Key Takeaways

- The private limited company (Ltd) is the dominant incorporation choice in Kenya, serving resident entrepreneurs, foreign investors, and multinational subsidiaries under the Companies Act, 2015.

- Entity registration in Kenya falls under the Business Registration Service (BRS) through the Registrar of Companies, which has been expanding its digital infrastructure for processing new filings.

- Foreign businesses entering Kenya can operate through a branch office or representative office without undergoing separate local incorporation, though each carries distinct regulatory obligations.

- Cooperative societies, companies limited by guarantee, and partnerships each occupy a specific structural niche — collective economic activity, membership-based organisations, and professional service providers, respectively.

Introduction to Entity Types in Kenya

Kenya sits in East Africa, bordered by Tanzania, Uganda, South Sudan, Ethiopia, and Somalia, with a coastline along the Indian Ocean. It is an independent republic and one of the region's most active destinations for foreign direct investment. Businesses registering in the country fall under the jurisdiction of the Registrar of Companies, operating under the Business Registration Service (BRS) and governed by the Companies Act, 2015.

The tax posture is residential and source-based, with corporate income tax applied to locally derived profits. Available types of business entities in Kenya span a range of structures suited to different ownership models, liability preferences, and operational scales.

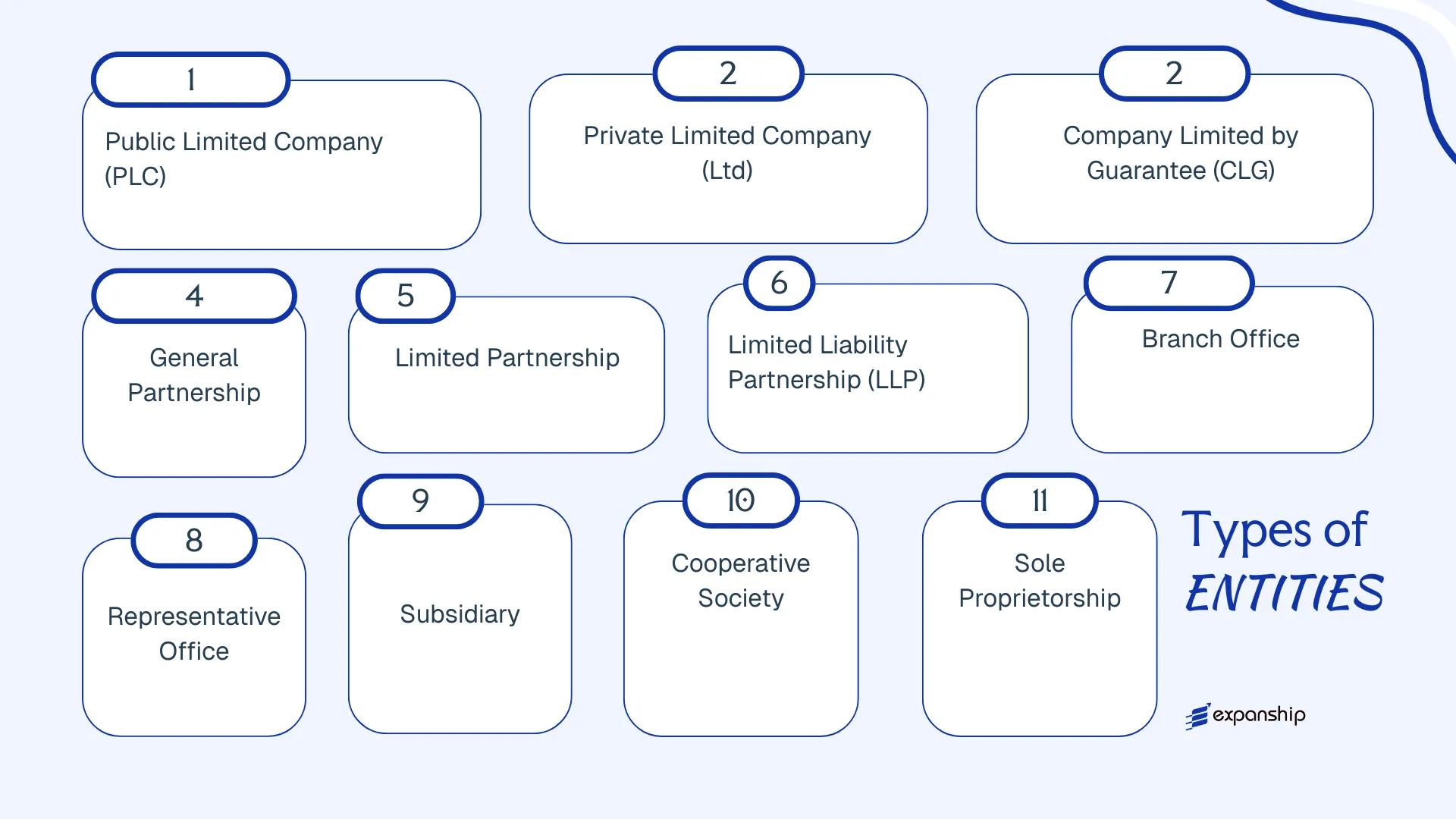

Entities recognized under Kenyan law include the Private Limited Company, Public Limited Company, Company Limited by Guarantee, General Partnership, Limited Partnership, Limited Liability Partnership, Branch Office, Representative Office, Subsidiary, Cooperative Society, and Sole Proprietorship. Each carries distinct registration requirements, governance obligations, and liability implications that this article examines in turn.

