Key Takeaways

- Malta's statutory corporate tax rate sits at 35%, and while the shareholder refund mechanism under the Companies Act (Chapter 386) can reduce the effective rate significantly, the cash flow burden of paying full tax upfront before refunds are processed creates a real liquidity constraint for foreign shareholders.

- The MFSA enforces ongoing compliance obligations that extend well beyond incorporation, requiring structured reporting, substance demonstration under EU Anti-Tax Avoidance Directives, and continuous adherence to AML frameworks that add material operational cost for non-resident-owned entities.

- Sourcing a qualified, Malta-resident company secretary is a mandatory legal requirement rather than an administrative formality, and the limited local talent pool makes filling this role — and other skilled positions — both time-consuming and expensive.

- Professional and legal service fees in Malta trend higher than in comparable offshore jurisdictions, meaning the net cost advantage of the refund-based tax system can erode quickly once incorporation, compliance, and advisory costs are factored into annual operating budgets.

Malta operates under a heavily regulated corporate framework, shaped by its obligations as an EU member state and its longstanding position as a financial services hub. The Companies Act (Chapter 386 of the Laws of Malta) forms the primary legislative foundation for company formation and governance.

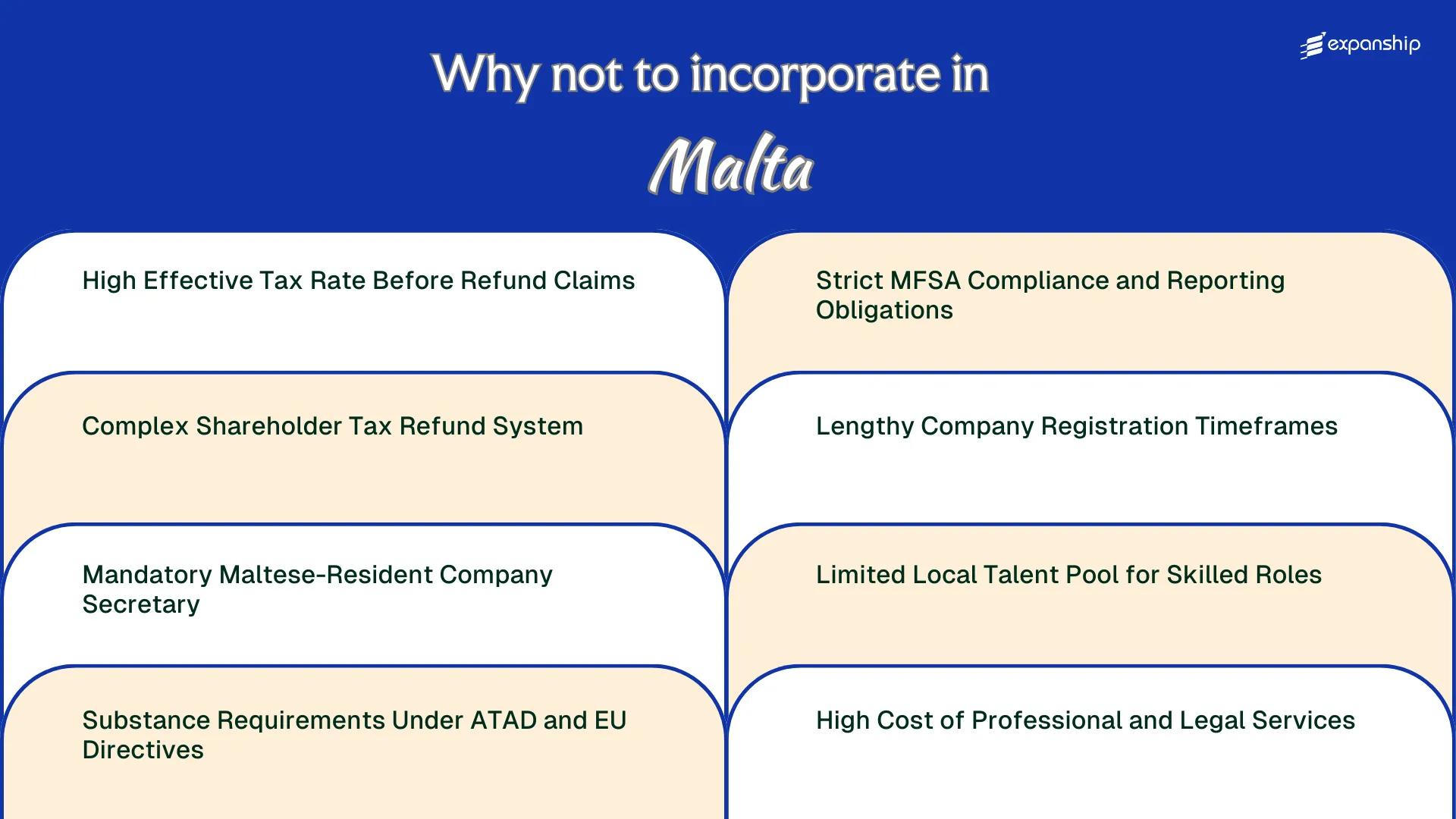

The disadvantages of incorporating in Malta span several distinct areas, from tax mechanics to compliance infrastructure.

Not all of these drawbacks carry equal weight for every business. A holding company with passive income faces a different set of pressures than a trading entity or a regulated financial services firm.

Foreign investors and non-resident shareholders, particularly those structuring holding or IP entities in Malta, are most likely to encounter the friction points this article addresses. Your exposure to specific obstacles will depend substantially on your business model, the corporate structure you adopt, and the industry you operate in.

High Effective Tax Rate Before Refund Claims

Malta's headline corporate tax rate of 35% is among the highest in the European Union, creating an immediate cash flow problem for foreign business owners operating through a Maltese company.

Upfront Tax Liability at 35%

Under the Income Tax Act, companies incorporated in Malta are subject to corporation tax at 35% on chargeable income. This rate applies before any shareholder refund claims are processed, meaning your business must first settle the full liability with the Commissioner for Revenue.

For a foreign-owned firm, this creates a significant working capital requirement at the point of tax payment. The gap between paying at 35% and recovering a portion later can stretch over several months.

Cash Flow Exposure During the Refund Gap

The refund mechanism under Malta's full imputation system is not instantaneous. Your business absorbs the full 35% charge upfront, and the timing of any repayment depends on administrative processing by the tax authorities.

Companies with thinner operating margins face measurable liquidity pressure during this interval.

