Key Takeaways

- Niger's corporate legal framework is governed by the OHADA Uniform Act on Commercial Companies, making its entity types and governance rules consistent with other OHADA member states rather than derived from purely domestic legislation.

- Company registration in Niger is administered through the Centre de Formalités des Entreprises (CFE), operating under the Ministry of Commerce.

- The SARL is the most commonly registered private sector structure in Niger, suited to small and mid-sized ventures with a defined shareholder group.

- Foreign entities can establish a presence in Niger without forming a separate legal entity by operating through a Branch Office or Representative Office structure.

Introduction to Entity Types in Niger

Niger is a landlocked country in West Africa, bordered by Algeria, Libya, Chad, Nigeria, Benin, Burkina Faso, and Mali. It is an independent republic and a member state of the Economic Community of West African States (ECOWAS). For the purposes of company registration and corporate governance, the types of business entities in Niger are governed primarily by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups (Acte Uniforme relatif au droit des sociétés commerciales et du groupement d'intérêt économique), which Niger adopted as a signatory to the OHADA treaty.

Company registration is administered through the Centre de Formalités des Entreprises (CFE), which operates under the Ministry of Commerce. Niger applies a territorial tax system, meaning corporate tax obligations generally apply to income sourced within the country.

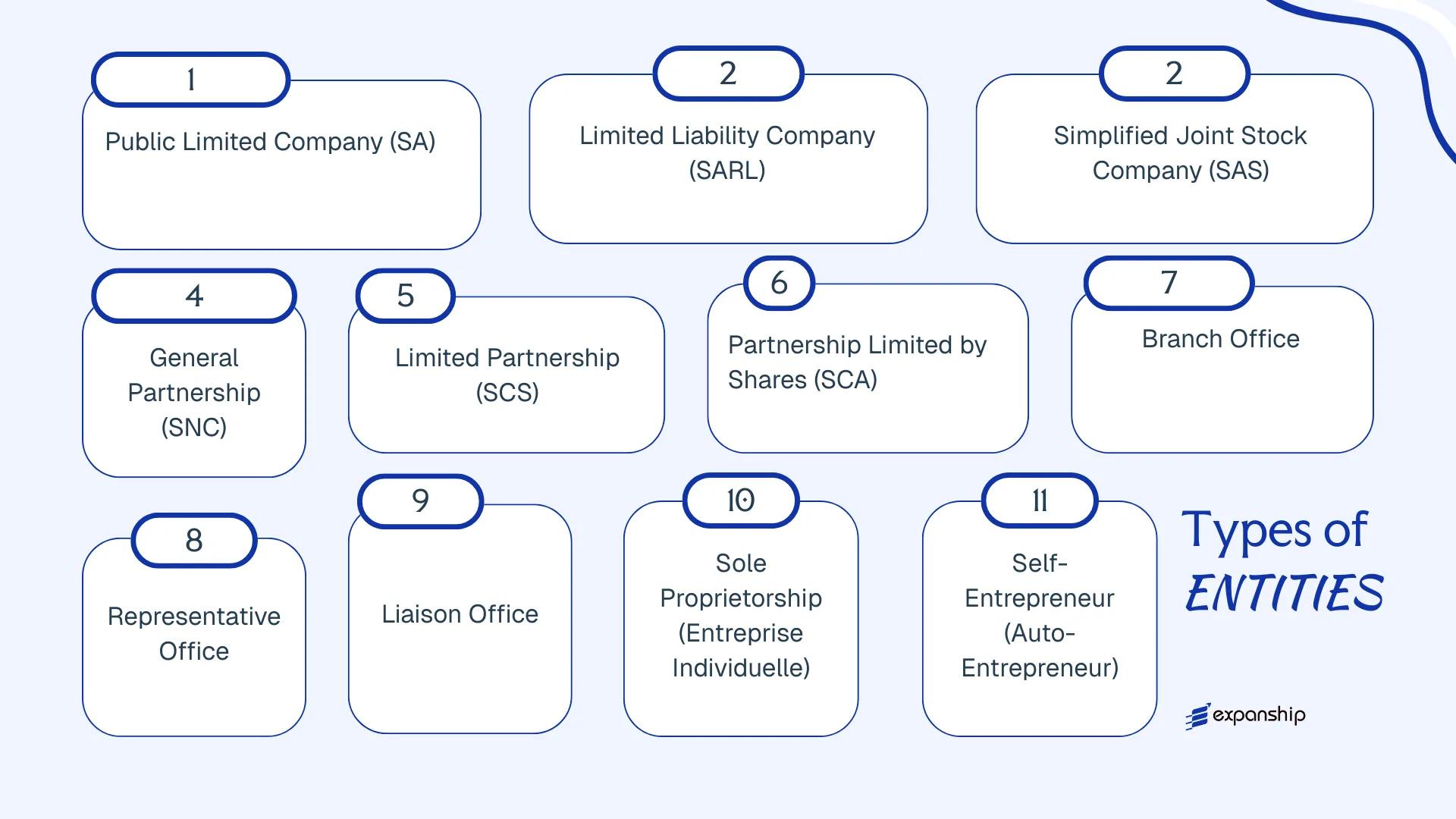

Legal entities Niger OHADA framework recognizes include the Société Anonyme (SA), Société à Responsabilité Limitée (SARL), Société par Actions Simplifiée (SAS), Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA), Branch Office, Representative Office, and Sole Proprietorship structures such as the Entreprise Individuelle and Auto-Entrepreneur. Each of these Niger corporate structures carries distinct liability, governance, and capital requirements, all of which this article examines in detail.

An Overview of Business structures in Niger

