Key Takeaways

- Foreign investors in Mozambique must navigate a registration process governed by the Commercial Code and the CMEL (Commercial, Industrial, and Service Activities Licensing regime) that layers multiple sequential approvals across different public bodies, extending timelines well beyond what comparable regional jurisdictions require.

- Corporate tax and withholding tax rates in Mozambique impose a meaningful cost burden on foreign-owned entities, particularly those repatriating dividends or servicing cross-border loans from a jurisdiction with limited double tax treaty coverage.

- Certain strategic sectors impose restrictions on the extent of foreign ownership permitted, requiring investors to structure equity arrangements around local participation thresholds that constrain operational control.

- Currency controls and restrictions on converting and repatriating Mozambican metical create additional financial friction for multinational entities that need to move profits or intercompany payments across borders efficiently.

Mozambique operates under an evolving regulatory framework, where the rules governing foreign investment and corporate compliance continue to develop alongside broader economic reforms. The disadvantages of incorporating in Mozambique span areas including registration procedures, ownership restrictions, tax obligations, and financial infrastructure — each addressed in detail across this article.

The extent to which these drawbacks affect your business depends significantly on the sector, corporate structure, and the level of foreign participation involved. A mining joint venture faces a different compliance burden than a services firm or a small trading entity.

Governing commercial activity in the country is the Commercial Code, which sets out the foundational rules for business formation and operation. This article is most relevant to foreign investors and multinational entities considering market entry into Mozambique for the first time, particularly those unfamiliar with the local regulatory environment.

