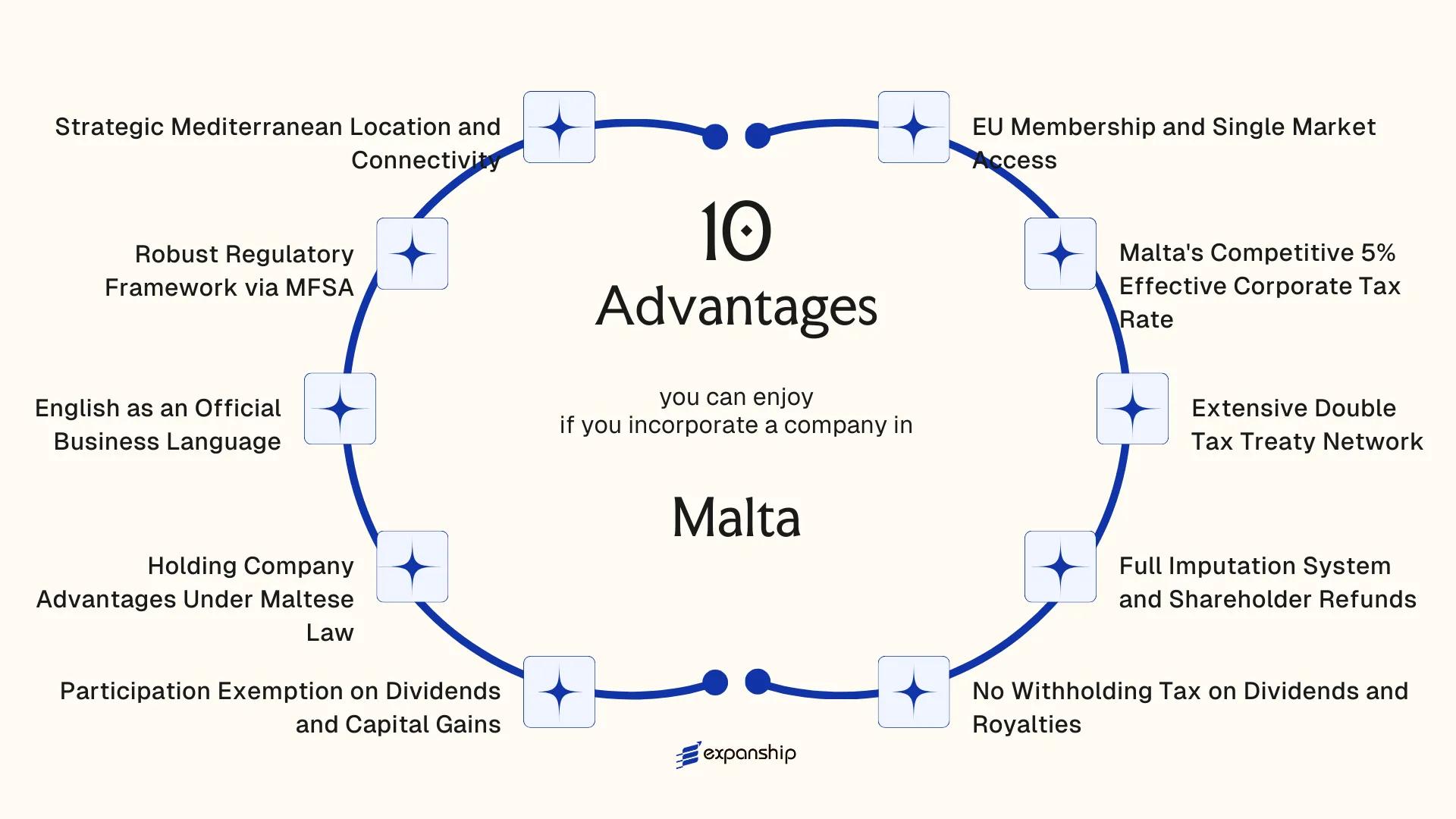

Key Takeaways

- Malta's full imputation system, governed by the Income Tax Act, enables foreign shareholders to reclaim tax paid at the corporate level, reducing the effective corporate tax burden to approximately 5% on distributed profits.

