Key Takeaways

- Iceland's most widely registered entity, the einkahlutafélag (ehf.), offers limited liability to both domestic and foreign investors under the Act on Private Limited Companies (No. 138/1994).

- The hlutafélag (hf.) is governed by the Act on Public Limited Companies (No. 2/1995) and is the appropriate structure for companies seeking public financing or stock exchange listing.

- Foreign companies can establish a regulated presence in Iceland without creating a separate legal entity by registering a branch office (Útibú) or representative office (Tengiliðskrifstofa) through Fyrirtækjaskrá.

- Sole proprietorships (Einstaklingsfyrirtæki) carry unlimited personal liability, making them suitable only for low-risk, owner-operated businesses rather than ventures with significant financial or legal exposure.

Introduction to Entity Types in Iceland

Iceland is a North Atlantic island nation, positioned between Greenland and Norway, with membership in the European Economic Area (EEA) but outside the European Union. Company registration falls under the authority of Fyrirtækjaskrá (the Company Registry), which operates under the Icelandic Directorate of Internal Revenue. The country maintains a standard corporate tax rate with a territorial dimension, and businesses operating here are subject to the Act on Private Limited Companies (No. 138/1994) and the Act on Public Limited Companies (No. 2/1995) as the primary legislative frameworks.

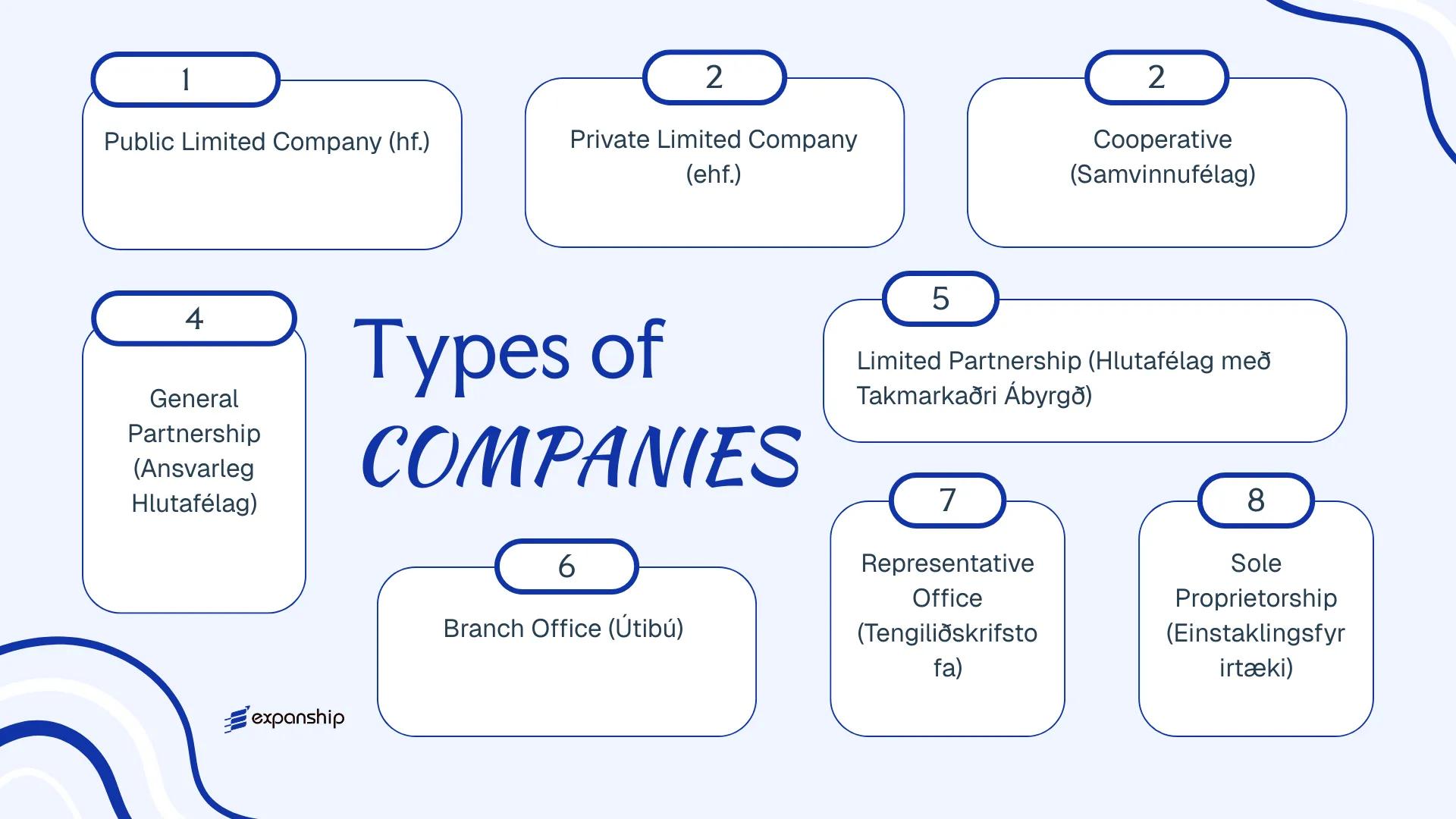

Several types of business entities in Iceland are available to domestic and foreign investors. These include the Public Limited Company (Hlutafélag, hf.), Private Limited Company (Einkahlutafélag, ehf.), Cooperative (Samvinnufélag), General Partnership (Ansvarleg Hlutafélag), Limited Partnership (Hlutafélag með Takmarkaðri Ábyrgð), Branch Office (Útibú), Representative Office (Tengiliðskrifstofa), and Sole Proprietorship (Einstaklingsfyrirtæki).

