Key Takeaways

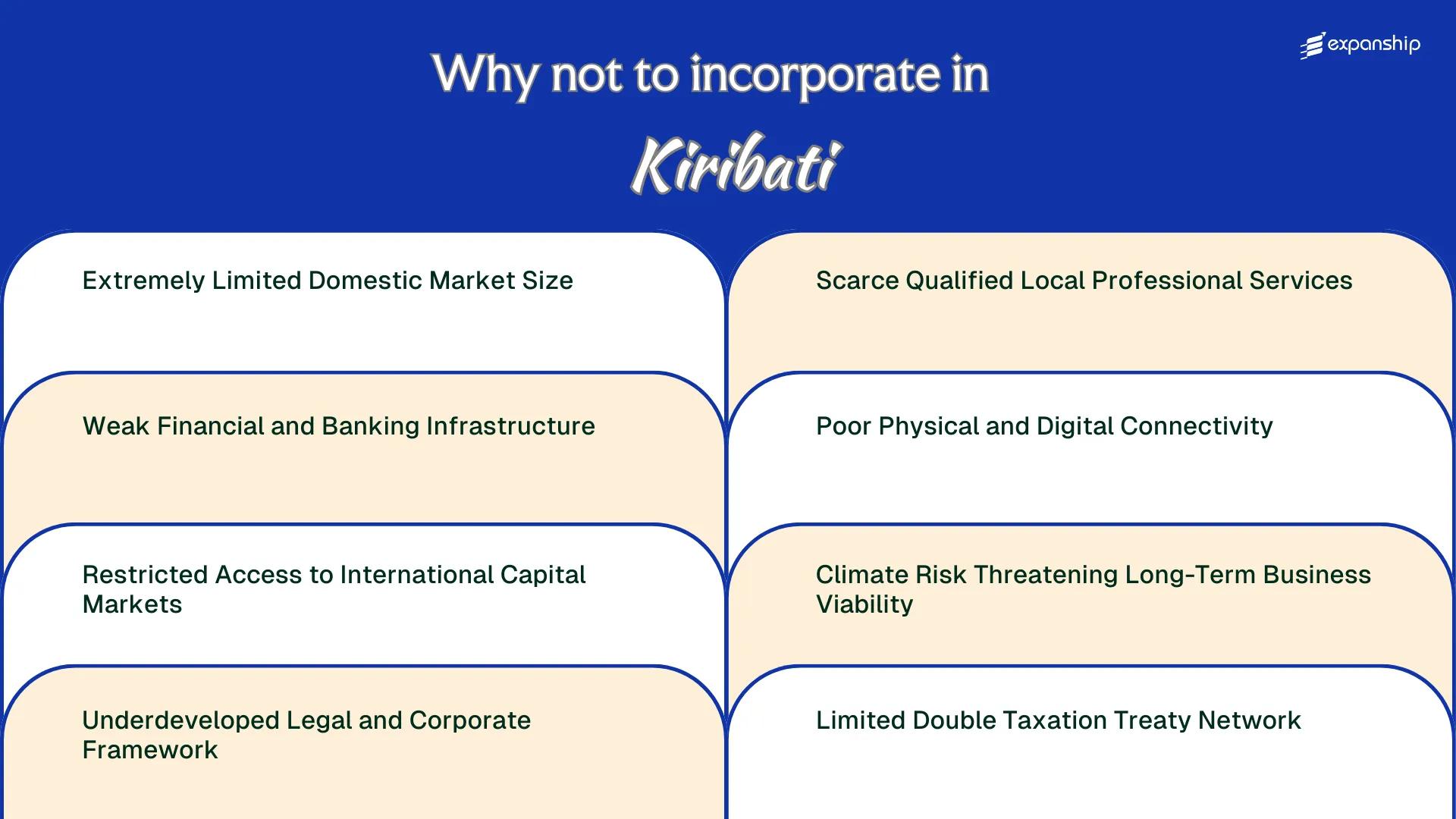

- Businesses incorporated under Kiribati's Companies Act face a domestic consumer base constrained by a national population of under 120,000 spread across remote atolls, making meaningful revenue generation from local trade structurally difficult for most commercial models.

- The absence of a developed interbank lending market and limited correspondent banking relationships in Kiribati restricts access to trade finance and routine treasury functions that businesses in larger Pacific jurisdictions take for granted.

