Key Takeaways

- The Isle of Man Companies Registry, operating under the Department for Enterprise, administers all business structures formed under Isle of Man legislation, including entities governed by the Companies Act 2006 and the Limited Liability Companies Act 1996.

- Among available structures, the private limited company under the Companies Act 2006 is the most commonly incorporated entity on the island and suits the broadest range of commercial operations.

- The LLC under the Limited Liability Companies Act 1996 offers flexible membership arrangements without share capital, distinguishing it from the standard limited company structure.

- Compliance frameworks in the Isle of Man continue to be refined in line with OECD standards, directly affecting how internationally mobile businesses evaluate the jurisdiction for holding and operational structures.

Introduction to Entity Types in Isle of Man

Situated in the Irish Sea between Great Britain and Ireland, the Isle of Man is a self-governing Crown Dependency of the British Crown. It operates its own parliament, Tynwald, and maintains independent legislative authority over taxation and company law — though it is not part of the United Kingdom or the European Union.

Company registration is administered by the Isle of Man Companies Registry, which operates under the Department for Enterprise. The Registry maintains records for all business structures formed under Isle of Man legislation and is the primary point of contact for incorporation filings and statutory compliance.

The jurisdiction applies a zero rate of corporate income tax for most businesses, which shapes its appeal as a location for international structuring.

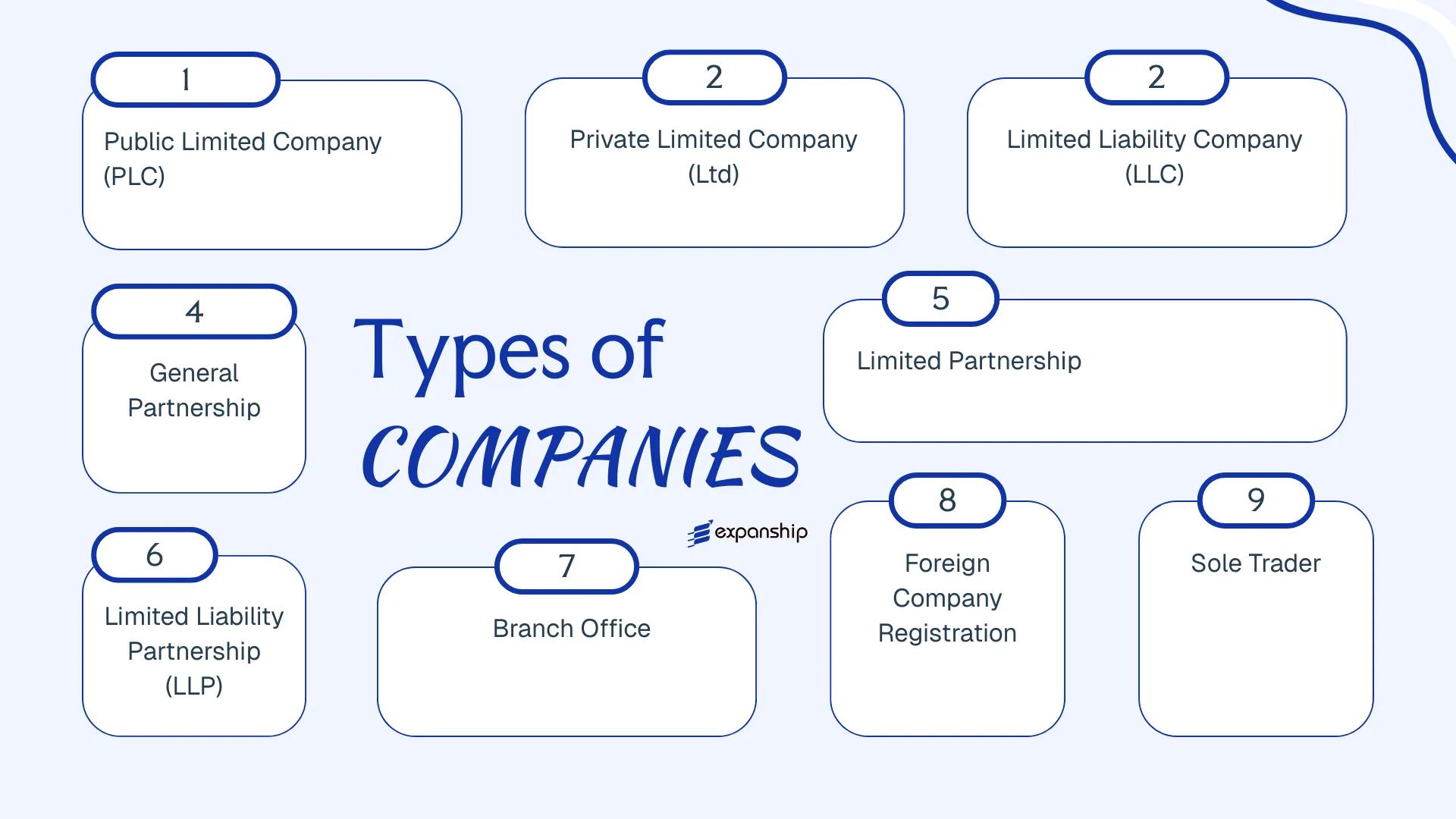

Available Isle of Man business entity types include the Public Limited Company (PLC), Private Limited Company (Ltd), Limited Liability Company (LLC), General Partnership, Limited Partnership, Limited Liability Partnership, Branch Office, Foreign Company registration, and Sole Trader. Each is governed by distinct legislation — among them the Companies Act 2006 and the Limited Liability Companies Act 1996. This article examines each of these Isle of Man company structures in turn.

