Key Takeaways

- Kiribati's territorial tax system exempts foreign-sourced income from domestic corporate tax, making it a structurally efficient base for holding entities and trade facilitation companies with earnings generated outside the jurisdiction.

- Under the Companies Ordinance, private companies limited by shares can be established by foreign investors with ownership structures that remain manageable without extraordinary legal complexity.

- The Registrar of Companies, operating within the Ministry of Finance and Economic Development, oversees a registration framework that imposes minimal ongoing compliance and reporting obligations on incorporated entities.

- Businesses oriented toward maritime operations or fisheries licensing stand to benefit from Kiribati's geographic position across the central Pacific and its access to regional trade arrangements that carry direct market implications.

Kiribati is an independent Pacific Island nation comprising 33 atolls and reef islands spread across the central Pacific Ocean. The benefits of incorporating in Kiribati draw interest from businesses looking toward the Pacific as part of broader regional strategies. Company registration falls under the oversight of the Registrar of Companies, operating within the Ministry of Finance and Economic Development. The most common legal vehicle used by foreign businesses is the private company limited by shares.

From a tax posture perspective, the jurisdiction applies a territorial approach, meaning foreign-sourced income is generally not subject to domestic corporate tax. Foreign ownership is permitted, though investment in certain sectors may be subject to local regulatory conditions under national investment policy.