- Through the participation exemption, qualifying investors in a Maltese holding company can receive dividends and realise capital gains from subsidiary disposals free from additional Maltese tax, making the structure particularly efficient for multi-tiered corporate groups.

- No withholding tax applies to outbound dividend, interest, or royalty payments made to non-resident shareholders, eliminating a layer of friction that is present in most other EU jurisdictions.

- Backed by the Malta Financial Services Authority (MFSA) under the Companies Act (Cap. 386), Malta's regulatory environment provides a recognised EU-compliant framework while permitting 100% foreign ownership without requiring a local partner or government approval.

Malta is an independent EU member state situated in the central Mediterranean, south of Sicily. For foreign businesses evaluating the benefits of incorporating in Malta, the starting point is the MFSA — the Malta Financial Services Authority — which oversees company registration and financial regulation across the jurisdiction. The private limited liability company, locally designated as a limited liability company under the Companies Act (Cap. 386), is the entity most commonly used by foreign investors establishing a presence here.

From a tax perspective, the system is treaty-based and imputation-driven, designed to reduce effective corporate tax rates through shareholder refund mechanisms. Foreign ownership faces no general restrictions; non-residents may hold 100% of shares in a locally registered company without requiring a local partner or special government approval. This openness extends across most sectors, making the jurisdiction accessible to a wide range of international business structures.

This article examines the principal advantages that Malta company formation offers to foreign businesses, directors, and investors operating across different industries and corporate structures.

EU Membership and Single Market Access

Malta EU membership business advantages begin with one foundational fact: as a Member State since 2004, any company incorporated here operates within the EU's internal market under the same legal standing as firms based in Germany, France, or the Netherlands.

What Single Market Membership Means in Practice

A Maltese-registered entity can supply goods and services across all 27 EU member states without facing customs duties, import quotas, or separate market-entry authorization in each country. For a foreign business owner, this eliminates the need to establish multiple subsidiaries just to reach European customers.

EU Passporting Rights and Financial Services

For regulated businesses, EU passporting rights attached to a Malta company are particularly consequential. A firm authorized by the Malta Financial Services Authority (MFSA) under EU directives, including MiFID II, AIFMD, or the E-Money Directive, can passport that authorization into other member states through a notification procedure rather than a full local licensing process. That single authorization, obtained in one jurisdiction, substitutes for what would otherwise be 26 separate regulatory approvals.

Your MFSA-issued license can serve as your entry point to the entire EU financial market without repeated authorization procedures in each member state.

Malta's Competitive 5% Effective Corporate Tax Rate

Malta's headline corporate tax rate sits at 35%, but for non-resident shareholders, the effective rate reduces to 5% through a statutory refund mechanism under the Income Tax Act. When a Maltese company distributes dividends from trading income, shareholders are entitled to claim back 6/7ths of the tax paid at the corporate level. That refund brings the combined tax cost on distributed profits down to approximately 5% of pre-tax income — a figure verified by the refund structure written into domestic legislation, not a negotiated ruling.

For a foreign investor, this matters because the outcome is predictable and rule-based. You are not relying on advance pricing agreements or discretionary exemptions. The entitlement to the refund is statutory, which means it applies consistently across qualifying structures.

The conditions that make this workable for foreign-owned companies are relatively straightforward:

- The trading income must be allocated to the correct tax account under the Five Tax Account system, specifically the Foreign Income Account or Malta Taxed Account

- The shareholder receiving the dividend must be non-resident or a qualifying entity

- The refund claim is filed after the dividend is distributed, with no pre-approval requirement

- The 6/7ths refund applies to active trading income; different rates apply to passive income streams

Compared to the EU average corporate tax rate of approximately 21%, the effective burden under this system is substantially lower, making Malta's tax refund system for companies structurally significant for cost planning.

Company Incorporation in Malta

Set up a Malta-registered company and access the statutory 5% effective tax rate through a compliant corporate structure.