Each structure carries distinct liability rules, capital requirements, and governance obligations. This article examines each form in detail to help you determine which structure suits your operational and regulatory requirements.

An Overview of Business Structures in Iceland

Iceland's company law framework accommodates several distinct entity types, each governed primarily by legislation including the Private Limited Companies Act (No. 138/1994), the Public Limited Companies Act (No. 2/1995), and the Commercial Register Act. Each structure carries different implications for liability, ownership, taxation, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (hf.) | Corporate entity | Limited to share capital | Taxed | Yes | 1 shareholder | Fyrirtækjaskrá (Company Registry) | Public Limited Companies Act No. 2/1995 |

| Private Limited Company (ehf.) | Corporate entity | Limited to share capital | Taxed | Yes | 1 shareholder | Fyrirtækjaskrá | Private Limited Companies Act No. 138/1994 |

| Cooperative (Samvinnufélag) | Collective entity | Limited | Taxed | Yes | Variable | Fyrirtækjaskrá | Cooperative Societies Act |

| General Partnership (Ansvarleg Hlutafélag) | Unincorporated | Unlimited, joint | Taxed | Yes | 2 partners | Fyrirtækjaskrá | Partnership Act |

| Limited Partnership (HT) | Unincorporated | Mixed | Taxed | Yes | 2 partners | Fyrirtækjaskrá | Partnership Act |

| Branch Office (Útibú) | Extension of foreign entity | Parent liable | Taxed on local income | Yes | N/A | Fyrirtækjaskrá | Foreign Companies Act |

| Representative Office (Tengiliðskrifstofa) | Non-trading presence | Parent liable | Generally exempt | No | N/A | Fyrirtækjaskrá | Foreign Companies Act |

| Sole Proprietorship (Einstaklingsfyrirtæki) | Individual trader | Unlimited, personal | Taxed | Yes | 1 individual | Fyrirtækjaskrá | Commercial Register Act |

Each of these structures is examined in full in the sections below.

