Key Takeaways

- Namibia's company registration and compliance framework is administered by the Business and Intellectual Property Authority (BIPA) under the Companies Act 28 of 2004 and the Close Corporations Act 26 of 1988.

- Close corporations are no longer open for new registrations but remain legally valid operating structures for businesses that incorporated under the Close Corporations Act 26 of 1988.

- Foreign businesses entering Namibia can choose between an external company, which permits direct trading, and a representative office, which restricts activity to liaison functions only.

- Among all available legal forms, the private company is the most commonly registered structure for both resident and non-resident investors operating in Namibia.

Introduction to Entity Types in Namibia

Namibia is an independent republic located in southern Africa, bordered by South Africa, Botswana, Zambia, and Angola, with a coastline along the Atlantic Ocean. Company registration and ongoing compliance fall under the authority of the Business and Intellectual Property Authority (BIPA), which administers the Companies Act 28 of 2004 and the Close Corporations Act 26 of 1988. The country operates a source-based tax system, meaning only income earned within its borders is generally subject to local taxation.

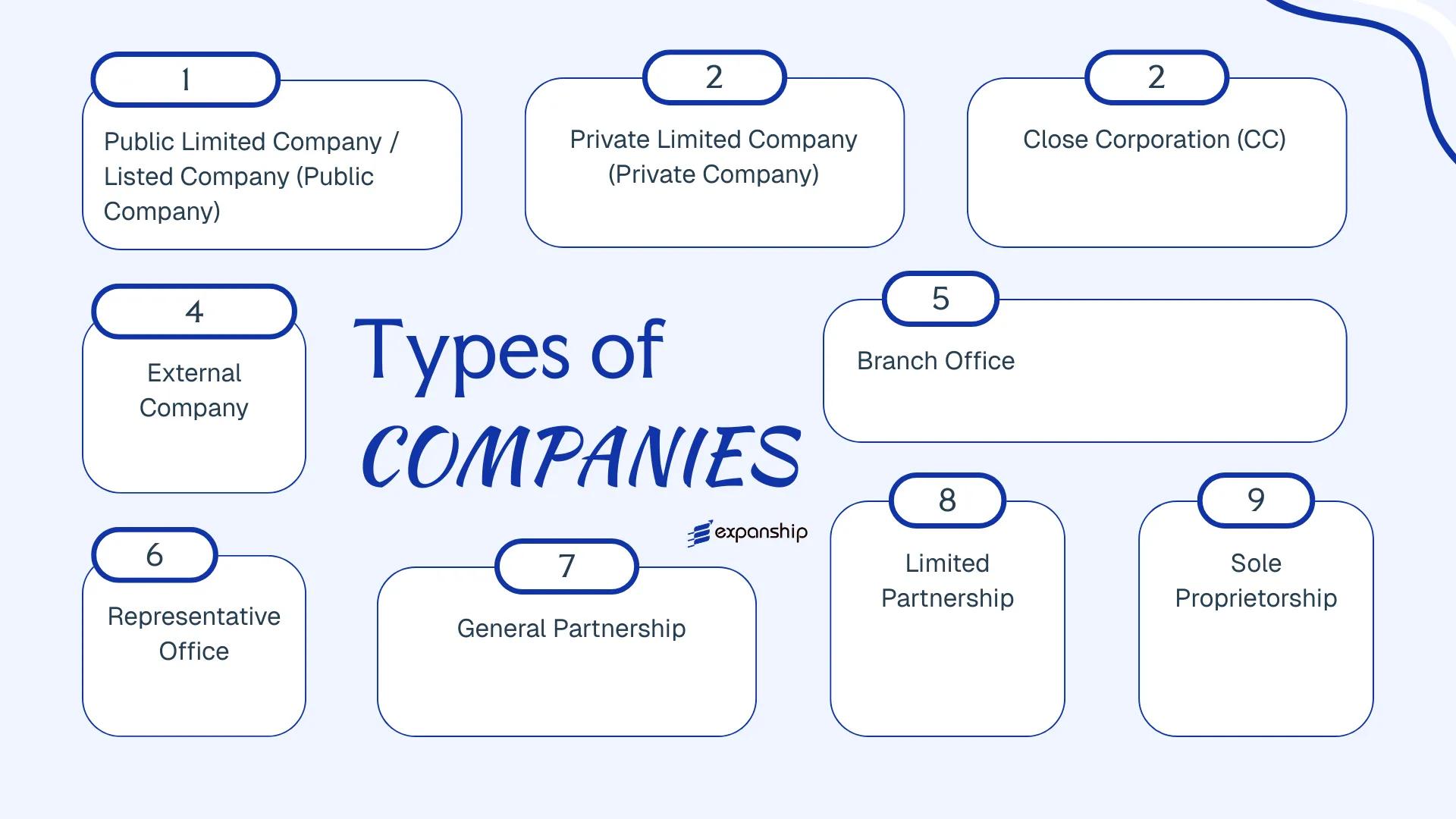

Understanding the types of business entities in Namibia is a prerequisite for anyone structuring a commercial presence there. The available legal forms include the private company, public company, close corporation, external company, branch office, representative office, general partnership, limited partnership, and sole proprietorship.

