigerian law, the general and limited partnership Nigeria framework is governed primarily by the Partnership Law (which operates at the state level, with Lagos State's Partnership Law being the most referenced) and the Companies and Allied Matters Act (CAMA) 2020 for limited partnerships registered at the federal level. Neither a general nor a limited partnership constitutes a separate legal entity distinct from its partners, meaning partners carry personal liability for the obligations of the firm.

Partnership registration Nigeria is administered through the Corporate Affairs Commission (CAC), the same body that oversees company incorporation. A general partnership requires no formal registration, though operating under a business name requires registration. A limited partnership must be registered with the CAC, and at least one general partner must assume unlimited liability.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated association | No separate legal personality from partners |

| Members | Partners (General / Limited) | Minimum 2; maximum 20 for general partnerships under CAMA |

| Liability | General partners: unlimited; Limited partners: capped at capital contribution | Limited partners cannot participate in management |

| Capital | No statutory minimum; contributions in NGN | Defined by partnership agreement |

| Local Presence | Registered address required; no mandatory local agent | CAC registration address must be in Nigeria |

| Privacy | Partnership deed not publicly filed in detail | Names of partners appear in CAC records |

Focus Points

- Taxation: Partnerships are fiscally transparent; each partner is taxed individually under the Personal Income Tax Act (PITA) or Companies Income Tax Act (CITA) depending on partner type; VAT obligations apply to taxable supplies made by the firm.

- Annual Compliance: General partnerships have minimal filing obligations; limited partnerships must file annual returns with the CAC.

- Treaty Access: Partnerships generally do not access Nigeria's double tax treaties directly, as treaty benefits flow to the individual partners based on their residency status.

- Restrictions: Limited partners lose liability protection if they participate in day-to-day management decisions.

Sub-Types

General Partnership

All partners share equal management rights and bear unlimited personal liability for the firm's debts. Commonly used for professional services such as law and accounting firms.

Limited Partnership

Comprises at least one general partner with unlimited liability and one or more limited partners whose exposure is restricted to their agreed capital contribution. Typically used for investment vehicles or joint ventures where passive investors require liability protection.

Closing

Partnerships suit professional service providers, joint ventures between individuals, and situations where pass-through taxation is preferred over corporate-level tax. The transparent tax treatment is a clear structural advantage; however, the absence of limited liability for general partners represents a significant exposure that trading businesses should weigh carefully.

Partnerships are most appropriate for professional firms and small joint ventures where the partners know each other well and pass-through taxation outweighs the need for liability protection.