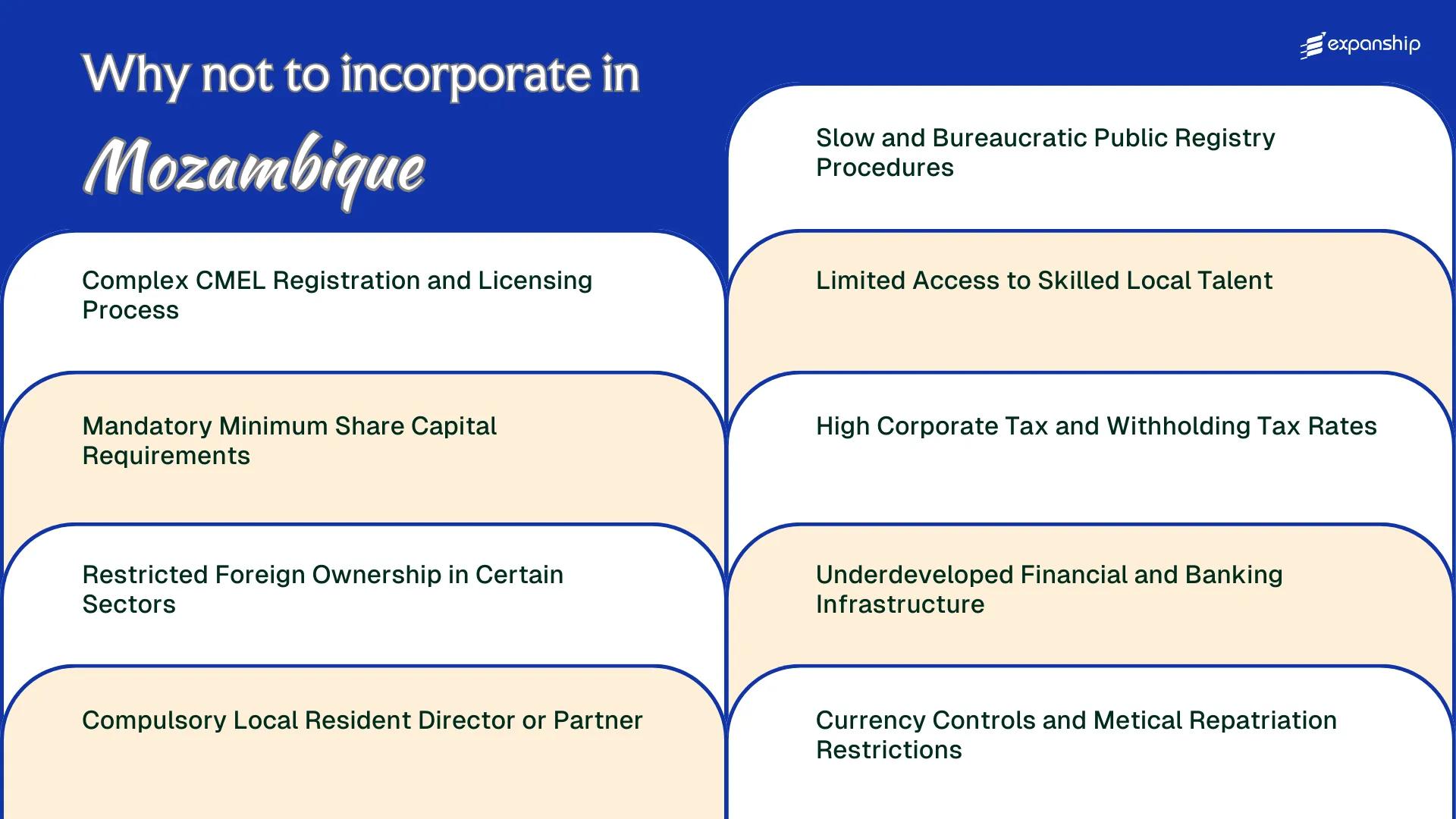

Complex CMEL Registration and Licensing Process

Mozambique CMEL registration challenges begin before your business opens its doors. Registering a commercial entity under the country's Commercial Code (Código Comercial) involves multiple sequential steps across several public bodies, and delays at any stage extend the entire timeline.

Multiple Mandatory Agencies, One Process

Registration requires interaction with CMEL (Conservatória do Registo das Entidades Legais), the Tax Authority (Autoridade Tributária de Moçambique), the National Institute of Social Security (INSS), and often a notary. Each body operates on its own schedule, meaning a hold at CMEL does not pause obligations at other agencies, forcing your firm to manage parallel processes with no single coordination point.

Unpredictable Processing Timelines

CMEL licensing problems in Mozambique are frequently tied to document verification delays and administrative backlogs within the registry itself. A business cannot legally operate until the certificate of incorporation is issued, so extended processing directly delays revenue generation.

Incomplete or improperly notarised documentation submitted to CMEL restarts the verification process, which can add weeks to your incorporation timeline with no guaranteed resolution date.

Mandatory Minimum Share Capital Requirements

Mozambique minimum share capital requirements vary by entity type, and for a Sociedade por Quotas (Lda), the Commercial Code sets the minimum at 20,000 meticais. That figure is low in isolation, but sector-specific investment frameworks impose far higher thresholds that can catch foreign founders off guard during planning.

Certain regulated industries require substantially greater paid-up capital before authorities grant operational licenses. This means your incorporation budget cannot be determined by the Commercial Code alone — it depends on which regulatory body governs your sector.

Beyond the headline figure, mandatory capital requirements in Mozambique create several practical burdens:

- Capital must be deposited in a local bank account before registration is finalized, tying up funds during a process that can take weeks

- Sector-specific minimums set outside the Commercial Code are not always consolidated in a single public source, creating due diligence costs

- Foreign-owned firms may face additional scrutiny over the source of contributed capital, prolonging the verification process

The requirement that capital be locally deposited before the entity is legally constituted means your money is committed before you have any operating structure in place.

Company Incorporation in Mozambique

Set up your Mozambican entity with accurate capital structuring from the start, guided by local regulatory requirements.

Restricted Foreign Ownership in Certain Sectors

Foreign ownership restrictions in Mozambique affect multiple industries that are central to the country's economy, creating structural barriers that limit how much equity a foreign investor can hold or control.

Under the Investment Law (Law No. 3/93) and subsequent sectoral regulations, certain industries impose mandatory local equity participation. This means your firm cannot hold 100% of shares in these sectors, regardless of the capital you commit.

| Sector | Maximum Foreign Equity | Practical Restriction |

|---|---|---|

| Artisanal fishing | 0% | Entirely closed to foreign ownership |

| Small-scale agriculture | Restricted | Priority reserved for Mozambican nationals |

| Media and broadcasting | Restricted | Local ownership majority required |

| Some natural resource concessions | Varies | State or local partner participation mandated |

In sectors such as natural resources, the government retains the right to require state participation through entities like ENH (hydrocarbons) or EMATUM (fisheries), effectively reducing your ownership stake by law rather than negotiation. This is not a minor administrative condition — it directly limits the financial returns and operational control available to foreign shareholders.

Sectors tied to land use present a separate constraint. Land in Mozambique cannot be privately owned; it is held by the state under the Land Law (Law No. 19/97), so any business dependent on long-term land rights operates under a concession framework that foreign firms cannot fully secure independently.

