Key Takeaways

- The Companies Office of Jamaica administers all entity registrations under the Companies Act, 2004, which governs the full range of available business structures in the country.

- Jamaica's private company limited by shares is the most widely used incorporation vehicle, valued for combining liability protection with operational flexibility.

- Structures such as the company limited by guarantee and the unlimited company serve specialized purposes — non-profit or membership organizations in the former case, and arrangements involving full member liability in the latter.

- Jamaica's territorial-based tax system means resident companies are generally taxed only on Jamaica-sourced income, a factor that directly influences entity selection decisions for foreign investors.

Introduction to Entity Types in Jamaica

Jamaica is an island nation in the Caribbean Sea, situated south of Cuba and west of Hispaniola. An independent state within the Commonwealth, it operates under a Westminster-style parliamentary system and maintains a legal framework rooted in English common law.

Company formation and ongoing compliance fall under the authority of the Companies Office of Jamaica, the statutory body responsible for registering and regulating business entities. The country applies a territorial-based tax system, meaning resident companies are generally taxed on Jamaica-sourced income.

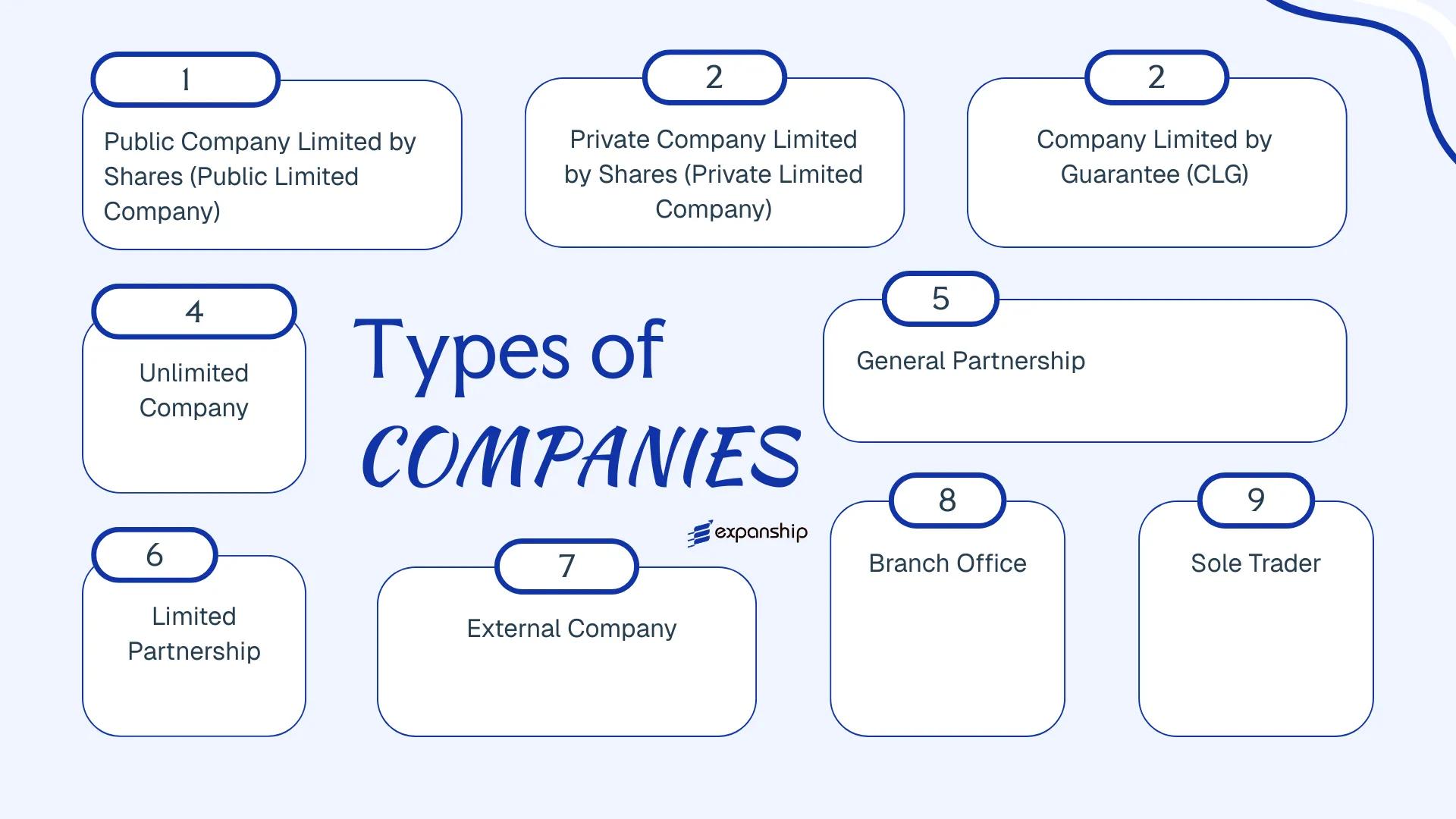

The types of business entities in Jamaica span several distinct legal structures, each governed primarily by the Companies Act of 2004. Available options include:

- Public Company Limited by Shares

- Private Company Limited by Shares

- Company Limited by Guarantee

- Unlimited Company

- General Partnership

- Limited Partnership

- External Company (Branch)

- Sole Trader

Each structure carries different requirements around liability, ownership, governance, and reporting obligations. This article examines each option in detail, covering what distinguishes one form from another and what registration entails under Jamaican law.

