Key Takeaways

- Latvia's most widely used business structure is the Sabiedrība ar Ierobežotu Atbildību (SIA), which supports single-shareholder ownership and carries an accessible minimum capital requirement.

- All business entities in Latvia are registered through the Uzņēmumu reģistrs (Enterprise Register) and governed primarily under the Commercial Law.

- Unlike conventional corporate tax systems, Latvia applies corporate income tax only upon profit distribution rather than on retained earnings, reflecting a deferred taxation model.

- Foreign companies can establish a presence in Latvia without full incorporation by registering a branch office or representative office, each carrying different scopes of permitted commercial activity.

Introduction to Entity Types in Latvia

Latvia is a Baltic state in Northern Europe, bordered by Estonia to the north, Lithuania to the south, Belarus to the east, and Russia to the northeast. An independent EU member state, it operates under a civil law system, with company registration administered by the Latvian Enterprise Register (Uzņēmumu reģistrs). The tax regime is territorial in orientation, with a deferred corporate income tax model that only taxes distributed profits rather than retained earnings.

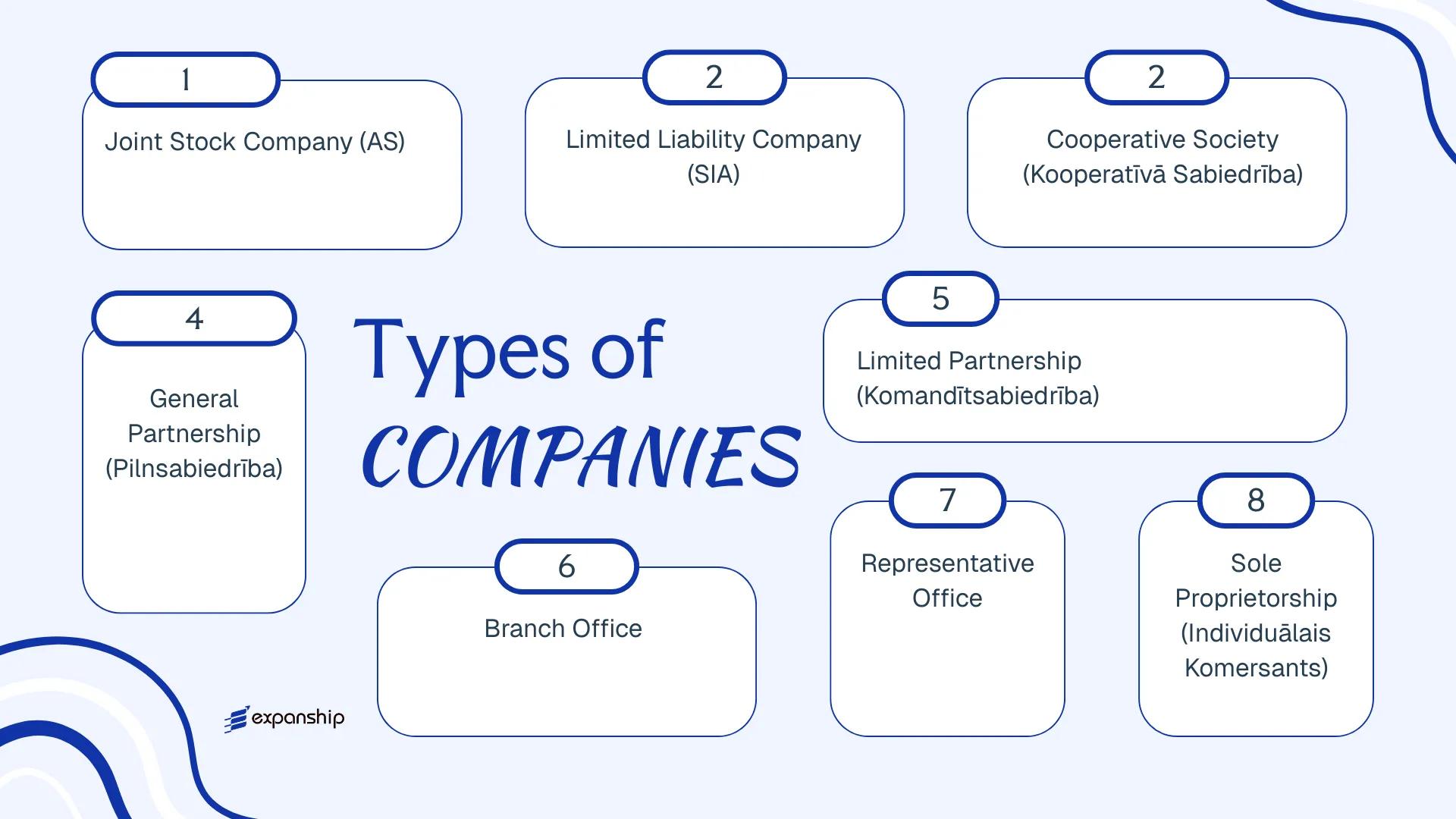

Several types of business entities in Latvia are available to both residents and foreign investors. These include:

- Sabiedrība ar Ierobežotu Atbildību (SIA)

- Akciju Sabiedrība (AS)

- Pilnsabiedrība (General Partnership)

- Komandītsabiedrība (Limited Partnership)

- Kooperatīvā Sabiedrība (Cooperative Society)

- Individuālais Komersants (Sole Proprietorship)

- Branch Office

- Representative Office

Each structure carries distinct requirements around share capital, liability, governance, and permitted activity. This article examines each Latvian legal entity structure in turn, covering formation requirements, ownership rules, tax treatment, and practical use cases to help you determine which business form fits your objectives.

