Key Takeaways

- Business entities in the CNMI are registered through the Division of Corporations and Business Licensing under the Department of Commerce, which oversees all domestic and foreign entity filings.

- The LLC is the most commonly registered entity in the Northern Mariana Islands due to its pass-through taxation structure and comparatively lower administrative requirements.

- Foreign corporations and foreign LLCs can extend their existing legal structures into the CNMI through a registration process rather than forming a new domestic entity.

- General partnerships carry unlimited personal liability for all partners, while limited partnerships allow passive investors to participate in a CNMI business without operational exposure.

Introduction to Entity Types in Northern Mariana Islands (MP)

Located in the western Pacific Ocean, the Commonwealth of the Northern Mariana Islands (CNMI) is a self-governing U.S. territory and part of the Micronesia island group, situated north of Guam and east of the Philippines. Its political relationship with the United States means federal law applies in many areas, while the territory retains authority over local business registration and certain tax matters through its own legislature.

Business entities in the CNMI are registered through the CNMI Division of Corporations and Business Licensing, which sits under the Department of Commerce. The territory operates a territorial tax system, with residents and local businesses subject to a mirrored version of the U.S. Internal Revenue Code administered locally.

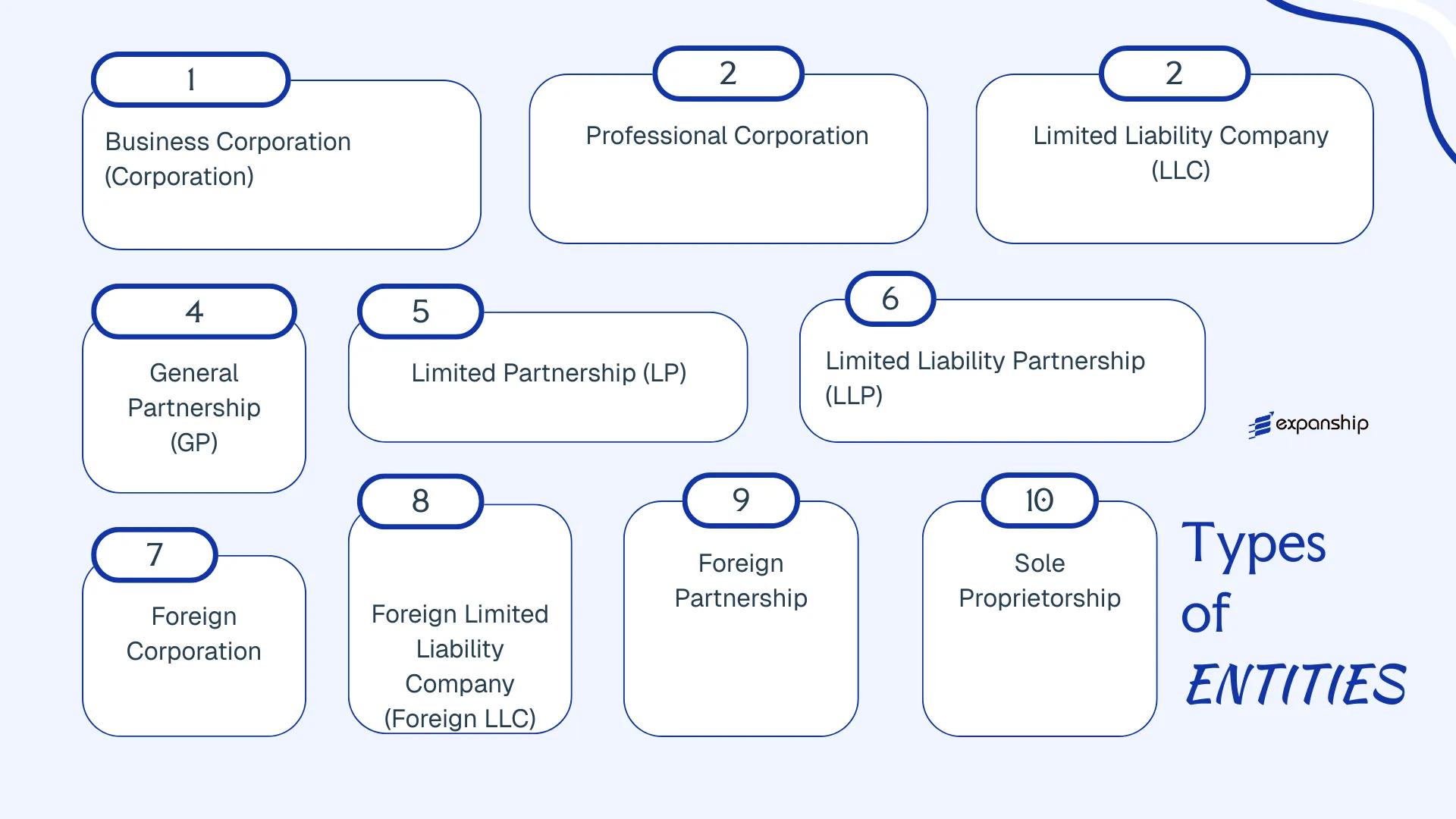

Understanding the available business entity types in Northern Mariana Islands is the starting point for any firm considering operating in or from the CNMI. The main CNMI business structures recognized under local law include:

- Business Corporation

- Professional Corporation

- Limited Liability Company (LLC)

- General Partnership

- Limited Partnership

- Limited Liability Partnership (LLP)

- Foreign Corporation, Foreign LLC, and Foreign Partnership

