Key Takeaways

- Mozambique's IRPC corporate tax regime, combined with territorial-based taxation that generally exempts foreign-sourced income, means companies operating across multiple jurisdictions can contain their Mozambican tax exposure to domestically generated earnings only.

- Under Investment Law No. 3/93 and its revisions, foreign investors receive formal legal protections and are permitted 100% ownership in most sectors, removing the structural barriers to full profit repatriation and operational control that apply in many comparable African jurisdictions.

- Membership in both SADC and COMESA gives companies incorporated in Mozambique preferential access to a combined regional market that spans a substantial portion of the African continent, reducing tariff friction on qualifying goods traded across member states.

- Businesses whose operations align with Mozambique's designated Special Economic Zones can access significant tax exemptions that materially alter the cost structure of export-oriented manufacturing or resource-linked activity compared with standard incorporation outside those zones.

Mozambique is an independent sovereign state located on the southeastern coast of Africa, bordered by Tanzania, Zambia, Zimbabwe, South Africa, and Eswatini, with direct access to the Indian Ocean. The benefits of incorporating in Mozambique draw interest from businesses seeking a foothold in sub-Saharan Africa, and company registration is overseen by the CIAR (Centro de Internacionalização das Actividades e Registos), the body responsible for business registration and licensing. Most foreign businesses establish a presence through a Sociedade por Quotas.

The country operates a territorial-based tax system, taxing income sourced within its borders while generally exempting foreign-sourced earnings from domestic liability. Foreign direct investment is formally welcomed under the Investment Law (Law No. 3/93) and its subsequent revisions, which establish legal protections and guarantees for investors from abroad.

This article outlines the principal advantages your business can expect when forming a company in this jurisdiction.

