Key Takeaways

- The Limited Liability Company (Societatea cu Răspundere Limitată – SRL) is Moldova's most registered entity type, distinguished by its minimal capital requirements and eligibility for single-member ownership.

- Legal entity registration in Moldova falls under the authority of the State Registration Chamber (Camera Înregistrării de Stat), which operates under the Ministry of Justice.

- Foreign businesses entering Moldova can establish a branch office or representative office to maintain a local presence without forming a separate legal entity.

- Moldova's status as an EU candidate country continues to drive reforms across its corporate governance framework, including expanded double taxation treaty coverage governed by the Civil Code and Law No. 135/2007.

Introduction to Entity Types in Moldova

Moldova is a landlocked country in Eastern Europe, bordered by Romania to the west and Ukraine to the north, east, and south. It is an independent republic and a candidate country for European Union accession, a status that has shaped recent reforms to its commercial legislation. Registration of legal entities falls under the authority of the State Registration Chamber (Camera Înregistrării de Stat), which operates under the Ministry of Justice and maintains the public register of companies.

The country applies a territorial-based tax system with a standard corporate income tax rate, and has concluded a network of double taxation treaties that affects how foreign-owned structures are treated.

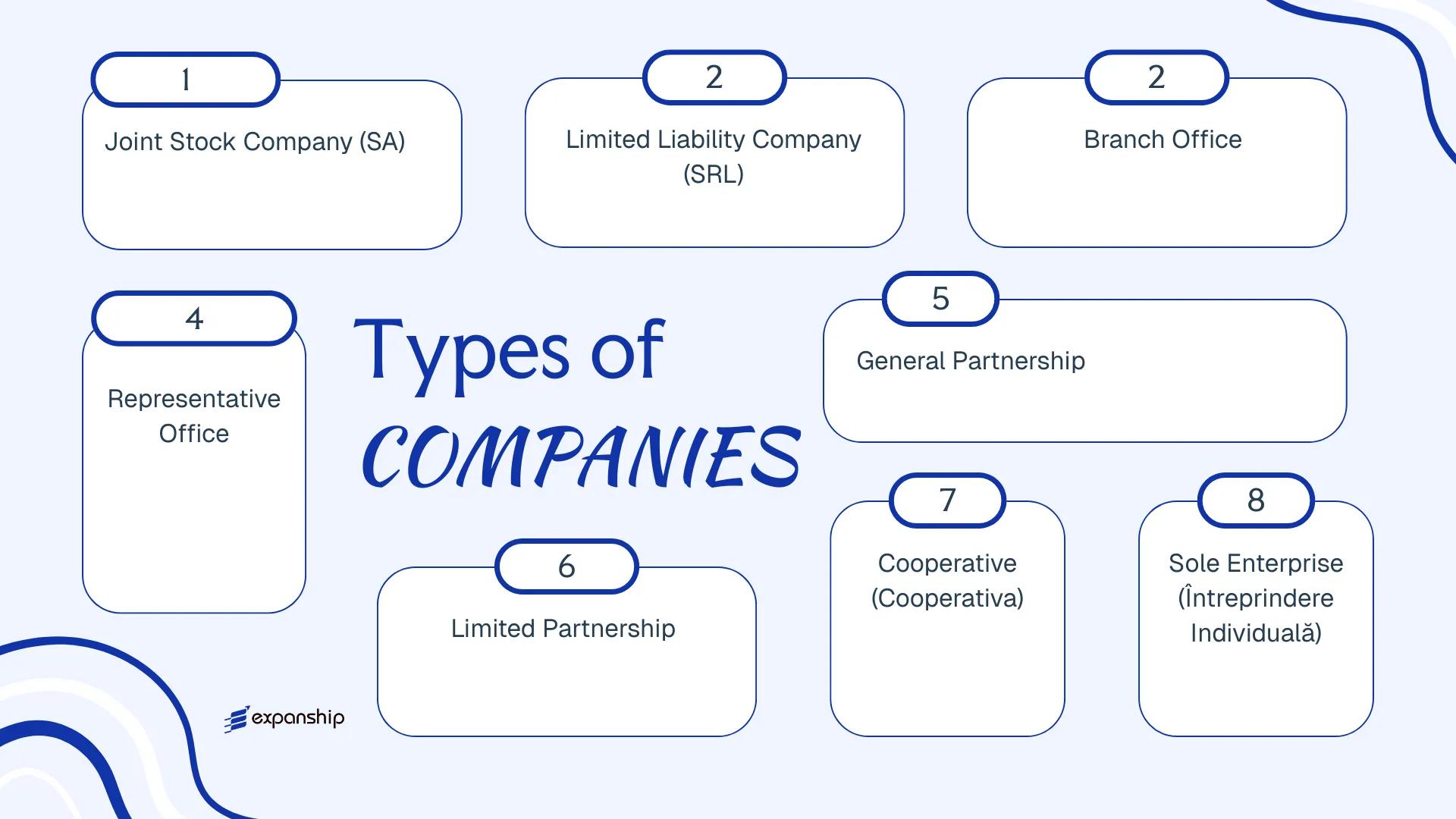

Several types of business entities in Moldova are available to both resident and non-resident founders. These include the Limited Liability Company (SRL), Joint Stock Company (SA), General Partnership, Limited Partnership, Cooperative, Sole Enterprise, Branch Office, and Representative Office. Each structure carries distinct requirements for capital, governance, and liability under the Law on Entrepreneurship and Enterprises and the Civil Code of the Republic of Moldova. This article examines each Moldovan legal entity structure in turn, covering formation requirements, ownership rules, and practical considerations for your business.