Each structure carries distinct implications for liability, governance, ownership, and regulatory obligations. This article examines each entity type in detail — covering formation requirements, capital rules, and suitability for different operational purposes.

An Overview of Business Structures in Namibia

Namibia's company law framework recognises several distinct entity types, each governed primarily by the Companies Act 28 of 2004 and, for older formations, its predecessor legislation. Close Corporations, though no longer registrable for new applicants following legislative reform, remain operational under the Close Corporations Act 26 of 1988. Each structure carries different implications for liability, ownership, and permitted commercial activity.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company | Incorporated company | Limited to shares | Taxed | Yes | 7 shareholders | BIPA | Companies Act 28 of 2004 |

| Private Company | Incorporated company | Limited to shares | Taxed | Yes | 1 shareholder | BIPA | Companies Act 28 of 2004 |

| Close Corporation | Incorporated entity | Limited to interest | Taxed | Yes | 1–10 members | BIPA | Close Corporations Act 26 of 1988 |

| External Company | Registered foreign entity | Per parent company | Taxed | Yes | N/A | BIPA | Companies Act 28 of 2004 |

| Branch Office | Extension of foreign entity | Unlimited (parent) | Taxed | Yes | N/A | BIPA | Companies Act 28 of 2004 |

| Representative Office | Non-trading presence | Per parent company | Generally exempt | No | N/A | BIPA | Companies Act 28 of 2004 |

| General Partnership | Unincorporated | Unlimited | Taxed | Yes | 2+ partners | N/A | Common law |

| Limited Partnership | Unincorporated | Mixed | Taxed | Yes | 1 GP + 1 LP | N/A | Common law |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed (personal) | Yes | 1 owner | N/A | N/A |

Each of these structures is examined in full in the sections below.