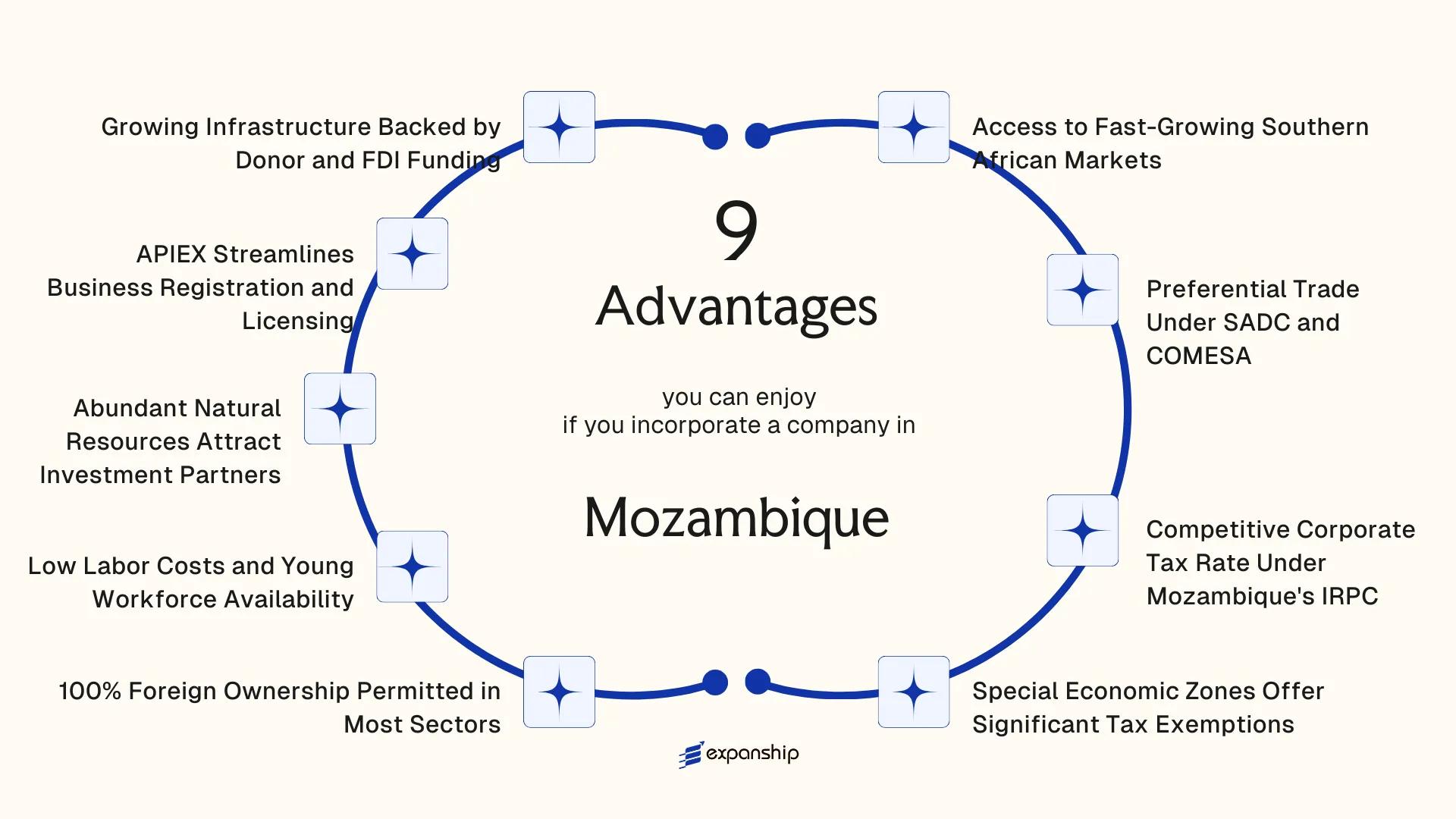

Access to Fast-Growing Southern African Markets

Mozambique's geographic position along the Indian Ocean coastline, sharing borders with six countries, gives incorporated entities direct physical access to Southern African markets without requiring a regional holding structure.

A Frontier Location With Commercial Reach

The country borders Tanzania, Malawi, Zambia, Zimbabwe, Eswatini, and South Africa. That corridor covers a combined population exceeding 300 million people, which means your business can serve multiple national markets from a single registered entity.

Beira and Maputo function as active transit hubs for landlocked neighbors. Goods moving through these ports into Zimbabwe or Zambia originate from a Mozambican commercial address, giving your firm a credible operational presence at the point of entry into the subregion.

Regional Consumer Growth and Trade Flows

Southern Africa's urban middle class has expanded steadily across the past decade, increasing demand for manufactured goods, financial services, and logistics. A company incorporated here sits within that demand zone rather than outside it.

Incorporating in Mozambique for Southern Africa expansion positions your entity inside the SADC free trade area, where intra-regional trade volumes have grown as tariff schedules between member states continue to reduce.

A Mozambican entity can ship goods and invoice clients across six neighboring markets without establishing separate legal presences in each country.

Preferential Trade Under SADC and COMESA

Mozambique SADC COMESA trade benefits for businesses are among the most structurally significant advantages available to a foreign-incorporated entity operating in the region. As a member of both the Southern African Development Community (SADC) and the Common Market for Eastern and Southern Africa (COMESA), a company registered here gains preferential market access across a combined population exceeding 700 million people, without facing standard import tariffs in participating member states.

Under the SADC Trade Protocol, qualifying goods that meet rules-of-origin requirements move between member states at reduced or zero duty rates. For a manufacturer or trading company, this directly lowers the landed cost of exports across Southern Africa, improving price competitiveness without changing the product itself.

COMESA membership benefits Mozambique companies differently, extending preferential access northward into East Africa, including markets such as Kenya, Ethiopia, and Egypt. This dual membership is uncommon among regional peers and gives your firm geographic reach that a single-bloc member cannot replicate.

