Key Takeaways

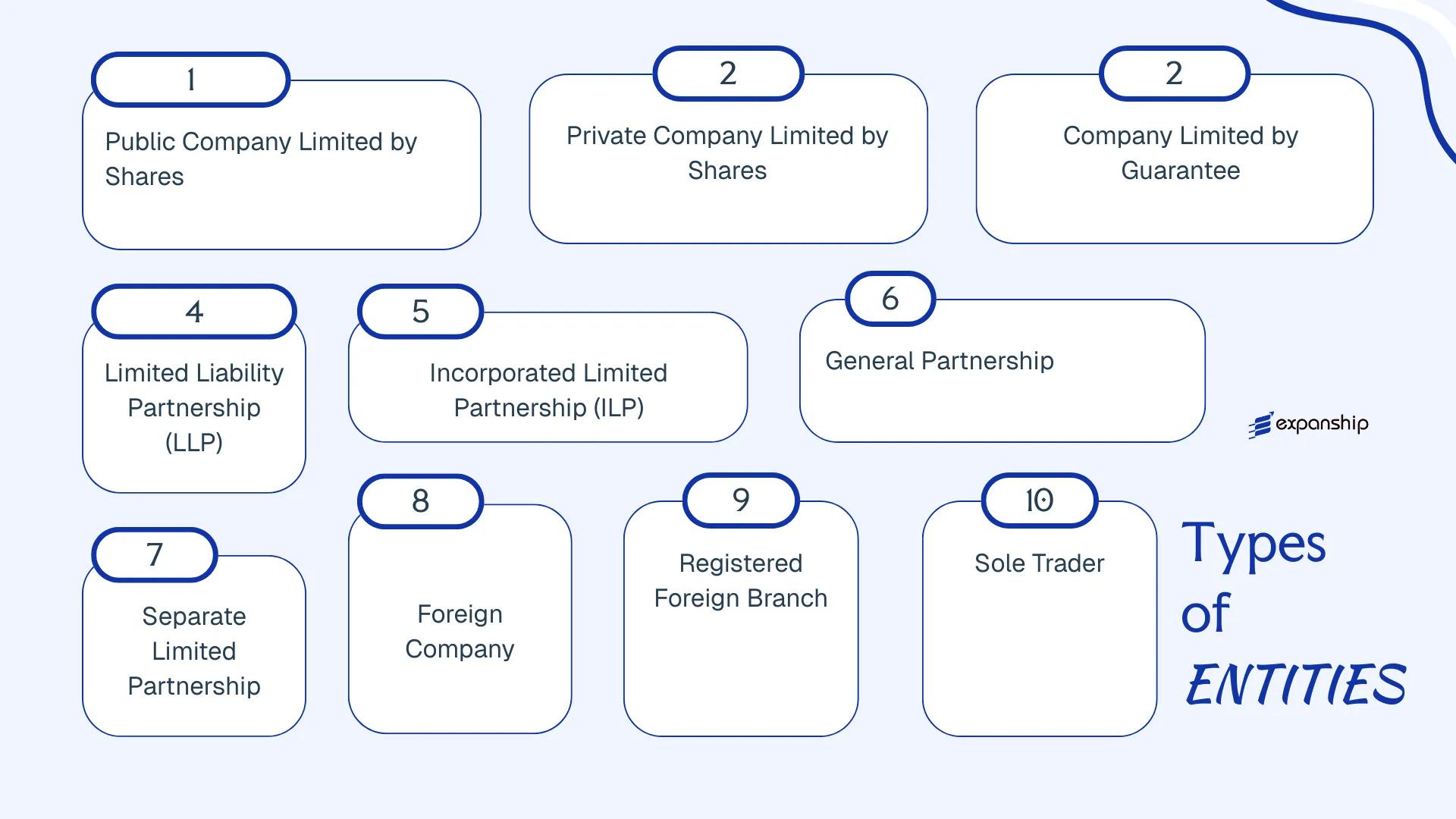

- Jersey's corporate framework, governed primarily by the Companies (Jersey) Law 1991 and overseen by the Jersey Financial Services Commission (JFSC), spans twelve distinct entity types ranging from public companies to sole traders.

- Most non-finance companies incorporated in Jersey benefit from a zero percent corporate tax rate under the island's territorial fiscal framework, distinguishing it from standard onshore jurisdictions.

- The private company limited by shares is the dominant registration choice in Jersey, valued for its structural flexibility and closed membership model.

- Incorporated Limited Partnerships and Limited Liability Partnerships provide liability separation for partnership structures, while Separate Limited Partnerships operate without separate legal personality under Jersey law.

Introduction to Entity Types in Jersey (JE)

Jersey is a Crown Dependency of the British Crown, situated in the English Channel approximately 14 miles off the coast of Normandy, France. It is not part of the United Kingdom, though the UK is responsible for its international relations and defence. Company registration falls under the jurisdiction of the Jersey Financial Services Commission (JFSC), which maintains the companies registry and oversees regulatory compliance for businesses incorporated on the island.

The types of business entities in Jersey span a broad range of structures, each governed primarily by the Companies (Jersey) Law 1991 and associated legislation. Jersey applies a standard corporate tax rate of zero percent for most non-finance companies, making it a recognized low-tax jurisdiction under its territorial fiscal framework.

Available entity types include the Public Company Limited by Shares, Private Company Limited by Shares, Company Limited by Guarantee, Limited Liability Partnership, Incorporated Limited Partnership, Separate Limited Partnership, General Partnership, Foreign Company, Registered Foreign Branch, Jersey Foundation, Non-Profit Organization, and Sole Trader. Each structure carries distinct formation requirements, liability implications, and regulatory obligations — this article examines each in detail to help you identify which suits your business objectives.

An Overview of Business Structures in Jersey (JE)

Jersey's corporate law framework accommodates more than ten distinct entity types, each governed primarily by the Companies (Jersey) Law 1991, alongside supplementary legislation such as the Limited Liability Partnerships (Jersey) Law 2017 and the Limited Partnerships (Jersey) Law 1994. The Jersey Financial Services Commission (JFSC) serves as the principal regulatory authority across most of these structures. Each entity type is designed for a different commercial purpose, ownership profile, or operational context.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company Limited by Shares | Corporate | Limited to shares | 0% standard rate | Permitted | 2 shareholders | JFSC | Companies (Jersey) Law 1991 |

| Private Company Limited by Shares | Corporate | Limited to shares | 0% standard rate | Permitted | 1 shareholder | JFSC | Companies (Jersey) Law 1991 |

| Company Limited by Guarantee | Corporate | Limited to guarantee | 0% standard rate | Permitted | 1 member | JFSC | Companies (Jersey) Law 1991 |

| Limited Liability Partnership (LLP) | Partnership | Limited | 0% standard rate | Permitted | 2 partners | JFSC | LLPs (Jersey) Law 2017 |