An Overview of Business Structures in Moldova

Moldovan company law recognises several distinct legal forms for conducting business, each governed primarily by Law No. 135/2007 on the Joint Stock Company, Law No. 845/1992 on Entrepreneurship and Enterprises, and the Civil Code of the Republic of Moldova. Each structure carries different rules on liability, governance, and permitted activities. The sections that follow examine each form in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Joint Stock Company (SA) | Corporate entity | Limited to share capital | Taxed | Yes | 1 shareholder | State Registration Agency | Law No. 135/2007 |

| Limited Liability Company (SRL) | Corporate entity | Limited to contribution | Taxed | Yes | 1–50 members | State Registration Agency | Civil Code; Law No. 845/1992 |

| Branch Office | Foreign entity extension | Parent bears liability | Taxed on local income | Yes | N/A | State Registration Agency | Civil Code |

| Representative Office | Non-trading entity | Parent bears liability | Generally exempt | No | N/A | State Registration Agency | Civil Code |

| General Partnership | Unincorporated firm | Unlimited, joint | Taxed | Yes | Min. 2 partners | State Registration Agency | Civil Code |

| Limited Partnership | Hybrid entity | Mixed liability | Taxed | Yes | Min. 2 partners | State Registration Agency | Civil Code |

| Cooperative | Member-owned entity | Limited | Taxed | Yes | Min. 5 members | State Registration Agency | Law on Cooperatives |

| Sole Enterprise | Individual-owned firm | Unlimited | Taxed | Yes | 1 individual | State Registration Agency | Law No. 845/1992 |

Each of these structures is examined in full in the sections below.

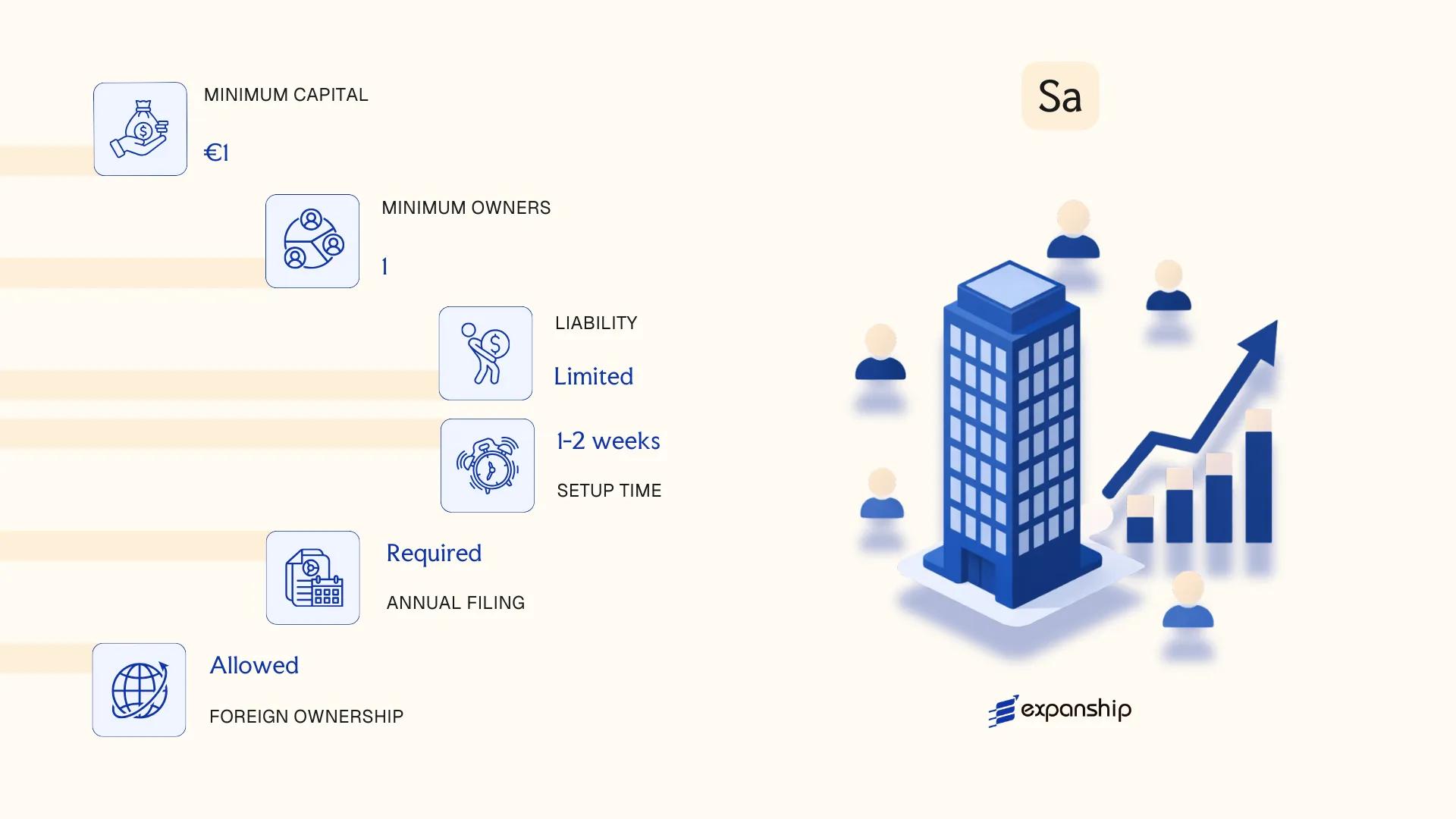

Joint Stock Company (Societatea pe Acțiuni – SA)

Governed by Law No. 1134-XIII on Joint Stock Companies (1997, as amended), the SA is Moldova's principal corporate vehicle for large-scale or publicly oriented business activity. Moldova SA joint stock company formation results in a separate legal entity in which shareholders bear no personal liability beyond their capital contribution.