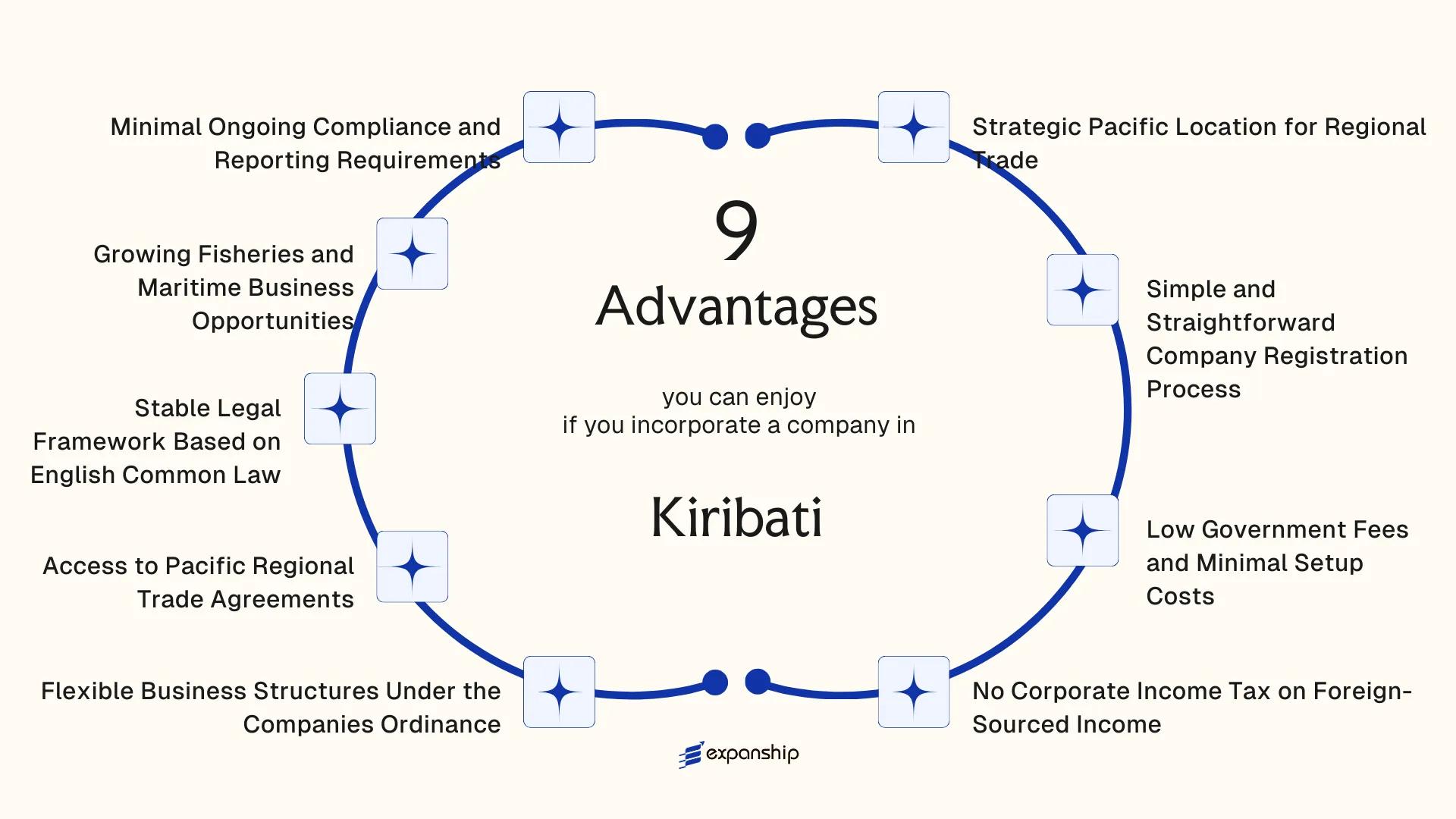

This article examines the key advantages that the jurisdiction's corporate framework offers to foreign investors and business operators. Kiribati company formation advantages span regulatory, geographic, and fiscal dimensions — each addressed in the sections that follow.

Strategic Pacific Location for Regional Trade

Kiribati spans approximately 3.5 million square kilometres of the central Pacific Ocean, placing it within practical reach of major regional economies including Australia, New Zealand, Japan, and the United States. This geographic spread across three island groups — the Gilbert, Phoenix, and Line Islands — gives a registered entity a genuine multi-ocean positioning that few Pacific jurisdictions can match.

Proximity to Key Asia-Pacific Markets

The Line Islands, including Kiritimati (Christmas Island), sit close to the International Date Line, making them among the first territories to begin each business day. For firms managing time-sensitive transactions across Asian and American markets, that position creates a scheduling advantage that is structural, not incidental.

Access to Pacific Shipping and Aviation Routes

Kiribati's position along established trans-Pacific shipping corridors means businesses in maritime trade, fishing logistics, and cargo services can operate within well-trafficked international routes. Regional air connectivity, though limited to select carriers, connects the islands to Fiji and other Pacific transit hubs, supporting operational continuity for businesses dependent on physical movement of goods or personnel.

A company registered in Kiribati Pacific location trade advantages context can hold regional contracts, manage Pacific-facing operations, and maintain a compliant presence at the intersection of Asian and American trade flows.

Simple and Straightforward Company Registration Process

Registering a company under the Kiribati Companies Ordinance is a process that foreign investors can complete without the procedural burden associated with many other Pacific or Commonwealth jurisdictions. The Kiribati company registration simple process benefits stem largely from a registration framework that does not require extensive pre-approval stages, local directorship mandates, or complex notarization procedures.

The Registrar of Companies administers business registration, and the documentation requirements are relatively contained. A foreign investor does not need to establish a physical presence before incorporation is complete.

Several structural features keep the registration process accessible:

- Applicants are not required to submit audited financials at the point of incorporation

- No minimum paid-up capital threshold applies during the registration stage

- Foreign nationals can act as directors without a local co-director requirement

- Name reservation can be handled as a preliminary step, reducing back-and-forth delays

The practical consequence is a shorter timeline between decision and operational readiness. For businesses looking to begin trading or holding assets in the Pacific region, a faster formation process means earlier access to commercial activity. Straightforward business registration in a jurisdiction reduces the administrative cost of entry, which matters particularly for smaller firms testing a new market before committing significant resources.

Company Incorporation in Kiribati

Register your company in Kiribati through a straightforward process with minimal documentation requirements and no local directorship mandate.

Low Government Fees and Minimal Setup Costs

Government fees for incorporating a company in Kiribati rank among the lowest in the Pacific region, which translates directly into reduced upfront capital requirements for foreign founders. Under the Companies Ordinance (Cap 160), the fees payable to the Registrar of Companies for registering a new entity are structured at a modest flat rate, meaning your initial cost exposure is predictable from day one.

| Fee Type | Applicable Stage | General Cost Level |

|---|---|---|

| Company name reservation | Pre-registration | Low flat fee |

| Registration fee (private company) | Incorporation | Low flat fee |

| Certificate of incorporation | Incorporation | Included or nominal |

| Annual return filing fee | Ongoing compliance | Low flat fee |

For a foreign business owner, the practical effect is that capital which would otherwise go toward administrative costs remains available for operational use. Many comparable small-island jurisdictions charge significantly higher registration fees relative to their economic scale, so the affordability here is a structural feature of the regulatory design, not an anomaly.

Ongoing government charges for maintaining a registered company also remain low. Annual return fees payable to the Registrar are set at rates that do not increase materially with company size or activity level, which keeps the cost of maintaining a dormant or holding entity proportionally small. This structure suits businesses that require a formal Pacific presence without generating immediate local revenue.

