Key Takeaways

- Foreign investors operating in Namibia face a corporate tax rate that imposes a heavier burden on non-manufacturing entities, reducing after-tax returns compared to jurisdictions with more competitive general business tax regimes.

- Under the Companies Act 28 of 2004 and the oversight of the Business and Intellectual Property Authority, registration delays can extend the timeline before a foreign-owned entity is legally permitted to commence operations in Namibia.

- Bank of Namibia's foreign exchange controls restrict the cross-border movement of capital, creating compliance obligations that add cost and administrative friction to routine treasury and repatriation activities.

- Namibia's shallow domestic capital markets and limited access to local financing mean that businesses incorporated there often cannot source growth capital within the jurisdiction and must rely on offshore funding arrangements instead.

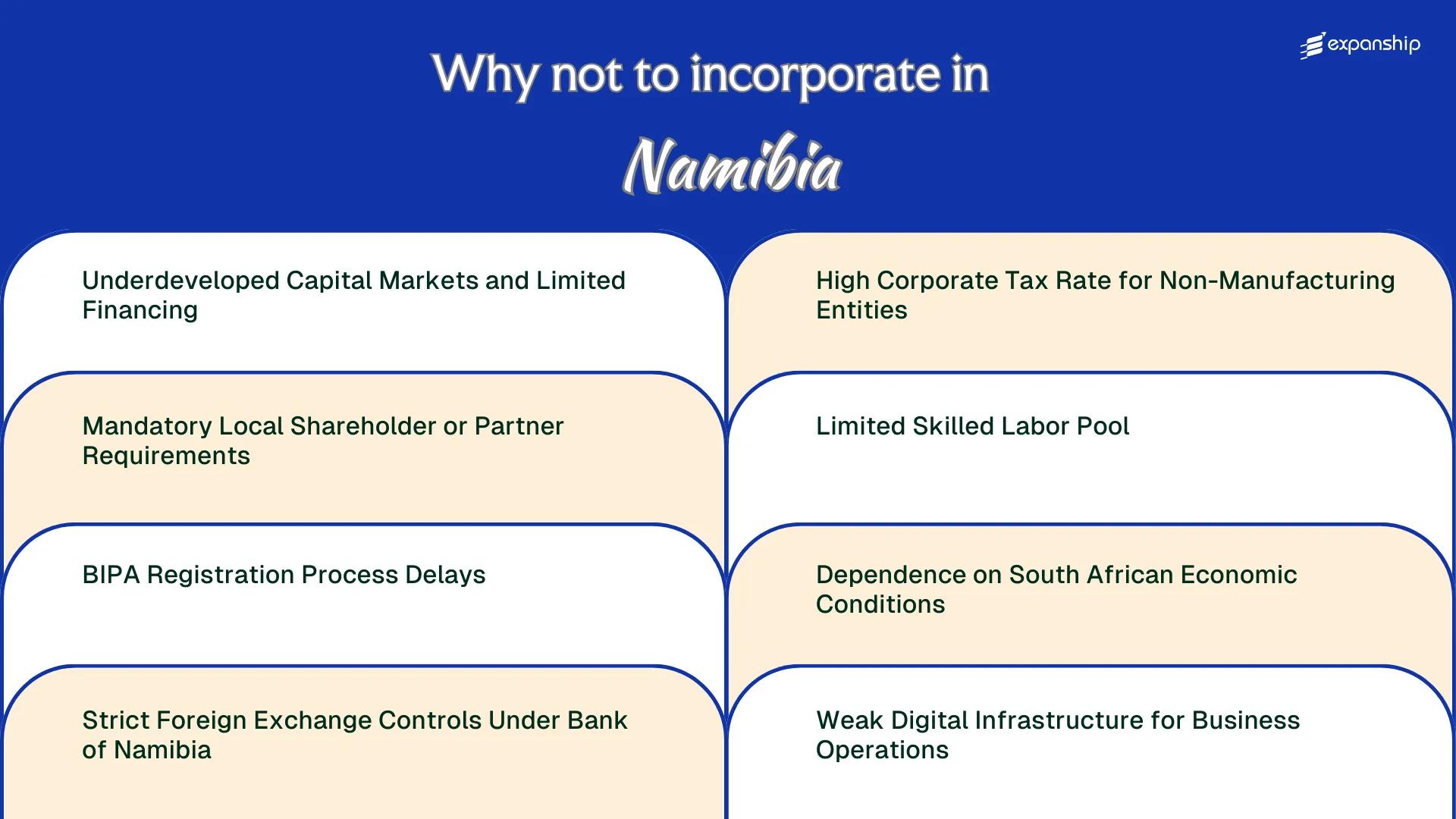

Namibia operates under an evolving regulatory framework, shaped in part by the Companies Act and a growing body of investment and exchange control legislation that continues to be refined. The disadvantages of incorporating in Namibia span several distinct categories, from financing constraints and ownership restrictions to labor market limitations and foreign exchange controls.