An Overview of Business Structures in Isle of Man

Several distinct entity types are available under the jurisdiction's company law framework, governed primarily by the Companies Act 2006, the Limited Liability Companies Act 1996, and the Limited Partnerships Act 1909, among other statutes. Each structure carries different implications for liability, taxation, membership, and permitted activity. The sections that follow examine each in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (PLC) | Incorporated company | Limited to shares | 0% corporate tax | Permitted | 2 shareholders | Companies Registry | Companies Act 2006 |

| Private Limited Company (Ltd) | Incorporated company | Limited to shares | 0% corporate tax | Permitted | 1 shareholder | Companies Registry | Companies Act 2006 |

| Limited Liability Company (LLC) | Hybrid entity | Members not liable | 0% corporate tax | Permitted | 1 member | Companies Registry | LLC Act 1996 |

| General Partnership | Unincorporated firm | Unlimited | Taxed at partner level | Permitted | 2 partners | Income Tax Division | Partnership Act 1909 |

| Limited Partnership (LP) | Unincorporated firm | Mixed (general/limited) | Taxed at partner level | Permitted | 2 partners | Companies Registry | Limited Partnerships Act 1909 |

| Limited Liability Partnership (LLP) | Incorporated body | Limited | Taxed at member level | Permitted | 2 members | Companies Registry | Limited Liability Companies Act 1996 |

| Branch Office | Foreign entity extension | Parent liable | Dependent on parent | Permitted | N/A | Companies Registry | Companies Act 2006 |

| Sole Trader | Unincorporated individual | Unlimited | Personal income tax | Permitted | 1 person | Income Tax Division | General law |

Each of these structures is examined in full in the sections below.