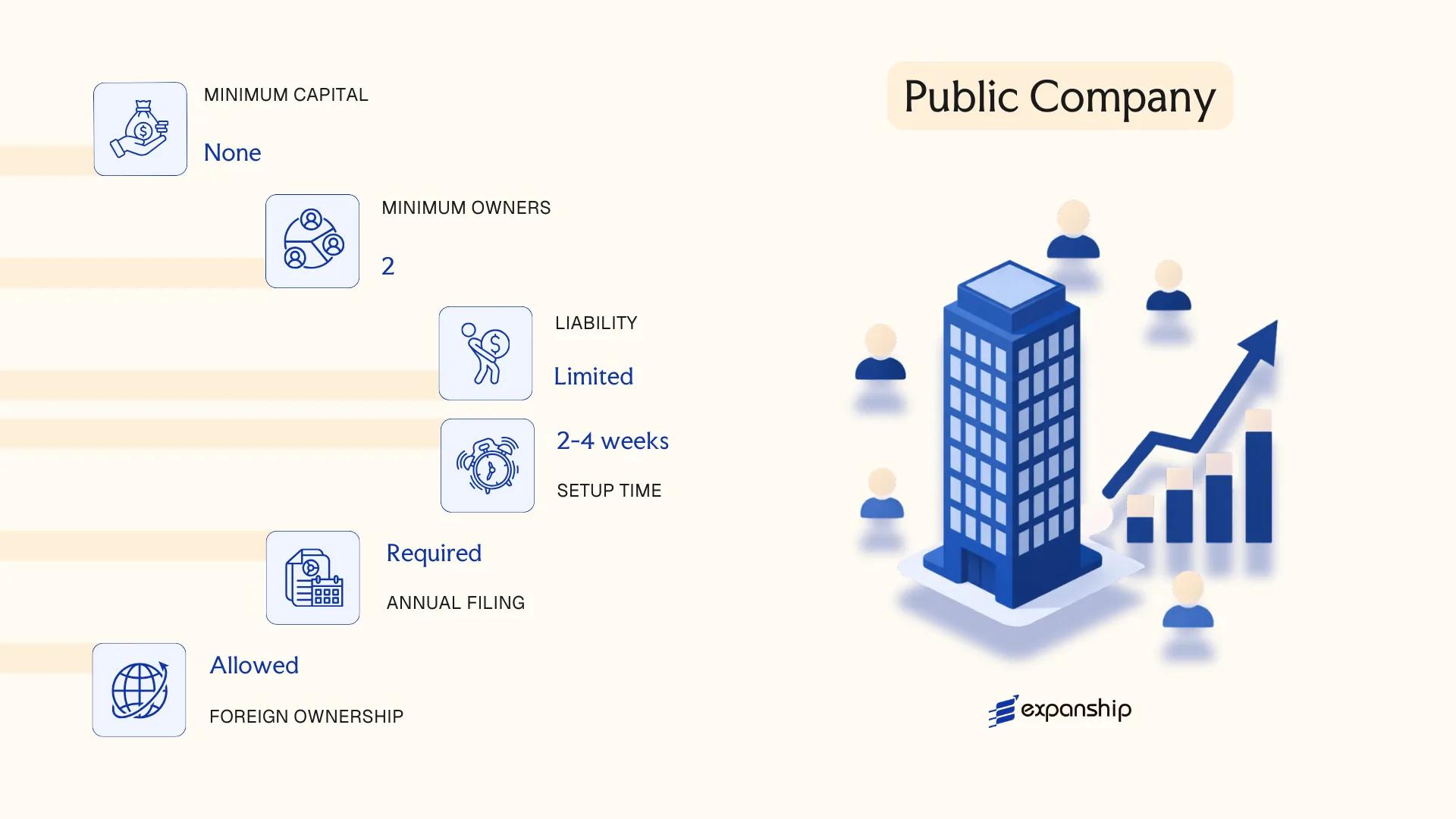

Public Company (Public Limited Company / Listed Company)

Under the Namibian Companies Act 28 of 2004, a public company is a distinct legal entity with separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name. Shareholders' liability is limited to the amount unpaid on their shares.

Namibia public limited company registration suits businesses seeking to raise capital from the public or pursue a listing on the Namibian Stock Exchange (NSX), which is regulated by the Namibia Financial Institutions Supervisory Authority (NAMFISA).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Company (Ltd) | Incorporated under the Companies Act 28 of 2004 |

| Governance | Board of Directors + Shareholders | Minimum 2 directors; no maximum for shareholders |

| Members | Minimum 1 shareholder; no maximum | Shares may be offered to the general public |

| Local Presence | Registered office in Namibia | A company secretary is required |

| Share Capital | No statutory minimum; denominated in NAD | Shares are freely transferable |

| Privacy | Accounts and annual returns filed publicly | Financial statements accessible via BIPA |

Focus Points

- Taxation: Subject to corporate income tax at 32%, standard VAT at 15%, and withholding taxes on dividends, interest, and royalties paid to non-residents.

- Annual Compliance: Mandatory audited financial statements, annual general meetings, and annual returns filed with the Business and Intellectual Property Authority (BIPA).

- NSX Listing: A listing on the NSX requires compliance with NSX Listing Requirements and ongoing disclosure obligations under NAMFISA oversight.

- Conversion: A public company may convert to a private company by special resolution, subject to BIPA approval and satisfaction of the Companies Act conversion requirements.

Closing

A public company suits large-scale commercial operations, businesses seeking institutional investment, or firms planning a public share offering. The ability to raise capital from an unlimited number of shareholders is a clear structural advantage; however, the mandatory public disclosure of financial statements and the cost of statutory audits make this structure operationally heavier than most other entity types.

Best suited for established businesses targeting capital market access or institutional investors in Namibia.

Company Incorporation in Namibia

Incorporate a public or private company in Namibia with end-to-end support from entity selection through registration.