- Kiribati maintains one of the smallest double taxation treaty networks in the Pacific region, exposing cross-border transactions to withholding tax exposure that cannot be mitigated through treaty relief available in competing incorporation jurisdictions.

- Physical isolation across 33 atolls spanning 3.5 million square kilometres of ocean, combined with unreliable internet infrastructure, imposes logistical and operational costs on any entity requiring consistent communication with international counterparties or supply chains.

Incorporating a business in Kiribati places your firm within an evolving regulatory framework, governed primarily by the Companies Act and administered through the Ministry of Commerce, Industry and Cooperatives. The framework is relatively lightly regulated by international standards, though that characteristic introduces its own set of operational complications rather than simplifying compliance.

The disadvantages of incorporating in Kiribati span infrastructure, legal, financial, and environmental categories. How severely these affect your business depends on the industry, the intended corporate structure, and whether the entity is oriented toward domestic trade or international operations.

Foreign investors exploring Pacific incorporation options and business owners considering Kiribati company formation drawbacks as part of a broader market-entry assessment will find this article most directly relevant. The cons of registering a business here are not uniform — a holding structure faces different constraints than an operationally active firm.

Extremely Limited Domestic Market Size

Kiribati small domestic market limitations make the jurisdiction structurally unsuitable for revenue-driven incorporation. The entire nation holds a population of roughly 120,000 people spread across 33 atolls, most of which lack meaningful commercial infrastructure.

A Consumer Base Too Small to Sustain Local Operations

Total GDP sits below USD 300 million, placing the economy among the smallest in the Pacific. For a foreign business, this means the local population cannot realistically absorb goods or services at volumes that justify the fixed costs of incorporation, staffing, and compliance maintenance.

Household purchasing power is constrained further by heavy dependence on remittances and fishing license revenue rather than productive private-sector income. Any business model requiring a domestic consumer base to reach break-even is commercially unviable here.

Scale Constraints on Business Registration and Growth

The limited consumer base compounds the difficulty of registering a commercially active entity under the Companies Act 2015, since the compliance burden remains fixed regardless of revenue generated.

Operational costs do not scale down proportionally to match the market size, meaning your overhead-to-revenue ratio will structurally disadvantage the entity from the outset.

A firm incorporated in Kiribati for domestic trade purposes will almost certainly fail to generate sufficient local revenue to cover operational and compliance costs, given a consumer market this small.

Weak Financial and Banking Infrastructure

Kiribati banking infrastructure problems stem primarily from the country's near-total dependence on a single state-owned institution. The Bank of Kiribati, a majority government-owned commercial bank, handles the bulk of formal financial services, creating a monopolistic environment where foreign businesses have no meaningful choice of banking partner.

With only one functional commercial bank and no meaningful interbank competition, your firm cannot negotiate terms, diversify banking relationships, or access specialized financial products. Corporate credit facilities are extremely limited, and foreign-currency transactions can involve substantial delays.

Practical burdens this creates for a foreign business include:

- Wire transfers to overseas suppliers or parent companies often take significantly longer than in jurisdictions with correspondent banking networks

- Opening a corporate account requires physical presence and documentation processes that cannot be completed remotely, adding travel costs and delays

- No local capital markets exist, so debt financing must be sourced entirely offshore

- Access to trade finance instruments such as letters of credit is severely restricted domestically

Regulatory oversight of financial services falls under the Financial Supervision Commission, but the institutional framework it governs remains thin relative to comparable Pacific island jurisdictions such as Fiji.

Company Incorporation in Kiribati

Understand the full process and requirements for registering a business entity in Kiribati before committing to this jurisdiction.