- Sole Proprietorship

Each structure carries distinct formation requirements, liability implications, and tax treatment — all of which this article addresses in turn.

An Overview of Business Structures in Northern Mariana Islands (MP)

The CNMI Business Corporation Act, the LLC Act, and related partnership statutes collectively govern the available entity types under commonwealth law. An overview of business structures in CNMI reveals six principal formations: the business corporation, the professional corporation, the limited liability company, the general partnership, the limited partnership, the limited liability partnership, and the sole proprietorship. Each structure carries distinct implications for liability, taxation, and operational requirements.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Business Corporation | Separate legal entity | Limited to investment | Pass-through or corporate | Permitted | 1 shareholder | CNMI DCCA | CNMI Business Corporation Act |

| Professional Corporation | Separate legal entity | Limited (profession-specific) | Corporate level | Licensed professions only | 1 shareholder | CNMI DCCA | CNMI Business Corporation Act |

| LLC | Hybrid legal entity | Members limited | Pass-through default | Permitted | 1 member | CNMI DCCA | CNMI LLC Act |

| General Partnership | Unincorporated association | Unlimited, joint | Pass-through | Permitted | 2 partners | CNMI DCCA | CNMI Partnership Act |

| Limited Partnership | Unincorporated association | Mixed (general/limited) | Pass-through | Permitted | 2 partners | CNMI DCCA | CNMI LP Act |

| LLP | Unincorporated association | Limited for partners | Pass-through | Permitted | 2 partners | CNMI DCCA | CNMI Partnership Act |

| Sole Proprietorship | Unregistered | Unlimited, personal | Personal income tax | Permitted | 1 individual | CNMI DCCA / Tax Division | No dedicated statute |

Each of these structures is examined in full in the sections below.

Corporation (Business Corporation, Professional Corporation)

