Key Takeaways

- Malta's company registration framework is administered by the Malta Business Registry under the Companies Act (Cap. 386), which governs all legal entity types available in the jurisdiction.

- The private limited liability company (Ltd) is the most commonly registered entity form in Malta, valued for combining liability protection with manageable administrative requirements.

- Partnerships en nom collectif and en commandite offer pass-through tax treatment, distinguishing them from the corporate imputation system that applies to limited liability companies.

- Foreign firms can enter the Maltese market through a branch or representative office before committing to full incorporation, providing a lower-commitment testing structure under Maltese law.

Introduction to Entity Types in Malta

Malta is an archipelago in the central Mediterranean, situated south of Sicily and north of the Libyan coast. An independent republic and EU member state since 2004, it operates a civil law legal system that draws from both English common law traditions and continental influences — a duality reflected directly in its available business entity types in Malta.

Company registration falls under the authority of the Malta Business Registry (MBR), which administers the Companies Act (Cap. 386) and maintains the official register of legal persons. The tax framework is treaty-based, with an imputation system that can significantly affect the net tax burden for qualifying shareholders.

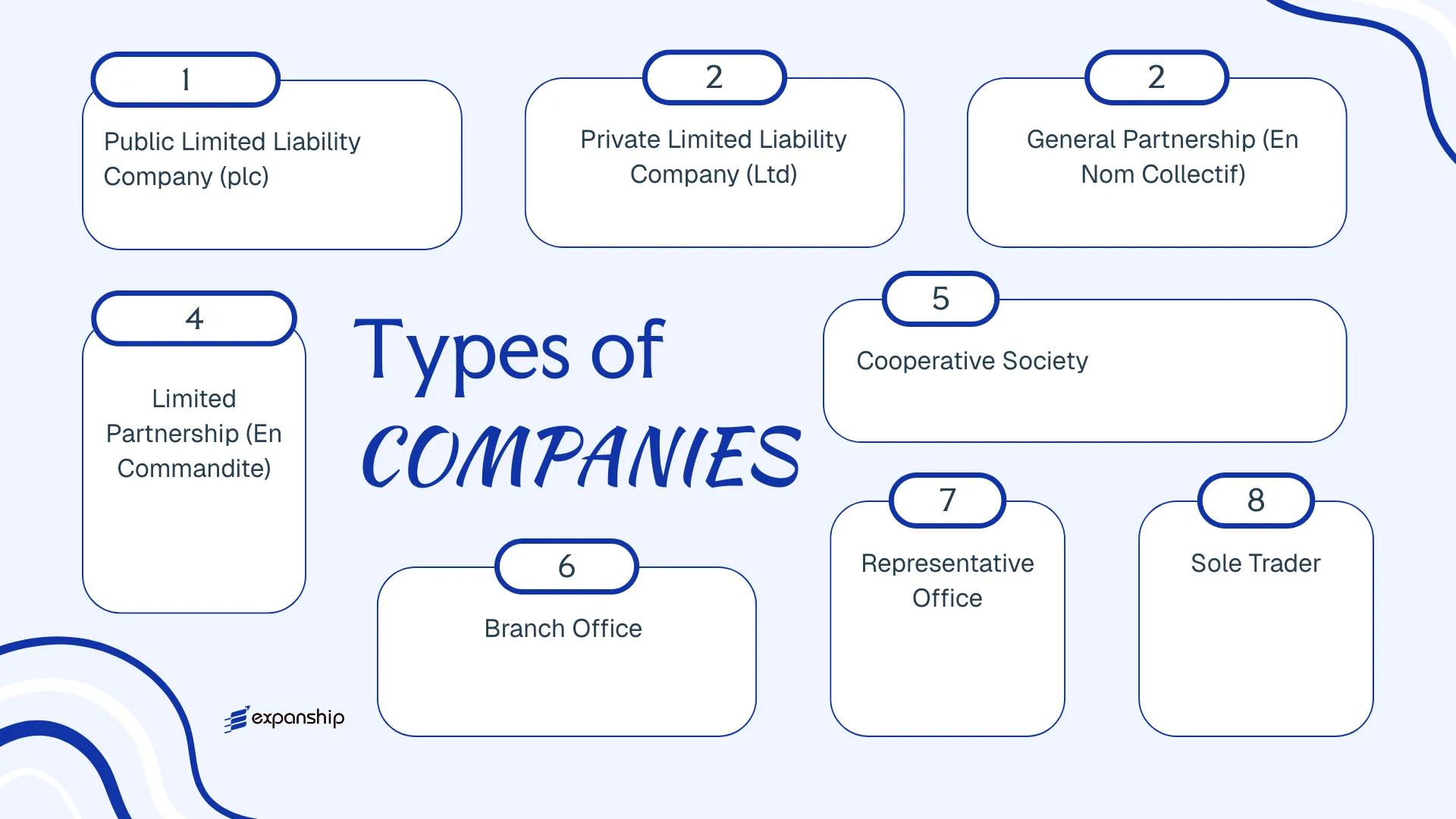

Firms operating in or through this jurisdiction may register under several distinct legal forms: Private Limited Liability Company (Ltd), Public Limited Liability Company (plc), General Partnership (En Nom Collectif), Limited Partnership (En Commandite), Cooperative Society, Branch Office, Representative Office, and Sole Trader.

