Key Takeaways

- Malaysia's corporate framework is governed by the Companies Act 2016 and administered by the Companies Commission of Malaysia (SSM), which also oversees sole proprietorships and partnerships under the Registration of Businesses Act 1956.

- The Private Limited Company (Sendirian Berhad / Sdn Bhd) is the most widely registered business form in Malaysia, available to both resident and foreign-owned businesses.

- Foreign entities entering Malaysia can operate through a branch office, representative office, or regional office without incorporating a local entity, each carrying different regulatory and operational constraints.

- Malaysia operates a territorial tax system, under which foreign-sourced income is generally exempt from domestic corporate tax, though specific rules vary depending on the entity type and nature of activity.

Introduction to Entity Types in Malaysia

Malaysia sits in Southeast Asia, bordered by Thailand to the north and sharing maritime boundaries with Singapore, Indonesia, and the Philippines. A federal constitutional monarchy and independent nation, it operates a territorial tax system — meaning foreign-sourced income is generally not subject to domestic corporate tax, though specific rules apply depending on the entity and activity.

Companies are registered and regulated under the Companies Commission of Malaysia (Suruhanjaya Syarikat Malaysia, or SSM), which administers the Companies Act 2016 as the primary legislative framework governing corporate formation and compliance. Businesses operating as partnerships or sole proprietorships fall under the Registration of Businesses Act 1956, also enforced by the SSM.

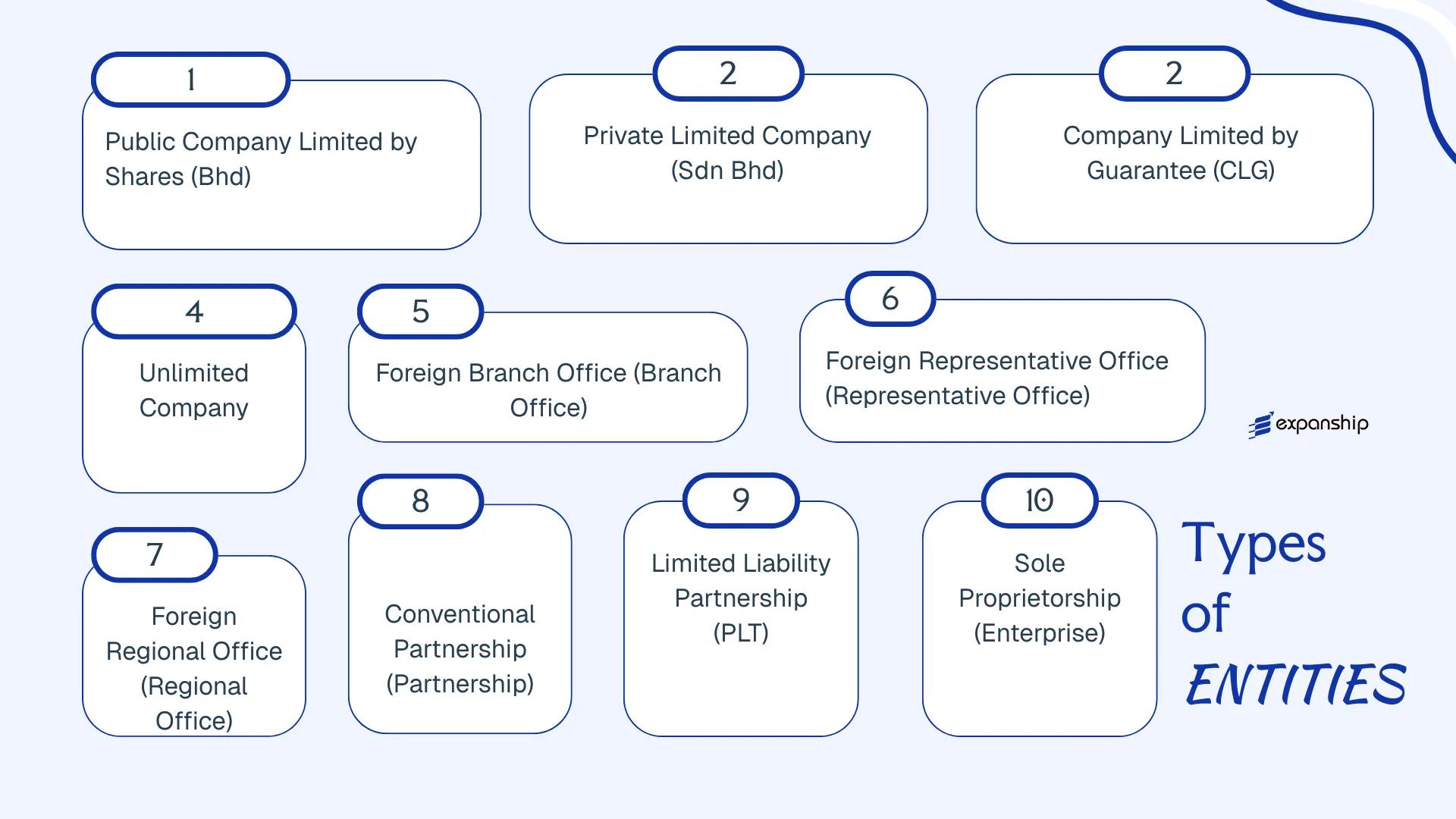

The types of business entities in Malaysia span a range of structures suited to different ownership models, liability preferences, and operational purposes. Available forms include:

- Private Limited Company (Sendirian Berhad / Sdn Bhd)

- Public Company Limited by Shares (Berhad / Bhd)

- Company Limited by Guarantee

- Unlimited Company

- Limited Liability Partnership (PLT)

- Conventional Partnership

- Sole Proprietorship

- Branch Office, Representative Office, and Regional Office

Each structure carries distinct legal, tax, and compliance implications, which the sections below examine in detail.

An Overview of Business Structures in Malaysia

Under the Companies Act 2016 and supplementary legislation such as the Limited Liability Partnerships Act 2012, businesses operating in Malaysia can be structured across several distinct legal forms. The Companies Commission of Malaysia (SSM) serves as the primary registrar for most of these entities. Each structure carries different implications for liability, taxation, membership requirements, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Private Limited Company (Sdn Bhd) | Incorporated company | Limited | Taxed | Yes | 1 shareholder | SSM | Companies Act 2016 |

| Public Limited Company (Bhd) | Incorporated company | Limited | Taxed | Yes | 2 shareholders | SSM / SC | Companies Act 2016 |

| Company Limited by Guarantee (CLG) | Incorporated company | Limited by guarantee | Taxed / Exempt | Restricted | 1 member | SSM | Companies Act 2016 |

| Unlimited Company | Incorporated company | Unlimited | Taxed | Yes | 1 shareholder | SSM | Companies Act 2016 |

| Branch Office | Foreign company | Per parent entity | Taxed | Yes | N/A | SSM | Companies Act 2016 |

| Representative Office | Foreign presence | Per parent entity | Exempt | No | N/A | MIDA / relevant ministry | Guidelines-based |

| Regional Office | Foreign presence | Per parent entity | Exempt | No | N/A | MIDA | Guidelines-based |

| Limited Liability Partnership (PLT) | Hybrid entity | Limited | Taxed | Yes | 2 partners | SSM | LLP Act 2012 |

| Conventional Partnership | Unincorporated firm | Unlimited | Taxed | Yes | 2–20 partners | SSM | Partnership Act 1961 |

| Sole Proprietorship (Enterprise) | Unincorporated | Unlimited | Taxed | Yes | 1 owner | SSM | Registration of Businesses Act 1956 |

Each of these structures is examined in full in the sections below.

