Key Takeaways

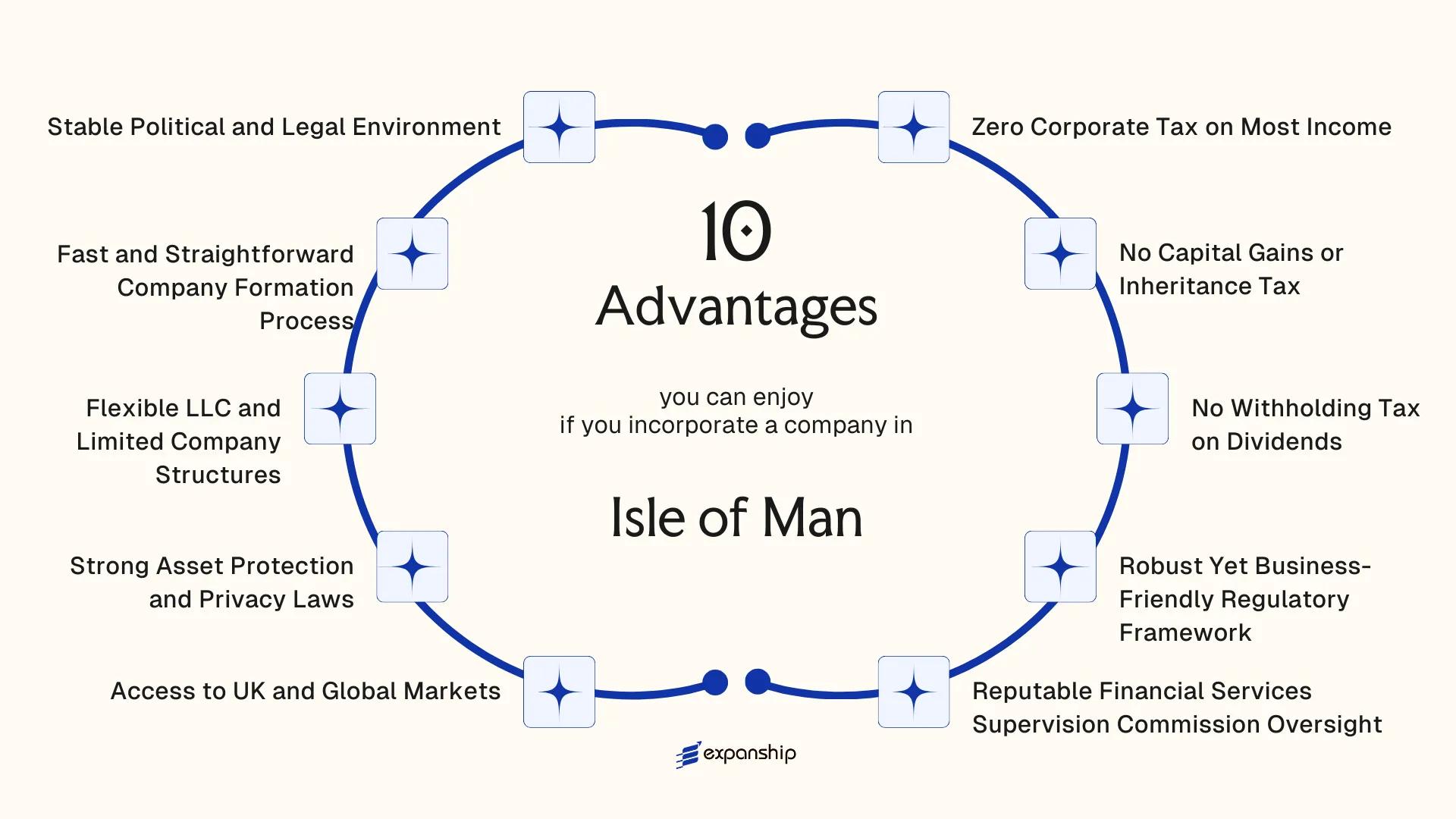

- The Isle of Man's zero percent corporate tax rate on most income categories, combined with the complete absence of capital gains, inheritance, and withholding taxes, creates a compounding tax efficiency that few jurisdictions can match within a single framework.