Not every disadvantage applies equally across all sectors. A manufacturing firm registered under an Export Processing Zone concession faces a different compliance burden than a financial services entity or a foreign-owned holding company.

This article is most relevant to foreign investors and business owners seeking to establish a private company, branch, or joint venture in Namibia, particularly those without prior operating experience in Southern African regulatory environments. The cons of registering a company here often surface only once incorporation is underway, making advance awareness material to your planning.

Underdeveloped Capital Markets and Limited Financing

Raising capital through equity or debt markets is significantly harder in Namibia than in more developed financial centers, and this structural gap directly affects how foreign-owned entities can fund growth.

Shallow Equity Markets Limit External Funding Options

The Namibia Stock Exchange (NSX) lists a limited number of domestic companies, and most of its market capitalization is attributed to dual-listed South African firms rather than locally incorporated entities. For a foreign business seeking to raise equity capital through a public listing or attract institutional investors domestically, the pool of active participants is too shallow to generate meaningful liquidity.

Private capital markets carry the same constraint. Venture capital and private equity activity within the country remains limited, meaning early-stage or growth-phase businesses cannot realistically rely on local private funding rounds.

Debt Financing Conditions Create Additional Pressure

Commercial lending from local banks typically requires substantial collateral, and interest rates for business loans have historically tracked above those available in South Africa or the broader OECD. Foreign-incorporated subsidiaries without established local credit histories face stricter lending terms, which increases your cost of capital from the outset.

If your business model depends on sequential funding rounds or debt refinancing, the limited depth of both public and private capital markets means you will likely need to source financing externally, adding currency and transfer risk.

Mandatory Local Shareholder or Partner Requirements

Namibia local shareholder requirements restrictions do not apply universally across all sectors, but in several regulated industries, foreign ownership is capped or conditioned on local equity participation. The Namibia Investment Promotion Act 9 of 2016 governs the general framework for foreign investment, yet sector-specific legislation imposes additional ownership thresholds that can materially limit how your business is structured.

Certain sectors, including fishing, land ownership, and some areas of retail trade, require meaningful Namibian citizen or resident participation in the ownership structure. This forces foreign investors to identify, vet, and legally bind a local partner before operations can begin.

That process carries real costs:

- Finding a compliant local shareholder introduces due diligence expenses that would not exist in a fully open investment regime

- Minority foreign ownership positions reduce your control over dividend policy and strategic decisions

- Local partner disputes can trigger shareholder deadlock, with resolution subject to Namibian courts and timelines

- Equity dilution directly reduces your return on invested capital without a corresponding reduction in operational risk

Outside restricted sectors, foreign entities can hold 100% ownership in most standard commercial structures. That exception does not eliminate the burden for firms operating in or near regulated industries.

Company Incorporation in Namibia

Understand ownership structures and sector-specific requirements before registering your business in Namibia.

BIPA Registration Process Delays

BIPA registration process delays in Namibia represent one of the more tangible operational burdens for foreign investors attempting to establish a presence. The Business and Intellectual Property Authority, which administers company registrations under the Companies Act 28 of 2004, has faced persistent capacity constraints that extend processing times well beyond what many investors initially anticipate.

Submitted applications frequently require multiple rounds of correspondence before approval, particularly where name reservations, director disclosures, or founding statement documents require correction. Each cycle of revision adds days or weeks to a timeline that your business cannot control.

| Registration Stage | Reported Delay Range | Implication for Foreign Incorporators |

|---|---|---|

| Name reservation | 5–10 business days | Delays the entire filing chain before it begins |

| Company registration (standard) | 3–6 weeks | Prevents legal operation until completion |

| Document apostille or notarization | Additional 1–3 weeks | Foreign-origin documents add a separate processing layer |

| Post-registration compliance filings | Variable | Annual returns and director changes face the same backlog |

Physical document submission remains a requirement for certain filings, meaning remote incorporation without local representation carries real logistical risk. For a foreign firm working across time zones, this dependency on in-person processes introduces unpredictable delays.