Shares are freely transferable and may be distributed to an unrestricted number of holders, making the SA structurally suitable for raising external capital through public or private placements. The National Commission for Financial Markets (NCFM) oversees share issuance and securities-related compliance for this entity type.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Societatea pe Acțiuni (SA) | Separate legal personality; limited liability |

| Members | Shareholders; minimum 1 (closed SA) or unrestricted (open SA) | Board of Directors required if >50 shareholders |

| Local Presence | Registered legal address in Moldova | No statutory requirement for a local resident director |

| Share Capital | Minimum MDL 20,000 (closed); MDL 500,000 (open/public) | Must be fully subscribed at registration |

| Privacy | Shareholder register maintained by NCFM-licensed registrar | Register is not fully public but accessible to authorised parties |

| Governance | General Meeting of Shareholders; Board of Directors; executive body | Audit commission mandatory above statutory thresholds |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate; VAT registration required once turnover exceeds the statutory threshold; dividends distributed to non-residents attract withholding tax at rates potentially reduced under Moldova's bilateral tax treaties.

- Annual Compliance: Annual financial statements must be filed with the State Tax Service; publicly held SAs are additionally subject to NCFM reporting and audit requirements.

- Treaty Access: As a Moldovan tax-resident entity, the SA qualifies for benefits under Moldova's network of double taxation agreements, subject to substance conditions.

- Conversion: An SA may be reorganised into an SRL or other permitted legal form through a formal restructuring procedure under Moldovan civil and corporate law.

- Restrictions: Foreign ownership is generally unrestricted, though sector-specific licensing (banking, insurance, media) may impose additional conditions.

Sub-Types

Closed Joint Stock Company (SA Închisă)

Shares are distributed exclusively among a defined, closed group of shareholders and may not be publicly offered. This structure suits founder-controlled businesses or private investment vehicles where external market participation is not intended.

Open Joint Stock Company (SA Deschisă)

Shares may be offered to the public and traded, subject to NCFM registration and ongoing securities disclosure obligations. The higher minimum capital threshold of MDL 500,000 applies, reflecting the entity's capacity for broader capital mobilisation.

Recommendations

The SA suits holding structures, capital-intensive trading operations, and businesses anticipating future equity investment rounds or eventual public listing. Its principal advantage is unrestricted share transferability; the primary drawback is the comparatively heavy compliance burden, including mandatory audit and NCFM oversight for open structures.

The SA is most appropriate for businesses requiring scalable equity structures, institutional investment readiness, or eventual access to public capital markets.

Company Incorporation in Moldova

Incorporate a Joint Stock Company or other legal entity in Moldova with end-to-end support from Expanship.

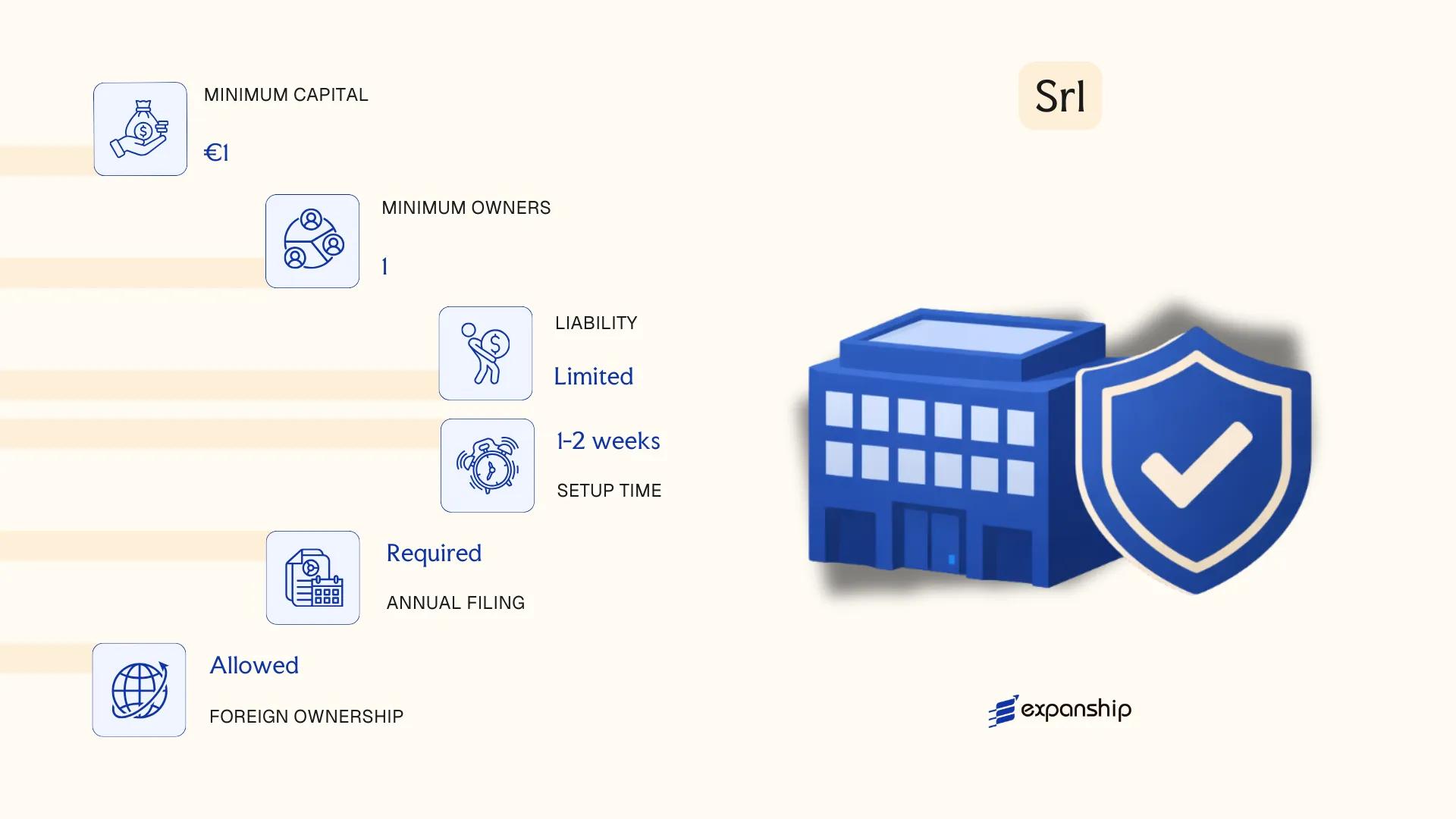

Limited Liability Company (Societatea cu Răspundere Limitată – SRL)

The SRL is the most widely used commercial structure for Moldova SRL limited liability company setup, governed primarily by Law No. 135/2007 on the Limited Liability Company. Each member's liability is restricted to their contribution to the share capital, and the entity holds a distinct legal personality separate from its founders.