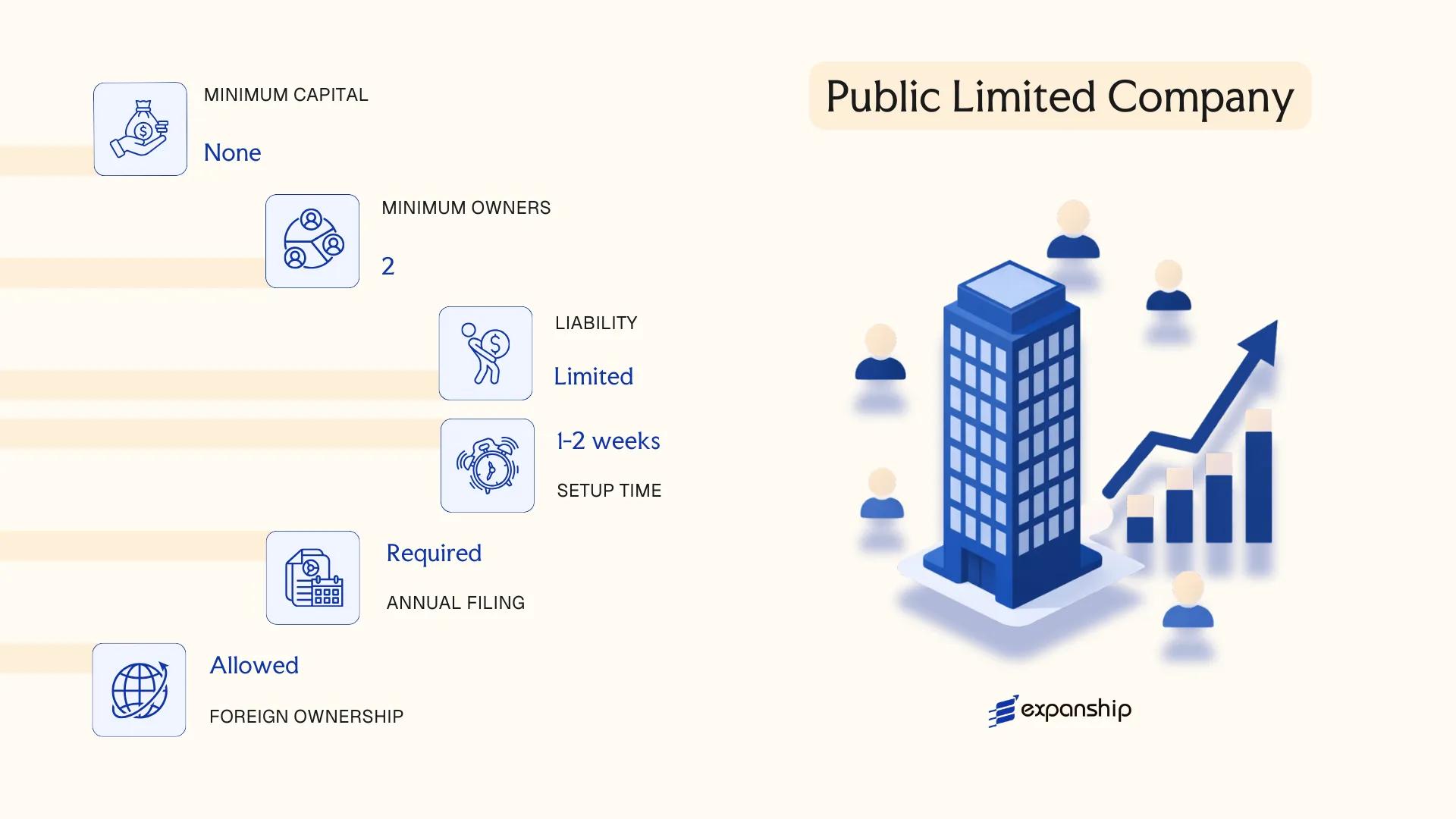

Public Limited Company (PLC) Under the Companies Act 2006

Governed by the Isle of Man PLC Companies Act 2006, the public limited company is a distinct legal entity capable of holding assets, entering contracts, and incurring liabilities in its own name. Shareholders' exposure is confined to the amount unpaid on their shares.

Formed primarily for access to public capital markets, a PLC may offer its shares to the public and seek admission to a recognised stock exchange. The Isle of Man Financial Services Authority (IOMFSA) oversees the regulatory framework within which these entities operate.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Separate legal personality; limited liability |

| Members | Shareholders (min. 2, no maximum) | At least 1 director required; corporate directors permitted |

| Local Presence | Registered office in Isle of Man | No mandatory local director, but a registered agent is standard practice |

| Share Capital | Minimum authorised share capital of £2,000 | Shares may be denominated in any currency |

| Privacy | Director and shareholder details filed at Companies Registry | Register is publicly accessible |

Focus Points

- Taxation: Subject to standard Isle of Man corporate income tax at 0% for most income; banking and retail activities taxed at 10%; no capital gains tax, inheritance tax, or withholding tax on dividends.

- Economic Substance: Trading and holding PLCs must satisfy economic substance requirements under the Income Tax Act 1970 (as amended).

- Annual Compliance: Annual return and audited financial statements required; audit obligation is mandatory for PLCs regardless of size.

- Treaty Access: Isle of Man has a limited double tax agreement network; PLCs may benefit from applicable arrangements with the UK and certain other jurisdictions.

- Conversion: A PLC may be re-registered as a private company under the Companies Act 2006 by passing a special resolution and satisfying statutory conditions.

Closing

A PLC suits businesses seeking public investment, exchange-listed vehicles, or large-scale capital raises. The mandatory audit requirement and public disclosure obligations make it a structurally heavier option compared to private alternatives.

Best suited for businesses intending to list on a recognised stock exchange or raise capital from the general public.

Company Incorporation in Isle of Man

Incorporate a PLC or other entity type in Isle of Man with end-to-end support from Expanship.

Private Limited Company (Ltd) Under the Companies Act 2006

The Isle of Man private limited company (Ltd) is governed by the Companies Act 2006, which introduced a modernised framework distinct from the older Companies Acts of 1931 and 1992. As a separate legal entity, the company holds rights and obligations in its own name, and members' liability is confined to any unpaid amount on their shares.

Incorporated under the 2006 Act, this structure supports both trading and holding arrangements. The Registrar of Companies, operating under the Department for Enterprise, oversees Isle of Man Ltd company registration and ongoing filing obligations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate with limited liability by shares | Separate legal personality from its members |

| Members | Shareholders: minimum 1, no maximum | Corporate shareholders are permitted |

| Directors | Minimum 1; no residency requirement under the 2006 Act | No upper limit; corporate directors are allowed |

| Local Presence | Registered office address on the Island required; no mandatory local director | Registered agent not mandated but commonly used in practice |

| Share Capital | No minimum capital requirement; shares can be in any currency | No-par-value shares are permitted under the 2006 Act |

| Privacy | Shareholder and director details are filed with the Registrar and are publicly accessible | Beneficial ownership held on a non-public central register |

Focus Points

- Taxation: Isle of Man companies are subject to a 0% standard corporate income tax rate; a 10% rate applies to income from Manx land and property and certain retail activities. No capital gains tax, inheritance tax, or withholding tax on dividends. VAT registration may be required for Isle of Man-sourced trading activity.

- Economic Substance: Companies engaged in relevant sectors (banking, insurance, fund management, shipping, holding, IP, and others) must satisfy substance requirements under the Income Tax (Substance Requirements) (Implementation) Order 2018.

- Annual Compliance: Annual return and confirmation statement filings are required; financial statements must be prepared, though audit requirements vary by company size and activity.

- Treaty Access: The Island's tax agreements are limited; access to full double tax treaty networks is not available, which affects cross-border structures reliant on treaty relief.

- Conversion: A company incorporated under the 2006 Act can re-register under the 1931 Act framework and vice versa, subject to prescribed procedures with the Registrar.

Closing Paragraph

The private limited company under the 2006 Act suits holding structures, IP ownership, and active trading businesses that benefit from a modern, flexible statutory framework. The absence of minimum capital requirements lowers the barrier to incorporation, though limited treaty access constrains its utility for certain international tax planning arrangements.

This entity suits founders and corporate groups seeking a flexible, low-cost structure for trading, holding, or asset ownership with straightforward compliance obligations.