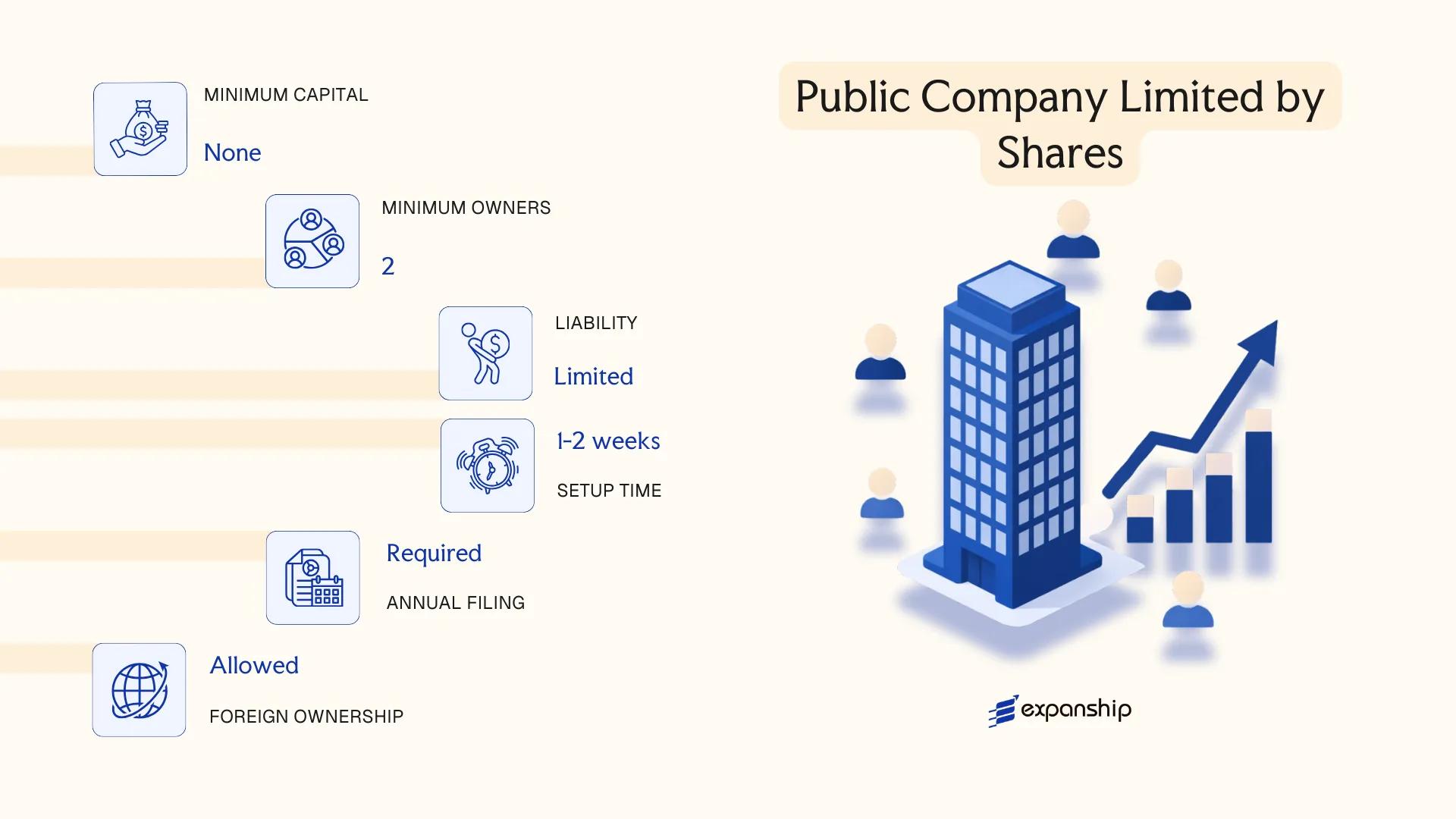

Public Company Limited by Shares (Berhad / Bhd)

Governed by the Companies Act 2016, a Berhad (Bhd) is a separate legal entity whose shareholders bear liability only to the extent of their unpaid shares. A Malaysia Berhad public company setup is the structure of choice when the objective is to raise capital from the general public, whether through a stock exchange listing or a public offering.

Shares in a Bhd are freely transferable, and the entity can offer securities to the public subject to approval from the Securities Commission Malaysia and, for listed firms, compliance with Bursa Malaysia's listing requirements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Company Limited by Shares | Separate legal personality; governed by Companies Act 2016 |

| Members | Shareholders: minimum 1, no maximum | Directors: minimum 2; at least 1 must be ordinarily resident in Malaysia |

| Local Presence | Registered office in Malaysia; company secretary required | Secretary must be a member of a prescribed body (e.g., MAICSA) |

| Capital | MYR; no statutory minimum paid-up capital for incorporation | Listed companies must meet Bursa Malaysia's minimum capital thresholds |

| Share Transferability | Shares freely transferable | No restriction clause permitted in constitution |

| Privacy | Accounts and annual returns filed with SSM; publicly accessible | Lower privacy compared to private entities |

Focus Points

- Taxation: Subject to corporate income tax (generally 24%) administered by the Inland Revenue Board of Malaysia (LHDN); SST may apply to applicable supplies; dividends distributed under the single-tier system carry no further withholding tax at shareholder level; stamp duty applies to share transfers.

- Annual Compliance: Must hold an AGM, file audited financial statements, and lodge an annual return with the Companies Commission of Malaysia (SSM).

- Treaty Access: Eligible for benefits under Malaysia's network of Double Taxation Agreements as a tax-resident entity.

- Conversion: A Bhd can be converted to a private company (Sdn Bhd) under the Companies Act 2016, provided it meets the requisite conditions and shareholder approval.

- Restrictions: Public offering of securities requires a prospectus registered with the Securities Commission Malaysia; foreign ownership restrictions may apply in regulated sectors.

Sub-Types

Listed Company (Bursa Malaysia)

A Bhd that has been admitted to the official list of Bursa Malaysia Securities Berhad. Listing obligations include continuous disclosure requirements, corporate governance compliance under the Malaysian Code on Corporate Governance, and adherence to Bursa Malaysia's Listing Requirements — obligations that do not apply to unlisted Berhad entities.

Unlisted Public Company

Incorporated as a Bhd but not admitted to any exchange. This structure is used where a business requires more than 50 shareholders or needs the ability to offer shares publicly without pursuing a formal exchange listing.

When to Use This Structure

A Bhd suits large enterprises seeking access to public capital markets or those with broad ownership structures that cannot be accommodated within a private company. The primary advantage is unrestricted share transferability and access to equity fundraising. The principal limitation is the compliance burden: mandatory audits, AGMs, public disclosure of financial statements, and securities regulation add considerable administrative cost.

Best suited for established businesses targeting a Bursa Malaysia listing or those requiring a broad shareholder base that exceeds the 50-member ceiling of a private company.

