Key Takeaways

- Jordan's primary registration authority is the Companies Control Department (CCD), operating under the Ministry of Industry, Trade and Supply, which maintains the commercial register for all legal entities in the country.

- The Limited Liability Company is the most commonly registered structure in Jordan, making it the default choice for small to mid-size ventures seeking a balance of flexibility and limited liability.

- Foreign companies entering Jordan can operate through a Branch Office without establishing a separate legal entity, or through a Representative Office restricted to non-commercial activities.

- All Jordanian business structures are governed primarily by Companies Law No. 22 of 1997 and its subsequent amendments, which continue to evolve in alignment with international standards.

Introduction to Entity Types in Jordan

Jordan is a sovereign nation in the Middle East, bordered by Saudi Arabia, Iraq, Syria, Israel, and the Palestinian territories. Business registration falls under the jurisdiction of the Companies Control Department (CCD), which operates within the Ministry of Industry, Trade and Supply and maintains the official commercial register for all legal entities incorporated in the country.

The tax system is territorial in orientation, with corporate income tax applying to locally sourced profits at rates that vary by sector.

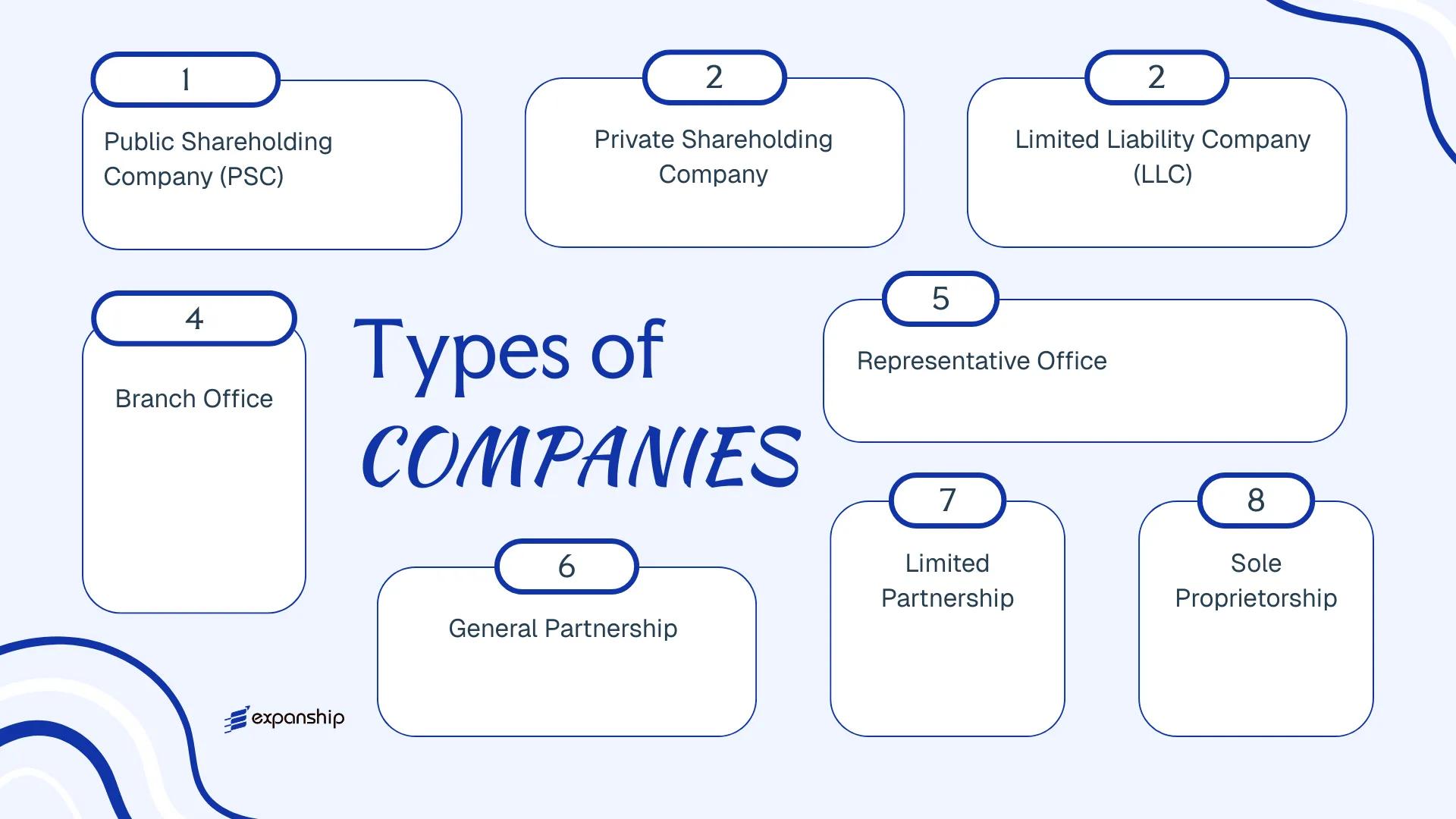

Entities available under Jordanian law include the Public Shareholding Company, Private Shareholding Company, Limited Liability Company, General Partnership, Limited Partnership, Branch Office, Representative Office, and Sole Proprietorship. Each structure carries distinct requirements around minimum capital, liability, ownership, and permitted activities — all governed primarily by the Companies Law No. 22 of 1997 and its subsequent amendments.

This article examines each of these Jordanian legal entity structures in detail, covering formation requirements, ownership rules, and the practical considerations relevant to your business registration decision.