Practical advantages of this dual-bloc positioning include:

- Reduced customs duty exposure across two distinct regional trading blocs

- Access to COMESA's Free Trade Area, which covers a significant share of the bloc's membership

- Eligibility for preferential treatment under SADC's tariff phase-down schedule

- A broader pool of duty-advantaged sourcing destinations for inputs and raw materials

Rules-of-origin compliance under both frameworks requires careful documentation, but the threshold conditions are defined within each respective protocol rather than left to discretionary customs assessment.

Company Incorporation in Mozambique

Register your business in Mozambique and access preferential trade across SADC and COMESA member states.

Competitive Corporate Tax Rate Under Mozambique's IRPC

Mozambique's IRPC corporate tax rate advantages are most apparent when you examine the headline figure: the standard corporate income tax rate sits at 32%. That number requires context. For businesses operating within designated industrial free zones or benefiting from investment incentives under the Investment Law (Law No. 3/93, as updated by subsequent legislation), effective rates can be reduced substantially through approved tax reductions and multi-year exemptions granted by the government.

| Entity Type / Status | Standard IRPC Rate | Applicable Instrument |

|---|---|---|

| Standard resident company | 32% | IRPC Code |

| Agricultural sector entities | 10% | IRPC preferential rate |

| Companies in industrial free zones | 0% (exemption period) | Industrial Free Zones Decree |

| Micro and small enterprises | Simplified regime applies | IRPC Code |

The agricultural sector rate of 10% under the IRPC Code is a concrete example of how sector-specific structuring affects your firm's tax position directly. For a foreign investor establishing operations in agribusiness or primary production, that differential translates to a materially lower annual tax obligation compared to a standard commercial entity.

Tax administration falls under the Autoridade Tributária de Moçambique (AT), which governs IRPC filings, assessments, and compliance. Knowing the administering body matters because your entity's registration, fiscal identification, and annual declarations are all processed through AT's framework, giving you a single point of reference for corporate tax obligations.

Special Economic Zones Offer Significant Tax Exemptions

Mozambique special economic zones tax exemptions represent one of the more concrete fiscal advantages available under the country's investment framework. Two principal zone types exist: Zonas Económicas Especiais (ZEE) and Zonas Francas Industriais (ZFI). Each carries distinct tax treatment governed by the Lei de Zonas Francas e Zonas Económicas Especiais and administered under the authority of APIEX (Agência para a Promoção de Investimento e Exportações).

Businesses operating within a ZFI benefit from a full corporate income tax (IRPC) exemption for the first ten years of operation. A reduced rate applies in subsequent years, structured to decrease progressively over time. For export-oriented manufacturers, this phased relief means a significantly lower effective tax burden during the years when capital recovery is most critical.

ZEE-registered entities benefit from customs duty exemptions on imported equipment and inputs used in production. For capital-intensive industries, this directly reduces upfront establishment costs.

Keep these points in mind:

- ZFI status is generally reserved for firms exporting the majority of their output

- Zone eligibility and incentive duration are confirmed through a formal investment authorisation from APIEX

- IRPC exemptions apply to zone-registered entities specifically; standard registration outside a zone does not qualify

- Customs exemptions cover inputs, but domestic sales from ZFI entities may trigger duty obligations

Foreign firms operating within a ZFI are not required to have a Mozambican shareholder, meaning full foreign ownership and full tax exemption can apply simultaneously under the same legal structure.

100% Foreign Ownership Permitted in Most Sectors

Mozambique permits 100% foreign ownership Mozambique company benefits across most sectors, meaning your business does not need a local partner to operate legally. This structural feature, grounded in the country's Investment Law (Law No. 3/93, as revised), removes a constraint that remains common across many African jurisdictions.

No Mandatory Local Partner Requirement

Full foreign equity control means you retain complete decision-making authority over your Mozambican entity. Profit repatriation, dividend distribution, and strategic direction all remain within your purview without dilution through a compulsory domestic shareholding arrangement. Under the Investment Law and its supporting regulations, foreign investors are entitled to transfer funds abroad after fulfilling applicable tax obligations.