No Corporate Income Tax on Foreign-Sourced Income

Kiribati operates a territorial tax system, meaning resident companies are generally not taxed on income derived from foreign sources. For a holding company or international trading entity incorporated under the Companies Ordinance, this is a direct cost advantage: profits generated outside the jurisdiction's territory remain outside the reach of local corporate tax assessment.

The underlying framework is administered by the Kiribati Revenue Authority under the Income Tax Ordinance (Cap 26). Under this regime, a locally incorporated entity conducting business internationally can retain foreign earnings without triggering a domestic tax liability on those funds, provided the income originates and is earned outside Kiribati.

For businesses structured to separate domestic and foreign revenue streams, this distinction carries material financial weight. A company earning consultancy fees, licensing royalties, or service income from clients in Asia or the Pacific can record those receipts without a corporate income tax charge applying at the entity level.

Keep the following points in mind to preserve this benefit:

- Income must demonstrably originate outside Kiribati's territorial boundary

- Maintain clear accounting separation between domestic and foreign revenue

- Confirm classification under the Income Tax Ordinance (Cap 26) with a local tax adviser

- Local-source income remains subject to standard corporate tax rates

Kiribati's tax-free treatment of foreign earnings applies to standard locally incorporated companies, not just a special offshore class, meaning no separate offshore registration category is required to access this benefit.

Flexible Business Structures Under the Companies Ordinance

The Kiribati Companies Ordinance provides a legal framework that accommodates different levels of liability, ownership, and operational complexity. For foreign investors, this flexibility means your entity can be structured to match your business model rather than requiring adaptation to a rigid, one-size-fits-all corporate form.

Private Companies Limited by Shares

The most commonly used structure under the Ordinance is the private company limited by shares, which caps shareholder liability to the amount unpaid on their shares. This boundary between personal assets and business obligations is a practical protection for overseas investors who cannot be physically present to manage day-to-day risk. A single shareholder and single director suffice for incorporation, which reduces setup overhead for small or holding-purpose entities.

Companies Limited by Guarantee

Where profit distribution is not the primary objective, a company limited by guarantee offers an alternative form with members' liability fixed to a predetermined contribution amount. This structure suits foundations, regional representative offices, or entities established for specific project-based activity rather than ongoing commercial trade. Because the Ordinance recognizes both forms within the same registration system, your business can transition between structures through a formal alteration process without re-incorporating from scratch, preserving your corporate history and registration standing.

Structure Your Kiribati Company the Right Way

Get expert guidance on selecting and registering the most suitable entity type under the Kiribati Companies Ordinance for your specific business objectives.

Access to Pacific Regional Trade Agreements

Kiribati's membership in Pacific regional trade agreements offers tangible access advantages that are difficult to replicate through incorporation in non-Pacific jurisdictions. As a member of the Pacific Islands Forum and a signatory to PACER Plus (Pacific Agreement on Closer Economic Relations Plus), companies registered here operate within a framework designed to reduce trade barriers across Forum Island Countries and facilitate movement of goods and services within the Pacific region.

- PACER Plus, which entered into force in 2020, creates preferential trade conditions among its signatories, including Australia and New Zealand. A firm incorporated in Kiribati may be positioned to benefit from these preferences when engaging in qualifying regional commerce, rather than entering those markets as a third-country entity subject to standard tariff arrangements.

- Forum membership also connects your business to regional economic cooperation mechanisms and development frameworks administered through Pacific Forum bodies, which can support market entry discussions and institutional engagement across member states.

- For businesses oriented toward regional supply chains, service exports, or fisheries-related trade, the Pacific regional trade agreement benefits available through Forum membership provide a structural footing that businesses incorporated outside the Pacific cannot access through treaty equivalence alone.

Eligibility for specific preferential treatment depends on the nature of your business activity and applicable rules of origin under PACER Plus.

Stable Legal Framework Based on English Common Law

Kiribati's legal system is rooted in English common law, a heritage carried forward from its time as a British protectorate. For foreign business owners, this matters because common law jurisdictions offer a body of established judicial precedent, making contractual obligations and property rights more predictable than in civil law systems with less interpretive history.

Corporate activity in the country is governed by the Companies Ordinance, which itself draws on common law principles. Courts apply precedent-based reasoning, meaning disputes over contracts, liability, or directorial duties are resolved through a framework that international lawyers and advisors already understand. You are not required to engage specialists in an unfamiliar legal tradition.

English remains the official language of legislation and legal proceedings. This removes translation risk from your contracts and governance documents, which is a practical consideration when managing cross-border relationships or resolving disputes involving overseas parties.

