Key Takeaways

- All commercial entities in Mexico must have their deed of incorporation formalized by a Mexican Notario Público before registration can proceed through the Registro Público de Comercio.

- Under the Ley General de Sociedades Mercantiles, foreign investors forming a Sociedad Anónima de Capital Variable (S.A. de C.V.) or Sociedad de Responsabilidad Limitada (S. de R.L.) must satisfy entity-specific structural and capital requirements as a condition of obtaining legal standing.

- Companies with foreign ownership are subject to beneficial ownership disclosure obligations under the SAT's UBO regime, adding a compliance layer beyond standard commercial registration.

- Prior to registration, any proposed company name must receive authorization from the Secretaría de Economía, making name clearance a mandatory step in the incorporation process rather than an administrative formality.

Entity formation in Mexico is governed by the Ley General de Sociedades Mercantiles (General Law of Commercial Companies), with the Secretaría de Economía and the Registro Público de Comercio overseeing registration at the federal level. Meeting the incorporation requirements in Mexico is a prerequisite to obtaining legal standing as a business entity.

This article covers the structural, documentary, and compliance requirements that apply across the formation process, from capital thresholds to beneficial ownership obligations.

Failure to satisfy these conditions results in rejection of the registration application or, in cases of ongoing non-compliance, exposure to administrative penalties under Mexican commercial law. Specific requirements may also differ depending on the entity type selected, the industry sector involved, and whether foreign capital is present in the ownership structure.

Foreign investors and business owners directing capital into the Mexican market, particularly those forming a Sociedad Anónima de Capital Variable (S.A. de C.V.) or a Sociedad de Responsabilidad Limitada (S. de R.L.), will find this article most directly applicable to their situation.