An Overview of Business Structures in Latvia

Latvia's company law framework provides six principal entity types available for registration and operation within the country. The primary legislation governing these structures is the Commercial Law (Komerclikums), which came into force in 2002 and has been amended several times since. Each entity type is designed to serve a distinct commercial purpose, differing in liability exposure, governance requirements, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Akciju Sabiedrība (AS) | Joint Stock Company | Limited to share capital | Taxed | Yes | 1 shareholder | Enterprise Register | Commercial Law |

| Sabiedrība ar Ierobežotu Atbildību (SIA) | Limited Liability Company | Limited to share capital | Taxed | Yes | 1 shareholder | Enterprise Register | Commercial Law |

| Kooperatīvā Sabiedrība | Cooperative Society | Limited | Taxed | Yes | 5 members | Enterprise Register | Cooperative Societies Law |

| Pilnsabiedrība | General Partnership | Unlimited, joint | Taxed | Yes | 2 partners | Enterprise Register | Commercial Law |

| Komandītsabiedrība | Limited Partnership | Mixed | Taxed | Yes | 2 partners | Enterprise Register | Commercial Law |

| Branch Office | Foreign entity branch | Parent liable | Taxed | Yes | Parent company | Enterprise Register | Commercial Law |

| Representative Office | Non-trading presence | Parent liable | Exempt from CIT | No | Parent company | Enterprise Register | Commercial Law |

| Individuālais Komersants | Sole Proprietorship | Unlimited, personal | Taxed | Yes | 1 individual | Enterprise Register | Commercial Law |

Each of these structures is examined in full in the sections below.