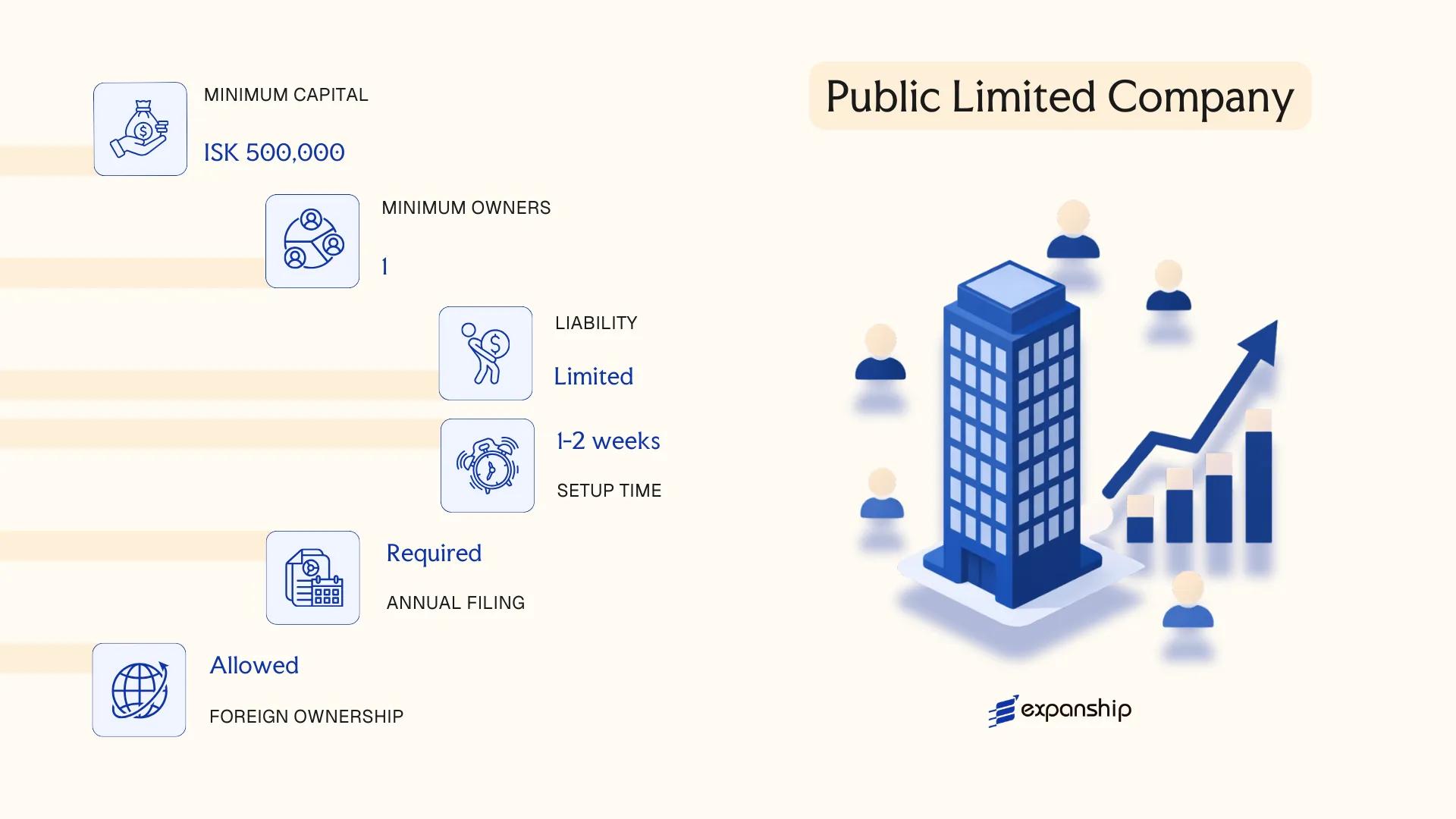

Public Limited Company (Hlutafélag, hf.)

Governed by the Act on Public Limited Companies No. 2/1995, the Hlutafélag is the standard vehicle for Iceland public limited company hf registration where public share offerings or stock exchange listing are intended. The entity carries separate legal personality, and shareholder liability is capped at the value of their subscribed shares.

Hlutafélag formation in Iceland follows a formal deed of incorporation process supervised by the Directorate of Internal Revenue (Ríkisskattstjóri), which handles the company registry. Shares in an hf. may be freely transferred and, where the firm meets listing requirements, admitted to trading on Nasdaq Iceland.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (Hlutafélag, hf.) | Separate legal personality; limited liability |

| Members | Shareholders (no maximum); minimum 1 shareholder at formation | Shareholders may be natural persons or legal entities |

| Governing Body | Board of Directors (minimum 3 members) + Managing Director | Managing director cannot chair the board |

| Local Presence | Registered office in Iceland required | No statutory requirement for a local resident director, but board must be reachable |

| Share Capital | Minimum ISK 4,000,000 (fully paid on registration) | Shares must have a stated nominal value |

| Privacy | Shareholder register is publicly accessible | Annual accounts filed with the Registry are publicly available |

Focus Points

- Taxation: Subject to 20% corporate income tax; VAT applies at standard 24% (11% reduced rate); withholding tax on dividends paid to non-residents is generally 20%, subject to applicable tax treaty reductions.

- Annual Compliance: Audited financial statements mandatory; annual general meeting required within eight months of financial year-end.

- Treaty Access: Iceland's extensive double taxation treaty network is accessible, supporting cross-border dividend, interest, and royalty flows.

- Conversion: An hf. may be converted into an ehf. (private limited company) provided it meets the relevant statutory conditions under Act No. 138/1994.

- Restrictions: Regulated sectors such as banking and insurance impose additional licensing requirements beyond standard company registration.

Recommendations

The hf. structure suits businesses seeking equity capital from public markets, large joint ventures, or firms planning a Nasdaq Iceland listing. Its primary advantage is unrestricted share transferability; the main constraint is the higher minimum capital threshold and mandatory audit obligations, which increase ongoing compliance costs.

This entity type is most appropriate for established businesses or investment vehicles intending to raise capital publicly or operate at scale within Iceland.

Company Incorporation in Iceland

Incorporate an hf. or other entity type in Iceland with end-to-end support from Expanship's corporate services team.

Private Limited Company (Einkahlutafélag, ehf.)

The einkahlutafélag (ehf.) is governed by the Private Limited Companies Act No. 138/1994, as amended, and is the most widely used corporate structure for Iceland private limited company ehf formation. It carries separate legal personality, meaning the entity holds rights and obligations distinct from its shareholders, with liability confined to contributed capital.

Einkahlutafélag registration Iceland follows a relatively straightforward process through Fyrirtækjaskrá, the Icelandic Register of Enterprises, operated under the Directorate of Internal Revenue (Ríkisskattstjóri). Shares in an ehf. are non-publicly tradeable and transfer is subject to restrictions set out in the company's articles of association.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company (Einkahlutafélag, ehf.) | Separate legal personality; limited liability |

| Members | Shareholders; minimum 1, no maximum | Single-shareholder structure permitted |

| Management | Board of Directors (optional for small firms) or Managing Director | Companies with share capital above ISK 4,000,000 must appoint a board |

| Local Presence | Registered office in Iceland required | No mandatory resident director, but a registered address is compulsory |

| Share Capital | Minimum ISK 500,000; no authorised maximum | Must be fully subscribed at incorporation |

| Privacy | Shareholder register is not public; financial statements are filed publicly | Beneficial ownership is reported to a central register |

Focus Points

- Taxation: Subject to corporate income tax at 20%; VAT applies at standard 24% (reduced 11% rate for select services); withholding tax applies on dividends paid to non-residents; no stamp duty on share transfers.