Company Incorporation in Malaysia

Incorporate a Berhad or Sdn Bhd in Malaysia with end-to-end support from entity selection through to SSM registration.

Private Limited Company (Sendirian Berhad / Sdn Bhd)

The Sendirian Berhad is the most widely used business structure for Malaysia Sdn Bhd company registration, governed by the Companies Act 2016 administered by the Companies Commission of Malaysia (SSM). It carries separate legal personality, meaning the company can own assets, enter contracts, and incur liabilities in its own name.

Liability of each member is limited to the amount unpaid on their shares. This protection, combined with the entity's capacity to raise equity and its suitability for both resident and foreign-owned businesses, makes the Sdn Bhd a practical vehicle for a broad range of commercial activities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private company limited by shares | Governed by the Companies Act 2016 |

| Members | Shareholders (min. 1, max. 50) | Single-shareholder companies permitted; shares not offered to the public |

| Management | Directors (min. 1, must be ordinarily resident in Malaysia) | At least one director aged 18+ with a principal place of residence in Malaysia |

| Local Presence | Registered office address in Malaysia (SSM requirement) | Must be a physical address; P.O. boxes not accepted |

| Capital | No minimum paid-up capital for most structures; denominated in MYR | Foreign-owned entities in certain sectors may face capital thresholds set by regulatory agencies |

| Privacy | Beneficial ownership disclosure required to SSM; not publicly searchable | Register of beneficial owners maintained internally and filed with SSM |

Focus Points

- Taxation: Subject to corporate income tax at 24% (SME rate of 15%/17% on chargeable income up to MYR 600,000 where conditions are met); SST applies to applicable goods and services; withholding tax applies to certain payments to non-residents; stamp duty payable on share transfers and certain instruments.

- Annual Compliance: Annual return and audited financial statements filed with SSM; statutory audit mandatory regardless of revenue.

- Treaty Access: Eligible for benefits under Malaysia's double taxation agreements as a tax-resident entity, subject to substance requirements.

- Restrictions: Cannot offer shares to the public or list on a stock exchange; foreign ownership restrictions apply in regulated sectors such as finance, media, and certain professional services.

- Conversion: May be converted to a public company (Berhad) under the Companies Act 2016, subject to SSM approval and structural changes.

Primarily used for trading, holding, and professional services operations, the Sdn Bhd offers the combination of limited liability and a straightforward Sendirian Berhad incorporation process under a single codified statute. The mandatory annual audit adds a recurring compliance cost that sole proprietorships and partnerships do not carry.

Foreign investors and local entrepreneurs seeking a separate legal entity with limited liability for commercial, holding, or service-based operations in Malaysia.

Company Limited by Guarantee (CLG)

A company limited by guarantee Malaysia structures liability differently from share-based entities. Instead of shareholders contributing paid-up capital, members commit to a guaranteed amount — payable only if the company is wound up. Governed by the Companies Act 2016 (CA 2016), this structure carries full separate legal personality, meaning the entity holds its own rights, obligations, and assets distinct from its members.

Incorporated under the Companies Commission of Malaysia (SSM), a CLG operates without share capital by default. It suits organisations where income is applied toward stated objectives rather than distributed as profit.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate | Separate legal personality under CA 2016 |

| Members | Minimum 1; no statutory maximum | Members hold no shares; liability capped at their guaranteed amount |

| Governing Body | Board of Directors; minimum 1 director ordinarily resident in Malaysia | Directors manage operations; members vote on constitutional matters |

| Registered Office | Required in Malaysia | Must be maintained with SSM at all times |

| Share Capital | None | Guarantee amount (typically MYR 1 per member) replaces capital contribution |

| Privacy | Director and member particulars filed with SSM | Publicly searchable via SSM's online registry |

Focus Points

- Taxation: CLGs are subject to standard corporate income tax (24% for resident companies) unless granted tax-exempt status under Section 44(6) of the Income Tax Act 1967; GST/SST obligations apply if thresholds are met; dividend distributions are not applicable given the no-share-capital structure.

- Annual Compliance: Annual returns and audited financial statements must be lodged with SSM; accounts are required regardless of activity level.

- Restrictions: A CLG cannot distribute profits or assets to members during operation; any surplus must be reinvested toward the entity's stated objects.

- Conversion: Conversion from a CLG to a share-based company structure is not permitted under CA 2016.

- Treaty Access: Tax treaty benefits are available where the entity qualifies as a tax resident, though exempt status may affect treaty applicability depending on the treaty terms.

Closing

A CLG is the standard structure for non-profit organisations, professional associations, trade bodies, and charitable foundations requiring legal standing without profit-distribution mechanisms. Its primary advantage is the ability to hold assets and enter contracts as a legal person while shielding members from personal liability beyond their guaranteed sum; the principal drawback is the prohibition on profit distribution, which limits its use to non-commercial or mission-driven purposes.