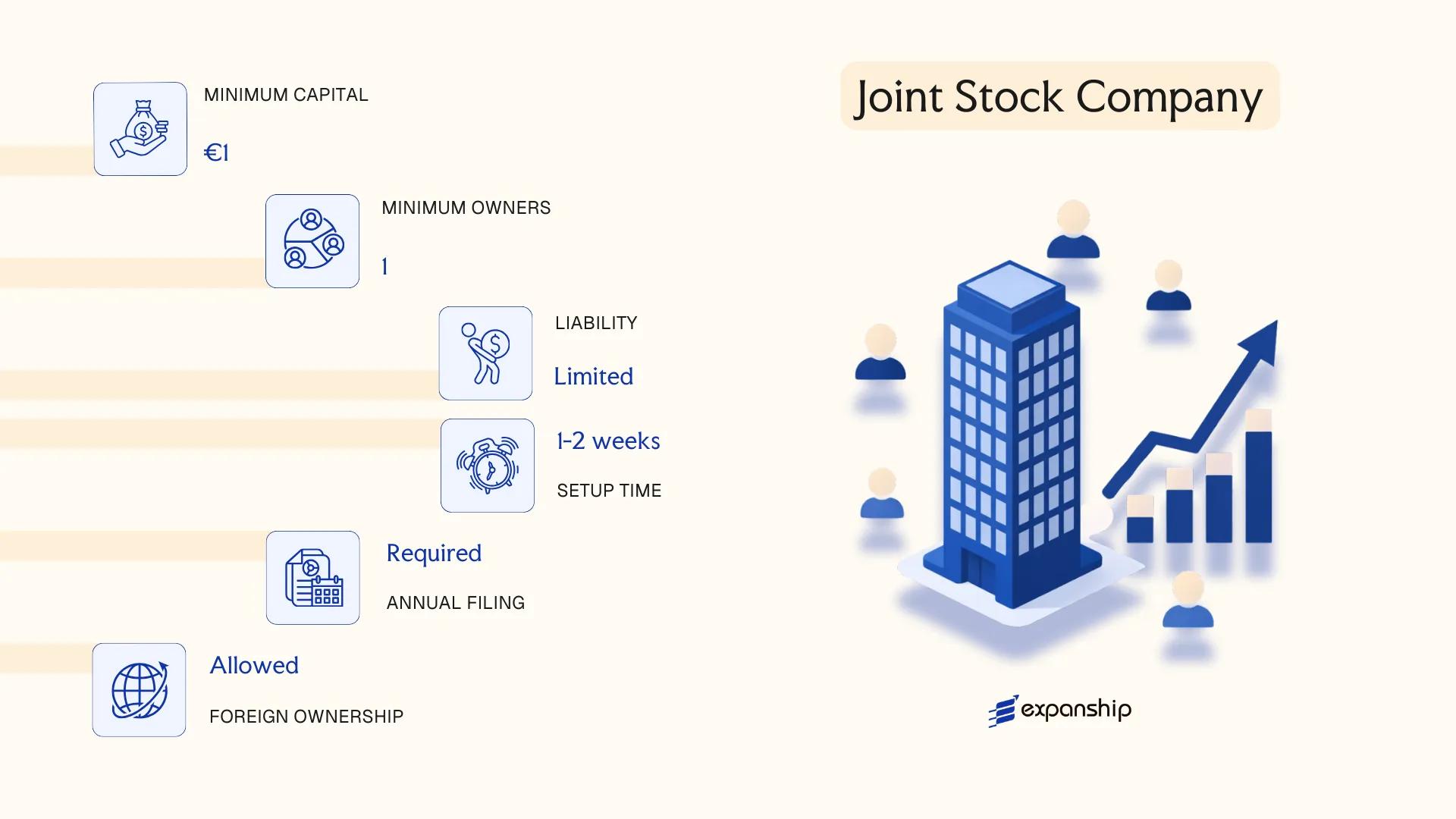

Akciju Sabiedrība (AS) — Joint Stock Company

The AS joint stock company Latvia recognises as its primary vehicle for large-scale capital raising is governed by the Commercial Law (Komerclikums), adopted in 2000. As a distinct legal entity, the AS carries its own rights and obligations separate from its shareholders, who bear liability only to the extent of their share contributions.

Shares in an AS may be publicly listed or privately held, which makes this structure function as both a closed corporate vehicle and a potential candidate for listing on Nasdaq Riga. Akciju Sabiedrība registration Latvia requires submission to the Enterprise Register (Uzņēmumu reģistrs), after which the entity acquires full legal personality.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (Akciju Sabiedrība) | Separate legal personality; limited liability |

| Members | Shareholders (minimum 1, no maximum) | Single-member AS is permitted |

| Governing Bodies | Board of Directors + Supervisory Board | Supervisory board mandatory if share capital exceeds EUR 285,714 |

| Local Presence | Registered legal address in Latvia required | No mandatory local director requirement |

| Share Capital | Minimum EUR 35,000; must be fully paid before registration | Latvia AS company requirements permit contributions in cash or in kind |

| Share Types | Registered shares only; bearer shares not permitted | Shares may be ordinary or preference shares |

| Privacy | Shareholders disclosed in the Enterprise Register | Beneficial ownership reported to the Beneficial Ownership Register |

Focus Points

- Taxation: Subject to Latvia's corporate income tax at a 20% rate applied to distributed profits only; standard VAT rate is 21%; withholding tax applies to dividends paid to non-residents, subject to treaty relief.

- Annual Compliance: Annual accounts must be filed with the Enterprise Register; audited financial statements are mandatory above statutory size thresholds.

- Treaty Access: Qualifies as a resident entity for purposes of Latvia's double tax treaty network, currently covering over 60 jurisdictions.

- Conversion: An AS may be reorganised into an SIA or another commercial form under Part D of the Commercial Law without dissolution.

- Public Offering Restrictions: A public share offering triggers obligations under the Financial Instruments Market Law and oversight by the Financial and Capital Market Commission (FKTK).

Closing

The AS suits holding structures, joint ventures requiring institutional investors, and businesses preparing for a public listing; the ability to issue multiple share classes provides structural flexibility. The principal drawback is administrative weight — mandatory supervisory bodies, audit requirements, and higher minimum capital make it disproportionate for small or single-owner businesses.

Best suited for large enterprises, institutional joint ventures, or businesses with active plans to access public capital markets through Nasdaq Riga.

Company Incorporation in Latvia

Incorporate an Akciju Sabiedrība or other Latvian entity with end-to-end registration support through the Enterprise Register.