Extensive Double Tax Treaty Network

Malta's double tax treaty network benefits foreign businesses through reduced or eliminated withholding taxes on cross-border income flows. With over 70 signed tax treaties in force, your company gains access to one of the wider treaty networks among EU member states, covering key financial centres across Europe, Asia, the Middle East, and Africa.

| Treaty Partner | Dividends (WHT %) | Interest (WHT %) | Royalties (WHT %) |

|---|---|---|---|

| United Kingdom | 0–15 | 10 | 10 |

| Germany | 5–15 | 0 | 0 |

| United Arab Emirates | 0 | 0 | 0 |

| Singapore | 0 | 7 | 10 |

| China | 5–10 | 10 | 10 |

Each treaty is negotiated under the OECD Model Tax Convention, which means the rules governing permanent establishment, residency, and income classification follow a consistent and predictable framework. For a foreign investor structuring cross-border operations, that consistency reduces the legal uncertainty typically associated with multi-jurisdictional income flows.

Treaty protection applies to dividend distributions, interest payments, royalties, and capital gains in qualifying circumstances. A Maltese-resident company receiving income from a treaty partner country can apply the applicable treaty rate rather than the domestic withholding rate of that jurisdiction, directly reducing the tax cost on repatriated earnings. Treaty eligibility generally requires that your entity meets the tax residency conditions under Maltese law, meaning it must be incorporated locally or effectively managed and controlled from within the country.

Full Imputation System and Shareholder Refunds

The Malta full imputation system shareholder refunds mechanism is one of the most structurally significant tax features available to foreign investors operating through a Maltese company. Under the Income Tax Act and the Income Tax Management Act, corporate tax paid at the entity level is credited in full to shareholders upon dividend distribution, eliminating economic double taxation at source.

The standard corporate tax rate is 35%, but the refund mechanism is where the effective rate shifts substantially. Non-resident shareholders and qualifying Maltese holding structures can claim refunds of up to 6/7ths of the tax paid, reducing the effective rate to around 5%. For passive interest and royalties, a 5/7ths refund applies, and a 2/3rds refund is available where the company itself has claimed double tax relief.

Refunds are processed by the Maltese tax authority, the Commissioner for Revenue, and are typically issued after the company's tax return is assessed.

Keep the following in mind:

- Refunds are paid to shareholders, not to the company itself

- The shareholder must be registered and the dividend formally distributed before a refund claim can be filed

- Different refund fractions apply depending on the nature of the income

- Non-resident shareholders are eligible for refunds under current legislation

The refund is a statutory entitlement under Maltese law, not a discretionary relief, meaning it cannot be withheld by the Commissioner for Revenue once all conditions are met.

No Withholding Tax on Dividends and Royalties

Malta imposes no withholding tax on dividends distributed to non-resident shareholders, making it one of the few EU member states where cross-border profit extraction carries no additional tax cost at source. This applies regardless of the shareholder's country of residence, with no requirement to invoke a double tax treaty or satisfy minimum holding thresholds for the exemption to apply.

Dividend Distributions to Foreign Shareholders

Under the Income Tax Act (Chapter 123 of the Laws of Malta), dividends paid out of a Maltese company's tax-paid profits to non-resident individuals and corporate shareholders are not subject to any withholding. For a foreign investor repatriating profits to a holding structure abroad, this means the full after-tax dividend reaches the parent entity without deduction at the Maltese level.

Most jurisdictions levy withholding tax on outbound dividends ranging from 5% to 30%, depending on the recipient's location and applicable treaty provisions. Eliminating this layer entirely reduces the effective cost of distributing earnings and simplifies inter-company cash flows within multinational structures.

Royalties and Outbound Payments

Royalty payments made from a Maltese entity to non-resident recipients are equally exempt from withholding tax under domestic law. Intellectual property held within or licensed through a Maltese structure can therefore generate royalty income that flows outbound without any deduction at source, without relying on treaty relief or EU Directive provisions, though those remain available as an additional layer of protection.

Maximize Your Tax Position in Malta

Speak with an Expanship specialist about structuring dividend distributions and royalty flows through a Maltese entity to take full advantage of the zero withholding tax framework.

Participation Exemption on Dividends and Capital Gains

Under the Malta participation exemption on dividends and capital gains, qualifying companies can receive dividend income and dispose of shareholdings entirely free from corporate tax. This treatment is grounded in the Income Tax Act and applies where specific ownership thresholds are met, giving foreign-owned holding structures a material tax advantage on cross-border returns.