Mozambique foreign investor ownership rights apply to a wide range of sectors, from services and manufacturing to retail and logistics. Certain industries, including some areas of natural resources extraction, may carry additional licensing conditions, but the default position for most commercial activities is unrestricted foreign ownership.

Practical Implications for Entity Structure

Wholly foreign-owned company advantages become most tangible during the setup phase. You can register a Limitada (Lda.) or a public company (SA) with a 100% foreign shareholding without seeking government approval for the ownership structure itself. This reduces both setup time and the legal costs associated with structuring minority local stakes or partnership agreements.

Foreign ownership rules Mozambique incorporation frameworks apply consistently across all provinces, administered through APIEX and the relevant commercial registries. A single-owner foreign firm is equally valid under the Commercial Code (Decree-Law No. 2/2005).

Structure Your Mozambique Company With Full Foreign Ownership

Get guidance on incorporating a wholly foreign-owned entity in Mozambique and understand your rights under the Investment Law.

Low Labor Costs and Young Workforce Availability

Mozambique low labor costs benefits for businesses are among the more tangible structural advantages for foreign companies establishing operations there. Wage levels are governed by the National Minimum Wage Commission, which sets sector-specific minimums annually. As of recent years, these minimums have remained significantly below regional comparators such as South Africa, making payroll costs for entry-level and mid-skilled positions considerably lower for labor-intensive operations.

- The minimum wage is set by sector rather than as a single national figure, meaning your actual labor cost baseline depends on the industry in which your entity operates, with agriculture and domestic services among the lower bands.

- Approximately 70% of the population is under the age of 35, which means the available labor pool skews toward working age, reducing recruitment competition for foundational roles.

- The Lei do Trabalho (Labor Law No. 23/2007) governs employment contracts, termination procedures, and working conditions, giving foreign firms a codified framework within which to structure hiring.

- For investors in authorized zones, additional flexibility in fixed-term contracting may apply, subject to APIEX approval and the specific investment agreement terms.

Lower base wages, combined with a numerically large young population, mean your firm can scale headcount without the payroll pressure common in more developed regional markets.

Abundant Natural Resources Attract Investment Partners

Mozambique natural resources investment advantages are anchored in geology and geography. The country holds some of the largest natural gas reserves in sub-Saharan Africa, concentrated in the Rovuma Basin off the northern coast, with recoverable estimates exceeding 100 trillion cubic feet. For investors structuring entities to participate in upstream or midstream activities, this positions the country among a small group of African jurisdictions with proven, large-scale hydrocarbon assets actively under development.

Beyond hydrocarbons, the country holds substantial deposits of coal, titanium, graphite, and rubies. The Moatize coal basin in Tete Province has attracted major multinational mining firms, which signals that large-scale extractive operations have already been de-risked through prior foreign participation.

Investments in extractive sectors are governed primarily under Law 14/2017, the Petroleum Law, and Law 20/2014, the Mining Law, both of which define the licensing framework, fiscal terms, and rights available to foreign concession holders. Operating within a codified legal framework gives your firm a defined contractual basis, which reduces exposure to ad hoc regulatory interpretation.

A single LNG train at the Mozambique LNG project anchored by TotalEnergies carries an estimated production capacity of 6.44 million tonnes per annum, illustrating the scale of offtake contracts available to service and supply chain entities incorporated locally.

APIEX Streamlines Business Registration and Licensing

APIEX Mozambique business registration benefits are largely administrative in nature, but their practical effect is significant. The Agency for Investment and Export Promotion (APIEX) serves as a one-stop facility for foreign investors, centralizing approvals that would otherwise require coordination across multiple ministries and public bodies.

Foreign companies can submit registration documents, obtain operating licenses, and receive investment authorization through a single institutional point of contact. This consolidation reduces the time your business spends waiting on cross-departmental bureaucracy before it can legally operate.

APIEX also issues the Investment Authorization required under the Investment Law (Law No. 3/93, as revised), which grants registered investors access to fiscal incentives tied to their approved project. Without this authorization, a foreign entity would not qualify for the tax benefits that Mozambique's investment framework makes available.

