Key Takeaways

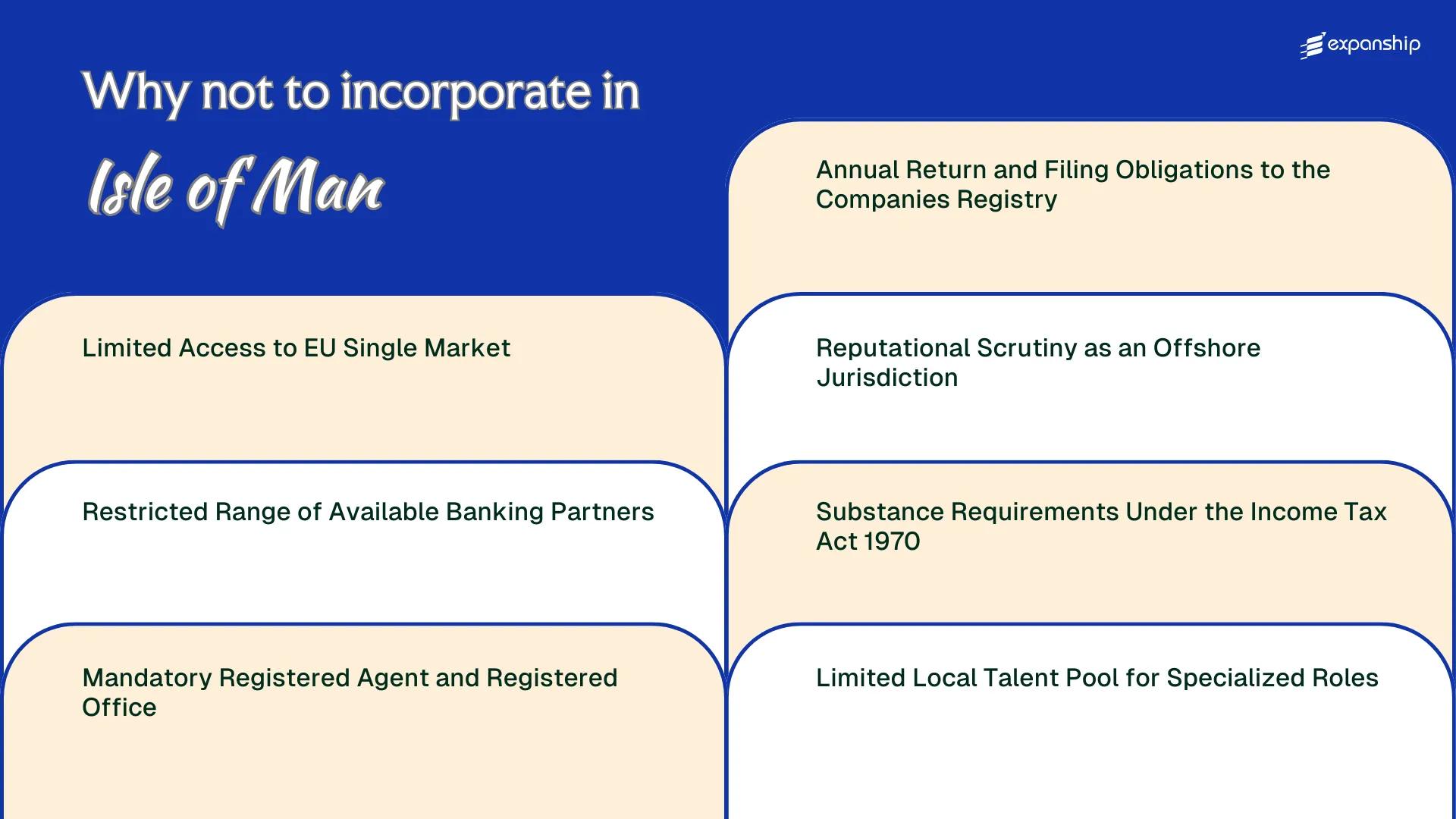

- Companies incorporated in the Isle of Man fall outside the EU Single Market, meaning trading firms and service businesses must navigate third-country access rules and cannot rely on passporting rights available to EU-incorporated entities.