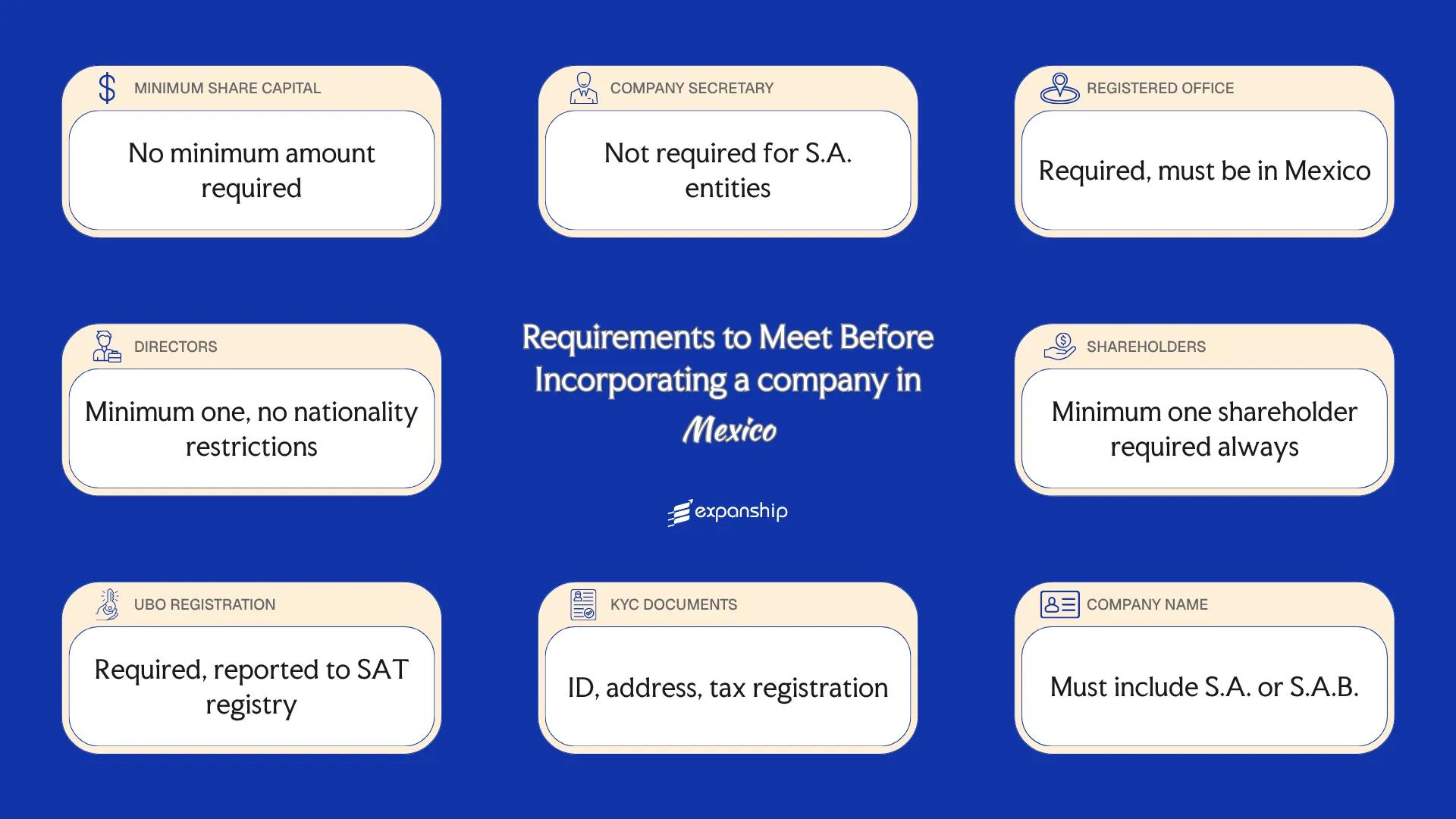

Minimum Share Capital Requirements in Mexico

Minimum share capital requirements in Mexico vary by entity type and are governed primarily by the Ley General de Sociedades Mercantiles (LGSM). Both the Sociedad Anónima de C.V. (SA de CV) and the Sociedad de Responsabilidad Limitada (SRL de CV) operate on a par value share system, where each share carries a stated nominal value.

Capital contributions are recorded at the point of incorporation through the public deed executed before a Notario Público, which is then registered with the Registro Público de Comercio. This is primarily a one-time incorporation requirement, though any subsequent capital changes must be reflected in amended articles and re-registered.

| Parameter | Detail |

|---|---|

| Minimum Authorized Share Capital | MXN 50,000 for SA de CV under the LGSM |

| Maximum Authorized Share Capital | No statutory maximum |

| Minimum Paid-Up Capital | 20% of subscribed capital at incorporation |

| Paid-Up Requirement at Incorporation | Yes; partial payment permitted, balance callable by the board |

| Accepted Currency | Mexican Peso (MXN); foreign currency permissible with peso equivalence declared |

| Accepted Forms of Contribution | Cash or in-kind contributions; in-kind assets must be appraised |

| Timeframe to Deposit Capital | At the time of executing the incorporation deed |

A low or nominal authorized capital figure does not eliminate the obligation to define a formal capital structure in the incorporation deed. The Registro Público de Comercio requires a fully documented capital breakdown before registration is accepted.

Company Secretary Requirements in Mexico

Under Mexican corporate law, the company secretary requirements Mexico imposes apply specifically to Sociedades Anónimas (SAs) and Sociedades Anónimas de Capital Variable (SA de CVs). The secretary, known as the secretario de actas, is appointed by the board of directors and holds a formal role distinct from a registered agent.

Mexico corporate secretary obligations include recording minutes of shareholder and board meetings, certifying resolutions, and maintaining the corporate books required under the Ley General de Sociedades Mercantiles. The secretario de actas also authenticates documentation presented to third parties and government authorities such as the Servicio de Administración Tributaria (SAT).

Qualification criteria for who may serve as secretary:

- No statutory requirement for the secretary to be a Mexican national or resident

- The role may be filled by an individual or, in some structures, a legal entity

- The secretary need not be a licensed attorney, though legal training is common in practice

- Board membership is not required; the secretary may be an external appointee

- No government licensing or prior registration with a regulatory body is mandated for the position

Incorporate a Company in Mexico

Set up your legal entity in Mexico with full compliance support, from notarial deed preparation to SAT registration.

