Key Takeaways

- Namibia's source-based tax system means foreign-owned companies are not liable on worldwide income, limiting tax exposure to earnings generated within the country's borders.

- Under the Companies Act 28 of 2004, foreign investors can hold full ownership of a Namibian entity without mandatory local partnership requirements in most sectors, removing a structural barrier common in comparable African jurisdictions.

- Registration through the Business and Intellectual Property Authority (BIPA) provides a clearly defined regulatory pathway for private limited companies and Private Business Corporations, reducing procedural uncertainty during incorporation.

- Trade access under AGOA and EU preference arrangements means a Namibia-registered entity can serve as an effective export platform, extending commercial reach well beyond the SADC region.

Namibia is an independent republic in southern Africa, governed by a stable constitutional framework since its independence in 1990. Company registration falls under the authority of the Business and Intellectual Property Authority (BIPA), which administers the formation and ongoing compliance of business entities in the country. Foreign investors most commonly use the Private Business Corporation or a private limited company as their preferred legal vehicle for establishing a presence here.

The country operates a source-based tax system, meaning tax liability generally applies to income earned within its borders rather than on worldwide income. On the question of foreign ownership, the general regulatory posture is open — most sectors permit full foreign ownership without mandatory local partnership requirements, though certain industries carry specific conditions under sector-specific legislation.

Incorporating here carries a range of structural, geographic, and fiscal considerations that matter to internationally oriented businesses. This article examines the principal benefits of incorporating in Namibia, drawing on the specific legal, regulatory, and economic factors that shape the operating environment for foreign-owned companies.