An Overview of Business Structures in Jamaica

Jamaican company law recognises several distinct entity types, each governed primarily by the Companies Act of 2004 and administered by the Companies Office of Jamaica (COJ). The business structures available in Jamaica range from incorporated companies to unincorporated arrangements, each designed to serve a different commercial purpose. The sections below examine each in full detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company Limited by Shares | Incorporated | Limited to shares | Taxed | Yes | 7 shareholders | COJ | Companies Act 2004 |

| Private Company Limited by Shares | Incorporated | Limited to shares | Taxed | Yes | 1 shareholder | COJ | Companies Act 2004 |

| Company Limited by Guarantee | Incorporated | Limited to guarantee | Taxed / Exempt | Yes | 1 member | COJ | Companies Act 2004 |

| Unlimited Company | Incorporated | Unlimited | Taxed | Yes | 1 shareholder | COJ | Companies Act 2004 |

| General Partnership | Unincorporated | Unlimited | Taxed | Yes | 2 partners | COJ | Partnership Act |

| Limited Partnership | Unincorporated | Mixed | Taxed | Yes | 2 partners | COJ | Partnership Act |

| External Company | Registered foreign entity | Per home jurisdiction | Taxed | Yes | N/A | COJ | Companies Act 2004 |

| Branch Office | Registered foreign entity | Per parent entity | Taxed | Yes | N/A | COJ | Companies Act 2004 |

| Sole Trader | Unincorporated | Unlimited | Taxed | Yes | 1 person | COJ | Registration of Business Names Act |

Each of these structures is examined in full in the sections below.

