Key Takeaways

- Lesotho's principal legislation governing company formation is the Companies Act 2011, with registration administered by the Registrar of Companies under the Office of the Registrar of Companies and Intellectual Property.

- The private company limited by shares is the most widely used structure in Lesotho, preferred by both resident and foreign investors for its defined liability framework and straightforward governance requirements.

- Foreign businesses may operate in Lesotho without incorporating a new local entity by registering as a branch office or external company under the Companies Act 2011.

- General partnerships in Lesotho lack separate legal personality, while limited partnerships offer partial liability separation, making the choice between them a consequential structural decision.

Introduction to Entity Types in Lesotho

Lesotho is a landlocked sovereign nation located entirely within South Africa, governed as a constitutional monarchy under King Letsie III. As an independent state, it regulates commercial activity through domestic legislation — principally the Companies Act 2011 — with company registration administered by the Registrar of Companies, operating under the Office of the Registrar of Companies and Intellectual Property.

The tax regime is territorial in orientation, with corporate income tax applied to locally sourced profits rather than worldwide earnings.

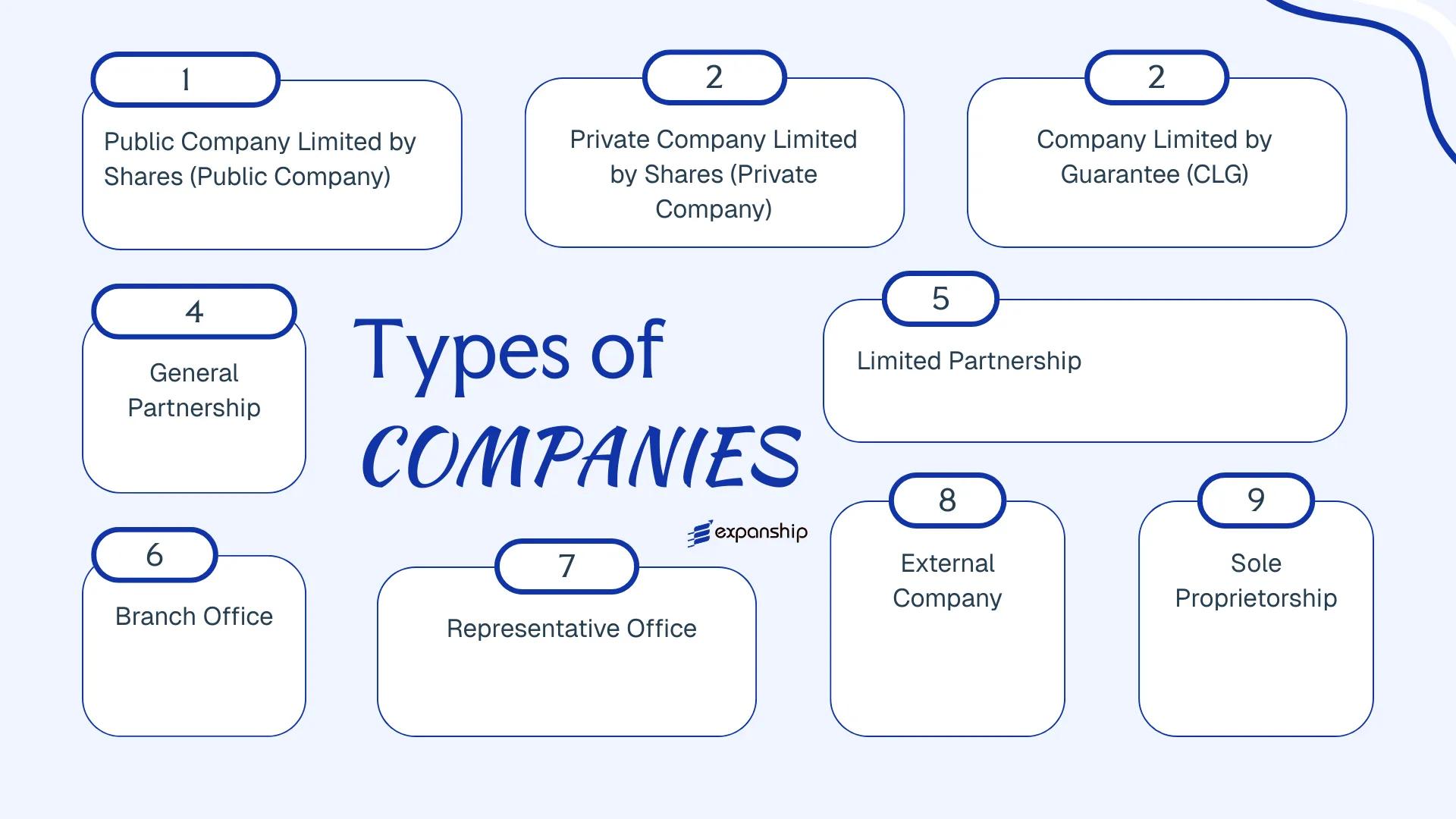

Several types of business entities in Lesotho are available to both resident and foreign investors. These include the private company limited by shares, the public company limited by shares, the company limited by guarantee, general and limited partnerships, the sole proprietorship, and foreign business structures such as branch offices, representative offices, and external companies registered under the Companies Act.