An Overview of Business Structures in Kenya

Under the Companies Act No. 17 of 2015 and several complementary statutes, Kenya recognizes multiple distinct entity types available to both local and foreign investors. Each structure carries different implications for liability, taxation, governance, and permitted commercial activity. The sections that follow examine each form in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company | Incorporated company | Limited to shares | Taxed | Yes | 7 shareholders | Registrar of Companies | Companies Act 2015 |

| Private Limited Company | Incorporated company | Limited to shares | Taxed | Yes | 1 shareholder | Registrar of Companies | Companies Act 2015 |

| Company Limited by Guarantee | Incorporated company | Limited to guarantee | Taxed / Exempt | Restricted | 1 member | Registrar of Companies | Companies Act 2015 |

| General Partnership | Unincorporated firm | Unlimited | Taxed | Yes | 2 partners | Registrar of Companies | Partnership Act Cap 29 |

| Limited Partnership | Unincorporated firm | Mixed | Taxed | Yes | 2 partners | Registrar of Companies | Partnership Act Cap 29 |

| Limited Liability Partnership | Incorporated body | Limited | Taxed | Yes | 2 partners | Registrar of Companies | Limited Liability Partnership Act 2011 |

| Branch Office | Foreign company extension | Parent liable | Taxed | Yes | N/A | Registrar of Companies | Companies Act 2015 |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | No | N/A | Kenya Revenue Authority | Various |

| Subsidiary | Incorporated company | Limited to shares | Taxed | Yes | 1 shareholder | Registrar of Companies | Companies Act 2015 |

| Cooperative Society | Incorporated society | Limited | Taxed / Exempt | Yes | 10 members | Commissioner for Co-operatives | Co-operative Societies Act Cap 490 |

| Sole Proprietorship | Unincorporated business | Unlimited | Taxed | Yes | 1 owner | County Government / Registrar | Registration of Business Names Act Cap 499 |

Each of these structures is examined in full in the sections below.