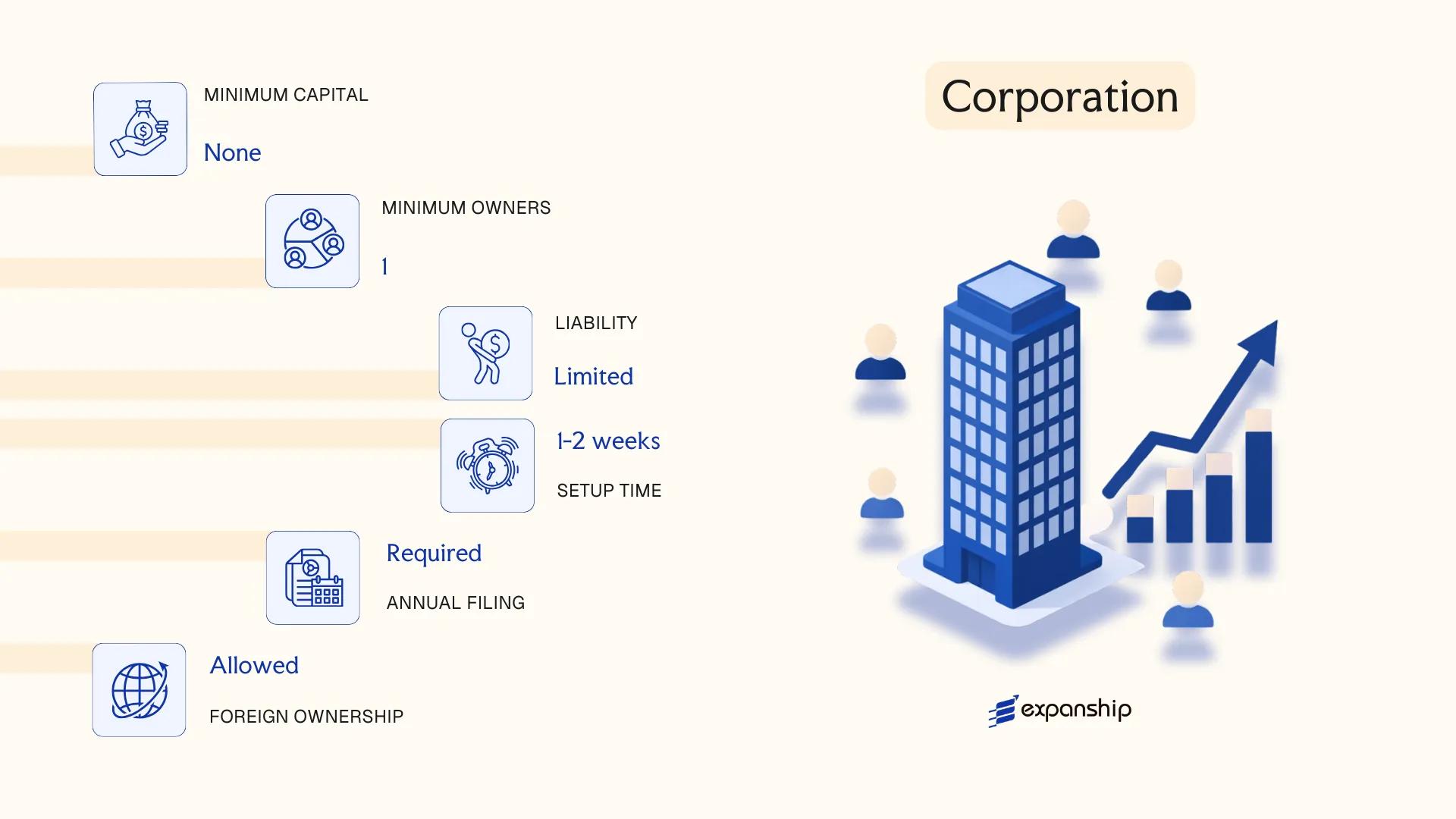

To incorporate a corporation in Northern Mariana Islands, you must comply with the CNMI Business Corporation Act, which governs the formation and operation of domestic corporations under Title 4 of the Commonwealth Code. A corporation exists as a separate legal entity, meaning the business holds its own rights and obligations distinct from its shareholders.

Liability exposure for shareholders is limited to their capital contribution. The structure suits both resident and non-resident founders, though certain ownership and activity restrictions apply under CNMI land and licensing laws.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | For-profit corporation | Governed under Title 4, CNMI Commonwealth Code |

| Members | Shareholders (min. 1), Directors (min. 1), Officers required | No maximum on shareholders; sole director permitted |

| Local Presence | Registered Agent with CNMI address required | Registered office must be maintained in the Commonwealth |

| Capital | USD; no statutory minimum | Authorized shares must be stated in Articles of Incorporation |

| Privacy | Director and officer names filed publicly | Shareholder details not required in public filings |

Focus Points

- Taxation: CNMI operates a mirrored U.S. federal income tax system; corporations are subject to CNMI income tax at rates mirroring federal schedules, with no separate VAT or general sales tax at the corporate level; withholding taxes apply to certain payments.