Each of these Lesotho company types carries distinct legal characteristics, liability implications, and registration requirements. This article examines the corporate structures explained above in detail — covering formation procedures, governance obligations, and practical considerations for each structure.

An Overview of Business Structures in Lesotho

Lesotho recognises several distinct business structures under the Companies Act 2011, which serves as the primary legislation governing corporate formation and registration in the country. The business structures available in Lesotho range from private and public companies to partnerships, sole proprietorships, and registered external companies. Each structure carries its own legal characteristics, liability implications, and suitability for different commercial activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Private Company (Ltd) | Separate legal entity | Limited to shares | Taxable | Permitted | 1 shareholder | OBFC | Companies Act 2011 |

| Public Company (Ltd) | Separate legal entity | Limited to shares | Taxable | Permitted | 2 shareholders | OBFC | Companies Act 2011 |

| Company Limited by Guarantee | Separate legal entity | Limited to guarantee | Taxable / Exempt | Permitted | 1 member | OBFC | Companies Act 2011 |

| General Partnership | Not separate | Unlimited, joint | Taxable | Permitted | 2 partners | OBFC | General Law |

| Limited Partnership | Partial separation | Mixed liability | Taxable | Permitted | 1 GP + 1 LP | OBFC | General Law |

| External Company (Branch) | Extension of parent | Parent liable | Taxable | Permitted | 1 parent entity | OBFC | Companies Act 2011 |

| Representative Office | Not separate | Parent liable | Generally exempt | Not permitted | 1 parent entity | OBFC | Companies Act 2011 |

| Sole Proprietorship | Not separate | Unlimited | Taxable | Permitted | 1 individual | OBFC | General Law |

Each of these structures is examined in full in the sections below.