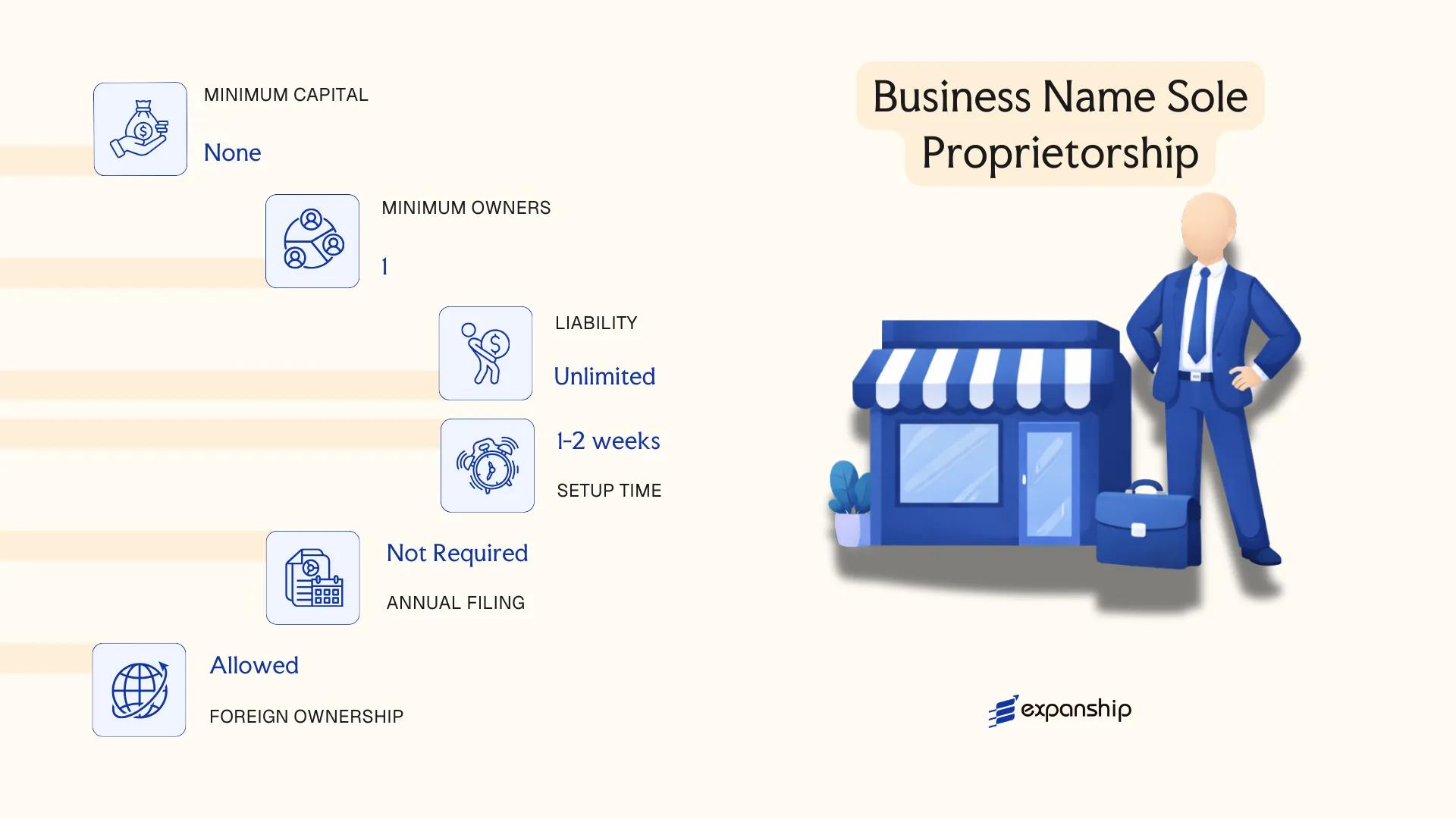

Business Name / Sole Proprietorship

Business name registration in Nigeria, operating as a sole proprietorship, is governed by the Companies and Allied Matters Act (CAMA) 2020 and administered by the Corporate Affairs Commission (CAC). This structure carries no separate legal personality — the business and its owner are legally the same, meaning personal assets remain exposed to business liabilities.

Registration is mandatory before trading under any name other than your own. The CAC processes business name registrations through its online portal, and the registration is valid for an indefinite period subject to annual renewal obligations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Business Name (unincorporated) | No distinct legal personality from the owner |

| Owner Designation | Proprietor | Single individual; no concept of shareholders or directors |

| Membership | 1 proprietor only | Cannot have multiple owners; use a partnership or company for shared ownership |

| Local Presence | Registered business address in Nigeria | Must be a physical address; CAC correspondence directed here |

| Capital | No minimum capital requirement | Owner funds the business directly from personal resources |

| Privacy | Proprietor's name and address on public CAC register | No confidentiality provisions under CAMA |

Focus Points

- Taxation: Subject to personal income tax under the Personal Income Tax Act (PITA); VAT obligations apply where annual turnover exceeds the registration threshold; stamp duty applies to qualifying instruments.

- Annual Compliance: Annual renewal of registration is required with the CAC; failure to renew attracts penalties.

- Conversion: A business name can be converted into a private limited company under CAMA, subject to a formal incorporation process with the CAC.

- Treaty Access: No access to Nigeria's tax treaty network, as benefits apply only to corporate entities recognized under those treaties.