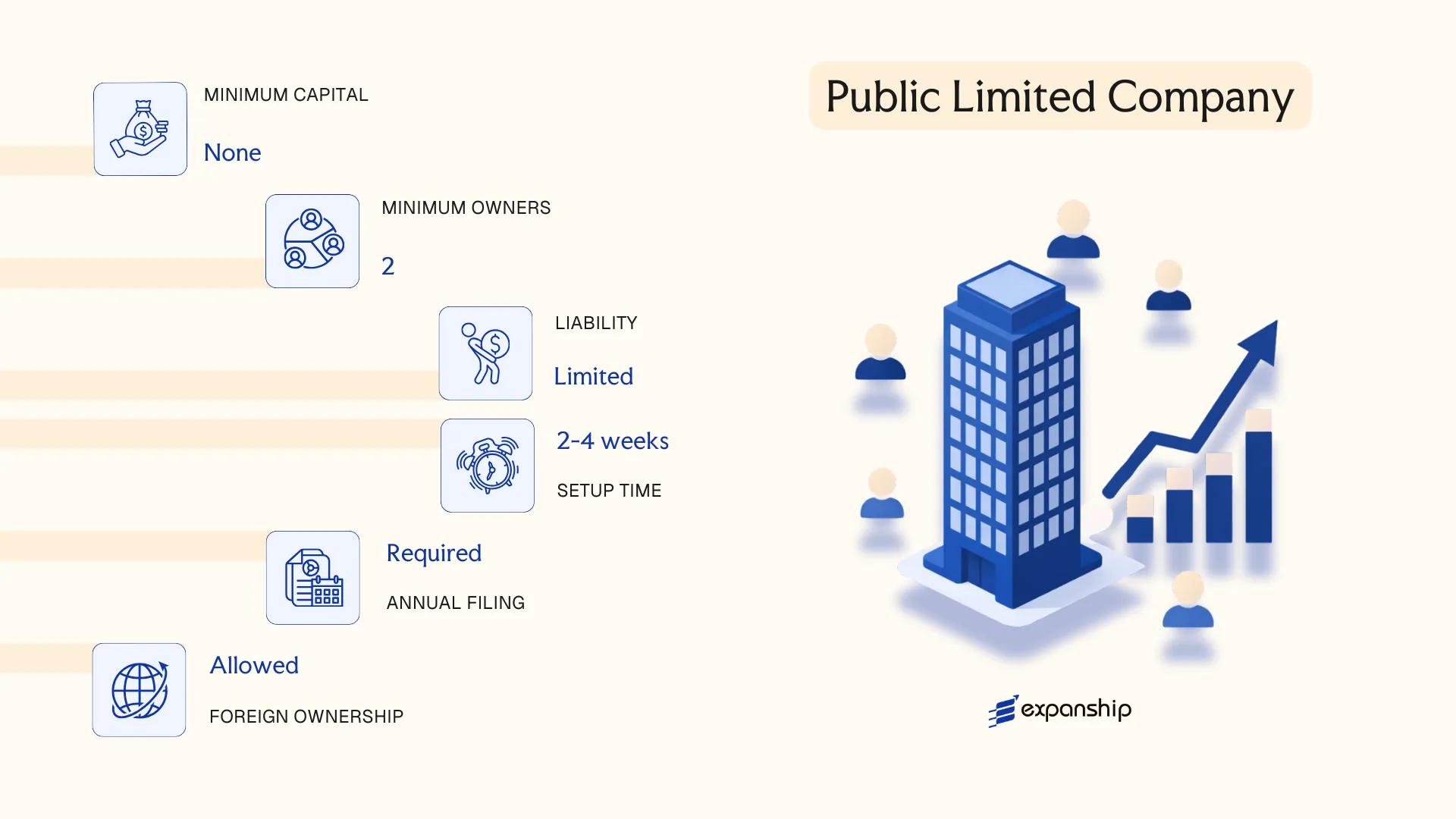

Public Limited Company (PLC)

A public limited company Kenya PLC is governed by the Companies Act, 2015 (Cap. 486), which replaced the older Companies Act of 1962 and brought Kenyan corporate law broadly in line with modern Commonwealth standards. Like its private counterpart, a PLC holds a separate legal personality distinct from its shareholders, meaning the entity can own assets, enter contracts, and incur liabilities in its own name.

Shares in a public company may be offered to the general public and, where applicable, listed on the Nairobi Securities Exchange (NSE). This distinguishes the structure from a private limited company, where any public offering of shares is prohibited.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Incorporated under the Companies Act, 2015 |

| Members | Shareholders (minimum 7; no maximum) and Directors (minimum 2) | Company Secretary required; must be a qualified professional |

| Local Presence | Registered office address in Kenya | Physical address required; P.O. Box not sufficient |

| Share Capital | Minimum allotted share capital of KES 500,000 | Must be denominated in Kenyan Shillings unless otherwise approved |

| Share Transferability | Shares freely transferable to the public | Listing on the NSE is optional, not mandatory |

| Privacy | Accounts and shareholder register are publicly accessible | Filed with the Registrar of Companies under the Business Registration Service |

Focus Points

- Taxation: Subject to corporate income tax at 30% for resident companies; VAT at 16% applies to taxable supplies; withholding tax applies to dividends, royalties, and management fees at rates varying by residency and applicable treaty.

- Annual Compliance: Must file annual returns, audited financial statements, and hold an Annual General Meeting (AGM); filings submitted to the Business Registration Service (BRS).

- Treaty Access: Kenya has double taxation agreements with several countries including the UK, India, and Zambia; a PLC resident in Kenya may access these treaties.

- Listing Requirements: PLCs seeking NSE listing must separately satisfy the Capital Markets Authority (CMA) requirements under the Capital Markets Act.

- Conversion: A PLC may be re-registered as a private limited company under the Companies Act, 2015, subject to shareholder approval and BRS filing.

Closing

A PLC suits large-scale commercial or industrial operations intending to raise capital from the public or pursue an eventual exchange listing; the structure's mandatory audit and disclosure obligations, however, make it administratively heavier than a private company. The freely transferable share structure provides liquidity for investors, but compliance costs are correspondingly higher.

Established businesses seeking public capital raising or NSE listing, where the administrative burden of full disclosure and audited reporting is operationally viable.