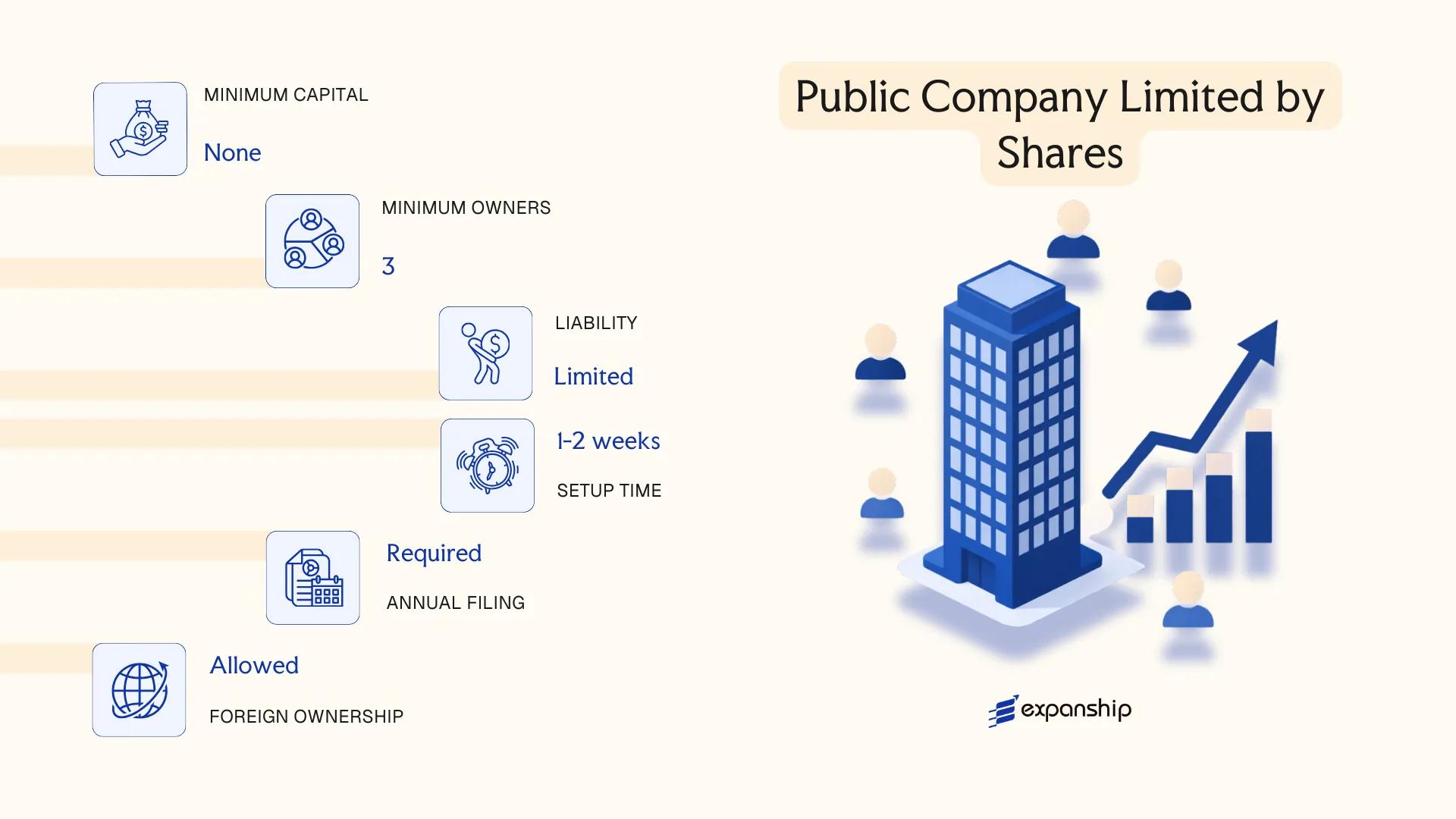

Public Company Limited by Shares

A Jamaica public company limited by shares is incorporated under the Companies Act 2004, administered by the Companies Office of Jamaica (COJ). It carries separate legal personality, meaning the entity exists independently of its shareholders, whose liability is capped at the value of their unpaid shares.

Structured for broader capital access, this form is the standard vehicle for businesses seeking public investment through stock exchange listings or widespread share issuance.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Company Limited by Shares | Incorporated under the Companies Act 2004 |

| Members | Shareholders; minimum 1 director, minimum 7 shareholders | No upper limit on shareholders; shares may be offered to the public |

| Local Presence | Registered office in Jamaica required | Must maintain a physical address on record with the COJ |

| Capital | Denominated in Jamaican Dollars (JMD); no statutory minimum | Authorised and issued share capital disclosed publicly |

| Public Disclosure | Annual returns, financial statements, and shareholder register filed with COJ | Financial statements must be audited |

| Privacy | Low | Shareholder and director information is publicly accessible via the COJ registry |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate of 25% (33⅓% where applicable to regulated sectors); GCT (General Consumption Tax) applies to taxable supplies; withholding tax applies to dividends, interest, and royalties paid to non-residents; transfer tax and stamp duty apply to share transfers.

- Annual Compliance: Must hold an Annual General Meeting (AGM), file audited financial statements, and submit annual returns to the COJ.

- Stock Exchange Listing: Listing on the Jamaica Stock Exchange (JSE) triggers additional disclosure, governance, and continuing obligations under JSE rules.

- Treaty Access: Jamaica maintains double taxation agreements with several jurisdictions, which may reduce withholding tax rates on cross-border payments.

- Conversion: A public company may be re-registered as a private company under the Companies Act 2004, subject to meeting the relevant conditions and shareholder approval.

Closing

This structure suits large trading operations, financial institutions, and businesses raising capital from the public. The primary advantage is unrestricted share issuance to the public; the offsetting drawback is the significant ongoing compliance burden, including mandatory audits and public disclosure requirements.

Established businesses or institutions seeking public capital investment, particularly those with a realistic path to a Jamaica Stock Exchange listing.

Company Incorporation in Jamaica

Incorporate a public or private company in Jamaica with support from Expanship's corporate services team.