- A qualifying holding company must hold at least 5% of the equity in the subsidiary, or alternatively satisfy conditions related to the value of the holding, the duration of ownership, or the nature of the investee entity.

- Dividend income received from a qualifying participating holding is exempt at the company level, meaning profits distributed upstream are not taxed again in Malta before reaching the shareholder.

- On disposal of shares in a qualifying subsidiary, any capital gain realized by the Maltese entity is equally exempt, removing a layer of taxation that many jurisdictions impose on exit events.

- The exemption extends to holdings in both EU and non-EU entities, provided the subsidiary is not predominantly passive or based in a low-tax jurisdiction that falls outside accepted parameters under Maltese tax rules.

- For foreign investors structuring international groups, this means retained proceeds from asset sales or subsidiary dividends can be redeployed without reduction by Maltese corporate tax, preserving full capital efficiency within the holding structure.

Holding Company Advantages Under Maltese Law

Malta holding company advantages are grounded in specific structural features of Maltese corporate law that directly reduce the tax burden on international group structures.

A holding company incorporated under the Companies Act (Cap. 386) can own shares in foreign subsidiaries and receive dividends or capital gains with no tax at the holding company level, provided the participation exemption conditions are met. This means profits earned by operating subsidiaries can flow up to the Maltese holding entity without triggering a second layer of corporate tax.

Qualifying holdings generally require ownership of at least 10% of the equity in a subsidiary, or an investment value exceeding €1.164 million held for a minimum of 183 days. Once these thresholds are satisfied, both dividend income and gains on disposal of shares are exempt from tax in the hands of the holding entity.

A foreign investor holds 15% of a non-EU subsidiary valued at €5 million. Upon selling that stake for €7 million, the €2 million capital gain is fully exempt from Maltese corporate tax under the participation exemption, resulting in zero tax due at the holding company level on that transaction.

This structure suits businesses that consolidate ownership of multiple international subsidiaries under a single EU-domiciled entity, as it eliminates tax leakage between group tiers.

English as an Official Business Language

Malta's status as a bilingual country, with both Maltese and English holding official language recognition under the Constitution of Malta, is a direct operational advantage for foreign business owners. English serves as the primary language of commerce, law, and government administration. Corporate documents, court proceedings, regulatory filings with the Malta Financial Services Authority (MFSA), and the Companies Act (Cap. 386) are all available and enforceable in English.

For a foreign-incorporated entity or an entrepreneur forming a new structure here, this eliminates the cost and delay associated with certified translations. Contracts drafted in English carry full legal weight without requiring a parallel Maltese version.

The practical effect extends to day-to-day operations:

- Local legal counsel, accountants, and corporate service providers work natively in English

- Statutory forms submitted to the Malta Business Registry are in English

- Regulatory correspondence from the MFSA is conducted in English

This means your legal and compliance workflows remain consistent with those in other English-speaking jurisdictions, reducing friction when coordinating across a multi-jurisdictional structure.

While English is fully operative in legal and regulatory contexts, certain official government communications may still be issued in Maltese, so confirming language preferences with your local service provider is advisable.

Robust Regulatory Framework via MFSA

The Malta MFSA regulatory framework benefits foreign business owners by providing a clearly structured, EU-aligned supervisory environment that reduces legal uncertainty. The Malta Financial Services Authority, established under the Malta Financial Services Authority Act of 1988, serves as the single regulator for banking, insurance, investment services, and other financial activities. Having one unified authority means your business interacts with a single point of accountability rather than multiple overlapping agencies.

Recognised Authorisations Across the EU

Because the MFSA operates within the EU regulatory architecture, licences and authorisations granted in Malta can carry passporting rights under applicable EU directives, including MiFID II, AIFMD, and Solvency II. This means a firm authorised by the MFSA may conduct regulated activities across other EU member states without obtaining separate local licences in each jurisdiction. For fund managers, payment institutions, or insurance undertakings, that reach has direct operational value.