Company Incorporation in Kenya

Incorporate a Public Limited Company or any other business structure in Kenya with end-to-end support from Expanship.

Private Limited Company (Ltd)

Governed by the Companies Act, 2015 (Cap. 486), a private limited company in Kenya is a distinct legal entity separate from its shareholders. The Kenya Ltd company registration process is administered by the Registrar of Companies under the Business Registration Service (BRS). Liability of each member is limited to any unpaid amount on their shares, meaning personal assets are not exposed to company debts.

This structure is the most common vehicle for commercial activity among resident and foreign investors alike. To incorporate a private limited company in Kenya, the entity must restrict share transfers, prohibit public share offerings, and limit its membership count.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by shares | Separate legal personality; governed by Companies Act, 2015 |

| Members | Shareholders: min. 1, max. 50 | Excludes employees who hold shares |

| Directors | Min. 1 director required | No mandatory local director requirement under current law |

| Local Presence | Registered office address in Kenya required | Must be a physical address; P.O. Box alone is insufficient |

| Share Capital | KES-denominated; no statutory minimum | Authorized and paid-up capital declared at incorporation |

| Privacy | Beneficial ownership disclosed to BRS | Register of members is not publicly searchable by default |

Focus Points

- Taxation: Subject to 30% corporate income tax on resident companies; VAT applies at 16% on taxable supplies; withholding tax applies to dividends, interest, royalties, and management fees at varying rates; stamp duty applies to share transfers.

- Annual Compliance: Annual returns must be filed with the BRS; audited financial statements required unless exempt under the Act.

- Treaty Access: Kenya's tax treaty network may reduce withholding tax rates on cross-border payments for qualifying resident entities.

- Conversion: A private limited company may re-register as a public limited company by passing a special resolution and meeting PLC requirements under the Companies Act, 2015.

- Restrictions: Cannot offer shares to the public or list on a securities exchange without first converting to a PLC.

Closing

A private limited company suits trading operations, holding structures, and local subsidiary arrangements where liability containment and operational continuity are priorities. One clear limitation is the 50-member cap on shareholders, which restricts equity fundraising at scale.

Best suited for foreign investors establishing a locally incorporated operating entity or a wholly owned subsidiary in Kenya.

Company Limited by Guarantee

A company limited by guarantee Kenya is governed by the Companies Act, 2015 (Cap. 486), the same legislation that regulates share-based companies. Unlike a standard limited company, this entity has no share capital. Instead, members commit to contributing a defined amount toward the company's debts if it is wound up — this commitment is the "guarantee." The entity holds separate legal personality and its members bear limited liability.

Registered through the Business Registration Service (BRS), this structure is the standard vehicle for non-profit organisations, professional associations, trade bodies, and charitable foundations. A non-profit company Kenya guarantee arrangement can also apply for exemptions under the Income Tax Act and, depending on its activities, may require further registration with the NGO Coordination Board.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate | Separate legal personality; no share capital |

| Members | Referred to as Members; minimum 1, no statutory maximum | Members are guarantors, not shareholders |

| Directors | Minimum 1 director required | At least one director must be a natural person |

| Local Presence | Registered office address in Kenya required | PO Box alone is not sufficient |

| Guarantee Amount | Set in the memorandum; typically KES 1–1,000 | Only called upon during winding up |

| Privacy | Memorandum, articles, and member register filed with BRS | Publicly searchable via the BRS portal |

Focus Points

- Taxation: Generally exempt from corporation tax on non-profit income if approved by the Kenya Revenue Authority (KRA), but commercial or trading income remains taxable; VAT registration is required if taxable turnover exceeds the statutory threshold; withholding tax applies to payments such as dividends, royalties, and management fees as standard.

- NGO Registration: Entities soliciting public funds or operating as charities must also register with the NGO Coordination Board under the Non-Governmental Organizations Co-ordination Act, 1990.

- Annual Compliance: Annual returns must be filed with BRS; audited financial statements are required under the Companies Act, 2015.

- Restrictions: Profits cannot be distributed to members; any surplus must be applied toward the entity's stated objectives.

- Conversion: Conversion to a share-based company is not provided for under the Companies Act, 2015; dissolution and re-incorporation would be required to change structure.

This entity suits membership organisations, NGOs, and professional bodies that need a formal corporate structure without distributable equity. The liability protection it offers members is a clear operational advantage; its restriction on profit distribution makes it unsuitable for any commercial venture where investor returns are expected.

Best suited for non-governmental organisations, charities, professional associations, and trade bodies operating in Kenya on a non-profit basis.