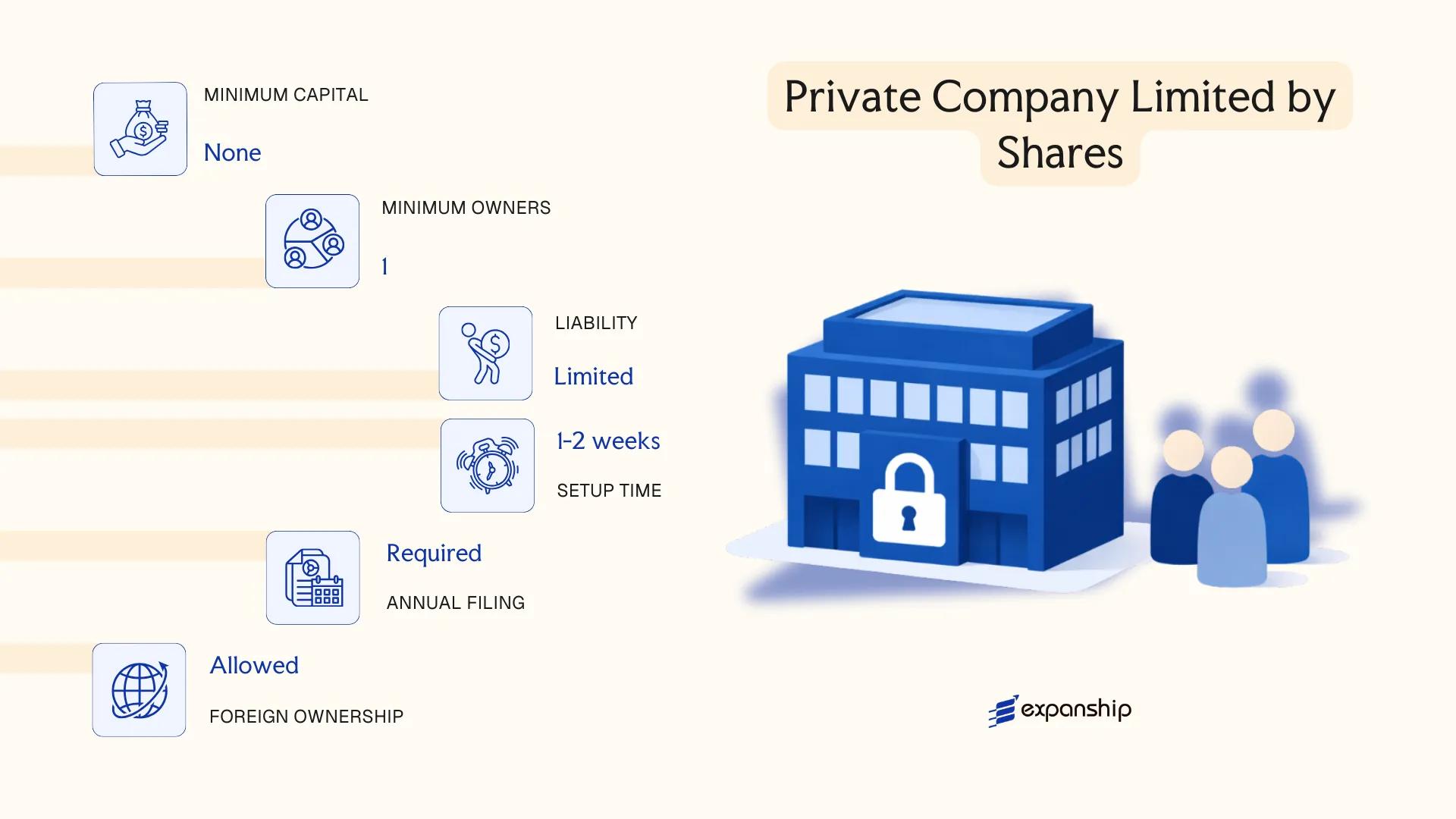

Private Company Limited by Shares

A Jamaica private company limited by shares is governed by the Companies Act 2004, administered by the Companies Office of Jamaica (COJ). The entity holds a legal personality separate from its shareholders, meaning it can own property, enter contracts, and incur liabilities in its own name. Shareholder liability is capped at the amount unpaid on their shares.

Restrictions on share transfers and a prohibition on public subscription of shares distinguish this structure from its public counterpart. For most foreign investors and domestic entrepreneurs, private limited company Jamaica formation through the COJ is the standard entry point for commercial activity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Incorporated under the Companies Act 2004 |

| Members | Shareholders: min. 1, max. 50 | Excludes employees who hold shares |

| Directors | Min. 1 director required | No mandatory residency requirement for directors |

| Local Presence | Registered office in Jamaica required | Must be a physical address on record with the COJ |

| Share Capital | Denominated in JMD or foreign currency; no statutory minimum | Par value or no-par-value shares permitted |

| Privacy | Shareholder register is publicly accessible at the COJ | Director details are also filed on public record |

Focus Points

- Taxation: Subject to corporate income tax at 25% (33.33% for regulated entities); liable for GCT (General Consumption Tax) at 15% if turnover exceeds the registration threshold; withholding tax applies to dividends, interest, and royalties paid to non-residents at rates that may be reduced under applicable tax treaties.

- Annual Compliance: Annual returns must be filed with the COJ; audited financial statements are generally required unless a specific exemption applies.

- Treaty Access: Jamaica maintains double taxation agreements with several jurisdictions, including the UK, US, Canada, and CARICOM member states, which may reduce withholding tax rates on cross-border payments.

- Conversion: A private company may re-register as a public company under the Companies Act 2004 by satisfying the requisite statutory conditions and shareholder approval.

- Restrictions: Shares cannot be offered to the public, and any transfer of shares is subject to the restrictions set out in the company's articles of incorporation.

Closing

A private company limited by shares suits trading operations, holding structures, and businesses seeking a defined liability boundary without the disclosure obligations of a listed entity. The single-shareholder option offers structural flexibility, though the public accessibility of the shareholder register may be a consideration for those with privacy requirements.