Where joint ventures are required, finding a compliant local partner with adequate capital and legal standing takes considerable time and due diligence, adding cost before operations begin.

Compulsory Local Resident Director or Partner

Mozambique local director requirements present a structural constraint that foreign investors rarely anticipate before committing to incorporation. Under the Commercial Code (Lei n.º 10/2013), certain business forms and regulated sectors require at least one locally resident director or partner, meaning your appointed individual must be physically present and legally resident in the country, not simply a nominee on paper.

This creates an immediate dependency on a third party whose interests may not align with your business objectives. If that person resigns, becomes unavailable, or acts outside their remit, your entity's compliance status can be compromised before you have time to appoint a replacement.

The compulsory resident partner obligation in Mozambique is not a formality. A resident director carries legal liability under Mozambican law, which means finding a qualified, willing individual who accepts that exposure involves both effort and ongoing cost.

- At least one director or partner must hold legal residency in Mozambique, not merely citizenship or a work permit in process

- The resident individual assumes personal legal liability under the Commercial Code, not the foreign parent entity alone

- Replacing a non-compliant or departing resident director requires a formal registry update with the Conservatória do Registo das Entidades Legais (CREL)

- Failure to maintain a qualifying resident director can trigger suspension of operating licenses issued by sector-specific regulators

- The obligation applies regardless of the foreign company's ownership percentage in the local entity

Even a 100% foreign-owned entity in a non-restricted sector may still face a de facto requirement to appoint a locally resident director to satisfy CREL registration conditions in practice.

Slow and Bureaucratic Public Registry Procedures

Mozambique public registry delays represent one of the more tangible friction points for foreign investors attempting to establish a legal presence in the country. Registration through the Conservatória do Registo de Entidades Legais (CREL) routinely extends beyond official processing windows, adding weeks to incorporation timelines.

Structural Inefficiencies in the CREL Process

CREL, the body responsible for registering commercial entities, operates with limited digitisation and relies heavily on manual document handling, which creates backlogs that compound during peak filing periods. Your business cannot legally operate until registration is complete, meaning these delays translate directly into lost revenue and deferred market entry.

Consequences for Foreign Business Owners

Slow company registration through the Conservatória also affects downstream obligations, since tax registration with the Autoridade Tributária de Moçambique and municipal licensing cannot proceed until the CREL certificate is issued. Firms with time-sensitive operational commitments, such as project-based contracts or joint ventures with fixed start dates, face contractual exposure when the registry falls behind schedule. Delays tend to be shorter for straightforward single-member entities, though multi-partner structures with foreign shareholders typically encounter additional scrutiny.

Assistance With Corporate Registry Challenges in Mozambique

Get structured guidance on managing CREL registration timelines and reducing delays in your Mozambique incorporation process.

Limited Access to Skilled Local Talent

Mozambique skilled workforce limitations present a concrete operational constraint for foreign firms, particularly in technical, financial, and managerial functions. The gap between available local qualifications and the competency levels required for specialised roles forces many incorporated entities into costly and administratively burdensome workarounds.

- Under the Labour Law (Law No. 23/2007), foreign nationals employed by a local entity cannot exceed 5% of the total workforce in most categories, which directly restricts your ability to substitute scarce local skills with international hires.

- The Instituto Nacional de Emprego e Formação Profissional (INEFP) does not consistently supply candidates with sector-specific technical credentials, forcing businesses to fund training at their own expense before staff become operationally effective.

- Obtaining work permits for foreign specialists through the Ministry of Labour requires demonstrated proof that no qualified local candidate exists, adding documentary burden and processing delays to each hire.

- Talent shortage risks for companies in Mozambique are compounded in the extractive and financial sectors, where qualified local professionals remain scarce relative to industry demand.

High Corporate Tax and Withholding Tax Rates

Mozambique corporate tax rate drawbacks stem primarily from the IRPC (Imposto sobre o Rendimento das Pessoas Colectivas), which applies to corporate profits at a standard rate of 32%. For most regional peers in sub-Saharan Africa, standard corporate rates fall between 25% and 30%, placing your business at a structural cost disadvantage from the outset.

Withholding tax compounds this burden. Dividends paid to non-resident shareholders attract a 20% withholding rate under the IRPC regime, and interest payments to foreign entities are subject to the same rate.