- Under the substance requirements embedded in the Income Tax Act 1970, businesses claiming Isle of Man tax residency must demonstrate genuine local activity — including adequate staff, expenditure, and decision-making on the island — adding operational costs that lighter offshore structures typically avoid.

- The Isle of Man Financial Services Authority's active supervisory posture, combined with the jurisdiction's offshore perception among international banks, narrows the pool of correspondent banking partners willing to onboard Isle of Man-registered entities without extensive due diligence.

- Mandatory appointment of a registered agent and maintenance of a registered office are non-negotiable compliance requirements that introduce recurring costs and a layer of administrative dependency that domestically incorporated structures in larger jurisdictions do not always require.

Incorporating in the Isle of Man operates under a structured and actively supervised regulatory environment, governed primarily through the Companies Registry and overseen by the Isle of Man Financial Services Authority. This framework is neither lax nor opaque — it reflects a jurisdiction that has worked to align with international standards, which brings its own compliance demands for foreign business owners.

This article examines the specific disadvantages of incorporating in the Isle of Man that arise from that regulatory posture, spanning tax substance rules, banking access, and filing obligations under Isle of Man law.

Not every drawback applies equally to all entities. A holding company faces different constraints than a trading firm or a fund structure, and your industry will shape which friction points carry the most practical weight.

Foreign investors establishing trading companies, holding structures, or service businesses outside the UK and EU markets are most likely to encounter the limitations this article addresses.

Limited Access to EU Single Market

Isle of Man EU single market restrictions represent one of the more consequential structural limitations for businesses that rely on frictionless cross-border trade with European clients or partners.

No Passporting Rights for Financial Services

The Isle of Man is a Crown Dependency, not a member of the European Union or the European Economic Area. A firm incorporated there cannot use EU financial services passporting, which means it has no automatic right to offer regulated services across EU member states without obtaining separate authorizations in each target jurisdiction.

This applies even to firms that previously benefited from transitional arrangements before Brexit redrew the regulatory boundaries. For a business targeting multiple EU markets, the cost and administrative burden of pursuing individual country authorizations can be prohibitive.

Customs and Trade Friction with the EU

Under Protocol 3 of the UK's Act of Accession, the Isle of Man has a defined but limited relationship with EU customs arrangements, covering goods but not services or capital in the same way full membership would.

Your business cannot assume that incorporation here provides a gateway to EU single market access for services. Sectors such as financial services, professional services, and digital commerce face real structural barriers when trying to serve EU-based clients from this jurisdiction.

A company incorporated in the Isle of Man has no passporting rights and no EEA membership, meaning any regulated activity directed at EU clients requires separate licensing within the EU itself.

Restricted Range of Available Banking Partners

Isle of Man banking limitations for companies are a practical constraint that foreign directors encounter early in the incorporation process. Most major international banks no longer actively onboard offshore-structured entities, and those that do apply extensive due diligence requirements that can delay account opening by weeks or months.

The island has no domestic clearing bank of its own. Corporate accounts are typically held with subsidiaries or branches of UK banking groups, a small number of private banks, and a limited set of international institutions with a local presence.

This concentration creates real friction for your business:

- Fewer competing institutions means less negotiating leverage on fee structures, interest terms, or credit facilities

- If your primary bank withdraws from the market or tightens its acceptance criteria, finding an alternative locally can take considerable time

- Banks operating under Financial Services Authority (Isle of Man) oversight apply rigorous beneficial ownership verification, which adds document burden for multi-layered corporate structures

- Non-resident directors often face additional identity checks that domestic applicants do not, extending onboarding timelines

Correspondent banking relationships further complicate the picture. Some international payment corridors are restricted or subject to enhanced screening, which affects transaction speed for companies that operate across multiple jurisdictions.

Company Incorporation in Isle of Man

Understand the full scope of requirements before you commit to incorporating in the Isle of Man.