- Businesses subject to financial licensing operate under the Regulated Activities Order 2011, administered by the Financial Services Authority, giving regulated entities a compliance structure that international counterparties and banking partners treat as credible rather than opaque.

- Foreign nationals face no material ownership or directorship restrictions under Isle of Man company law, making the Companies Registry accessible to international investors without the nominee structures that other offshore jurisdictions often require.

- Unlike many low-tax territories that carry reputational risk with institutional banks and trading partners, the Isle of Man's regulatory standing allows businesses to combine tax efficiency with the kind of jurisdictional legitimacy that supports cross-border commercial relationships.

The benefits of incorporating in Isle of Man draw the attention of business owners across a wide range of industries, from financial services to technology. Situated in the Irish Sea between Great Britain and Ireland, the Isle of Man is a self-governing Crown Dependency — not part of the United Kingdom, though closely connected to it through constitutional ties. Company registration falls under the oversight of the Companies Registry, which operates within the Isle of Man Government's Department for Enterprise.

Foreign nationals face no material restrictions on owning or directing a business registered here, making the jurisdiction accessible to international investors. The private limited company remains the most common vehicle through which overseas businesses establish a presence on the island. From a tax perspective, the territory operates a predominantly zero-tax regime on most categories of income.

This article examines the principal advantages that Isle of Man company formation offers to businesses considering establishing or expanding their corporate structure in this jurisdiction.

Zero Corporate Tax on Most Income

The Isle of Man zero corporate tax advantage stems from a deliberate legislative position, not a temporary incentive or treaty arrangement. Under the Income Tax Act 1970 (as amended), the standard corporate income tax rate is 0% for the vast majority of trading and investment income.

What the 0% Rate Actually Covers

Resident companies conducting general trading, holding investments, or providing services outside of specifically carved-out sectors pay no corporate income tax on those profits. This means retained earnings remain whole, giving your business a structurally lower cost of operation compared to jurisdictions applying standard rates of 19% to 25% or higher.

Where Exceptions Apply

A 10% rate applies to income derived from Manx land and property, and to licensed banking business. Isle of Man tax-free income for companies therefore covers most commercial structures that foreign investors typically establish, including holding entities and international trading firms. The 0% rate is not a temporary measure subject to political revision but is embedded in the island's core tax legislation, which provides your business with reliable, long-term planning certainty.

Profits generated outside banking and Manx property activity leave your company subject to zero corporate income tax under current Manx law.

No Capital Gains or Inheritance Tax

No capital gains tax Isle of Man companies are subject to is a structural feature of the territory's tax code, not a temporary relief or a rate concession. Capital gains are simply outside the charge to tax. For investors holding appreciated assets within a Manx structure, this means disposals of shares, property, or other capital assets generate no additional tax liability at the entity level.

Inherited wealth held through Isle of Man structures benefits from the same logic. There is no inheritance tax or equivalent estate duty imposed on assets passing between individuals or through corporate arrangements under Manx law. Families and high-net-worth individuals using the territory for succession planning retain the full value of transferred assets rather than surrendering a portion to a government levy.

These exemptions apply consistently across standard corporate forms, including companies incorporated under the Companies Act 2006 (Isle of Man). A few practical reasons this framework works in your favour:

- Gains realised on exit are not eroded by a tax charge that would otherwise reduce returns to shareholders

- Estate planning structures do not require complex workarounds to neutralise inheritance exposure

- No capital gains calculation, filing, or deferral mechanism is required, reducing compliance overhead

Incorporate a Company in the Isle of Man

Set up a Manx company with no capital gains or inheritance tax obligations. Expanship manages the full incorporation process across all required filings.

No Withholding Tax on Dividends

Distributed profits leaving an Isle of Man company carry no withholding tax deduction at source. This means shareholders resident abroad receive their full dividend without any portion retained by the paying entity on behalf of local tax authorities. For foreign investors extracting returns from a trading or holding company, this directly increases the net amount received compared to jurisdictions that impose source-country deductions.