Restricted Access to International Capital Markets

Kiribati capital markets access restrictions are among the most structurally binding constraints a foreign business owner will encounter after incorporation. The country has no domestic stock exchange, no public debt market, and no formal capital market regulatory framework in the conventional sense. For any entity requiring equity financing or bond issuance, there is simply no local mechanism to facilitate it.

| Financing Mechanism | Availability in Kiribati | Practical Impact on Foreign Business |

|---|---|---|

| Domestic stock exchange | None | Equity listing impossible locally |

| Corporate bond market | None | Debt capital raising not viable domestically |

| Venture capital ecosystem | Effectively absent | Early-stage funding must be sourced entirely offshore |

| Development finance access | Restricted to specific sectors | Most commercial businesses do not qualify |

| Foreign currency lending | Severely limited | Cross-border loan structures face banking constraints |

Accessing offshore capital markets requires your business to demonstrate creditworthiness, audited financials, and regulatory standing that a Kiribati-registered entity struggles to establish. International lenders and institutional investors apply jurisdiction-level risk assessments, and a Pacific microstate without a functioning securities regulator or recognized financial reporting standards authority is frequently excluded from consideration.

Development finance through bodies such as the Asian Development Bank exists but targets infrastructure and government-linked projects. Private commercial firms incorporated locally rarely qualify, leaving foreign investment limitations Kiribati presents as a persistent structural gap rather than a temporary procedural hurdle.

Underdeveloped Legal and Corporate Framework

The Kiribati corporate legal framework weaknesses stem largely from the country's reliance on legislation that was drafted with minimal adaptation for modern international commercial activity. The primary statute governing company formation is the Companies Act, which reflects a basic common law inheritance rather than a developed commercial code designed to attract or regulate foreign investment at scale.

Dispute resolution presents a structural problem. The domestic court system lacks specialist commercial judges, which means complex corporate or contractual matters may be adjudicated by generalist magistrates without deep familiarity with corporate law principles.

There is no functional securities regulator, no dedicated foreign investment tribunal, and no established body of case law that foreign businesses can use to predict legal outcomes. Your firm cannot rely on precedent the way you could in a jurisdiction with decades of commercial court decisions.

- Company registrations and filings are administered under the Companies Act, with no dedicated corporate registry authority separate from general government administration.

- No independent securities or investment regulatory body exists to oversee shareholder disputes or capital-related grievances.

- Foreign ownership restrictions or conditions may apply under the Investment Promotion Act, requiring separate regulatory clearance.

- Enforcement of foreign judgments follows common law principles but lacks a codified treaty framework to guarantee recognition.

Kiribati has no dedicated commercial court, meaning a contractual dispute between two registered companies would be heard in the same court system handling general civil and criminal matters.

Scarce Qualified Local Professional Services

Qualified professional services are acutely scarce in Kiribati, and that scarcity translates directly into higher costs and slower timelines for any foreign business attempting to establish or maintain a compliant corporate presence.

Shortage of Accountants and Legal Advisors

The domestic pool of certified accountants and licensed legal practitioners is extremely thin. Your business will likely struggle to source professionals with direct experience in corporate compliance, financial reporting, or cross-border tax structuring — disciplines that are routine requirements under the Companies Act 2015 administered by the Registrar of General Jurisdiction.

Engaging foreign professionals to fill these gaps is expensive and logistically difficult given the country's geographic isolation.

Operational Consequences for Foreign Entities

Routine compliance tasks — filing annual returns, preparing audited accounts, or obtaining legal opinions — can face significant delays when qualified local support is unavailable. The lack of qualified accountants familiar with Kiribati's regulatory requirements means errors in filings are more likely, creating potential liability for directors.

This skills gap is particularly acute for businesses that cannot justify the cost of retaining offshore advisory firms on a continuous basis.

Professional Guidance for Operating in Kiribati

Expanship helps you address the professional services gap in Kiribati by connecting your business with the right advisory support for compliance, legal, and accounting requirements.

Poor Physical and Digital Connectivity

Kiribati connectivity problems for business are among the most structurally embedded constraints any foreign operator will encounter in the Pacific. The archipelago's 33 islands are spread across 3.5 million square kilometres of ocean, making reliable physical and digital access consistently difficult to maintain.

- Inter-island transport depends heavily on infrequent government-operated vessels and limited air services, meaning supply chains and personnel movements face unpredictable delays that directly increase operational costs.

- International broadband access is constrained by reliance on satellite connectivity, as the country lacks a submarine fibre-optic cable connection, resulting in high latency and bandwidth costs that make data-intensive business operations commercially unviable.

- Poor internet infrastructure in Kiribati companies forces dependency on satellite providers charging rates well above those typical in fibre-connected Pacific neighbours like Fiji or Tonga.