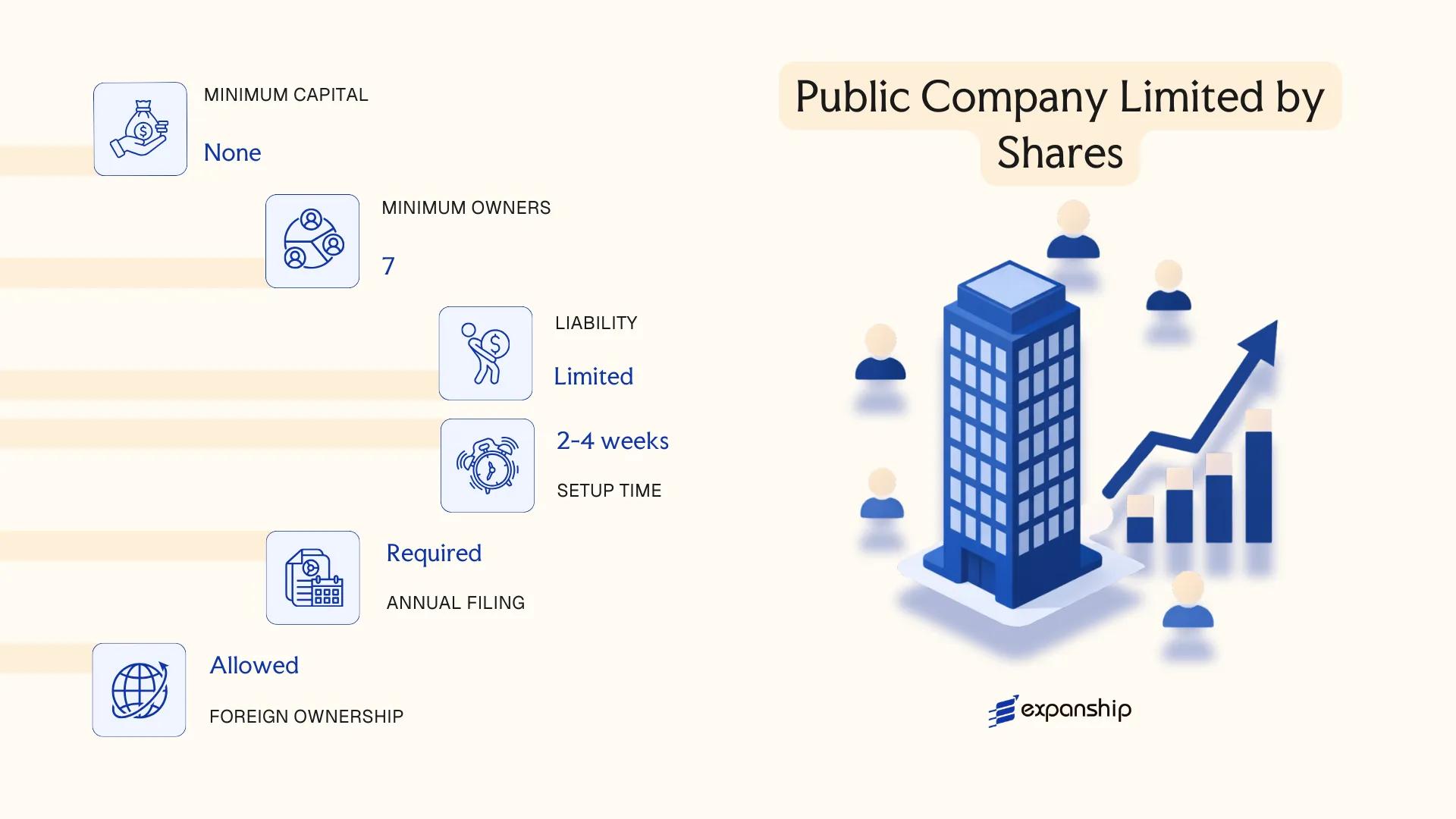

Public Company Limited by Shares in Lesotho

A public company limited by shares in Lesotho is governed by the Companies Act 2011, the primary legislation regulating corporate entities in the kingdom. The Act confers separate legal personality on the entity, meaning the company can own assets, incur liabilities, and enter contracts in its own name, distinct from its shareholders.

Shareholders' exposure to loss is confined to the unpaid amount on their shares. This structure allows the entity to raise capital from the general public, including through a listing on a recognised stock exchange, making it the form of choice for larger enterprises and public offerings.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Company Limited by Shares | Incorporated under the Companies Act 2011 |

| Members | Shareholders; minimum 1 director, no upper limit on shareholders | Shares may be offered to the general public |

| Local Presence | Registered office in Lesotho required | Must maintain a physical registered address within the jurisdiction |

| Capital | Lesotho Loti (LSL); no statutory minimum share capital | Capital structure defined in the constitution of the company |

| Privacy | Shareholder and director information filed with the Registrar of Companies | Register is generally accessible to the public |

| Secretary | Company secretary required | Must meet qualification requirements under the Act |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate; VAT registration required above the applicable threshold; withholding taxes apply to dividends, interest, and royalties paid to non-residents; stamp duty may apply to certain instruments.

- Annual Compliance: Annual returns must be filed with the Registrar of Companies; audited financial statements are required and must be laid before shareholders at the annual general meeting.

- Listing Requirements: A public offering or stock exchange listing triggers additional regulatory oversight, potentially involving the Central Bank of Lesotho and applicable securities regulations.

- Conversion: A public company may be re-registered as a private company under the Companies Act 2011, subject to meeting the relevant conditions and shareholder approval.

- Restrictions: Offering shares to the public without compliance with prospectus and disclosure requirements is prohibited under the Act.

Closing

A public company limited by shares suits large-scale commercial operations, entities seeking capital market access, or businesses structured for institutional investment. The ability to raise public capital is a clear structural advantage; however, ongoing disclosure obligations and mandatory audits create a compliance burden that smaller enterprises may find disproportionate.

Best suited for large enterprises, joint ventures with institutional investors, or businesses intending to list on a public exchange.

Company Incorporation in Lesotho

Register a public or private company in Lesotho with end-to-end support from our corporate services team.