Most European Union member states apply dividend withholding tax rates between 15% and 26% at the corporate level before treaty relief. Your company registered on the island faces no such obligation, regardless of where the recipient shareholder is based or how large the distribution is.

| Feature | Detail |

|---|---|

| Withholding tax rate on dividends | 0% |

| Applies to non-resident shareholders | Yes |

| Applies to corporate shareholders | Yes |

| Minimum shareholding threshold required | None |

| Governing income tax framework | Income Tax Act 1970 (as amended) |

Under the Income Tax Act 1970, as subsequently amended, no statutory mechanism exists requiring an Isle of Man company to withhold tax on dividend payments. This is a structural feature of the tax code, not a conditional exemption that requires pre-approval or a minimum ownership stake to activate.

For holding structures where a parent company in another jurisdiction receives periodic distributions from a subsidiary, the absence of source-level deduction simplifies treasury operations and removes the administrative burden of reclaim procedures that otherwise arise under standard withholding regimes.

Robust Yet Business-Friendly Regulatory Framework

The Isle of Man business-friendly regulatory framework is built on a deliberate policy choice: oversight without overreach. The Companies Act 2006 governs the majority of corporate structures and was designed from the outset to reduce administrative friction for internationally operating entities, not just domestic ones.

Regulated activities are subject to supervision by the Financial Services Authority (FSA), but ordinary trading companies fall outside FSA licensing requirements entirely. This distinction matters practically. A holding company or consultancy structure can be incorporated and operated without triggering licensing obligations, keeping compliance costs proportionate to actual business activity.

Annual obligations for standard companies are limited. There is no mandatory audit requirement for most private companies, and financial statements are not publicly filed with the Companies Registry. Your firm's financial data remains internal unless you choose otherwise.

Keep the following in mind:

- The Companies Act 2006 distinguishes between regulated and unregulated activities; confirm which category your business falls into before incorporation

- Annual returns are required; non-filing can result in strike-off

- Certain sectors, including insurance and fund management, require FSA licensing regardless of company size

- Substance requirements apply if your entity claims tax residency; passive registration without genuine activity may not be sufficient

Most private companies on the Isle of Man are not required to file annual financial statements publicly, meaning competitor access to your company's financials is structurally restricted by default.

Reputable Financial Services Supervision Commission Oversight

The Isle of Man Financial Services Authority oversight benefits any foreign-owned entity by placing it under a regulator with clear statutory powers, defined supervisory categories, and an established track record of enforcement. The FSA operates under the Financial Services Act 2008 and the Insurance Act 2008, giving it authority over banking, investment, fiduciary services, and insurance activities. That legal foundation means your business is supervised by a body with internationally recognized standing, not an opaque administrative office.

What FSA Regulation Means for Your Business Credibility

Counterparties, institutional investors, and correspondent banks apply heightened scrutiny to entities incorporated in jurisdictions with weak oversight. A firm licensed or registered under FSA supervision can demonstrate compliance with anti-money laundering obligations under the Proceeds of Crime Act 2008 and the associated Anti-Money Laundering and Countering the Financing of Terrorism Code 2019. That documented compliance record materially reduces friction when opening bank accounts or entering contracts with regulated counterparties in the UK, EU, or elsewhere.

FATF and OECD Standing as a Practical Advantage

The jurisdiction holds a favorable assessment from the Financial Action Task Force and is included on the OECD's list of jurisdictions committed to the internationally agreed tax standard. For your business, this translates into a lower due-diligence burden when dealing with foreign financial institutions, since the regulatory baseline is already accepted as credible. Isle of Man FSA regulation advantages extend to fund structures as well, where the Designated Business Register provides an additional layer of formalized oversight for non-licensed entities.

Maximize Your Isle of Man Incorporation Benefits

Speak with an Expanship specialist about FSA compliance requirements and how to structure your Isle of Man entity for full regulatory credibility.