An Overview of Business Structures in Jordan

Jordanian company law recognises several distinct entity types, each governed primarily by the Companies Law No. 22 of 1997 and its subsequent amendments. The Ministry of Industry, Trade and Supply, through the Companies Control Department, serves as the principal registration authority for most commercial entities. Each structure carries different implications for liability, ownership, and permitted activities.

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Shareholding Company | Corporate entity | Limited to shares | Taxable | Permitted | 3 founders | Companies Control Department | Companies Law No. 22/1997 |

| Private Shareholding Company | Corporate entity | Limited to shares | Taxable | Permitted | 2 shareholders | Companies Control Department | Companies Law No. 22/1997 |

| Limited Liability Company | Corporate entity | Limited to capital | Taxable | Permitted | 2 shareholders | Companies Control Department | Companies Law No. 22/1997 |

| Branch Office | Extension of parent | Parent liable | Taxable | Permitted | N/A | Companies Control Department | Companies Law No. 22/1997 |

| Representative Office | Non-trading entity | Parent liable | Generally exempt | Not permitted | N/A | Companies Control Department | Companies Law No. 22/1997 |

| General Partnership | Unincorporated firm | Unlimited | Taxable | Permitted | 2 partners | Companies Control Department | Companies Law No. 22/1997 |

| Limited Partnership | Unincorporated firm | Mixed liability | Taxable | Permitted | 2 partners | Companies Control Department | Companies Law No. 22/1997 |

| Sole Proprietorship | Individual business | Unlimited | Taxable | Permitted | 1 owner | Ministry of Industry, Trade and Supply | Companies Law No. 22/1997 |

Each of these structures is examined in full in the sections below.

Public Shareholding Company (PSC)

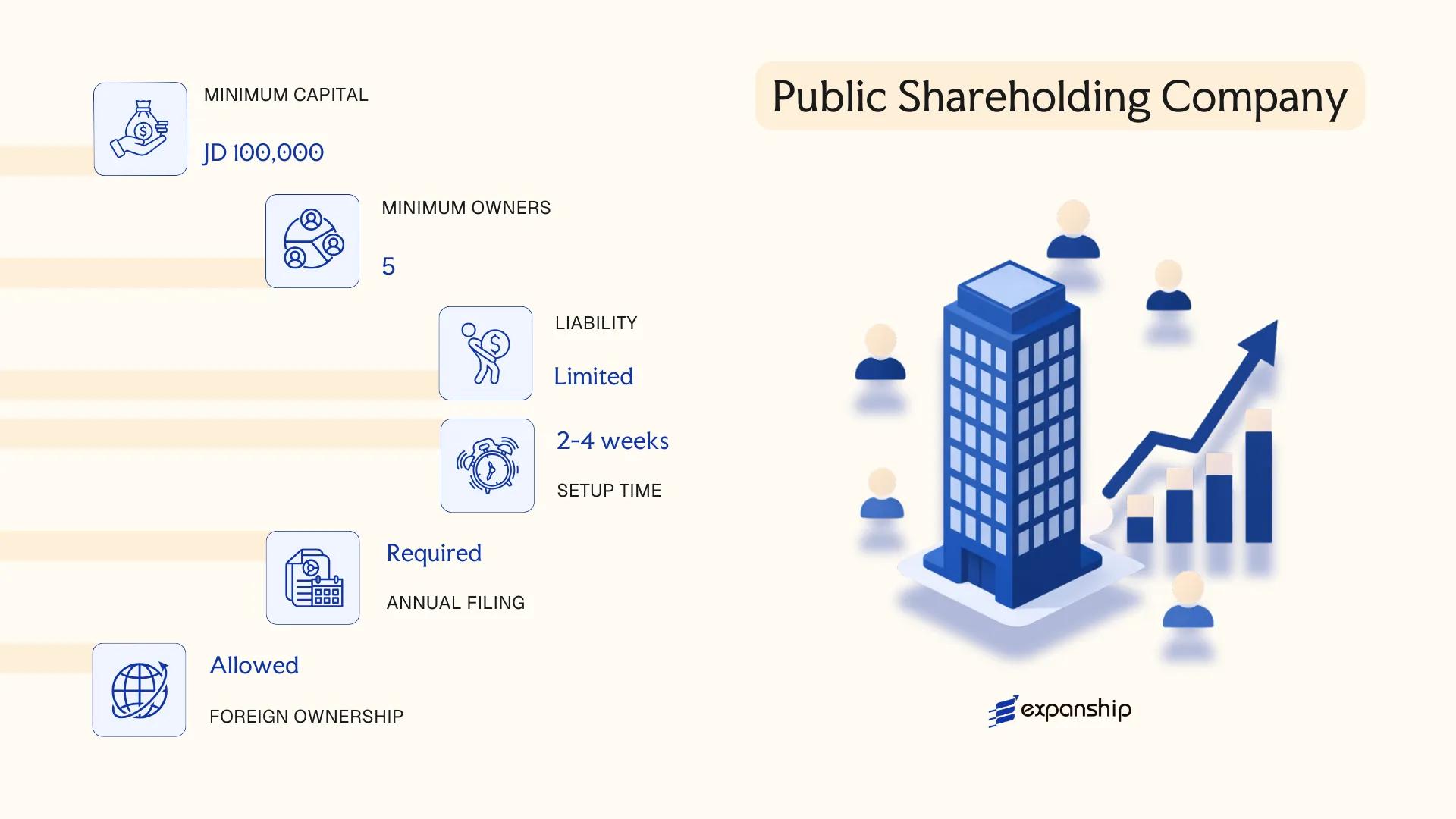

A Jordan Public Shareholding Company PSC is governed by the Companies Law No. 22 of 1997 and its subsequent amendments, administered by the Companies Control Department (CCD) under the Ministry of Industry, Trade and Supply. The entity carries a separate legal personality, meaning its obligations are distinct from those of its shareholders, who bear liability only to the extent of their paid-up share capital.