- Restrictions: Cannot own property, sue, or be sued in its own name; all legal action involves the proprietor personally.

Closing

A registered business name suits small-scale traders, freelancers, and micro-enterprises where simplicity and low compliance costs outweigh the need for liability protection. The primary drawback is unlimited personal liability, which creates material financial risk as the business grows.

Individuals operating small, low-risk businesses in Nigeria who require a formal registration without the administrative overhead of incorporation.

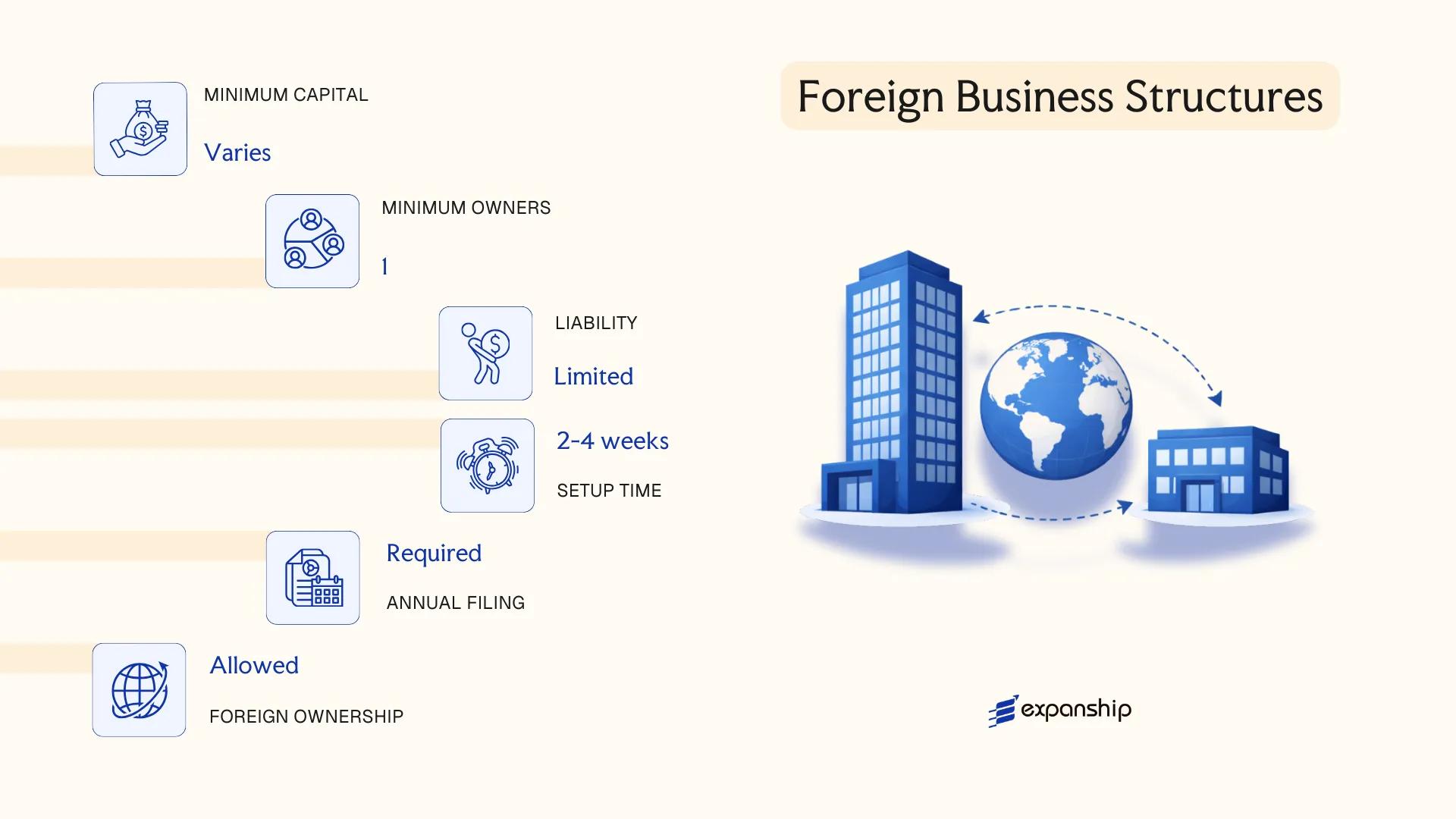

Foreign Business Structures (Branch Office, Representative Office, Subsidiary)