Sabiedrība ar Ierobežotu Atbildību (SIA) — Limited Liability Company

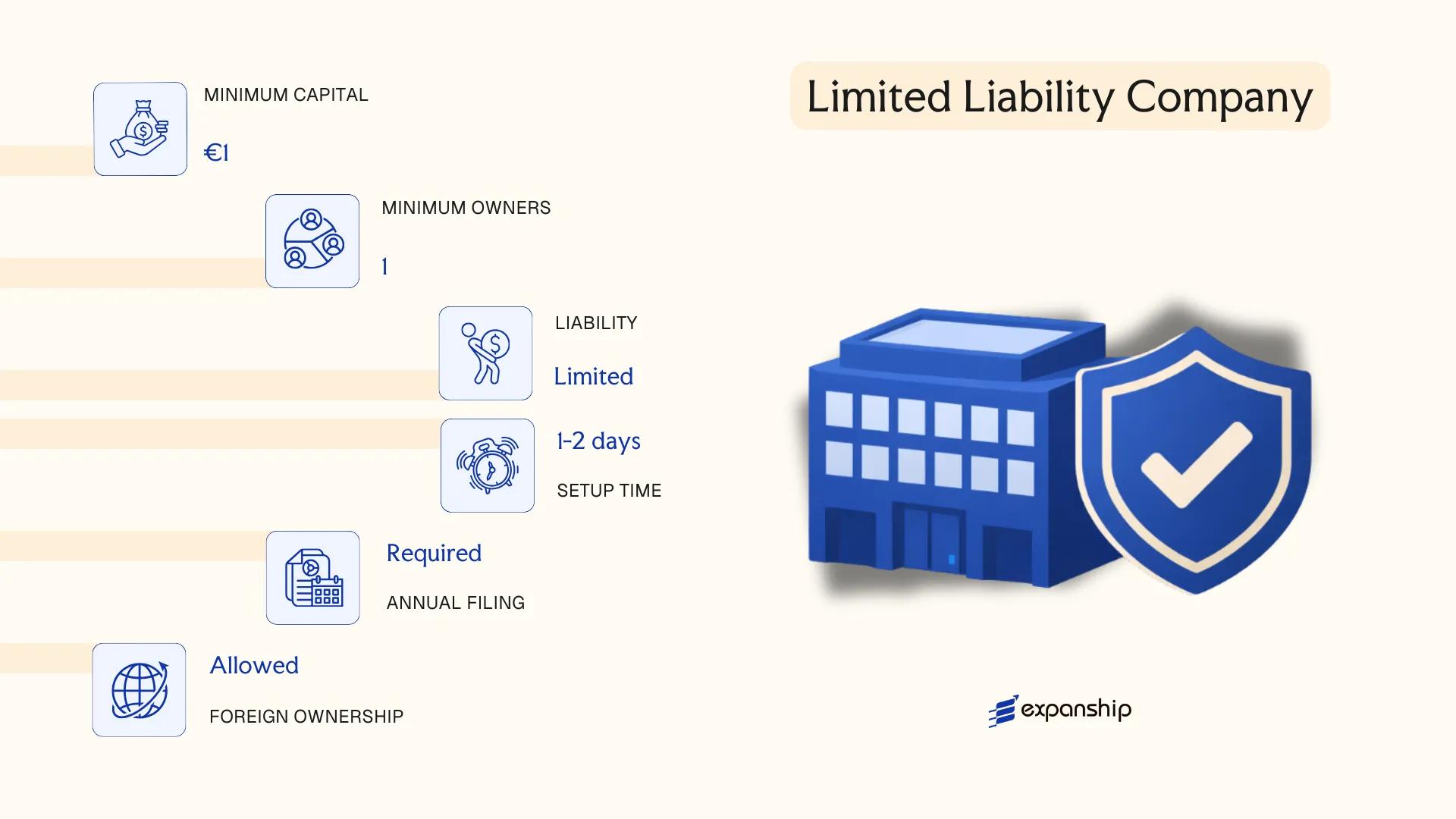

The SIA limited liability company Latvia is the most widely used corporate structure in the country, governed by the Law on Commercial Companies (Komerclikums), which came into force in 2002. As a separate legal entity, an SIA holds its own rights and obligations distinct from its shareholders, who bear liability only to the extent of their capital contributions.

Structurally, the SIA sits between a sole proprietorship and a joint stock company. Ownership is divided into shares, but those shares are not publicly tradable, making it a closed, privately held form suited to small and medium-sized businesses as well as holding arrangements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited liability company | Shares are non-transferable on public markets |

| Members | Shareholders: 1–50 | A single legal or natural person may be the sole shareholder |

| Governing Bodies | Board of Directors (valde); Supervisory Board optional | Supervisory Board mandatory only if share capital exceeds EUR 71,149 |

| Local Presence | Registered legal address in Latvia required | A registered agent is not a statutory requirement, but a local address is |

| Share Capital | Minimum EUR 2,800; reduced regime allows EUR 1 with profit reinvestment conditions | Full EUR 2,800 must be paid up before registration under standard rules |

| Privacy | Shareholders and directors disclosed in the Business Register | Register is publicly searchable |

Focus Points

- Taxation: Corporate income tax of 20% applies to distributed profits only; undistributed profits are not taxed. Standard VAT rate is 21%, with registration mandatory once turnover exceeds EUR 50,000. Withholding tax applies to dividends paid to non-residents at 0% within the EU (subject to conditions) or up to 20% otherwise.

- Annual Compliance: Annual financial statements must be filed with the State Revenue Service (Valsts ieņēmumu dienests); audit obligations depend on size thresholds.

- Economic Substance: No formal substance regime, but tax residency and treaty access may require genuine management and control to be exercised locally.

- Treaty Access: Latvia maintains an extensive double tax treaty network; SIAs qualify as residents for treaty purposes.