Shares in a PSC may be offered to the public and listed on the Amman Stock Exchange (ASE), making this structure the standard vehicle for large-scale commercial and financial enterprises. Listing is subject to oversight by the Jordan Securities Commission (JSC).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Shareholding Company | Separate legal personality; shares are transferable and may be publicly traded |

| Members | Shareholders; minimum 3 founders at incorporation | No maximum shareholder limit; shares divided into equal nominal values |

| Management | Board of Directors (minimum 3, maximum 13 members) | Board elected by shareholders; a general assembly must convene annually |

| Local Presence | Registered office in Jordan required | Physical address mandatory; no statutory requirement for a local agent |

| Capital | Minimum JOD 500,000 (paid-up); sector-specific minimums may apply | Banking, insurance, and financial institutions face higher thresholds set by sector regulators |

| Privacy | Shareholder register is publicly accessible via the CCD | Listed companies have additional disclosure obligations under JSC rules |

Focus Points

- Taxation: Corporate income tax applies at rates varying by sector (generally 20%, with banks and financial institutions taxed at higher rates); VAT at 16% applies to taxable supplies; dividend distributions to non-residents may attract withholding tax subject to applicable double tax treaties — see the Jordan Income and Sales Tax Department for current rates.

- Annual Compliance: Audited financial statements must be filed annually with the CCD; listed PSCs have additional continuous disclosure obligations to the JSC.

- Treaty Access: Jordan maintains an active network of double taxation agreements, and a PSC qualifies as a resident entity for treaty purposes.

- Conversion: A PSC may be converted to a private shareholding company or LLC subject to CCD approval and shareholder resolution, provided the resulting entity meets minimum capital requirements.

- Restrictions: Foreign ownership is permitted in most sectors, though certain industries impose ownership caps under the Investment Environment Law.

Closing

A PSC suits large enterprises seeking public capital markets access, joint ventures with broad investor bases, or operations in regulated sectors such as banking and insurance. The structure's access to public equity is its primary structural advantage; the corresponding burden of continuous regulatory disclosure and higher minimum capital requirements makes it unsuitable for most small or mid-sized businesses.

A PSC is best suited for large enterprises in regulated industries or those planning to raise capital through a public listing on the Amman Stock Exchange.

Company Incorporation in Jordan

Incorporate your business entity in Jordan with support across entity selection, registration, and compliance setup.