Foreign business owners must fund the full 35% tax liability from company cash reserves before any refund entitlement is assessed, which can strain liquidity for early-stage or cash-sensitive operations.

Complex Shareholder Tax Refund System

Malta shareholder tax refund complexity is not a minor administrative detail — it is a structural feature of the tax system that places a significant procedural burden on foreign shareholders. Under the full imputation system, corporate tax is paid at 35% by the company, and shareholders must then file separate refund claims to recover a portion of that tax, typically 6/7ths for trading income, reducing the effective rate to approximately 5%.

That refund does not arrive automatically. It must be actively claimed through the Maltese Commissioner for Revenue, and processing times can extend well beyond twelve months.

For a foreign investor, this creates several concrete operational problems:

- Cash flow is locked at the 35% rate until the refund clears, which can distort financial planning for distributions-dependent business models.

- You must engage local tax advisors to prepare and submit claims correctly, adding recurring professional fees each refund cycle.

- Errors or omissions in refund documentation can trigger delays or rejections, with no guarantee of resolution within a predictable timeframe.

- If your company holds multiple account categories under the Maltese tax account framework, misallocation between the Immovable Property Account, Final Tax Account, or Maltese Taxed Account can invalidate or reduce the refund entitlement.

The Malta imputation system problems become most acute for shareholders based outside the EU, where additional treaty verification requirements may apply before a refund is processed.

Company Incorporation in Malta

Set up your Malta company with full support on tax structure, shareholder arrangements, and compliance requirements from day one.

Mandatory Maltese-Resident Company Secretary

Under the Companies Act (Chapter 386 of the Laws of Malta), every registered company must appoint a secretary who is ordinarily resident in Malta. This Malta resident company secretary requirement applies regardless of where your shareholders or directors are based, meaning foreign-owned entities cannot fulfill the role remotely or appoint someone from abroad.

| Requirement | Detail | Burden on Foreign Owner |

|---|---|---|

| Residency condition | Secretary must be ordinarily resident in Malta | Eliminates group-level or home-country appointments |

| Ongoing obligation | Appointment must be maintained at all times | Vacancy triggers immediate non-compliance |

| Registered office link | Secretary typically connected to local registered office | Adds a second recurring local service dependency |

| Typical annual cost | EUR 500 – EUR 1,500+ depending on service provider | Fixed overhead with no remote alternative |

Because the position cannot be held by a non-resident, your business must contract a local corporate service provider or individual to fulfill this role on an ongoing basis. This creates a permanent, unavoidable cost tied directly to the mandatory local company secretary rule rather than to any operational activity your firm actually conducts.