Structured as a hybrid between a partnership and a corporation, the Societatea cu Răspundere Limitată Moldova offers operational flexibility without the disclosure requirements imposed on joint stock companies. Registration is processed through the State Registration Chamber (now administered under the Public Services Agency).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Separate legal personality; civil and commercial capacity |

| Members | 1–50 shareholders | Single-member SRL permitted; natural or legal persons |

| Management | Administrator (director) | Minimum one administrator; need not be a resident |

| Local Presence | Registered legal address in Moldova | Physical or registered agent address required |

| Share Capital | MDL 5,400 minimum | Must be fully subscribed at incorporation |

| Privacy | Member register filed with state | Beneficial ownership disclosed to authorities; not fully public |

Focus Points

- Taxation: Subject to 12% corporate income tax; standard VAT rate of 20% applies above the registration threshold; dividend withholding tax at 6% for residents; Moldova's treaty network may reduce withholding on cross-border payments.

- Annual Compliance: Annual financial statements must be submitted to the National Bureau of Statistics; tax returns filed with the State Tax Service.

- Economic Substance: No formal substance requirement, though genuine business activity is expected for treaty access.

- Conversion: An SRL may be reorganised into a joint stock company (SA) through a statutory reorganisation procedure under the Civil Code.

- Restrictions: Cannot exceed 50 shareholders; securities issued by an SRL may not be publicly offered.

Closing

The SRL suits trading operations, holding structures, and service businesses requiring a straightforward governance framework. Its low capital threshold and single-member option make entry accessible, though the 50-shareholder cap limits its use for broader equity arrangements.

Small to mid-sized businesses, foreign investors entering the Moldovan market, and entrepreneurs seeking a cost-efficient, privately held operating entity.

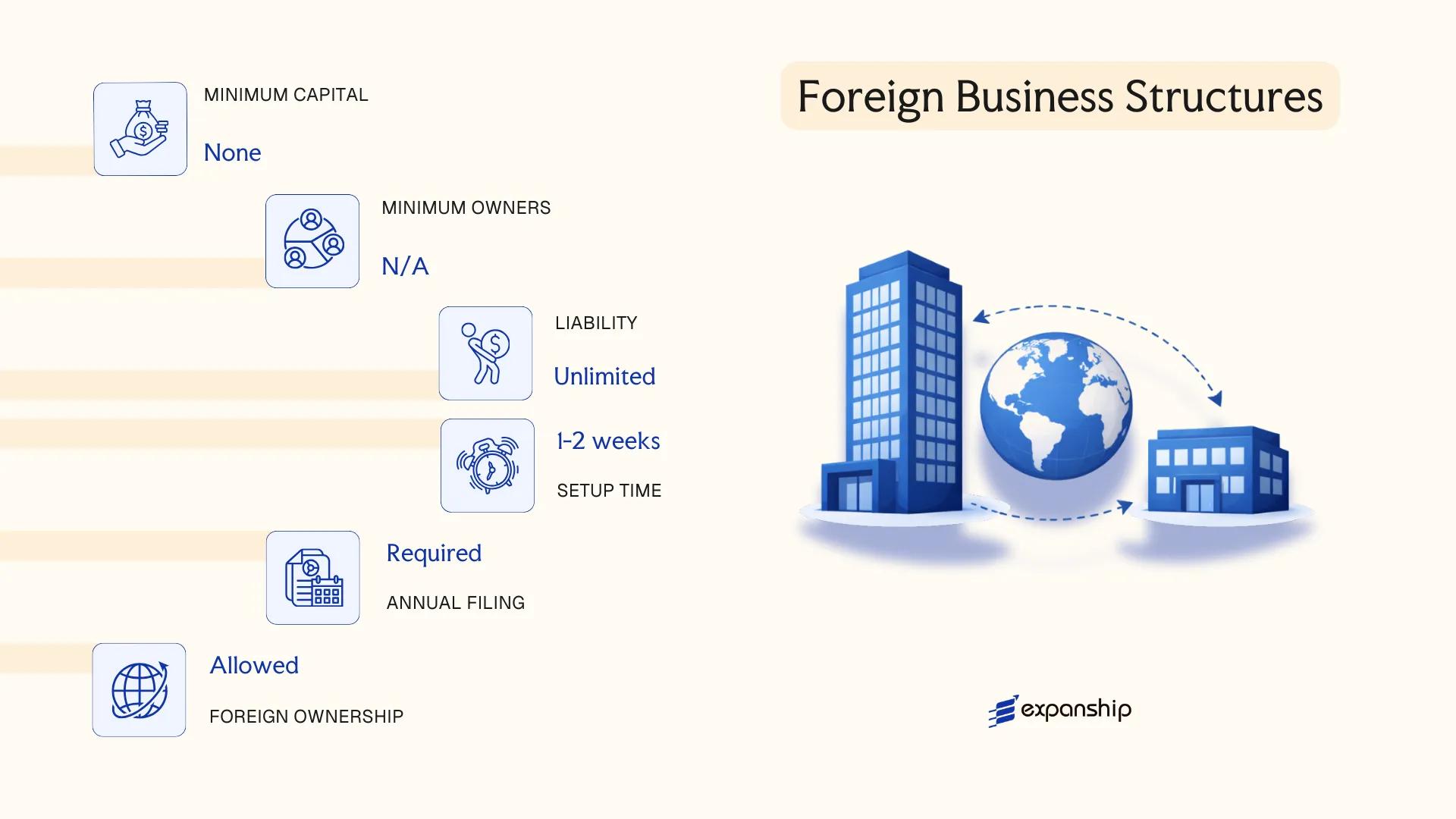

Foreign Business Structures in Moldova [Branch Office, Representative Office]

Opening a branch office in Moldova allows a foreign company to conduct commercial activities without forming a separate legal entity. Both branch offices and representative offices are governed by the Law on Entrepreneurship and Enterprises (No. 845/1992) and registered with the State Registration Chamber (now administered through the Agency of Public Services). Neither structure carries separate legal personality — the parent company retains full liability for obligations incurred.