- Conversion: An SIA may be converted into an AS (joint stock company) or other commercial forms under Komerclikums provisions without dissolution.

Closing

The SIA suits trading companies, holding structures, and IP-owning entities where shareholders want liability protection without the administrative burden of a public company. Its primary constraint is the 50-shareholder ceiling, which limits its use for larger investor pools.

The SIA is best suited for small to mid-sized businesses, family-owned firms, and foreign investors establishing a privately held operating or holding entity in Latvia.

Kooperatīvā Sabiedrība — Cooperative Society

Kooperatīvā Sabiedrība Latvia registration is governed by the Law on Cooperative Societies (Kooperatīvo sabiedrību likums), which came into force in 2007. The entity holds separate legal personality and operates on a membership basis, where economic benefit flows to members in proportion to their participation rather than capital contribution.

Liability is generally limited to each member's subscribed share. The structure occupies a middle ground between a classic capital company and a members' association, making it functionally distinct from both the SIA and AS frameworks.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative Society (separate legal personality) | Governed by Kooperatīvo sabiedrību likums (2007) |

| Members | Referred to as members; minimum 5 founding members required | No statutory maximum; legal persons may be members |

| Governance | Management board and supervisory council | Supervisory council mandatory when membership exceeds 50 |

| Local Presence | Registered office in Latvia required | No registered agent requirement under current law |

| Capital | No fixed statutory minimum share capital | Member shares defined in the articles of association |

| Privacy | Member register maintained internally; not fully public | Board members disclosed in the Uzņēmumu reģistrs |

Focus Points

- Taxation: Subject to standard 20% corporate income tax on distributed profits; VAT registration required once turnover exceeds the threshold (currently EUR 50,000); dividend distributions to members may attract withholding tax depending on residency.

- Economic Substance: No specific substance regime applies, but the entity must conduct genuine cooperative activity among its members.

- Annual Compliance: Annual financial statements must be filed with the Uzņēmumu reģistrs; member meetings required at least once per year.

- Treaty Access: As a resident legal entity, qualifies for Latvia's double tax treaty network, subject to beneficial ownership tests.

- Restrictions: Cannot freely transfer membership shares to third parties without member approval; profit distribution logic differs from standard capital companies.

Closing

The cooperative structure suits agricultural groups, consumer associations, and sector-specific professional collectives where shared economic activity among members is the primary purpose. Its key advantage lies in the participatory profit model; however, the minimum membership threshold and restrictions on share transferability limit its suitability for investor-driven or single-owner structures.

This entity type is best suited for groups of five or more individuals or organisations pursuing a common economic activity on a collective, non-speculative basis.

Partnerships in Latvia [Pilnsabiedrība (General Partnership), Komandītsabiedrība (Limited Partnership)]

Both forms of Latvia general and limited partnership are governed by the Commercial Law (Komerclikums), adopted in 2000. Neither structure carries separate legal personality in the way a capital company does, meaning partners bear direct liability for the entity's obligations — though the extent of that liability differs significantly between the two forms.

Registering either structure requires an application to the Enterprise Register of the Republic of Latvia (Latvijas Republikas Uzņēmumu reģistrs). Pilnsabiedrība Latvia registration and Komandītsabiedrība Latvia formation both follow the same administrative channel, with the partnership agreement serving as the foundational constitutional document.

Key Characteristics

| Requirement | Pilnsabiedrība (GP) | Komandītsabiedrība (LP) | Notes |

|---|---|---|---|

| Legal Form | General Partnership | Limited Partnership | Neither holds separate legal personality |

| Members | Partners (complementary) | General partners + limited partners | GP: min. 2 general partners; LP: min. 1 general + 1 limited partner |

| Liability | Unlimited for all partners | Unlimited for general partners; limited to contribution for limited partners | Limited partners cannot participate in management |

| Capital | No statutory minimum | No statutory minimum | Contributions defined in the partnership agreement |

| Local Presence | Registered address in Latvia required | Registered address in Latvia required | No resident agent requirement under current law |

| Privacy | Partnership agreement not fully public | Partnership agreement not fully public | Partner identities are disclosed in the register |

Focus Points

- Taxation: Partnerships are fiscally transparent; profits flow through to partners and are taxed at the individual or corporate level depending on partner type. Latvia's standard corporate income tax rate of 20% applies upon profit distribution for corporate partners, while VAT registration is required once the EUR 40,000 turnover threshold is met.

- Annual Compliance: Both forms must submit annual accounts to the Enterprise Register; failure to comply can result in forced liquidation proceedings.

- Treaty Access: As pass-through structures, partnerships may face limitations accessing Latvia's double tax treaty network, since treaty benefits generally attach to the partner rather than the entity.

- Conversion: A general partnership may be reorganised into a limited partnership or a capital company under the Commercial Law reorganisation provisions.

- Restrictions: Limited partners who participate in management activities risk losing their limited liability protection under Latvian law.