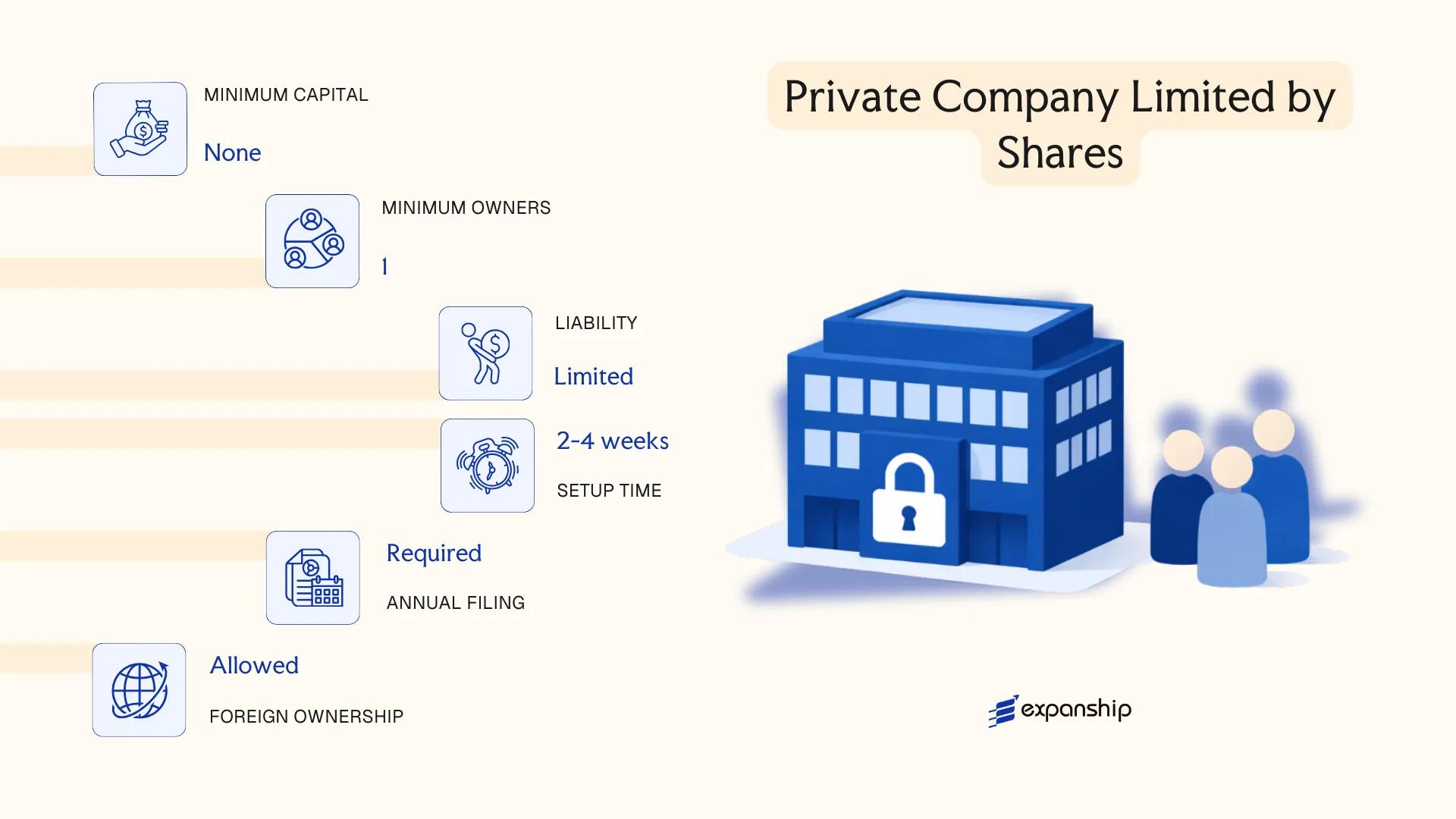

Private Company Limited by Shares in Lesotho

The private company limited by shares is the most widely used commercial vehicle for foreign and domestic investors operating under Lesotho's Companies Act 2011. Governed by that Act and administered through the Registrar of Companies within the Ministry of Trade and Industry, this entity carries separate legal personality distinct from its shareholders.

Liability is confined to the amount unpaid on a member's shares, making it a suitable structure for risk containment. The firm may not offer its shares to the general public, and any transfer of shares is subject to restrictions set out in its constitutional documents.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company (Pty) Ltd | Separate legal personality; cannot offer shares publicly |

| Members | Shareholders: min. 1, max. 50 | Single-shareholder companies are permitted |

| Directors | Min. 1 director | No residency requirement specified under the Act |

| Local Presence | Registered office in Lesotho required | Must maintain a physical address for official correspondence |

| Share Capital | No statutory minimum; denominated in Lesotho Loti (LSL) | Authorised and issued capital stated in constitutional documents |

| Privacy | Beneficial ownership disclosure required to the Registrar | Shareholder register is maintained at the registered office |

Focus Points

- Taxation: Corporate income tax applies at 25% on business income; a reduced 10% rate applies to manufacturing entities; VAT registration is required once turnover exceeds the prescribed threshold; withholding tax applies to dividends, interest, and royalties paid to non-residents.

- Annual Compliance: Annual returns must be filed with the Registrar of Companies; audited financial statements are generally required unless an exemption applies.

- Economic Substance: No formal economic substance regime equivalent to certain offshore jurisdictions, but tax residency and permanent establishment rules under domestic law apply.

- Treaty Access: Lesotho has a limited tax treaty network; confirm applicable treaties before structuring cross-border flows.

- Conversion: The Companies Act 2011 provides mechanisms to convert a private company to a public company, subject to regulatory approval and constitutional amendments.

Closing

A Lesotho private company limited by shares suits trading operations, subsidiary structures, and joint ventures where liability containment and operational flexibility are priorities. The single-member option reduces structural complexity, though the restriction on public share offerings limits capital-raising options as a business scales.

This entity type is best suited for foreign investors establishing a locally incorporated subsidiary or a market-entry trading operation in Lesotho.

Company Limited by Guarantee in Lesotho

A company limited by guarantee Lesotho law recognises is governed by the Companies Act 2011, the same statute that regulates share-based companies. Unlike a company with share capital, this structure has no shareholders. Instead, members agree to contribute a fixed amount toward the entity's liabilities if it is wound up. The entity carries full separate legal personality and limited liability, making it a legally distinct body from its members.

This structure is used predominantly for non-profit purposes, including associations, charities, professional bodies, and similar organisations. Lesotho NGO company structure requirements channel these entities through the Companies Registry, with registration formalities broadly aligned to those of private companies.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by guarantee | Separate legal personality; no share capital |

| Members | Referred to as members; minimum 1, no statutory maximum | Members provide a guarantee amount, not capital investment |

| Directors | Minimum 1 director required | Must be a natural person |

| Local Presence | Registered office in Lesotho required | Must be a physical address, not a PO Box |

| Capital | No share capital; members' guarantee amount specified in memorandum | Guarantee sum is typically nominal |

| Privacy | Memorandum and articles filed publicly at the Companies Registry | Beneficial ownership subject to applicable disclosure rules |

Focus Points

- Taxation: Non-profit guarantee companies may qualify for income tax exemption under the Income Tax Act 1993 if approved; VAT registration obligations apply if turnover thresholds are met; distributions of profit are structurally prohibited, removing dividend withholding tax considerations.