Under the OHADA (Organisation pour l'Harmonisation en Afrique des Affaires) framework, businesses operating in Niger are governed primarily by the Acte Uniforme relatif au Droit des Sociétés Commerciales et du Groupement d'Intérêt Économique (AUDSCGIE), which defines the available legal forms for commercial activity. This treaty-based legislation, adopted across 17 member states including Niger, standardises company formation, governance, and dissolution. Each structure carries distinct liability, capital, and operational characteristics suited to different commercial contexts.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Société Anonyme (SA) | Corporation | Limited to shares | Taxable | Permitted | 1 shareholder | RCCM, ANSI | AUDSCGIE |

| Société à Responsabilité Limitée (SARL) | Private limited | Limited to contribution | Taxable | Permitted | 1 member | RCCM, ANSI | AUDSCGIE |

| Société par Actions Simplifiée (SAS) | Simplified corporation | Limited to shares | Taxable | Permitted | 1 shareholder | RCCM, ANSI | AUDSCGIE |

| Société en Nom Collectif (SNC) | General partnership | Unlimited, joint | Taxable | Permitted | 2 partners | RCCM | AUDSCGIE |

| Société en Commandite Simple (SCS) | Limited partnership | Mixed liability | Taxable | Permitted | 2 partners | RCCM | AUDSCGIE |

| Société en Commandite par Actions (SCA) | Partnership by shares | Mixed liability | Taxable | Permitted | 4 members | RCCM | AUDSCGIE |

| Branch Office | Extension of parent | Parent liable | Taxable | Permitted | N/A | RCCM, ANSI | AUDSCGIE |

| Representative Office | Non-trading entity | Parent liable | Generally exempt | Not permitted | N/A | ANSI | Local regulation |

| Liaison Office | Non-trading entity | Parent liable | Generally exempt | Not permitted | N/A | ANSI | Local regulation |

| Entreprise Individuelle | Sole proprietorship | Unlimited | Taxable | Permitted | 1 owner | RCCM | Local regulation |

| Auto-Entrepreneur | Simplified sole trader | Unlimited | Simplified regime | Permitted | 1 owner | RCCM, Tax Authority | Local regulation |

Each of these structures is examined in full in the sections below.

Société Anonyme (SA)

Société Anonyme SA Niger registration falls under the OHADA Uniform Act on Commercial Companies and Economic Interest Groups (AUSC), which Niger adopted as a member state of the Organisation pour l'Harmonisation en Afrique du Droit des Affaires. The SA is a joint stock company with separate legal personality, meaning the entity itself holds rights and obligations distinct from its shareholders.