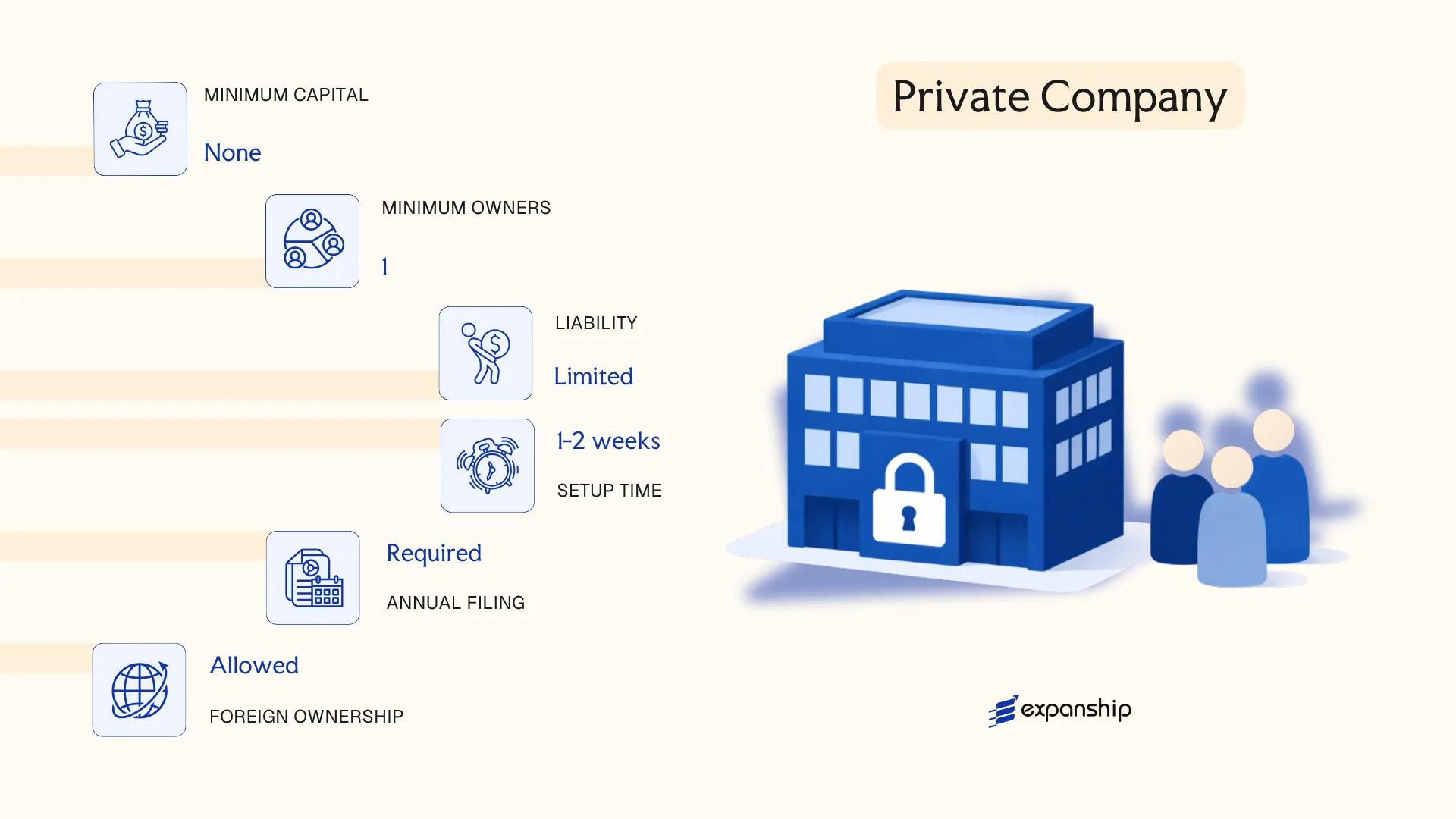

Private Company (Private Limited Company / Close Corporation)

Two distinct entity forms serve the private business segment under Namibian law. The private company is governed by the Companies Act 28 of 2004, while the close corporation (CC) falls under the Close Corporations Act 26 of 1988. Both carry separate legal personality and limit member liability to their contributed capital, though the CC was designed as a lighter-weight alternative for smaller, owner-managed operations.

Namibia private company formation and CC registration are administered by the Business and Intellectual Property Authority (BIPA). A private company restricts share transfers and prohibits public share offers, whereas a CC issues membership interests rather than shares, with internal governance set out in a founding statement rather than articles of association.

Key Characteristics

| Requirement | Private Company (Pty) Ltd | Close Corporation (CC) |

|---|---|---|

| Members / Holders | Shareholders & Directors | Members (no director/shareholder distinction) |

| Member Count | Min. 1, Max. 50 shareholders; Min. 1 director | Min. 1, Max. 10 natural persons only |

| Local Presence | Registered office in Namibia required | Registered office in Namibia required |

| Capital | NAD; no statutory minimum share capital | NAD; member contributions expressed as percentage interests totalling 100% |

| Privacy | Beneficial ownership disclosure required at BIPA | Members listed in founding statement filed at BIPA |

| Audit | Required if above statutory thresholds | Accounting officer (not full audit) generally sufficient for smaller CCs |

Focus Points

- Taxation: Both entity types are subject to corporate income tax at 32% (standard rate); VAT registration is mandatory once taxable turnover exceeds NAD 500,000; withholding tax applies to dividends paid to non-residents at 10%.

- Annual Compliance: Annual returns must be filed with BIPA; financial statements must meet requirements set under the Companies Act or Close Corporations Act respectively.

- Conversion: A CC may be converted to a private company under procedures outlined in the Companies Act 28 of 2004; the reverse is not provided for.

- Restrictions: CC membership is restricted to natural persons; juristic entities such as other companies cannot hold a membership interest directly.

- Treaty Access: Both entity types are resident for tax purposes and may access Namibia's double tax agreement network, subject to beneficial ownership conditions.

Sub-Types

Registered Close Corporation with Accounting Officer

Smaller CCs that fall below audit thresholds appoint an accounting officer rather than a registered auditor. This reduces compliance cost and is the predominant structure used by owner-operated businesses with turnover beneath the prescribed threshold.

Recommendations

A private limited company suits trading businesses, subsidiaries of foreign groups, and any operation anticipating future equity investment, while a CC remains practical for small professional practices or family-run businesses with no more than ten individual members. The principal limitation of the CC is its cap on membership and the exclusion of corporate members, which makes it unsuitable for joint ventures involving corporate shareholders.