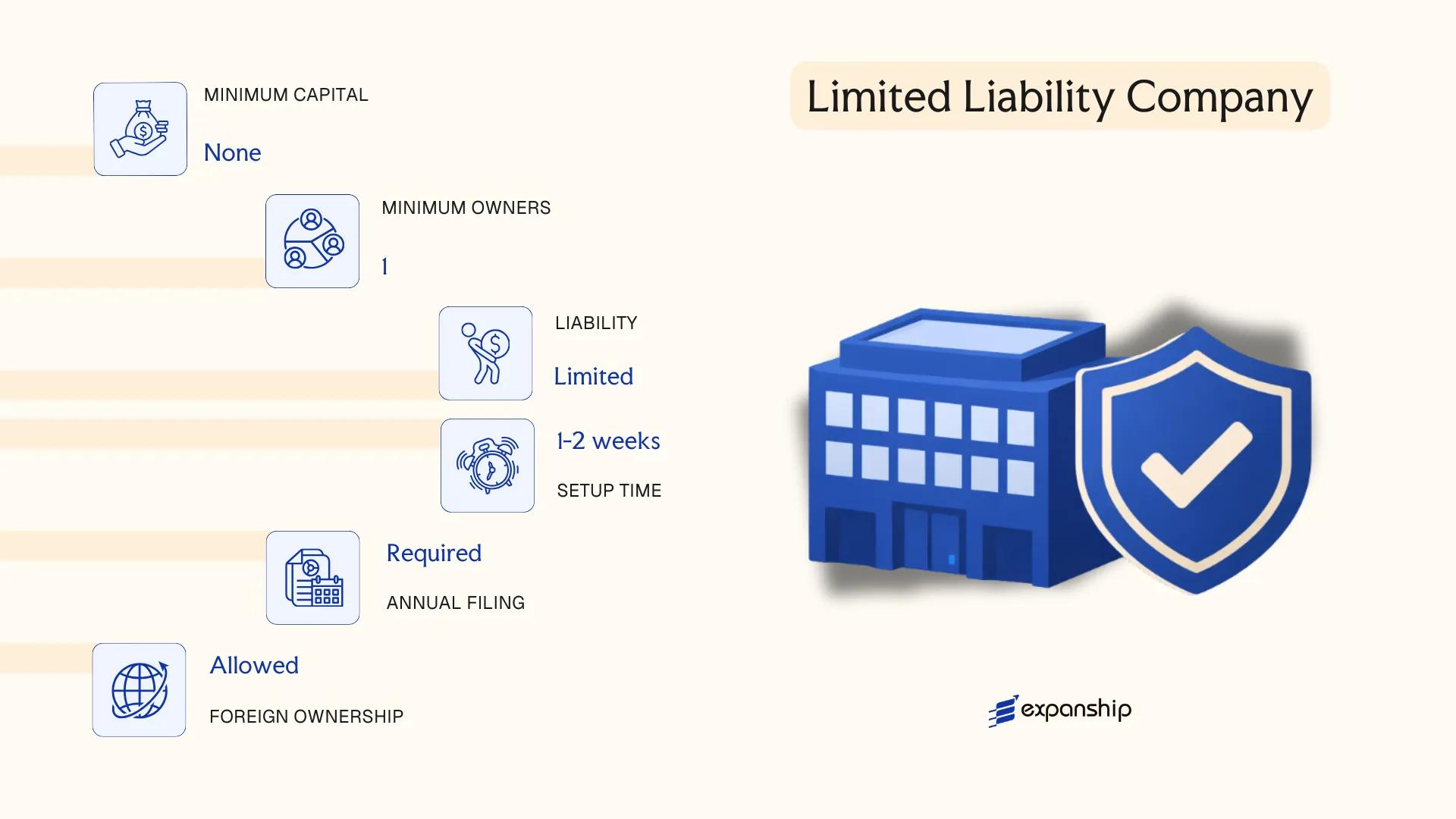

Limited Liability Company (LLC) Under the Limited Liability Companies Act 1996

The Isle of Man LLC formation 1996 Act framework established a structure that blends elements of a partnership with the liability protections of a corporate body. Governed by the Limited Liability Companies Act 1996, this entity holds separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name.

Unlike a company formed under the Companies Acts, an LLC is member-managed or manager-managed by default, and its internal governance is largely determined by an operating agreement rather than statutory articles. This contractual flexibility makes it a hybrid structure suited to joint ventures and fund vehicles.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (LLC) | Governed by the Limited Liability Companies Act 1996 |

| Members / Management | Members and/or appointed Managers | Minimum 1 member; no maximum; can be managed by members or designated managers |

| Local Presence | Registered Agent required | Registered Agent must be a person resident in the Isle of Man or an authorised body |

| Capital | No minimum capital requirement; USD or other currencies permitted | No par value requirement; contributions can be cash, property, or services |

| Privacy | Members not on public register | Manager names may appear depending on filing obligations |

Focus Points

- Taxation: LLCs are generally treated as tax-transparent for Isle of Man income tax purposes, though members' individual tax positions depend on their residence; no VAT registration requirement arises from the structure alone; no withholding tax on distributions.

- Economic Substance: If the LLC conducts relevant activities as defined under the Income Tax Act 1970 (as amended), substance obligations apply regardless of member residency.