- Annual Compliance: Annual returns must be filed with the Companies Registry; audited financial statements may be required depending on the entity's size and funding sources.

- Profit Distribution: Surplus funds must be applied toward the entity's stated objects; members cannot receive financial gain from operations.

- Conversion: Conversion to a share-based company is not a standard or straightforward procedure under the Companies Act 2011.

- Regulatory Oversight: Entities engaged in development or humanitarian activities may also fall under oversight of the Lesotho Council of NGOs or relevant line ministries.

Closing

This structure suits professional associations, registered charities, trade bodies, and similar non-commercial organisations that require legal personality without distributing profits. The main advantage is the combination of limited liability with a non-profit mandate; the primary limitation is that the entity cannot raise equity capital or offer financial returns to its members.

Best suited for non-profit organisations, membership associations, and civil society bodies that require a formal legal structure with capped member liability.

Partnerships in Lesotho (General Partnership, Limited Partnership)

Partnership registration in Lesotho is governed primarily by the Companies Act 2011, which also provides a framework for business associations beyond incorporated entities, alongside general common law principles inherited from Roman-Dutch law. Partnerships do not carry separate legal personality in Lesotho, meaning partners remain personally liable for the obligations of the firm.

Liability exposure differs between the two recognised forms. In a general partnership, all partners bear unlimited joint and several liability. A limited partnership permits designated limited partners to cap their liability to the amount of capital contributed, provided they take no active role in management.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business association | No separate legal personality under Lesotho law |

| Members | Partners (minimum 2, no statutory maximum) | General partners: unlimited liability; limited partners: liability capped at contribution |

| Local Presence | Registered business address required | No statutory registered agent requirement, but a physical address for correspondence is expected |

| Capital | Lesotho Loti (LSL); no statutory minimum | Capital contributions defined by partnership agreement |

| Privacy | Partnership agreement not filed publicly | Partner identities may require disclosure upon regulatory request |

Focus Points

- Taxation: Partnerships are taxed on a pass-through basis; individual partners declare their share of income under personal income tax rates; VAT registration is required once annual turnover exceeds the statutory threshold.

- Annual Compliance: No annual return filing equivalent to companies, but tax filings with the Lesotho Revenue Authority remain mandatory.

- Treaty Access: Partnerships generally do not access double tax treaties as stand-alone entities; treaty benefits flow through to qualifying resident partners individually.

- Restrictions: Limited partners must not participate in management or they risk losing limited liability protection.

- Conversion: A partnership may convert to an incorporated entity under the Companies Act 2011, though the process requires fresh registration.

Sub-Types

General Partnership

All partners hold equal management rights and bear unlimited personal liability for debts and obligations of the firm unless the partnership agreement stipulates otherwise. This structure suits professional service firms and small trading ventures where partners share operational control.

Limited Partnership

At least one general partner manages the business and carries unlimited liability, while one or more limited partners contribute capital without management authority. This arrangement is used where passive investors wish to participate in a venture without assuming full personal liability.

Closing Paragraph and Recommendations

Partnerships suit early-stage ventures, joint ventures between known parties, and professional practices where shared management is preferred, though the absence of limited liability in the general form presents meaningful personal financial risk for each partner. The limited partnership structure addresses this partially but restricts the operational role of protected partners.

Limited partnerships are best suited to investment-oriented ventures where one party contributes capital passively and another manages day-to-day operations under full liability.