Partnerships [General Partnership, Limited Partnership, Limited Liability Partnership]

Partnerships in Kenya are governed primarily by the Partnerships Act, 2012 (No. 16 of 2012), which consolidated and modernised the earlier framework. A limited liability partnership Kenya LLP formation results in a body with separate legal personality, distinct from its partners, and with members shielded from personal liability for the firm's debts beyond their agreed contribution.

Three recognised forms exist under this legislation. Each carries a different liability profile, making the choice of structure a consequential decision for the partners involved.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Registered under the Partnerships Act, 2012 | LLPs have separate legal personality; General Partnerships do not |

| Members | Partners (no universal cap; LLPs require minimum 2) | General Partnerships have no statutory maximum; LLPs must file a partnership agreement |

| Local Presence | Registered office address in Kenya required | Must be maintained throughout the life of the partnership |

| Capital | No statutory minimum; denominated in KES | Contributions defined by the partnership agreement |

| Privacy | Partnership agreements filed with the Registrar of Companies | Certain details become part of the public record |

Focus Points

- Taxation: Partnerships are generally taxed at the partner level at the individual or corporate rate applicable to each partner; LLPs may attract corporate income tax treatment depending on structure; VAT registration applies if turnover exceeds the KES 5 million threshold; withholding tax applies on applicable payments to partners.

- Annual Compliance: Annual returns must be filed with the Registrar of Companies; changes to partners or the partnership agreement require formal notification.

- Restrictions: Foreign nationals may face restrictions on certain regulated activities; professional LLPs are typically limited to licensed practitioners in the relevant field.

- Conversion: A general partnership may convert to an LLP under the Partnerships Act, 2012 through a formal registration process with the Registrar.

Sub-Types

General Partnership

All partners bear unlimited joint and several liability for the firm's obligations. This structure is common among small trading businesses and professional practices where partners prefer minimal formality.

Limited Partnership

One or more general partners carry unlimited liability, while limited partners are liable only to the extent of their capital contribution. Limited partners may not participate in management without losing their limited liability protection.

Limited Liability Partnership (LLP)

The LLP grants all partners limited liability and operates as a separate legal entity. It is the preferred structure for professional service firms, including law and accountancy practices, where liability ring-fencing alongside operational flexibility is required.

Recommendations

Partnerships suit professional services firms, joint ventures, and situations where pass-through taxation or shared management is preferred; the LLP form offers liability protection without the formality of a corporate board structure, though the public filing of partnership agreements reduces confidentiality compared to some other structures.

LLPs are best suited for licensed professionals and multi-partner service businesses seeking liability protection without full corporate governance obligations.