Foreign entities seeking a formal presence are governed primarily by the Companies and Allied Matters Act (CAMA) 2020 and the Companies Regulations 2021, both administered by the Corporate Affairs Commission (CAC). A foreign company branch office Nigeria registration is a distinct process from domestic incorporation and requires separate filings under Part B of CAMA, which covers foreign company registration.

A subsidiary incorporated locally is treated as a separate legal entity under Nigerian law, carrying its own limited liability. A branch, by contrast, has no independent legal personality — the parent company remains directly liable for its obligations.

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary |

|---|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Limited-purpose presence; no separate legal personality | Separate Nigerian legal entity (typically a Private Limited Company) |

| Liability | Parent bears full liability | Parent bears full liability | Liability limited to the subsidiary's own assets |

| Registered Agent / Local Address | Mandatory; must file registered address with CAC | Required for CAC filing purposes | Mandatory registered office in Nigeria |

| Minimum Capital | No statutory minimum, but subject to sector-specific requirements (e.g., CBN rules for financial services) | Generally none | Subject to sector-specific thresholds |

| Permitted Activities | Can conduct revenue-generating operations | Restricted to liaison, market research, and promotional activities — cannot generate revenue | Full commercial operations permitted |

| Privacy | Directors and officers disclosed to CAC; publicly searchable | Similar disclosure obligations | Directors and shareholders filed with CAC |

Focus Points

- Taxation: Branch profits are subject to 30% Companies Income Tax; VAT at 7.5% applies to taxable supplies; withholding tax obligations apply to payments made; stamp duty is payable on instruments executed in Nigeria.

- Treaty Access: Subsidiaries may access Nigeria's double tax treaties as a resident entity; branches generally face limitations depending on treaty provisions and the parent's home jurisdiction.

- Annual Compliance: All registered foreign entities must file annual returns with the CAC; branches must also submit audited accounts of the parent company.

- Sector Restrictions: Certain sectors — including oil and gas, banking, and defence-related activities — impose additional licensing or local participation requirements on foreign-owned structures.

- Conversion: A branch can be converted to a subsidiary, though this requires a fresh incorporation process rather than a straightforward administrative conversion.

Sub-Types

Branch Office

Registered under Part B of CAMA, a branch conducts active business in Nigeria while remaining an extension of the foreign parent. It is suited to companies that want operational presence without establishing a separate local entity.

Representative Office

This structure is limited strictly to non-commercial activities such as liaison, market intelligence, and promotion of the parent's products or services. It cannot enter contracts or invoice clients directly in Nigeria.

Subsidiary

Incorporated as a Private Limited Company under Part A of CAMA, a subsidiary operates as a fully independent Nigerian entity. It is the structure most commonly used where long-term commercial activity, local contracts, or regulated sector licensing is required.

Foreign companies conducting active trade or holding local assets typically favour the subsidiary structure for its liability protection and cleaner regulatory profile. The branch office suits entities that need operational presence without the administrative overhead of a separate incorporation, though it exposes the parent to direct legal liability in Nigeria.

Foreign companies entering Nigeria for long-term commercial operations are best served by a subsidiary; the branch office is more appropriate for established multinationals with a defined, time-limited project scope.