Predictable Enforcement Standards

MFSA oversight follows published rulebooks, including the Investment Services Rules and the Banking Rules, which set out licensing conditions, capital requirements, and ongoing obligations in explicit terms. Regulators operating under codified frameworks apply rules consistently, which makes compliance planning more predictable for foreign-owned entities. This contrasts with jurisdictions where regulatory decisions depend heavily on administrative discretion.

Proportionate Structure for Smaller Operators

Certain MFSA licensing categories, such as the Recognised Incorporated Cell Company framework or the Notified Alternative Investment Fund regime, are structured to accommodate smaller operators without requiring the same capital thresholds as full authorisation. This tiered approach allows earlier-stage businesses to enter regulated activity without disproportionate upfront compliance costs.

Strategic Mediterranean Location and Connectivity

Sitting at the crossroads of Europe, North Africa, and the Middle East, Malta's Mediterranean location business advantages are largely geographic in nature. The island lies roughly 90 kilometres south of Sicily and approximately 300 kilometres north of the Libyan coast, placing it within short reach of three distinct economic regions simultaneously. For businesses managing multi-regional operations, that physical position reduces friction across time zones, shipping routes, and in-person meetings.

Malta International Airport connects the island to over 50 countries through direct routes, with frequent services to major European, North African, and Gulf hubs. The Port of Valletta functions as a transshipment point in the central Mediterranean, which is relevant for firms in logistics, trade finance, or physical goods distribution.

As an EU member state, entities incorporated here carry European legal standing when dealing with counterparties in the Middle East and Africa who treat EU jurisdiction as a credibility signal. That dual-facing position, European on paper and Mediterranean in practice, is a structural feature that few EU jurisdictions can replicate.

Time zone alignment is also a practical factor. The CET/CEST time zone means Maltese business hours overlap with both Gulf business days and standard European working hours, reducing scheduling gaps for firms operating across those regions. Consider the practical implications for your business:

- Direct air links to Dubai, Cairo, Tunis, and major European capitals

- Port access relevant to Mediterranean trade and logistics operations

- EU legal standing accepted by counterparties across Africa and the Middle East

- Overlap with Gulf and European business hours within a single working day

Why Malta Stands Out Among EU Jurisdictions

Foreign investors evaluating Malta for incorporation typically compare it against Ireland, Cyprus, and the Netherlands — three EU jurisdictions that target a similar profile of international holding structures, IP-holding entities, and trading companies. Each offers EU membership and treaty access, yet the specific combination of tax mechanics, official language, and regulatory structure differs in ways that affect the practical cost and complexity of operating a foreign-owned entity.

What the comparison reveals is not that Malta's advantages are unique in isolation, but that their convergence in a single jurisdiction is uncommon. An effective 5% corporate tax rate, achieved through the full imputation system and shareholder refund mechanism under the Income Tax Act, sits at the lower bound among EU members. Ireland's 12.5% trading rate and Cyprus's 12.5% headline rate both exceed Malta's effective rate for qualifying refund structures. The absence of withholding tax on dividends paid to non-resident shareholders also holds without a minimum shareholding threshold — a condition that applies in varying degrees elsewhere in the EU.

| Parameter | Malta | Ireland | Cyprus | Netherlands |

|---|---|---|---|---|

| Effective Corporate Tax Rate | ~5% (post-refund) | 12.5% (trading) | 12.5% | 19–25.8% |

| Withholding Tax on Dividends | 0% | 25% (standard) | 0% | 15% (standard) |

| Official Business Language | English | English | Greek / English | Dutch |

| EU Member | Yes | Yes | Yes | Yes |

| Participation Exemption Available | Yes | Yes (substantial) | Yes | Yes |

Compliance Services for Companies in Malta

Maintain your Maltese company's good standing with ongoing compliance support, including annual returns, statutory filings, and regulatory obligations under Maltese law.

Conclusion

Malta's tax architecture, built around the full imputation system and the 5% effective corporate rate achieved through shareholder refund mechanisms, gives foreign-owned entities a structural cost advantage that few EU jurisdictions can replicate through standard rate competition alone. Combined with the absence of withholding tax on outbound dividends, a holding company established under Maltese law can repatriate profits to non-resident shareholders without the friction that typically accompanies cross-border distributions.