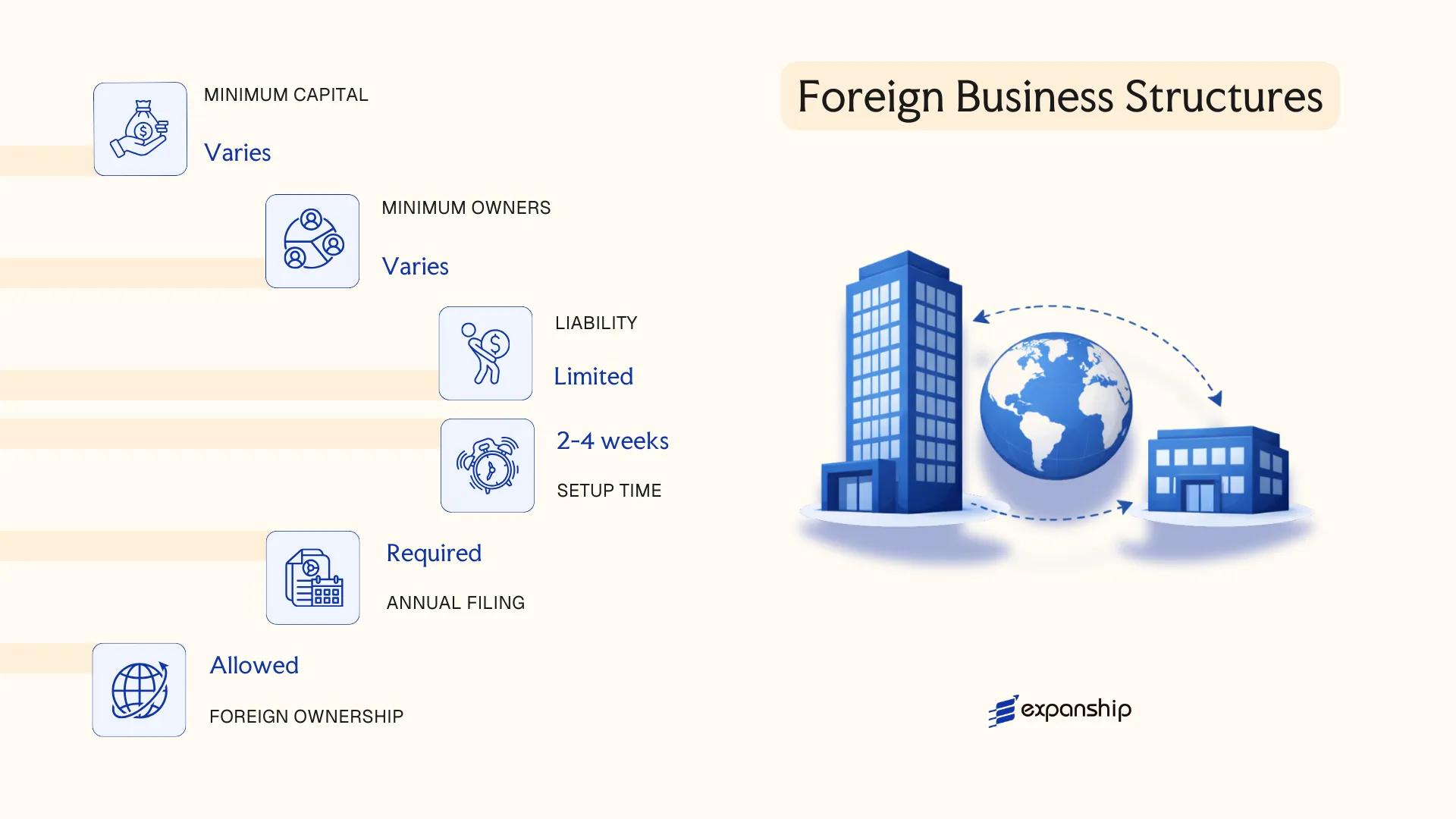

Foreign Business Structures [Branch Office, Representative Office, Subsidiary]

Registering a foreign company branch office in Kenya is governed by Part XXVII of the Companies Act, 2015, which requires foreign entities conducting business within the country to register with the Registrar of Companies. A branch does not constitute a separate legal entity — it remains an extension of the parent company, which bears full liability for the branch's obligations.

| Requirement | Branch Office | Representative Office | Subsidiary |

|---|---|---|---|

| Legal Form | Extension of foreign parent | Liaison office only | Separate legal entity (Private Ltd) |

| Liability | Parent bears full liability | Parent bears full liability | Limited to subsidiary's assets |

| Local Representative | Mandatory local agent | Mandatory local agent | Local director required |

| Registered Office | Required in Kenya | Required in Kenya | Required in Kenya |

| Minimum Capital | No statutory minimum | No statutory minimum | No statutory minimum (KES recommended) |

| Privacy | Parent financials may be disclosed | Limited disclosure | Subsidiary financials filed separately |

Focus Points

- Taxation: Branch profits subject to corporate income tax at 30%; withholding tax applies to remittances to the parent; VAT registration required if turnover thresholds are met.

- Economic Substance: No specific economic substance regime modelled on offshore frameworks, but tax residency rules under the Income Tax Act may determine where profits are assessed.

- Annual Compliance: Branches must file annual returns and audited accounts with the Registrar; failure attracts penalties under the Companies Act, 2015.

- Treaty Access: Kenya has double tax treaties with several countries; a branch may access treaty benefits depending on the parent's jurisdiction and treaty provisions.

- Restrictions: Representative offices are prohibited from generating revenue or entering commercial contracts directly.

Sub-Types

Branch Office

A branch operates under the parent company's name and legal identity, registered under Part XXVII of the Companies Act, 2015. It suits foreign firms seeking operational presence without establishing a locally incorporated entity.

Representative Office

This structure is restricted to promotional, market research, and liaison activities — it cannot engage in revenue-generating transactions. Foreign firms typically use it to test market conditions before committing to full incorporation.

Subsidiary

A subsidiary is incorporated as a Private Limited Company under Kenyan law, making it a distinct legal entity from its foreign parent. This structure offers liability insulation and is generally preferred for full commercial operations.

Closing

Foreign firms requiring full commercial activity with liability separation typically opt for a subsidiary, while those preferring operational simplicity and consolidated reporting lean toward a branch. The key limitation of a branch is the parent's unlimited exposure to Kenyan liabilities.