- Annual Compliance: Annual financial statements must be filed with Ríkisskattstjóri; audit requirements depend on company size thresholds.

- Treaty Access: As an Icelandic tax-resident entity, an ehf. can access Iceland's network of double taxation agreements.

- Conversion: An ehf. may be converted to a public limited company (hf.) by resolution and fulfilment of the higher capital requirements under the Public Limited Companies Act No. 2/1995.

- Restrictions: Shares cannot be offered to the public; transfer restrictions in articles are binding on prospective purchasers.

Closing

The ehf. suits trading operations, holding structures, and SME activity where limited liability and operational flexibility are priorities, though the non-negotiable minimum capital and public filing of financial statements are practical constraints to plan for.

Founders and foreign investors establishing a closely held operating or holding business in Iceland with no intention of public share issuance.

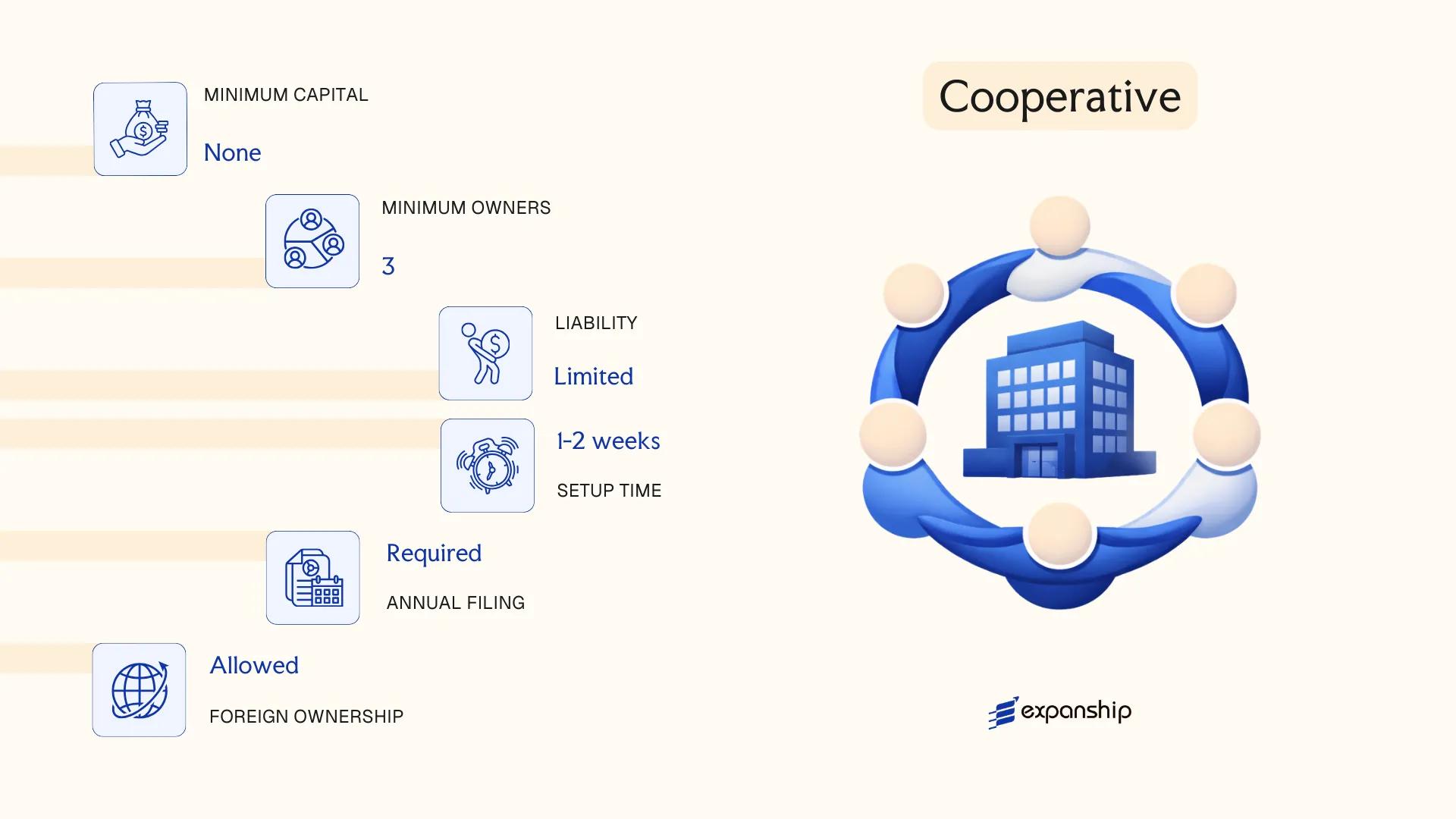

Cooperative (Samvinnufélag)

Iceland cooperative Samvinnufélag registration is governed primarily by the Act on Cooperatives No. 22/1991, which establishes the legal framework for forming and operating member-owned entities in the country. A Samvinnufélag holds separate legal personality and offers its members limited liability, distinguishing it from general partnerships where personal exposure is unlimited.