Each structure carries different requirements around share capital, liability, governance, and regulatory obligations. This article examines each form in detail so your business can assess which structure fits its operational and legal requirements.

An Overview of Business Structures in Malta

Malta's company law framework provides several distinct entity types, each governed primarily by the Companies Act (Cap. 386 of the Laws of Malta), with additional provisions under the Civil Code and the Co-operatives Societies Act for non-corporate structures. Registered and supervised through the Malta Business Registry (MBR), these structures range from sole trader arrangements to publicly listed companies. Each form carries a different liability profile, tax treatment, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (plc) | Corporate | Limited | Taxed | Yes | 2 shareholders | Malta Business Registry | Companies Act (Cap. 386) |

| Private Limited Company (Ltd) | Corporate | Limited | Taxed | Yes | 1 shareholder | Malta Business Registry | Companies Act (Cap. 386) |

| General Partnership (En Nom Collectif) | Partnership | Unlimited | Taxed | Yes | 2 partners | Malta Business Registry | Companies Act (Cap. 386) |

| Limited Partnership (En Commandite) | Partnership | Mixed | Taxed | Yes | 2 partners | Malta Business Registry | Companies Act (Cap. 386) |

| Cooperative Society | Cooperative | Limited | Taxed | Yes | 3 members | Malta Business Registry | Co-operative Societies Act (Cap. 442) |

| Branch Office | Foreign Entity | Parent liable | Taxed on local income | Yes | N/A | Malta Business Registry | Companies Act (Cap. 386) |

| Representative Office | Foreign Entity | Parent liable | Generally exempt | Restricted | N/A | Malta Business Registry | Companies Act (Cap. 386) |

| Sole Trader | Unincorporated | Unlimited | Taxed | Yes | 1 individual | Malta Business Registry | Civil Code / VAT Act |

Each of these structures is examined in full in the sections below.

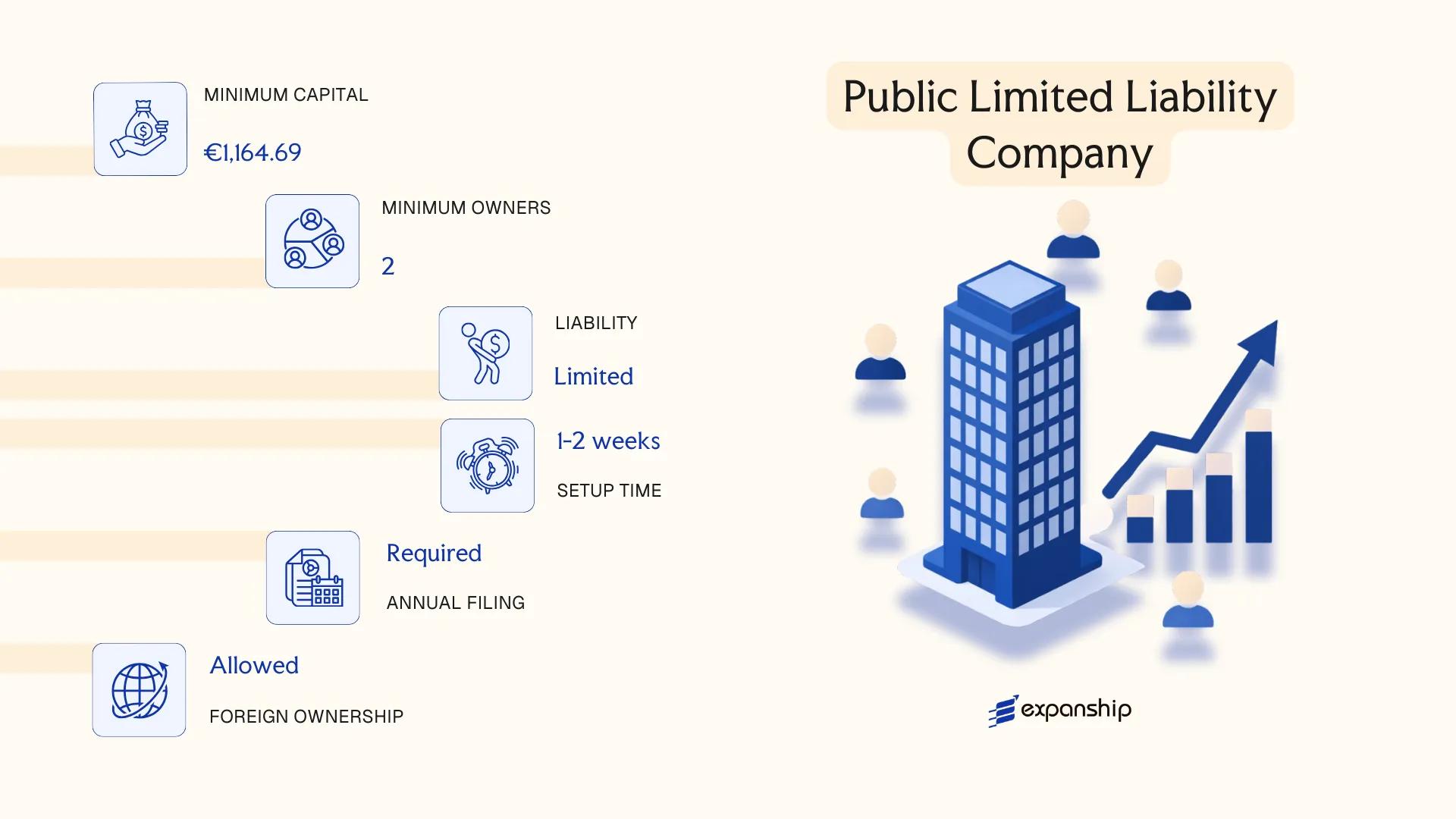

Public Limited Liability Company (plc)