| Incorporated Limited Partnership (ILP) | Partnership | Mixed | 0% standard rate | Permitted | 1 GP, 1 LP | JFSC | Limited Partnerships (Jersey) Law 1994 |

| Separate Limited Partnership | Partnership | Mixed | 0% standard rate | Permitted | 1 GP, 1 LP | JFSC | Limited Partnerships (Jersey) Law 1994 |

| General Partnership | Partnership | Unlimited | 0% standard rate | Permitted | 2 partners | No registration required | Customary law |

| Foreign Company | Corporate | Limited | Varies | Restricted | 1 entity | JFSC | Companies (Jersey) Law 1991 |

| Registered Foreign Branch | Branch | Parent liability | Varies | Permitted | N/A | JFSC | Companies (Jersey) Law 1991 |

| Jersey Foundation | Foundation | Limited | 0% standard rate | Restricted | 1 founder | JFSC | Foundations (Jersey) Law 2009 |

| Non-Profit Organization | Varies | Varies | Exempt | Restricted | Varies | JFSC / relevant body | Various |

| Sole Trader | Unincorporated | Unlimited | Personal income tax | Permitted | 1 individual | None | Customary law |

Each of these structures is examined in full in the sections below.

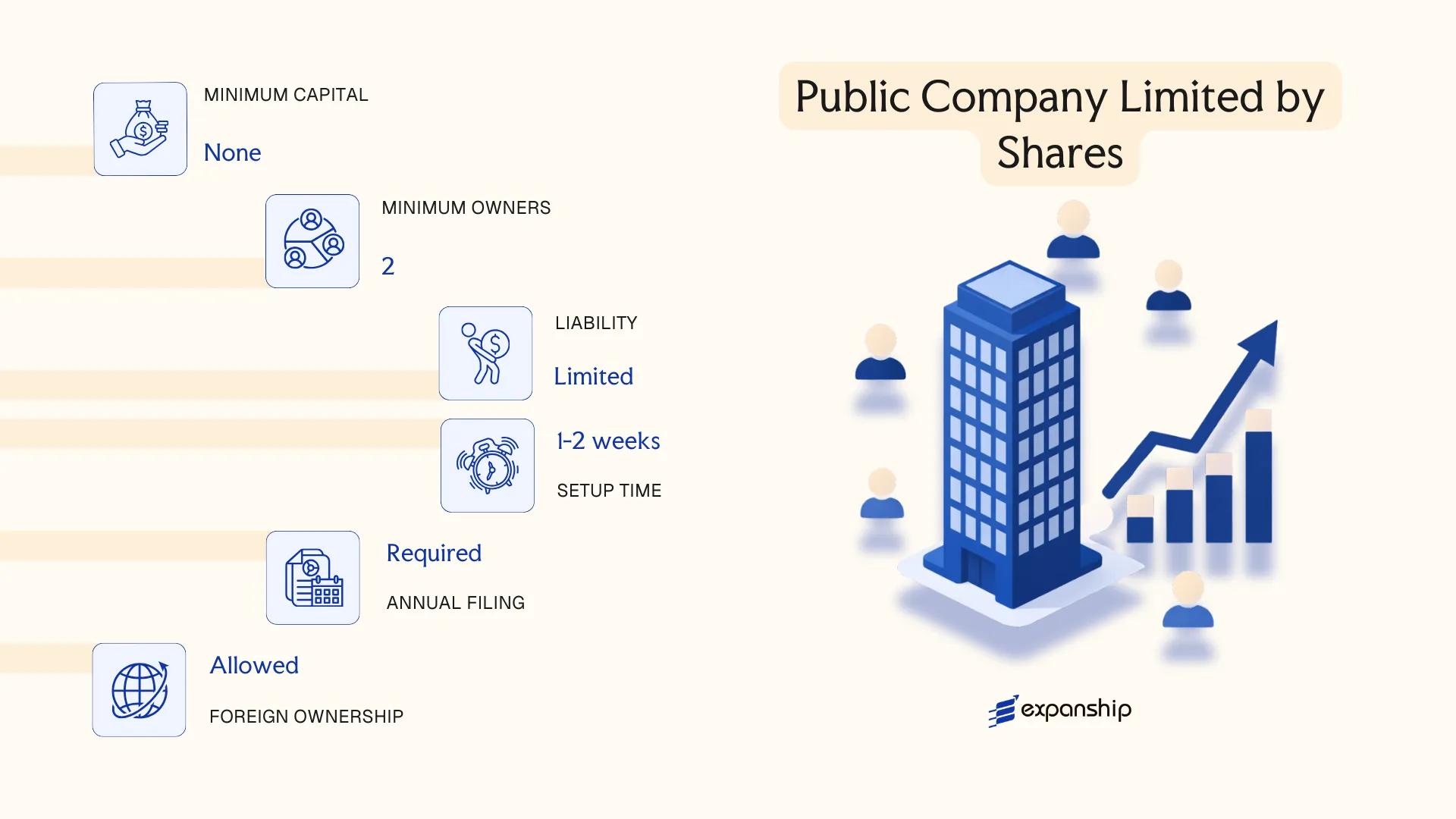

Public Company Limited by Shares

A Jersey public company limited by shares is governed by the Companies (Jersey) Law 1991, as amended, which establishes the foundational framework for its formation, governance, and ongoing obligations. The entity holds separate legal personality distinct from its shareholders, and liability is limited to the amount unpaid on shares held.

Designed for businesses seeking access to capital markets or broad public ownership, this structure supports both listed and unlisted configurations. Listing on a recognised exchange, such as The International Stock Exchange (TISE) based in St. Helier, is a common path for Jersey public company formation but is not a statutory requirement for the designation itself.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public company limited by shares | Incorporated under the Companies (Jersey) Law 1991 |

| Members | Directors: minimum 2; Shareholders: minimum 2, no maximum | Directors need not be Jersey-resident; corporate directors permitted |

| Local Presence | Registered office in Jersey required | Must be maintained at all times; registered agent not mandatorily required by statute but typically engaged in practice |

| Capital | No minimum share capital prescribed by law; denominated in any currency | Shares must be paid up to the extent required by the memorandum |

| Privacy | Register of members is not publicly accessible | Beneficial ownership information held by registered agent under AML obligations |

| Governance | Memorandum and Articles of Association required | Articles govern internal management; constitution must state "public company" |

Focus Points

- Taxation: Jersey-resident companies are subject to a standard 0% corporate income tax rate on most income; a 10% rate applies to Jersey financial services companies and 20% to certain utility and property income; no capital gains tax, no VAT (GST at 5% applies domestically), and no withholding tax on dividends.

- Economic Substance: Public companies carrying on relevant activities — including holding company, finance and leasing, or headquartering functions — must satisfy Jersey's economic substance requirements under the Taxation (Companies — Economic Substance) (Jersey) Law 2019.