Membership in a cooperative is open and variable by design, meaning the number of members can change without requiring formal amendments to the founding documents. This structural flexibility suits organisations oriented around a shared economic purpose rather than profit distribution to investors.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative Society | Separate legal personality under Act No. 22/1991 |

| Members | Referred to as members; minimum 5 required | No fixed maximum; membership can fluctuate |

| Governance | Board of Directors elected by members | General meeting (aðalfundur) is the supreme decision-making body |

| Registered Office | Must maintain a registered address in Iceland | Required for official correspondence and filings |

| Capital | No statutory minimum share capital | Members contribute according to cooperative bylaws |

| Privacy | Member register maintained internally | Not fully public, but board details filed with Fyrirtækjaskrá |

Focus Points

- Taxation: Subject to corporate income tax at 20%; VAT registration required if annual turnover exceeds the statutory threshold; no special cooperative tax exemption applies under general rules.

- Annual Compliance: Must hold an annual general meeting, file audited accounts with Ársreikningaskrá (the Register of Annual Accounts), and maintain updated bylaws.

- Economic Substance: No specific substance rules beyond maintaining a genuine registered address and operational governance structure within Iceland.

- Treaty Access: As a domestic legal entity, a Samvinnufélag can access Iceland's tax treaty network, subject to the relevant treaty's definition of a qualifying resident.

- Conversion: Conversion to another entity type is not straightforwardly provided for under Act No. 22/1991 and would generally require dissolution and re-incorporation.

Closing

A Samvinnufélag suits agriculture, fishing, retail, and housing sectors where members pool resources for collective economic benefit rather than external investor returns. The open membership structure offers operational flexibility, though the absence of a capital market mechanism makes it unsuitable for businesses seeking equity investment.

Best suited for member-driven industries such as agriculture, fisheries, or consumer retail where profit redistribution to members outweighs the need for external capital raising.

Partnerships (Ansvarleg Hlutafélag, Hlutafélag með Takmarkaðri Ábyrgð) [General Partnership, Limited Partnership]

Iceland general and limited partnership formation is governed by the Act on Private Limited Companies and Partnerships, with partnerships specifically regulated under the Law on Partnerships (Lög um sameignarfélög). These structures do not carry separate legal personality in the same sense as a limited company — partners share direct legal and financial exposure to the firm's obligations.

Two distinct forms exist. The Ansvarleg Hlutafélag (ANS) is a general partnership where all partners bear unlimited, joint, and several liability. The Hlutafélag með Takmarkaðri Ábyrgð (HLT) is a limited partnership, combining at least one general partner with unlimited liability alongside one or more limited partners whose exposure is capped at their contributed capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | ANS (General) / HLT (Limited) | Neither form carries full separate legal personality |

| Members | Partners (general and/or limited) | ANS: minimum 2 general partners; HLT: minimum 1 general + 1 limited partner |

| Liability | ANS: unlimited for all; HLT: general partner unlimited, limited partner capped | Limited partners must not participate in management |

| Local Presence | Registered address in Iceland required | No statutory resident agent requirement, but a local address must be on file with Fyrirtækjaskrá |

| Capital | No statutory minimum for either form | Contributions recorded in partnership agreement |

| Registration | Registered with Fyrirtækjaskrá (Companies Registry) | Partnership agreement must be submitted at registration |

Focus Points

- Taxation: Partnerships are fiscally transparent — income is allocated to partners and taxed at their applicable rates; VAT registration applies if annual turnover exceeds the statutory threshold; no corporate income tax at entity level.

- Annual Compliance: Annual accounts must be filed; general partners are personally responsible for submission obligations.

- Treaty Access: Fiscal transparency means the entity itself generally cannot claim double tax treaty benefits directly; access depends on the residency status of individual partners.

- Restrictions: Limited partners in an HLT are prohibited from managing the business; doing so may trigger reclassification to unlimited liability.

- Conversion: Conversion to a private limited company (ehf.) is possible but requires full re-registration and compliance with the Private Limited Companies Act.

Sub-Types

Ansvarleg Hlutafélag (ANS) — General Partnership

All partners carry unlimited personal liability, and each partner may bind the firm unless the partnership agreement restricts this. This structure is typically used by small professional practices or family-run businesses where partners maintain active operational control.