- Annual Compliance: Annual report filing and registered agent maintenance required with the CNMI Commonwealth Register of Corporations.

- Restrictions: Non-U.S. citizens face land ownership restrictions under the CNMI Constitution, which can affect real-property-holding structures.

- Conversion: A corporation may convert to an LLC under CNMI statutory procedures, subject to creditor protections.

Sub-Types

Business Corporation

The standard for-profit entity used for trading, holding, and general commercial activity. Northern Mariana Islands business corporation formation follows the standard Title 4 procedures, with no sector-specific licensing embedded in the formation process itself.

Professional Corporation

CNMI professional corporation registration applies to licensed professionals — including attorneys, physicians, and accountants — who wish to practice within a corporate structure. The distinguishing feature is that all shareholders must hold a valid professional license in the relevant field, and the entity's permissible activities are restricted to that profession.

Closing

A corporation is well-suited for trading operations, IP holding, and ventures requiring a clear capital structure with defined investor roles. The mirrored federal tax system provides familiarity for U.S.-connected businesses, though the land ownership restrictions present a structural constraint for real-estate-focused entities.

U.S.-affiliated businesses and licensed professionals seeking limited liability within a familiar federal-mirror tax framework.

Company Incorporation in Northern Mariana Islands

Incorporate a corporation or other business entity in the CNMI with Expanship's end-to-end formation support.

Limited Liability Company (LLC)