Governed by the Companies Act (Chapter 386 of the Laws of Malta), a Malta public limited liability company (plc) carries separate legal personality distinct from its shareholders. Liability is limited to each member's capital contribution.

Shares in a plc may be offered to the general public, and listing on the Malta Stock Exchange is permissible, which distinguishes this structure from its private counterpart.

Company Incorporation in Malta

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Liability Company (plc) | Separate legal personality; governed by Chapter 386 |

| Members | Shareholders; minimum 2, no maximum | Directors: minimum 2; a company secretary is also required |

| Minimum Share Capital | €46,587.47 (at least 25% paid up on incorporation) | Capital must be denominated in euros or another stated currency |

| Local Presence | Registered office in Malta required | No mandatory resident director, but a registered address is obligatory |

| Shares | Freely transferable; public offering permitted | May apply for listing on the Malta Stock Exchange |

| Privacy | Shareholder and director details filed at the Malta Business Registry | Publicly searchable records |

Focus Points

- Taxation: Subject to the standard 35% corporate tax rate; Malta's full imputation system allows shareholders to claim refunds of up to 6/7ths of tax paid; VAT registration is required where applicable; no withholding tax on dividends to non-residents in most cases; stamp duty applies to share transfers at 2% generally.

- Annual Compliance: Annual return and audited financial statements must be filed with the Malta Business Registry; statutory audit is mandatory regardless of size.

- Treaty Access: Qualifies for Malta's extensive double tax treaty network (70+ agreements), provided substance requirements are met.

- Economic Substance: No statutory minimum substance rules specific to plcs, but treaty benefits and tax refund claims are subject to anti-abuse provisions under the Income Tax Act.

- Conversion: A plc may be converted to a private limited company provided it no longer meets the criteria for public status, subject to shareholder resolution and Registry approval.

Closing

A plc suits large-scale trading operations, businesses seeking public investment, or entities targeting a stock exchange listing; the mandatory audit requirement and higher capital threshold make it less practical for small or closely held businesses.

This structure is most appropriate for established businesses seeking to raise capital from the public or pursuing a regulated market listing in Malta.