Best suited for non-profit entities, charities, industry associations, and regulatory or professional bodies that require corporate legal standing without a commercial profit motive.

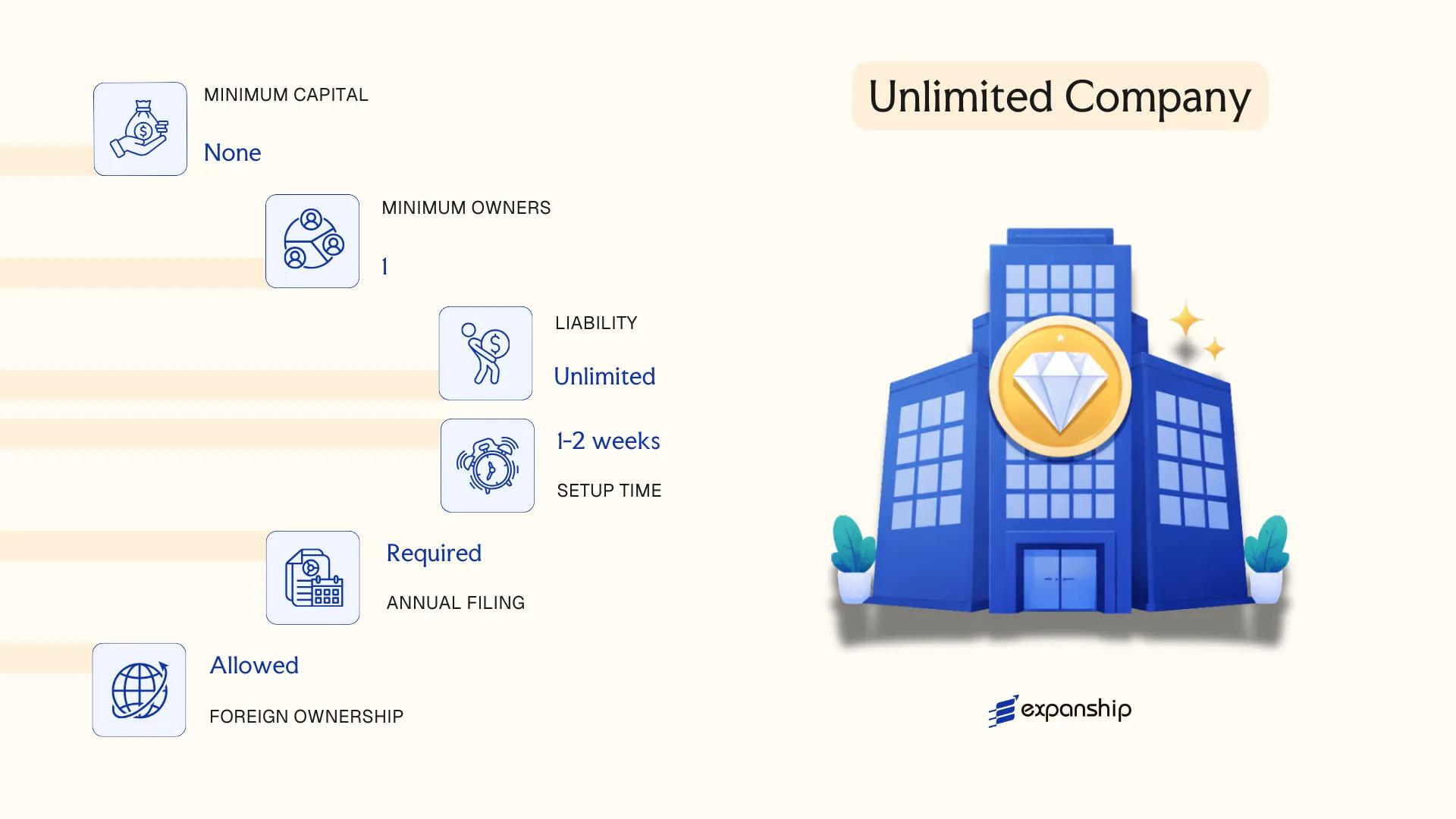

Unlimited Company

Unlimited company registration Malaysia falls under the Companies Act 2016, administered by the Companies Commission of Malaysia (SSM). Unlike a limited company, an unlimited company confers no liability protection to its members — shareholders remain personally liable for the company's debts without any cap.

This structure retains separate legal personality, meaning the entity can sue, be sued, and hold assets in its own name. The absence of a liability ceiling is what separates it from its limited counterparts, making it a structurally distinct form rather than a variation of standard share-based entities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unlimited Company | Registered under the Companies Act 2016 with SSM |

| Members | Shareholders; minimum 1, no statutory maximum | Members bear unlimited personal liability for company debts |

| Directors | Minimum 2 resident directors | Must be ordinarily resident in Malaysia |

| Registered Office | Required in Malaysia | Must maintain a physical registered address with SSM |

| Share Capital | No minimum paid-up capital requirement | Shares may or may not have par value |

| Privacy | Financial statements may have reduced disclosure obligations | One practical reason firms choose this structure |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate (24% for resident companies); SST, withholding tax, and stamp duty obligations apply in the same manner as for limited companies.