Liability is limited to each shareholder's capital contribution. This structure suits larger enterprises requiring access to external capital, since shares may be offered to the public under specific conditions governed by the AUSC.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (Joint Stock Company) | Governed by OHADA AUSC |

| Members | Shareholders (minimum 1, no maximum) | Single-shareholder SA permitted under revised AUSC |

| Governance | Board of Directors (minimum 3 directors) or single Administrator | Two-tier governance option available |

| Registered Office | Physical address in Niger required | P.O. Box alone insufficient |

| Minimum Capital | XOF 10,000,000 | Must be fully subscribed; at least 50% paid up at incorporation |

| Share Transfers | Freely transferable unless restricted by articles | Restrictions must be explicitly stated in the statutes |

| Privacy | Shareholder register is not public; accounts filed with RCCM | Beneficial ownership disclosure rules apply under OHADA frameworks |

Focus Points

- Taxation: Corporate income tax applies at the standard rate; VAT registration is mandatory above the applicable threshold; withholding taxes apply to dividends, interest, and service fees paid to non-residents — full details are published by the Direction Générale des Impôts (DGI).

- Annual Compliance: Audited financial statements required; at least one statutory auditor (commissaire aux comptes) must be appointed where thresholds are met under the AUSC.

- Treaty Access: Niger maintains a limited network of double taxation agreements; treaty eligibility depends on beneficial ownership and substance conditions.

- Conversion: An SA may be converted into a SARL or SAS without dissolution, subject to shareholder approval and compliance with capital requirements of the target form.

- Public Offering Restriction: Only an SA may issue shares to the public, but doing so triggers additional regulatory obligations under OHADA capital markets rules.

Closing

The SA suits holding structures, large trading operations, and businesses anticipating external investment or eventual listing. Its principal advantage is the ability to raise capital through share issuance; the main limitation is the administrative burden, including mandatory auditor appointment and board governance requirements that increase operating costs.

Best suited for large-scale enterprises, joint ventures, or businesses planning to attract institutional investors or operate across multiple OHADA member states.

Company Incorporation in Niger

Register your SA or other business entity in Niger with Expanship's end-to-end incorporation service.