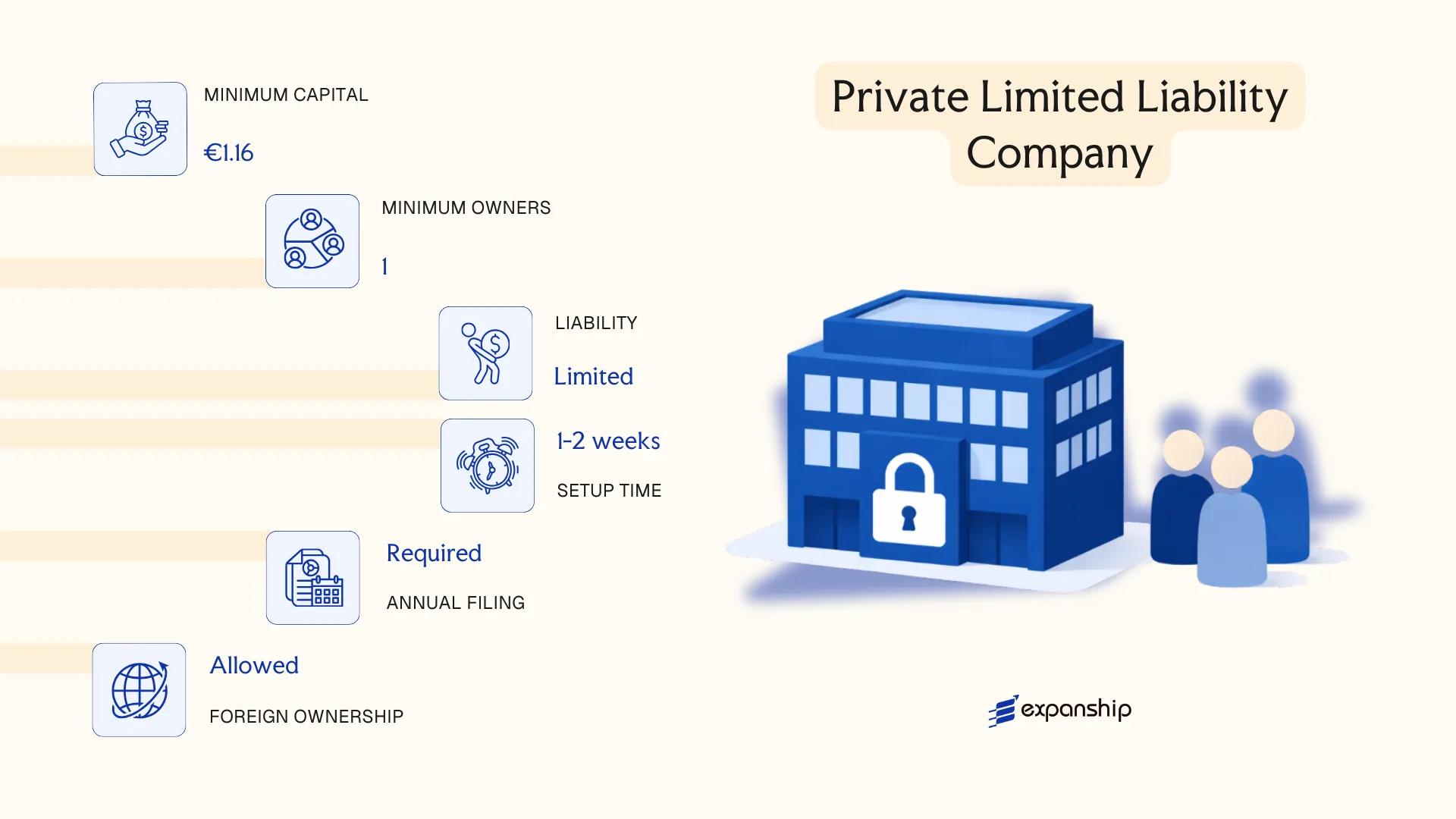

Private Limited Liability Company (Ltd)

Governed by the Companies Act, Chapter 386 of the Laws of Malta, the Malta private limited liability company Ltd is the most widely used corporate vehicle for both domestic and foreign investment. It carries separate legal personality from the moment of registration with the Malta Business Registry (MBR).

Shares in a private company cannot be offered to the public, and any transfer of shares is restricted by the Memorandum and Articles of Association. This hybrid structure combines the protection of limited liability with the operational flexibility suited to closely held businesses.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Liability Company | Governed by Companies Act, Cap. 386 |

| Members | Shareholders: min. 1, max. 50; Directors: min. 1 (natural person) | Corporate directors not permitted; sole member companies allowed |

| Local Presence | Registered office in Malta; Company Secretary required | Secretary must be ordinarily resident in Malta |

| Capital | EUR 1,164.69 minimum authorised share capital; 20% paid-up on incorporation | No maximum cap; shares can be in any currency |

| Share Transferability | Restricted by M&AA; no public offering permitted | Transfer restrictions must be explicitly stated in constitutional documents |

| Privacy | Beneficial ownership disclosed to MBR; not on public register | Shareholder register is accessible to members and competent authorities |

Focus Points

- Taxation: Subject to 35% corporate tax rate; shareholders may claim a refund of up to 6/7ths under the Full Imputation System, reducing effective tax; standard VAT rate of 18%; no withholding tax on dividends to non-residents in most cases; stamp duty applies on share transfers at 2% (5% for immovable property).

- Annual Compliance: Annual return and audited financial statements must be filed with the MBR; audit is mandatory regardless of company size.

- Treaty Access: Eligible for Malta's extensive double tax treaty network, covering 70+ jurisdictions.

- Economic Substance: No statutory substance requirements, though tax residence claims may require genuine management and control to be exercised in Malta.

- Conversion: A private company can be converted to a public limited company (plc) by satisfying the higher capital and governance thresholds under the Companies Act.

Closing

The private limited company suits trading operations, holding structures, and IP ownership arrangements where liability protection and shareholder confidentiality are priorities; its mandatory audit requirement, however, adds a recurring compliance cost regardless of turnover.

This structure works well for small to mid-sized foreign-owned businesses, joint ventures, and group holding entities seeking access to Malta's treaty network with capped personal liability.