Registration requires submission of the parent company's constituent documents, a resolution authorising establishment, and proof of the parent's legal existence in its home jurisdiction. A branch may generate revenue directly; a representative office is restricted to non-commercial functions such as market research, promotion, and liaison activities.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Commercial Activity | Permitted | Not permitted |

| Parent Liability | Full | Full |

| Registered Address | Required in Moldova | Required in Moldova |

| Capital Requirement | None prescribed | None prescribed |

| Head of Office | Appointed manager acting under notarised power of attorney | Appointed representative under power of attorney |

Focus Points

- Taxation: Branches are subject to Moldovan corporate income tax (12%) on locally sourced income; VAT at 20% applies to taxable supplies; representative offices with no revenue typically have no corporate tax liability but must still register with tax authorities.

- Annual Compliance: Both structures must file annual reports with the Agency of Public Services and maintain local accounting records under Moldovan accounting standards.

- Treaty Access: Access to Moldova's double tax treaties depends on whether the parent qualifies as a tax resident in a treaty partner country; treaty benefits are not guaranteed at the branch level without analysis.

- Duration and Renewal: Registration is granted for an indefinite term, though the authorisation document must reflect any changes in the parent company's structure or details.

- Restrictions: A representative office cannot sign commercial contracts, invoice clients, or repatriate profits in its own right.

Closing

Branch offices suit foreign firms testing the Moldovan market or executing specific project-based work, while representative offices serve companies needing a local presence for administrative or promotional purposes without commercial exposure. The absence of a minimum capital requirement reduces the setup barrier, but the parent's unlimited liability remains a significant structural risk.

Branch and representative offices are best suited for established foreign companies seeking a controlled, low-commitment entry point before committing to full local incorporation.

Partnerships in Moldova [General Partnership, Limited Partnership]

Governed by the Civil Code of the Republic of Moldova and the Law on Entrepreneurship and Enterprises (No. 845-XII, 1992), partnerships are among the oldest recognised business forms in the country. Moldova general partnership registration falls under two distinct structures: the Societate în Nume Colectiv (General Partnership) and the Societate în Comandită (Limited Partnership, or Moldova societate in comandita). Both forms carry separate legal personality, yet neither offers general liability protection to all participants.

Under the general partnership, all partners bear unlimited joint and several liability for the firm's obligations. The limited partnership Moldova structure introduces a two-tier membership model, where at least one general partner assumes unlimited liability while one or more limited partners are liable only up to their contributed capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Forms | Societate în Nume Colectiv (SNC); Societate în Comandită (SC) | Both have separate legal personality |

| Members | SNC: minimum 2 general partners, no maximum; SC: minimum 1 general partner + 1 limited partner | Natural persons or legal entities permitted |

| Liability | SNC: unlimited for all; SC: unlimited for general partners, capped at contribution for limited partners | Key structural distinction between the two forms |

| Local Presence | Registered legal address in Moldova required | No statutory requirement for a local resident manager |

| Minimum Capital | No statutory minimum capital prescribed | Contributions defined in the founding agreement |

| Privacy | Partner names disclosed in the State Register of Legal Entities | No nominee partner arrangements recognised |

Focus Points

- Taxation: General and limited partnerships are treated as transparent entities for tax purposes; profits are allocated to partners and taxed at the partner level, with corporate income tax, VAT registration thresholds, and withholding tax obligations applying depending on partner residency and activity type.

- Annual Compliance: Partners must file annual financial statements with the State Tax Service and maintain updated records at the State Registration Chamber (now integrated under the Public Services Agency).

- Economic Substance: No formalised substance test is prescribed specifically for partnerships, though genuine commercial activity is expected for tax residency purposes.

- Conversion: A partnership may be reorganised into an SRL or SA through a statutory reorganisation procedure under the Civil Code, subject to creditor notification requirements.

- Restrictions: Foreign nationals may act as general partners, but unlimited personal liability exposure makes this structure uncommon for international investors.

Sub-Types

General Partnership (Societate în Nume Colectiv – SNC)

All partners hold equal standing with regard to liability and, unless the founding agreement specifies otherwise, management authority. This form suits small professional practices or family-run businesses where all participants are directly involved in operations.

Limited Partnership (Societate în Comandită – SC)

Limited partners may not participate in management; doing so risks converting their status to that of a general partner with full liability. The structure is occasionally used where a passive investor wishes to contribute capital without assuming operational control.

Closing Remarks

Partnerships suit closely held ventures where the founders seek organisational flexibility and are willing to accept personal liability exposure in exchange for minimal formation requirements. The primary limitation is that unlimited liability for general partners creates significant personal financial risk, making this Moldovan partnership business structure unsuitable for higher-risk commercial activities.

Partnership structures in Moldova are best suited for small professional firms or family businesses where all principals are active participants and personal liability is an accepted trade-off for structural simplicity.