This structure is best suited for foreign investors, joint venture partners, and domestic businesses seeking a scalable, liability-protected entity for active commercial or holding operations in Jamaica.

Company Limited by Guarantee

A company limited by guarantee Jamaica operates under the Companies Act of 2004, administered by the Companies Office of Jamaica (COJ). Unlike a company limited by shares, this structure has no share capital. Instead, members undertake to contribute a nominal sum to the entity's assets in the event of winding up.

Commonly used by non-profit organisations, charities, professional associations, and educational bodies, the entity holds separate legal personality and members benefit from limited liability. Their financial exposure is capped at the amount stated in the memorandum of association.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by guarantee | Incorporated under the Companies Act, 2004 |

| Members | Referred to as members; minimum 1, no statutory maximum | No shareholders; members hold no ownership interest in assets |

| Governance | Minimum 1 director | Directors manage operations; a company secretary is required |

| Local Presence | Registered office address in Jamaica required | Must be maintained at all times with the COJ |

| Capital | No share capital; members' guarantee typically JMD 1–100 | Guarantee amount is stated in the memorandum |

| Privacy | Director and member details filed with COJ | Register is publicly accessible |

Focus Points

- Taxation: Exempt from income tax if registered as a charitable or non-profit organisation with Tax Administration Jamaica (TAJ); otherwise standard corporate income tax at 25% (unregulated) or 33.33% (regulated) applies; GCT (Jamaica's VAT) exemptions may apply depending on activities.

- Annual Compliance: Annual returns and audited financial statements must be filed with the COJ; charities registered under the Charities Act, 2013 face additional reporting to the Charities Commission of Jamaica.

- Restrictions: Cannot distribute profits or assets to members; any surplus must be applied toward the stated objects of the organisation.

- Conversion: Conversion to a company limited by shares is not a standard procedure; dissolution and re-incorporation is the typical path if restructuring is required.

- Treaty Access: No access to Jamaica's tax treaty network in a meaningful sense, as income tax exemption typically removes treaty relevance for qualifying non-profits.

Closing

This structure suits non-profit organisations, industry regulators, alumni associations, and foundations that require legal personality without distributing profits to members. The principal limitation is the prohibition on profit distribution, which makes this structure unsuitable for any commercial venture.

Best suited for charities, professional bodies, and non-governmental organisations that require formal legal standing under Jamaican law without a commercial profit objective.