Mandatory Registered Agent and Registered Office

Every company incorporated under the Isle of Man Companies Act 2006 must appoint a registered agent who holds a licence issued by the Isle of Man Financial Services Authority (FSA). This is not a formality you can bypass by using a postal address or a local contact. The registered agent must be a licensed corporate services provider, and that licensing requirement means your ongoing compliance costs are tied to a regulated third party whose fees you cannot easily negotiate down.

| Requirement | Detail | Implication for Foreign Owner |

|---|---|---|

| Registered Agent | FSA-licensed provider mandatory | No option to self-appoint or use a nominee without a licence |

| Registered Office | Must be a physical Isle of Man address | Virtual offices in foreign jurisdictions not permitted |

| Typical Annual Agent Fee | £500–£2,000+ depending on service scope | Recurring fixed cost regardless of company activity level |

| Consequence of Non-Compliance | Company may be struck off the Companies Registry | Loss of legal standing in the jurisdiction |

The registered office must also be maintained at a physical address on the island, which adds a layer of dependency on a local provider. For a dormant or holding entity generating no active revenue, this mandatory recurring expenditure is a structural cost that cannot be reduced.

Changing your registered agent requires formal notification to the Companies Registry, which creates administrative friction if your provider relationship deteriorates.

Annual Return and Filing Obligations to the Companies Registry

Isle of Man annual return filing obligations apply to all companies registered under the Companies Act 2006, and non-compliance carries automatic penalties that accumulate over time. For a foreign business owner with no on-the-ground presence, tracking these deadlines from abroad adds a layer of administrative cost that has no direct operational benefit.

Under the Companies Registry framework, every company must file an annual return confirming its registered details, including directors, shareholders, and registered office address. Failure to file on time results in late filing fees, and persistent default can lead to the company being struck off the register.

The filing obligation exists regardless of whether your company traded during that year. A dormant entity still triggers the same compliance burden as an active one.

- Annual returns must be filed with the Isle of Man Companies Registry each year, even for dormant companies

- Late submission incurs financial penalties that increase with the length of delay

- Director and shareholder information must remain current in the registry at all times

- Striking off the register is a statutory consequence of persistent non-compliance under the Companies Act 2006

- Reinstatement after a strike-off requires a separate legal process and additional fees

A company struck off the Isle of Man register can have its assets treated as bona vacantia, meaning they vest in the Crown automatically without any further legal action required.

Reputational Scrutiny as an Offshore Jurisdiction

Despite meeting OECD standards and holding a strong regulatory record, Isle of Man offshore jurisdiction reputational risks remain a persistent concern for foreign business owners, particularly those operating in or seeking clients from onshore markets.

How Perception Diverges from Regulatory Reality

The island is not listed on the EU's list of non-cooperative jurisdictions for tax purposes, and it has implemented the OECD's Common Reporting Standard. Yet banking institutions, institutional investors, and corporate partners in Europe and North America frequently apply heightened due diligence to entities incorporated there, regardless of actual compliance status. That friction translates directly into slower account openings, additional documentation requirements, and in some cases, outright refusal of service.

The Practical Cost of Offshore Perception

Your business may face reputational exposure simply by disclosing its registered territory to clients or counterparties who associate low-tax offshore structures with opacity. Professional service providers, particularly in regulated sectors like finance or fintech, sometimes decline to engage with offshore-incorporated entities as a matter of internal policy rather than legal obligation. This perception-driven exclusion is harder to resolve than a formal compliance gap, because no regulatory certificate or filing corrects a counterparty's risk appetite.

Addressing Reputational and Compliance Challenges in the Isle of Man

Understand how structural and perception-related hurdles affect your Isle of Man entity, and get guidance on how to position your business appropriately from the outset.

Substance Requirements Under the Income Tax Act 1970

Under the Income Tax Act 1970, Isle of Man substance requirements challenges affect any entity claiming local tax residency, since the business must demonstrate genuine economic activity on the island rather than a purely administrative presence.

- Your firm must maintain a physical office, conduct core income-generating activities locally, and employ adequate qualified staff in the jurisdiction, all of which create ongoing operational costs that do not apply in jurisdictions with no substance rules.

- Compliance with Isle of Man economic substance obligations requires detailed annual reporting to the Income Tax Division, which increases your administrative burden and professional service fees each year.

- Failing to meet Isle of Man company substance compliance drawbacks the test triggers penalties, automatic exchange of information with foreign tax authorities under international reporting frameworks, and potential reclassification of tax residency.