Hlutafélag með Takmarkaðri Ábyrgð (HLT) — Limited Partnership

The HLT separates management responsibility from passive investment — limited partners contribute capital without taking on management duties. This form suits arrangements where one party provides operational expertise and another provides funding.

Closing

Partnerships are most appropriate for closely held operations, professional services firms, or joint ventures where two or more parties wish to share profits directly without a corporate intermediary. The pass-through tax treatment is a material advantage, but unlimited personal liability for general partners remains a significant exposure that warrants careful consideration before adopting this structure.

Partnerships in Iceland are best suited for small professional firms or joint ventures where partners accept direct liability in exchange for operational simplicity and pass-through taxation.

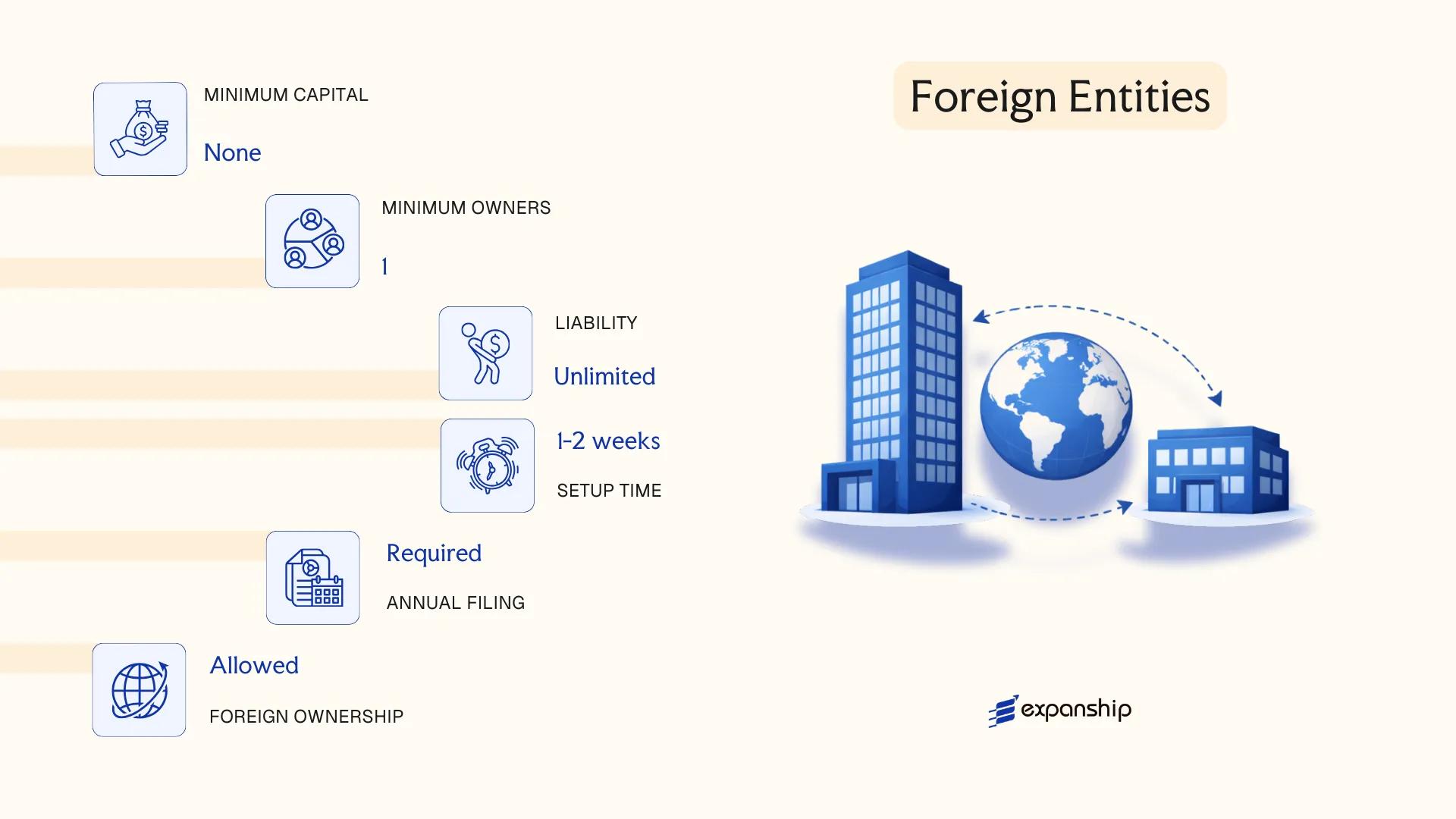

Foreign Entities (Branch Office, Representative Office) [Útibú, Tengiliðskrifstofa]

Opening a branch office in Iceland is governed by the Companies Act No. 2/1995, which sets out the registration obligations for foreign firms operating through a local presence. A branch (Útibú) is not a separate legal entity — it remains an extension of the parent company, which bears full liability for the branch's obligations.