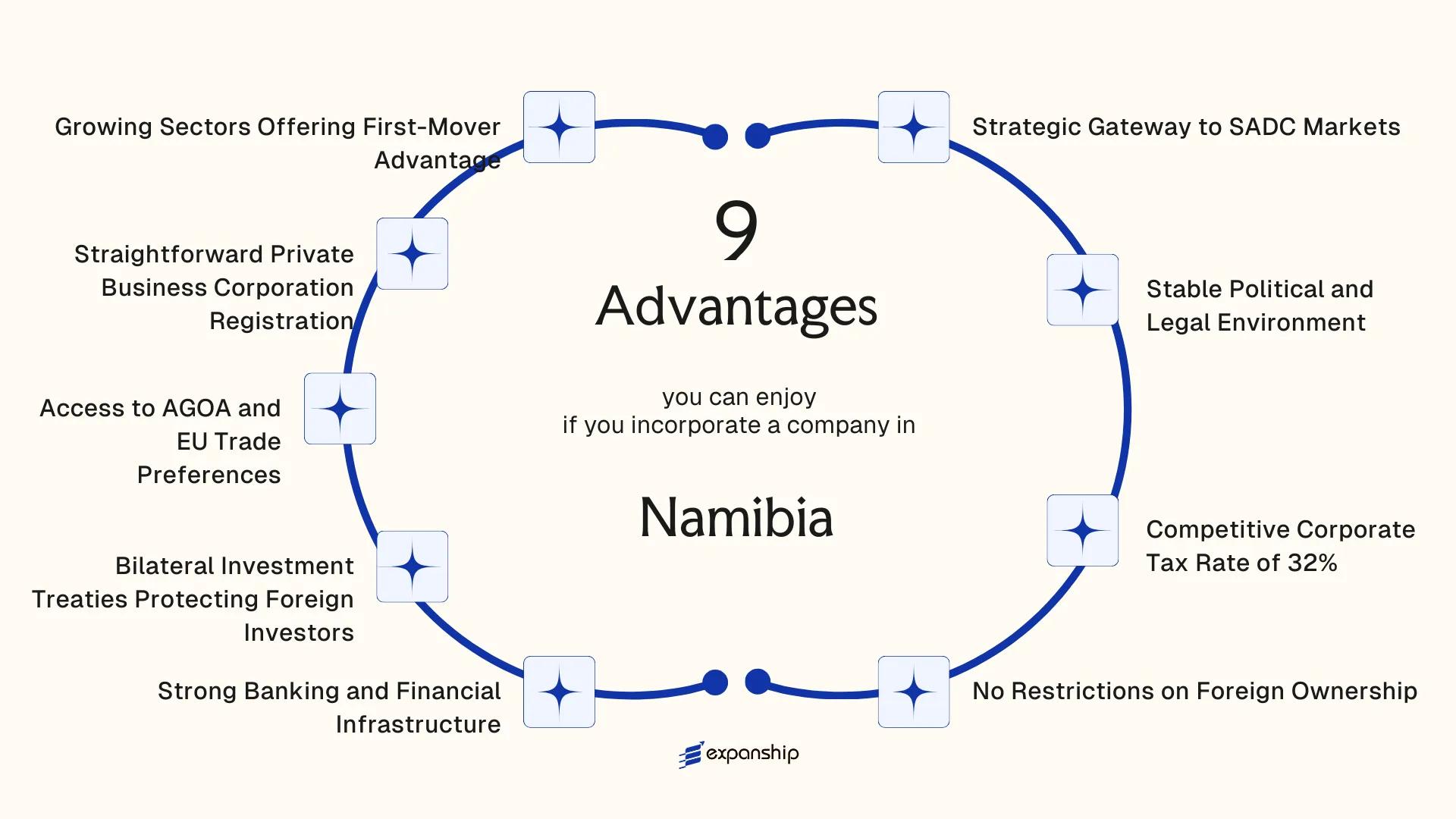

Strategic Gateway to SADC Markets

Namibia's membership in the Southern African Development Community positions any business incorporated here with direct, treaty-backed access to a bloc of 16 member states representing over 345 million consumers. Using Namibia as a gateway to SADC markets is a structural advantage, not a circumstantial one.

Regional Trade Frameworks That Work in Your Favor

The SADC Free Trade Area, which entered into force in 2008, eliminates or reduces tariffs on a substantial share of goods traded between member states. A company registered in Namibia can export into markets like South Africa, Zambia, Botswana, and Tanzania under preferential tariff schedules that are unavailable to firms incorporated outside the bloc.

Infrastructure Position Within the Region

The Port of Walvis Bay sits along one of the shortest shipping routes between South America, West Africa, and landlocked Southern African markets. Goods moving through this corridor reach inland SADC destinations faster than those routed through South Africa's busier ports, which directly reduces logistics timelines for distribution-oriented businesses.

Goods exported from your Namibia-registered entity into SADC member states may qualify for reduced or zero tariff rates under the SADC Free Trade Area agreement.

Stable Political and Legal Environment

Namibia's constitutional framework has remained intact since independence in 1990, with no military coups, unconstitutional transfers of power, or prolonged civil conflict in the intervening decades. For a foreign business owner, that continuity translates directly into predictability: the rules governing your entity today are unlikely to be overturned by political upheaval tomorrow.

The legal system operates under English common law principles, which means contract enforcement, property rights, and dispute resolution follow a framework familiar to investors from the UK, Australia, Canada, and other common law jurisdictions. Courts apply precedent-based reasoning, which reduces interpretive unpredictability when commercial disputes arise.

The Namibia stable political environment for business is further reinforced at the constitutional level. Article 16 of the Namibian Constitution expressly protects the right to acquire, own, and dispose of property, giving your firm a constitutional guarantee rather than a policy-level assurance.

Several features of the legal and regulatory environment deserve specific attention:

- The Companies Act 28 of 2004 provides a codified, publicly accessible foundation for corporate governance, reducing ambiguity in compliance obligations

- The High Court and Supreme Court are independent, with judges appointed through a structured process involving the Judicial Service Commission

- Anti-corruption legislation, enforced through the Anti-Corruption Commission, is institutionally separate from the executive branch

Company Incorporation in Namibia

Register your business in Namibia with end-to-end support from entity selection through to certificate of incorporation.

Competitive Corporate Tax Rate of 32%

Namibia's standard corporate income tax rate sits at 32%, applicable to most registered companies earning income from sources within the country. This rate is defined under the Income Tax Act (Act 24 of 1981), which remains the governing legislation for corporate taxation. For foreign businesses assessing the Namibia corporate tax rate advantages, 32% positions the country competitively relative to several other sub-Saharan African economies where rates can reach 35% or higher.

| Entity / Income Type | Applicable Tax Rate |

|---|---|

| Standard corporate entities | 32% |

| Registered manufacturers (approved) | 18% |

| Branches of foreign companies | 32% |

| Diamond mining companies | 55% |

| Other mining companies | 37.5% |

The 18% rate available to approved manufacturers under the Manufacturing Incentive Programme offers a meaningful reduction for qualifying foreign firms that establish production operations in the country. This is not automatic; the entity must meet specific approval criteria administered by the Ministry of Industrialisation and Trade.

Dividend withholding tax applies at 10% on distributions to non-resident shareholders, which affects your actual post-tax return when repatriating profits. Understanding this alongside the headline rate gives a more accurate picture of the effective tax position for a foreign-owned entity operating under the Income Tax Act's corporate framework.