BIPA has introduced an online portal to reduce some administrative friction, though uptake and system reliability have been inconsistent. Until processing capacity matches registration volumes, incorporation timelines remain difficult to forecast with confidence.

Strict Foreign Exchange Controls Under Bank of Namibia

Namibia foreign exchange controls restrictions present one of the more consequential operational constraints for foreign-owned entities. The country is part of the Common Monetary Area (CMA) alongside South Africa, Lesotho, and Eswatini, and the Namibian Dollar is pegged 1:1 to the South African Rand. This arrangement means your firm's treasury decisions are indirectly tied to South African Reserve Bank monetary policy, without any direct influence over it.

Under the Currency and Exchanges Act, the Bank of Namibia enforces strict controls on cross-border capital flows. Transferring dividends, royalties, or loan repayments out of the country requires prior approval and supporting documentation, which delays repatriation of profits and increases administrative overhead for parent companies abroad.

Foreign currency restrictions in Namibia apply to both current and capital account transactions above defined thresholds. Any offshore investment or intercompany loan from a resident entity requires exchange control approval, which adds a compliance layer that most CMA-adjacent jurisdictions do not impose with the same rigor.

- Dividend repatriation requires Bank of Namibia exchange control approval before funds are transferred

- Intercompany loans between a Namibian resident entity and a foreign parent are subject to prior authorization

- All foreign currency transactions above prescribed limits must be reported to an authorized dealer bank

- Documentation requirements for capital transfers include audited financials and proof of tax compliance

Despite being pegged to the Rand, the Namibian Dollar is not legal tender in South Africa, meaning your business cannot use its Namibian cash holdings directly across the border without conversion.

High Corporate Tax Rate for Non-Manufacturing Entities

Non-manufacturing companies incorporated in Namibia face a standard corporate income tax rate of 32%, which sits noticeably above the global average of roughly 23%.

Who Bears the Higher Rate

Under the Income Tax Act (No. 24 of 1981), as amended, the 32% rate applies to most commercial entities that fall outside the manufacturing sector. Foreign-owned holding companies, trading firms, and service businesses are all subject to this rate, with no reduction tied to company size or revenue threshold.

This creates a measurable cost disadvantage relative to regional peers. Mauritius, for instance, applies a headline rate of 15%, meaning a foreign investor structuring operations through Namibia rather than a lower-tax jurisdiction absorbs a substantially higher ongoing tax liability.

Practical Consequences for Foreign Entities

The burden intensifies when combined with withholding taxes on dividends repatriated to foreign shareholders, which reduces after-tax returns further. Your effective return on investment shrinks not at a single point, but across multiple layers of the tax structure.

Manufacturing entities qualify for a reduced 18% rate, but that concession is narrowly defined and unavailable to the majority of foreign-owned businesses entering the market for trade or services.

Managing Namibia's Corporate Tax Burden for Your Business

Understand how Namibia's 32% corporate income tax rate affects your entity structure and what options exist before you incorporate.

Limited Skilled Labor Pool

Namibia limited skilled labor pool challenges are a direct operational cost for foreign businesses that require specialized technical, financial, or managerial talent. The country's population of approximately 2.5 million limits the absolute size of the available workforce across all sectors.

- Tertiary enrollment rates remain relatively low by regional standards, meaning your firm cannot assume a readily available pipeline of locally qualified professionals in fields such as engineering, finance, or information technology.

- The Immigration Control Act 7 of 1993 requires employers to demonstrate that no qualified Namibian citizen is available before a work permit for a foreign national can be approved, adding time and administrative cost to every senior hire.

- Brain drain to South Africa and other regional economies further reduces the pool of experienced professionals who remain in-country and available to your business.

- Sectors covered under Namibia's Industrialisation Policy face additional pressure to meet local hiring quotas, compounding recruitment difficulty for firms operating in designated industries.

Dependence on South African Economic Conditions

Namibia's dependence on South Africa's economy risks flowing directly into your business through the currency peg. The Namibian dollar is fixed at a 1:1 ratio with the South African rand under the Common Monetary Area (CMA) agreement, which also includes Lesotho and Eswatini. This arrangement means your firm has no independent monetary policy buffer when the rand depreciates or South African inflation rises.