A hypothetical scenario: A foreign-owned trading firm incorporated under the Companies Ordinance enters a supply contract with a regional partner. A breach occurs. Because the governing law defaults to principles consistent with English common law precedent, the firm's overseas legal counsel can assess liability exposure and draft a claim without commissioning local legal translation or independent statutory interpretation. Estimated legal advisory savings versus a non-English civil law jurisdiction: 15 to 30% on international dispute preparation costs.

Growing Fisheries and Maritime Business Opportunities

Kiribati fisheries sector business opportunities are among the most commercially significant in the Pacific, rooted in sovereign control over one of the world's largest Exclusive Economic Zones (EEZ), covering approximately 3.5 million square kilometers. Foreign fishing operators and maritime businesses that incorporate locally gain direct access to licensing arrangements administered under this EEZ framework, which would otherwise require negotiating access from outside the jurisdiction.

Fishing license revenues represent a primary source of national income for Kiribati, meaning the government has a structural incentive to maintain and administer licensing processes for foreign commercial operators. Your business benefits from operating within a framework that the state actively sustains.

Key commercial entry points for incorporated entities include:

- Access to tuna fishing licenses under the Vessel Day Scheme (VDS), administered through the Parties to the Nauru Agreement (PNA)

- Participation in joint venture arrangements with local operators

- Shore-based processing and transshipment services tied to the fishing fleet

The PNA's VDS allocates fishing days across member states, and an incorporated entity in the jurisdiction can engage with this system under terms not available to purely foreign-registered firms.

Fishing licenses and maritime operating rights are subject to national fisheries legislation and may require local equity participation or government approval before a foreign-owned entity qualifies.

Minimal Ongoing Compliance and Reporting Requirements

Kiribati minimal compliance requirements for companies translate directly into lower administrative costs and reduced management overhead for foreign business owners. Under the Companies Ordinance (Cap 160), registered companies face relatively limited statutory obligations compared to many other jurisdictions, meaning less time spent on paperwork and fewer fees paid to advisers or filing agents each year.

Annual Return Obligations

Companies registered under the Companies Ordinance are generally required to file an annual return with the Registrar of Companies. This filing confirms basic corporate details rather than demanding extensive financial disclosure. For a foreign-owned entity with no local trading activity, this represents a contained and predictable compliance cycle.

Financial Statement Requirements

The reporting threshold for full audited accounts is not applied universally to all registered companies, particularly smaller or dormant entities. This means your business may avoid the cost of a statutory audit altogether, depending on its size and activity level. The practical saving here can be significant when compared to jurisdictions that mandate audits regardless of turnover.

Absence of Complex Regulatory Filings

There is no securities regulator or financial services commission imposing ongoing disclosure obligations on standard trading companies. Required filings generally include:

- Annual return submission to the Registrar of Companies

- Maintenance of a registered office address within the jurisdiction

- Keeping an updated register of directors and shareholders

This limited filing structure means your administrative calendar stays manageable without specialist compliance staff or recurring regulatory engagement.

Is Kiribati the Right Jurisdiction for Your Business?

Deciding whether Kiribati suits your business depends on the type of entity you intend to operate and the markets you plan to serve. As a primary keyword consideration, the question of whether Kiribati is the right jurisdiction for your business is best answered by comparing it against the Pacific jurisdictions a foreign investor would realistically evaluate alongside it. Vanuatu, the Marshall Islands, and Fiji each target overlapping investor profiles, particularly those seeking low-cost Pacific incorporation with limited domestic tax exposure.

The comparison below focuses on parameters where the Republic of Kiribati holds a neutral or favourable position. Vanuatu attracts offshore holding structures but carries higher professional service costs. Fiji has a more developed financial sector yet imposes corporate tax on resident companies at rates that affect operational entities. The Marshall Islands is well-regarded for maritime registry purposes but has limited regional trade positioning. Kiribati's registration framework under the Companies Ordinance and its fisheries access agreements within the Pacific Island Forum create a specific niche that these alternatives do not replicate in the same configuration.

| Parameter | Kiribati | Vanuatu | Marshall Islands | Fiji |

|---|---|---|---|---|

| Corporate Tax on Foreign-Sourced Income | None | None | None | Subject to tax if resident |

| Legal System | English Common Law | Dual (English/French) | US Common Law | English Common Law |

| Maritime/Fisheries Framework | Established via WCPFC | Limited | Strong (registry focus) | Moderate |

| Government Registration Fees | Low | Moderate | Moderate | Moderate to High |

| Pacific Forum Membership | Yes | Yes | No | Yes |

Compliance Services for Companies in Kiribati

Understand your ongoing filing, reporting, and regulatory obligations under Kiribati's Companies Ordinance.