No Restrictions on Foreign Ownership

Namibia imposes no foreign ownership restrictions on most private companies, meaning a non-resident investor can hold 100% of the shares in a locally registered entity. This is grounded in the Companies Act 28 of 2004, which treats foreign and domestic shareholders equally in terms of ownership rights. For you as a foreign investor, this eliminates the need for a local partner, nominee shareholder, or joint venture arrangement simply to satisfy legal thresholds.

Full ownership translates directly into full control. Profits, dividends, and capital gains belong entirely to your entity's structure without mandatory profit-sharing with a resident partner. That operational autonomy is a concrete financial advantage, not just a structural one.

Under the Companies Act, a private company can be formed with a single director and a single shareholder, both of whom may be foreign nationals. There is no minimum local equity requirement applicable to standard private business incorporations.

Keep these points in mind:

- Namibian law permits 100% foreign shareholding in private companies

- No resident director is legally required under the Companies Act

- Certain regulated sectors, such as fishing or land ownership, carry separate statutory restrictions

- Always confirm sector-specific rules with the Business and Intellectual Property Authority before incorporating

Foreign investors can serve as the sole director and sole shareholder simultaneously in a Namibian private company, with no residency requirement attached to either role.

Strong Banking and Financial Infrastructure

Namibia's banking infrastructure for businesses is regulated by the Bank of Namibia under the Banking Institutions Act of 1998, which sets capital adequacy requirements, liquidity standards, and governance obligations for all licensed commercial banks. This regulatory framework means your business deposits and transactions are held within a system that meets internationally recognized prudential standards, reducing counterparty risk when operating across borders.

Access to Multi-Currency and Cross-Border Banking Services

Commercial banks operating in Namibia, including Standard Bank, First National Bank, and Nedbank, offer accounts denominated in Namibian dollars and foreign currencies, along with SWIFT-connected international wire transfer facilities. For a foreign-owned entity, this eliminates the friction of routing payments through correspondent banks in third countries, which is a structural cost that compounds over time.

The Namibian dollar maintains a fixed 1:1 peg with the South African rand under the Common Monetary Area agreement. This peg provides exchange rate predictability when transacting with South African counterparties, who represent a significant share of regional trade flows.

Payment Systems and Financial Sector Oversight

The Namibia Financial Institutions Supervisory Authority (NAMFISA) supervises non-banking financial institutions, covering insurance, pension funds, and capital markets. A business operating in Namibia can access a regulated ecosystem of financial services beyond basic banking, including trade finance instruments and investment products.

Real-time electronic payment infrastructure through the Namibia Interbank Payment System (NIPS) supports same-day settlement for domestic transactions. Reliable settlement reduces working capital delays that would otherwise affect operational liquidity.

Structure Your Business to Access Namibia's Financial Advantages

Speak with an Expanship specialist about how to set up your Namibia entity in a way that maximizes access to the country's regulated banking and financial services ecosystem.

Bilateral Investment Treaties Protecting Foreign Investors

Namibia bilateral investment treaties protection gives foreign investors a degree of legal security that goes beyond domestic law. The country has concluded a number of BITs with partner states, including Germany, France, Spain, the Netherlands, and several others, each providing treaty-level guarantees that sit above ordinary commercial arrangements.

- Fair and equitable treatment clauses in these agreements require the host state to treat your investment without arbitrary interference, meaning regulatory changes cannot be applied in a discriminatory or capricious manner against foreign-held assets.

- Expropriation protections under most active BITs obligate the government to pay prompt, adequate, and effective compensation if assets are nationalised or taken for public purposes, removing the risk of uncompensated seizure.

- Free transfer provisions allow you to repatriate profits, dividends, and capital in convertible currency without the government blocking outward remittances under treaty obligations.

- Investor-state dispute resolution clauses, typically referencing ICSID or UNCITRAL arbitration, give your business access to neutral international tribunals rather than relying solely on domestic Namibian courts.

- Most-favoured-nation provisions in several of these treaties extend to your investment any more favourable treatment granted to investors from third countries in subsequent agreements.

Eligibility depends on the nationality of the investing entity, so the specific BIT in force between Namibia and your home jurisdiction determines which protections apply.

Access to AGOA and EU Trade Preferences

Namibia AGOA trade preferences for businesses represent a concrete export advantage. Under the African Growth and Opportunity Act, qualifying Namibian-incorporated entities can export over 6,500 product categories to the United States duty-free. For manufacturers or processors operating in the country, this eliminates a cost layer that competitors based outside eligible African nations must absorb.