Access to UK and Global Markets

The Isle of Man's access to UK markets benefit stems from a unique constitutional relationship with Britain. As a Crown Dependency, the island is covered by Protocol 3 of the UK's former EU accession treaty, and it maintains a customs union with the United Kingdom under the Isle of Man Act 1979. This means goods originating from a company registered there move into the UK market without customs duties or tariff barriers, a structural advantage that most offshore jurisdictions cannot replicate.

- Under the customs union arrangement, your business can trade physical goods into the UK as if operating from within British territory, without needing a separate UK entity or import clearance processes.

- The island uses the British pound and operates within the UK's VAT area under a revenue-sharing agreement, so VAT-registered businesses can account for UK VAT through Isle of Man Customs and Excise rather than registering directly with HMRC.

- Financial services firms can apply for recognition under certain UK regulatory frameworks, giving Isle of Man-licensed entities structured pathways into British financial markets.

- Beyond the UK, the island's compliance reputation, built through adherence to FATF standards and OECD transparency requirements, supports access to correspondent banking relationships and counterparty agreements across major international markets.

Strong Asset Protection and Privacy Laws

Isle of Man asset protection benefits for businesses are grounded in statute rather than administrative discretion. Under the Companies Act 2006, company ownership information is held by the Companies Registry but is not made publicly available in the same manner as in many onshore jurisdictions. Beneficial ownership data is reported to authorities under the Beneficial Ownership Act 2017, satisfying international compliance standards without exposing your ownership structure to public search.

For foreign investors holding assets through an Isle of Man entity, the legal separation between personal and corporate assets is well-established. Creditor claims against a shareholder generally cannot pierce the corporate veil absent fraud or specific statutory grounds, which provides a meaningful structural barrier for wealth held through a properly maintained company.

Foundations, established under the Foundations Act 2011, offer an additional vehicle for asset segregation. Unlike a trust, a foundation holds assets in its own name as a distinct legal person, which can suit estate planning arrangements where outright trust structures are less appropriate.

A foreign investor holding a property portfolio through an Isle of Man foundation, with a personal net worth of £5 million, maintains separation between those assets and personal liabilities. In a jurisdiction requiring full public beneficial ownership disclosure, that same structure would be visible to any party conducting a registry search.

Flexible LLC and Limited Company Structures

Isle of Man LLC and limited company structure benefits stem from the legal architecture established under the Limited Liability Companies Act 1996 and the Companies Act 2006. Two distinct entity types are available: the LLC, which operates under a members' agreement without mandatory share capital, and the standard limited company, which follows a more conventional corporate form.

For foreign investors, the LLC's contractual flexibility is particularly significant. Profit allocation, management rights, and membership interests can all be configured within the members' agreement rather than being dictated by statute. This means your business structure can mirror the economic arrangements agreed between principals, without forcing those arrangements into a rigid statutory template.

Under the Companies Act 2006, private limited companies face no minimum share capital requirement. A single director and a single shareholder are sufficient to form and operate the entity, with no residency conditions attached to either role.

Key structural options available to foreign-owned entities include:

- Single-member LLCs with full liability separation

- Companies limited by shares or by guarantee

- Redeemable shares and varied share class rights permitted under the 2006 Act

- Corporate directors permitted for limited companies

LLC members' agreements govern internal arrangements privately, but the LLC itself must still maintain a registered agent on the island at all times.

Fast and Straightforward Company Formation Process

One of the concrete Isle of Man fast company formation advantages is the speed at which a private limited company can be incorporated under the Companies Act 2006 (Isle of Man). Registration through the Isle of Man Companies Registry can typically be completed within 24 to 48 hours for standard applications. For a foreign business owner, this means operational readiness within days rather than weeks.

Same-Day Incorporation Option

An expedited same-day registration service is available for an additional fee, provided all documentation is submitted before the registry's cut-off time. This matters because delays at the formation stage often translate into deferred contracts, missed banking windows, and idle capital. Having a confirmed company number within hours removes that operational gap entirely.