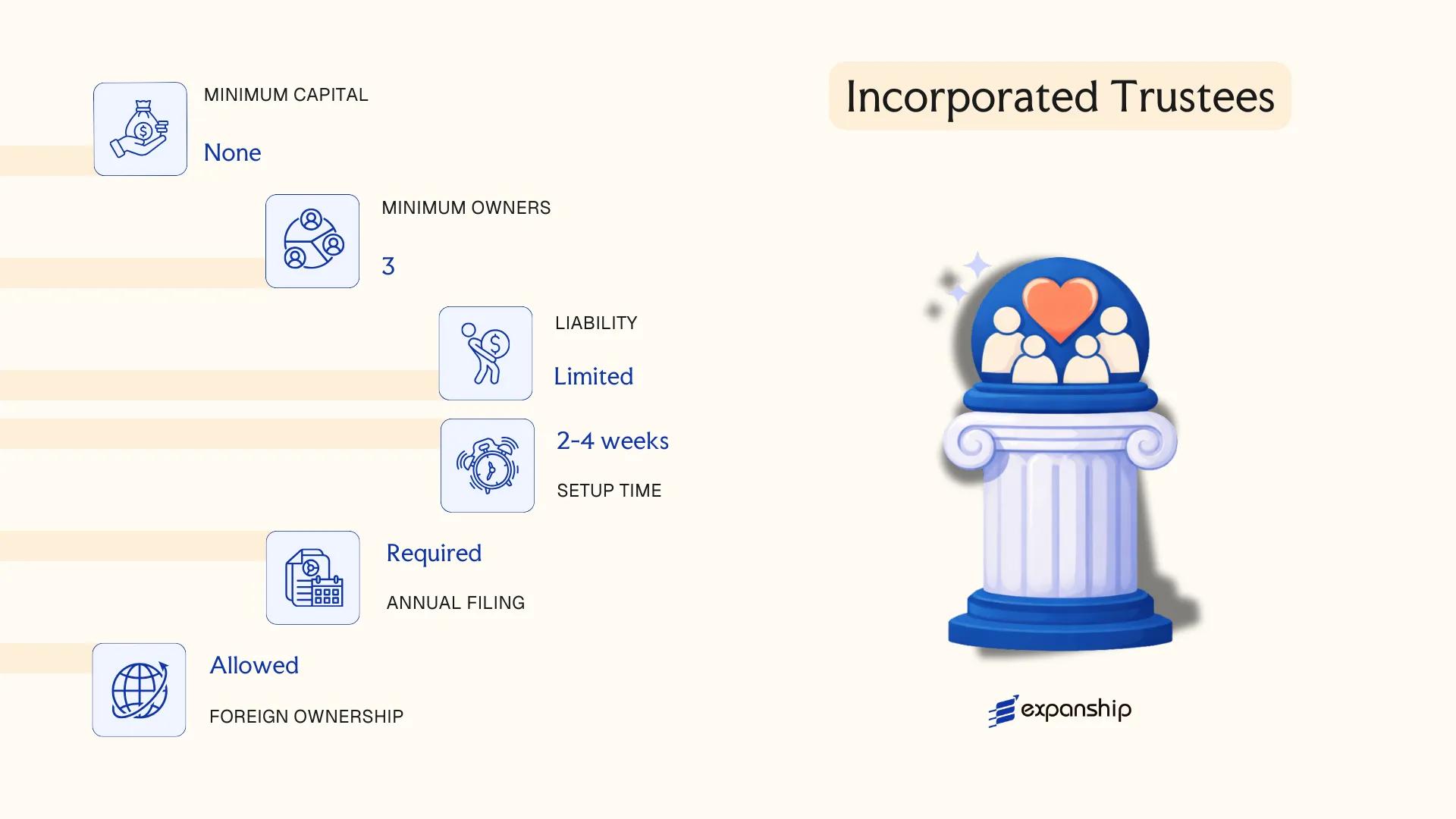

Incorporated Trustees (NGOs, Associations, and Non-Profits)

Incorporated trustees Nigeria NGO registration is governed by Part F of the Companies and Allied Matters Act (CAMA) 2020, administered by the Corporate Affairs Commission (CAC). Unlike commercial entities, this structure is designed for associations, religious bodies, educational institutions, and charitable organisations that operate without a profit-sharing objective.