Registered Office Requirements in Mexico

Registered office requirements in Mexico are governed by the Código de Comercio and the Ley General de Sociedades Mercantiles, which together require every company to maintain a domicilio fiscal — a registered fiscal address — that corresponds to a real, physically verifiable location within the country. Non-compliance with domicilio fiscal requirements can result in the Servicio de Administración Tributaria (SAT) classifying your entity as a "non-locatable taxpayer," which triggers suspension of tax certificates, cancellation of digital tax invoicing (CFDI) capabilities, and potential deregistration.

- A physical address is required; PO boxes are not accepted as a valid domicilio fiscal.

- Virtual offices may be used if the address can be physically verified by SAT during an inspection visit.

- The address must be located within Mexico; foreign addresses do not satisfy this requirement.

- A lease agreement, title deed, or equivalent proof of occupancy must be available to substantiate the address.

- The registered address is recorded with the Registro Público de Comercio and is publicly accessible.

- Any change of address must be formally notified to SAT and updated in the Registro Público de Comercio within the statutory period to avoid compliance gaps.

Director Requirements in Mexico

Under Mexico's Ley General de Sociedades Mercantiles (LGSM), director requirements Mexico company structures must satisfy vary depending on whether the entity adopts a sole administrator (administrador único) or a board of directors. Upon appointment, directors assume fiduciary duties toward the company and its shareholders, including the duty of loyalty and the duty of care, and bear personal liability for acts carried out outside the scope of their authority or in violation of corporate statutes.

| Parameter | Detail |

|---|---|

| Minimum Number of Directors | One director (or administrador único) is sufficient for an S. de R.L. or S.A. |

| Maximum Number of Directors | No statutory maximum; the number is typically defined in the company's estatutos sociales. |

| Local/Resident Director Required | No statutory requirement for a Mexican resident or locally domiciled director. |

| Nationality Restrictions | No nationality restrictions apply under the LGSM. |

| Minimum Age Requirement | Directors must have legal capacity under Mexican civil law, which generally requires a minimum age of 18 years. |

| Corporate Directors Permitted | The LGSM does not expressly permit corporate entities to serve as directors; natural persons are the standard requirement. |

| Director Must Be a Shareholder | No statutory requirement, though the estatutos sociales may impose this condition internally. |

| Publicly Listed on Registry | Directors of S.A. companies are recorded in the Registro Público de Comercio as part of the corporate filing. |

| Disqualification Conditions | Persons declared bankrupt, convicted of fraud, or otherwise legally incapacitated under Mexican law are disqualified from serving. |

Unlike many civil law jurisdictions, Mexico permits a single foreign individual with no local ties to serve as the sole administrador único of an S.A. or S. de R.L., with no resident co-director required by statute.

Shareholder Requirements in Mexico

Under the Ley General de Sociedades Mercantiles (LGSM), a Sociedad Anónima de Capital Variable (SA de CV) requires a minimum of two shareholders, with no statutory maximum. A sole shareholder structure is not permitted for this entity type.

Nationality and Residency Restrictions

Meeting shareholder requirements Mexico incorporation rules impose is straightforward on the nationality front: neither residency nor Mexican nationality is required of shareholders. Foreign nationals and foreign-domiciled persons may hold shares without restriction, subject to any sector-specific foreign investment limits set by the Ley de Inversión Extranjera and administered by the Comisión Nacional de Inversiones Extranjeras (CNIE).

Corporate Shareholders

Corporate entities may act as shareholders in a Mexican SA de CV. No conditions specific to the corporate shareholder's jurisdiction of incorporation are imposed under the LGSM, though sector restrictions under foreign investment law may apply where the corporate shareholder is foreign-owned.

Shareholder Liability

Liability for socios in an SA de CV is limited to each shareholder's subscribed capital contribution. Personal assets are not exposed under ordinary circumstances.

Register of Shareholders

The firm must maintain a private registro de accionistas. This record is not publicly accessible, but must be updated upon any transfer of shares or change in shareholding structure.