South Africa accounts for a significant share of Namibian imports, meaning cost pressures in South Africa transmit directly into the local operating environment. If rand volatility erodes purchasing power, your business absorbs higher input costs without any exchange rate adjustment mechanism available domestically.

The South African Reserve Bank effectively sets the monetary conditions that the Bank of Namibia must broadly follow, given the peg. For a foreign entity with revenues in other currencies, this dual exposure to rand-linked inflation and South African economic cycles creates a structural pricing and planning constraint that jurisdictions with independent currencies do not impose.

A hypothetical scenario: a foreign-owned trading company invoicing clients in USD but paying Namibian staff and suppliers in NAD could see its local cost base increase by 10-15% during a rand depreciation cycle, with no offsetting devaluation benefit, since NAD moves in lockstep with ZAR regardless of domestic conditions.

Weak Digital Infrastructure for Business Operations

Namibia weak digital infrastructure business problems stem largely from uneven connectivity across the country. Fixed broadband penetration remains low, and internet speeds in commercial centers like Windhoek lag behind peer economies in East Africa, let alone global benchmarks. For a foreign entity relying on cloud-based operations, real-time data transfers, or remote team coordination, this directly increases operational friction and cost.

Mobile data costs are among the higher in sub-Saharan Africa relative to average income levels, which affects the practical affordability of connectivity for locally-hired staff and contractors.

Internet connectivity limitations affect Namibia companies beyond simple speed concerns. Power infrastructure inconsistencies compound the problem, as load-shedding events disrupt uptime for businesses without backup generation. Your firm absorbs those costs directly.

The ICT regulatory environment is overseen by the Communications Regulatory Authority of Namibia (CRAN), established under the Communications Act 8 of 2009. Despite CRAN's mandate to expand access, last-mile connectivity outside major urban centers remains commercially underdeveloped, meaning any business with operations outside Windhoek or Walvis Bay faces a material infrastructure gap.

Digital business challenges in Namibia are not uniform: foreign firms operating outside primary commercial hubs should independently verify connectivity availability at their specific location before committing to any operational model that depends on consistent broadband access.

Overcoming Namibia's Incorporation Challenges

Overcoming Namibia's Incorporation Challenges

Overcoming Namibia incorporation challenges requires a structural approach grounded in the country's specific legal and regulatory requirements. No single workaround resolves every constraint — each disadvantage covered in this blog demands its own compliance-oriented response.

- Engage a BIPA-accredited registered office and confirm all incorporation documents meet the Companies Act 28 of 2004 requirements before submission to reduce registration delays.

- Structure equity arrangements in advance to satisfy any sector-specific local ownership thresholds under applicable investment policies.

- Apply for a Foreign Investment Certificate through BIPA to formalise your entity's standing and access available investment protections.

- Open a dedicated Non-Resident Rand or foreign currency account and establish pre-approved remittance arrangements under Bank of Namibia exchange control directives.

- Register for corporate income tax and confirm your applicable rate with the Namibia Revenue Agency prior to commencing operations.

- Assess staffing requirements against the Immigration Control Act to determine whether work permit applications are necessary for foreign personnel.

Each of these steps operates within a regulatory framework that involves multiple statutory bodies, including BIPA, the Bank of Namibia, and the Namibia Revenue Agency. Mitigating risks of incorporating in Namibia means treating compliance as a precondition for operations, not a parallel process.

Namibia's Overall Investment Potential

Namibia investment risks and limitations are real and documented, but they exist within a jurisdiction that has maintained political stability, a functioning legal system rooted in Roman-Dutch law, and active participation in SADC trade frameworks. For the right business profile, the country presents a credible base for regional operations in southern Africa.

| Pros | Cons |

|---|---|

| Political stability and an independent judiciary provide a predictable legal environment | Foreign exchange controls under the Bank of Namibia restrict cross-border capital movement |

| Membership in SADC and AGOA creates preferential trade access for qualifying exports | The corporate tax rate of 32% for non-manufacturing entities is above the regional median |

| The Namibia Stock Exchange operates as a regulated, recognized bourse | Domestic capital markets are shallow, limiting access to local debt and equity financing |

| Manufacturing entities benefit from a reduced tax rate of 18% | The skilled labor pool is constrained, particularly in technical and professional sectors |

| Namibia's legal framework recognizes and enforces foreign investment agreements | BIPA registration delays add administrative lead time before operations can begin |

Dependence on South African monetary policy and economic cycles remains a structural constraint that falls outside any single investor's control. Digital infrastructure gaps, particularly outside Windhoek, continue to affect operational efficiency for businesses requiring consistent connectivity.