Private Shareholding Company

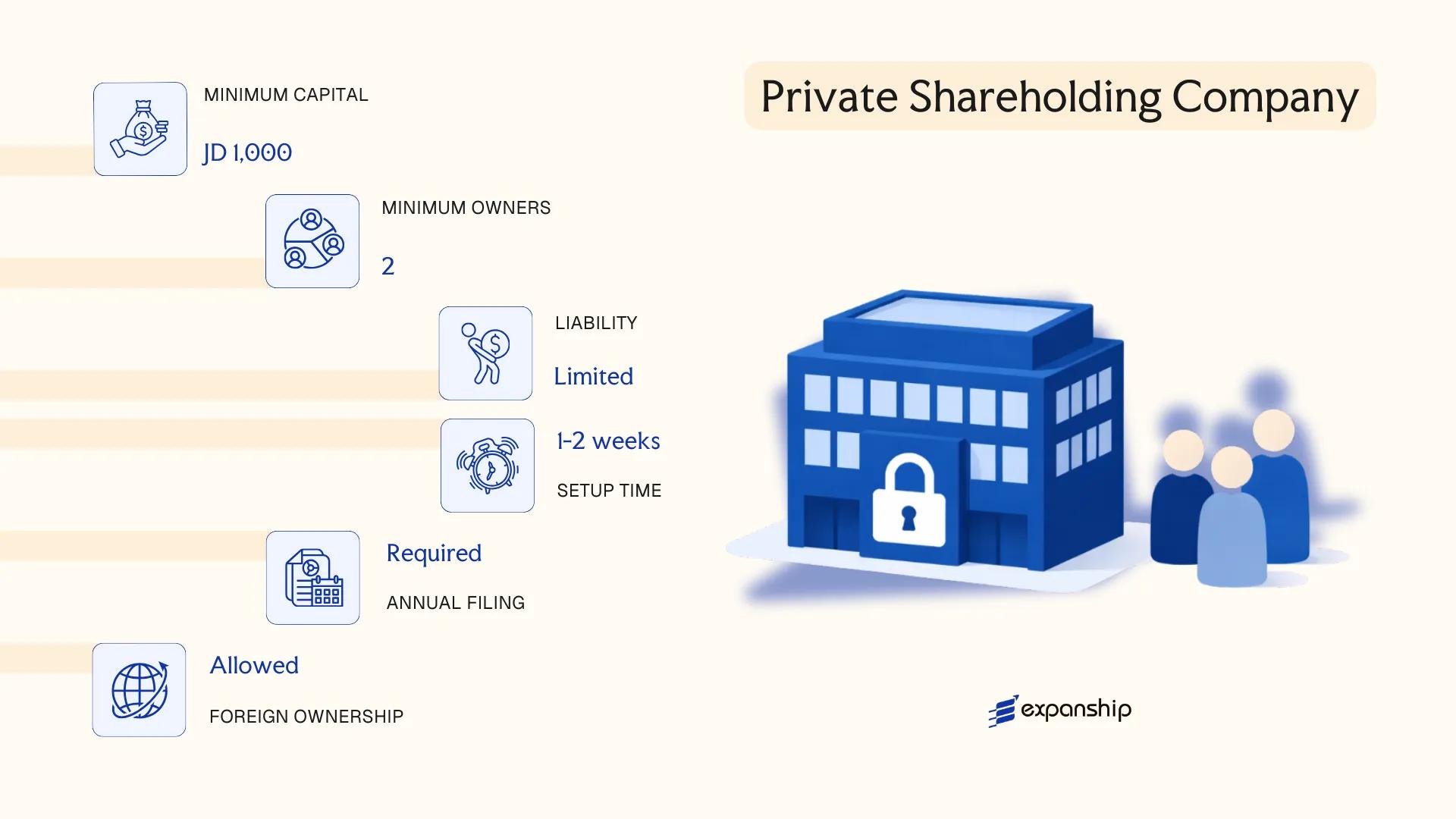

Jordan Private Shareholding Company formation is governed by the Companies Law No. 22 of 1997 and its subsequent amendments, administered by the Companies Control Department (CCD) under the Ministry of Industry, Trade and Supply. Known locally as a closed joint stock company, this structure carries a separate legal personality distinct from its shareholders, with liability limited to each member's capital contribution.

The entity occupies a middle ground between the fully public shareholding company and the more flexible limited liability company. Shares are not offered to the public and cannot be traded on the Amman Stock Exchange, making this structure suited to closely held ownership arrangements where control remains within a defined group.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Closed Joint Stock Company (Private Shareholding) | Separate legal personality; governed by Companies Law No. 22 of 1997 |

| Members | Shareholders; minimum 2, maximum 50 | Directors appointed separately; board of directors required |

| Capital | Minimum JOD 50,000 | Must be fully subscribed at incorporation; denominated in Jordanian Dinar |

| Local Presence | Registered address in Jordan required | Physical office address; no mandatory local director requirement |

| Share Transfer | Restricted; subject to shareholder approval or articles provisions | Shares cannot be publicly offered or listed |

| Privacy | Shareholder register maintained with CCD | Register is not fully public but accessible to regulatory authorities |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate (varies by sector, generally 20% for most industries); VAT applies at 16% on taxable supplies; withholding tax applies to dividends, interest, and royalties paid to non-residents at rates governed by applicable double taxation treaties.

- Annual Compliance: Audited financial statements must be filed annually with the CCD; a board of directors meeting and general assembly are required each year.

- Treaty Access: As a Jordanian-resident entity, qualifies for Jordan's network of double taxation treaties.

- Economic Substance: No formal economic substance regime equivalent to Gulf jurisdictions, though genuine operational presence is expected.

- Conversion: Can be converted to a public shareholding company if statutory thresholds for capital and shareholders are met under the Companies Law.

Closing

This structure suits mid-sized privately held operating businesses, family-owned enterprises, and joint ventures requiring formal governance without public market exposure. The defined share transfer restrictions provide ownership stability, though the minimum capital requirement and mandatory audit obligations add to the cost of maintenance.

Closely held businesses and joint ventures requiring formal corporate governance, limited liability, and treaty access without public listing obligations.

Limited Liability Company (LLC)