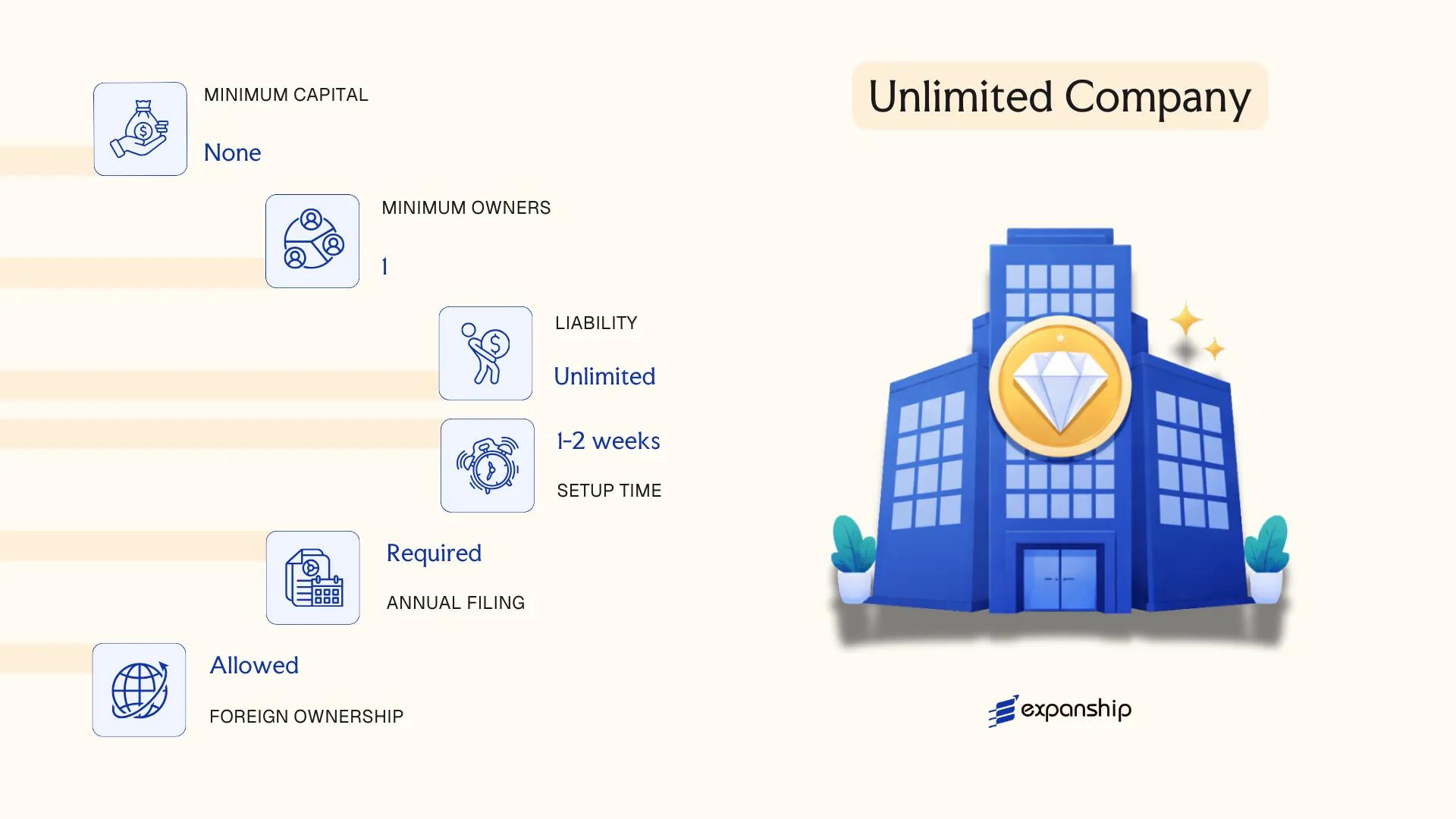

Unlimited Company

Unlimited company Jamaica registration is governed by the Companies Act 2004, administered by the Companies Office of Jamaica (COJ). Like other registered companies under the Act, an unlimited company holds a separate legal personality distinct from its members — but unlike limited structures, members bear personal liability for the company's debts without any cap.

This structure is relatively uncommon in practice. The absence of liability protection makes it unsuitable for most commercial activities, yet it retains certain structural flexibilities — particularly around capital distribution — that can attract specific use cases.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unlimited company with separate legal personality | Registered under the Companies Act 2004 |

| Members | Shareholders; minimum 1, no statutory maximum | Members bear unlimited personal liability for company debts |

| Local Presence | Registered office in Jamaica required | Must maintain a physical address on record with the COJ |

| Capital | No minimum share capital; denominated in Jamaican Dollars (JMD) | Can issue and return capital more freely than limited companies |

| Privacy | Director and shareholder details filed with COJ | Public register; limited privacy on beneficial ownership |

Focus Points

- Taxation: Subject to standard corporate income tax at 25% (33.33% for regulated entities); GCT, withholding tax, and transfer tax obligations apply on the same basis as other registered companies.

- Annual Compliance: Must file annual returns with the COJ and maintain statutory registers; same filing obligations as limited companies.

- Conversion: Can be converted to a limited company under the Companies Act 2004, subject to COJ approval and re-registration procedures.

- Treaty Access: Qualifies for Jamaica's tax treaty network on the same basis as other resident companies, subject to substance requirements.

- Restrictions: No liability shield for members; personal assets of shareholders are exposed to creditors if the company cannot meet its obligations.

Closing

Unlimited companies are occasionally used in professional services or intra-group holding arrangements where capital flexibility outweighs liability concerns, though the unrestricted personal exposure of members remains a significant structural drawback.

This entity suits scenarios where the members are corporate entities that can absorb liability risk and where unrestricted capital return is a priority over personal asset protection.

Partnerships [General Partnership, Limited Partnership]

Under the Partnership Act and the Limited Partnerships Act, both general and limited partnership Jamaica structures operate as contractual arrangements between two or more persons carrying on business with a view to profit. A general partnership does not have separate legal personality, meaning partners bear joint and unlimited liability for the firm's debts. A limited partnership introduces a two-tier structure: at least one general partner retains unlimited liability, while limited partners are liable only to the extent of their contributed capital.

Registration is handled through the Companies Office of Jamaica (COJ). General partnerships register under the Registration of Business Names Act, whereas limited partnership registration in Jamaica requires filing a declaration with the COJ under the Limited Partnerships Act.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Form | Unincorporated; no separate legal personality | Unincorporated; no separate legal personality |

| Members | Partners (min. 2, no statutory maximum) | Min. 1 general partner + 1 limited partner |

| Local Presence | Registered business address in Jamaica | Registered business address in Jamaica |

| Capital | No minimum; contributions in any agreed form | No minimum; limited partner's liability capped at contribution |

| Management | All partners may participate | Only general partners manage; limited partners may not control |

| Privacy | Partner names filed on public register at COJ | Declaration of limited partners filed publicly at COJ |

Focus Points

- Taxation: Partnerships are fiscally transparent; profits are taxed in the hands of individual partners at the personal income tax rate of 25% (or 30% above the threshold); no entity-level corporate income tax applies, though partners remain subject to GCT obligations where applicable.