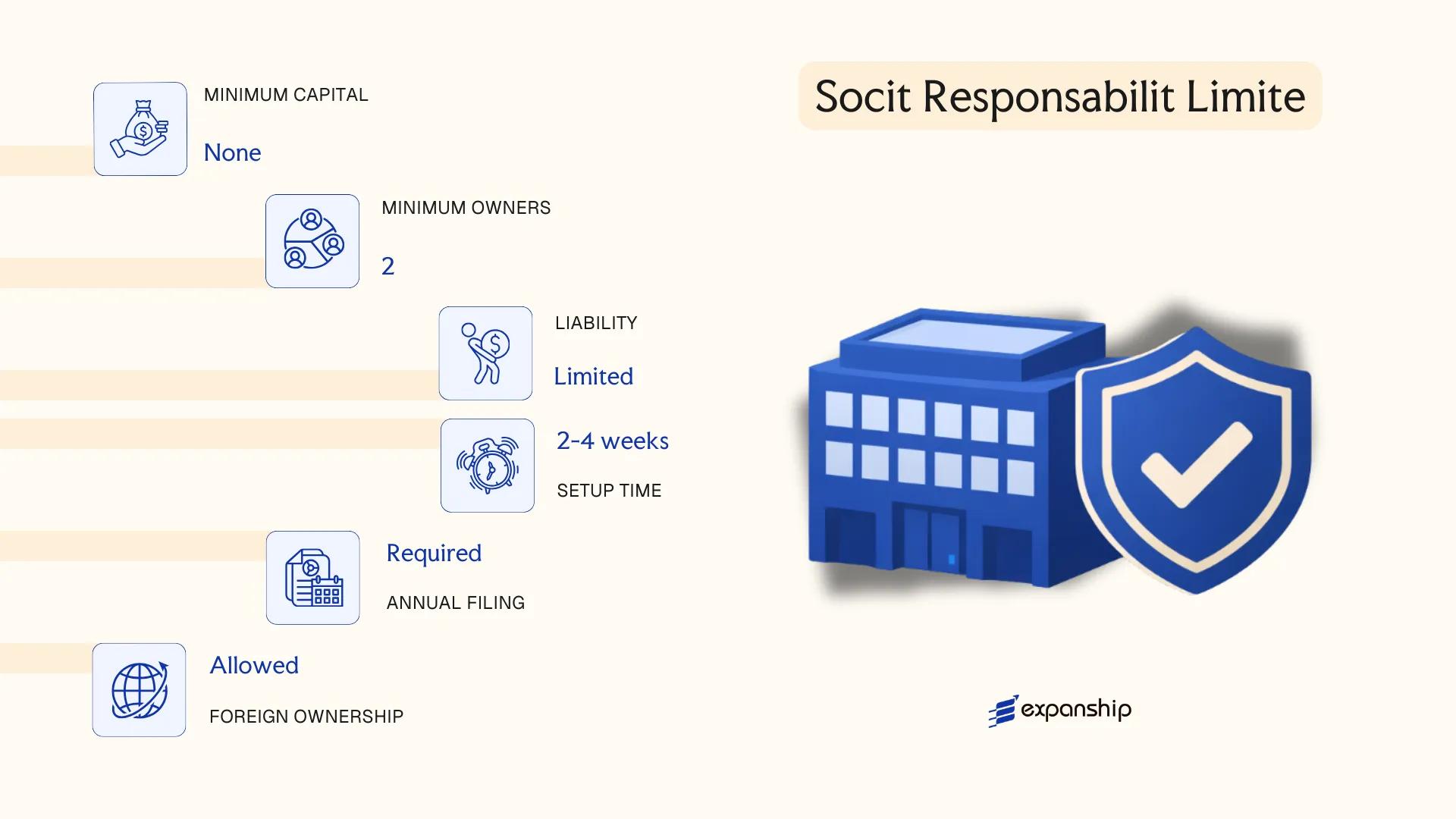

Société à Responsabilité Limitée (SARL)

The Société à Responsabilité Limitée SARL Niger is governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, most recently revised in 2014. As a hybrid structure, it combines the liability protection of a corporation with the operational flexibility typically associated with smaller private firms, giving the entity separate legal personality distinct from its members.

Each member's financial exposure is capped at their capital contribution. This makes the SARL a commonly chosen form for small to medium-sized businesses, joint ventures, and locally established foreign-owned operations in Niger.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company | Governed by OHADA Uniform Act (revised 2014) |

| Members | 1–50 shareholders (referred to as associés) | Single-member variant is the SARL Unipersonnelle |

| Management | One or more gérants (managers) | Need not be shareholders; no nationality restriction under OHADA |

| Registered Office | Physical address in Niger required | A registered office address within the jurisdiction is mandatory |

| Share Capital | No statutory minimum under the revised OHADA Act | Capital divided into parts sociales (non-negotiable shares) |

| Privacy | Shareholder details filed with RCCM | Not publicly searchable in the same manner as listed entities |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate applicable in Niger; VAT registration required once turnover thresholds are met; withholding taxes apply to dividends, interest, and service fees paid to non-residents.

- Annual Compliance: Must file annual financial statements with the Registre du Commerce et du Crédit Mobilier (RCCM) and hold an annual general meeting of associates.

- Transfer Restrictions: Parts sociales are not freely transferable to third parties; transfers require approval from associates holding a specified majority, as prescribed by the OHADA Act.

- Treaty Access: Niger is a member of ECOWAS and the WAEMU zone; tax treaty access depends on the residency of the SARL and applicable bilateral agreements.

- Conversion: A SARL may be converted into an SA once it meets the relevant capital and membership thresholds under the OHADA framework.