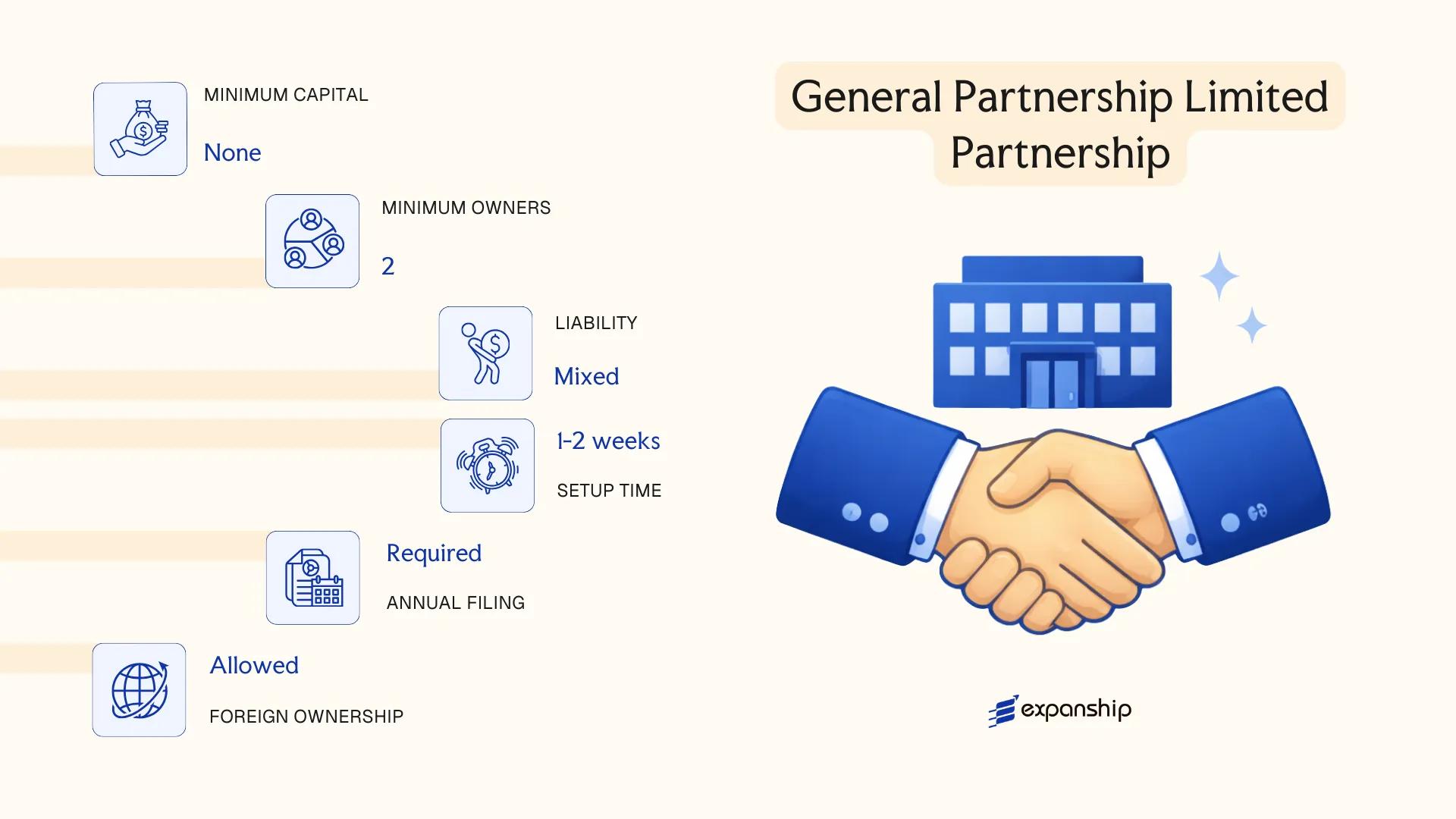

General Partnership, Limited Partnership (En Nom Collectif, En Commandite)

Both partnership forms in Malta are governed by the Companies Act, Chapter 386 of the Laws of Malta, which dedicates specific provisions to partnerships operating alongside corporate entities. The Malta en nom collectif en commandite distinction determines how liability is distributed among partners and shapes the overall structure of the business.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (En Nom Collectif or En Commandite) | Both possess separate legal personality under Chapter 386 |

| Members | Partners (General Partners; Limited Partners in En Commandite) | En Nom Collectif: minimum 2 general partners, no cap; En Commandite: minimum 1 general + 1 limited partner |

| Liability | Unlimited for general partners; limited to capital contribution for limited partners | En Nom Collectif partners bear joint and several liability |

| Local Presence | Registered office in Malta required | Must be maintained at all times |

| Capital | No statutory minimum; denominated in any agreed currency | Capital contributions defined in the partnership deed |

| Privacy | Partner names disclosed in the deed filed with the Malta Business Registry | No equivalent to shareholder register privacy |

Focus Points

- Taxation: Partnerships are fiscally transparent by default; income is taxed at partner level under Malta's Income Tax Act, though an election to be treated as a company may be available — VAT registration obligations apply if turnover thresholds are met.

- Annual Compliance: Annual accounts must be filed with the Malta Business Registry; audit requirements depend on size thresholds.

- Treaty Access: Because income flows to partners directly, treaty access depends on the tax residency of each individual partner, not the partnership itself.

- Conversion: A partnership may be converted to a limited liability company under Chapter 386, subject to regulatory approval and restructuring of liability.

- Restrictions: General partners in an En Commandite cannot allow limited partners to participate in management without risking reclassification of their liability status.

Sub-Types

En Nom Collectif (General Partnership)

All partners carry unlimited joint and several liability for the partnership's obligations. This structure is typically used by professional firms or family-owned businesses where partners accept mutual exposure and shared control.

En Commandite (Limited Partnership)

This form introduces a two-tier partner structure: general partners manage the business and bear unlimited liability, while limited partners contribute capital and remain passive. It is frequently used for investment vehicles and fund structures where capital contributors seek liability protection without operational involvement.

Closing Paragraph

Malta general partnership registration suits closely held ventures and investment vehicles where flexible governance outweighs the need for liability insulation. The absence of a minimum capital requirement lowers the entry threshold, though unlimited liability exposure for general partners represents a significant structural risk.

This structure is best suited for investment funds, professional firms, and joint ventures where the parties accept defined liability roles and prefer pass-through taxation over corporate-level tax obligations.