The secretary carries statutory duties under the Companies Act, including maintaining registers, filing annual returns with the Malta Business Registry, and ensuring document execution is compliant. Any lapse in these obligations exposes the company to regulatory penalties, making the quality of your appointed secretary a genuine compliance variable outside your direct control.

Substance Requirements Under ATAD and EU Directives

Malta substance requirements ATAD compliance imposes structural demands that go well beyond basic registration. Under the EU's Anti-Tax Avoidance Directives (ATAD I and ATAD II), transposed into Maltese law, your entity must demonstrate genuine economic activity on the island to access treaty benefits and avoid controlled foreign company reclassification in your home jurisdiction.

Substance is not self-certifying. You must show that key management decisions are made locally, that directors physically present in Malta have real authority, and that adequate staff and premises exist. For a foreign owner managing operations remotely, this creates ongoing operational costs that are fixed regardless of revenue levels.

The EU anti-tax avoidance challenges embedded in these rules mean that nominee director arrangements, without genuine decision-making, expose the entity to challenge both by the Maltese tax authority (the Commissioner for Revenue) and by tax authorities in your home country.

- Key management and control decisions must demonstrably occur within Malta

- Nominee or passive directors without real authority increase reclassification risk

- Physical premises and locally present staff may be required depending on activity type

- The Commissioner for Revenue can scrutinize substance during tax refund audits

- Home-country CFC rules may apply independently of Maltese compliance

Malta's ATAD implementation means a holding company with purely passive income and no local staff can be reclassified as a controlled foreign company by another EU member state, even if it is fully tax-compliant under Maltese law.

Strict MFSA Compliance and Reporting Obligations

Malta MFSA compliance obligations extend well beyond standard EU baseline requirements, creating a reporting burden that many foreign business owners underestimate before incorporating.

Scope of Regulatory Obligations

The Malta Financial Services Authority enforces ongoing disclosure requirements that apply to a broad range of corporate activities, not just licensed financial entities. Even standard trading companies must maintain accurate beneficial ownership registers, file annual returns with the Malta Business Registry, and submit audited financial statements, regardless of revenue size. For a foreign-owned firm without in-house legal staff, meeting these parallel obligations requires retaining local professionals year-round.

Practical Burden on Foreign-Owned Entities

Malta corporate compliance challenges become acute when your entity operates remotely, since MFSA can initiate inquiries that require timely, documented responses from company officers. Non-compliance carries administrative penalties under the Companies Act, Chapter 386 of the Laws of Malta, and persistent failures can trigger striking-off proceedings. Companies operating across multiple EU jurisdictions may find that Malta's enforcement posture demands more active local oversight than comparable holding structures elsewhere in the bloc.

Managing MFSA Compliance Obligations in Malta

If your business is facing the reporting demands and regulatory requirements of operating in Malta, our team can help you understand what's required and how to stay on track.

Lengthy Company Registration Timeframes

Malta company registration delays are a documented friction point for foreign investors, and processing times at the Malta Registry of Companies (MBR) can extend well beyond initial estimates. Unlike jurisdictions that offer same-day or 24-hour incorporation, your business formation timeline here is subject to MBR workload and document verification queues.

- Standard MBR processing for a private limited company (Ltd) typically runs between five and ten business days, but backlogs can push this further, delaying your ability to open corporate bank accounts or execute contracts.

- Apostille verification and notarisation requirements for foreign-sourced identity documents add additional days before the MBR will accept your submission as complete.

- If your submitted documents contain errors or inconsistencies, the MBR issues a requisition notice requiring corrections, restarting the review clock and extending the Malta incorporation timeframe problems further.

- Regulated activities requiring concurrent MFSA licensing compound the delay, as operational approval depends on two separate bodies processing your application independently.