A Namibian CC suits small owner-managed businesses with up to 10 individual members; a private company is preferable for any structure requiring corporate shareholders or scalable equity arrangements.

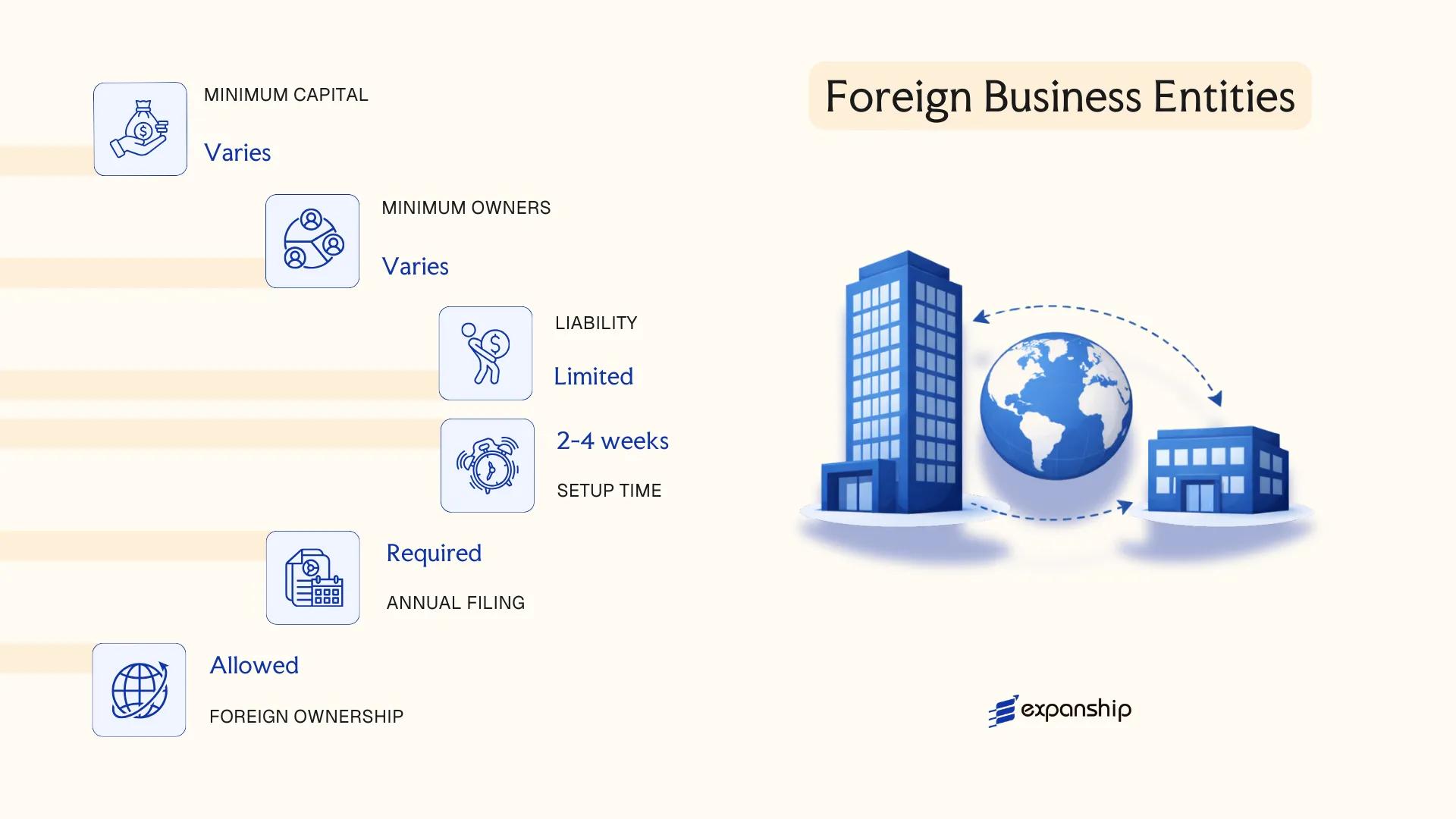

Foreign Business Entities in Namibia [External Company, Branch Office, Representative Office]

To register a foreign company in Namibia, the governing legislation is the Companies Act 28 of 2004, which classifies any overseas entity conducting business in the country as an external company. Registration is administered by the Business and Intellectual Property Authority (BIPA). An external company does not form a separate legal entity distinct from its parent — it remains an extension of the foreign firm, meaning the parent retains full legal liability for the branch's obligations.