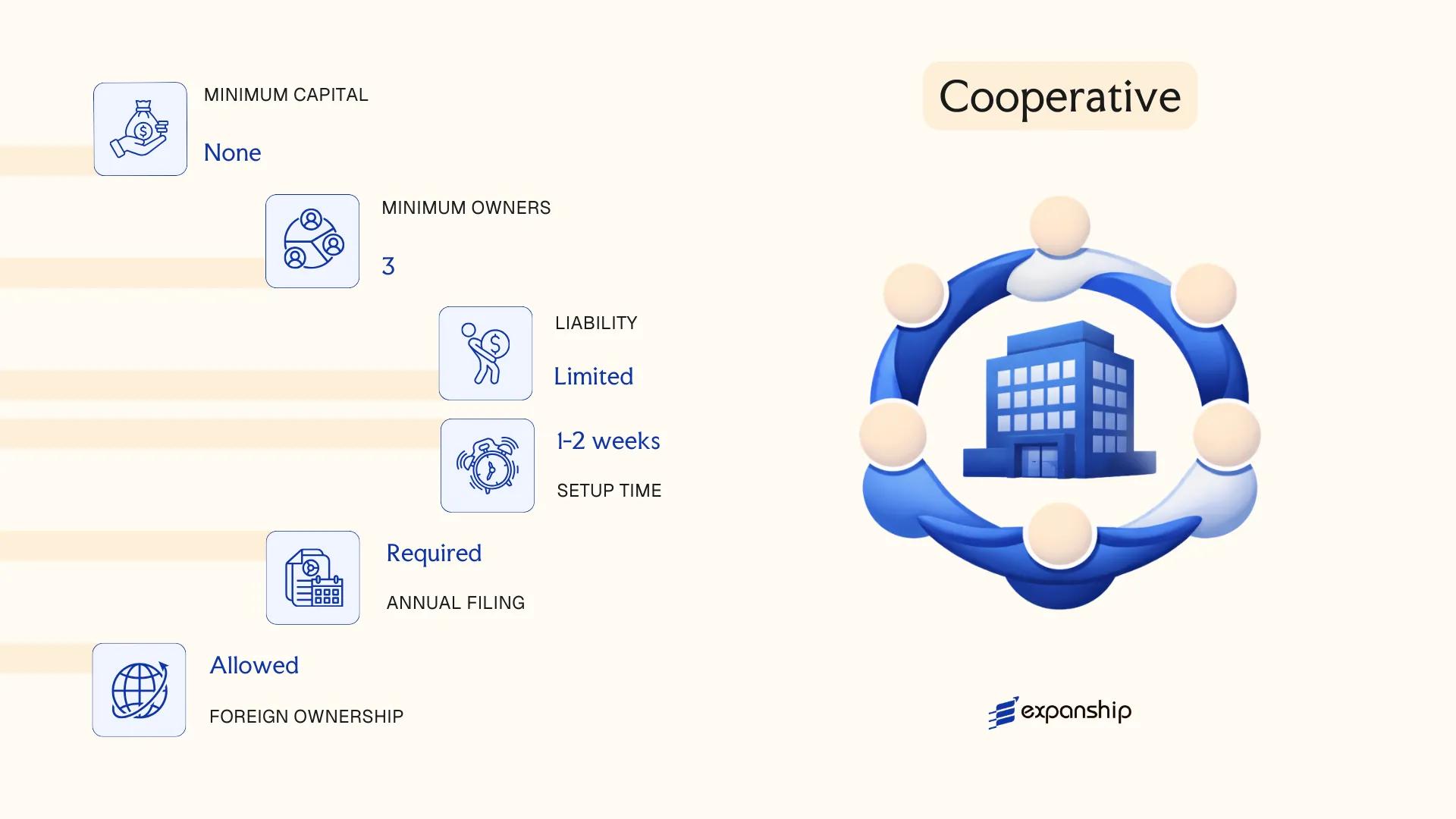

Cooperative (Cooperativa)

The cooperative business structure Moldova recognises is governed primarily by the Law on Cooperatives No. 1007-XIV of 2002, which establishes the cooperative as a distinct legal entity with its own rights and obligations separate from its members. Unlike a purely commercial vehicle, a cooperative operates on the principle of mutual benefit, where members participate both as contributors and beneficiaries of the entity's activities.

Cooperativa Moldova registration is open to natural persons and, in certain cases, legal entities who associate voluntarily to conduct joint economic or social activities. Liability of members is generally limited to their subscribed contributions, though the specific terms depend on the cooperative's charter and type.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative (Cooperativa) | Separate legal personality; hybrid commercial-social structure |

| Members | Referred to as members (membri); minimum 5 | No statutory upper limit; natural persons primarily, legal entities in some types |

| Local Presence | Registered office required in Moldova | No statutory registered agent requirement |

| Capital | No universal statutory minimum; defined in charter | Contributions may be monetary or in-kind |

| Governance | General Assembly (supreme body); Board of Directors; Supervisory Council | General Assembly holds ultimate authority |

| Privacy | Member register maintained internally; not fully public | Charter and registration data filed with the State Registration Chamber |

Focus Points

- Taxation: Subject to standard corporate income tax at 12%; VAT registration applies where turnover thresholds are met; dividend distributions to members may attract withholding tax under general rules.

- Annual Compliance: Annual financial statements must be submitted; General Assembly must convene at least once per year to approve accounts and board decisions.

- Treaty Access: Resident cooperatives may access Moldova's double tax treaty network, subject to meeting beneficial ownership requirements.

- Conversion: A cooperative may be reorganised into another legal form through merger, division, or transformation under the Civil Code and the Law on Cooperatives.

- Restrictions: Cooperatives cannot freely transfer membership interests; admission of new members requires General Assembly or board approval per the charter.

Sub-Types

Production Cooperative (Cooperativa de Producție)

Focused on joint manufacturing or service delivery, where members actively participate in the cooperative's operations rather than functioning as passive investors.

Consumer Cooperative (Cooperativa de Consum)

Organised to supply goods or services to its members, common in agricultural retail and community supply contexts; members use the cooperative's output rather than contributing labour.

Agricultural Cooperative (Cooperativa Agricolă)

A specialised structure for joint agricultural production, processing, or marketing; governed partly by sector-specific provisions and historically prevalent in rural Moldova.