- Annual Compliance: Annual confirmation statement and financial statements required; audit obligations apply unless an exemption is granted; annual return filed with the Jersey Financial Services Commission (JFSC).

- Treaty Access: Jersey is not an EU member state and has a limited network of double taxation agreements; access to certain treaty benefits may require careful structuring.

- Conversion: A public company may be converted to a private company by special resolution, subject to JFSC filing and compliance with the Companies (Jersey) Law 1991 conversion procedures.

Closing

Public companies limited by shares are most commonly used for collective investment vehicles, capital-market-facing holding structures, and cross-border listings via TISE. The structure provides genuine access to public capital markets, though the compliance burden — including potential audit requirements and ongoing governance obligations — is considerably heavier than for a private equivalent.

Best suited for businesses seeking public investment, planning a stock exchange listing, or operating large-scale holding and finance structures that require the credibility of a publicly designated entity.

Company Incorporation in Jersey

Incorporate a public or private company in Jersey with full compliance support across all JFSC requirements.

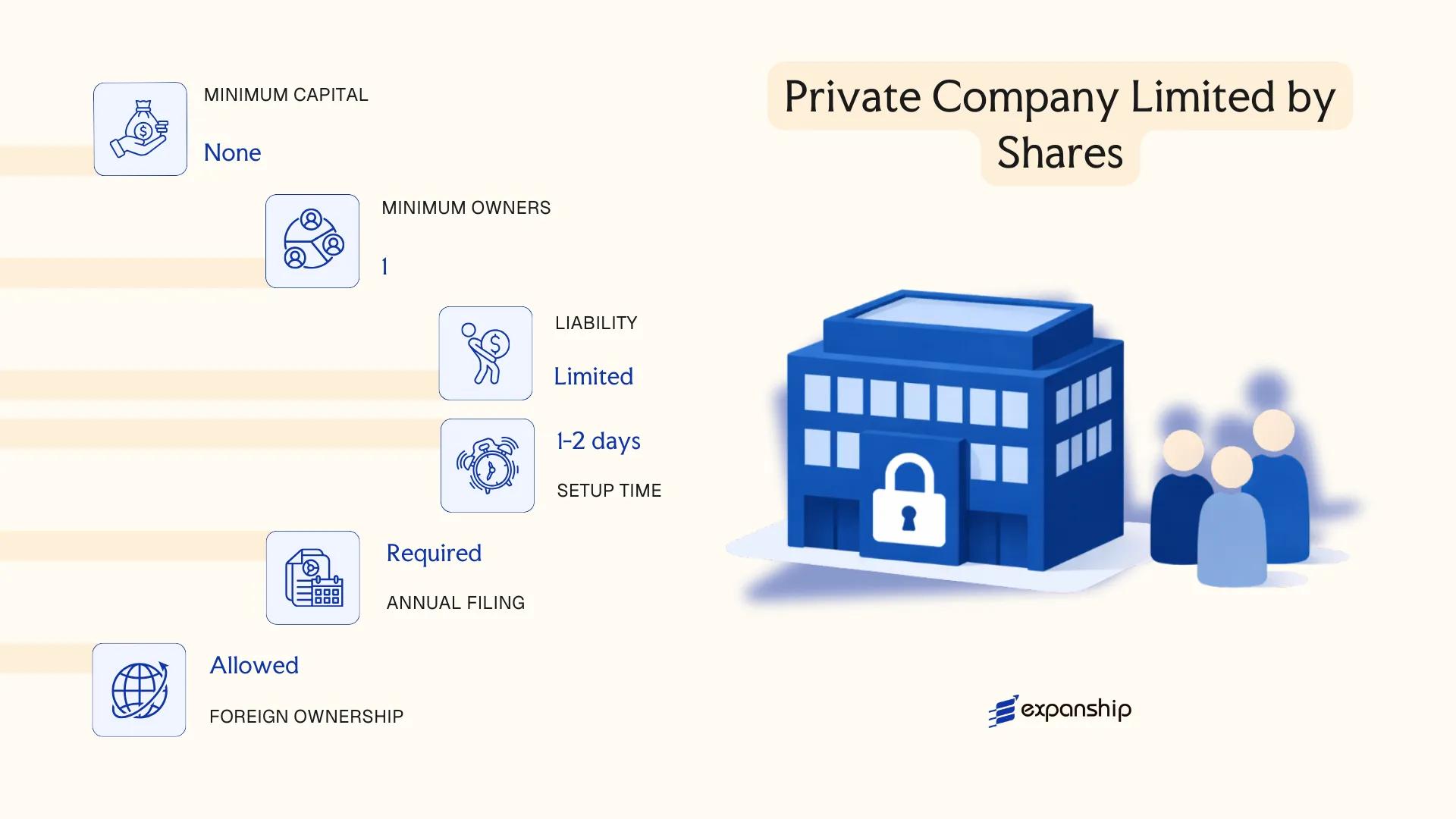

Private Company Limited by Shares

A Jersey private company limited by shares is the most widely used corporate structure on the island, governed by the Companies (Jersey) Law 1991. It holds separate legal personality, meaning the entity can own assets, enter contracts, and incur liabilities in its own name, distinct from those of its shareholders.

Liability of each shareholder is capped at the nominal value of their shares. This structure sits between a purely offshore vehicle and an operationally active firm, making it suitable across a range of commercial purposes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private company limited by shares | Cannot offer shares to the public |

| Members | Shareholders (min. 1, max. 30) | Corporate shareholders permitted; 30-member cap distinguishes it from a public company |

| Officers | Min. 1 director; company secretary optional | Directors can be corporate; no residency requirement for directors |

| Local Presence | Registered office in Jersey required | Must be maintained through a regulated service provider if the company lacks a local office |

| Capital | No minimum share capital; shares can be denominated in any currency | Par value and no-par-value shares both permitted under the 1991 Law |

| Privacy | Shareholder details not on the public register | Beneficial ownership held on a private central register accessible to authorities |

Focus Points

- Taxation: Jersey-resident companies pay corporate income tax at 0% under the standard rate (10% for financial services firms, 20% for utility companies); no VAT, no withholding tax on dividends, and no capital gains tax applies.

- Economic Substance: Companies in scope under the Taxation (Companies - Economic Substance) (Jersey) Law 2019 must demonstrate adequate substance if conducting relevant activities such as holding company, finance, or IP business.

- Annual Compliance: Annual confirmation statement and financial statements required; audit obligations depend on company size and shareholder agreement.

- Treaty Access: Jersey is not an EU member and has a limited tax treaty network; access to double tax agreements is restricted compared to onshore EU jurisdictions.

- Conversion: A private company may be converted to a public company or re-registered as a different structure under the 1991 Law, subject to JFSC approval where applicable.

Closing

A private company limited by shares suits holding structures, trading operations, and IP ownership arrangements, with the absence of minimum capital requirements offering practical flexibility at formation. The 30-shareholder ceiling, however, limits scalability for businesses seeking to bring in a broader investor base.