Closing

The SARL suits trading operations, wholly owned subsidiaries of foreign groups, and domestic ventures where ownership is to remain private and liability contained. Its principal constraint is the restriction on transferring shares to outside parties, which limits equity liquidity.

Best suited for foreign investors establishing a locally operating subsidiary or small-to-medium domestic businesses that require liability protection without the compliance burden of a full SA structure.

Société par Actions Simplifiée (SAS)

The Société par Actions Simplifiée (SAS) Niger framework operates under the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, most recently revised in 2014. As a distinct legal entity, the SAS offers separate legal personality and limited liability, with shareholders exposed only to the extent of their capital contributions. Its hybrid character sits between the structural rigidity of the SA and the flexibility of a SARL, making it particularly suited to bespoke governance arrangements.

Shareholder agreements carry significant weight in an SAS, as the OHADA framework grants wide latitude to define voting rights, share transfer conditions, and management structure through the company statutes. This contractual flexibility is the defining feature distinguishing the SAS Niger setup from other corporate forms.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Share-based company with separate legal personality | Governed by OHADA Uniform Act 2014 |

| Members | Shareholders; minimum 1, no maximum | Single-shareholder SAS (SASU) is permitted |

| Management | President (mandatory); no board requirement | Additional managers may be appointed by statute |

| Local Presence | Registered office in Niger required | Physical address; no statutory agent requirement under OHADA |

| Share Capital | No statutory minimum under OHADA 2014 | Capital defined in statutes; must reflect actual activity |

| Privacy | Shareholder identity disclosed at registration | Beneficial ownership rules apply under FATF-aligned reforms |

Focus Points

- Taxation: Corporate income tax applies at the standard rate; VAT registration required for taxable turnover; withholding taxes apply to dividends, interest, and royalties paid to non-residents under domestic rules, subject to any applicable tax treaty.

- Annual Compliance: Annual financial statements must be filed; general meeting obligations apply as defined in company statutes.

- Treaty Access: Niger's tax treaty network is limited; treaty benefits depend on residency status and substance requirements.

- Conversion: An SAS may be converted to an SA or SARL subject to compliance with OHADA conversion procedures and shareholder approval.

- Restrictions: Shares in an SAS cannot be offered to the public; public fundraising requires conversion to an SA.

Closing

The SAS suits holding structures, joint ventures, and businesses requiring tailored governance terms not achievable under the SA or SARL framework. Its principal advantage is statutory flexibility; the primary limitation is that public capital raising is prohibited, restricting growth options for businesses requiring broad investor access.

Best suited for joint venture vehicles, investor-backed startups, or holding entities where custom shareholder arrangements and governance provisions are a priority.

Partnerships [Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA)]

Niger's partnership structures fall under the OHADA Uniform Act on Commercial Companies and Economic Interest Groups (AUSC), adopted in 1997 and revised in 2014. All three partnership forms — the Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), and Société en Commandite par Actions (SCA) — are governed by this supranational framework, which takes precedence over domestic law.

The primary keyword partnership structures Niger SNC SCS SCA refers to entities where liability exposure varies by form. The SNC confers unlimited joint and several liability on all partners. The SCS and SCA introduce a tiered liability model, separating general partners who bear unlimited liability from limited partners or shareholders whose exposure is capped at their capital contribution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société en Nom Collectif (SNC) / Société en Commandite Simple (SCS) / Société en Commandite par Actions (SCA) | All three are distinct legal entities under OHADA AUSC |

| Members | Partners (associés); SCS/SCA distinguish commandités (general) and commanditaires (limited) | SNC: min. 2 partners, no max; SCS: min. 1 general + 1 limited partner; SCA: min. 1 general + 3 shareholders |

| Liability | SNC: unlimited for all; SCS: unlimited for general, capped for limited; SCA: same as SCS | General partners in SCS/SCA remain personally exposed to business debts |

| Minimum Capital | No statutory minimum for SNC or SCS; SCA requires share capital divided into negotiable shares | SCA capital structure resembles an SA in its shareholder component |

| Local Presence | Registered office (siège social) required in Niger; registration with RCCM (Registre du Commerce et du Crédit Mobilier) mandatory | No requirement for a resident manager in SNC, though a gérant must be designated |

| Privacy | Partner names are publicly registered with the RCCM | No confidentiality mechanism exists for partner identity |

Focus Points

- Taxation: Partnerships are generally treated as fiscally transparent under Niger's tax framework, meaning profits are taxed at the partner level; VAT, withholding taxes on distributions, and applicable stamp duties follow standard OHADA-member rules.