- APIEX operates under the Ministry of Economy and Finance

- It processes applications for both the Investment Authorization and Single Authorization (Autorização Única)

- Foreign investors in priority sectors may receive expedited processing

Investment Authorization through APIEX is project-specific, meaning the incentives and protections granted apply only to the approved scope of activity — expanding into new sectors may require a separate application.

Growing Infrastructure Backed by Donor and FDI Funding

Mozambique infrastructure investment advantages for businesses are increasingly concrete, not aspirational. The country has been the recipient of significant capital from multilateral institutions, including the World Bank, the African Development Bank (AfDB), and the United States Government's Millennium Challenge Corporation (MCC), directing funds toward roads, energy grids, and port expansion.

Port and Corridor Access

The Port of Maputo and the Nacala Corridor have both received sustained investment from public and private sources. For a business moving goods regionally, these corridors provide direct rail and road links into landlocked markets including Zambia, Malawi, and Zimbabwe. Functional transit infrastructure reduces logistics costs that would otherwise erode operating margins.

Energy Infrastructure Investment

Electrification projects, including those tied to the Cahora Bassa hydroelectric facility and the developing LNG sector, are expanding grid access to industrial and commercial zones. Reliable power availability at an operational site directly affects production continuity and overhead.

What This Means for Your Business

- Capital expenditure requirements for your firm may be lower where public infrastructure already serves key zones

- Free Industrial Zones (ZFIs) and Industrial Free Zones (ZEIs) are often positioned near upgraded logistics corridors, reducing your site selection complexity

- AfDB and World Bank co-financing signals a degree of sovereign commitment to project completion, which reduces counterparty risk in infrastructure-dependent operations

FDI infrastructure development benefits compound over time. As anchor projects near completion, surrounding commercial activity tends to attract further private capital, which expands supplier and service networks available to your entity.

Why Mozambique Stands Out Among African Incorporation Destinations

Compared against other Southern African incorporation destinations, Mozambique presents a distinct combination of treaty access, ownership rights, and fiscal incentives that neighbouring jurisdictions do not replicate in the same configuration. Countries like South Africa, Tanzania, and Zambia are frequently evaluated by the same category of foreign investor, making them the most relevant points of reference when assessing where to register.

The comparison below isolates parameters where Mozambique's incorporation profile holds a neutral or favourable position. South Africa carries higher corporate compliance costs and a more complex regulatory entry process for foreign-owned entities. Tanzania imposes restrictions on foreign equity in certain sectors and has a less developed SEZ incentive structure. Zambia offers ZIDA investment incentives but lacks equivalent COMESA and SADC dual membership benefits. Across these variables, the Mozambican framework, governed by the Commercial Code and administered through APIEX, offers measurable structural advantages for externally incorporated businesses seeking Southern African market access.

| Parameter | Mozambique | South Africa | Tanzania | Zambia |

|---|---|---|---|---|

| Standard Corporate Tax Rate | 32% (IRPC) | 27% | 30% | 30% |

| 100% Foreign Ownership | Yes (most sectors) | Yes | Restricted in some sectors | Yes |

| SEZ Tax Incentives | Yes (extensive) | Yes (limited) | Yes (limited) | Yes (moderate) |

| SADC Membership | Yes | Yes | Yes | Yes |

| COMESA Membership | Yes | No | Yes | Yes |

| Dual SADC + COMESA Access | Yes | No | Yes | Yes |

Compliance Services for Companies in Mozambique

Meet your ongoing statutory obligations under Mozambican law, including annual filings, tax registration, and regulatory reporting managed by local specialists.

Conclusion

Incorporating in Mozambique offers a coherent set of structural advantages that are grounded in specific legislation and bilateral frameworks, not general emerging market appeal. The combination of the IRPC corporate tax regime, access to SADC and COMESA preferential trade arrangements, and the incentive structures available within designated Special Economic Zones creates a measurable case for foreign entity formation rather than a speculative one.