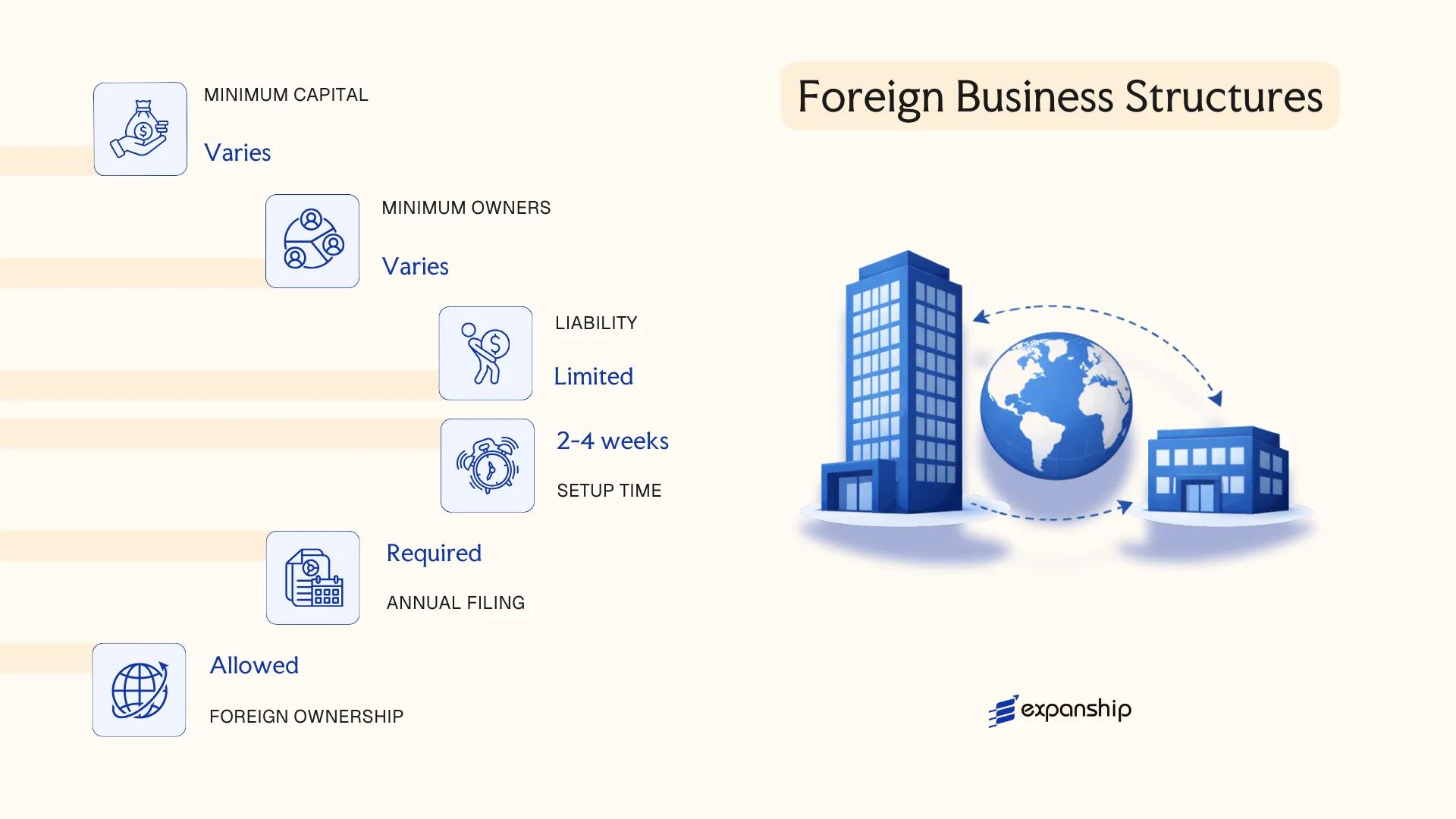

Foreign Business Structures in Lesotho (Branch Office, Representative Office, External Company)

Foreign company registration in Lesotho is governed by the Companies Act 2011, which classifies any overseas entity conducting business within the country as an "external company." Under this legislation, such entities do not form a new legal person in Lesotho; the foreign parent retains its original legal personality and remains liable for the local operation's obligations.

Registration is administered by the Registrar of Companies under the Ministry of Law and Justice. An external company must submit its constitutional documents, details of local representatives, and a registered office address to the Registrar within 28 days of commencing business activities in the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | External Company (branch of foreign entity) | No separate legal personality; parent company bears full liability |

| Local Representatives | Minimum one locally resident authorised agent | Must be formally appointed and registered with the Registrar |

| Registered Office | Physical address required in Lesotho | P.O. Box alone is insufficient |

| Capital | No prescribed minimum capital | Parent company's capital structure applies |

| Privacy | Parent company's constitutional documents are filed publicly | Beneficial ownership subject to general disclosure rules |

| Name | Must match or clearly derive from the parent company's name | Registrar may require a distinguishing addition |

Focus Points

- Taxation: External companies are taxed on Lesotho-sourced income at the standard corporate rate of 25%; VAT registration is required if annual turnover exceeds the statutory threshold; withholding tax applies to dividends, interest, and royalties remitted abroad.

- Annual Compliance: Audited financial statements of the foreign parent, along with local accounts, must be filed annually with the Registrar.

- Treaty Access: Lesotho has a limited double taxation treaty network; treaty benefits depend on the parent entity's residence jurisdiction.

- Restrictions: External companies may not engage in activities beyond those authorised under the parent's constitutional documents without amendment and re-filing.

- Conversion: An external company can subsequently incorporate as a domestic entity, but this requires a separate registration process rather than a simple conversion.

Sub-Types

Branch Office

A branch operates as a full trading extension of the parent, generating revenue and entering contracts directly. It is the standard structure for foreign firms seeking active commercial operations under the external company framework.

Representative Office

A representative office is limited to promotional and liaison activities; it cannot conclude contracts or generate income locally. This structure suits foreign businesses that wish to explore the market or coordinate regional activities without establishing a revenue-generating presence.

Closing Paragraph and Recommendations

External companies are most commonly used by multinational firms in sectors such as infrastructure, mining services, and financial services that require a defined operational footprint without incurring the cost of incorporating a separate subsidiary. The primary advantage is speed of establishment relative to full incorporation; the significant drawback is that the parent bears unlimited liability for all local obligations.

Foreign entities already operating in the region that need a formalised, revenue-generating presence in Lesotho without a separately capitalised local subsidiary.