- Annual Compliance: Annual return filing with the Isle of Man Companies Registry is required; failure to file can result in striking off.

- Treaty Access: As a pass-through entity, the LLC itself generally cannot access double tax agreements; treaty relief, if any, must be assessed at member level.

- Conversion: An LLC may be converted to another entity type or continued to or from another jurisdiction under the applicable provisions of the 1996 Act.

Closing Paragraph

An Isle of Man limited liability company is commonly used for joint ventures, collective investment structures, and asset holding arrangements where contractual flexibility over governance is a priority. The absence of minimum capital and the pass-through tax treatment are practical features, though the structure's limited international recognition outside common law jurisdictions can restrict its utility for cross-border trading operations.

This entity suits sophisticated investors, fund managers, and joint venture partners seeking flexible governance and tax transparency without the formality of a standard corporate structure.

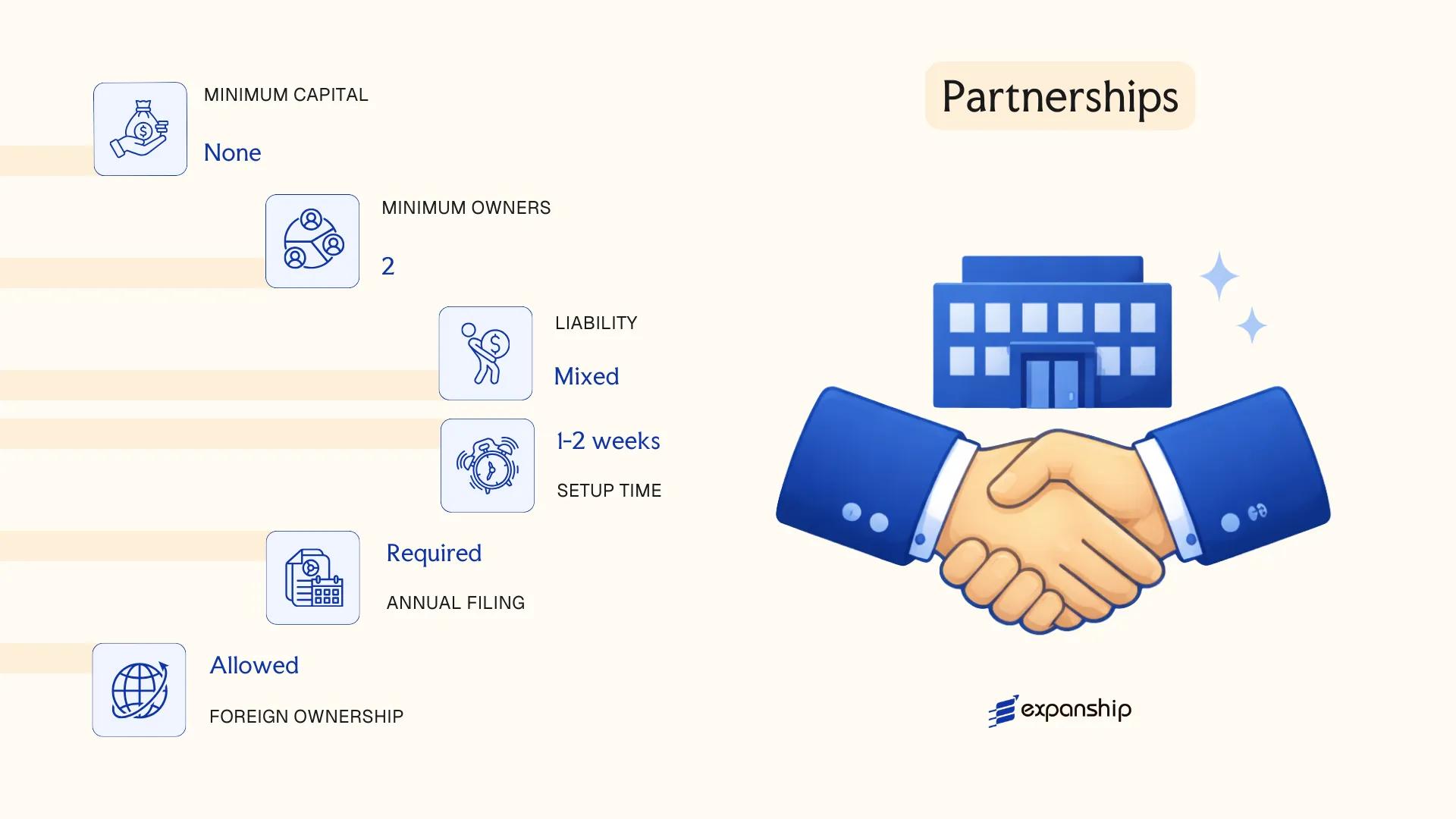

Partnerships [General Partnership, Limited Partnership, Limited Liability Partnership]

Isle of Man partnership structures are governed by several distinct statutes depending on the form chosen. The Partnership Act 1909 covers general partnerships, the Limited Partnerships Act 1909 governs limited partnerships, and the Limited Liability Partnerships Act 2004 provides the framework for LLPs.