Shareholder Structuring Support for Your Mexican Entity

Get guidance on meeting shareholder requirements when setting up a company in Mexico, including foreign ownership rules and registro de accionistas obligations.

UBO / Beneficial Ownership Registration Requirements in Mexico

Under Mexico's beneficial ownership registration framework, the beneficiario controlador regime is governed by reforms to the Código Fiscal de la Federación (CFF), effective January 2022, which define a beneficial owner as any individual holding 25% or more of equity or control, directly or indirectly.

- Identify all individuals meeting the 25% ownership or control threshold under Article 32-B Ter of the CFF.

- Compile the required identifying information for each beneficiario controlador, including full name, tax identification, nationality, and nature of the controlling interest.

- File and maintain this information in your entity's internal registry, which must be kept current and available for SAT review upon request.

- Submit the beneficial ownership data to the SAT when formally requested during a tax audit or compliance review.

| Parameter | Detail |

|---|---|

| Ownership Threshold for UBO Status | 25% of equity or control, directly or indirectly |

| Filing Authority | Servicio de Administración Tributaria (SAT) |

| Disclosure Deadline at Incorporation | No fixed statutory deadline at incorporation; records must exist from the moment of formation |

| Publicly Accessible Register | No |

| Penalties for Non-Disclosure | Fines ranging from MXN 1,500,000 to MXN 2,000,000 under the CFF |

| Ongoing Update Obligation | Yes; records must be updated within 15 days of any change |