- Annual Compliance: Partnerships must maintain a current business name registration and file renewals with the COJ; limited partnerships must update their declaration upon any material change in partners or contributions.

- Treaty Access: As pass-through entities without separate legal personality, partnerships do not directly access Jamaica's double taxation treaties; treaty benefits, where available, apply at the partner level depending on each partner's residence.

- Restrictions: Limited partners who participate in management risk losing their limited liability status and being treated as general partners under the Limited Partnerships Act.

- Conversion: No direct statutory conversion mechanism exists from a partnership to a company; restructuring requires forming a new entity and transferring assets.

Sub-Types

General Partnership

All partners share management authority and carry unlimited, joint liability. This structure is common among professional services firms such as legal or accounting practices where shared control is operationally necessary.

Limited Partnership

One or more general partners manage the business and bear full liability, while limited partners contribute capital and remain passive. This structure is used in fund arrangements and joint ventures where investors seek liability protection without operational involvement.

A partnership structure suits joint ventures, professional practices, and investment arrangements where pass-through taxation is preferred and at least one participant is willing to bear management responsibility. The absence of a minimum capital requirement offers flexibility, but unlimited personal liability for general partners represents a material exposure that incorporated structures avoid.

Partnerships in Jamaica are most appropriate for small professional firms or two-party joint ventures where the participants are known to one another, liability exposure is manageable, and corporate formalities are not required.

Foreign Business Structures [External Company, Branch Office]

Registering a foreign company in Jamaica is governed by the Companies Act 2004, which classifies any overseas body corporate conducting business in the jurisdiction as an External Company. The entity does not gain separate Jamaican legal personality through this registration; it remains an extension of the parent company, meaning the parent retains full liability for the branch's obligations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch of a foreign corporation | No separate legal personality in Jamaica |

| Local Representative | Registered agent plus at least one local representative | Must be ordinarily resident in Jamaica |

| Registered Office | Physical address required | Cannot be a P.O. Box |

| Capital | No minimum prescribed | Parent company's capital structure applies |

| Filing Obligations | Certified constitutional documents, list of directors, and financial statements | Documents must be filed with the Companies Office of Jamaica (COJ) |

| Privacy | Director details and constitutional documents are on public record | Parent company financials may be subject to disclosure |

Focus Points

- Taxation: The branch's Jamaican-sourced income is subject to corporate income tax at the standard rate; branch profits remitted abroad may attract withholding tax, and GCT (General Consumption Tax) applies to taxable supplies.

- Economic Substance: No specific substance regime currently mirrors Cayman or BVI frameworks, but commercial substance is relevant for transfer pricing purposes.

- Annual Compliance: Annual returns and updated financial statements must be filed with the COJ; failure to maintain filings can result in deregistration.

- Treaty Access: As an extension of the parent, treaty benefits depend on the parent's jurisdiction and the applicable double taxation agreement Jamaica has in force.

- Restrictions: Certain regulated sectors, including banking and insurance, require separate licensing regardless of branch status.

Closing

A branch office suits foreign firms testing the Jamaican market or executing specific contracts without committing to a locally incorporated subsidiary. The primary advantage is avoiding a separate incorporation process; the key drawback is unlimited parental liability for all local obligations.

Established foreign corporations seeking a direct operational presence for project-based or sector-specific activity, where creating a separate legal entity is not yet commercially justified.

Sole Trader

Sole trader registration in Jamaica is governed by the Registration of Business Names Act, which requires any individual trading under a name other than their own legal name to register that business name with the Companies Office of Jamaica (COJ). No separate legal entity is created — you and the business are legally the same person, meaning personal assets are fully exposed to business liabilities.

Registration is straightforward. The COJ processes business name registrations for sole traders, and the certificate issued is valid for a defined period before renewal is required.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Member Type | Sole Proprietor | One individual only; no co-ownership permitted under this structure |

| Local Presence | Registered business address | No statutory agent requirement, but a local address must be provided to the COJ |

| Capital | No minimum capital requirement | Funding is personal; no share capital structure exists |

| Privacy | Business name and owner details are publicly registered | Filed records are accessible via the COJ |

Focus Points

- Taxation: Business income is taxed as personal income under the Income Tax Act; you are subject to Pay As You Earn (PAYE) or self-assessment, General Consumption Tax (GCT) registration is required once turnover crosses the statutory threshold, and no separate corporate tax applies.

- Annual Compliance: Business name registration must be renewed periodically with the COJ; failure to renew can result in deregistration.

- Treaty Access: As an unincorporated individual, you do not benefit from Jamaica's tax treaties in a business capacity the way a company would.

- Conversion: A sole trader can transition to a limited company by incorporating separately and transferring business assets, though no automatic conversion mechanism exists.

- Restrictions: You cannot raise equity capital or admit partners without restructuring into a different business form.