- Annual Compliance: Must file annual returns and financial statements with SSM; audit requirements apply under the Companies Act 2016.

- Conversion: An unlimited company may be re-registered as a private limited company under the Companies Act 2016, subject to SSM approval and requisite member resolutions.

- Treaty Access: Qualifies as a Malaysian tax resident entity and may access Malaysia's double taxation agreement network, subject to meeting substance requirements.

- Restrictions: Rarely used for trading or investment purposes given the absence of liability protection; regulated industries may impose additional conditions.

Recommendations

An unlimited company suits scenarios where reduced financial disclosure is operationally valuable, such as certain holding or family-owned structures, though the absence of liability protection represents a significant structural drawback for most commercial purposes.

This entity type is most appropriate for sophisticated investors or family groups who accept personal liability in exchange for greater financial privacy under Malaysian law.

Foreign Company Structures in Malaysia [Branch Office, Representative Office, Regional Office]

Foreign company structures in Malaysia are governed by the Companies Act 2016, which under Part XI sets out the registration requirements for foreign corporations intending to operate within the country. A foreign company that establishes a branch does not create a separate legal entity — it remains an extension of the parent corporation, which retains full legal liability for the branch's activities.

Registration of a foreign company branch is administered by the Companies Commission of Malaysia (SSM). Beyond the branch structure, foreign businesses may also establish a Representative Office or Regional Office, both of which are approved and regulated by the Malaysia Investment Development Authority (MIDA) rather than SSM.

Key Characteristics

| Requirement | Branch Office | Representative Office / Regional Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Administrative presence only; not a separate legal entity |

| Governing Body | Parent company directors; local authorised agent required | Appointed staff; no independent management structure |

| Local Presence | Registered address in Malaysia; named local agent under Companies Act 2016 | Physical office required; approved by MIDA |

| Permitted Activities | Full trading and commercial operations | Liaison, market research, coordination — no revenue-generating activities |

| Capital | No minimum paid-up capital prescribed for branch registration | No capital requirement; funding remitted from parent |

| Privacy | Filed documents publicly accessible via SSM registry | Not publicly registered; details held with MIDA |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at 24%; no separate withholding tax rate applies to branch profit remittances, though payments to the foreign parent may attract withholding tax on royalties, interest, or services under domestic rules or applicable tax treaties.

- Treaty Access: Branches can access Malaysia's tax treaties in principle, but treaty benefits depend on residency determinations — advice specific to the parent's jurisdiction is necessary.

- Annual Compliance: Branches must file audited financial statements with SSM annually; Representative and Regional Offices submit annual reports to MIDA confirming permitted activities and headcount.

- Restrictions: Representative and Regional Offices cannot invoice clients, earn local revenue, or engage in import/export trading; any commercial activity requires conversion to a registered entity.

- Conversion: A branch may be converted into a locally incorporated private limited company (Sdn Bhd), though this requires a separate incorporation process rather than a direct structural conversion.

Sub-Types

Branch Office

A branch office under Part XI of the Companies Act 2016 is registered with SSM and may conduct full commercial and trading operations in Malaysia. The parent company bears unlimited liability for all obligations incurred by the branch.

Representative Office

A Representative Office is approved by MIDA for a fixed term and is restricted to non-revenue activities such as market research, sourcing coordination, and liaison functions. It cannot enter contracts on behalf of the parent or generate income locally.

Regional Office

Functionally similar to a Representative Office, a Regional Office is approved by MIDA for companies coordinating operations across multiple countries in the Asia-Pacific region from a Malaysian base. The permitted activities remain non-commercial, but the scope of coordination is broader in geographic terms.

A branch is suited to foreign firms requiring a direct trading presence without incorporating a local subsidiary, while Representative and Regional Offices serve businesses in a pre-operational or coordination phase. The principal limitation of all three structures is that none confers the liability protection of a separately incorporated entity.

Foreign companies seeking a temporary market presence, regional coordination hub, or a preliminary operational foothold before committing to full local incorporation.

Partnership Structures in Malaysia [Conventional Partnership, Limited Liability Partnership (LLP / PLT)]

Two partnership structures are available for registration: the conventional partnership and the Limited Liability Partnership, known locally as Persatuan Liabiliti Terhad (PLT). For businesses pursuing a Malaysia LLP PLT registration guide, the primary legislative reference is the Limited Liability Partnerships Act 2012, which introduced the PLT as a hybrid entity combining partnership flexibility with a distinct legal personality separate from its partners.

Conventional partnerships, by contrast, are governed by the Partnership Act 1961 and carry no separate legal personality. Partners bear unlimited joint and several liability for the firm's debts, making this structure markedly different from the PLT in terms of risk exposure.