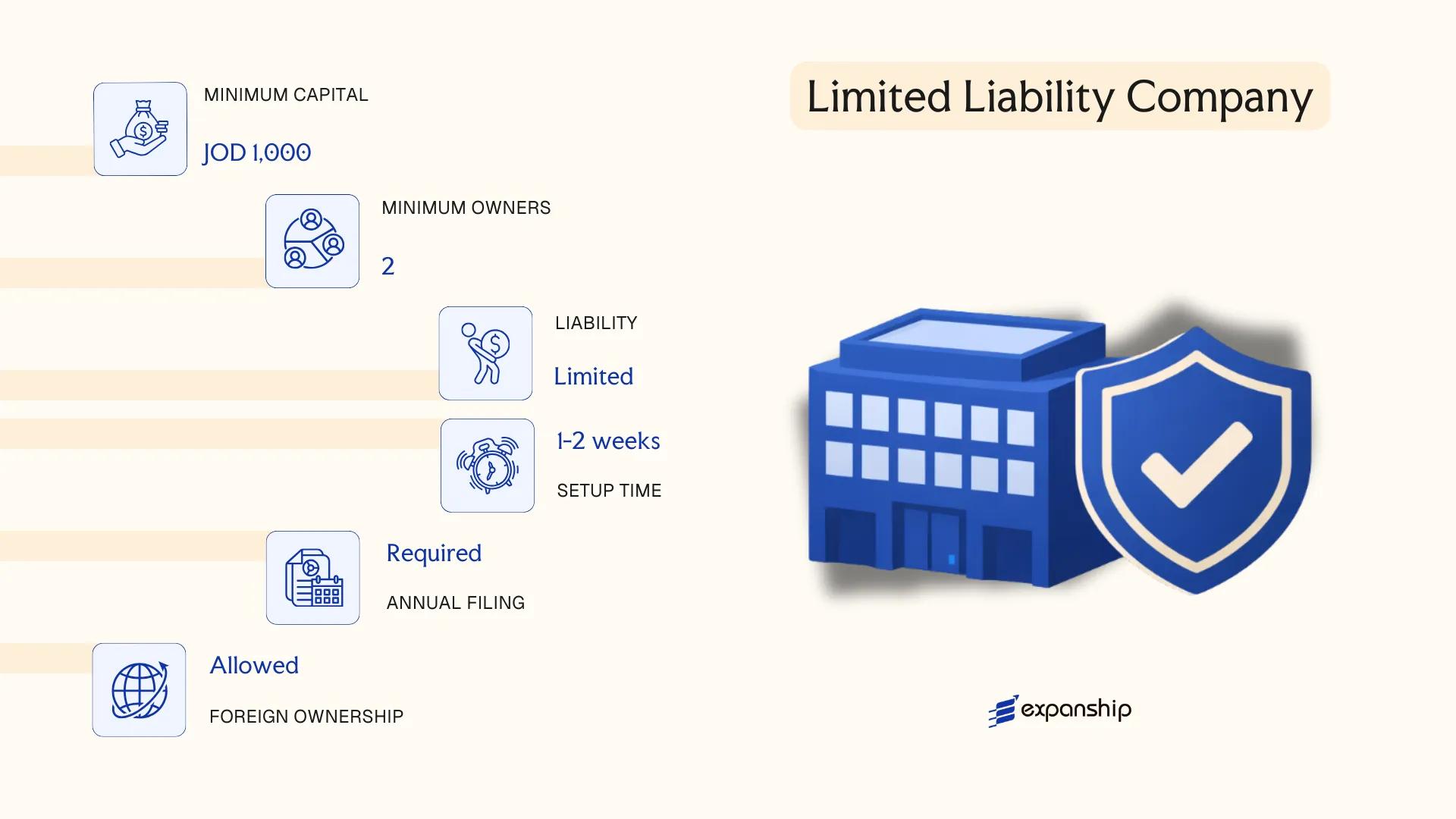

The LLC is the most widely used business structure for foreign investors and local entrepreneurs alike, governed by the Companies Law No. 22 of 1997 and its subsequent amendments. Jordan LLC registration requirements are administered by the Companies Control Department (CCD) under the Ministry of Industry, Trade and Supply, which serves as the primary regulatory authority for incorporation and ongoing compliance.

As a separate legal entity, the LLC shields its members from personal liability beyond their subscribed capital contributions. This hybrid character — combining elements of a partnership in internal management with corporate liability protections — makes it a practical vehicle for a broad range of commercial activities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (LLC) | Holds separate legal personality under Companies Law No. 22 of 1997 |

| Members | 2–50 members (shareholders) | Single-member LLCs are not permitted; exceeding 50 members triggers mandatory conversion to a shareholding company |

| Management | One or more managers appointed by members | Managers need not be members; a board of directors is not required |

| Local Presence | Registered office address in Jordan required | A physical or c/o address within the Kingdom; no mandatory local agent unless sector-specific licensing requires one |

| Capital | Minimum JOD 1,000 (approx. USD 1,400) for most activities | Certain regulated sectors (banking, insurance, financial services) impose higher statutory minimums |

| Foreign Ownership | Up to 100% foreign ownership permitted in most sectors | Restricted or prohibited in sectors listed under the Investment Law No. 30 of 2014 |

| Privacy | Member names filed with CCD; register is publicly accessible | No bearer shares permitted |

Focus Points

- Taxation: Subject to corporate income tax at a flat rate of 20% for most sectors (higher rates apply to banking, insurance, and telecoms); VAT applies at a standard rate of 16%; withholding tax applies to dividends, royalties, and certain service payments to non-residents at rates typically between 10%–14%.

- Annual Compliance: Annual financial statements must be filed with the CCD; entities exceeding statutory thresholds are required to have accounts externally audited.

- Economic Substance: Jordan does not currently impose OECD-style economic substance rules, though sector-specific regulators may impose operational presence requirements independently.

- Treaty Access: Jordan maintains a network of double taxation agreements; LLCs resident in Jordan are generally eligible to claim treaty benefits, subject to beneficial ownership conditions.

- Conversion: An LLC that exceeds 50 members must convert to a Public or Private Shareholding Company under the Companies Law.

Closing

The LLC suits trading operations, professional services firms, joint ventures, and wholly owned foreign subsidiaries conducting active business within the Kingdom. Its straightforward formation process and low Jordan LLC minimum capital make entry accessible, though the 50-member ceiling limits its utility for businesses planning broad equity distribution or future public fundraising.

Foreign investors and SMEs seeking a commercially active presence with full liability protection and without the administrative burden of a shareholding structure.

Foreign Company Structures in Jordan [Branch Office, Representative Office]

A foreign company branch office Jordan registration is governed primarily by the Companies Law No. 22 of 1997 and its subsequent amendments, administered by the Companies Control Department (CCD) under the Ministry of Industry, Trade and Supply. A branch office does not constitute a separate legal entity — it remains an extension of the parent company, which bears full legal and financial liability for its activities in Jordan.