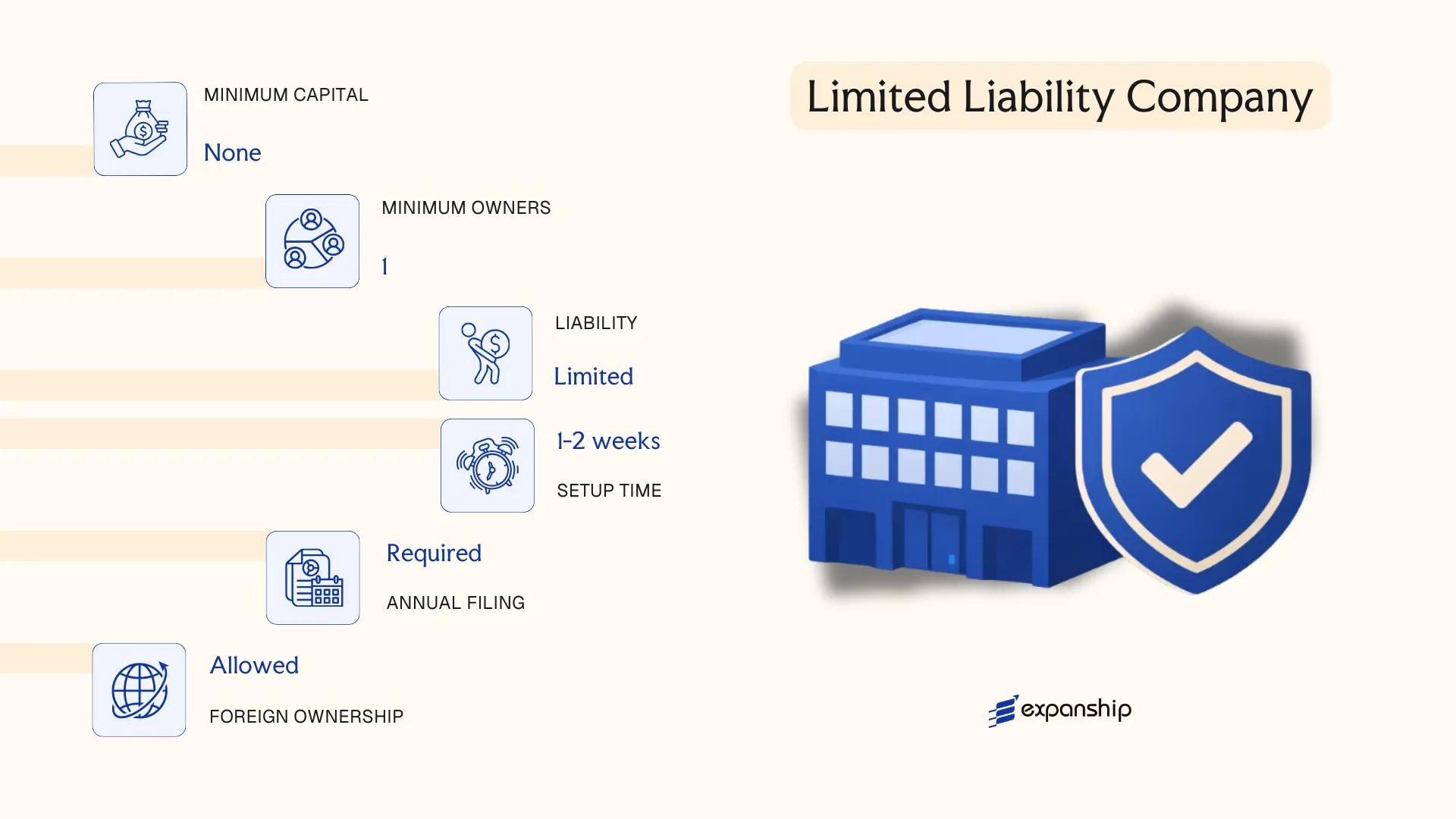

To form an LLC in Northern Mariana Islands, the process is governed by the CNMI Limited Liability Company Act, codified under Title 4 of the Commonwealth Code. The entity carries separate legal personality, shielding its members from personal liability for company debts, while allowing the flexibility of pass-through taxation typical of partnership structures.

Registration is filed with the CNMI Department of Commerce, Corporations Division. A CNMI LLC operating agreement is not required by statute to be filed publicly, but it serves as the governing document between members and should be drafted before operations begin.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Hybrid structure: corporate liability shield with partnership-style taxation |

| Members | Minimum 1; no maximum | Members may manage directly or appoint a manager |

| Local Presence | Registered Agent required; registered office in CNMI | Registered agent must have a physical CNMI address |

| Capital | USD; no statutory minimum | Contributions may be cash, property, or services |

| Privacy | Member names not always publicly disclosed | Operating agreement remains private |

Focus Points

- Taxation: No federal corporate income tax at the entity level; CNMI imposes its own income tax mirror system, and distributions may be subject to local tax; no VAT or general sales tax at the Commonwealth level.

- Annual Compliance: Annual report and fee due to the Corporations Division; failure to file risks administrative dissolution.

- Economic Substance: No formal economic substance regime currently enacted in CNMI.

- Treaty Access: CNMI is a U.S. territory but does not benefit from U.S. tax treaties in the same manner as states; consult a tax adviser before relying on treaty positions.

- Conversion: Existing entities may convert to LLC form under the Commonwealth Code, subject to filing requirements.

Closing

The LLC structure suits holding arrangements, small trading operations, and service businesses where liability protection without corporate formality is the priority. Its pass-through tax treatment is an operational advantage, though the limited treaty access compared to a domestic U.S. state entity can complicate cross-border structuring.

Best suited for small to mid-size businesses, foreign investors seeking a U.S.-territory presence, or holding structures where simplified governance and liability protection are the primary requirements.

Partnership Structures [General Partnership, Limited Partnership, Limited Liability Partnership]

Partnership structures in Northern Mariana Islands are governed by the CNMI Business Corporation Act and related partnership statutes codified under Commonwealth law. Three recognized forms exist: the general partnership (GP), limited partnership (LP), and limited liability partnership (LLP), each carrying distinct liability implications for partners.