Corporate Compliance Services in Namibia

Maintain your company's good standing in Namibia with timely filing, regulatory reporting, and ongoing compliance support under local statutory requirements.

Conclusion

Incorporating in Namibia presents a defined set of structural constraints that your business must account for before committing to registration. The cons of starting a business in Namibia are not incidental — foreign exchange controls administered by the Bank of Namibia, delays within the BIPA registration process, and a corporate tax rate of 32% for non-manufacturing entities represent material operational considerations. Firms requiring speed, capital flexibility, or cross-border payment efficiency will encounter friction. Specialist guidance through the applicable legal and regulatory frameworks remains the practical path forward for foreign entities.

Expanship's Namibia Incorporation Services

Namibia company incorporation services from Expanship are designed to reduce the operational weight that BIPA's filing requirements, the Bank of Namibia's foreign exchange controls, and the country's local ownership considerations place on foreign investors. From preparing documentation that meets BIPA's standards to coordinating with relevant tax and regulatory authorities, Expanship handles the procedural side so your attention stays on the business itself.

Beyond registration, our services cover the full incorporation and post-incorporation cycle.

- Your company documents are prepared and submitted correctly for registration with BIPA.

- A registered agent and local office address are provided to meet statutory presence requirements.

- Government filings and regulatory body correspondence are managed on your behalf.

- Ongoing compliance obligations are monitored and maintained after incorporation.

- Banking introduction support is arranged to help establish your corporate account.

- Tax registration and liaison with the Namibia Revenue Agency are handled as part of the setup process.

Reach out to Expanship Namibia to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The standard corporate income tax rate of 32% applies to most non-manufacturing companies registered in Namibia, including branches of foreign firms. Manufacturing entities and businesses operating under specific incentive regimes may qualify for a reduced rate, but those concessions are conditional and require approval from the Namibia Revenue Agency. If your business falls outside those categories, the 32% rate applies from the first taxable dollar of income.

Operating a business in Namibia without proper registration through the Business and Intellectual Property Authority (BIPA) constitutes a violation of the Companies Act 28 of 2004, and can expose your entity to fines and potential deregistration. Beyond the statutory penalties, an unregistered or non-compliant company cannot legally enter contracts, open corporate bank accounts, or apply for operating licenses. The practical consequences extend well beyond the financial penalty itself.

Local ownership requirements in Namibia are sector-specific rather than universally applied. The New Equitable Economic Empowerment Framework (NEEEF) sets out broad empowerment targets, and certain regulated industries, including fishing, mining, and broadcasting, carry more prescriptive local participation thresholds than others. For sectors without explicit mandates, the pressure to include local partners may still arise through licensing conditions or procurement requirements imposed by government entities.

Namibia's currency, the Namibian dollar, is pegged at parity to the South African rand under the Common Monetary Area agreement, which means monetary shocks in South Africa transmit directly into Namibia's economy without any independent exchange rate buffer. A contraction in South African economic output or a rand depreciation event affects your Namibian entity's real purchasing power and import costs simultaneously. Your business has no practical hedge against this exposure through domestic monetary policy instruments.

BIPA processing times for company registration can extend several weeks beyond initial estimates, particularly when documentation queries arise or name reservation processes stall. Because a company cannot legally operate, open a bank account, or apply for sector-specific licenses until BIPA issues the registration certificate, any administrative delay creates a direct commercial gap. Foreign investors who factor in a 30-day incorporation timeline frequently encounter timelines that run to 60 days or longer.

Namibia's Employment Services Act requires employers to demonstrate that foreign nationals are hired only when suitably qualified Namibian citizens are not available, a standard enforced through the Ministry of Labour, Industrial Relations and Employment Creation. In practice, sourcing senior technical or specialist staff locally is difficult given the size of the talent pool, yet the work permit and quota processes for expatriate hires are administratively intensive and subject to discretionary approval. Your payroll and HR timelines need to account for this friction from day one of operations.

The constraint applies across company stages, though it manifests differently depending on your firm's size. Early-stage entities face difficulty accessing equity financing because the Namibian Stock Exchange lists a limited number of domestic companies and venture capital activity remains shallow. Established firms seeking to raise debt capital are similarly constrained by a banking sector concentrated among a small number of institutions, which limits competitive loan pricing and restricts access to structured financing products that are standard in larger markets.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.