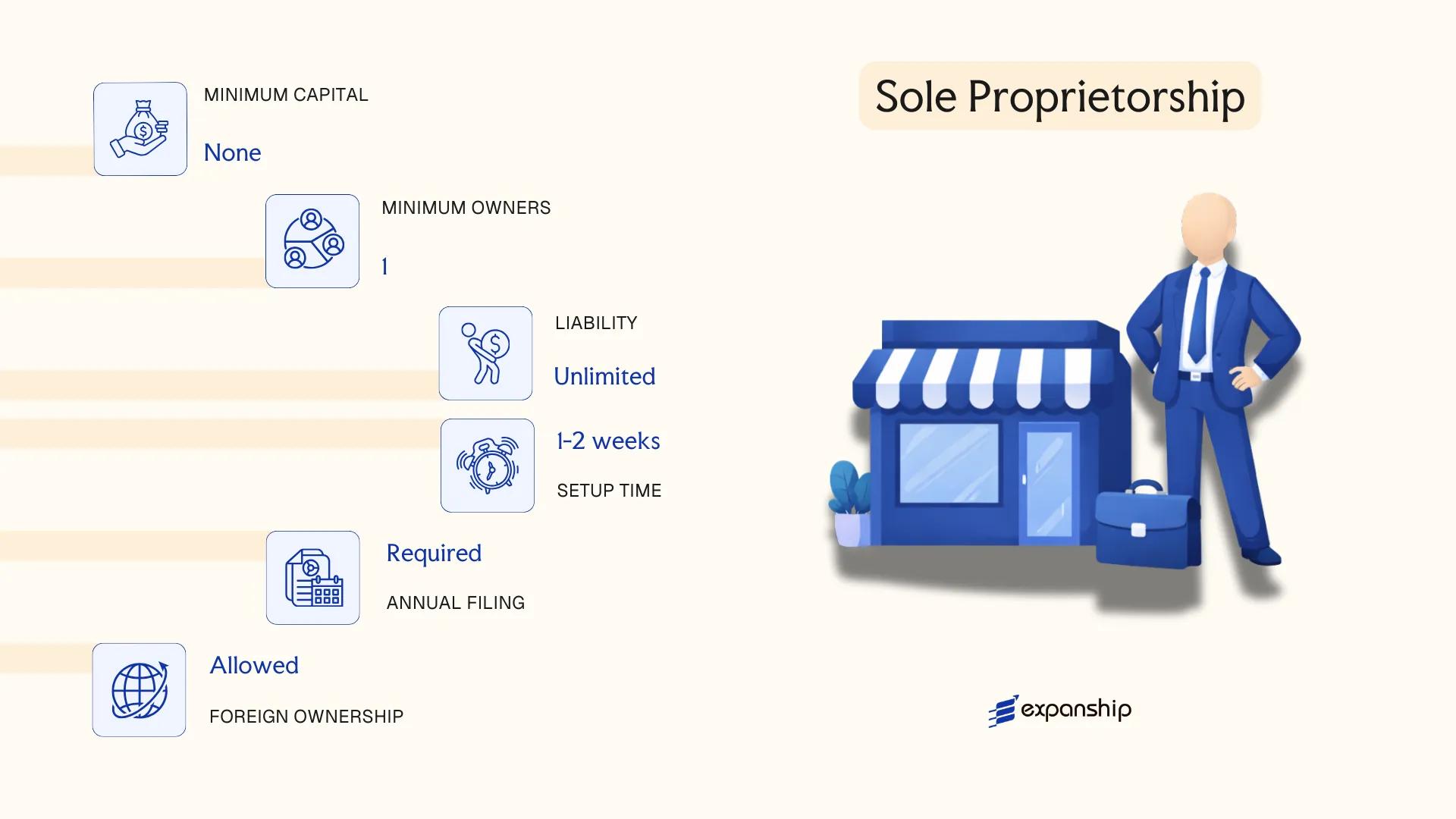

Sole Proprietorship in Lesotho

Sole proprietorship registration in Lesotho is governed primarily by the Business Names Act and the Companies Act 2011, with registration administered through the Ministry of Trade and Industry. Unlike incorporated entities, a sole proprietorship carries no separate legal personality — the owner and the business are the same legal person, which means personal assets are directly exposed to business liabilities.

Registration is required when trading under a name other than your own. The process involves registering the business name with the relevant authority and obtaining a trading licence from the local authority in the area where the business operates.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated individual business | No separate legal personality from the owner |

| Members | Sole proprietor (1 individual only) | No co-owners permitted under this structure |

| Local Presence | Trading licence from local authority; registered business address required | Licence issued by the relevant municipal or district council |

| Capital | LSL; no statutory minimum | Owner contributes personal funds; no share capital structure |

| Privacy | Business name and owner details appear on the public register | Limited privacy protection |

| Liability | Unlimited personal liability | Owner's personal assets are exposed to all business debts |

Focus Points

- Taxation: Subject to personal income tax on business profits under the Income Tax Act 1993; VAT registration required if annual turnover exceeds the statutory threshold; no corporate tax applies.

- Annual Compliance: Trading licence renewal is required periodically with the issuing local authority; no annual return filing with a company registry applies.

- Treaty Access: No access to double tax treaty benefits available to corporate entities; income is taxed at the individual level only.