Registered through the CNMI Department of Commerce, Division of Corporations, each structure requires filing the appropriate formation documents. Northern Mariana Islands general partnership formation involves no formal registration requirement, though limited partnerships and LLPs must file with the Division to achieve their respective liability protections.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (non-corporate) | LPs and LLPs have limited statutory liability protections; GPs do not |

| Members Referred To As | Partners (general/limited) | GPs have general partners only; LPs have at least one general and one limited partner |

| Minimum Members | GP: 2 partners; LP: 2 partners; LLP: 2 partners | No statutory maximum on partner count |

| Local Presence | Registered Agent with CNMI address required for LP and LLP | GP has no formal registration requirement |

| Capital | No minimum capital prescribed; USD denomination applies | Capital contributions defined by partnership agreement |

| Privacy | Partner names disclosed in formation filings for LP and LLP | GP agreements are private documents |

Focus Points

- Taxation: Partnerships are generally pass-through entities under CNMI tax law; partners report income individually and pay the applicable local income tax rate, with no entity-level corporate income tax, VAT, or withholding tax on distributed profits.

- Annual Compliance: LPs and LLPs must file annual reports with the Division of Corporations and maintain a registered agent; GPs face no equivalent statutory filing obligation.

- Economic Substance: No formal economic substance regime currently applies to partnerships in the CNMI.

- Conversion: Commonwealth statutes permit conversion between partnership types through formal filing with the Division of Corporations.

- Restrictions: General partners in both GPs and LPs bear unlimited personal liability for partnership obligations; only LLP status and limited partner classification offer liability limitation.

Sub-Types

General Partnership (GP)

A GP carries no separate legal personality distinct from its partners and requires no formal registration. It is commonly used for small, informal business arrangements where all partners actively participate in management and accept unlimited liability.

Limited Partnership (LP)

An LP separates passive investors (limited partners) from active managers (general partners). CNMI limited partnership requirements include filing a certificate of limited partnership with the Division of Corporations, making it suitable for investment ventures.

Limited Liability Partnership (LLP)

CNMI limited liability partnership registration shields partners from personal liability for the wrongful acts of other partners. This structure is most frequently used by professional service firms such as law and accounting practices.

Closing

Partnership structures suit joint ventures, professional service firms, and investment arrangements where pass-through taxation is a priority, though the unlimited liability exposure of general partners in GPs and LPs remains a significant structural drawback.

Partnership structures in the CNMI are best suited for professionals and co-investors seeking pass-through taxation, provided liability exposure is carefully managed through an LLP structure or limited partner classification.

Foreign Business Entities [Foreign Corporation, Foreign LLC, Foreign Partnership]

To register a foreign business entity in CNMI, you must comply with the foreign qualification requirements set out in the Commonwealth Business Corporation Act and the corresponding provisions governing LLCs and partnerships under CNMI Title 4 of the Commonwealth Code. A foreign entity does not form a new legal structure locally — it registers its existing legal personality to conduct business within the Commonwealth, retaining the liability protections and governance rules of its home jurisdiction.

Qualification is required before a foreign firm can transact business in the CNMI. The Department of Commerce, Corporations Division administers the registration process, which requires a Certificate of Good Standing from the home jurisdiction, a registered agent appointed within the Commonwealth, and the filing of an Application for Certificate of Authority.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Foreign-qualified entity (corporation, LLC, or partnership) | Retains home-jurisdiction legal personality |

| Local Representatives | Registered Agent required | Must have a physical CNMI address |

| Governing Authority | CNMI Department of Commerce, Corporations Division | Administers foreign qualification filings |

| Home Jurisdiction Proof | Certificate of Good Standing | Must accompany the qualification application |

| Capital | No separate local capital requirement | Home-jurisdiction capital rules apply |

| Privacy | Officers/managers publicly listed in filings | No nominee framework specific to foreign qualification |

Focus Points

- Taxation: Foreign entities operating in CNMI are subject to the same local income tax obligations as domestic entities for income sourced within the Commonwealth; no separate VAT or withholding tax regime applies at the territorial level beyond standard federal tax mirror rules.

- Annual Compliance: Foreign entities must file annual reports with the Corporations Division and maintain a continuously appointed registered agent to remain in good standing.