Each form carries different liability and governance implications. General partnerships offer no liability protection, while limited partnerships and LLPs introduce partial or full liability separation for qualifying partners.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | GP: unincorporated; LP: unincorporated; LLP: incorporated body | Only the LLP has separate legal personality |

| Members | Partners (general/limited) | GP: min. 2, no statutory max; LP: min. 1 general + 1 limited partner; LLP: min. 2 designated members |

| Local Presence | Registered address required; LLPs must have a registered office on-island | LPs must be registered with the Isle of Man Companies Registry |

| Capital | No statutory minimum for any form; contributions in any agreed currency | LP limited partners' liability capped at capital contributed |

| Privacy | Partnership agreements are private; LLP incorporation documents are on public record | Beneficial ownership subject to reporting requirements |

Focus Points

- Taxation: Partnerships are generally tax-transparent; partners taxed individually on their share of profits. LLPs may be subject to the standard 0% corporate income tax rate if structured appropriately. No VAT registration requirement unless trading thresholds are met.

- Economic Substance: LLPs conducting relevant activities must satisfy substance requirements under the Income Tax (Substance Requirements) (Implementation) Regulations 2019.

- Annual Compliance: LLPs must file an annual return with the Companies Registry; general and limited partnerships have comparatively lighter filing obligations.

- Treaty Access: Partnerships generally do not independently access double tax agreements; treaty benefits depend on the residence status of individual partners.

- Restrictions: Limited partners in an LP forfeit liability protection if they participate in management of the business.

Sub-Types

General Partnership

Formed by agreement between two or more persons carrying on business in common with a view to profit. No registration is required, though the business name may need to be disclosed under the Business Names Registration Act 2012.

Limited Partnership

Requires at least one general partner with unlimited liability and one limited partner whose exposure is capped at their capital contribution. Registration with the Companies Registry is mandatory for LP formation.

Limited Liability Partnership

A corporate body with separate legal personality, offering members protection from personal liability for business debts. Commonly used for professional services firms.

Closing

Partnerships are suited to joint ventures, professional practices, and investment structures where pass-through taxation is a priority. The LLP's separate legal personality offers a meaningful structural advantage, though compliance obligations for LLPs are heavier than those of general or limited partnerships.

LLPs are well-suited to professional services firms and fund structures seeking liability protection with tax transparency; general and limited partnerships suit smaller joint ventures where simplified administration is preferred.