Sub-Types

Pilnsabiedrība (General Partnership)

All partners carry joint and several unlimited liability for the partnership's debts. This structure is typically used by professional firms or small business ventures where partners are closely involved in day-to-day operations.

Komandītsabiedrība (Limited Partnership)

At least one general partner holds unlimited liability while one or more limited partners contribute capital with liability capped at their contribution. This Latvian partnership business structure is commonly used where passive investors wish to participate financially without assuming full operational risk.

When to Use This Structure

Partnerships are suited to professional services arrangements, joint ventures between closely aligned parties, or domestic trading operations where the pass-through tax treatment is a deliberate planning consideration. The absence of a minimum capital requirement lowers the barrier to formation; however, unlimited liability exposure for general partners remains a material constraint for most commercial applications.

Latvian partnerships are most appropriate for small professional practices or domestic joint ventures where partners accept personal liability and prefer fiscal transparency over the protections offered by a capital company.

Foreign Business Presence in Latvia [Branch Office, Representative Office]

Establishing a foreign company branch office Latvia is governed by the Commercial Law (Komerclikums), adopted in 2000, along with the Law on the Register of Enterprises. Neither a branch nor a representative office constitutes a separate legal entity — both remain extensions of the foreign parent company, which bears full liability for their activities. This distinction has direct consequences for how obligations, debts, and regulatory exposure are attributed.

Registration in both cases is handled by the Enterprise Register of the Republic of Latvia (Uzņēmumu Reģistrs). Latvia branch vs representative office distinctions come down primarily to permitted activity: a branch may conduct full commercial operations, while a representative office is restricted to promotional, market research, and liaison functions.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Commercial Activity | Permitted in full | Not permitted; limited to liaison and promotional activities |

| Parent Liability | Unlimited | Unlimited |

| Local Representative | Mandatory — must be registered | Mandatory — must be registered |

| Registered Address | Required in Latvia | Required in Latvia |

| Registered Capital | None required | None required |

| Registration Body | Enterprise Register (Uzņēmumu Reģistrs) | Enterprise Register (Uzņēmumu Reģistrs) |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at 20% (applied on distribution basis); VAT registration is required if taxable turnover exceeds the statutory threshold; withholding tax may apply to profit remittances depending on the parent's jurisdiction and applicable tax treaty.

- Economic Substance: A registered local representative with authority to act on behalf of the foreign firm is required; purely nominal presence carries regulatory risk.

- Annual Compliance: Annual financial statements of the branch must be filed with the Enterprise Register; representative offices have reduced reporting obligations.

- Treaty Access: Access to Latvia's tax treaty network depends on the parent company's tax residency, not the branch's presence.

- Restrictions: A representative office cannot sign commercial contracts, generate revenue, or invoice clients in its own capacity.

Closing

A branch suits foreign firms testing the Latvian market or managing active operations without incorporating a separate subsidiary, though the absence of liability separation means the parent carries full exposure for local activities.

Opening a branch in Latvia as a foreign company is best suited for established businesses seeking operational presence without the administrative burden of a standalone subsidiary, provided the parent is comfortable with unlimited liability exposure.