Conclusion

Kiribati presents a coherent case for foreign business incorporation: a foreign-sourced income exemption grounded in territorial tax principles, a Companies Ordinance that keeps structural and compliance requirements manageable, and access to Pacific regional trade arrangements that carry tangible market implications. The benefits of incorporating in Kiribati are most relevant to specific business models, particularly those oriented toward maritime operations, fisheries licensing, or Pacific-facing trade activity.

Your business structure, industry, and cross-border obligations will determine how well this jurisdiction fits. A holding entity or a trade facilitation company will relate to Kiribati's framework differently than an operationally active firm with local revenue.

For businesses where the fit is sound, the practical steps of company formation under local law are well-defined and manageable without extraordinary legal complexity. Knowing that the framework exists is the starting point; understanding how to apply it to your specific situation is where the real work begins.

Let Expanship Handle Your Kiribati Incorporation

Expanship's Kiribati company incorporation service covers the full formation process under the Companies Ordinance, from name reservation with the Registrar of Companies to certificate of incorporation issuance. The blog sections above cover the tax treatment of foreign-sourced income, compliance obligations, and the structural flexibility available under local law. Expanship's role is to translate those regulatory features into a functioning entity without requiring you to manage the process directly from abroad.

Our service scope includes:

- Document preparation, notarization, and legalization for foreign directors and shareholders

- Registered agent and registered office provision as required under the Companies Ordinance

- Government filing and direct liaison with the Registrar of Companies

- Post-incorporation compliance management, including annual return obligations

- Banking introduction assistance for corporate account setup

- Ongoing support for any amendments to the company's constitutional documents

For foreign business owners, the practical challenge is not understanding the rules but executing the steps accurately across a remote Pacific jurisdiction with limited local infrastructure. Expanship coordinates each stage with the relevant authorities on your behalf, reducing the administrative friction that typically accompanies formation in smaller island jurisdictions.

To discuss your incorporation requirements, contact Expanship Kiribati directly.

Frequently Asked Questions (FAQ)

Foreign-sourced income is not subject to corporate income tax under the general tax framework applicable to qualifying companies. This territorial approach means that a firm conducting business operations outside the jurisdiction is not assessed on those offshore earnings by the Kiribati Tax Administration. Income generated domestically from local activities is treated differently and may attract applicable taxes under the Revenue Ordinance.

Registration timelines are generally short compared to many other Pacific jurisdictions, with approvals often processed within a matter of days once documentation is complete and submitted to the Registrar of Companies. The exact duration depends on document accuracy and any queries raised by the Registrar during review. Delays most commonly arise from incomplete submissions rather than processing backlogs.

A local director is not an absolute statutory requirement under the Companies Ordinance for foreign-owned entities, though maintaining a registered address within the jurisdiction is required for official correspondence. Some foreign investors appoint a local registered agent to satisfy this address requirement without establishing a full physical office. The registered agent's address serves as the official point of contact for regulatory notices.

Failure to meet compliance obligations, including filing annual returns with the Registrar of Companies, can result in administrative penalties and, in persistent cases, deregistration of the company. Once deregistered, the entity loses its legal standing and any contracts or licenses tied to that registration may become unenforceable. Reinstatement is possible in some circumstances but involves additional fees and procedural requirements under the Companies Ordinance.

The answer depends on the specific operational requirements of your business. Kiribati holds one of the largest Exclusive Economic Zones in the Pacific, covering approximately 3.5 million square kilometres, which gives fisheries and maritime-linked businesses direct access to commercially significant waters under licensing arrangements administered by the Kiribati Fisheries Division. Other Pacific jurisdictions may offer different tax incentives or treaty networks, so a direct comparison requires evaluating those specifics against your intended business activity.

As a member of the Pacific Island Countries Trade Agreement (PICTA) and a participant in broader regional frameworks under the Pacific Agreement on Closer Economic Relations (PACER), businesses registered in Kiribati may qualify for preferential trade terms with participating Pacific and Australasian economies. Eligibility for specific treaty benefits depends on the nature of the goods or services and applicable rules of origin. You should confirm current treaty participation status directly with the Kiribati Ministry of Commerce, Industry and Cooperatives, as treaty schedules are subject to revision.

Under the Companies Ordinance (Cap 160), registered companies are required to file annual returns with the Registrar of Companies to maintain their status in good standing. The reporting obligations are comparatively limited relative to many OECD jurisdictions, with no mandatory statutory audit requirement for smaller private entities in the general framework. Specific obligations may vary depending on the company's size, sector, and whether it holds particular licences or operates under separate regulatory schemes.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.