On the European side, the EU-SADC Economic Partnership Agreement (EPA), which Namibia signed as a member of the SADC EPA Group, grants duty-free, quota-free access to EU markets for a defined range of goods. Beef, grapes, and fish products are among the categories that benefit directly. Your business can price exports more competitively into a combined EU consumer market of over 440 million people.

- AGOA eligibility is reviewed annually by the U.S. Trade Representative; Namibia has maintained continuous eligibility.

- EPA benefits apply to goods meeting the agreement's rules-of-origin requirements, so local value addition matters.

A Namibian beef processor exporting 50 tonnes annually to the EU avoids import duties that could otherwise reach 12.8% under standard WTO tariff schedules, representing a meaningful reduction in landed cost for EU buyers.

Straightforward Private Business Corporation Registration

One of the Namibia Private Business Corporation advantages most relevant to foreign founders is the speed and simplicity of the formation process. A Private Business Corporation, governed by the Close Corporations Act 26 of 1988, can be incorporated without a board of directors, company secretary, or mandatory audit requirement in most cases.

Membership is capped at ten natural persons, and each member holds a defined percentage interest rather than shares. This structure reduces administrative overhead compared to a full company registration under the Companies Act 28 of 2004, which carries more extensive compliance obligations.

Registration is filed with the Business and Intellectual Property Authority (BIPA), the central registry for business entities. Processing times are generally measured in days rather than weeks, meaning your business can become operational faster than in jurisdictions with multi-stage approval processes.

- No share capital structure is required

- Members can act as both owners and managers simultaneously

- Annual filing obligations are limited compared to public companies

The practical effect is lower formation cost and reduced legal structuring work before your business begins generating revenue.

Foreign nationals can hold membership interests in a PBC, but membership is restricted to natural persons only; corporate entities cannot be registered as members.

Growing Sectors Offering First-Mover Advantage

Several Namibia growing sectors first-mover advantage positions are available to foreign investors precisely because commercial activity in these industries remains limited relative to confirmed resource potential and policy commitment.

Green Hydrogen

The country has committed to developing one of Africa's largest green hydrogen programs under the Namibia Green Hydrogen Programme, backed by the Ministry of Mines and Energy. Offtake agreements and infrastructure development are still in early stages, which means foreign firms entering now encounter fewer established competitors than they would in mature markets. Your business can secure land use rights, supply agreements, and local partnerships before pricing and access conditions tighten.

Critical Minerals and Mining Supply Chain

Namibia holds confirmed deposits of uranium, lithium, copper, and rare earth elements. The Minerals (Prospecting and Mining) Act governs licensing, and the Ministry of Mines and Energy issues exploration and mining licenses through a defined application process. Firms that establish service, logistics, or processing entities now position themselves ahead of the extraction scale-up projected over the next decade.

Agro-Processing and Fisheries

The Namibia Agro-Processing Incentive Programme offers registered manufacturers preferential treatment on certain duties and levies. Fisheries, governed under the Marine Resources Act, allocate quota rights through a licensing system, with processing capacity remaining underdeveloped relative to catch volumes.

- Green hydrogen infrastructure and supply chain services

- Lithium and rare earth mineral processing

- Fish meal, fish oil, and cold-chain logistics

- Solar energy equipment supply and installation

Why Namibia Stands Out Against Regional Competitors

Comparing Namibia against its SADC neighbours is useful precisely because the region presents several credible incorporation destinations. South Africa, Botswana, and Mauritius each attract foreign capital for different reasons, making them the most realistic alternatives a foreign investor would weigh. What the comparison reveals is not simply a difference in tax rates, but structural differences in ownership rules, currency stability, and access to trade preferences that affect how a business actually operates day-to-day.

South Africa carries a standard corporate tax rate of 27% but imposes exchange controls administered by the South African Reserve Bank, which can restrict cross-border profit repatriation in ways that a Namibia-incorporated entity is not subject to. Botswana offers political stability and a flat 22% corporate rate, yet lacks Namibia's direct AGOA eligibility and the EU Economic Partnership Agreement access that applies to goods originating here. Mauritius is frequently used as a holding jurisdiction, but its Africa positioning is financial rather than operational, with no equivalent land border access to Angola, Zambia, or South Africa simultaneously.