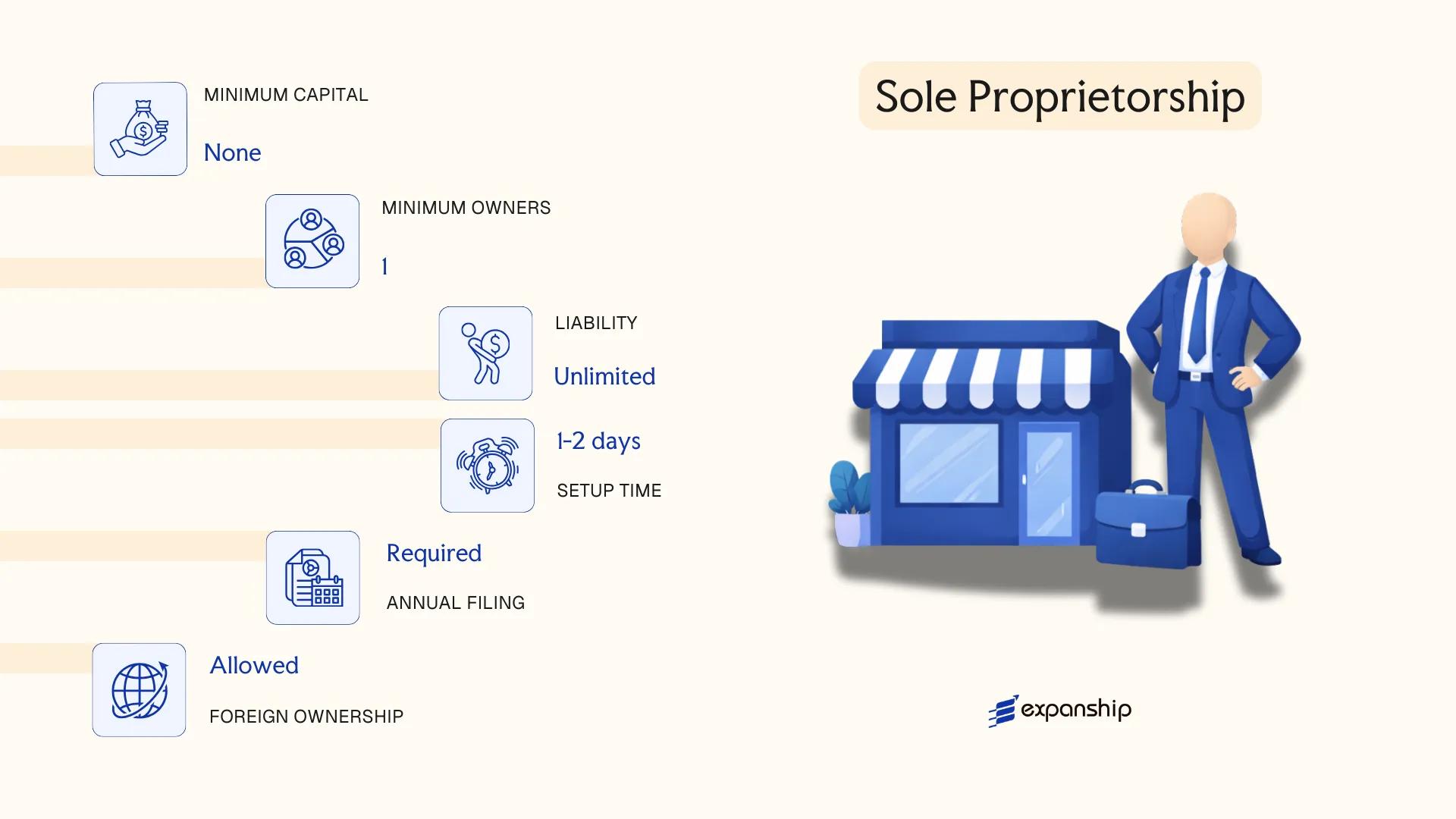

Individuālais Komersants — Sole Proprietorship

The Individuālais Komersants (IK), or Latvian sole proprietorship, is governed by the Commercial Law (Komerclikums) adopted in 2000. Unlike a limited liability company, the IK does not confer separate legal personality distinct from its owner — the individual and the business are treated as one legal subject, meaning personal assets are fully exposed to business liabilities.

Registration is handled through the Enterprise Register of the Republic of Latvia (Latvijas Republikas Uzņēmumu reģistrs). Any natural person who is a resident or meets the qualifying criteria for self-employed business registration in Latvia may apply. The IK is subject to the same commercial registration requirements as other merchant forms, including a registered address and entry in the Commercial Register.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole proprietorship (merchant individual) | No separate legal personality; owner bears unlimited liability |

| Owner | Single individual (proprietor) | Cannot have multiple owners; no shareholder or director structure |

| Minimum Capital | None prescribed | No statutory minimum share capital requirement |

| Local Presence | Registered address in Latvia required | Must be maintained throughout the entity's existence |

| Liability | Unlimited personal liability | All personal assets are at risk for business debts |

| Privacy | Owner's name appears in the public Commercial Register | No privacy from public disclosure |

Focus Points

- Taxation: Business income is taxed as personal income under the Personal Income Tax Law; VAT registration is required if annual turnover exceeds the statutory threshold (currently EUR 50,000); no separate corporate income tax applies to the IK itself.

- Annual Compliance: Annual financial statements must be filed with the Enterprise Register; accounting obligations apply under the Law on Annual Reports and Consolidated Annual Reports.

- Conversion: An IK can be reorganised or converted into a capital company (such as an SIA) through a transformation procedure under the Commercial Law, though this involves additional registration steps.

- Treaty Access: As a non-corporate entity, access to Latvia's double tax treaty network is limited and generally does not apply in the same manner as for corporate residents.

- Restrictions: Certain regulated activities, including financial services and insurance, cannot be conducted through an IK.

Closing

The IK suits individual traders, freelancers, and small-scale service providers who operate with minimal capital and low liability exposure. Its primary advantage is administrative simplicity and low formation cost; the significant drawback is unlimited personal liability, which makes it unsuitable for any business carrying material financial or legal risk.

Best suited for resident individuals conducting low-risk, low-turnover commercial activity who do not require liability protection or corporate structure.

How to Choose the Right Entity Type in Latvia

Selecting the correct structure before you register determines your tax position, liability exposure, and ongoing compliance obligations for the life of the business. Knowing how to choose a business entity in Latvia requires examining your operational model against the legal consequences of each structure, not just the registration costs.

Why Your Entity Choice Matters

The structure you register has binding legal and financial consequences.

- Selecting an SIA or AS when your activity requires a licensed entity under the Financial Instruments Market Law means your registration may be refused or revoked by the Financial and Capital Market Commission.