Closing

A sole trader structure suits individuals running small, low-risk operations who want minimal administrative overhead and direct control over their business affairs. The main advantage is simplicity of setup; the principal drawback is unlimited personal liability for all business debts and obligations.

Freelancers, consultants, and small-scale traders operating in Jamaica who do not require liability protection or outside investment.

How to Choose the Right Entity Type in Jamaica

Knowing how to choose a business entity in Jamaica requires more than comparing registration fees — the structure you select has direct legal, tax, and operational consequences that compound over time.

Why Your Entity Choice Matters

- Registering as an external company while conducting substantive local trade without the correct registration under the Companies Act can result in penalties or striking off by the Companies Office of Jamaica.

- Choosing a structure that does not qualify under Jamaica's tax treaties means you cannot access reduced withholding tax rates available to qualifying residents or entities.

- Forming a limited company when your purpose is asset protection or estate planning locks your structure into annual shareholder obligations, director filings, and statutory meetings that would not apply under a trust arrangement.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each fall under different statutory frameworks and require distinct entity forms.

- Ownership Structure: A sole trader or general partnership suits single-owner or small multi-party operations, while a private limited company provides clearer separation of ownership and management.

- Tax Position: Your eligibility for specific relief under the Income Tax Act depends on entity type and residency status.

- Liability Exposure: Unlimited companies and general partnerships expose members to personal liability, which may be unsuitable depending on the risk profile of your operations.

- Exit and Continuity: Not all structures permit straightforward conversion or redomiciliation, so your anticipated exit route should factor into the initial decision.

Company Compliance Services in Jamaica

Maintain good standing with the Companies Office of Jamaica — annual returns, statutory filings, and ongoing compliance support.

Conclusion

Each entity structure registered under the Companies Act, 2004 and administered by the Companies Office of Jamaica serves a distinct purpose. The private company limited by shares remains the most commonly incorporated form, favored for its liability protection and operational flexibility. Public companies suit businesses seeking capital from external investors; companies limited by guarantee serve non-profit and membership-based organizations. Unlimited companies accommodate arrangements where members accept full liability exposure. General and limited partnerships apply where profit-sharing between individuals or firms is the organizing principle, while a sole trader structure suits single-person operations without formal registration requirements beyond the business name.

Your choice of structure affects tax treatment, reporting obligations, and how the entity is perceived by counterparties and regulators. Ongoing reforms to Jamaica's corporate registry processes and the country's expanding treaty network continue to shape how foreign investors approach local registration decisions. Professional guidance at the entity selection stage reduces downstream compliance friction.

How Expanship Can Assist You

Expanship's company formation services in Jamaica cover the full registration process, from selecting the right structure under the Companies Act to filing with the Companies Office of Jamaica. Whether you are establishing a private company limited by shares, a limited partnership, or registering as an external company, our team coordinates each step with the relevant authority on your behalf.

From document preparation to post-incorporation obligations, our Jamaica business incorporation assistance includes:

- Memorandum and Articles of Association preparation

- Government filing and Companies Office of Jamaica liaison

- Registered agent and registered office provision

- Ongoing annual return and compliance management

- Document legalization and apostille support

- Banking introduction assistance

Reach out to Expanship Jamaica to discuss how we can support your entry into the Jamaican market.

Frequently Asked Questions (FAQ)

The private company limited by shares is the most frequently incorporated structure. Its combination of limited liability, a single-shareholder minimum, and no public share offering requirements makes it accessible for a wide range of commercial purposes.

A private company restricts share transfers and cannot offer securities to the public, whereas a public company may list on the Jamaica Stock Exchange and solicit public investment. Public companies carry substantially heavier disclosure and audit obligations under the Companies Act 2004.

The private company limited by shares discloses less publicly than a public company, though director and shareholder details are filed with the COJ. Nominee director and shareholder arrangements are legally permissible and can reduce the visibility of beneficial ownership in public records.

A sole trader requires only one individual by definition, and a private company can be formed by a single shareholder and one director. General partnerships and limited partnerships each require at least two partners, so a sole individual cannot form those structures.

All principal structures — private and public companies, companies limited by guarantee, unlimited companies, partnerships, and registration as an external company — are accessible to foreign nationals. Non-residents face no nationality-based ownership restrictions under the Companies Act 2004, though certain regulated sectors require additional licensing regardless of entity type.

The Companies Act 2004 provides mechanisms for re-registration, allowing a private company to convert to a public company and vice versa upon meeting the relevant statutory criteria. Conversion between fundamentally different structures — such as from a partnership to a limited company — generally requires dissolving the original entity and incorporating a new one.

Companies incorporated under the Companies Act 2004 — whether limited by shares, limited by guarantee, or unlimited — hold separate legal personality distinct from their members. Sole traders and general partnerships do not; in both cases, the individual or partners remain personally liable for all obligations of the business.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.