Limited Local Talent Pool for Skilled Roles

Malta's limited skilled workforce is a structural constraint that directly affects your ability to staff a business locally. With a total population of roughly 520,000, the absolute number of qualified professionals across specialised fields — finance, technology, engineering, and regulated services — is small by any measure.

Sectors licensed under the Malta Financial Services Authority (MFSA) or the Malta Gaming Authority (MGA) require personnel with specific regulatory knowledge. Finding locally qualified candidates for these roles is competitive, and the shortage often forces businesses to recruit from abroad, triggering additional costs and timelines associated with work permit applications under Jobsplus, Malta's employment regulatory body.

Reliance on expatriate talent is common, but it is not cost-free. Salary expectations for international hires tend to be higher, and housing costs in Malta have risen sharply over recent years, inflating total employment packages.

The constraint is most acute for firms operating in dual-regulated environments or building out compliance and technical functions simultaneously.

A foreign technology firm establishing a Malta-based entity and needing to hire five senior software engineers and two MFSA-qualified compliance officers locally could realistically face a 6-to-12-month recruitment cycle, with relocation packages adding an estimated €15,000 to €25,000 per hire above standard compensation benchmarks.

High Cost of Professional and Legal Services

Malta professional services costs rank among the more significant operational burdens for foreign-owned entities, particularly when measured against the volume of mandatory engagements. A licensed company secretary, a registered auditor, and a tax compliance specialist are not optional appointments — they are structural requirements that generate recurring annual fees before your business turns a single euro in profit.

Audit fees in Malta are driven upward by a small pool of licensed practitioners and consistent demand from both regulated and non-regulated entities. The Malta Financial Services Authority's compliance expectations add scope to audit engagements, which pushes billable hours higher than in comparable EU jurisdictions with larger professional markets.

Legal fees for corporate work, including shareholder agreements, MFSA correspondence, and regulatory submissions, are priced at rates comparable to Western European capitals despite Malta's small domestic economy. For a foreign firm managing these costs remotely, without a local presence to oversee service quality, the exposure to billing inefficiencies compounds over time.

If your company holds or applies for any licence under the Investment Services Act or the Malta Financial Services Authority's regulatory frameworks, professional fees increase substantially due to the mandatory involvement of licensed advisors at each submission and compliance stage.

Overcoming Malta's Incorporation Drawbacks

Overcoming Malta's incorporation drawbacks requires structural planning rather than reactive fixes, particularly given the layered compliance obligations imposed by both domestic legislation and EU directives.

- Appoint a Malta-resident company secretary at incorporation to satisfy the requirement under the Companies Act, Cap. 386.

- Structure your shareholding through a non-resident holding entity to position the firm for the 6/7ths shareholder tax refund under the Income Tax Act.

- Establish documented economic substance in Malta prior to operations to meet ATAD and EU anti-avoidance standards enforced by the MFSA.

- Submit the annual return and audited financial statements within the statutory deadlines set by the Malta Business Registry to avoid accumulated penalties.

- Budget for local professional service costs at the outset, factoring in mandatory audit and legal fees as fixed operational expenses rather than discretionary costs.

Each of these steps addresses obligations that are enforceable under Maltese law, and non-compliance carries formal regulatory consequences administered by the Malta Business Registry or the MFSA.

Malta's Overall Value as a Business Destination

Malta's position as a European Union member state with an established financial services framework gives it genuine credibility as a corporate jurisdiction. The disadvantages covered in this blog are real and material, yet they do not make the territory universally unsuitable — they do narrow the profile of businesses for which incorporation here makes practical and financial sense.

| Pros | Cons |

|---|---|

| EU membership grants access to EU directives, passporting rights, and cross-border legal frameworks | The 35% headline corporate tax rate requires upfront payment before shareholders can reclaim the effective rate through the refund system |

| Malta operates a full imputation tax system that can reduce the effective rate to 5% for qualifying structures | Refund claims add administrative cycles and cash flow delays that many smaller businesses cannot absorb easily |

| English is an official language, reducing drafting and communication friction for foreign owners | A resident company secretary is a mandatory legal requirement, adding a recurring local compliance cost |

| The MFSA is an internationally recognised regulator, which supports credibility with banks and partners | The local talent pool for specialised roles is constrained by the island's small population |

Substance requirements under ATAD and EU anti-avoidance directives have raised the operational bar considerably over recent years. Maintaining a genuine presence is no longer optional for businesses seeking to rely on treaty benefits or defend their tax position under scrutiny.