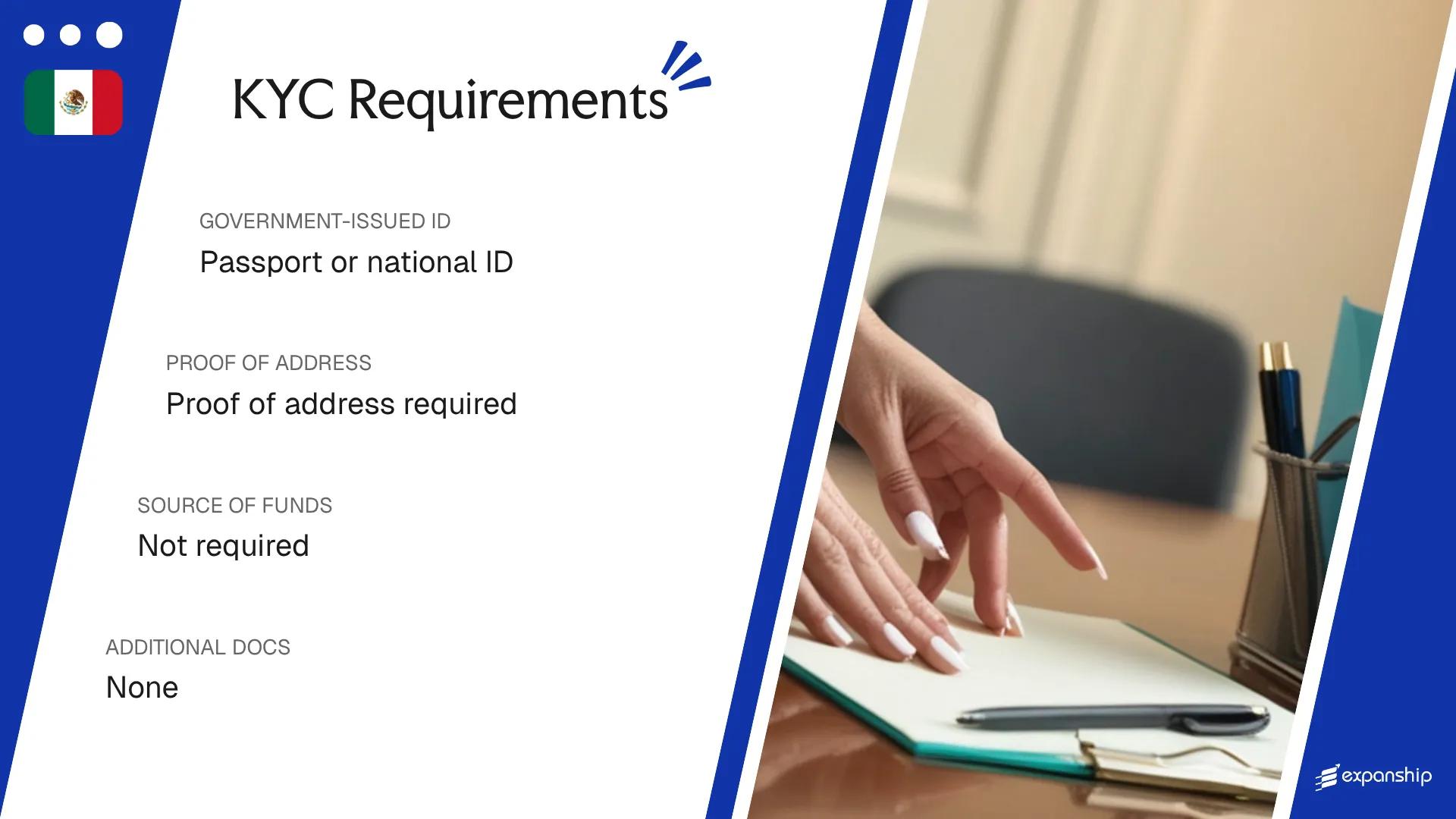

KYC / Document Requirements in Mexico

KYC document requirements for a Mexico company formation are governed by the Ley Federal para la Prevención e Identificación de Operaciones con Recursos de Procedencia Ilícita (LFPIORPI), with oversight exercised by the UIF.

Individual / Personal Documents

- Valid government-issued photo identification (INE credential, passport, or consular ID)

- Proof of residential address dated within three months (utility bill or official bank correspondence)

- Mexican tax identification number (RFC) where the individual holds one, or a foreign equivalent

- Completed know-your-customer form disclosing the individual's nationality, occupation, and beneficial ownership status

Corporate Documents

- Certificate of incorporation or equivalent constitutive document from the entity's home jurisdiction

- Current register of directors or equivalent officer list

- Proof of the corporate entity's registered address in its home jurisdiction

- Constitutional documents, such as articles of association or bylaws, confirming the firm's ownership structure

Source of Funds Documentation

- Recent bank statements (typically covering the preceding three to six months)

- Audited financial statements or accountant's letter where bank statements are insufficient

- Documentary evidence of the specific transaction or event generating the capital being introduced

Notarisation and Apostille Requirements

- Foreign public documents must generally be apostilled under the Hague Convention before submission

- Certified Spanish translations are required for all documents issued in a foreign language

- A Mexican notario público (notary) must authenticate or ratify certain documents at the incorporation stage

Submission of foreign documents without a certified Spanish translation is among the most common reasons for delays in the incorporation process before the Registro Público de Comercio.

Company Name Requirements in Mexico

Prior to registration, proposed company names in Mexico are reviewed to confirm they meet federal requirements for distinctiveness and clarity. Meeting the company name requirements Mexico sets out is a prerequisite before incorporation documents can be processed.

Structurally, a name must include the appropriate legal suffix corresponding to the entity type, such as "S.A. de C.V." for a variable capital stock corporation. Spanish is the standard language, though foreign words are permitted provided the name remains intelligible.

Certain words are outright prohibited or require prior government authorisation before use. Terms implying a connection to federal or state institutions fall into the restricted category.

Name reservation is available through the Secretaría de Economía via its online portal. A reservation is typically valid for a limited period, after which it must be renewed or the name lapses.

Compliance Services for Companies in Mexico

Maintain your Mexican entity's legal standing with ongoing compliance support, from annual filings to regulatory reporting obligations.

Conclusion

Mexico company incorporation requirements are defined across several legal instruments, with the Ley General de Sociedades Mercantiles governing the formation of most commercial entities, including the widely used Sociedad de Responsabilidad Limitada and Sociedad Anónima. Among the requirements covered, the mandatory use of a Mexican notary public (Notario Público) to formalize the deed of incorporation and the Secretaría de Economía's name authorization process are particularly consequential for foreign investors. Beneficial ownership registration under the SAT's UBO regime adds a further compliance layer. Once these requirements are understood, the practical work of executing formation, securing registrations, and establishing local administrative structures begins.