Services rendered by non-resident firms without a permanent establishment in the country are also subject to withholding, reducing the net value of cross-border commercial arrangements. This affects how foreign parent companies structure intra-group transactions and fee arrangements with local subsidiaries.

Reduced rates may apply where a double taxation agreement (DTA) is in force, but Mozambique's DTA network remains limited in scope.

A foreign investor receiving a USD 200,000 dividend distribution from a Mozambican subsidiary would face a USD 40,000 withholding deduction at the 20% non-resident rate before any repatriation, before accounting for taxes owed in the investor's home jurisdiction on the same income.

Underdeveloped Financial and Banking Infrastructure

Mozambique banking infrastructure limitations present a direct operational obstacle for foreign businesses, not merely an inconvenience. The banking sector is concentrated among a small number of institutions, with Millennium BIM, BCI, and Nedbank Mozambique dominating commercial services, leaving limited competition and minimal incentive to accommodate complex corporate clients efficiently.

Opening a business bank account can take several weeks and requires extensive documentation, including notarised corporate documents, proof of registered address, and shareholder identification verified through the CMEL-registered entity. Delays at this stage directly stall your ability to receive payments, pay suppliers, or meet payroll obligations.

Digital banking infrastructure for corporate clients remains underdeveloped relative to the region, with limited API integrations, unreliable online banking platforms, and restricted access to trade finance products. For a foreign-owned firm dependent on cross-border transactions, this creates friction at every financial touchpoint.

Correspondent banking relationships are also constrained, which affects the speed and cost of international wire transfers. Transactions can attract elevated fees and processing times that erode operational efficiency.

- Branch networks outside Maputo and Beira are sparse, complicating payroll or supplier payments in interior provinces.

- Access to credit facilities for foreign-owned entities is restricted without substantial collateral held locally.

- Multi-currency corporate accounts are not uniformly available across banks.

If your business operates outside Maputo province, banking access may be severely limited, and you should verify branch or agent banking availability in your specific operating region before completing your incorporation.

Currency Controls and Metical Repatriation Restrictions

Mozambique currency repatriation restrictions create direct cash flow risks for foreign investors. The Bank of Mozambique, operating under the Foreign Exchange Law (Law No. 11/2009) and its implementing regulations, requires that cross-border transfers of profits, dividends, and capital gains follow an approved documentation process before funds can exit the country.

Delays in obtaining transfer approval can lock earnings inside the jurisdiction for extended periods, disrupting the financial planning of the parent entity abroad.

The Metical is not freely convertible on international markets, which means your firm is exposed to exchange rate depreciation between the time profits are earned and when conversion is permitted. This risk compounds when transaction volumes are high.

Businesses operating in sectors under investment agreements may access more structured repatriation terms, but those arrangements require prior negotiation with government authorities and are not available to all foreign entities.

Strategies to Overcome These Challenges

Overcoming Mozambique incorporation challenges requires structural preparation before the entity is registered, not after problems surface.

- Pre-verify sector-specific foreign ownership caps under the Investment Law (Law 3/1993 and its revisions) before selecting your company structure.

- Confirm minimum share capital thresholds with the Conservatória do Registo das Entidades Legais (CREL) for your chosen entity type prior to opening a local bank account.

- Identify a qualifying resident director or partner early, as this requirement affects your timeline and governs signatory authority under Mozambican commercial law.

- Apply for all required CMEL licences in parallel with your CREL registration to reduce sequential delays in the public registry process.

- Establish a local Metical account through a Banco de Moçambique-licensed institution and document your repatriation approval process under the Foreign Exchange Law (Law 11/2009).

These steps address the structural and regulatory layers that govern foreign business entry. The Investment Law framework sets the outer boundaries within which all mitigation approaches must operate.

Mozambique's Overall Investment Viability

Mozambique's investment viability risks are real and well-documented, but they do not uniformly disqualify the country as an incorporation destination. For businesses with a clear sectoral focus, tolerance for procedural friction, and a long-term horizon, the underlying opportunity — particularly in energy, agriculture, and infrastructure — remains substantive.

| Pros | Cons |

|---|---|

| Significant natural resource base, including gas reserves, creates genuine commercial opportunities | CMEL registration and licensing procedures are slow, multi-agency, and document-intensive |

| Investment protections exist under the Investment Law and applicable bilateral investment treaties | Minimum share capital requirements apply and vary by business activity and ownership structure |

| Foreign ownership is permitted in most sectors with no blanket prohibition | Restricted foreign ownership applies in specific strategic sectors |

| The metical is a functioning currency with an established central banking framework under Banco de Moçambique | Currency controls and repatriation restrictions limit how freely profits can be moved offshore |

| Corporate structures such as the Sociedade por Quotas offer recognised limited liability frameworks | IRPC corporate tax rates and withholding tax obligations increase the overall cost of doing business |

Skilled labour availability remains a structural constraint, and the underdeveloped banking system adds friction to day-to-day financial operations. These are not short-term conditions likely to resolve quickly.