- Annual Compliance: Annual financial statements must be filed; general partners in all three forms bear personal compliance obligations alongside the entity.

- Treaty Access: Niger has a limited double tax treaty network; partnership income attribution to foreign partners may not qualify for treaty relief depending on the counterparty jurisdiction's classification of the entity.

- Restrictions: General partners in an SNC cannot freely transfer their interests without unanimous partner consent, significantly limiting exit options.

- Conversion: An SNC or SCS may be converted to another OHADA-recognised form, subject to partner approval and RCCM re-registration.

Sub-Types

Société en Nom Collectif (SNC)

The SNC is a general partnership in which every partner bears unlimited, joint, and several liability. It suits closely held professional or family businesses where partners accept full personal exposure in exchange for operational simplicity.

Société en Commandite Simple (SCS)

The SCS separates active management (general partners) from passive investors (limited partners). Limited partners may not participate in management without forfeiting their liability protection under the AUSC.

Société en Commandite par Actions (SCA)

The SCA replaces the limited partner interest with transferable shares, making it structurally closer to an SA on the investor side. It is used when a business requires capital from multiple shareholders while preserving managerial control in the hands of one or more general partners.

Partnership forms are most commonly used for professional firms, family-controlled trading operations, or structures where one party supplies capital and another manages operations. The tiered liability model in the SCS and SCA offers structural flexibility, but unlimited personal liability for general partners remains a material constraint for any investor unwilling to accept that exposure.

SNC, SCS, and SCA structures suit closely held businesses or professional partnerships where the partners have an established relationship and are prepared to accept personal liability obligations under OHADA law.

Foreign Business Structures [Branch Office, Representative Office, Liaison Office]

Establishing a foreign company branch office Niger allows an overseas parent to operate directly without forming a separate local entity. Under the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, a branch has no distinct legal personality — the parent company remains fully liable for all obligations the branch incurs. Registration is handled through the Centre de Formalités des Entreprises (CFE) and requires filing the parent company's constitutive documents alongside a power of attorney for a designated representative.

A representative or liaison office operates under a more restricted mandate, limited to non-commercial activities such as market research, promotion, and coordination. Neither structure generates independent legal personality, and both derive their authority entirely from the parent entity.

Key Characteristics

| Requirement | Branch Office | Representative / Liaison Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Permitted Activities | Commercial and operational | Non-commercial only |

| Local Representative | Mandatory (resident manager) | Mandatory (designated contact) |

| Capital Requirement | No minimum, but parent financials required | None |

| Liability | Parent bears full liability | Parent bears full liability |

| Registration Body | CFE / RCCM (Commercial Registry) | CFE / RCCM |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at the standard rate; VAT and withholding tax obligations apply to transactions in the same manner as local entities.

- Economic substance: A resident manager with operational authority must be appointed and maintained.

- Annual compliance: Audited financial statements of the parent and branch accounts must be filed annually with the RCCM.

- Treaty access: Niger representative office registration does not typically confer tax treaty benefits; access depends on the parent's jurisdiction and treaty terms.

- Restrictions: A liaison office Niger foreign business structure cannot invoice clients, sign commercial contracts, or repatriate profits directly.

Sub-Types

Branch Office

A branch conducts full commercial operations under the parent's name and liability, making it suitable for foreign firms seeking active market participation without incorporating a standalone subsidiary.

Representative Office

Distinguished from a branch by its strictly non-revenue-generating mandate, a representative office is used for promotional activities, client liaison, and feasibility studies prior to full market entry.