Expanship's Corporate Services for Mexico Expansion

Forming a business in Mexico involves a specific set of regulatory obligations, from notarial deed execution before a Mexican Notario Público to SAT tax registration and UBO disclosure under the Anti-Money Laundering Law. Expanship's Mexico company formation services are structured around these local requirements, reducing the coordination burden your team would otherwise carry across multiple government bodies and legal processes.

Beyond initial registration, our support covers the full establishment and maintenance cycle:

- We prepare and file all incorporation documents, including the acta constitutiva and company bylaws, with the relevant authorities.

- Our registered agent and office provision satisfies Mexico's local address and representation requirements.

- We liaise directly with the SAT, Registro Público de Comercio, and other regulatory bodies on your behalf.

- Post-incorporation compliance management keeps your entity in good standing under Mexican law.

- Banking introduction assistance connects your business with suitable financial institutions operating in Mexico.

- Tax registration and coordination with local authorities ensures your entity meets its federal and state obligations from day one.

To discuss how we can support your Mexico expansion, contact Expanship Mexico.

Frequently Asked Questions (FAQ)

A foreign national can serve as the sole administrator or as part of a board of directors of a Mexican entity without requiring a Mexican co-director, provided they hold a valid immigration status that permits business activities in the country. Under Mexican law, there is no statutory nationality requirement for directors, but immigration compliance under the Ley de Migración must be satisfied before assuming active management responsibilities. Failing to meet immigration conditions does not invalidate the directorship legally, but it exposes the individual to administrative penalties.

Failure to register beneficial ownership information with the Servicio de Administración Tributaria (SAT) as required under the reforms to the Código Fiscal de la Federación can result in fines and restrictions on the company's tax standing. The SAT has authority to impose economic sanctions and, in cases of repeated non-compliance, suspend the entity's tax identification (RFC), which effectively halts the firm's ability to issue invoices or enter into formal contracts. All entities with foreign ownership or complex shareholding structures are subject to these obligations, not only large corporations.

A notarized deed (escritura constitutiva) executed before a Mexican notario público is mandatory for all standard commercial entities, including the S.A. de C.V. and S. de R.L. de C.V., as required by the Ley General de Sociedades Mercantiles. The notario público does not simply authenticate signatures but formally constitutes the entity by drafting and certifying the articles of incorporation, which are then registered with the Registro Público de Comercio. Skipping this step means the entity has no legal existence under Mexican commercial law, regardless of any other filings completed.

The Secretaría de Economía (SE) is the authority that approves company names in Mexico, and it will reject any name that duplicates or closely resembles an already-registered entity or that includes prohibited terms under the Ley General de Sociedades Mercantiles. Names must clearly reflect the entity type through the corresponding suffix, such as S.A. de C.V. or S. de R.L. de C.V., and cannot include references to government bodies or terms that imply state affiliation. Approval must be obtained before the notario público can execute the incorporation deed.

A minimum of two shareholders is required to incorporate an S.A. de C.V. or S. de R.L. de C.V. under the Ley General de Sociedades Mercantiles, meaning a single foreign investor cannot hold 100% of shares at incorporation without a second shareholder. That second shareholder can hold as little as one share, and there is no requirement for them to be a Mexican national. If sole ownership is the objective, structuring options exist, but they require specific legal arrangements that go beyond standard incorporation.

Foreign directors and shareholders typically must provide a notarized and apostilled copy of their passport, proof of foreign address, and a tax identification number from their country of residence as part of the KYC process during incorporation. If the shareholder is a corporate entity rather than an individual, certified constitutional documents and a certificate of good standing from the home jurisdiction are required, also apostilled in accordance with the Hague Convention. These documents must meet the standards set by the notario público handling the incorporation and, where applicable, satisfy FINCEN-equivalent anti-money laundering obligations under Mexico's Ley Federal para la Prevención e Identificación de Operaciones con Recursos de Procedencia Ilícita.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.