This structure fits closely held businesses, family-owned enterprises, and international holding vehicles where a small, defined shareholder group is maintained.

Company Limited by Guarantee

A company limited by guarantee Jersey structures differ from share-capital companies in that members contribute a nominal guaranteed amount upon winding up rather than subscribing for shares. Governed by the Companies (Jersey) Law 1991, this entity has separate legal personality and confers limited liability on its members, capped at the amount each member agrees to guarantee.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by guarantee | No share capital; liability limited to each member's guarantee amount |

| Members | Minimum 1 member; no statutory maximum | Members hold no shares; governance rights defined in articles |

| Directors | Minimum 1 director | No residency requirement under Jersey law, though regulated entities may face additional rules |

| Local Presence | Registered office in Jersey required | Must be maintained at all times; registered agent appointment common in practice |

| Capital | No share capital; guarantee amount typically £1 per member | Guarantee is contingent liability, only callable on winding up |

| Privacy | Director and member details held on public register at the Jersey Financial Services Commission (JFSC) | Beneficial ownership held on a non-public register |

Focus Points

- Taxation: Companies limited by guarantee resident in Jersey are subject to the standard zero rate of corporate income tax, unless income falls within a ring-fenced category attracting 10% or 20%; no VAT applies in Jersey, and there is no withholding tax on distributions.

- Annual Compliance: Annual confirmation statement and financial statements required; filing obligations vary depending on whether the entity is regulated by the JFSC.

- Economic Substance: Guarantee companies engaged in relevant activities must satisfy Jersey's economic substance requirements under the Taxation (Companies — Economic Substance) (Jersey) Law 2019.

- Conversion: Jersey law permits conversion to a share capital company subject to member approval and JFSC notification.

- Restrictions: Cannot distribute profits to members; any surplus on dissolution must be applied in accordance with the articles, typically to a similar purpose.

Closing

A non-profit company limited by guarantee in Jersey suits membership associations, charities, sports clubs, and industry bodies where asset lock and profit retention within the organisation are priorities. The absence of share capital simplifies governance, though the restriction on profit distribution makes this structure unsuitable for any commercially driven venture.

This entity type is best suited for non-profit organisations, member associations, and purpose-driven bodies that require a formal legal structure without distributing returns to members.

Limited Liability Partnership (LLP)

Governed by the Limited Liability Partnerships (Jersey) Law 2017, a Jersey Limited Liability Partnership registration creates a body with full separate legal personality, distinct from its members. The structure blends the contractual flexibility of a partnership with the liability protection typically associated with incorporated companies, making it a recognised hybrid form under Jersey law.

Members contribute to the LLP under the terms of a partnership agreement, and their personal liability for the firm's debts is generally limited to their agreed contribution. Unlike a general partnership, the LLP itself can hold assets, enter contracts, and sue or be sued in its own name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Separate legal personality | Registered under the LP Law 2017 |

| Members Referred To As | Members | No distinction between general and limited members |

| Membership | Minimum 2 members; no statutory maximum | Members can be individuals or corporate bodies |

| Local Presence | Registered office in Jersey required | No mandatory local member requirement |

| Capital | No minimum capital; denominated in any currency | Contributions defined in the partnership agreement |

| Privacy | Partnership agreement is private | Register of members is not publicly disclosed |

Focus Points

- Taxation: LLPs are fiscally transparent; profits are taxed at the member level rather than the entity level, with no corporate-level income tax, and no Jersey VAT, withholding tax, or stamp duty generally applicable on membership interests.

- Economic Substance: If the LLP carries on a relevant activity, substance obligations under the Taxation (Companies — Economic Substance) (Jersey) Law 2019 may apply depending on member residency and activity classification.

- Annual Compliance: An annual return must be filed with the Jersey Financial Services Commission (JFSC), confirming membership and registered office details.

- Conversion: Jersey law does not provide a straightforward statutory conversion mechanism from an LLP to a company; restructuring requires separate legal steps.

- Regulated Activities: LLPs conducting financial services activities require JFSC authorisation under the applicable licensing legislation.

Closing

LLPs are used in professional services, fund management, and joint venture arrangements where pass-through taxation and contractual flexibility are priorities. The fiscal transparency is a notable structural advantage, though the absence of shares limits its suitability for arrangements requiring equity distribution or external investment rounds.

Jersey LLP formation is most appropriate for professional firms, fund managers, and joint ventures seeking pass-through tax treatment with limited liability protection.