A representative office (Tengiliðskrifstofa) occupies a more limited position. It may conduct market research or liaison activities but cannot generate revenue or enter into commercial contracts on behalf of the parent firm.

Key Characteristics

| Requirement | Branch (Útibú) | Representative Office (Tengiliðskrifstofa) |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Non-trading liaison structure; no legal personality |

| Registered Representative | Mandatory local representative resident in Iceland | Local contact required |

| Local Office | Physical registered address required | Registered address required |

| Capital Requirement | None prescribed; parent company capital applies | None |

| Commercial Activity | Permitted; subject to Icelandic tax obligations | Not permitted |

| Privacy | Parent company details publicly disclosed via Fyrirtækjaskrá (Company Registry) | Same disclosure obligations apply |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at 20%; VAT registration required if taxable turnover exceeds the statutory threshold; no separate withholding tax regime applies at branch level, though treaty access depends on the parent's residency.

- Economic Substance: The branch must demonstrate genuine operational activity in Iceland; substance requirements follow general Icelandic tax authority (Skatturinn) guidelines.

- Annual Compliance: Annual accounts of the parent must be filed with Fyrirtækjaskrá; the branch is also required to submit local financial statements where applicable.

- Treaty Access: Access to Iceland's tax treaty network is not guaranteed at branch level; treaty benefits flow through the parent entity's jurisdiction of residence.

- Restrictions: Representative offices are prohibited from invoicing, signing contracts, or conducting any revenue-generating activity.

Closing

A branch suits foreign companies seeking a direct commercial footprint without incorporating a separate subsidiary, though full parental liability exposure is a material drawback that warrants careful consideration before proceeding.

Foreign companies testing the Icelandic market or fulfilling specific contracts without committing to a standalone subsidiary structure.

Sole Proprietorship (Einstaklingsfyrirtæki)

An Iceland sole proprietorship (Einstaklingsfyrirtæki) setup is governed primarily by the Act on Private Enterprises (Lög um einstaklingsfyrirtæki) and general provisions within Icelandic commercial law. The structure carries no separate legal personality — the proprietor and the business are treated as a single legal entity, meaning personal assets are exposed to all business liabilities.

Self-employment registration in Iceland is handled through Skatturinn, the Icelandic Tax Authority, and Fyrirtækjaskrá, the Companies Registry. Registration is straightforward and does not require a minimum capital contribution, making this the most accessible commercial form for individual operators.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Einstaklingsfyrirtæki) | No separate legal personality from the proprietor |

| Member Type | Proprietor | Single individual only; no co-owners permitted |

| Local Presence | Registered address in Iceland required | Proprietor must be an Icelandic resident or EEA national |

| Capital | No minimum capital requirement | No share structure exists |

| Liability | Unlimited personal liability | Personal assets are fully exposed to business debts |

| Privacy | Name and registration details publicly recorded | No beneficial ownership filing separate from the proprietor's identity |

Focus Points

- Taxation: Sole traders are taxed under personal income tax rates (progressive, up to 46.25%), not corporate tax; VAT registration is mandatory once annual turnover exceeds ISK 2,000,000; no withholding tax applies at the entity level.

- Annual Compliance: Annual tax return filed with Skatturinn; no separate audited accounts required below defined revenue thresholds.

- Residency Restriction: The proprietor must generally be resident in Iceland or hold EEA/EEA-equivalent status; non-EEA nationals face significant access restrictions.

- Conversion: The structure can be converted into an Einkahlutafélag (ehf.) as business activity grows, though the conversion requires a formal incorporation process.

- Treaty Access: As a pass-through structure with no separate legal personality, access to Iceland's tax treaty network at the entity level is not available; treaty benefits flow through the individual proprietor's residence status.

Closing Paragraph

This structure suits freelancers, consultants, and small-scale traders operating with limited counterparty risk and low initial capital. The primary advantage is minimal administrative burden at formation; the clear limitation is unlimited personal liability, which makes it unsuitable for activities carrying material financial or legal exposure.

Best suited for Iceland-resident individuals testing a business concept or operating in low-risk, service-based sectors before committing to a formal corporate structure.

How to Choose the Right Entity Type in Iceland

Selecting the correct structure from the outset shapes your tax position, liability exposure, and regulatory obligations for the life of your business. Knowing how to choose the right company structure in Iceland requires examining several concrete variables before filing with Fyrirtækjaskrá (the Companies Registry).

Why Your Entity Choice Matters

The structure you register has direct legal and financial consequences:

- Operating as a branch (útibú) while conducting substantive independent trade may be treated as an undisclosed permanent establishment, exposing the entity to back taxes and penalties.

- Registering a cooperative (samvinnufélag) when treaty-based withholding tax relief is needed may disqualify you, as not all Icelandic entity types qualify equally under Iceland's double tax agreements.

- Selecting an einkahlutafélag (ehf.) subject to mandatory audit thresholds when your firm is a single-person consultancy imposes annual audit costs that would not apply under a sole proprietorship registration.