Cooperative Society

Cooperative society registration Malta falls under the Co-operatives Societies Act (Chapter 442 of the Laws of Malta), which governs formation, governance, and dissolution. A cooperative is a separate legal entity with limited liability for its members, structured around the principle of mutual benefit rather than profit distribution to investors. The Malta Co-operatives Board, operating under the Ministry responsible for co-operatives, serves as the primary supervisory authority.

Unlike standard commercial entities, a cooperative distributes surplus in proportion to member participation, not shareholding. This makes it structurally closer to a mutual association than a conventional company, though it retains full legal personality under Maltese law.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative Society | Registered under Chapter 442; separate legal personality |

| Members | Minimum 5 members; no statutory maximum | Members hold equal voting rights regardless of contribution size |

| Governance | Board of Directors elected by members | General meeting is the supreme governing body |

| Local Presence | Registered office in Malta required | Must maintain physical or administrative presence |

| Capital | No prescribed minimum share capital | Shares are typically of equal nominal value; transferability is restricted |

| Privacy | Member register not publicly searchable | Annual returns filed with the Malta Co-operatives Board |

Focus Points

- Taxation: Cooperatives are subject to corporate income tax at the standard 35% rate; VAT registration obligations apply where applicable; specific exemptions or deductions may apply to qualifying surplus distributions under domestic provisions.

- Annual Compliance: Annual general meeting required; audited financial statements must be submitted to the Malta Co-operatives Board.

- Restrictions: Membership and surplus distribution rules are governed by the cooperative's statute; shares cannot be freely transferred to non-members without approval.

- Treaty Access: Cooperatives are resident entities and, in principle, may access Malta's tax treaty network, though treaty eligibility depends on the specific treaty and the entity's tax position.

- Conversion: No direct statutory conversion pathway to a limited liability company exists; restructuring would require dissolution and re-incorporation.

Closing Paragraph

A cooperative society suits member-based enterprises in sectors such as agriculture, housing, retail, or professional services where participants share operational activity rather than seeking passive returns. The structure offers strong internal governance protections but is poorly suited to attracting third-party investment or scaling beyond a member-driven model.

Cooperative societies are most appropriate for groups of individuals or businesses operating a shared economic activity with equal governance participation, such as worker-owned enterprises or producer groups.