- South Tarawa concentrates what limited infrastructure exists, so any business operating outside the capital faces compounded transport isolation that satellite connectivity alone cannot offset.

- Even where digital access is available, frequent service interruptions create compliance risks for businesses with time-sensitive reporting obligations under the Companies Act 2015.

Climate Risk Threatening Long-Term Business Viability

Kiribati climate risk business viability is not a theoretical concern — it is an active, measurable threat with direct consequences for corporate continuity. The country consists of 33 low-lying atolls, most sitting less than two metres above sea level, making physical business operations acutely vulnerable to permanent inundation.

Sea level rise projections from the IPCC place atoll nations among the most endangered land territories on Earth. If your business holds physical assets, employs local staff, or depends on local infrastructure, that exposure is unhedgeable within the jurisdiction itself.

Saltwater intrusion is already degrading freshwater supplies and agricultural land across the islands. This undermines workforce stability and local supply chains, both of which impose operational costs on any firm with a physical presence.

The government has publicly acknowledged that some outer islands may become uninhabitable within decades, which introduces sovereign-level uncertainty. No legal or contractual framework can fully protect a registered entity against the dissolution of its operating environment.

"Kiribati's highest point is approximately 3 metres above sea level. With mean sea level rise projections reaching up to 1 metre by 2100 under high-emission scenarios, a significant portion of the country's land area faces permanent flood risk." — IPCC Sixth Assessment Report, 2021

Limited Double Taxation Treaty Network

Kiribati's tax treaty network limitations are essentially total: the country has not concluded any double taxation agreements with foreign states. For a business operating across borders, that absence means income earned through a Kiribati-registered entity may be taxed in full by both the source country and your home jurisdiction, with no treaty mechanism to reduce or eliminate that overlap.

Most jurisdictions that host international business activity maintain at least a partial DTT network, even if modest. Without any no double taxation agreement in place, withholding taxes on dividends, royalties, and service fees paid out of partner countries apply at domestic statutory rates, which can significantly increase the effective tax burden on cross-border transactions.

The Kiribati Income Tax Act governs domestic tax obligations, but it contains no provisions that substitute for treaty-level protections. Your business cannot claim reduced withholding rates, tie-breaker residency rules, or mutual agreement procedures that treaties typically provide, leaving disputes over double taxation entirely unresolved at the bilateral level.

This gap is particularly consequential for holding structures, IP licensing arrangements, or businesses with multinational revenue streams, where treaty protection is not a convenience but a structural requirement for tax efficiency.

If your home country does not grant unilateral foreign tax credits under its domestic law, income routed through a Kiribati entity will face full double taxation with no legal remedy available at the treaty level.

Strategies to Overcome These Drawbacks

Overcoming Kiribati incorporation drawbacks requires structural adjustments rather than marginal fixes. The disadvantages discussed in this blog reflect systemic constraints that no single compliance measure can fully resolve.

- Register your entity's operational activities in a jurisdiction with functional banking infrastructure, using the Kiribati company as a holding or nominee structure only.

- Appoint a foreign-qualified legal representative to handle corporate filings under the Companies Act 2015, given the scarcity of locally trained practitioners.

- Source satellite-based connectivity solutions independently to compensate for the absence of reliable undersea cable infrastructure serving I-Kiribati operations.

- Engage correspondent banking relationships through Pacific-region financial institutions before attempting to open a local account with the Bank of Kiribati.

- Obtain climate risk and business continuity insurance from international underwriters, given the documented existential threat to low-lying atoll territories.

- Monitor treaty developments through the Ministry of Finance to assess any future bilateral tax arrangements that may affect your entity's tax position.

These steps operate within the constraints of the Companies Act 2015 and the oversight of the Registrar of Companies. Structural solutions address individual disadvantages but do not alter the underlying regulatory and geographical conditions that define this jurisdiction.