Registration of a representative office follows the same legislative framework, though its operational scope is strictly limited by regulation.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent (no separate legal personality) | Extension of foreign parent (no separate legal personality) |

| Authorized Signatory | Appointed local manager (must be named in registration) | Appointed local representative |

| Local Presence | Registered office address in Jordan required | Registered office address in Jordan required |

| Minimum Capital | No statutory minimum, but parent's capital may be scrutinized | No statutory minimum |

| Commercial Activity | Permitted (revenue-generating operations allowed) | Not permitted — limited to liaison, market research, promotion |

| Privacy | Parent company details disclosed in CCD filings | Parent company details disclosed in CCD filings |

Focus Points

- Taxation: Branch profits are subject to the standard corporate income tax rate (currently 20% for most sectors); VAT at 16% applies to taxable supplies; withholding tax applies to remittances of profits to the foreign parent; no separate stamp duty regime specific to branches.

- Treaty Access: Jordan's double taxation agreements may apply to branch income, but eligibility depends on the parent entity's residency and treaty terms.

- Annual Compliance: Branches must file audited financial statements with the CCD annually and renew their registration; representative offices face similar renewal obligations.

- Restrictions: A representative office cannot invoice clients, sign commercial contracts, or generate local revenue; violation risks deregistration.

- Conversion: A branch can be converted to a locally incorporated entity, such as an LLC, though this requires a separate incorporation process rather than a direct structural conversion.

Sub-Types

Branch Office

A branch office is authorized to conduct the same commercial activities as its parent company within Jordan, subject to CCD approval. It is commonly used by foreign firms seeking to operate directly in the local market without establishing a separate subsidiary.

Representative Office

A representative office is restricted to non-commercial functions — promotional activities, market research, and liaison work on behalf of the parent. It cannot enter into contracts or generate revenue, making it unsuitable for active trading operations.

Closing

Both structures are used by foreign businesses that require a physical presence without committing to full local incorporation, with the branch office suited to revenue-generating activity and the representative office serving only preparatory or promotional purposes. The principal limitation of both structures is the absence of liability separation — the foreign parent assumes all legal obligations arising from local operations.

A branch office is most appropriate for established foreign companies seeking direct market entry in Jordan; a representative office suits those in early-stage market assessment only.

Partnership Structures in Jordan [General Partnership, Limited Partnership]

Governing general partnership registration Jordan falls under the Companies Law No. 22 of 1997, as amended, which recognises two distinct partnership forms: the general partnership (sharikat tadamun) and the limited partnership (sharikat tawsiya basita). Both structures carry separate legal personality upon registration with the Companies Control Department (CCD) under the Ministry of Industry, Trade and Supply.

Unlike corporate entities, partnership liability is not uniformly capped. In a general partnership, all partners bear joint and unlimited personal liability for the firm's obligations, while the Jordan limited partnership structure introduces a split between general and limited partners, the latter being liable only to the extent of their capital contribution.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Form | Separate legal personality; not a corporate entity | Separate legal personality; hybrid structure |

| Members | Partners (minimum 2, no statutory maximum); all bear unlimited liability | Minimum 1 general partner (unlimited liability) + 1 limited partner (capped liability) |

| Local Presence | Registered office in Jordan required; no mandatory local agent | Registered office in Jordan required |

| Capital | No statutory minimum; contributions in cash or kind | No statutory minimum; limited partner's liability capped at contributed capital |

| Privacy | Partner names disclosed in the trade name and registration records | General partner names publicly disclosed; limited partner details on record |

Focus Points

- Taxation: Partnerships are generally treated as pass-through entities for income tax purposes under the Income Tax Law, though partners' shares of profit may attract personal income tax; VAT registration is required if annual turnover exceeds the statutory threshold.

- Annual Compliance: Audited financial statements and annual renewal filings must be submitted to the CCD.

- Conversion: A partnership may be converted to a limited liability company or shareholding company, subject to CCD approval and restructuring of liability.

- Restrictions: Foreign nationals face ownership restrictions in certain regulated sectors regardless of partnership form.

- Treaty Access: Access to Jordan's double tax treaty network depends on the tax residency status of the individual partners, not the partnership itself.

Sub-Types

General Partnership (Sharikat Tadamun)

All partners manage the business and carry unlimited joint liability. This structure is used primarily by small professional or family-run businesses where all principals are active in operations.

Limited Partnership (Sharikat Tawsiya Basita)

At least one general partner manages the firm and bears unlimited liability, while one or more limited partners contribute capital without participating in management. This Jordanian partnership company formation model suits investors seeking passive exposure without operational involvement.

When to Consider a Partnership Structure

Partnership structures in Jordan are most suited to small-scale trading, professional services, or family businesses where principals seek a straightforward formation process without minimum capital requirements. The absence of a capital floor is a practical advantage, though unlimited liability exposure for general partners remains a significant structural risk.

General and limited partnerships are most appropriate for closely-held family businesses or small professional firms where all partners are known to one another and capital requirements are minimal.