Foreign companies with established operations seeking market entry in East Africa, where legal separation from the parent is a priority, are best served by incorporating a subsidiary under the Companies Act, 2015.

Cooperative Society

Cooperative society registration Kenya falls under the Co-operative Societies Act (Cap. 490), which governs the formation, registration, and dissolution of these entities. A cooperative society holds a separate legal personality upon registration and confers limited liability on its members, making it a hybrid structure that combines commercial activity with collective ownership principles.

Registration is administered by the Commissioner for Co-operative Development under the State Department for Co-operatives. Members pool resources toward a shared economic purpose, and governance follows the one-member-one-vote principle regardless of individual capital contribution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate with separate legal personality | Registered under Cap. 490 |

| Members | Referred to as members; minimum 10 individuals or 2 registered cooperatives | No statutory maximum for membership |

| Local Presence | Registered office within Kenya required | Must be accessible to the Commissioner |

| Capital | No prescribed minimum share capital; contributions defined in by-laws | Shares are non-transferable to non-members |

| Privacy | Member register held internally; not fully public | Subject to inspection by the Commissioner |

Focus Points

- Taxation: Subject to corporate income tax at 30%; qualifies for certain exemptions on surplus distributions to members under Kenya Revenue Authority guidelines; standard VAT and withholding tax obligations apply.

- Annual Compliance: Must file audited accounts and an annual return with the Commissioner for Co-operative Development.

- Restrictions: Membership is limited to persons with a defined common bond; shares cannot be freely transferred outside the membership.

- Conversion: Conversion to another entity type requires dissolution and fresh incorporation; no direct conversion mechanism exists under Cap. 490.

Sub-Types

Savings and Credit Cooperative (SACCO)

SACCOs are the most prevalent cooperative variant, regulated additionally by the SACCO Societies Regulatory Authority (SASRA) under the SACCO Societies Act, 2008. Deposit-taking SACCOs require a SASRA licence, which imposes additional capital and governance requirements beyond Cap. 490.

Agricultural Cooperative

Formed specifically for production, processing, or marketing of agricultural produce, these cooperatives often access government-facilitated credit lines and commodity programmes not available to general cooperatives.

Consumer Cooperative

Organised to procure goods or services collectively for members at reduced cost, consumer cooperatives operate primarily in retail and housing sectors.

Closing

A cooperative society suits businesses or communities pursuing collective economic objectives, particularly in agriculture, finance, or housing, though the common-bond membership requirement limits its use as a general commercial vehicle.

Groups with a shared economic interest — particularly farmer collectives, employee savings groups, or housing associations — seeking a democratic ownership structure.

Sole Proprietorship

Sole proprietorship registration Kenya is governed by the Registration of Business Names Act (Cap. 499), which requires any individual trading under a name other than their own to register that name with the Registrar of Business Names. This structure carries no separate legal personality — the business and its owner are legally the same, meaning personal assets are exposed to all business liabilities.

Registration is processed through eCitizen, Kenya's government digital services portal, and is administered by the Business Registration Service (BRS). The process is straightforward and relatively low-cost compared to incorporating a limited company.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Members | Single proprietor | One individual only; no co-owners permitted |

| Liability | Unlimited personal liability | Owner's personal assets are at full risk |

| Local Presence | Physical address required | Must maintain a registered business address in Kenya |

| Capital | No minimum capital requirement | Owner funds the business directly |

| Privacy | Business name is publicly registered | Owner's details filed with BRS |

Focus Points

- Taxation: Subject to personal income tax under the Income Tax Act (Cap. 470) at graduated rates up to 35%; VAT registration is mandatory once annual turnover exceeds KES 5 million; no corporate tax applies.

- Annual Compliance: Business name renewal is required periodically with the BRS; no annual returns filing equivalent to that of a limited company.

- Conversion: Can be converted into a private limited company by incorporating a new entity and transferring business assets; no direct conversion mechanism exists under Cap. 499.

- Restrictions: Cannot issue shares, raise equity from investors, or enter contracts in a business capacity distinct from the owner.

Closing

A sole proprietorship suits individuals operating small-scale, low-risk service or retail businesses who require minimal administrative overhead. The primary advantage is ease of setup; the significant drawback is unlimited personal liability, which leaves the owner fully exposed to business debts and legal claims.

Local sole traders testing a business concept or operating independently at a small scale, with no immediate need for external investment or liability protection.

How to Choose the Right Entity Type in Kenya

Choosing the right business structure in Kenya determines your tax exposure, liability, regulatory obligations, and operational capacity — before you earn a single shilling.

Why Your Entity Choice Matters

The structure you register has binding legal consequences that are difficult and costly to reverse.