Namibia external company registration requires filing with BIPA within 21 days of establishing a place of business. Required documents typically include certified copies of the foreign entity's constitutional documents, a list of directors, and the appointment of a local registered representative.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | External company (branch of foreign entity) | No separate legal personality from parent |

| Representation | Locally appointed representative | Must be ordinarily resident in Namibia |

| Local Presence | Registered office address required | Must maintain a physical place of business |

| Capital | No minimum capital requirement | Parent company's capital structure applies |

| Liability | Unlimited liability rests with parent | Parent is fully exposed to branch obligations |

| Privacy | Documents filed with BIPA are publicly accessible | Director details and constitutional docs on record |

Focus Points

- Taxation: Subject to corporate income tax at 32% on Namibian-sourced income; VAT registration required if turnover exceeds NAD 500,000; withholding taxes apply on dividends, interest, and royalties remitted to the foreign parent.

- Annual Compliance: Annual returns must be filed with BIPA; financial statements may be required depending on activity level.

- Treaty Access: Tax treaty access depends on whether the parent entity qualifies under applicable double taxation agreements Namibia has concluded.

- Restrictions: External companies cannot hold shares in Namibian entities in certain regulated sectors without additional approvals.

Sub-Types

Branch Office

A branch office is the standard operational form of an external company, registered to conduct active trading or service delivery. It is the most commonly used structure for foreign firms with ongoing commercial activity.

Representative Office

A representative office is permitted for liaison and promotional activities only — it cannot generate income or enter into contracts on behalf of the parent. This structure suits firms conducting market research or managing client relationships prior to full establishment.

An external company structure is commonly used by foreign businesses entering the market for trading, construction projects, or professional services, with the primary advantage being a relatively straightforward setup process through BIPA. The key limitation is unlimited parental liability, which exposes the foreign parent to all obligations incurred locally.

Foreign companies seeking a temporary or project-based operational presence without committing to a separately incorporated local entity.

Partnerships in Namibia [General Partnership, Limited Partnership]

Partnership registration in Namibia is not governed by a single dedicated partnership statute. Instead, general partnerships are regulated primarily through common law principles inherited from Roman-Dutch law, supplemented by contractual arrangements between partners. Partnerships do not possess separate legal personality, meaning partners are personally liable for the firm's obligations.

A partnership agreement is the foundational document. While no prescribed form is legally mandated, a written agreement is strongly recommended to define profit-sharing ratios, capital contributions, management responsibilities, and dissolution terms.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (unincorporated) | No separate legal personality; partners act in their own names |

| Members | Partners; minimum 2, maximum 20 | Exceeding 20 partners generally requires incorporation |

| Liability | Unlimited (General); Limited for limited partners | Limited partners may not participate in management |

| Local Presence | No statutory registered agent requirement | A physical address for correspondence is advisable |

| Capital | NAD; no statutory minimum | Defined by partnership agreement |

| Privacy | Partnership agreements are not publicly registered | No public disclosure requirement under current rules |

Focus Points

- Taxation: Partnerships are taxed on a pass-through basis; each partner declares their share of profits under personal or corporate income tax at applicable Namibian rates; VAT registration applies if turnover thresholds are met.

- Annual Compliance: No statutory annual return filing exists for partnerships, though tax obligations with the Namibia Revenue Agency (NamRA) apply annually.

- Conversion: A partnership cannot convert directly into a company; a new entity must be incorporated separately.

- Treaty Access: Partners may individually access Namibia's tax treaty network depending on their own residency status.

Sub-Types

General Partnership

All partners carry unlimited joint and several liability for the firm's debts. Management authority is shared equally unless the partnership agreement specifies otherwise.

Limited Partnership

At least one general partner retains unlimited liability, while limited partners contribute capital and are liable only up to their contributed amount. A limited partner who participates in management risks losing limited liability status.

Closing Paragraph and Recommendations

Partnerships suit professional service providers, joint ventures, and small trading operations where formality is a lower priority than operational flexibility. The pass-through tax treatment is a practical advantage, though the absence of limited liability for general partners represents a significant exposure for any business carrying substantial financial risk.

Partnerships are best suited for small professional practices or two-party joint ventures where the partners know each other well and prefer a minimal compliance structure.