The benefits of incorporating in Malta are most pronounced for businesses where IP ownership, dividend flows, or group holding structures generate the bulk of value. The participation exemption under the Income Tax Act further insulates qualifying investors from double taxation on both dividends and capital gains, making the framework particularly coherent for multi-tiered corporate groups.

That said, the optimal fit depends on your business structure, the jurisdictions where your customers or assets are located, and the nature of your income. A trading company with purely domestic operations will interact with this framework differently than a holding entity managing cross-border investments. Understanding which benefits apply to your specific circumstances is the first step toward a formation that performs as intended.

Start Your Malta Company Formation With Expanship

Starting your Malta company formation with Expanship means working with a team that understands the specific mechanics covered throughout this blog — from the 5% effective tax rate achieved through the full imputation and refund system, to the participation exemption on qualifying dividends and capital gains, to the regulatory environment administered by the Malta Financial Services Authority. The entity structures available under the Companies Act, Cap. 386, each carry distinct compliance obligations, and Expanship's engagement is built around those obligations, not generic corporate administration.

From document preparation to post-incorporation filings, the scope of services covers the full formation and maintenance cycle:

- Memorandum and Articles of Association drafting and notarisation

- Registered office and resident company secretary provision under Cap. 386 requirements

- Submission to and liaison with the Malta Business Registry

- Ongoing statutory compliance management, including annual returns and director filings

- Apostille and document legalisation coordination

- Banking introduction assistance with locally licensed credit institutions

Incorporate in Malta through Expanship and you have a defined point of contact for every stage, from the initial registry filing to ongoing MFSA-related obligations where applicable.

Expanship Malta is available to answer jurisdiction-specific questions and begin the formation process.

Frequently Asked Questions (FAQ)

The standard corporate tax rate in Malta is 35%, but non-resident shareholders are entitled to claim a refund of 6/7ths of the tax paid at the company level upon distribution of dividends, reducing the effective rate to approximately 5%. This refund is governed by the Income Tax Act and the Income Tax Management Act and is paid directly to the shareholder by the Maltese tax authorities. The 6/7ths refund applies to trading income; different refund fractions apply to passive income and royalties.

No statutory requirement mandates a Maltese-resident director for a standard private limited company under the Companies Act, Chapter 386. However, tax residency and substance considerations under the MFSA's guidance and OECD standards may require sufficient local management and control to establish genuine tax residency in Malta. Appointing at least one local director is therefore a common practice for companies seeking to establish verifiable substance.

Under Maltese tax law, dividends received from a qualifying participating holding are exempt from tax at the company level, provided certain conditions are met, including that the Maltese company holds at least 5% of the equity in the subsidiary or satisfies one of several alternative qualifying criteria. Capital gains on the disposal of a qualifying participating holding can also be exempt under the same provisions. Where the exemption applies, the income is not included in the company's chargeable income, removing the tax liability entirely rather than reducing it through a refund.

No withholding tax is imposed on dividends distributed by a Maltese company to non-resident shareholders under current Maltese tax legislation. This applies regardless of whether a double tax treaty exists between Malta and the shareholder's country of residence. The absence of withholding tax is a feature of domestic law, not solely a treaty benefit.

Incorporation through the Malta Business Registry typically takes between two and five business days once all required documentation is submitted in proper form. The timeframe can extend if the proposed company name requires additional clearance or if submitted documents need amendment. Preparation of the Memorandum and Articles of Association, identity verification, and payment of registration fees must all be completed before the Registry processes the application.

The full imputation and shareholder refund system has been in place since Malta's EU accession in 2004 and has not been formally designated as incompatible state aid by the European Commission. The system applies uniformly to all shareholders based on the source of income rather than targeting specific companies or nationalities. That said, EU regulatory positions can evolve, and businesses should monitor any developments from the Commission regarding member state tax regimes.

The Malta Financial Services Authority (MFSA) is the single regulator for financial services in Malta, covering banking, investment services, insurance, and collective investment schemes. It operates under the Malta Financial Services Authority Act and issues licences, sets conduct requirements, and exercises ongoing supervisory oversight. Companies providing regulated financial services must obtain the appropriate MFSA authorisation before commencing operations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.