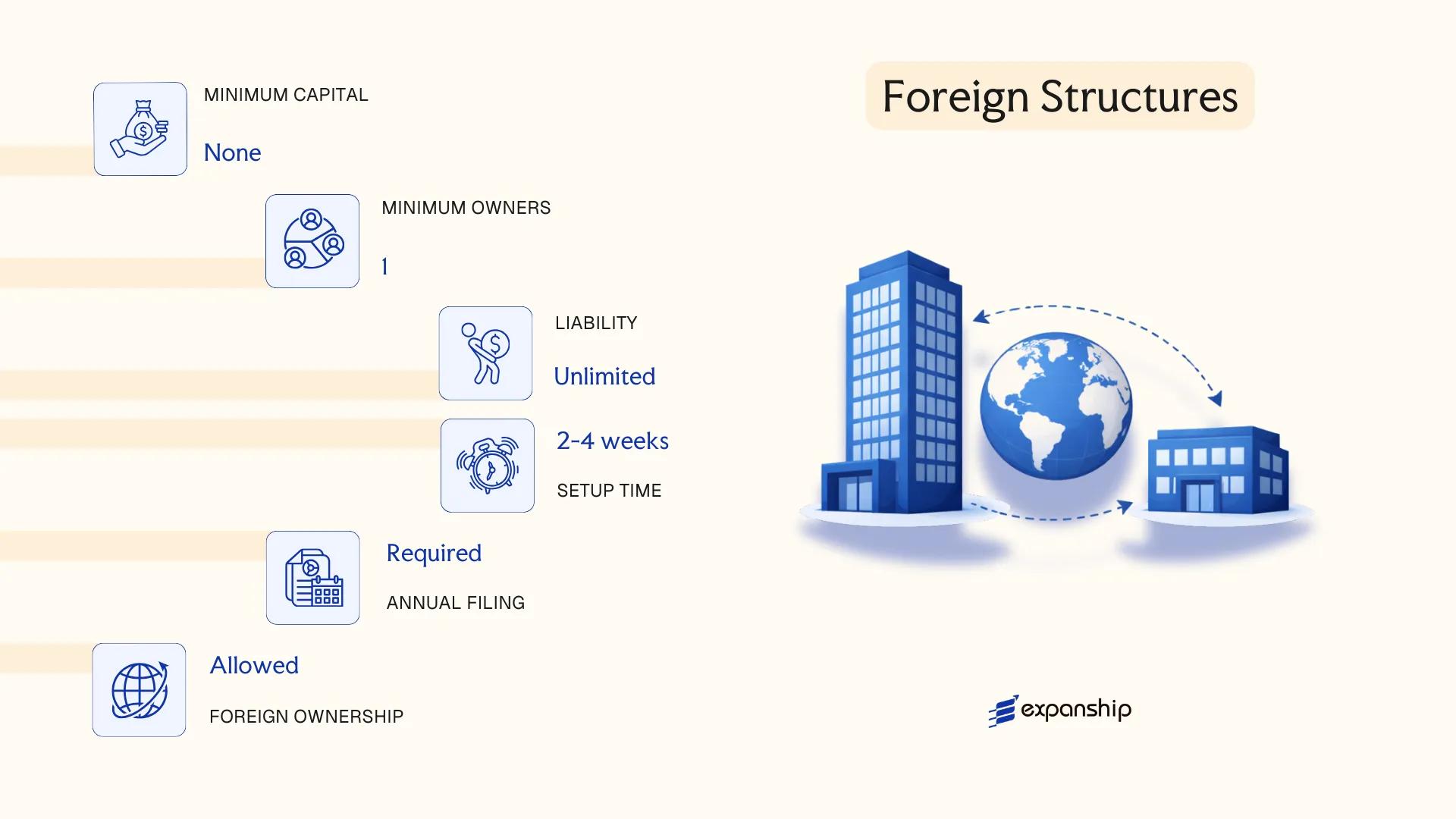

Foreign Structures (Branch Office, Representative Office)

Foreign companies seeking a presence in Malta without incorporating a separate legal entity may register under the Companies Act (Chapter 386 of the Laws of Malta). A foreign branch office registration Malta operates as an extension of the parent company, meaning the overseas entity retains full legal and financial responsibility for the branch's obligations. There is no separate legal personality; the parent bears unlimited liability for all local activities.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Registration Body | Malta Business Registry (MBR) | Malta Business Registry (MBR) |

| Local Representative | Mandatory — a locally resident authorised representative must be appointed | Mandatory — locally resident authorised representative required |

| Registered Office | Required in Malta | Required in Malta |

| Capital Requirement | None; parent's capital applies | None |

| Permitted Activities | Full commercial and trading operations | Promotional, liaison, and market research only — no revenue-generating activity |

| Privacy | Parent company details filed publicly at MBR | Parent company details filed publicly at MBR |

Focus Points

- Taxation: The branch's Malta-sourced profits are subject to the standard 35% corporate tax rate; VAT registration is required if taxable supplies exceed the applicable threshold; withholding tax may apply on profit remittances depending on the parent's jurisdiction and applicable double tax treaties.

- Economic Substance: No formal substance regime applies specifically to branches, but the authorised representative must maintain a genuine local presence to satisfy MBR and tax authority requirements.

- Annual Compliance: Audited financial statements of the parent, along with branch accounts where applicable, must be filed annually with the MBR under the Companies Act.

- Treaty Access: Access to Malta's double tax treaty network depends on the parent entity's tax residency; a branch itself is not a treaty resident.

- Activity Restrictions: A representative office is legally barred from generating income locally; conducting commercial transactions through this structure creates compliance exposure.

Sub-Types

Branch Office

A branch is permitted to conduct full trading and commercial activities on behalf of the parent company. It is commonly used by foreign firms entering the Maltese market who wish to test operations before committing to a standalone subsidiary.

Representative Office

A representative office is limited strictly to non-commercial functions such as market research, promotional activities, and liaison with local counterparts. No contracts may be concluded, and no revenue may be earned directly through this structure.

Closing

Both structures suit foreign companies requiring a defined local footprint without the administrative burden of a separate incorporated entity, though the branch's unlimited parent liability is a significant operational consideration.

Established foreign firms conducting short-term market entry or project-based work in Malta where full incorporation is not commercially justified.

Sole Trader

Sole trader registration in Malta follows a straightforward process, yet the structure carries distinct legal and financial implications that warrant careful consideration. A sole trader, locally known as a self-employed person or sole proprietor, is not a separate legal entity under Maltese law. The business and the individual are legally indistinct, meaning personal assets are fully exposed to business liabilities.

Registration is handled through the Malta Business Registry (MBR) and the Commissioner for Revenue. You must obtain a VAT number if your annual turnover exceeds the applicable threshold, and register for income tax purposes as a self-employed individual. No minimum capital is required, and no memorandum of association is needed.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality |

| Member Type | Sole Proprietor | One individual; no co-owners permitted |

| Local Presence | Registered address in Malta | Required for MBR and tax registration |

| Capital | No minimum | No paid-up or authorised capital requirement |

| Liability | Unlimited personal liability | Personal assets at risk for business debts |

| Privacy | Name and trade name publicly registered | Limited privacy; no shareholder register separation |

Focus Points

- Taxation: Income taxed at personal income tax rates (up to 35%); VAT registration required above threshold; no corporate tax, withholding tax, or stamp duty applicable at entity level.

- Social Security: Mandatory Class 2 National Insurance contributions apply to all self-employed persons registered in Malta.

- Annual Compliance: Annual income tax return required; VAT returns filed periodically depending on turnover category; no annual MBR filing fee equivalent to companies.

- Treaty Access: As an unincorporated individual, access to Malta's double tax treaties depends on personal residency status, not entity structure.

- Conversion: A sole trader can convert to a limited liability company at any time, though asset transfer and re-registration with the MBR are required.

Closing Paragraph

A sole trader structure suits freelancers, consultants, and small-scale operators conducting low-risk activities with limited third-party exposure. The absence of incorporation formalities keeps setup costs minimal, but unlimited personal liability remains a significant structural drawback for anyone operating in sectors with material financial or legal risk.

This structure is most appropriate for individual professionals or sole operators testing a market with low startup costs and no immediate need for investor participation.