- Choosing a structure that lacks treaty eligibility prevents you from claiming reduced withholding tax rates under Latvia's bilateral tax treaty network.

- Forming a general partnership when liability needs to be limited exposes each partner personally to the firm's full debt obligations with no statutory cap.

- Registering an entity that triggers mandatory audit requirements — applicable to SIA and AS companies that exceed two of three thresholds under the Annual Accounts Law — adds recurring audit costs that may be disproportionate for a single-operator consultancy.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each correspond to distinct structures under the Commercial Law of Latvia.

- Ownership and Management: Single-member ownership with flexible management favors an SIA, while multi-investor capital structures with share classes point toward an AS.

- Tax Objectives: Your need for treaty access, dividend exemption eligibility, or micro-enterprise tax regime qualification should align with your chosen entity's legal status.

- Liability Exposure: Whether you require statutory limited liability or can accept unlimited personal exposure shapes the choice between capital companies and partnerships.

- Substance Capacity: If you cannot maintain a physical presence, decision-making, or staff locally, you need a structure whose compliance obligations do not trigger substance-related penalties.

- Exit Strategy: Not all Latvian entities support redomiciliation or conversion; confirm whether your structure permits a future change of form under the Law on Reorganization of Commercial Companies.

Compliance Services for Companies in Latvia

Ongoing compliance support for Latvian entities, including annual reporting, accounting obligations, and regulatory filings.

Conclusion

Latvia's company formation landscape — condensed into a summary guide — centers on a clear hierarchy of entity types, each serving a distinct profile of investor or operator. The SIA (Sabiedrība ar Ierobežotu Atbildību) is by far the most commonly registered structure, favored for its accessible minimum capital and single-shareholder eligibility. The AS suits larger enterprises requiring public capital markets access. Partnerships serve those prioritizing operational flexibility over liability protection. Cooperatives address member-owned, sector-specific commercial activity. Branch offices and representative offices allow foreign firms to test the market before full incorporation, while the Individuālais Komersants suits self-employed operators with straightforward regulatory exposure.

Registered under the Commercial Law and supervised by the Enterprise Register of Latvia, each structure carries obligations that persist well beyond initial registration. Latvia's expanding bilateral investment treaty network and its EU membership continue to shape its regulatory posture. Professionals advising on incorporating in Latvia track ongoing amendments to the Commercial Law and AML compliance directives as benchmarks of its evolving framework. Expanship's advisory team follows these developments directly.

How Expanship Can Assist You

Expanship's Latvia company incorporation services cover the full registration process, from selecting the right entity structure to filing with the Uzņēmumu Reģistrs (Enterprise Register of Latvia). Every entity type discussed in this guide, from an SIA to an AS or a branch office, carries distinct registration requirements and ongoing compliance obligations that our team handles directly on your behalf.

From document preparation to post-registration administration, our corporate services Latvia registration support covers:

- Document preparation, notarisation, and apostille where required

- Registered address and local agent provision

- Filing and liaison with the Enterprise Register of Latvia

- Post-incorporation compliance management, including annual reporting

- Corporate bank account introduction assistance

- Shareholder and directorship maintenance support

Your business deserves structured, jurisdiction-specific guidance rather than generic advice. Reach out through Expanship Latvia to discuss your setup requirements.

Frequently Asked Questions (FAQ)

The Sabiedrība ar Ierobežotu Atbildību (SIA) is by far the most frequently registered business form, governed by the Commercial Law (Komerclikums). Its low minimum share capital, single-shareholder eligibility, and manageable compliance requirements make it the default choice for small and medium-sized businesses.

The SIA, AS, and Kooperatīvā Sabiedrība all hold separate legal personality under the Commercial Law. General partnerships (Pilnsabiedrība) and limited partnerships (Komandītsabiedrība) do not possess full legal personality in the same sense, meaning partners retain direct liability exposure depending on their role.

An Individuālais Komersants carries the lightest administrative burden, with no annual accounts required in the same format as capital companies. However, the sole proprietor bears unlimited personal liability, which significantly affects risk exposure compared to limited liability structures.

Not all structures permit sole formation. An SIA or AS can be established by one shareholder, while a Pilnsabiedrība requires at least two partners by definition. A Kooperatīvā Sabiedrība requires a minimum of three founding members under the Law on Cooperative Societies.

Non-residents may register any entity type, including an SIA or AS, without residency requirements for shareholders. Directors of capital companies must have a registered address accessible to the Enterprise Register (Uzņēmumu reģistrs), and at least one board member may be required to hold a valid address within the European Economic Area for correspondence purposes.

The Commercial Law permits the reorganisation of legal entities, including transformation of an SIA into an AS and vice versa. The process involves preparing a transformation plan, notifying creditors, and registering the change with the Enterprise Register. Conversions between capital companies and partnerships follow stricter procedural requirements given the liability implications.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.