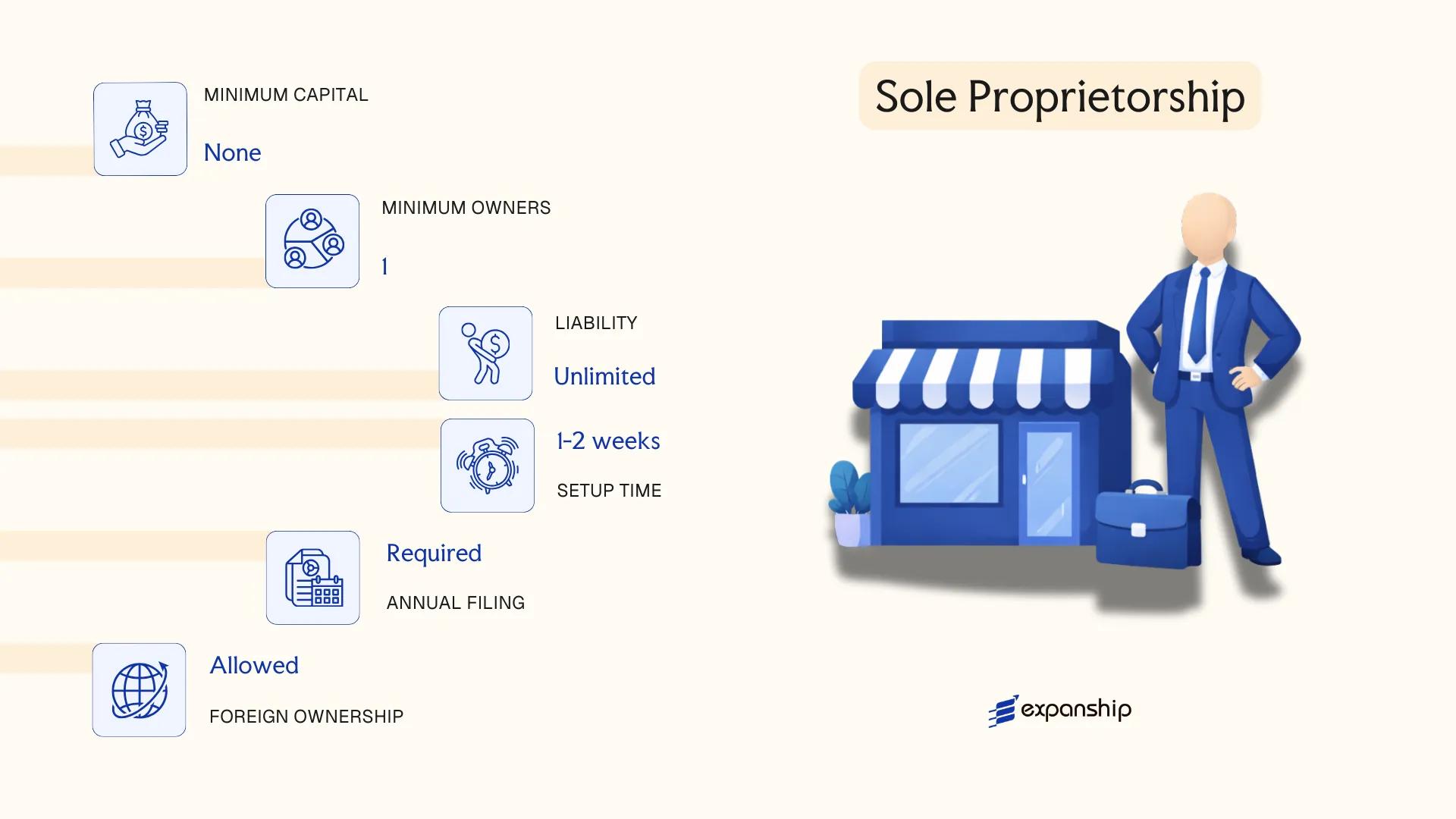

Sole Proprietorship

Sole proprietorship Jordan registration falls under the Companies Law No. 22 of 1997 and its subsequent amendments, alongside the provisions administered by the Ministry of Industry and Trade. Unlike corporate structures, a sole proprietorship does not constitute a separate legal entity from its owner — the proprietor bears unlimited personal liability for all business obligations.

Registration is processed through the Companies Control Department or the relevant local authority depending on the nature of the activity. The business operates under the proprietor's name or a registered trade name, and the owner retains full control over decision-making without the governance requirements that apply to multi-member structures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated individual business | No separate legal personality from the owner |

| Member Type | Sole Proprietor | One natural person only; no minimum capital threshold prescribed for most activities |

| Local Presence | Registered business address in Jordan | Physical or virtual office acceptable depending on activity type |

| Capital | Jordanian Dinar (JOD); no statutory minimum for most activities | Certain licensed activities may require sector-specific capital |

| Liability | Unlimited personal liability | Owner's personal assets are exposed to business debts |

| Privacy | Proprietor's name linked to the registration record | Trade name registration possible to operate under a distinct name |

Focus Points

- Taxation: Subject to personal income tax on business profits under the Income Tax Law; VAT registration required if annual turnover exceeds the prescribed threshold; no corporate tax applies as the entity is not a separate legal person.

- Annual Compliance: Annual tax filing with the Income Tax Department is required; bookkeeping obligations apply based on turnover levels.

- Restrictions: Foreign nationals are generally not permitted to register a sole proprietorship without meeting specific residency or investment conditions under Jordanian investment regulations.

- Conversion: Can be converted into a limited liability company or other corporate form through a formal registration process with the Companies Control Department.

- Treaty Access: As an unincorporated structure, access to double tax treaty benefits available to corporate entities does not apply.

A sole proprietorship suits individual service providers, freelancers, and small traders operating within Jordan who require a straightforward registration with minimal administrative overhead. The primary advantage is the simplicity and low cost of setup, while the defining limitation is unlimited personal liability, which exposes the owner's personal assets to all business debts.

This structure is best suited for Jordanian nationals or eligible residents operating a single-owner, low-risk service or trade business with limited external liability exposure.