- Registering a foreign branch to conduct local trade without complying with the Companies Act, 2015 can result in penalties or deregistration by the Registrar of Companies.

- Forming a company limited by guarantee when your business generates taxable profit misaligns your structure with your obligations, since that form is intended for non-profit purposes.

- Selecting a sole proprietorship for a multi-investor business creates personal liability exposure that a private limited company would otherwise contain.

- Choosing a structure that mandates audited financial statements for a single-director consultancy adds recurring compliance costs that may not reflect the firm's scale or risk profile.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors such as banking or insurance each require distinct registration pathways under Kenyan law.

- Ownership Structure: A sole operator has different governance needs than a multi-party arrangement requiring a defined shareholding and board structure.

- Tax Position: Your eligibility for specific tax treatments under the Income Tax Act depends on the entity type you register.

- Liability Exposure: Unincorporated structures do not separate personal assets from business debts.

- Substance Capacity: If you cannot maintain a physical presence, some entity types carry higher compliance risk than others.

- Exit Planning: Not all structures permit straightforward conversion, redomiciliation, or voluntary winding-up under Kenyan company law.

Compliance Services for Companies in Kenya

Maintain good standing with the Registrar of Companies and meet your ongoing statutory obligations under Kenyan law.

Conclusion

Kenya company incorporation summary points to a single dominant structure: the private limited company (Ltd) accounts for the substantial majority of new registrations processed through the Business Registration Service (BRS) each year. It suits resident entrepreneurs, foreign investors, and subsidiaries of multinational groups alike, given its liability protection and relatively straightforward compliance obligations under the Companies Act, 2015.

Each other structure fills a defined role. The public limited company fits firms seeking capital from public markets. A company limited by guarantee serves membership-based or non-profit organisations. Partnerships and LLPs suit professional service providers. Branch offices and representative offices give foreign firms a foothold without separate incorporation. Cooperative societies remain the structure of choice for collective economic activity.

Regulatory oversight continues to evolve, with the BRS expanding digital registration infrastructure and Kenya's bilateral investment treaty network broadening gradually. For businesses weighing entity selection, professional guidance on current BRS procedures and compliance timelines remains relevant before committing to a structure.

How Expanship Can Assist You

Expanship provides corporate services and company formation in Kenya across the full range of structures covered in this guide — from private limited companies registered under the Companies Act 2015 to limited liability partnerships and branch offices. Your filing is handled directly with the Business Registration Service (BRS) under the Attorney General's office, with no steps outsourced to third parties unfamiliar with your specific situation.

Depending on your entity type and operational requirements, our Kenya incorporation services include:

- Preparation and notarization of incorporation documents

- Registered office and local agent provision

- Filing and liaison with the Business Registration Service

- Post-incorporation compliance management, including annual returns

- KRA PIN registration and tax compliance setup

- Banking introduction assistance with local and international institutions

Reach out to Expanship Kenya to discuss your specific structure and timeline.

Frequently Asked Questions (FAQ)

The private limited company (Ltd) is the most frequently incorporated entity. Its combination of limited liability, a single-member minimum, and eligibility for most commercial activities makes it the default choice for both resident and foreign entrepreneurs.

A branch is a direct extension of its foreign parent and holds no separate legal personality, while a private limited company is an independent legal entity under the Companies Act, 2015. Tax treatment also diverges: branches are taxed only on Kenyan-sourced income, whereas a locally incorporated subsidiary is subject to resident corporate tax on its worldwide income.

A company limited by guarantee does not have shareholders, so no share register is exposed publicly. Nominee directorship arrangements are available for private limited companies, though beneficial ownership disclosure requirements under the Business Registration Service Act apply.

A sole proprietorship and a private limited company can each be formed by one individual. Partnerships, by definition under the Partnership Act, require at least two partners, and a cooperative society requires a minimum of ten members.

Foreigners may incorporate a private limited company, register a branch, or establish a subsidiary without restriction, provided they comply with sector-specific licensing where applicable. Certain regulated sectors, such as media and land ownership, impose foreign participation limits regardless of the chosen structure.

The Companies Act, 2015 permits re-registration between certain categories, including conversion from a private to a public limited company and vice versa. Conversion from an incorporated company to a partnership or cooperative is not directly provided for under the same statute and would require dissolution and fresh registration.

No. Sole proprietorships, general partnerships, and branch offices do not constitute separate legal persons from their owners or parent entities. Private limited companies, public limited companies, companies limited by guarantee, limited liability partnerships, and cooperative societies each hold distinct legal personality under their respective governing statutes.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.