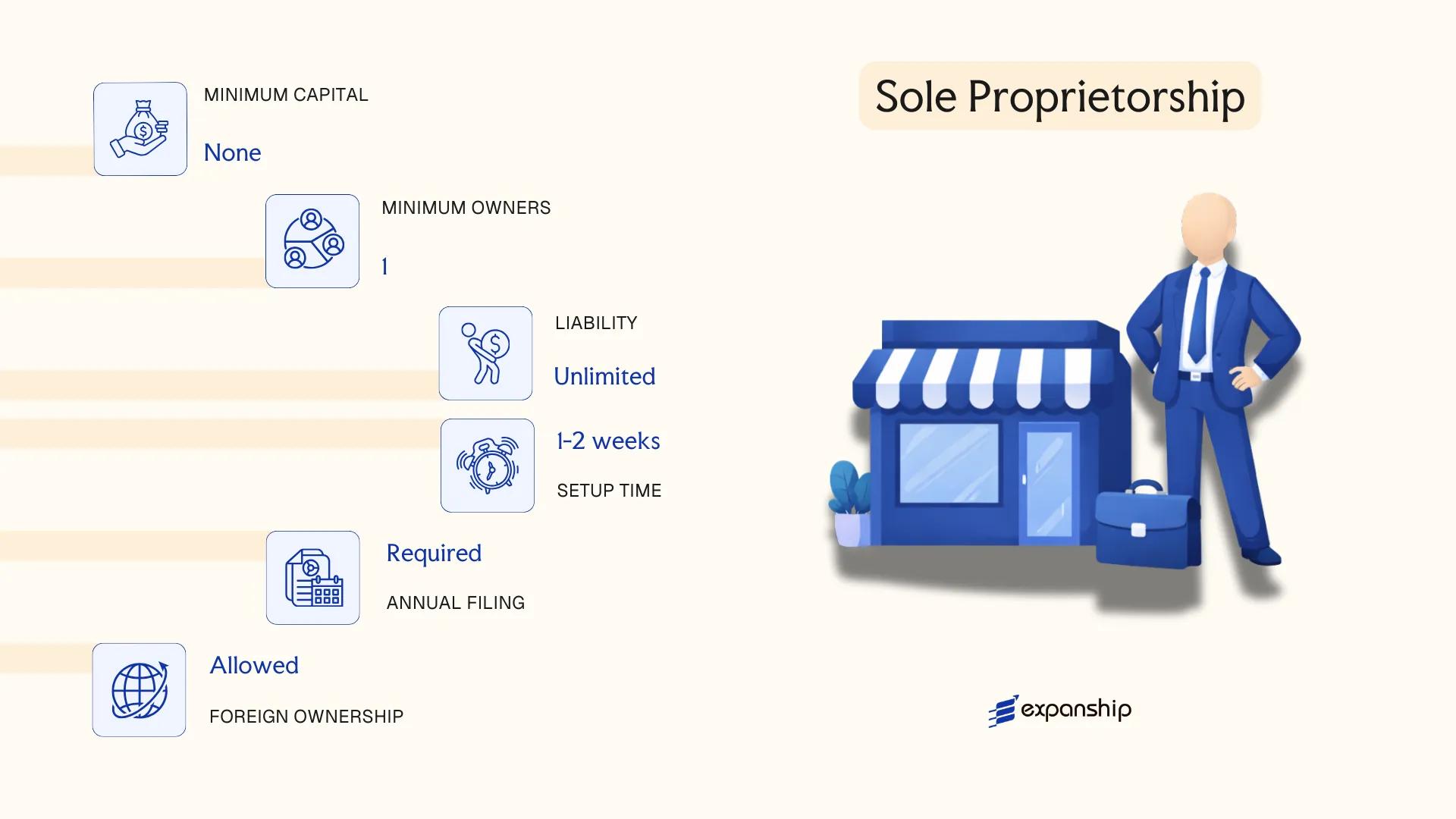

Sole Proprietorship

A sole proprietorship in Namibia is the simplest form of business operation available to individuals. Unlike companies registered under the Companies Act 28 of 2004, this structure carries no separate legal personality — the owner and the business are legally the same person, meaning personal assets are exposed to business liabilities without limitation.

Registration is handled through the Business and Intellectual Property Authority (BIPA) under the Business Name Act 16 of 1973, which requires any person trading under a name other than their own to register that business name. The process is straightforward and relatively low-cost, making it accessible to self-employed individuals and micro-traders operating across the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Members | Sole proprietor (1 individual) | Cannot have co-owners; single natural person only |

| Liability | Unlimited personal liability | Personal assets are fully exposed to business debts |

| Local Presence | Business name registered with BIPA | Physical address required for registration |

| Capital | No minimum capital requirement | Funded entirely by the proprietor |

| Privacy | Owner's name linked to business name on public register | Limited privacy protection |

Focus Points

- Taxation: Income is taxed as personal income under the Income Tax Act; standard personal income tax rates apply, with VAT registration required once annual turnover exceeds the prescribed threshold (currently NAD 500,000).

- Annual Compliance: No annual returns are filed with BIPA, but tax filings with the Namibia Revenue Agency (NamRA) are mandatory.

- Economic Substance: No formal economic substance obligations apply, as this structure is not subject to the Companies Act.

- Conversion: A sole proprietorship can be converted to a private company or close corporation by incorporating a new entity and transferring business assets; there is no automatic conversion mechanism.

- Restrictions: Foreign nationals face restrictions on trading as sole proprietors without the appropriate work and business permits under the Immigration Control Act.

Closing Paragraph

A sole proprietorship suits micro-enterprises, freelancers, and individuals testing a business concept with minimal regulatory overhead. The primary advantage is low setup and compliance cost; the significant drawback is unlimited personal liability, which poses meaningful financial risk as the business grows.

Local individual entrepreneurs operating small-scale or informal businesses who require a registered trading name but are not yet ready for a formal corporate structure.