A cooperative suits member-based enterprises in agriculture, craft production, or community services where shared governance matters more than investor returns. The mutual ownership structure offers resilience against hostile takeovers, but the restriction on free transfer of membership interests limits capital mobility significantly.

Best suited for groups of individuals in agriculture, crafts, or community trade who prioritise collective control and shared benefit over external investment or profit distribution flexibility.

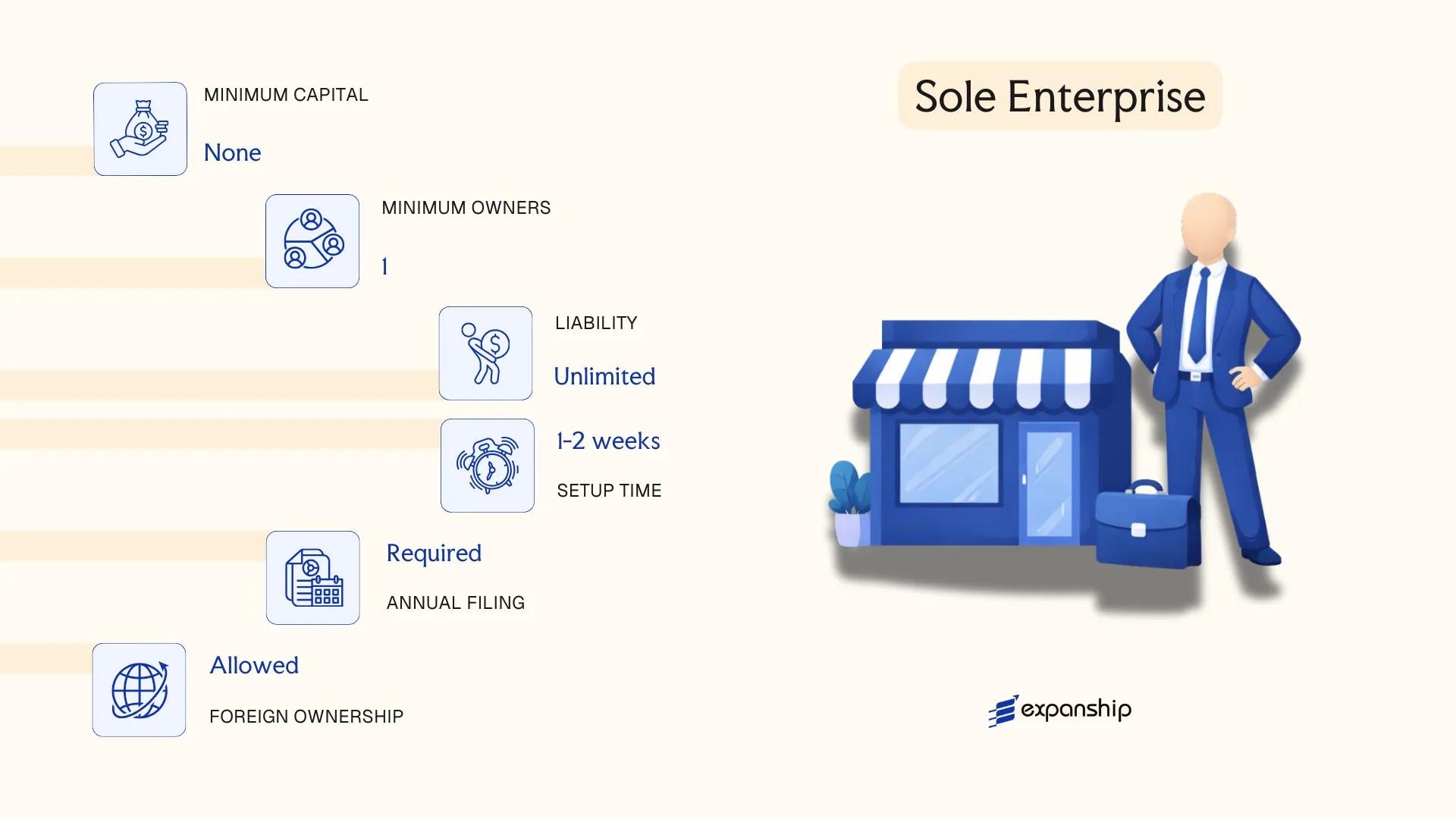

Sole Enterprise (Întreprindere Individuală)

Governed by the Law on Entrepreneurship and Enterprises No. 845-XII of 1992, the Întreprindere Individuală (II) is one of the oldest and simplest business forms available under Moldovan law. Moldova sole enterprise registration is processed through the State Registration Chamber (now integrated into the Agency of Public Services), making entry relatively straightforward for individuals operating independently.

Unlike an SRL, the sole enterprise does not confer separate legal personality on the business. The proprietor and the enterprise are legally treated as one, meaning personal assets are exposed to business liabilities without a protective corporate shield.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole enterprise | No separate legal personality; owner and business are legally unified |

| Members | Single individual (proprietor) | No shareholders or directors; one natural person owns and manages the entity |

| Local Presence | Registered address in Moldova required | No statutory requirement for a resident agent, but a verifiable local address must be maintained |

| Capital | No statutory minimum capital | Contributions are informal; no paid-up capital requirement under current law |

| Liability | Unlimited personal liability | All business debts are recoverable against the proprietor's personal assets |

| Privacy | Owner's name appears in the public register | Minimal privacy; the State Register is publicly accessible |

Focus Points

- Taxation: Subject to personal income tax rather than corporate income tax; VAT registration is required upon exceeding the MDL 1,200,000 annual turnover threshold; no separate withholding tax layer at the entity level.

- Annual Compliance: Must submit an annual financial report to the State Tax Service; accounting obligations are simplified relative to corporate entities.

- Conversion: Can be converted into an SRL or other corporate form through a restructuring procedure under Moldovan civil and commercial law, though the process requires re-registration.

- Treaty Access: As a non-corporate entity, access to Moldova's double tax treaty network is limited; treaty benefits generally apply to the individual proprietor rather than the enterprise itself.