Liaison Office

Functionally similar to a representative office, a liaison office serves as an internal coordination point between the parent and local partners, with no authority to engage in any form of trading activity.

Closing

Foreign firms typically use a branch for operational activities where a full subsidiary is premature, while representative and liaison offices suit pre-entry market assessment. The primary advantage of all three structures is speed of establishment relative to forming a new entity; the central drawback is that unlimited parental liability is unavoidable across all three forms.

These structures are best suited for foreign companies testing the Niger market or managing regional coordination before committing to a locally incorporated subsidiary.

Sole Proprietorship [Entreprise Individuelle, Auto-Entrepreneur]

Niger's sole proprietorship framework, which covers both the Entreprise Individuelle and the Auto-Entrepreneur status, operates under the OHADA Uniform Act on General Commercial Law and supplementary national provisions. The sole proprietorship Niger Entreprise Individuelle structure does not create a legal entity separate from its owner — the proprietor and the business are legally one, meaning personal assets remain exposed to business liabilities.

Registration for both forms is handled through the Centre de Formalités des Entreprises (CFE), which coordinates filings with the Registre du Commerce et du Crédit Mobilier (RCCM) under the OHADA framework.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Unincorporated) | No separate legal personality from the owner |

| Owner Designation | Proprietor / Exploitant individuel | Single natural person only |

| Membership | 1 proprietor; no maximum or minimum beyond sole ownership | Cannot admit partners or shareholders |

| Local Presence | Registered business address in Niger required | No separate registered agent requirement |

| Capital | No statutory minimum capital | Proportional to declared activity |

| Liability | Unlimited personal liability | Business debts enforceable against personal assets |

Focus Points

- Taxation: Subject to the Impôt sur le Bénéfice Industriel et Commercial (BIC) or a simplified flat-rate regime for micro-entrepreneurs; VAT registration required once turnover thresholds are exceeded under the Code Général des Impôts.

- Annual Compliance: Annual declaration of turnover to the tax authority (Direction Générale des Impôts); simplified bookkeeping obligations apply under the OHADA Acte Uniforme.

- Treaty Access: No access to double tax treaties, which apply only to legal entities with tax residence in the corporate sense.

- Conversion: Can be converted into a SARL or other incorporated form by transferring assets and re-registering; no automatic continuity of legal rights.

- Restrictions: Foreign nationals face restrictions on operating as sole proprietors and may require additional authorisations under Niger's investment and residency regulations.

Sub-Types

Entreprise Individuelle

The standard individual business form registered with the RCCM, used for commercial, artisanal, or industrial activities. It carries full accounting obligations relative to its turnover bracket under OHADA rules.

Auto-Entrepreneur

A simplified registration status introduced to formalise micro-scale activities, with reduced administrative requirements and a forfait (flat-rate) tax scheme. It is designed for low-turnover operators and imposes a turnover ceiling beyond which the operator must transition to the full Entreprise Individuelle regime.

Closing

Both forms suit individual operators running small-scale commercial or service activities who prioritise low setup costs over liability protection. The primary advantage is minimal administrative burden at inception; the critical limitation is unlimited personal liability, which makes these structures unsuitable for any activity carrying significant financial or legal risk.

Local individual traders, artisans, and micro-entrepreneurs operating below Niger's VAT and turnover thresholds who do not require liability separation.

How to Choose the Right Entity Type in Niger

Selecting how to choose a business entity in Niger requires more than comparing registration fees — the structural decision has direct legal, tax, and operational consequences that are difficult and costly to reverse.

Why Your Entity Choice Matters

An ill-matched entity structure creates concrete problems. Consider the following outcomes:

- Registering a branch or representative office when your business model requires contracting directly with local clients can result in regulatory non-compliance under the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, exposing the entity to administrative penalties or forced deregistration.

- Choosing a structure that falls outside Niger's tax treaty eligibility criteria means you cannot claim reduced withholding tax rates under applicable bilateral agreements, increasing the effective tax burden on cross-border payments.