Minimal Documentation Requirements

The Isle of Man quick business registration benefits are partly structural. The documents required to incorporate a private limited company are limited to a memorandum and articles of association, details of the registered agent, and director and shareholder information. No notarisation or apostille of foreign identity documents is required by the registry itself, which reduces the administrative burden for non-resident incorporators significantly.

Registered Agent Requirement

All companies must appoint a licensed registered agent holding authorisation from the Financial Services Authority. This requirement, rather than slowing formation, centralises the process through a single qualified intermediary who is already familiar with the filing system, which in practice accelerates preparation and submission of the required documents.

Stable Political and Legal Environment

The Isle of Man stable political environment for business stems from its constitutional status as a Crown Dependency with full internal self-governance. It operates under its own parliament, Tynwald, one of the oldest continuously sitting legislatures in the world, giving the island's legal and fiscal framework a degree of institutional continuity that few small jurisdictions can match.

Legislation is enacted through Tynwald and is not subject to UK parliamentary override on domestic matters. This separation means your business is not exposed to regulatory changes imposed from Westminster, providing a degree of policy predictability that investors in many EU-dependent territories do not have.

The island follows common law principles, grounded in English common law tradition with local statutory modifications. For foreign business owners, this matters because the legal standards for contract enforcement, corporate liability, and dispute resolution are familiar to any party operating under English law.

Key structural features that underpin this stability include:

- Courts apply well-established common law doctrines, reducing interpretive unpredictability in commercial disputes

- The Companies Act 2006 (Isle of Man) and the Companies Act 1931 provide a settled statutory base for corporate governance

- The Financial Services Authority (FSA) operates under defined statutory mandates, limiting scope for arbitrary regulatory action

- The island has no history of political coups, currency crises, or abrupt legislative reversals affecting corporate structures

- As a Crown Dependency, the entity benefits from the UK's sovereign guarantee framework without being bound by EU directives post-Brexit

Judicial decisions follow a transparent appeal pathway, with final appeals heard by the Judicial Committee of the Privy Council in London. This gives foreign investors access to one of the most respected appellate bodies in common law jurisdictions worldwide.

Why Isle of Man Outshines Other Offshore Jurisdictions

Comparing the Isle of Man against its most realistic competitors requires focusing on jurisdictions that attract the same profile of foreign investor: those seeking a politically stable, low-tax common law base with credible financial supervision. Gibraltar, Jersey, and Cayman Islands are the three jurisdictions most commonly evaluated alongside it, given their shared focus on zero or low corporate taxation, English legal systems, and international financial services activity.

What the comparison reveals is less about headline tax rates, where several offshore centres match or mirror each other, and more about the combination of regulatory credibility, market access, and structural flexibility. The Isle of Man's position on the OECD's white list and its tax agreements with the UK create practical advantages for businesses needing operational legitimacy alongside tax efficiency. That distinction matters when dealing with counterparties, banks, and regulators who treat jurisdiction of incorporation as a risk signal.

| Parameter | Isle of Man | Jersey | Gibraltar | Cayman Islands |

|---|---|---|---|---|

| Standard Corporate Tax Rate | 0% (most income) | 0% (most companies) | 10% (standard) | 0% |

| Capital Gains Tax | None | None | None | None |

| Withholding Tax on Dividends | None | None | None | None |

| OECD White List Status | Yes | Yes | Yes | Yes |

| UK Market Access Arrangement | Customs and VAT alignment with UK | No direct alignment | UK-linked via Gibraltar Protocol | None |

| Primary Regulatory Body | Financial Services Authority (FSA) | Jersey Financial Services Commission | Gibraltar Financial Services Commission | Cayman Islands Monetary Authority |

| Common Law Legal System | Yes | Yes (customary law base) | Yes | Yes |

| FATF Membership / Compliance | FATF-compliant | FATF-compliant | FATF-compliant | FATF-compliant |

Compliance Services for Companies in the Isle of Man

Maintain your Isle of Man company's good standing with ongoing compliance support, including annual returns, registered agent obligations, and regulatory filings under the Companies Acts 1931 and 2006.