Upon registration, the trustees acquire a distinct legal personality separate from individual members. This means the organisation can own property, enter contracts, and initiate legal proceedings in its own name. Liability of individual trustees is generally limited to the extent of their obligations under the governing constitution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body Corporate | Separate legal personality distinct from trustees and members |

| Governing Individuals | Trustees (minimum 2) | No statutory maximum; trustees are named in the application |

| Members | General membership body | Size not fixed by CAMA; defined by the organisation's constitution |

| Local Presence | Registered office address in Nigeria | Must be a physical address; a P.O. Box is not sufficient |

| Capital | No share capital or minimum capital requirement | Funded by donations, grants, subscriptions, or levies |

| Privacy | Constitution and trustee names filed with CAC | Publicly accessible on the CAC register |

Focus Points

- Taxation: Incorporated trustees are exempt from Companies Income Tax on non-commercial income; however, where the organisation carries on trade or business, that income is taxable. Value Added Tax (VAT) obligations apply to taxable supplies, and withholding tax applies to qualifying payments made by the organisation.

- Annual Compliance: Annual returns must be filed with the CAC; failure attracts penalties under CAMA 2020.

- Restrictions: Surplus income or assets cannot be distributed to trustees or members; dissolution requires assets to be transferred to a similar organisation or applied for public benefit.

- Conversion: CAMA 2020 does not provide a direct conversion pathway from incorporated trustees to a commercial entity.

- Regulatory Oversight: Certain sectors (health, education, fundraising) may require additional licences from sector-specific federal or state authorities beyond CAC registration.

Closing

This structure suits membership associations, religious bodies, civil society organisations, and foundations that require legal standing to hold assets and execute agreements. The principal advantage is the ability to operate as a recognised legal entity without share capital obligations; the main limitation is the absolute prohibition on profit distribution to members or trustees.

Incorporated trustees are most appropriate for non-governmental organisations, religious institutions, professional associations, and community groups that require legal personality but have no commercial profit objective.

How to Choose the Right Entity Type in Nigeria

Selecting the correct structure from the outset determines far more than your registration paperwork — it shapes your tax position, liability exposure, and operational capacity for years ahead. Knowing how to choose the right business structure in Nigeria requires working through a set of concrete, jurisdiction-specific factors rather than defaulting to the most familiar form.

Why Your Entity Choice Matters

Choosing the wrong entity type produces concrete legal and financial consequences under Nigerian law:

- Registering a foreign company branch without filing Form CAC/BR/01 with the Corporate Affairs Commission (CAC) and obtaining a business permit means you are trading in breach of the Companies and Allied Matters Act 2020, which can result in striking off and director penalties.

- Choosing Incorporated Trustee status when you require access to Nigeria's double taxation agreements means the entity cannot benefit from withholding tax reductions available to qualifying companies under those treaties.

- Forming a Private Limited Company for a solo consultancy triggers mandatory annual audit requirements under CAMA, adding costs that a Business Name registration would not.

- Selecting a structure that prohibits public capital raising when your growth plan requires equity investment from the public locks you into a conversion process that requires fresh CAC filings and shareholder resolutions.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as banking or insurance, and passive asset holding each require distinct entity forms under Nigerian law — some sectors mandate a PLC or a specific licensed vehicle.

- Ownership Structure: A sole operator and a multi-party joint venture face different governance requirements, since a Business Name suits single ownership while a company structure accommodates shareholding agreements and board composition.

- Tax Objectives: Your eligibility for the Pioneer Status Incentive under the Nigerian Investment Promotion Commission Act or applicable double taxation treaty benefits depends on operating through a qualifying corporate entity.

- Foreign Participation: Non-Nigerian investors are subject to the minimum paid-up capital requirements under the Nigerian Investment Promotion Commission Act, which vary by activity and directly influence which entity form is viable.

- Exit and Conversion: Not all Nigerian structures permit straightforward redomiciliation or conversion — a Limited Liability Partnership cannot simply be converted to a PLC without a full dissolution and re-registration process.

Corporate Compliance Services in Nigeria

CAC annual returns, regulatory filings, and ongoing compliance support for companies registered in Nigeria.