That case is strongest for businesses whose operations align with the country's resource base, regional trade corridors, or export-oriented manufacturing. A firm entering sectors with no connection to these structural features will find fewer of the benefits described here applicable. Suitability depends on your industry, ownership structure, and tolerance for an operating environment that is still developing its institutional depth.

For those whose business model does align with what this jurisdiction offers, the regulatory framework, including APIEX's centralised registration function and the foreign ownership provisions under the Commercial Code, provides a defined path to legal establishment. The next step is translating that framework into a correctly structured entity that meets both local compliance requirements and your broader corporate objectives.

Start Your Mozambique Company Formation With Expanship Today

Mozambique company formation with Expanship covers the full incorporation cycle for foreign investors, from preparing and legalizing constitutional documents under the Commercial Code (Código Comercial) to registering the entity with the Conservatória do Registo das Entidades Legais (CREL) and obtaining the necessary operating licenses. The benefits outlined across this blog, ranging from IRPC tax rates and SEZ exemptions to SADC preferential access, only translate into operational value once the underlying corporate structure is correctly established and maintained.

Expanship's scope of services for business formation in Mozambique includes:

- Preparation and notarization of pacto social and constitutional documents

- Registered agent and registered office provision for your Lda or SA

- Filing with CREL and liaison with Balcão de Atendimento Único (BAU) for business registration

- Post-incorporation compliance management, including annual returns and statutory filings

- Tax registration with the Autoridade Tributária de Moçambique (AT-M)

- Banking introduction assistance to support account opening for your newly formed entity

Reach out to Expanship Mozambique to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The Imposto sobre o Rendimento das Pessoas Colectivas (IRPC) applies a standard corporate income tax rate of 32% to resident companies on their taxable profit. Entities operating within designated Special Economic Zones or Industrial Free Zones may qualify for reduced rates or multi-year tax exemptions, which are governed by separate legal instruments rather than the IRPC itself. Your effective rate will depend on where and how the business is structured.

Companies granted SEZ or Industrial Free Zone status benefit from significantly reduced corporate tax rates and, in some cases, full exemptions for an initial period. These incentives are established under specific decrees governing each zone and are not automatically available to all businesses registered in Mozambique. Eligibility typically requires minimum investment thresholds and approval from the relevant zone authority.

Membership in both SADC and COMESA gives companies incorporated locally preferential access to a combined market covering much of sub-Saharan and East Africa. SADC's Trade Protocol provides for tariff reductions among member states, while COMESA's Common External Tariff framework creates additional preferential trading conditions. A firm incorporated in Mozambique can use these arrangements to reduce duties on goods traded across participating member countries.

APIEX, the Agency for Investment and Export Promotion, serves as the primary government body facilitating business registration and investment licensing for foreign investors. It operates as a single-window service, coordinating approvals across multiple public entities to reduce the number of separate filings required. For investments above certain thresholds, registration through APIEX is mandatory and also provides access to the investment guarantees available under Mozambican law.

Non-compliance can result in administrative penalties, suspension of operating licenses, or cancellation of investment certificates issued under the investment law. Companies that lose their investment certificate status may also forfeit any associated tax incentives, triggering retroactive tax obligations. The specific consequences depend on the nature of the violation and the regulatory body with oversight authority over the sector in question.

At 32%, the standard IRPC rate is broadly in line with the regional average but not the lowest among Southern African jurisdictions. The comparative advantage for certain investors comes not from the standard rate but from SEZ and Industrial Free Zone incentives, which can substantially reduce the effective tax burden for qualifying entities. Companies not operating within those frameworks should evaluate the overall cost structure, including labor and infrastructure, rather than focusing solely on the headline rate.

Mozambican corporate law does not impose a universal requirement for a locally resident director for all company types, but operational licensing and sector-specific regulations may introduce residency or local representation requirements in practice. Certain regulated industries and investment approvals may require a local contact or representative capable of engaging with public authorities. You should confirm the requirements applicable to your specific corporate form and sector before finalizing your governance structure.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.