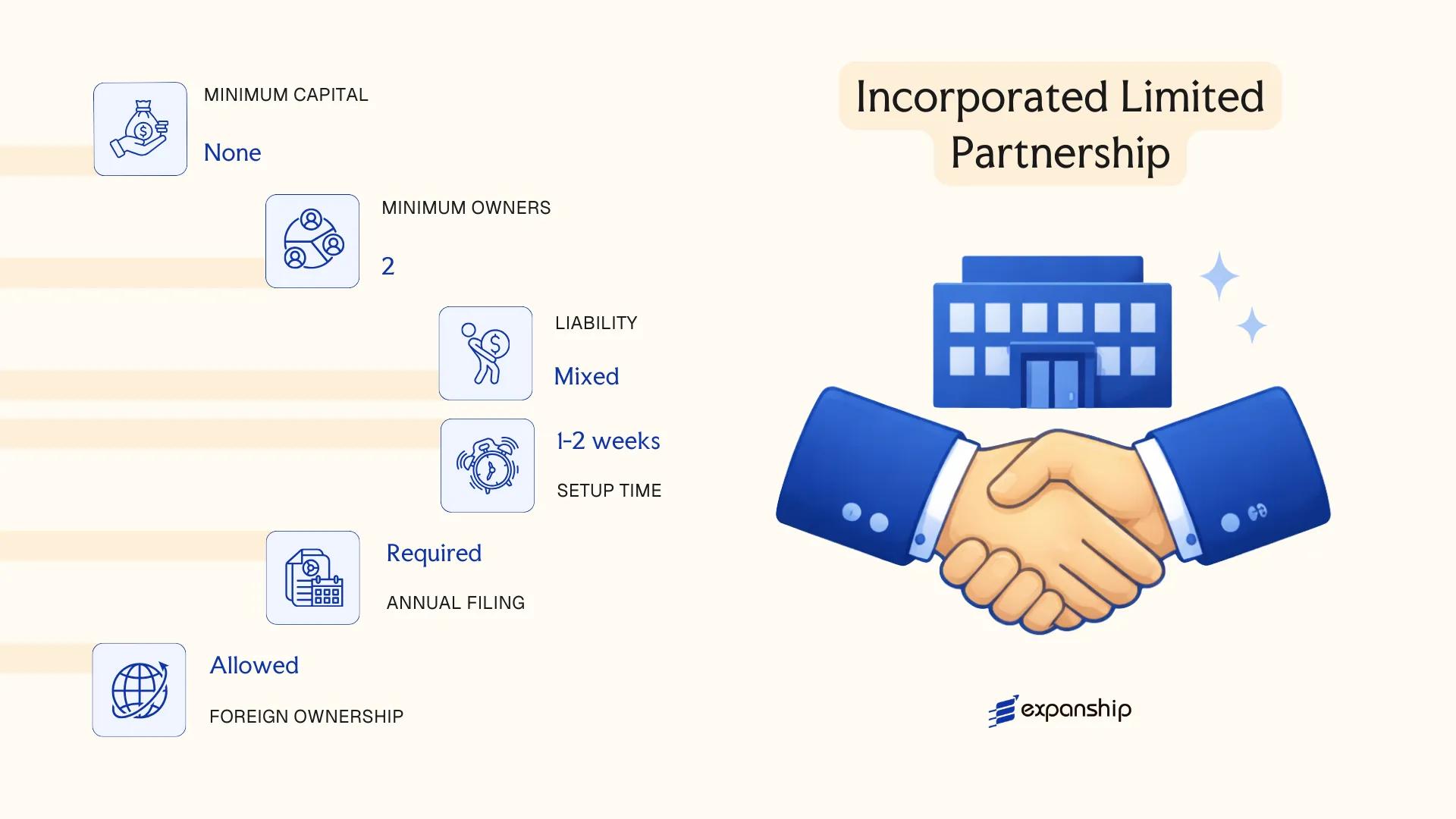

Incorporated Limited Partnership (ILP)

The Jersey Incorporated Limited Partnership ILP is governed by the Incorporated Limited Partnerships (Jersey) Law 2011. Unlike a standard limited partnership, an ILP possesses separate legal personality, meaning it can hold assets, enter contracts, and incur liabilities in its own name. This hybrid structure combines the contractual flexibility of a partnership with the legal autonomy more commonly associated with a company.

ILP registration in Jersey requires at least one general partner, who bears unlimited liability for the partnership's obligations, and one or more limited partners, whose liability is capped at their agreed contribution. The general partner may itself be a limited liability entity, which in practice contains the exposure at the top level.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Separate legal person | Can sue, be sued, and hold property in its own name |

| Partners | Min. 1 general partner (unlimited liability) + 1 limited partner | General partner may be a corporate entity |

| Local Presence | Registered office in Jersey required | Must be maintained at all times |

| Capital | No statutory minimum; contributions in any agreed form | Contributions recorded in partnership agreement |

| Register | Filed with the Jersey Financial Services Commission (JFSC) | Certificate of incorporation issued upon registration |

| Privacy | Partnership agreement not publicly filed | Partner names may appear on public register |

Focus Points

- Taxation: ILPs are generally treated as tax-transparent; income is attributed to partners and taxed at their applicable rates, with Jersey's standard 0% corporate rate applying to most non-financial-services income of corporate partners resident in Jersey.

- Economic Substance: Substance obligations do not typically apply to tax-transparent entities, though the general partner's activities may attract separate scrutiny.

- Annual Compliance: Annual confirmation filings with the JFSC are required; failure to comply can result in dissolution.

- Conversion: An ILP may convert to or from other partnership forms under Jersey law, subject to JFSC approval.

- Restrictions: Limited partners must not participate in management; doing so risks losing limited liability status.

Closing Paragraph

The Jersey ILP is used predominantly in private equity, fund structuring, and asset holding arrangements where investors require both liability protection and partnership-level tax transparency. The separate legal personality simplifies asset ownership, though the unlimited liability of the general partner remains a structural consideration that must be managed through entity design.

Best suited for fund managers and institutional investors requiring a tax-transparent vehicle with full legal personality and a defined separation between managing and investing parties.

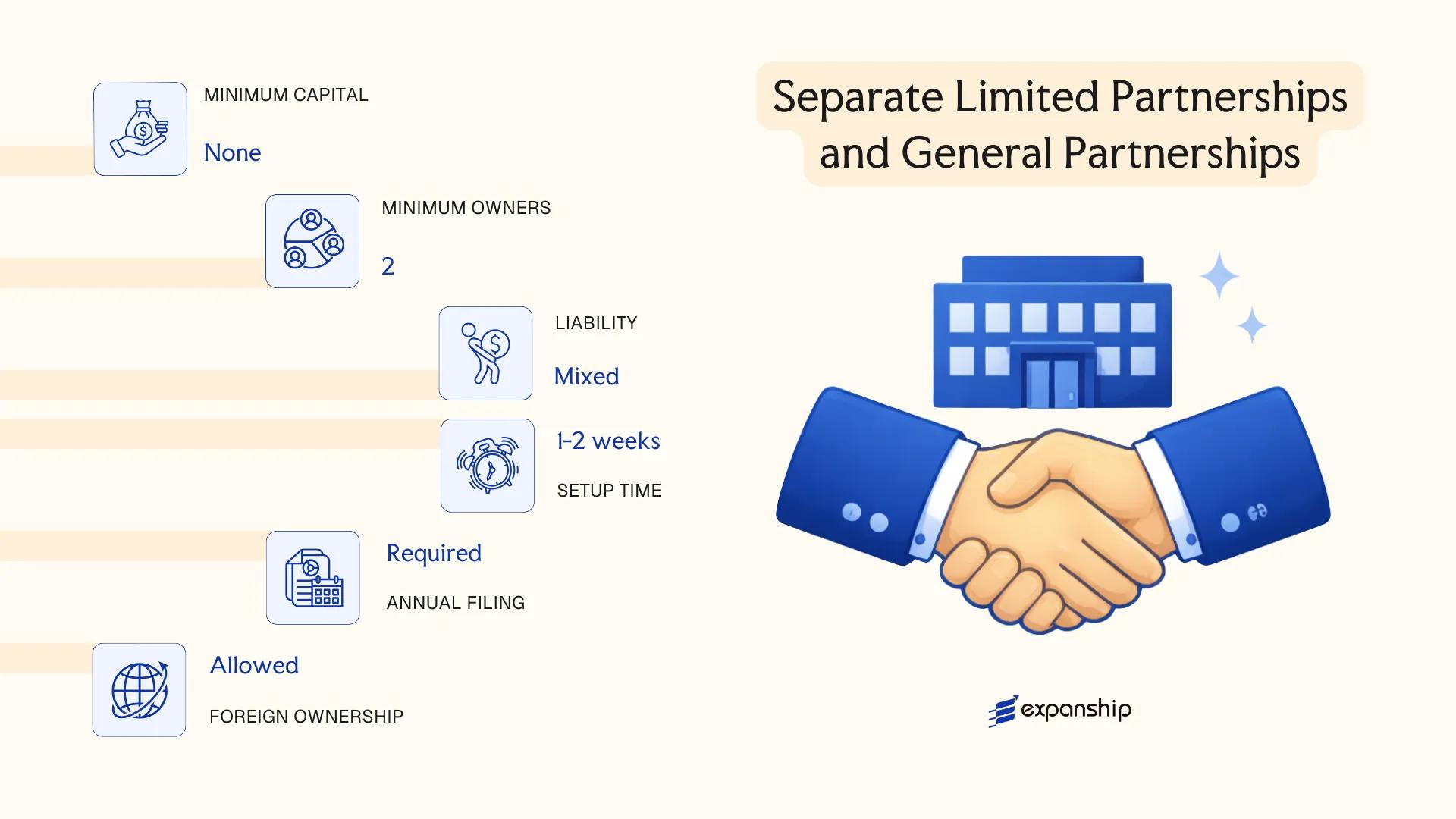

Separate Limited Partnerships and General Partnerships [General Partnership, Separate Limited Partnership]