Conclusion

Selecting the right structure is the first binding decision your business makes under Nigerian law, and this Nigeria company incorporation conclusion guide reflects that each entity type serves a distinct purpose. The Private Limited Company (Ltd) remains the most commonly registered structure, favoured by domestic and foreign-owned businesses alike for its liability protection and operational flexibility under the Companies and Allied Matters Act (CAMA) 2020. Public Limited Companies suit businesses targeting capital markets; Limited Liability Partnerships serve professional service providers; General and Limited Partnerships work for smaller, less formal arrangements. Business Names cover sole operators, while Incorporated Trustees are reserved for non-profit and associational purposes.

Registered by the Corporate Affairs Commission, each structure carries its own compliance obligations. Amendments introduced through CAMA 2020 have modernised filing procedures and reduced bureaucratic friction, signalling a continued trajectory toward greater regulatory efficiency and alignment with international standards.

How Expanship Can Assist You

Expanship's company registration services Nigeria covers the full arc of incorporation, from selecting the appropriate entity type under the Companies and Allied Matters Act (CAMA) 2020 to filing with the Corporate Affairs Commission (CAC) and maintaining post-incorporation compliance.

Across each structure covered in this guide, the documentation requirements, filing procedures, and regulatory obligations differ. Here is what Expanship manages on your behalf:

- Document preparation and notarization

- Registered office and registered agent provision

- CAC filing and government liaison

- Post-incorporation compliance management

- Annual returns and statutory record-keeping

- Banking introduction assistance

Your business does not need to be physically present in Nigeria at any stage of the process — Expanship coordinates directly with the relevant authorities on your behalf.

To discuss your specific requirements, contact Expanship Nigeria.

Frequently Asked Questions (FAQ)

The Private Limited Company (Ltd) is the most frequently incorporated structure, registered under CAMA 2020. Its combination of limited liability, a minimum share capital requirement of ₦100,000, and suitability for both resident and foreign shareholders makes it the default choice across most commercial sectors.

A Branch Office is an extension of its foreign parent and carries no separate legal personality under Nigerian law, while a Private Limited Company is an independent legal entity. For tax purposes, both are subject to Companies Income Tax, but a subsidiary structure typically offers cleaner liability separation. Compliance obligations also differ: a Branch must maintain its parent's registration documents with the CAC alongside local filings.

Among registered structures, the Private Limited Company does not require public disclosure of shareholder details beyond the CAC register, which is accessible upon formal request rather than open publication. Nominee directorships are permissible under CAMA 2020, subject to the beneficial ownership disclosure requirements introduced by the Companies Regulations 2021.

Not uniformly. A Private Limited Company can be formed by a sole shareholder under CAMA 2020, and a Business Name registration covers sole proprietors. General Partnerships and Limited Partnerships require a minimum of two partners, while an LLP also requires at least two designated partners.

Foreigners may incorporate a Private Limited Company, Public Limited Company, or Limited Liability Partnership, and may establish a Branch or Representative Office of a foreign firm. Each pathway requires registration with the CAC, and businesses in certain sectors must additionally obtain approval from the Nigerian Investment Promotion Commission (NIPC) under the Nigerian Investment Promotion Commission Act.

CAMA 2020 permits conversion between certain structures; a Private Limited Company may re-register as a Public Limited Company by meeting the applicable share capital and membership thresholds. Conversion from a Business Name registration into a limited liability structure requires fresh incorporation rather than a continuation process.

No. A Business Name and a General Partnership do not confer separate legal personality; the owners remain personally liable for obligations. By contrast, a Private Limited Company, Public Limited Company, LLP, and Incorporated Trustees each hold distinct legal identities under CAMA 2020, capable of holding assets, entering contracts, and suing in their own names.

A Business Name registration under Part B of CAMA 2020 involves the lightest post-registration burden, with no requirement to file annual returns in the same form as a limited liability company. The trade-off is the absence of limited liability protection, which makes this structure suited only to small-scale or low-risk sole trading activity.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.