- Forming a multi-shareholder SA when a sole-director SARL would suffice imposes mandatory auditor appointments and annual general meeting obligations, adding recurring compliance costs with no operational benefit.

- Selecting an entity without legal capacity to employ staff locally when your activity requires a physical presence triggers substance-related reporting failures with the Direction Générale des Impôts.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors such as banking or telecoms each map to distinct permissible structures under Niger's OHADA-aligned company law — view the applicable OHADA Uniform Act.

- Ownership and Management: A sole founder who needs operational flexibility points toward the SARL, while multiple institutional investors requiring formal governance lean toward the SA.

- Tax Objectives: Your eligibility for specific regimes under the Code Général des Impôts — including the synthetic tax regime for small businesses — depends on the entity type and declared turnover band.

- Privacy Requirements: Director and shareholder details are recorded in the Registre du Commerce et du Crédit Mobilier (RCCM), which is a public register; nominee arrangements may be needed if confidentiality is a priority.

- Exit Strategy: Not all entity types permit redomiciliation or conversion without dissolution; confirm restructuring options before formation if your long-term plans include a jurisdictional change.

Compliance Services for Companies in Niger

Ongoing compliance support for Niger-registered entities, including annual filings, RCCM maintenance, and regulatory reporting.

Conclusion

Incorporating a company in Niger guide decisions ultimately rest on the structure of your operations, your liability tolerance, and whether you require local or foreign participation. The SARL suits small to mid-sized ventures with a defined shareholder group, while the SA accommodates larger enterprises requiring capital market access. An SAS offers contractual flexibility that neither the SA nor SARL provides by default. Partnerships carry unlimited liability and serve closely held businesses where personal accountability is accepted. Branch and representative offices allow foreign entities to establish a presence without forming a separate legal entity.

The SARL remains the most commonly registered structure across Niger's private sector. Governing law derives from the OHADA Uniform Act on Commercial Companies, which continues to evolve through OHADA institutional review. As treaty networks and regional integration deepen, the regulatory framework shaping business formation here will continue to shift. Expanship's team tracks these developments as they occur.

How Expanship Can Assist You

Expanship's company incorporation services in Niger cover the full formation process, from selecting the right entity structure — whether an SA, SARL, or SAS — through registration with the Centre de Formalités des Entreprises (CFE) and the RCCM. Our team works directly with local regulatory processes so your business is properly constituted from day one.

From document preparation to ongoing compliance, our service scope includes:

- Notarization and legalization of incorporation documents

- Registered agent and registered office provision in Niger

- Filing with the RCCM and liaison with the CFE

- Post-incorporation compliance management, including annual obligations

- Banking introduction assistance for local account setup

- Ongoing registered address maintenance

Ready to establish your entity in Niger? Contact Expanship Niger to discuss your requirements.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is the most frequently registered business form. Its lower minimum share capital requirement and simplified governance structure make it accessible to small and medium-sized enterprises, both domestic and foreign-owned.

Foreign nationals may form a SARL, SA, or SAS under the OHADA Uniform Act on Commercial Companies. No nationality restriction bars foreign ownership, though certain regulated sectors may require local partnership or prior authorization from relevant Nigerien authorities.

A SARL may be formed by a single associé under OHADA rules, making it the only corporate form available to a sole founder. An SA requires a minimum of one shareholder but multiple directors in some configurations, while partnerships such as the SNC require at least two partners by definition.

The SA, SARL, and SAS each hold distinct legal personality separate from their members. General partnerships (SNC) also acquire legal personality upon registration in the RCCM, though partners retain joint and unlimited liability for the firm's obligations.

Conversion between entity types is permitted under the OHADA Uniform Act, most commonly from SARL to SA when a growing business exceeds shareholder or capital thresholds. The process requires a shareholders' resolution, updated articles, and re-registration with the RCCM.

No OHADA-governed entity in Niger offers the level of confidentiality associated with offshore structures. Beneficial ownership, directors, and share capital are filed with the RCCM and are generally accessible, though the SAS offers somewhat greater flexibility in structuring internal governance without prescriptive statutory disclosure of operational rules.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.