- Restrictions: Certain regulated industries — including insurance and banking — require separate licensing beyond the standard Certificate of Authority.

- Treaty Access: CNMI's status as a U.S. territory means foreign entities benefit from applicable U.S. tax treaties to the extent those treaties cover territorial operations, though application can be fact-specific.

- Withdrawal: A foreign entity ceasing CNMI operations must formally file a withdrawal application; simply stopping activity does not terminate registration obligations.

Closing

Foreign qualification suits businesses already incorporated elsewhere that need a defined legal presence in the CNMI for trading, service delivery, or contractual purposes, with the primary limitation being that the entity remains bound by two compliance regimes simultaneously — its home jurisdiction and the Commonwealth.

Foreign qualification is most appropriate for established companies incorporated in the U.S. mainland or another jurisdiction that require a formal CNMI presence without restructuring their existing corporate form.

Sole Proprietorship

A sole proprietorship Northern Mariana Islands setup is the most straightforward form of business registration available in the CNMI. It does not constitute a separate legal entity from its owner — the individual and the business are treated as one and the same under the law. This means personal assets carry full exposure to any business liabilities incurred.

Registration falls under the jurisdiction of the CNMI Department of Commerce, Division of Corporations. A business trade name, if different from the owner's legal name, must be registered as a fictitious business name with that office. CNMI sole proprietor registration does not require articles of incorporation or a formal organizational document.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole trader | No separate legal personality from the owner |

| Members | Single proprietor | No minimum capital members; one individual only |

| Local Presence | Business license required; no registered agent mandated | License issued through CNMI Department of Commerce |

| Capital | No statutory minimum; USD transactions | Owner funds the business directly |

| Privacy | Owner's name tied to the business | Fictitious name filing offers limited name separation |

Focus Points

- Taxation: Subject to U.S. federal income tax obligations; CNMI mirrors federal tax rules under the Covenant, with local income tax filed with the CNMI Division of Revenue and Taxation — no separate corporate tax, VAT, or withholding tax applicable at entity level.

- Annual Compliance: Business license renewal required annually through the Department of Commerce; no annual report filing separate from tax obligations.

- Liability Exposure: Unlimited personal liability; no statutory shield exists for debts or legal claims against the business.

- Conversion: Can be converted into an LLC or corporation by formally incorporating and transferring business assets, though no automatic statutory conversion mechanism exists for sole proprietorships.

- Treaty Access: As a U.S. territory, CNMI does not independently access tax treaties; U.S. federal treaty provisions may apply depending on the owner's residency status.

Closing

Starting a sole proprietorship in CNMI suits straightforward service or retail operations where administrative simplicity is the priority, though the absence of liability protection makes it unsuitable for ventures carrying meaningful financial or legal risk.

Resident individuals operating low-risk, owner-operated businesses — such as freelancers, tradespeople, or small local vendors — who do not require liability separation.

How to Choose the Right Entity Type in Northern Mariana Islands (MP)

Choosing the right business entity in CNMI is a structural decision with direct legal and financial consequences — not a formality.

Why Your Entity Choice Matters

Selecting the wrong structure can produce concrete, costly outcomes:

- Registering a foreign entity when your operations are locally directed means you are trading in breach of the CNMI Business Corporations Act, which can result in administrative penalties or involuntary dissolution.

- Choosing a structure without legal personality or treaty eligibility prevents your business from claiming withholding tax reductions under any applicable U.S. federal tax arrangements that flow through CNMI.

- Forming a corporation when a single-member LLC would suffice binds you to mandatory board formalities, annual shareholder meetings, and record-keeping obligations that do not apply to member-managed LLCs.

- Selecting an entity type that requires audited financials for a one-person consultancy introduces recurring professional costs with no regulatory benefit.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each point to a distinct structure under CNMI law.

- Ownership and Management: Single-member operations suit a member-managed LLC, while multi-party ventures may require a corporation's defined governance framework.

- Tax Objectives: CNMI operates its own mirror tax system; your chosen structure affects whether income is taxed locally, federally, or both.