Key Characteristics

| Requirement | PLT (Limited Liability Partnership) | Conventional Partnership |

|---|---|---|

| Legal Form | Separate legal entity with limited liability | No separate legal personality; unlimited liability |

| Members | Partners; minimum 2, no maximum; at least one must be a Malaysian citizen or PR | Partners; minimum 2, maximum 20 (general rule under Partnership Act 1961) |

| Compliance Manager | One designated compliance officer required (must be resident in Malaysia) | No statutory compliance officer required |

| Registered Office | Must maintain a registered address in Malaysia | No formal registered office requirement |

| Capital | No minimum capital requirement; denominated in MYR | No minimum capital requirement |

| Privacy | Names of partners disclosed in public registry via SSM | Names of partners disclosed upon business registration |

Focus Points

- Taxation: PLTs are taxed at corporate income tax rates (generally 24%; SME rates may apply at 17% on first MYR 150,000 if qualifying conditions are met); conventional partnerships are taxed at each partner's individual income tax rate; GST does not currently apply as Malaysia abolished it in 2018, with Sales and Service Tax (SST) applicable where relevant.

- Annual Compliance: PLTs must file an annual declaration with the Companies Commission of Malaysia (SSM); conventional partnerships file annual renewals under the Registration of Businesses Act 1956.

- Conversion: A conventional partnership or company may convert to a PLT under procedures provided in the Limited Liability Partnerships Act 2012.

- Restrictions: PLTs in certain regulated professions (such as legal and accounting) face sector-specific eligibility rules set by the relevant professional bodies.

- Treaty Access: PLTs are generally not eligible for benefits under Malaysia's double taxation agreements, as treaty access is typically reserved for companies.

Sub-Types

Conventional Partnership

Regulated under the Partnership Act 1961, this structure suits small, domestically focused businesses or professional practices where partners accept mutual liability. It offers minimal administrative overhead but provides no liability shield.

Limited Liability Partnership (PLT)

Introduced by the Limited Liability Partnerships Act 2012 and registered with SSM, the PLT suits professional firms and SMEs that require a legal entity with liability protection but prefer a less rigid governance structure than a private limited company.

Closing

The PLT suits professional service firms, consultancies, and SMEs that want legal personality and limited liability without the full compliance burden of a Sdn Bhd, though its exclusion from most tax treaty benefits limits its utility for cross-border structures.

The PLT is best suited for small professional practices and domestic service businesses where partners seek liability protection without the governance formalities of a share-capital company.

Sole Proprietorship (Enterprise)

Sole proprietorship registration Malaysia is governed by the Registration of Businesses Act 1956 (ROBA 1956), administered by the Companies Commission of Malaysia (Suruhanjaya Syarikat Malaysia / SSM). Unlike an Sdn Bhd, this structure carries no separate legal personality — the owner and the business are legally the same entity.

All debts and liabilities of the business fall directly on the proprietor's personal assets. Registration is mandatory for any individual conducting business in Malaysia under this form, and the registration is renewed annually with SSM.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Member Type | Sole Proprietor | One individual only; no partners or shareholders |

| Ownership Restriction | Malaysian citizens and permanent residents only | Foreign nationals are not permitted to register an Enterprise |

| Local Presence | Business address in Malaysia required | Registered with SSM; no separate registered agent requirement |

| Capital | No minimum capital requirement | Funds are personal assets of the proprietor |

| Privacy | Business name and owner details on public SSM record | Less privacy than a private company structure |

Focus Points

- Taxation: Business income is assessed as personal income under the Income Tax Act 1967 at individual tax rates (0–30%); no corporate tax, though SST obligations may apply depending on the activity.

- Annual Compliance: Business registration must be renewed yearly with SSM; no annual return or audited financial statements required.

- Conversion: An Enterprise can be converted to an Sdn Bhd, though assets and contracts must be formally transferred as there is no automatic continuity of legal identity.

- Restrictions: Restricted to Malaysian citizens and permanent residents; foreign-owned businesses cannot use this structure.

- Treaty Access: As a non-incorporated entity, it does not access double taxation agreements at the entity level; treaty benefits, where applicable, flow through the individual proprietor.

Closing

An Enterprise suits small-scale, low-risk local trading or service businesses where administrative simplicity is the primary consideration; the absence of liability protection is a significant structural drawback for any business carrying financial or legal exposure.

Best suited for Malaysian citizens or permanent residents running small local businesses with minimal liability risk and no plans for external investment or foreign ownership.

How to Choose the Right Entity Type in Malaysia

Selecting the wrong business structure in Malaysia carries concrete legal and financial consequences that can be difficult to reverse once operations have begun.

Why Your Entity Choice Matters

- Registering a foreign company branch when you intend to conduct long-term local trade without complying with Section 561 of the Companies Act 2016 can result in penalties or striking off by the Companies Commission of Malaysia (SSM).