- Conversion: A sole proprietorship can be converted into a private company by incorporating a new entity and transferring business assets; no automatic conversion mechanism exists.

- Restrictions: Foreign nationals face restrictions on operating as sole traders under Lesotho's business reservation policies, which reserve certain sectors for citizens.

Recommendations

This structure suits resident individuals running small-scale, low-risk trading or service businesses where administrative simplicity outweighs the need for liability protection. The primary advantage is minimal setup cost and straightforward administration; the significant limitation is unlimited personal liability, which exposes the proprietor's private assets to any business obligations.

Lesotho citizens operating small local businesses who require a low-cost, simple structure and do not anticipate significant liability exposure or external investment.

How to Choose the Right Entity Type in Lesotho

Selecting how to choose a business entity in Lesotho requires more than weighing registration costs. The structure you form determines your tax exposure, liability profile, compliance obligations, and operational permissions under the Companies Act 2011.

Why Your Entity Choice Matters

Forming the wrong structure produces concrete, correctable-but-costly outcomes:

- Registering an external company without filing the required documents with the Registrar of Companies means operating outside the Act's registration requirements, exposing the business to penalties and potential deregistration.

- Choosing a company limited by guarantee when your purpose is commercial trading creates a structural mismatch that restricts profit distribution.

- Selecting a sole proprietorship when the business will employ staff and hold assets in multiple sectors removes limited liability protection, placing personal assets directly at risk.

- Forming a private company when a partnership structure would suffice adds annual statutory obligations — including director filings — that a partnership does not require.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each require distinct structures under Lesotho's regulatory framework.

- Ownership Structure: Single-owner operations may suit a sole proprietorship or private company, while multi-party arrangements point toward a partnership or company with a defined share structure.

- Liability Exposure: If your business carries contractual or operational risk, structures offering limited liability protection become relevant.

- Local vs. Cross-Border Operations: Foreign entities intending to conduct business locally must register as external companies with the Registrar.

- Exit and Continuity: Private companies offer perpetual succession and cleaner transfer of ownership; partnerships dissolve upon a partner's exit unless the agreement states otherwise.

- Compliance Capacity: Some structures carry audit, reporting, or filing obligations that a small or single-person operation may find disproportionate to its scale.

Compliance Services for Companies in Lesotho

Ongoing compliance support for Lesotho-registered entities, including annual returns, statutory filings, and regulatory maintenance.

Conclusion

Starting a company in Lesotho guide requires understanding which structure aligns with your operational scope, liability tolerance, and ownership requirements under the Companies Act 2011. Registered and overseen by the Registrar of Companies within the Ministry of Trade and Industry, each entity carries distinct legal consequences.

The private company limited by shares remains the most commonly registered structure, favored by resident and foreign investors alike for its defined liability and straightforward governance. Public companies suit larger capital-raising ambitions; companies limited by guarantee serve non-profit or membership-based purposes. General partnerships offer simplicity without separate legal personality, while limited partnerships provide a degree of liability separation. A branch or external company allows foreign firms to operate directly without establishing a new local legal entity. Sole proprietorships carry the fewest formalities but the greatest personal exposure.

Lesotho's ongoing alignment with SACU trade frameworks and its bilateral investment treaty activity suggest a gradual strengthening of its regulatory infrastructure, which will shape future compliance obligations for businesses operating there.

How Expanship Can Assist You

Expanship provides company incorporation services in Lesotho across the full range of structures covered in this guide — from private companies limited by shares to external company registrations. Our team works directly with the Registrar of Companies under the Ministry of Trade and Industry to keep your filing process on track and in line with the Companies Act 2011.

From document preparation to post-registration obligations, we handle the operational side so your business can focus on its actual work.

- Memorandum and Articles of Association drafting and notarization

- Government filing and liaison with the Registrar of Companies

- Registered agent and registered office provision in Maseru

- Ongoing compliance management, including annual returns

- Banking introduction assistance for corporate account opening

- Document legalization for foreign-sourced materials

Reach out to Expanship Lesotho to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The private company limited by shares is the most frequently registered structure under the Companies Act 2011. Its comparatively low capital requirements, limited liability protection, and suitability for both resident and foreign-owned businesses make it the default choice for commercial activity.

A private company limited by shares distributes profits to shareholders and carries standard corporate tax obligations. A company limited by guarantee holds no share capital and is generally formed for non-profit purposes such as associations or charities, with any surplus reinvested into the organisation's stated objectives rather than distributed.

Private and public companies, along with companies limited by guarantee, hold distinct legal personality under the Companies Act 2011. General partnerships and sole proprietorships do not — the owners remain personally liable for all obligations of the business.

A private company requires at least one director and one shareholder, and a single individual may fulfill both roles. General and limited partnerships, by definition, require a minimum of two partners, so sole formation is not possible for those structures.

Foreign individuals and entities may register a private company, public company, or external company (branch) in Lesotho. External companies must register with the Registrar of Companies under the Companies Act 2011 and file annual returns accordingly.

The Companies Act 2011 provides mechanisms for re-registration, allowing a private company to convert to a public company and vice versa. Conversion from a corporate structure to a partnership is not a defined statutory process and would require dissolution and fresh registration.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.