How to Choose the Right Entity Type in Namibia

Choosing the right business structure in Namibia shapes everything from your tax exposure to your legal obligations under the Companies Act 28 of 2004 and its successor legislation. Structure determines compliance cost, liability, and operational capacity from day one.

Why Your Entity Choice Matters

Getting this wrong carries concrete consequences:

- Registering an external company but then trading domestically as though locally incorporated places your business in breach of the Companies Act, exposing it to deregistration by the Business and Intellectual Property Authority (BIPA).

- Selecting an entity without the capacity to meet substance requirements can trigger reporting failures under Namibia's transfer pricing and anti-avoidance provisions.

- Forming a company when a trust or foundation would serve asset-holding needs better locks your business into annual shareholder meetings, statutory filings, and directorship obligations that trusts do not carry.

- Choosing a structure that mandates audited financial statements for a single-director consultancy adds recurring professional fees that a sole proprietorship or close corporation would avoid.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or insurance each require a distinct structure under Namibian law.

- Ownership Structure: A single founder may prefer a close corporation or sole proprietorship, while multi-party ventures with investor obligations call for a private or public company.

- Tax Position: Your need for full tax residency, access to Namibia's double taxation agreements, or exemption determines which entity qualifies.

- Public Disclosure Tolerance: Directors and members of companies registered with BIPA appear on public records; nominee arrangements affect this differently.

- Substance Capacity: If you cannot maintain local staff or decision-making in the jurisdiction, your chosen structure must not trigger substance requirements your business cannot meet.

- Exit and Conversion: Not all Namibian entity types permit redomiciliation or conversion, so your long-term exit path should inform your formation decision.

Corporate Compliance Services in Namibia

Maintain good standing with BIPA and meet your ongoing statutory obligations under Namibian company law.

Conclusion

Namibia company incorporation summary begins with understanding that each structure registered under the Companies Act 28 of 2004 serves a distinct commercial purpose. Private companies suit closely held businesses where ownership transfer needs to remain restricted. Public companies are reserved for firms seeking access to capital markets through the Namibia Stock Exchange. Close corporations, though closed to new registrations, remain valid for existing small operators. Foreign businesses entering through an external company registration gain a direct trading presence, while a representative office limits activity to liaison functions only. General and limited partnerships, along with sole proprietorships, address lower-formality operating needs.

Among these, the private company remains the most commonly registered structure for both resident and non-resident investors. Regulated by the Business and Intellectual Property Authority, the registration environment has shown gradual movement toward procedural digitisation. For businesses evaluating their structure before filing, professional guidance on matching entity type to operational scope reduces downstream compliance exposure.

How Expanship Can Assist You

Expanship company registration Namibia services are built around the specific entity types examined in this blog — from private companies and close corporations governed under the Companies Act 28 of 2004 to external companies and branch offices registered with the Business and Intellectual Property Authority (BIPA). Your chosen structure determines your compliance obligations, and we work with those specifics directly.

We handle the full process of getting your business established and maintained in Namibia:

- Document preparation, notarization, and apostille legalization

- Registered office and resident agent provision

- Filing and liaison with BIPA on your behalf

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance with Namibian financial institutions

Every engagement is handled by specialists familiar with Namibian regulatory requirements, not generalists working from templates.

Ready to move forward? Contact Expanship Namibia to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The private company (Proprietary Limited, or (Pty) Ltd) is the most frequently incorporated entity, governed by the Companies Act 28 of 2004. Its combination of limited liability, a single-member minimum, and straightforward BIPA registration makes it the default choice for most commercial ventures.

An external company is a foreign-incorporated entity registered under Section 322 of the Companies Act to operate locally, while a private company is a newly formed Namibian legal person. The private company bears full domestic tax residency and compliance obligations, whereas an external company's tax treatment depends partly on its country of incorporation and any applicable double taxation agreement.

A close corporation registered under the Close Corporations Act 26 of 1988 discloses member interests rather than detailed shareholder registers in the same format as companies. Nominee arrangements are legally permissible, though beneficial ownership disclosure obligations have expanded under Namibia's financial intelligence framework.

A sole proprietorship and a single-member close corporation can each be established by one individual. Partnerships, by contrast, require a minimum of two partners, and public companies require at least three directors under the Companies Act.

Foreign individuals and corporate entities may register a private company, close corporation, or external company. There are no nationality restrictions on directorship or membership for these structures, though certain regulated industries require additional ministerial consent before a foreign-owned entity may commence operations.

The Companies Act allows for the conversion of a close corporation to a private company through a formal re-registration process administered via BIPA. Conversion in the reverse direction is not standard procedure, and restructuring from a branch to a locally incorporated entity requires a fresh registration rather than a continuation filing.

Private companies, public companies, and close corporations each hold separate legal personality distinct from their owners. Sole proprietorships and general partnerships do not — the owner or partners remain personally liable for all business obligations without a liability shield.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.