Governed by the Separate Limited Partnerships (Jersey) Law 2011, a Jersey Separate Limited Partnership formation results in an entity that, unlike a standard limited partnership, holds separate legal personality. This distinction makes the SLP particularly suited to fund structuring and asset holding arrangements where legal separation from partners is required. General partnerships in Jersey, by contrast, are formed under the Partnership (Jersey) Law 1995 and carry no such separation — partners bear joint and several liability for the firm's obligations.

Jersey general partnership registration requires no formal filing with the Jersey Financial Services Commission (JFSC) unless the partnership carries on regulated activity. The SLP, however, must be registered with the JFSC, with a designated general partner responsible for management and compliance.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | SLP: separate legal person; GP: contractual arrangement | SLP registered under 2011 Law; GP under 1995 Law |

| Members | General partner (min. 1) + limited partners (min. 1); GP: min. 2 partners, no cap | Limited partners in SLP have liability capped at capital contribution |

| Local Presence | SLP: registered office in Jersey + registered with JFSC; GP: no formal registration unless regulated | General partner of SLP may be a corporate entity |

| Capital | No statutory minimum; denominated in any currency | Capital contributions recorded in partnership agreement |

| Privacy | Partnership agreements are not publicly filed | Register of partners not publicly disclosed |

Focus Points

- Taxation: Both structures are tax-transparent by default; partners are taxed on their share of income in their home jurisdiction, though Jersey-source income may attract local tax considerations.

- Economic Substance: SLPs used as investment vehicles may fall under the Taxation (Companies — Economic Substance) (Jersey) Law 2019 depending on activity type.

- Annual Compliance: SLPs must file an annual return with the JFSC; general partnerships have no equivalent statutory filing unless conducting regulated business.

- Treaty Access: Neither structure benefits directly from tax treaties as a standalone entity; treaty access flows through the individual partners.

- Conversion: An SLP cannot be converted directly into a company under current Jersey law; restructuring requires dissolution and re-incorporation.

Sub-Types

General Partnership

Formed by agreement between two or more persons carrying on business in common with a view to profit. No separate legal personality exists, and all partners remain personally liable.

Separate Limited Partnership (SLP)

Distinguishable from a standard limited partnership by its separate legal personality under the 2011 Law, allowing the SLP itself to hold assets, enter contracts, and sue or be sued in its own name.

When to Use These Structures

Both structures are used primarily in private equity, fund formation, and joint venture arrangements where pass-through tax treatment is preferred. The SLP's separate legal personality offers a structural advantage for asset segregation, though the unlimited liability of the general partner remains a consistent constraint.

SLPs are best suited for fund managers and institutional investors seeking tax-transparent vehicles with legal separation; general partnerships suit smaller joint ventures where formal registration is not required.

Foreign and Overseas Business Presence [Foreign Company, Registered Foreign Branch]

Registering a foreign company in Jersey is governed primarily by the Companies (Jersey) Law 1991, which sets out the obligations applicable to overseas entities conducting business within the island. A foreign company registered under these provisions does not create a new legal entity — the parent body retains its existing legal personality, and the Jersey presence operates as an extension of that structure.

Two distinct routes exist for overseas businesses: registering the foreign company itself with the Jersey Financial Services Commission (JFSC), or establishing a registered foreign branch that formally represents the parent in Jersey. Both require filing with the JFSC, though the documentation and ongoing obligations differ.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Extension of existing overseas entity | No separate legal personality in Jersey |

| Registered Persons | Directors of the parent entity | Local contact or representative may be required |

| Local Presence | Registered office address in Jersey; local agent | JFSC filing address must be maintained |

| Capital | No separate capital requirement | Parent entity's capital structure applies |

| Filing Obligations | Certified constitutional documents; certified accounts of parent | Documents may require apostille or notarisation |

| Privacy | Parent entity's details disclosed on JFSC register | Jersey branch particulars are publicly accessible |

Focus Points

- Taxation: Subject to Jersey's standard 0% corporate income tax rate for most activities; financial services businesses are taxed at 10%, and utility companies at 20%. No VAT applies in Jersey; withholding tax on dividends paid to non-residents generally does not apply under domestic law.

- Economic Substance: Branches conducting relevant activities must satisfy Jersey's economic substance requirements under the Taxation (Companies — Economic Substance) (Jersey) Law 2019.

- Annual Compliance: Annual confirmation statements and updated parent accounts must be filed with the JFSC; failure to maintain filings can result in deregistration.

- Liability: The parent entity bears unlimited liability for obligations incurred through the branch; there is no liability ring-fence at the Jersey level.

- Treaty Access: Jersey is not a full EU member and has a limited double tax agreement network; treaty access depends on the parent entity's home jurisdiction.

Closing

A registered foreign branch is commonly used by multinational firms seeking a commercial or administrative presence without the cost of incorporating a standalone local entity. The primary advantage is operational simplicity; the clear drawback is that the parent company remains fully exposed to liabilities arising from Jersey operations.

Established overseas businesses looking to formalise a Jersey presence for operational, regulatory, or client-facing purposes without altering their existing corporate structure.