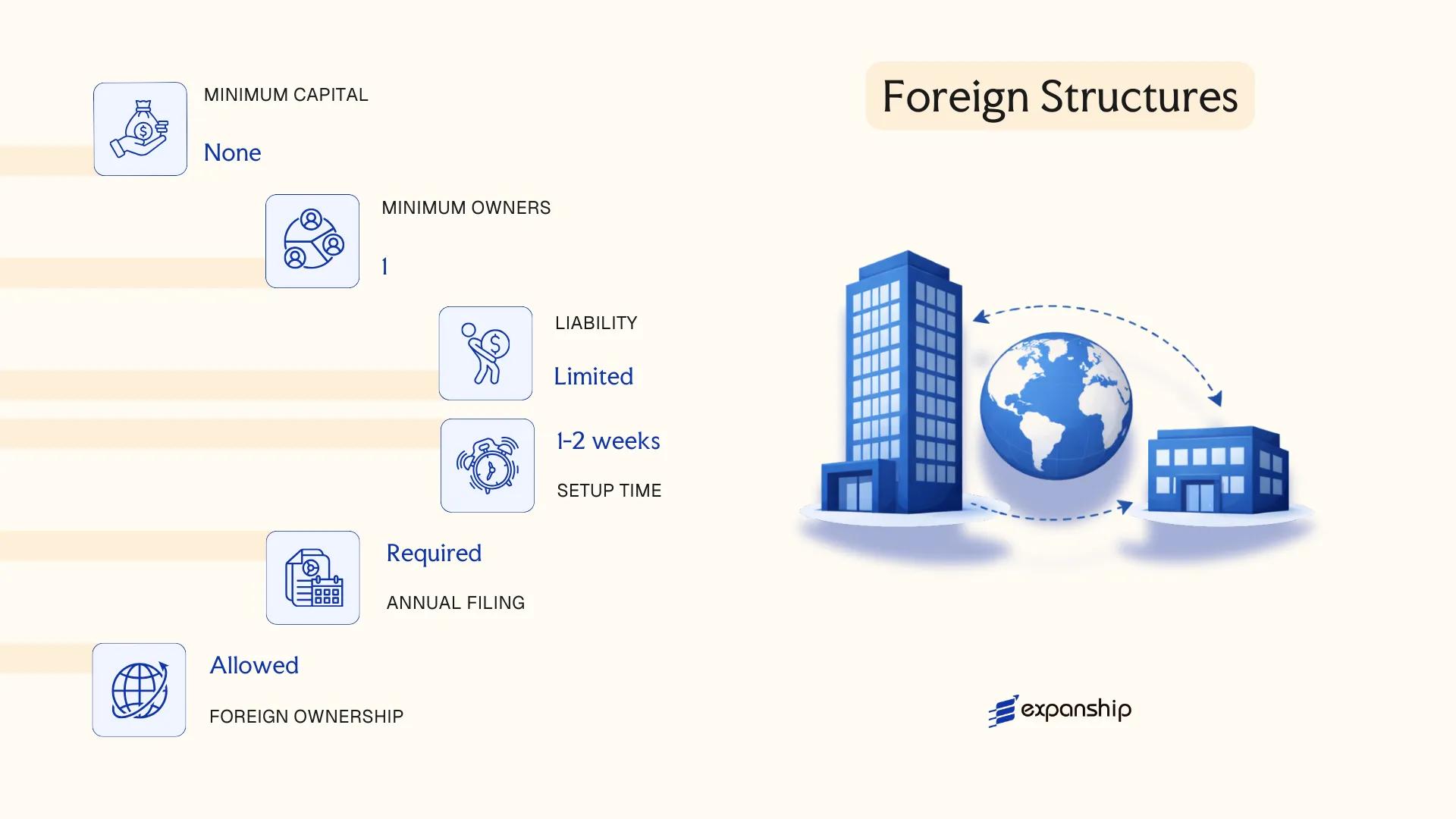

Foreign Structures [Branch Office, Foreign Company Registration]

Foreign businesses seeking a presence on the island without incorporating a new local entity have two primary routes: registering a branch office or registering as a foreign company. Both options are governed by Part XI of the Companies Acts 1931–2004, which applies to overseas companies establishing a place of business within the jurisdiction. Neither structure creates a separate legal entity — the parent company retains full liability for the branch's obligations.

Isle of Man foreign company registration requires the overseas entity to file prescribed particulars with the Companies Registry, including its constitutional documents, details of directors, and the name and address of a local agent authorised to accept service of process.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch / registered place of business | Not a separate legal entity; parent company bears full liability |

| Local Representative | Authorised agent required | Must have a registered address in the Isle of Man for service of process |

| Filing Obligations | Certified copy of constitutional documents and director details | Submitted to the Isle of Man Companies Registry |

| Capital | No minimum capital requirement | Parent company's capital structure applies |

| Registered Name | Must reflect overseas company name | Disclosures required on correspondence and business premises |

| Privacy | Director and agent details on public record | Parent company's home-jurisdiction filings may also be accessible |

Focus Points

- Taxation: The branch is subject to the standard 0% corporate income tax rate on most income; however, banking and retail activities may attract the 10% rate, and land/property income is taxed at 20%. No branch remittance tax applies, but VAT registration may be required depending on turnover.

- Economic Substance: Trading activities conducted through a branch may trigger economic substance obligations under the Income Tax Act 2015 if they fall within a relevant sector.

- Annual Compliance: Annual returns and updated particulars must be filed with the Companies Registry; changes to the parent's structure must be reported promptly.

- Treaty Access: The branch accesses tax treaties through the parent company's home jurisdiction, not independently.

- Restrictions: Certain regulated activities require separate licensing from the Isle of Man Financial Services Authority, regardless of branch status.

Closing Paragraph

A branch or foreign company registration suits businesses that want operational presence without the administrative overhead of a standalone local entity, though the absence of liability separation is a material drawback for risk-sensitive operations.

Established overseas companies testing the Isle of Man market or fulfilling a specific contract, where full local incorporation is not yet justified.

Sole Trader

Isle of Man sole trader registration does not create a separate legal entity. You and the business are legally the same person, which means personal assets are fully exposed to any business liabilities. No governing statute establishes a distinct sole trader structure; the arrangement operates under general common law principles, with registration requirements set by the Income Tax Division of the Isle of Man Government.

There is no incorporation process. Operating as a self-employed Isle of Man resident requires registration with the Income Tax Division for income tax and National Insurance purposes, typically before or shortly after commencing trade.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated; no separate legal personality | Owner and business are one legal person |

| Referred To As | Sole proprietor / sole trader | No formal designation under statute |

| Ownership | Single individual only | Cannot have co-owners; no members, shareholders, or partners |

| Local Presence | No registered office requirement | A trading address is advisable for correspondence |

| Capital | No minimum capital requirement | Funded entirely by the proprietor |

| Privacy | Business name and owner identity may appear on public records if trading under a name other than the proprietor's own | Business Names Registration Act 1918 may apply |

Focus Points

- Taxation: Income is assessed under personal income tax at Isle of Man rates (up to 20%); no separate corporate tax applies, and Class 2/Class 4 National Insurance contributions are payable; no VAT registration required below the current threshold.

- Annual Compliance: Annual income tax return filing with the Income Tax Division; no separate corporate filing or annual return to the Companies Registry.

- Conversion: Can convert to a limited company at any time, though assets and liabilities must be formally transferred as there is no statutory conversion mechanism.

- Treaty Access: No access to double tax treaties as a business structure; treaty benefits apply only to the individual proprietor where applicable.

- Restrictions: Cannot raise equity investment or issue shares; unsuitable for businesses with significant liability exposure.

Recommendations

A sole trader structure suits individuals providing services or running small-scale trade operations where administrative simplicity outweighs the need for liability protection. The absence of incorporation costs and filing obligations is a practical advantage, but the unlimited personal liability is a material drawback for any business carrying financial or legal risk.

Freelancers, consultants, and sole proprietors Isle of Man residents testing a new business concept before committing to formal incorporation.

How to Choose the Right Entity Type in Isle of Man

Choosing the right company structure in Isle of Man has direct legal and financial consequences — the wrong choice is not simply inefficient, it can result in regulatory breach, unexpected tax exposure, or structural obligations that don't match your actual operations.