- Forming a limited liability company when a partnership structure would suffice introduces shareholder meeting obligations and capital maintenance rules that add ongoing administrative burden.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as financial services each point to a different permissible structure under Icelandic law.

- Ownership Structure: A sole founder with no co-investors can operate as an ehf., while multi-party ventures may require a shareholders' agreement enforced within an hf. framework.

- Tax Objectives: Your need for treaty network access, participation exemption eligibility, or a specific corporate tax rate should align with the entity form you select.

- Substance Capacity: If you cannot maintain a physical presence with decision-making authority in Iceland, certain entity types will trigger controlled foreign corporation or substance reporting concerns.

- Exit Strategy: Not all Icelandic entity types permit redomiciliation or conversion; verify that your chosen structure supports your intended exit mechanism before incorporating.

The Companies Act No. 2/1995 governs the formation and operation of limited liability companies and remains the primary legislative reference for structural decisions.

Compliance Services for Companies in Iceland

Maintain your Icelandic entity in good standing with ongoing compliance support covering annual filings, reporting obligations, and regulatory requirements.

Conclusion

Setting up a company in Iceland requires matching your operational and ownership structure to the correct legal form under Icelandic law. The einkahlutafélag (ehf.) remains the most registered entity type, favored by domestic operators and foreign investors alike for its limited liability and accessible minimum capital threshold. The hlutafélag (hf.) suits firms seeking public financing or exchange listing. Cooperatives serve member-driven enterprises, while general and limited partnerships fit smaller ventures where personal liability is acceptable. Branches and representative offices give foreign companies a regulated presence without separate legal personality. Sole proprietorships carry full personal liability, making them appropriate only for low-risk, owner-operated activity.

Administered through Fyrirtækjaskrá, the Companies Register, Iceland's registration framework has grown more structured over time, reflecting the country's OECD membership and its participation in the European Economic Area. Your choice of entity will shape everything from tax treatment to governance obligations.

How Expanship Can Assist You

Expanship Iceland company formation services cover the full arc of establishing a legal entity under Icelandic law — from selecting between an ehf. and hf. to filing with the Companies Registry (Fyrirtækjaskrá) at Skatturinn, Iceland's tax and registry authority. Every entity type discussed in this blog carries distinct registration requirements, and Expanship's team works through those specifics with you directly.

Our service scope spans each stage of the incorporation and compliance cycle:

- Document preparation and notarization

- Registered office and agent provision in Iceland

- Filing and liaison with Skatturinn

- Post-incorporation compliance management, including annual reporting obligations

- Banking introduction assistance with Icelandic financial institutions

Your business doesn't have to work through Icelandic bureaucracy from a distance. Reach out to Expanship Iceland to discuss how we can support your specific entity structure and timeline.

Frequently Asked Questions (FAQ)

The Einkahlutafélag (ehf.) is the most frequently incorporated structure. Its lower minimum share capital, single-shareholder eligibility, and limited liability make it the default choice for small and medium-sized businesses across most sectors.

Both structures are subject to corporate income tax under Icelandic law, but the Hlutafélag (hf.) carries a higher minimum share capital requirement and is permitted to offer shares to the public. An ehf. restricts share transfers and cannot list on a regulated exchange, while compliance obligations for the hf. are notably more extensive, including mandatory auditor appointments regardless of size.

Einkahlutafélag ownership information is registered with Fyrirtækjaskrá (the Companies Registry), so beneficial ownership is not entirely private. Nominee director arrangements are not prohibited under Icelandic law, though the actual beneficial owner must still be disclosed to authorities under anti-money-laundering requirements.

A single individual can form an ehf. A general partnership (Ansvarleg Hlutafélag) requires at least two partners, and a cooperative (Samvinnufélag) requires a minimum number of founding members. The hf. can technically be formed by one shareholder, though governance requirements are more demanding.

Non-residents may register an ehf., hf., or establish a branch office (Útibú) without being Icelandic citizens. A branch must have a locally registered representative, and all foreign-owned entities must register with Skatturinn (the Directorate of Internal Revenue) for tax purposes. There are no general nationality restrictions on share ownership.

Conversion from an ehf. to an hf. is permitted under the Companies Act (Lög um einkahlutafélög and Lög um hlutafélög), typically requiring a shareholder resolution and updated registration with Fyrirtækjaskrá. Conversion between entirely different legal forms, such as from a partnership to a limited company, generally requires dissolution and re-incorporation rather than a direct continuation.

The ehf., hf., and cooperative each have distinct legal personality, meaning they can contract, own assets, and incur liabilities independently of their members. A general partnership does not have separate legal personality in the same sense; partners remain personally liable for obligations of the firm. A sole proprietorship (Einstaklingsfyrirtæki) carries no separation between the owner and the business at all.

The sole proprietorship carries the lightest compliance burden, with no annual accounts submission to Fyrirtækjaskrá and no share capital obligations. However, the absence of limited liability means the owner's personal assets remain fully exposed to business creditors, which is a significant structural trade-off for businesses carrying any meaningful commercial risk.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.