How to Choose the Right Entity Type in Malta

Knowing how to choose a company structure in Malta before committing to registration prevents costly structural corrections later.

Why Your Entity Choice Matters

The structure you register has binding legal and financial consequences that are difficult to reverse.

- Selecting a tax-exempt entity blocks access to Malta's double taxation treaty network, meaning you cannot claim withholding tax reductions in counterpart jurisdictions.

- Registering a structure without adequate substance capacity — where substance requirements apply — can trigger reporting failures and regulatory penalties under the Income Tax Act.

- Choosing a company when a foundation or trust would serve estate planning objectives locks your firm into annual shareholder obligations, audit cycles, and governance requirements that foundations are not subject to.

- Selecting an entity that mandates audited financial statements for a single-person consultancy introduces annual compliance costs that the business activity does not justify.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as funds or insurance each require a structurally distinct entity under Maltese law.

- Tax Objectives: Your need for full exemption, participation exemption eligibility, or access to Malta's treaty network will determine which structures are viable.

- Ownership and Management: Single-owner operations and multi-party arrangements have different requirements under the Companies Act (Cap. 386).

- Substance Capacity: If you cannot realistically maintain employees or decision-making activity locally, your chosen structure must align with applicable substance thresholds.

- Privacy Requirements: Director and shareholder details are publicly accessible through the Malta Business Registry, so confidentiality requirements affect your structural options.

- Exit Strategy: Not all Maltese entity types permit redomiciliation or conversion; confirm these rights before formation if an exit or restructure is foreseeable.

Corporate Compliance Services in Malta

Maintain good standing with the Malta Business Registry and meet ongoing statutory obligations across your Maltese entity.

Conclusion

Selecting the right structure is one of the more consequential decisions in any Malta company incorporation process, and this guide has outlined the main options governed primarily by the Companies Act (Chapter 386 of the Laws of Malta) and supervised by the Malta Business Registry.

Among the entities covered, the private limited liability company remains the most commonly registered form, favored for its balance of liability protection and administrative manageability. The public limited company suits larger ventures requiring capital market access; partnerships en nom collectif and en commandite serve those prioritizing pass-through tax treatment; cooperatives address member-owned operational models; and branches or representative offices fit foreign firms testing the market before committing to full incorporation.

Malta's corporate law summary reflects a jurisdiction that continues expanding its treaty network and aligning with EU regulatory developments, which shapes the long-term compliance environment for any entity registered here. Your choice of structure determines how those obligations apply.

How Expanship Can Assist You

Expanship Malta company formation services cover the full setup journey — from choosing between a private limited company (Ltd) and a public limited company (plc) to filing the memorandum and articles of association with the Malta Business Registry. Each entity type discussed in this blog carries distinct registration requirements, share capital thresholds, and ongoing compliance obligations that affect how your business operates from day one.

Across those structures, here is where Expanship supports you directly:

- Document preparation and notarization for MBR submission

- Registered office and resident company secretary provision

- Government filing and Malta Business Registry liaison

- Post-incorporation compliance, including annual return filing and VAT registration

- Director and shareholder register maintenance

- Banking introduction assistance with local and international institutions

Get in touch with Expanship Malta to discuss which structure fits your objectives and what the registration process looks like for your specific situation.

Frequently Asked Questions (FAQ)

The private limited liability company (Ltd), governed by the Companies Act (Chapter 386 of the Laws of Malta), is the most frequently incorporated structure. Its combination of limited liability, a single-shareholder minimum, and no restriction on foreign ownership makes it the default choice across most commercial sectors.

A branch is not a separate legal entity; the foreign parent bears full liability for its Maltese operations, whereas an Ltd carries liability limited to its share capital. Both are subject to Maltese corporate income tax on locally sourced income, but the Ltd can access Malta's extensive double tax treaty network as a resident entity, while a branch's treaty eligibility depends on the parent's jurisdiction of incorporation.

The private limited company permits the use of nominee shareholders, which means the beneficial owner's identity need not appear on the public register held by the Malta Business Registry. Director details are publicly filed, but nominee director arrangements are legally permissible, adding a further layer of separation between ownership and public record.

No. A sole trader and an Ltd can each be formed by one individual, but a general partnership (En Nom Collectif) and a limited partnership (En Commandite) each require a minimum of two partners. A cooperative society requires a minimum of three founding members under the Co-operatives Societies Act (Chapter 442).

Yes. Non-residents face no ownership restrictions for an Ltd or a public limited company (plc). Foreigners may also operate through a registered branch of a foreign entity. The Malta Business Registry processes applications from non-resident incorporators, though a registered office address within Malta is mandatory for all structures regardless of the owner's nationality.

Maltese company law allows a private limited company to convert to a public limited company, and vice versa, through a formal resolution and re-registration with the Malta Business Registry. Conversion between a company and a partnership structure is not a straightforward statutory process and would typically require dissolution and re-incorporation rather than a direct continuation mechanism.

Not all of them. An Ltd, plc, and cooperative society each possess separate legal personality, meaning they can own assets, enter contracts, and incur liabilities independently of their members. A sole trader does not form a distinct legal entity; the individual and the business are treated as one, leaving the owner personally exposed to all business obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.