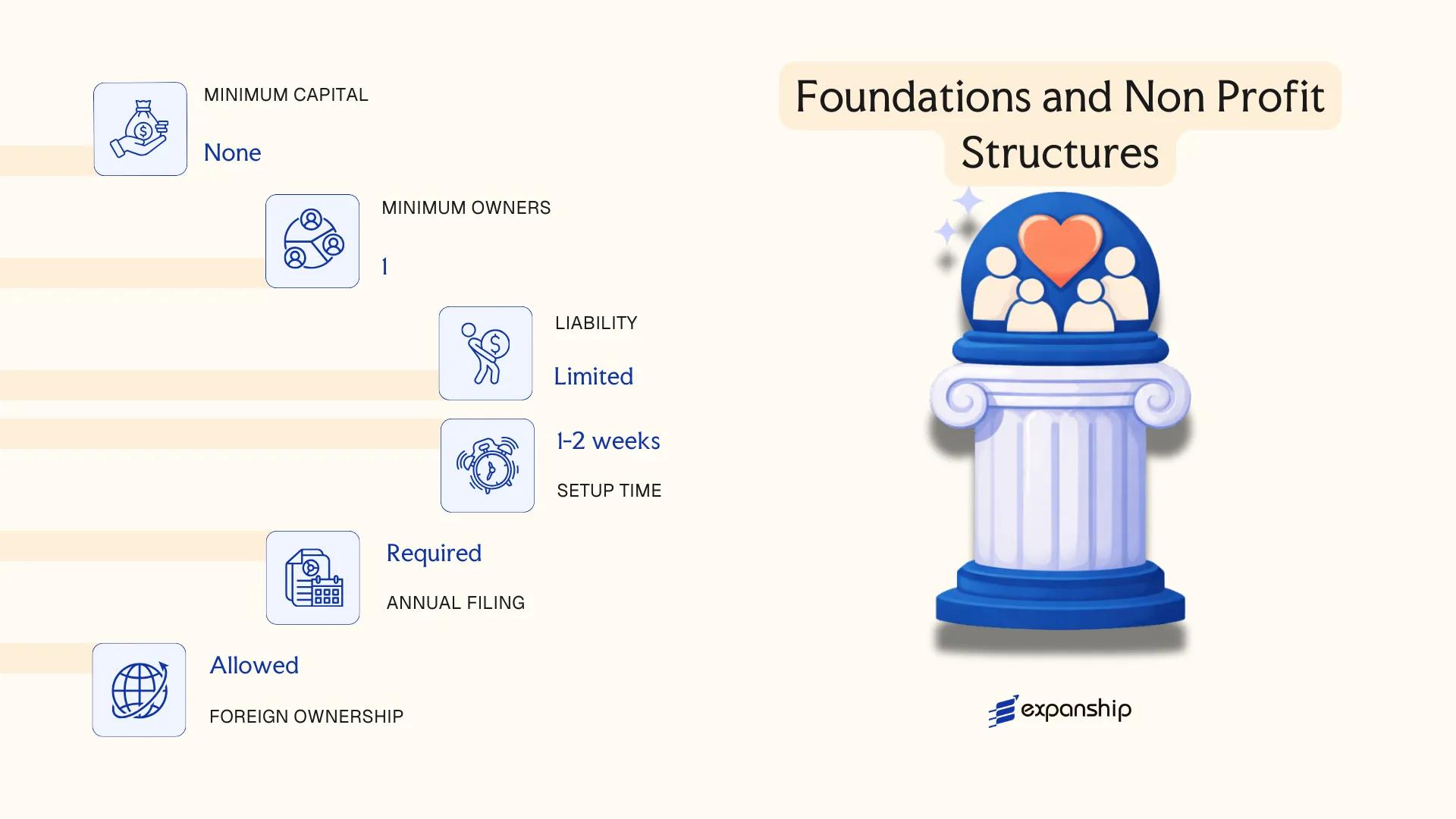

Foundations and Non-Profit Structures [Jersey Foundation, Non-Profit Organization]

Jersey Foundation registration and structure is governed by the Foundations (Jersey) Law 2009, which created a distinct legal form that sits between a trust and a company. A Foundation has separate legal personality, meaning it can hold assets, enter contracts, and incur liabilities in its own name, entirely separate from those who establish or benefit from it.

Unlike a trust, a Jersey Foundation has no beneficial owners in the traditional sense. Assets are dedicated to the purposes or persons specified in the Foundation's Charter and Regulations, making it suitable for both purpose-driven and philanthropic arrangements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Foundation (separate legal personality) | Governed by Foundations (Jersey) Law 2009 |

| Members / Officers | Council members; may also appoint a Guardian | Council manages the Foundation; Guardian oversees Council compliance with Charter |

| Minimum Members | At least one Council member; one Guardian if required by Charter | Guardian must not be a Council member |

| Local Presence | Registered office in Jersey; must appoint a Qualified Member (Jersey-regulated person) on the Council | Qualified Member requirement ensures Jersey nexus |

| Capital | No minimum capital requirement | Assets are dedicated to Foundation purposes; no share capital |

| Privacy | Charter filed with the Registrar; Regulations may remain private | Beneficial ownership details held by regulated service providers, not publicly disclosed |

Focus Points

- Taxation: Foundations are generally subject to Jersey's standard 0% corporate income tax rate for non-financial services income; distributions to non-Jersey beneficiaries are not subject to withholding tax, and no stamp duty applies on asset transfers into the Foundation in most cases.

- Annual Compliance: Annual return must be filed with the Jersey Financial Services Commission (JFSC); accounts are required but not publicly filed.

- Economic Substance: Foundations used for holding purposes are generally not subject to the economic substance requirements that apply to certain company types.

- Conversion: No statutory mechanism exists to convert a Foundation into a company or trust, though assets can be transferred out by following the Charter's terms.

- Restrictions: A Foundation cannot distribute assets to its founders or Council members unless the Charter explicitly permits it, limiting its use as a direct profit-extraction vehicle.

Sub-Types

Jersey Foundation (Charitable Purpose)

A Foundation may be established exclusively for charitable purposes, in which case its Charter must clearly define those purposes and restrict asset distribution to qualifying charitable objects. This structure is used by family offices and philanthropists seeking a formal charitable vehicle without registering a separate non-profit company.

Jersey Foundation (Purpose and Beneficiary Hybrid)

A Foundation may combine specific purposes with named or class beneficiaries, allowing both mission-driven activity and distributions to defined persons. This hybrid form is commonly used in succession planning and asset protection arrangements where flexibility in both purpose and benefit is required.

Closing

Jersey Foundations are used predominantly for wealth structuring, succession planning, philanthropy, and holding arrangements where the separation of asset ownership from personal estates is the primary objective. The absence of share capital and the privacy of Regulations are practical advantages, though the mandatory Qualified Member requirement means ongoing reliance on a Jersey-regulated service provider is unavoidable.

Jersey Foundations are best suited for high-net-worth individuals, family offices, and philanthropic organisations seeking a purpose-driven vehicle with legal personality and asset separation outside a conventional corporate structure.

Sole Trader

Sole trader registration in Jersey follows no dedicated incorporation statute — the structure is not a separate legal entity. You and your business are one and the same in law, meaning personal assets are exposed to any liabilities the business incurs. There is no equivalent of the Companies (Jersey) Law 1991 governing this form; instead, obligations arise through tax registration, social security enrolment, and, where applicable, sector-specific licensing.