- Local vs. External Operations: Entities transacting with CNMI residents must be locally registered in good standing with the CNMI Department of Commerce.

- Exit Strategy: Not all CNMI entity types permit redomiciliation or conversion; verify this under the CNMI Business Corporations Act before formation.

- Privacy Requirements: Director and member information filed with the Department of Commerce may be subject to public disclosure; assess whether nominee arrangements are appropriate.

Compliance Services for Companies in the Northern Mariana Islands

Maintain your entity's good standing with the CNMI Department of Commerce through structured compliance support.

Conclusion

Selecting the right structure is one of the most consequential decisions in any Northern Mariana Islands business incorporation summary. The corporation suits firms seeking investment capital or professional licensing, while the LLC remains the most commonly registered entity due to its pass-through taxation and reduced administrative burden. General partnerships carry unlimited personal liability and are typically used for informal ventures, whereas limited partnerships allow passive investors to participate without operational exposure. The LLP provides liability separation for licensed professionals operating collectively.

Regulatory oversight under the CNMI Division of Corporations has grown more consistent in recent years, and the jurisdiction's federal integration with U.S. standards continues to shape its compliance trajectory. For foreign entities, registration as a foreign corporation or foreign LLC extends existing structures into CNMI without forming a new domestic company. Understanding which structure aligns with your business activity determines both your compliance obligations and your long-term operational flexibility.

How Expanship Can Assist You

Expanship company formation services CNMI cover the full range of entity structures available under CNMI law, from domestic corporations and LLCs governed by the CNMI Business Corporation Act to limited partnerships and foreign entity registrations filed with the CNMI Department of Commerce, Corporations Division. Your specific structure determines which compliance obligations apply, and Expanship's work begins with getting that foundation right.

From initial document preparation through to ongoing post-incorporation requirements, we handle the operational details so your business can move forward:

- Document preparation and notarization or legalization

- Registered agent and local office provision in Saipan

- Government filing and liaison with the Corporations Division

- Post-incorporation compliance management, including annual reporting

- Banking introduction assistance for CNMI-based accounts

Reach out to Expanship MP to discuss your requirements directly with our corporate services team.

Frequently Asked Questions (FAQ)

The LLC is the most frequently formed business structure in the Commonwealth. Its combination of pass-through taxation and limited liability protection makes it practical for both resident entrepreneurs and foreign investors operating in the territory.

A corporation issues shares and is governed by a board of directors under the CNMI Corporations Act, while an LLC is managed by members or designated managers under the Limited Liability Company Act of 1996. Corporations face potential double taxation unless S-Corp status applies federally, whereas LLC income passes directly to members. Corporations also carry heavier annual compliance requirements, including mandatory shareholder meetings and formal record-keeping.

Among available structures, the LLC generally offers the greatest degree of privacy. Member information is not required on the public-facing certificate of organization filed with the CNMI Department of Commerce. Nominee manager arrangements are permissible under general agency principles, though their use does not affect underlying legal obligations.

A sole proprietorship and an LLC can each be formed by one individual. General partnerships and limited partnerships require at least two partners by definition. A corporation may technically be formed with one shareholder, though the statutory requirements for directors vary.

Foreign nationals may form or own LLCs and corporations in the CNMI without restriction on ownership percentage under general CNMI corporate statutes, subject to any applicable federal investment rules and the Covenant to Establish a Commonwealth. Alternatively, a foreign entity may register as a foreign corporation or foreign LLC rather than incorporating a new domestic entity. Certain regulated industries may impose additional licensing conditions regardless of entity type.

The CNMI Corporations Act and the Limited Liability Company Act of 1996 both provide mechanisms for conversion and merger between entity types. A corporation may convert to an LLC, and vice versa, through a formal plan of conversion filed with the Department of Commerce. The converted entity generally retains its existing contractual obligations and liabilities.

Corporations and LLCs both hold separate legal personality, meaning they can contract, hold property, and be sued independently of their owners. General partnerships do not automatically carry the same statutory separation, leaving partners personally exposed to business liabilities. Sole proprietorships have no legal distinction from the individual owner.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.