| Parameter | Namibia | South Africa | Botswana |

|---|---|---|---|

| Corporate Tax Rate | 32% | 27% | 22% |

| Foreign Ownership | 100% permitted | 100% permitted (sector restrictions apply) | 100% permitted (some reserved sectors) |

| Exchange Controls | None on foreign-owned entities | Yes, SARB administered | None |

| AGOA Eligibility | Yes | Yes | Yes |

| EU EPA Access | Yes | Yes (SADC EPA) | Yes (SADC EPA) |

| Private Business Corporation Structure | Yes (PBC available) | No direct equivalent | No direct equivalent |

| SADC Land Border Access | Angola, Zambia, Botswana, South Africa, Zimbabwe | Yes (multiple) | Limited (landlocked, fewer borders) |

| Primary Regulatory Body | BIPA | CIPC | CIPA |

Compliance Services for Companies in Namibia

Stay current with Namibia's regulatory requirements, including annual returns, tax filings, and BIPA obligations, with Expanship's compliance support for foreign-owned entities.

Conclusion

Namibia's case for foreign incorporation rests on a combination of structural stability and genuine market access. The absence of foreign ownership restrictions under the Companies Act 28 of 2004, combined with treaty protections under its bilateral investment agreements, means your business enters the jurisdiction with both operational freedom and legal recourse. Access to SADC markets and trade preferences under AGOA further extends the commercial reach of any entity registered here.

That said, the right fit depends on your industry, your target markets, and how your corporate structure is organised. A firm focused on mineral beneficiation operates under a different regulatory and tax calculus than one using Namibia as a distribution base for southern Africa. The benefits of incorporating in Namibia are real, but they are not uniform across all business models.

Formalising a presence here is a decision that benefits from jurisdiction-specific legal and compliance input. The regulatory framework, including the role of the Business and Intellectual Property Authority as the registrar of companies, is well-defined, but applying it correctly to your specific structure requires precise execution from the outset.

Start Your Namibia Company Formation With Expanship Today

Namibia company formation with Expanship begins with understanding the regulatory environment you have already read about in this blog. Expanship manages the full incorporation process through the Business and Intellectual Property Authority (BIPA), covering both Private Business Corporations under the Close Corporations Act 26 of 1988 and private companies registered under the Companies Act 28 of 2004. Post-registration compliance obligations, including annual returns and tax registration with the Namibia Revenue Agency (NamRA), are handled as part of the service scope.

Expanship's services for your Namibia entity include:

- Preparation and legalization of all incorporation documents

- Registered agent and registered office provision in Namibia

- Filing and liaison with BIPA and NamRA on your behalf

- Post-incorporation compliance management, including annual return submissions

- Banking introduction assistance to support your operational setup

To discuss your requirements, contact Expanship Namibia directly.

Frequently Asked Questions (FAQ)

The standard corporate income tax rate is 32%, as administered by the Namibia Revenue Agency (NamRA). Certain activities attract different rates — diamond mining companies, for instance, are taxed at a higher rate, while approved manufacturers may qualify for a reduced rate under investment incentive provisions. Your accountant or tax adviser should confirm which rate applies based on the nature of your business activities.

Registration timelines with the Business and Intellectual Property Authority (BIPA) vary, but incorporation of a Private Business Corporation generally takes between five and fifteen business days when documentation is in order. Delays typically arise from name reservation conflicts or incomplete founding statements submitted under the Close Corporations Act 26 of 1988.

A company incorporated in the country gains access to preferential tariff arrangements across SADC member states under the SADC Trade Protocol. This reduces or eliminates customs duties on qualifying goods traded within the bloc, which covers markets across southern and eastern Africa. The practical benefit depends on your product category and the specific bilateral schedules in force between Namibia and the destination country.

Bilateral investment treaties (BITs) that Namibia has concluded with various partner countries provide enforceable protections including fair and equitable treatment, protection against expropriation without compensation, and access to international arbitration. These protections apply to investments made by nationals of the treaty partner country, so eligibility depends on your nationality and the existence of a relevant treaty. Treaty protections do not override domestic law but do provide an additional layer of recourse outside the local court system.

A private limited company incorporated under the Companies Act 28 of 2004 must have at least one director, but that director is not required to be a Namibian resident or citizen. A Private Business Corporation requires at least one member, who similarly faces no residency requirement under the Close Corporations Act. Certain financial and regulated sector licences may impose additional requirements, which are set by the relevant sector regulator rather than the company registration framework itself.

Under the African Growth and Opportunity Act, qualifying Namibian exporters can ship eligible goods to the United States duty-free, which is an advantage that depends on maintaining AGOA beneficiary status and meeting the applicable rules of origin. Not all regional competitors hold this status, and some that do face graduation risks based on their income classification. For manufacturers and processors targeting the US market, the duty savings can materially affect landed cost competitiveness relative to goods originating from non-beneficiary countries.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.