How to Choose the Right Entity Type in Jordan

Choosing the right company type in Jordan is not a formality — the structure you register determines your tax exposure, liability, operational permissions, and regulatory obligations from day one.

Why Your Entity Choice Matters

- A branch office cannot enter contracts in its own name under Jordanian law; structuring a trading operation through one when a Limited Liability Company is required can result in contractual disputes and regulatory action by the Companies Control Department.

- Registering a representative office when you intend to generate local revenue violates its permitted scope, which is restricted to promotional and liaison activities only.

- Selecting a structure without considering Jordan's income tax obligations means you may be liable for corporate tax without the treaty protections available only to appropriately registered resident entities.

- Forming a general partnership exposes all partners to unlimited personal liability — a material risk where the business operates in a sector with significant commercial exposure.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as banking or insurance, and passive asset-holding each point to distinct structures under the Companies Law No. 22 of 1997 and its amendments.

- Ownership Structure: A single founder points toward an LLC or sole proprietorship, while multi-party investment with governance requirements points toward a Private or Public Shareholding Company.

- Tax Position: Your need for treaty access, exemptions, or eligibility under the Investment Environment Law affects which entity qualifies.

- Liability Exposure: Whether personal asset protection is required determines whether a limited liability structure is necessary.

- Operational Scope: Foreign entities must assess whether a branch or a locally incorporated subsidiary better fits their intended activities and ongoing compliance capacity.

- Exit Flexibility: Not all Jordanian entity types permit straightforward conversion or redomiciliation; confirm winding-up procedures before registering.

Corporate Compliance Services in Jordan

Ongoing compliance support for companies registered in Jordan, including annual filings, regulatory reporting, and Companies Control Department requirements.

Conclusion

Selecting the right structure is the first substantive decision in any Jordan company incorporation conclusion guide — and the choice has lasting implications for liability, taxation, and operational flexibility under Jordanian law. Registered with the Companies Control Department, each entity serves a distinct profile. The LLC suits small to mid-size ventures and remains the most commonly registered structure in Jordan. Private Shareholding Companies fit founder-led businesses anticipating equity rounds, while the Public Shareholding Company applies to firms pursuing public capital markets. Branch offices suit foreign companies testing the market without establishing a separate legal entity, and representative offices are limited to non-commercial activity.

Regulatory reform through the Companies Law No. 22 of 1997 and its successive amendments signals an ongoing effort to align local frameworks with international standards. Your choice of entity will also intersect with Jordan's expanding tax treaty network, which continues to grow.

How Expanship Can Assist You

Expanship provides corporate services company incorporation Jordan businesses rely on across every major entity type — from Limited Liability Companies registered under the Companies Law No. 22 of 1997 to Public and Private Shareholding Companies. Our team works directly with the Companies Control Department (CCD) at the Ministry of Industry, Trade and Supply to manage your registration from start to finish.

From initial document preparation through to ongoing compliance, our Jordan business registration services cover each stage of your setup:

- Document preparation, notarization, and legalization

- Registered agent and local office provision

- Government filings and CCD liaison

- Post-incorporation compliance management

- Banking introduction assistance

Every engagement is handled by specialists familiar with Jordan's regulatory requirements, not generalists working from a template.

Reach out to Expanship Jordan to discuss your specific incorporation needs.

Frequently Asked Questions (FAQ)

The Limited Liability Company (LLC) is the most frequently registered entity under the Companies Law No. 22 of 1997. Its combination of limited liability protection, a relatively low minimum capital threshold, and suitability for both local and foreign-owned operations makes it the default choice for small to mid-sized businesses.

A Branch Office operates as an extension of its parent company, meaning the foreign entity bears direct legal liability for the branch's activities in Jordan. An LLC, by contrast, is a separate legal person registered under Jordanian law with its own capital structure and liability shield. Compliance obligations for a Branch include annual reporting to the Companies Control Department and are generally tied to the parent's financials.

Among registered structures, the Private Shareholding Company permits share transfers without public disclosure of beneficial ownership changes in most circumstances. Nominee arrangements are permissible under Jordanian law but must comply with anti-money laundering regulations enforced by the Companies Control Department. Director and shareholder details are recorded in the commercial register, though full beneficial ownership disclosure requirements have been expanding under recent regulatory reforms.

No. A sole proprietorship and a Representative Office can each be established by one individual or parent entity, but an LLC requires a minimum of two shareholders under the Companies Law. General Partnerships require at least two partners, and Public Shareholding Companies require a minimum of three founders.

Foreigners may establish LLCs, Private Shareholding Companies, and Public Shareholding Companies, subject to sector-specific foreign ownership restrictions governed by the Investment Environment Law No. 30 of 2014 and relevant Jordanian Investment Commission regulations. Branch and Representative Offices are also available to foreign companies already incorporated abroad. Certain regulated sectors, including media and land ownership, impose additional nationality-based restrictions.

Conversion between entity types is recognized under the Companies Law, most commonly from an LLC to a Private or Public Shareholding Company as a business scales. The process requires approval from the Companies Control Department and involves updating the commercial registration and articles of association. Not all conversion directions are equally straightforward, and some may require meeting new minimum capital requirements.

LLCs, Private Shareholding Companies, and Public Shareholding Companies each hold distinct legal personality separate from their shareholders. General Partnerships and Sole Proprietorships do not create a separate legal person, meaning the individual partners or proprietor remain personally liable for business obligations. Branch Offices also lack independent legal personality, as they are extensions of the foreign parent.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.