- Restrictions: Foreign nationals face additional conditions when registering an individual enterprise, as residency requirements may apply under current regulatory practice.

Closing

The Întreprindere Individuală suits low-capital domestic trading, freelance services, and sole operators who prioritise minimal administrative overhead over liability protection. Its primary drawback is unlimited personal liability, which makes it unsuitable for activities carrying significant financial or legal risk.

This entity type is best suited for Moldovan residents running small-scale, single-operator businesses with limited third-party exposure and no requirement for investor participation.

How to Choose the Right Entity Type in Moldova

Choosing the right company type in Moldova affects your tax position, liability exposure, administrative burden, and long-term operational flexibility — so the decision warrants careful analysis before registration.

Why Your Entity Choice Matters

The structure you register determines your legal and financial obligations from day one. Selecting the wrong form can produce concrete, costly outcomes:

- Forming a Representative Office when your operations involve commercial transactions breaches the permitted scope under Moldovan law, exposing the entity to deregistration and fines.

- Choosing an entity that falls outside Moldova's double tax treaty eligibility means you cannot claim reduced withholding tax rates in counterpart jurisdictions.

- Registering a structure subject to mandatory statutory audit when you operate as a single-person consultancy introduces annual compliance costs that serve no commercial purpose.

- Selecting a form that lacks the legal capacity to hold immovable property or intellectual property rights creates title and transfer complications later.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors (banking, insurance, investment funds), and passive asset holding each require different legal forms under Moldovan company law.

- Ownership Structure: A single founder suits the SRL, while multi-investor arrangements with transferable share classes point toward the SA.

- Tax Objectives: Your eligibility for Moldova's treaty network or specific tax regimes depends on the entity type and its registered status.

- Management Flexibility: SRLs permit leaner governance; SAs require a formal board structure under Law No. 1134-XIII on Joint Stock Companies.

- Exit and Conversion: Not all Moldovan entity forms permit straightforward redomiciliation or conversion, so your long-term strategy should factor in restructuring options at the outset.

- Substance Capacity: If you cannot maintain a physical presence, employees, or local decision-making, certain structures will trigger compliance failures under applicable reporting obligations.

Compliance Services for Companies in Moldova

Maintain good standing and meet your ongoing statutory obligations under Moldovan law.

Conclusion

Choosing the right structure is the first binding legal decision your business makes in Moldova, and this Moldova company incorporation conclusion guide reflects the range of options the Civil Code and Law No. 135/2007 on the Limited Liability Company provide. The SRL is the most registered entity in the country, favoured for its minimal capital requirements and single-member eligibility. Joint Stock Companies suit businesses seeking equity investment or public listings. Branch offices and representative offices serve foreign firms that need a local operational or liaison presence without creating a separate legal entity. General and limited partnerships fit professional arrangements where personal liability is acceptable. Cooperatives serve member-owned collective activity, while the Sole Enterprise suits individual traders. Moldova's ongoing alignment with EU association commitments continues to shape its regulatory direction, including expanded tax treaty coverage and corporate governance reforms. Expanship's team works directly within this framework to assist your setup.

How Expanship Can Assist You

Expanship Moldova company formation services cover the full range of entities discussed in this blog — from registering a Societatea cu Răspundere Limitată (SRL) to establishing a branch office for a foreign parent company. All filings pass through the State Registration Chamber (now operating under the Public Services Agency), and understanding exactly what each structure requires at that level makes a measurable difference in how quickly your business becomes operational.

Across Moldova business registration assistance, Expanship supports clients at every stage:

- Document preparation and notarization

- Registered agent and registered office provision

- Filing and liaison with the Public Services Agency

- Post-incorporation compliance management, including annual reporting obligations

- Corporate secretarial support

- Banking introduction assistance

To discuss your specific situation, reach out through Expanship Moldova.

Frequently Asked Questions (FAQ)

The SRL (Societatea cu Răspundere Limitată) is the most frequently incorporated entity type. Its relatively low minimum share capital, single-shareholder eligibility, and simplified governance structure make it the default choice for small and medium-sized businesses.

An SA is subject to more stringent disclosure and governance requirements under Law No. 1134-XIII on Joint Stock Companies, including mandatory audits and a supervisory board at certain thresholds. An SRL operates under lighter compliance obligations and cannot issue publicly traded shares, whereas an SA can access capital markets. Both entity types are taxed under the same standard corporate income tax regime.

The SRL offers a comparatively higher degree of operational privacy, as it is not required to publish shareholder resolutions publicly in the same manner as an SA. Beneficial ownership information is, however, registered with the State Tax Service in line with anti-money laundering obligations. Nominee arrangements are legally permissible but subject to disclosure requirements.

An SRL can be formed by one person, and a Sole Enterprise (Întreprindere Individuală) is inherently single-owner. General Partnerships and Limited Partnerships, by their legal nature, require a minimum of two partners. An SA can technically be founded by one shareholder.

Foreign individuals and legal entities may establish an SRL, SA, Branch Office, or Representative Office without restriction on nationality. A Branch Office does not constitute a separate legal entity and remains an extension of the parent company, while an SA and SRL carry full legal personality under Moldovan law.

Reorganisation between entity types is governed by the Civil Code of Moldova and specific company laws, permitting transformation, merger, and division procedures. An SRL may be reorganised into an SA, subject to meeting the SA's minimum share capital and governance requirements. The State Registration Chamber administers the registration of such changes.

Not all structures do. A Representative Office and Branch Office lack independent legal personality and operate as extensions of their parent company. By contrast, the SRL, SA, General Partnership, Limited Partnership, and Cooperative each hold separate legal personality under Moldovan law.

The Sole Enterprise carries the lightest compliance burden, with no separate audit requirement and simplified accounting standards applicable to micro-entities. An SRL also benefits from reduced reporting obligations compared to an SA, particularly below the statutory thresholds that trigger mandatory external audit under Moldovan accounting legislation.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.