Operating as a self-employed sole trader in Jersey CI requires registration with the Taxes Office (Revenue Jersey) for income tax purposes and with the Social Security Department for Class 2 contributions. If annual turnover exceeds the GST registration threshold, registration under the Goods and Services Tax (Jersey) Law 2007 is also required.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Referred To As | Sole trader / proprietor | No directors, shareholders, or members |

| Participants | One individual only | Cannot have co-owners; must be the operator |

| Local Presence | No registered office requirement | A trading address is required for correspondence |

| Capital | No minimum capital | No formal share structure |

| Privacy | Financial accounts not publicly filed | Income reported via personal tax return |

Focus Points

- Taxation: Personal income tax applies at a standard rate of 20% under the Income Tax (Jersey) Law 1961; no corporate tax, no withholding tax on sole trader income, and GST registration required once the turnover threshold is met.

- Social Security: Class 2 contributions are mandatory and calculated on taxable earnings; rates are set annually by the Social Security Department.

- Annual Compliance: No annual return or audited accounts are required; obligations are limited to income tax filing and social security declarations.

- Treaty Access: Jersey is not an EU member and has limited double tax agreements; sole traders do not access treaties through any corporate vehicle.

- Conversion: A sole trader can convert to a private limited company under the Companies (Jersey) Law 1991, but assets must be formally transferred as there is no statutory conversion mechanism.

Closing

A sole trader structure suits individuals providing services or running small-scale trading operations where setup speed and minimal administrative overhead outweigh the need for liability protection. The absence of limited liability is the principal drawback for any activity carrying meaningful financial or legal risk.

Freelancers, consultants, and sole-operator service businesses with low liability exposure and no requirement for external investment or a formal corporate structure.

How to Choose the Right Entity Type in Jersey (JE)

Selecting how to choose the right business entity in Jersey requires more than weighing setup costs — the structure you register shapes your tax position, compliance burden, and operational capacity for the life of the business.

Why Your Entity Choice Matters

Structural mismatches produce concrete legal and financial consequences:

- Registering a foreign company branch when you intend to trade locally without completing the required notification process under the Companies (Jersey) Law 1991 can result in penalties or administrative dissolution.

- Choosing a standard Jersey company subject to the 0% corporate tax rate does not automatically grant treaty access — Jersey has a limited double taxation agreement network, so withholding tax reductions available under those agreements may not apply to your entity.

- Forming a company when a Jersey Foundation would serve estate planning or asset protection goals locks you into annual shareholder obligations, director filings, and potential audit requirements that foundations do not carry.

- Selecting a structure subject to substance requirements under the Taxation (Companies — Economic Substance) (Jersey) Law 2019 without the capacity to maintain genuine local presence triggers reporting failures and potential financial penalties.

Key Factors to Consider

- Business Activity: Passive asset holding, active trading, and regulated activities such as fund management each point to structurally distinct entities under Jersey financial services legislation.

- Local vs. Offshore Operations: Transacting with Jersey residents imposes different obligations than operating entirely outside the jurisdiction.

- Ownership and Management: Multi-party arrangements may favour an LLP or ILP for flexible governance, while a single operator may find a private company sufficient.

- Tax Objectives: Your entity choice determines eligibility for the 0% standard rate, the 10% or 20% higher rates applicable to specific sectors, or regulated fund treatment.

- Substance Capacity: If you cannot maintain employees, a registered office with real activity, and local decision-making, your chosen structure must either fall outside substance rules or qualify for an exemption.

- Exit Strategy: Not all Jersey structures permit redomiciliation or conversion — verify this before formation if a future structural change is foreseeable.

Compliance Services for Companies in Jersey

Maintain good standing with Jersey's regulatory requirements, from annual filings to economic substance obligations.

Conclusion

Jersey's summary of company formation options reflects a jurisdiction that has deliberately built its legal framework to serve both private wealth and commercial enterprise. The private company limited by shares dominates registrations under the Companies (Jersey) Law 1991, favoured for its flexibility and closed membership structure. Public companies suit capital-raising entities; companies limited by guarantee serve membership organisations. LLPs and ILPs address partnership structures where liability separation matters, while Separate Limited Partnerships retain the traditional model without separate legal personality. Foundations serve succession and philanthropic planning. Foreign companies and registered branches allow overseas firms to operate locally without full incorporation. Sole traders remain the entry point for individual operators.

Regulated by the Jersey Financial Services Commission, the island continues to refine its compliance standards in alignment with FATF recommendations and international transparency expectations, reinforcing its position as a well-regulated offshore centre. Your choice of structure will ultimately depend on ownership, activity, and long-term objectives.

How Expanship Can Assist You

Expanship company formation services Jersey cover every structure discussed in this guide, from Private Companies Limited by Shares to Incorporated Limited Partnerships and Jersey Foundations. Whether your entity requires registration with the Jersey Financial Services Commission (JFSC) or filing under the Companies (Jersey) Law 1991, our team manages each stage with jurisdiction-specific knowledge.

Engaging Expanship as your corporate services provider in Jersey CI means you receive end-to-end support across the full incorporation and compliance lifecycle:

- Document preparation, notarisation, and apostille where required

- Registered agent and registered office provision in Jersey

- Government filing and direct liaison with the JFSC and Companies Registry

- Post-incorporation compliance management, including annual confirmation statements

- Banking introduction assistance with Jersey-based and international financial institutions

- Ongoing corporate secretarial support

Reach out to Expanship Jersey to discuss your structure and start the process.

Frequently Asked Questions (FAQ)

The private company limited by shares is the most frequently incorporated structure under the Companies (Jersey) Law 1991. Its combination of limited liability, flexible share structures, and suitability for both resident and non-resident ownership makes it the default choice across a wide range of commercial purposes.

A private company limited by shares holds assets for the benefit of its shareholders, while a Jersey Foundation holds assets for defined purposes or beneficiaries without shareholders or members. Foundations do not distribute profits in the conventional sense and are governed by the Foundations (Jersey) Law 2009, which imposes distinct compliance obligations separate from standard company law.

A private company limited by shares, particularly when using nominee directors and shareholders, offers a meaningful degree of privacy. The public registry does not disclose beneficial ownership information to the general public, though the Jersey Financial Services Commission retains access to that data under regulatory obligations.

Not all structures permit sole formation. A private company requires at least one shareholder and one director, while a general partnership and a separate limited partnership each require a minimum of two partners. A sole trader, by definition, involves one individual operating without a separate legal structure.

Foreign nationals face no statutory prohibition on incorporating a company or establishing a foundation. However, certain regulated activities, including fund administration and trust services, require licensing from the Jersey Financial Services Commission regardless of the applicant's nationality. Substance requirements may also apply depending on the nature of the business conducted from Jersey.

The Companies (Jersey) Law 1991 permits certain structural changes, including the conversion of a private company to a public company and vice versa. Migration of foreign companies into Jersey as a registered entity is also possible through continuation procedures, though not all entity types can be directly converted into one another without dissolution and re-registration.

No. General partnerships do not hold separate legal personality under Jersey law, meaning partners bear direct liability for the firm's obligations. By contrast, private and public companies, incorporated limited partnerships, and Jersey Foundations each possess distinct legal personality, allowing them to hold assets, enter contracts, and incur liabilities in their own name.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.