Why Your Entity Choice Matters

- Registering an offshore entity while trading locally places the business in breach of the Companies Act 2006, which can result in striking off or financial penalties.

- Choosing a tax-exempt structure eliminates access to any double tax arrangement benefits, meaning withholding taxes levied by counterpart countries cannot be reduced or reclaimed.

- Selecting an entity without adequate substance capacity, where substance requirements apply, triggers reporting failures and potential penalties under the Income Tax Act 1970 and associated regulations.

- Forming a standard company when estate planning or asset protection is the primary goal imposes annual shareholder obligations and statutory filing requirements that a trust or foundation structure would not.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as funds or insurance each point to a distinct structure under Isle of Man law.

- Local vs. Offshore Operations: A firm transacting with Isle of Man residents faces different registration requirements than one operating entirely outside the jurisdiction.

- Ownership and Management: Single-owner businesses and multi-party arrangements have different governance needs, with LLCs and partnerships offering more flexibility than a statutory company board.

- Tax Objectives: Your need for full tax exemption, participation in a specific regime, or access to treaty networks will narrow your structural options significantly.

- Substance Capacity: If maintaining local employees, office space, and management decision-making is not feasible, the entity type must reflect that constraint.

- Exit Strategy: Not all structures permit redomiciliation or conversion; confirm that your chosen entity supports your intended exit mechanism before formation.

Compliance Services for Companies in Isle of Man

Maintain good standing and meet statutory obligations across annual filings, economic substance, and regulatory reporting requirements.

Conclusion

Each entity type registered under Isle of Man law serves a distinct purpose. The private limited company under the Companies Act 2006 suits the broadest range of commercial operations, and it remains the most commonly incorporated structure on the island. The LLC under the Limited Liability Companies Act 1996 appeals to those requiring flexible membership arrangements without share capital. PLCs are reserved for businesses seeking public investment, while partnerships accommodate professional service structures where personal liability is accepted or managed. Branches and foreign company registrations serve groups extending an existing legal presence.

Measured against its regulatory history, the jurisdiction continues to refine its compliance frameworks in line with OECD standards, which shapes how internationally mobile businesses assess its suitability for holding and operational structures. Your choice of entity will ultimately depend on ownership requirements, intended activity, and how the structure interacts with your home jurisdiction's tax rules. Expanship can help you assess these factors with precision.

How Expanship Can Assist You

Expanship's Isle of Man company formation services cover the full range of entities discussed in this guide — from a Private Limited Company under the Companies Act 2006 to an LLC formed under the Limited Liability Companies Act 1996. Every structure carries distinct filing obligations with the Isle of Man Companies Registry, and getting those right from the outset matters.

Your business will have dedicated support across each stage of the process:

- Document preparation and notarization

- Registered agent and registered office provision

- Filing and liaison with the Isle of Man Companies Registry

- Post-incorporation compliance management

- Banking introduction assistance

Expanship's Isle of Man registration support extends beyond incorporation. Ongoing obligations — annual returns, director updates, and regulatory correspondence — are handled so your entity stays in good standing.

Reach out to Expanship Isle of Man to discuss which structure fits your goals.

Frequently Asked Questions (FAQ)

The private limited company incorporated under the Companies Act 2006 is the most frequently registered structure. Its combination of limited liability, flexible share capital rules, and suitability for both local and international operations makes it the default choice across a wide range of commercial activities.

An LLC formed under the Limited Liability Companies Act 1996 is a hybrid structure that combines contractual flexibility with limited liability, and it does not issue shares. A private limited company under the Companies Act 2006 operates through a share capital framework with formal director and shareholder roles. Both structures are subject to Isle of Man tax residency rules, but their internal governance documents and profit-distribution mechanisms differ substantially.

The LLC under the 1996 Act generally offers a higher degree of privacy, as member and manager details are governed through the members' agreement rather than fully public filings. Beneficial ownership information is held by the Isle of Man Financial Services Authority under the Beneficial Ownership Act 2017 but is not publicly accessible. Nominee arrangements are available for both LLCs and limited companies through licensed corporate service providers.

A private limited company under the Companies Act 2006 can be formed by one shareholder and one director, who may be the same person. Partnerships, whether general, limited, or limited liability, require a minimum of two partners by definition. A sole trader carries no formation minimum, while an LLC requires at least one member but may also be formed by a single individual.

All principal entity types, including the private limited company, LLC, limited partnership, and limited liability partnership, are accessible to non-residents and foreign nationals. There is no statutory requirement for local shareholding or residency in most structures, though regulated activities require licensing from the Isle of Man Financial Services Authority regardless of the founder's nationality.

The Companies Act 2006 includes provisions allowing certain re-registration procedures, such as converting between company forms. Conversion between fundamentally different structures, such as from a partnership to a limited company, generally requires dissolution and fresh incorporation rather than a direct statutory conversion. You should confirm the applicable procedure with a licensed Isle of Man corporate service provider before initiating any restructuring.

A private limited company, public limited company, and LLC each carry separate legal personality distinct from their members or shareholders. General partnerships do not possess separate legal personality under Isle of Man law, meaning partners bear direct liability for partnership obligations. Limited partnerships and LLPs occupy intermediate positions, with LLPs holding separate legal personality under the Limited Liability Partnerships Act 1996.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.