Conclusion

The benefits of incorporating in Isle of Man rest on a coherent set of structural advantages: a zero percent corporate tax rate on most income categories, the complete absence of capital gains and withholding taxes, and a legal framework administered by established bodies like the Financial Services Authority that maintains credibility with international counterparties.

Tax efficiency and regulatory standing are rarely available together at this level. Many offshore jurisdictions offer low taxes at the cost of reputational risk, while well-regarded financial centres impose tax burdens that erode the commercial case for incorporation. The Isle of Man occupies a position where both conditions are met under a single framework.

That said, the right fit for your business depends on its specific structure, revenue model, and the jurisdictions where it operates. A holding entity with passive income sources will draw different advantages from this regime than an actively trading firm or a financial services business subject to licensing under the Regulated Activities Order 2011. Understanding how each structural feature applies to your circumstances is the step that turns general jurisdiction suitability into a concrete formation decision.

Start Your Isle of Man Company with Expanship Today

Isle of Man company formation with Expanship covers the full range of entity types available under the Companies Act 2006, from standard limited companies to LLC structures governed by the Limited Liability Companies Act 1996. Expanship's team works directly with the Companies Registry and understands the Financial Services Authority's compliance expectations, so your formation is handled in accordance with current statutory requirements from the outset.

Expanship's services across the incorporation and post-formation lifecycle include:

- Preparation and legalization of all formation documents required by the Companies Registry

- Registered agent and registered office provision in accordance with Isle of Man statutory requirements

- Government filing and direct liaison with the Companies Registry on your behalf

- Ongoing compliance management, including annual return filings and confirmation statements

- Banking introduction assistance to support your business account setup with Isle of Man financial institutions

Reach out to Expanship Isle of Man to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

Under the Companies Act 2006 (Isle of Man), there is no statutory requirement for a locally resident director for standard private companies. Directors can be appointed from any jurisdiction, though corporate governance considerations and substance requirements under the Income Tax (Substance Requirements) (Implementation) Regulations 2019 may affect whether a resident director is practically advisable depending on the nature of the business activities.

The standard corporate income tax rate is 0% for most classes of income. A 10% rate applies specifically to income derived from Manx land and property transactions and to profits of licensed banking businesses. Retail businesses with taxable profits exceeding £500,000 are also subject to a 10% rate under the Income Tax Act 1970 as amended.

If a company conducting relevant activities — such as banking, insurance, fund management, or holding company business — fails to satisfy the substance requirements under the 2019 Substance Regulations, the Isle of Man Income Tax Division can impose financial penalties and, in repeated cases, report the entity to foreign tax authorities in the jurisdiction of the parent company's ultimate beneficial owner. Substance compliance is assessed annually against criteria including adequate local expenditure, qualified staff, and core income-generating activities conducted on the island.

The jurisdiction is not listed on the EU's list of non-cooperative jurisdictions for tax purposes and has committed to OECD Base Erosion and Profit Shifting standards. The Financial Supervision Commission holds membership in the International Organization of Securities Commissions (IOSCO), which supports the island's standing with international correspondent banks and reduces the risk of de-risking by major financial institutions.

Incorporation through the Companies Registry typically completes within 24 to 48 hours for standard same-day or next-day applications when documents are filed correctly. The Companies Registry accepts electronic filings, and the Memorandum and Articles of Association, along with the prescribed incorporation fee, must be submitted before processing begins.

No capital gains tax exists in the Isle of Man, and there is no inheritance tax or estate duty levied on assets, including shares in locally incorporated entities. These taxes were abolished and have not been reintroduced, meaning transfers of shares upon death or disposal of shareholdings do not trigger a direct Isle of Man tax liability, though the tax treatment in your country of residence remains separately applicable.

The Financial Supervision Commission regulates entities conducting regulated activities as defined under the Financial Services Act 2008, which includes investment business, deposit-taking, insurance, and fund administration. Standard trading companies and holding structures with no regulated activity do not require FSC licensing, though they remain subject to Companies Registry obligations and anti-money laundering requirements under the Proceeds of Crime Act 2008.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.