Corporate Compliance Services in Malta

Manage your Maltese company's statutory obligations, including annual filings, MFSA reporting, and ongoing regulatory requirements.

Conclusion

Malta's overall position as a business destination remains substantive, but the Malta incorporation cons summary presented across this blog reflects a structurally demanding environment. The 35% corporate tax rate applied at the entity level — before any shareholder refund process is initiated — creates a cash flow timing problem that smaller firms often underestimate. Compliance obligations under the MFSA, combined with mandatory local appointments and substance requirements tied to ATAD implementation, add recurring operational costs that compound over time. Professional guidance specific to Maltese corporate law and MBR procedures will determine how efficiently your business absorbs these structural demands.

Expanship's Malta Company Formation Support

Dealing with MFSA reporting cycles, the shareholder refund mechanism, and Malta's substance requirements under ATAD generates significant administrative weight for any incoming business. Expanship's Malta company formation support is structured around reducing that operational burden, helping your firm stay aligned with local compliance obligations without losing focus on core business activity.

Beyond initial setup, Expanship covers the full incorporation and ongoing compliance cycle across the following areas:

- Expanship prepares and files all company registration documents with the Malta Business Registry on your behalf.

- A registered agent and local office address are provided to satisfy Malta's residency and presence requirements.

- Your firm's filings and regulatory correspondence with the MFSA and MBR are handled directly.

- Post-incorporation compliance management keeps your entity in good standing through annual returns and statutory obligations.

- Banking introduction assistance connects your business with suitable Maltese financial institutions.

- Tax registration and liaison with the Maltese tax authorities, including VAT and income tax, are coordinated on your behalf.

Reach out to Expanship Malta to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The refund mechanism under Malta's Income Tax Act applies to shareholders of Maltese-registered companies, but the refund rate varies depending on the nature of the income. Trading income generally qualifies for a 6/7ths refund, reducing the effective rate to around 5%, while passive income and royalties attract a lower 5/7ths refund. The structure only delivers its intended benefit when the company is set up correctly and the income is properly classified.

Under the Companies Act, Chapter 386 of the Laws of Malta, every private company must have a company secretary, and regulatory practice requires that individual to be resident in Malta. Failure to maintain this appointment puts the company in breach of its statutory obligations, which can trigger penalties from the Malta Business Registry and, in serious cases, affect the company's good standing status.

Costs vary based on the scope of services, but Malta consistently sits at the higher end among EU jurisdictions for ongoing corporate maintenance fees. Legal and compliance professionals in Malta command rates comparable to Western European markets, and because the shareholder refund mechanism requires precise structuring, professional advisory fees are not optional expenses you can defer.

For non-regulated trading companies, the Malta Financial Services Authority is not the primary supervisory body, so the compliance burden sits mainly with the Malta Business Registry and the Commissioner for Revenue. That said, if your business touches financial services, crypto assets, or investment activity even tangentially, the MFSA's oversight applies and its reporting requirements are detailed and strictly enforced, comparable in intensity to regulators in Luxembourg or Ireland.

Malta has transposed the EU's Anti-Tax Avoidance Directives into domestic law, and insufficient economic substance can result in the denial of tax treaty benefits, transfer pricing adjustments, or reclassification of income. Beyond the tax consequences, a substance challenge by the Commissioner for Revenue can expose your structure to back-taxes and interest charges. The risk is heightened for holding companies or IP-holding entities that have little or no operational activity on the island.

The Malta Business Registry does not offer a guaranteed same-day or next-day incorporation track in the way that some offshore jurisdictions do. Standard registration can take anywhere from one to three weeks depending on document completeness and back-office volumes. Engaging a licensed local agent with established Registry relationships can reduce delays, but there is no statutory fast-track that eliminates the waiting period entirely.

If your business needs to hire qualified staff locally to satisfy substance requirements under EU directives, Malta's small population of roughly 520,000 creates real constraints, particularly for specialised roles in finance, technology, and senior management. Competition for qualified professionals is high relative to supply, which drives up employment costs and can make it difficult to build a credible local operational presence quickly.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.