Kiribati's Overall Business Viability

Kiribati's overall business viability assessment points to a jurisdiction with a legitimate legal standing under the Companies Act 2015 and a functioning, if limited, corporate registry. The structural constraints documented across this blog are real and measurable, not theoretical risks.

| Pros | Cons |

|---|---|

| The Companies Act 2015 provides a statutory framework for foreign-owned entities | The domestic market is among the smallest by population and GDP in the Pacific region |

| The country maintains a stable political environment under a constitutional government | Banking infrastructure is thin, with few institutions offering trade finance or multi-currency accounts |

| Incorporation costs and annual compliance fees are generally low compared to major offshore centres | No significant double taxation treaty network exists to reduce withholding tax exposure |

| The jurisdiction is a recognised sovereign state, which supports corporate credibility in some markets | Climate risk poses a documented, long-term threat to the physical and economic continuity of the islands |

| Qualified legal and accounting professionals are scarce, complicating ongoing compliance obligations |

Your business profile determines whether the constraints above are tolerable.

Corporate Compliance Services in Kiribati

Maintain your company's good standing under the Companies Act 2015 with structured compliance support covering annual filings, registered agent requirements, and regulatory reporting.

Conclusion

This Kiribati incorporation drawbacks summary reflects a jurisdiction with genuine structural constraints. Banking access remains thin, physical and digital connectivity is among the most limited in the Pacific, and the absence of a developed double taxation treaty network adds measurable cross-border tax friction. Climate risk compounds these factors, introducing long-term uncertainty that few comparable jurisdictions face. Incorporating here requires a clear-eyed view of what the operating environment actually offers. Professional and legal support may need to be sourced externally, and compliance structures built largely without local institutional backing.

Expanship's Support for Your Kiribati Expansion

Expanship Kiribati company formation support starts with understanding what makes this jurisdiction operationally demanding. From coordinating with the Registrar of Companies under the Companies Ordinance to addressing the banking access difficulties and climate-related due diligence obligations covered throughout this blog, your workload as a foreign incorporator is significant. Expanship's role is to reduce that burden at each stage, not to reframe the jurisdiction's structural constraints.

Our team handles the full formation and ongoing compliance cycle for your entity in Kiribati.

- Your company registration documents are prepared and submitted to the relevant authority in proper form.

- A registered agent and local office address are provided to satisfy statutory presence requirements.

- Government filings and liaison with regulatory bodies are managed on your behalf.

- Post-incorporation compliance obligations are monitored and handled as they arise.

- Banking introductions are facilitated to support your firm's account opening process.

- Tax registration and coordination with local authorities are completed as required.

Reach out through Expanship Kiribati to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

It affects any company with cross-border income flows, though the severity depends on where your parent entity or shareholders are based. Kiribati has not signed double taxation agreements with major trading partners, meaning profits distributed to foreign shareholders may face taxation in both Kiribati and the recipient jurisdiction without any treaty mechanism to reduce or eliminate that double charge. Companies structured through jurisdictions with broad treaty networks will feel this gap more acutely than those operating solely within Kiribati.

Your company remains legally responsible for filing obligations regardless of local professional capacity. The scarcity of qualified service providers in Kiribati means delays in statutory filings, audits, or legal documentation are a structural risk rather than an exceptional circumstance. Regulators do not suspend compliance obligations because local expertise is thin.

By most measures, yes. Neighbouring jurisdictions such as Vanuatu and the Marshall Islands have developed dedicated offshore corporate legislation, specialist registries, and a body of case law that supports commercial dispute resolution. Kiribati's corporate framework remains limited in scope, and the absence of well-tested legal precedent creates uncertainty when contractual or ownership disputes arise.

The direct cost is difficult to quantify precisely, but businesses routinely absorb higher international wire transfer fees, longer settlement times, and currency conversion costs because Kiribati lacks a domestic interbank market and relies heavily on correspondent banking relationships through Australian and Fijian institutions. Delays in receiving or sending funds internationally can also create working capital shortfalls that compound over time.

Raising funds offshore before incorporation sidesteps the local capital market problem but does not resolve it entirely. Once your entity is registered in Kiribati, ongoing capital needs, refinancing, or equity raises remain constrained because international institutional investors and lenders typically require a credible legal framework, enforceable security interests, and a functioning court system before committing capital. Pre-incorporation funding buys time; it does not create the infrastructure that Kiribati currently lacks.

The risks are operational and financial. Kiribati's outer islands rely on intermittent satellite internet, and inter-island shipping schedules are infrequent, meaning supply chain delays and communication blackouts are a recurring feature of doing business rather than edge-case scenarios. Any business model requiring real-time data exchange, just-in-time inventory, or consistent client communication will face structural friction that directly increases operating costs.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.