Corporate Compliance Services in Mozambique

Maintain your Mozambique entity in good standing with local regulatory and filing obligations, including annual returns, tax submissions, and ongoing statutory requirements.

Conclusion

Incorporating in Mozambique carries a well-documented set of structural constraints that affect timeline, cost, and operational flexibility. The Mozambique company formation drawbacks summary presented across this article points to three friction points that consistently affect foreign investors: the multi-stage CMEL registration process, the sector-specific foreign ownership restrictions enforced under the Investment Law, and the currency controls that complicate profit repatriation through the Bank of Mozambique's regulatory framework. Structural constraints of this kind do not disappear through entity selection alone. Professional guidance from specialists with in-country regulatory experience materially affects how these obligations are managed from incorporation through ongoing compliance.

Expanship's Support for Your Mozambique Expansion

Mozambique expansion support services cover the specific regulatory and compliance demands that make operating here operationally intensive. From managing CMEL licensing requirements and liaising with APIE or IPEME, to handling currency control filings and meeting local directorship obligations, Expanship works to reduce the administrative burden your business carries at each stage of the incorporation process.

Our services span the full setup and post-registration cycle:

- Preparing and submitting company registration documents with the relevant conservatória

- Providing a registered agent and local office address in Mozambique

- Handling government filings and liaising directly with regulatory authorities on your behalf

- Managing ongoing compliance obligations after your entity is incorporated

- Facilitating introductions to local banking institutions to support account opening

- Registering your business for tax purposes and coordinating with the Autoridade Tributária de Moçambique

To discuss your setup requirements, contact Expanship Mozambique.

Frequently Asked Questions (FAQ)

Restrictions on foreign ownership apply to specific sectors rather than the entire economy, but those sectors include strategically significant industries such as natural resources, land, and certain regulated services. Under Mozambican law, land cannot be privately owned by any entity, foreign or local, and is held by the state under a land-use right system called DUAT, which adds a separate layer of process for any business requiring physical premises. Investors in extractive industries face additional concession and licensing requirements that go well beyond standard incorporation.

Mozambique imposes withholding tax rates that can reach 20% on dividends, interest, and royalties paid to non-resident entities. The exact rate depends on whether a double taxation agreement exists between Mozambique and your home jurisdiction, and Mozambique's treaty network remains limited. Where no treaty applies, the standard rates under the Imposto sobre o Rendimento das Pessoas Colectivas (IRPC) regime apply in full.

Non-compliance with local directorship or resident partner requirements can result in your company being considered improperly constituted under Mozambican commercial law, which exposes the entity to regulatory penalties and potential suspension of its operating licence. The Conservatória do Registo das Entidades Legais, which oversees entity registration, can refuse to complete registration or flag the entity for non-compliance review. Rectifying the structure after the fact requires additional legal filings and can reset processing timelines.

Mozambique's minimum share capital requirements are not the highest on the continent, but they are structured in a way that can create disproportionate upfront costs for smaller foreign businesses, particularly when combined with mandatory paid-up capital rules. In contrast, some neighbouring jurisdictions allow nominal minimum capital with no paid-up requirement at formation. The actual burden depends on the entity type you incorporate, with Sociedades por Quotas and Sociedades Anónimas carrying different thresholds under the Commercial Code.

Mozambique imposes foreign exchange controls administered by the Banco de Moçambique, and repatriating profits requires documented compliance with local tax obligations before transfers are approved. Transactions above certain thresholds require prior authorisation, and delays in that process can tie up working capital for weeks or longer. The Metical is also not freely convertible on international markets, which compounds the practical difficulty of moving funds across borders efficiently.

Some international banking groups do operate branches in Mozambique, which mitigates but does not eliminate the infrastructure challenges. Account opening for foreign-owned entities still requires extensive local documentation and can take considerably longer than in more developed financial centres, regardless of the bank's international standing. Access to trade finance, multi-currency accounts, and digital banking tools also remains more limited than what the same institution might offer in its home market.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.