- Choosing a Company Limited by Guarantee, which is exempt from corporate income tax on qualifying income, disqualifies your entity from claiming reduced withholding tax rates under Malaysia's double taxation agreements.

- Forming a private limited company when your needs are primarily estate planning or asset protection creates ongoing annual shareholder obligations — including AGM requirements and statutory filings — that do not apply to foundations or trusts.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or fund management each require distinct structures under SSM and sector-specific licensing frameworks.

- Ownership and Management: A sole operator may find a sole proprietorship or LLP sufficient, while multi-party ventures requiring formal governance need the Sdn Bhd structure.

- Tax Objectives: Your need for treaty access, a specific incentive regime, or full tax exemption will determine which entity qualifies.

- Substance Capacity: If you cannot maintain a physical presence, employees, or local decision-making, you must account for whether your chosen structure triggers substance reporting obligations.

- Exit Strategy: Not all entity types permit redomiciliation or conversion; confirm your structure supports your intended exit mechanism before incorporation.

Corporate Compliance Services in Malaysia

Ongoing compliance support for companies registered in Malaysia, including annual filings, statutory maintenance, and SSM obligations.

Conclusion

Selecting the right structure is a foundational decision in any Malaysia company incorporation summary, as each entity carries distinct legal, tax, and operational consequences under the Companies Act 2016 and related legislation. The Sdn Bhd remains the most widely registered business form in the country, favored by resident and foreign-owned businesses alike. Public companies suit large-scale capital-raising ambitions; companies limited by guarantee serve non-profit and membership-based purposes. Unlimited companies offer unrestricted profit distribution at the cost of member liability. For foreign entrants, branch and representative offices provide market access without local incorporation. Partnerships and sole proprietorships address smaller-scale or professional service needs.

Registrations are administered through the Companies Commission of Malaysia (SSM), and the regulatory framework has continued to align with international standards on beneficial ownership disclosure and anti-money laundering. Your choice of entity shapes everything from governance obligations to how profits are extracted.

How Expanship Can Assist You

Expanship provides corporate services Malaysia company setup clients rely on across the full incorporation lifecycle — from choosing between an Sdn Bhd, a Branch Office, or a Limited Liability Partnership, through to filing with the Companies Commission of Malaysia (SSM). Each engagement is structured around your specific entity type, ownership requirements, and operational intent.

Across that process, Expanship handles the practical and administrative work so your business moves forward without delays:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision in Malaysia

- SSM filing and ongoing registrar liaison

- Post-incorporation compliance management, including annual returns and statutory records

- Director and company secretary appointment support

- Banking introduction assistance for corporate account opening

Every service is coordinated by professionals familiar with Malaysian regulatory requirements, not outsourced to generalist agents.

Ready to incorporate in Malaysia? Reach out directly through Expanship Malaysia to discuss your structure.

Frequently Asked Questions (FAQ)

The Sdn Bhd (Sendirian Berhad), or private limited company, is the most frequently incorporated entity under the Companies Act 2016. Its combination of limited liability, separate legal personality, and permissibility of full foreign ownership makes it the default structure for most commercial purposes.

A branch office is not a separate legal entity; liabilities flow back to the parent corporation. An Sdn Bhd, once incorporated, stands as a distinct legal person, which generally reduces parent-company exposure and may simplify local banking and contract arrangements.

Among registered structures, a Company Limited by Guarantee (CLG) typically involves fewer publicly disclosed shareholder interests, since members hold no transferable shares. Nominee director and shareholder arrangements are permissible for Sdn Bhd entities, though beneficial ownership disclosure obligations apply under the Companies Act 2016.

No. A sole proprietorship and a single-member Sdn Bhd are both available to one individual, but a conventional partnership requires at least two partners, and a Limited Liability Partnership (PLT) under the Limited Liability Partnerships Act 2012 also requires a minimum of two partners.

Foreigners may incorporate an Sdn Bhd with 100% foreign ownership in most sectors, subject to any sector-specific equity conditions. Branch offices and representative offices are also available to foreign corporations, though representative offices are restricted from revenue-generating activities.

The Companies Act 2016 provides a formal conversion mechanism allowing an unlimited company to re-register as a company limited by shares, and a private company may convert to a public company (Berhad) through a prescribed process with the Companies Commission of Malaysia (SSM). Conversion between fundamentally different structures, such as from a partnership to a company, generally requires dissolution of the original entity and fresh incorporation.

No. Sole proprietorships and conventional partnerships do not carry separate legal personality; the owner or partners bear personal liability for business obligations. Sdn Bhd, Berhad, CLG, and PLT structures are each recognised as distinct legal persons under their respective governing statutes.

A sole proprietorship registered under the Registration of Businesses Act 1956 carries the lightest compliance burden, with no statutory audit requirement and minimal annual filing obligations. By contrast, both private and public limited companies must maintain statutory registers, file annual returns, and in most cases appoint an auditor under the Companies Act 2016.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.