- The Income Tax Act 1970 restrictions apply specifically to companies deriving income from relevant sectors such as banking, insurance, fund management, and holding company activities, meaning lower-risk businesses may face a narrower but still defined compliance threshold.

Limited Local Talent Pool for Specialized Roles

The Isle of Man limited talent pool drawbacks are most acute when your business requires resident specialists in areas such as financial technology, advanced engineering, or senior legal compliance. With a population of approximately 85,000, the resident workforce simply cannot supply the depth of candidates that larger financial centres can.

Recruiting locally for niche roles often means competing against the island's established financial services firms, which have long-standing relationships with the limited pool of qualified residents. For a newly incorporated entity, that competition is difficult to win without significant compensation premiums.

Bringing in talent from outside means engaging with the Isle of Man's immigration framework, administered by the Cabinet Office. Work permits and residency approvals add lead time and administrative cost to every senior hire made from abroad.

- Fintech and blockchain specialists are scarce relative to the sector's growth on the island

- Senior compliance officers with cross-border regulatory experience are in short supply

- Locally sourced board members with substance-qualifying credentials can be difficult to find

Hypothetical scenario: A foreign-owned financial services firm incorporating under the Companies Act 2006 (Isle of Man) requires two resident directors with qualifying sector experience to satisfy substance requirements. Sourcing them through local recruitment agencies at market rates could add £60,000–£90,000 annually in director service fees alone, before any permanent headcount costs are incurred.

Overcoming These Incorporation Challenges

Overcoming Isle of Man incorporation challenges requires a structured approach that accounts for both domestic compliance obligations and international positioning.

- Establish economic substance in the Isle of Man by ensuring that core income-generating activities, board meetings, and qualified staff are physically present on the island, consistent with the substance requirements under the Income Tax Act 1970.

- Appoint a licensed registered agent and secure a registered office address through a firm authorised under the Corporate Service Providers Act 2000.

- Open accounts with banks that maintain correspondent relationships in your target markets, prioritising institutions with established cross-border frameworks outside the EU.

- File annual returns and financial statements on time with the Companies Registry to avoid penalties under the Companies Act 2006.

- Document your ownership structure and beneficial ownership details in the Central Register to meet anti-money laundering obligations.

Each of these steps operates within a framework overseen by the Financial Services Authority and the Isle of Man Government. Compliance gaps in any one area can create compounding exposure across the others.

Isle of Man Still Worth Considering

Despite the disadvantages covered in this blog, Isle of Man company formation still worth it is a conclusion many foreign businesses reach after weighing the full picture. The jurisdiction holds a stable legal framework, a long-established Companies Registry, and a 0% corporate tax rate on most income — concrete structural features, not marketing claims.

| Pros | Cons |

|---|---|

| 0% corporate income tax rate on most trading income under the Income Tax Act 1970 | No access to EU Single Market passporting rights following Brexit |

| Politically stable jurisdiction with a well-regulated Companies Registry | Banking options are limited, with few international institutions maintaining a local presence |

| Established legal system based on English common law principles | Substance requirements under the Income Tax Act 1970 demand genuine local operational presence |

| No capital gains tax or inheritance tax | Mandatory registered agent and registered office add recurring compliance costs |

| Reputable regulatory environment supervised by the Financial Supervision Commission | Offshore perception invites enhanced due diligence from banks and counterparties |

| Flexible corporate structures available, including the LLC and LP | Local talent pool is shallow for specialized technical or financial roles |

Incorporating here suits businesses that can genuinely meet the substance threshold and operate without relying on EU market access. Those that cannot satisfy these conditions face material compliance exposure, not just administrative inconvenience.

Compliance Services for Companies in the Isle of Man

Maintain good standing with the Isle of Man Companies Registry and meet your ongoing filing, substance, and regulatory obligations.

Conclusion

The Isle of Man incorporation drawbacks summary presented across this blog reflects a jurisdiction that carries genuine structural constraints for certain businesses. Post-Brexit exclusion from the EU Single Market limits the firm's commercial reach into Europe. Substance requirements under the Income Tax Act 1970 add ongoing operational cost and commitment that many founders underestimate at the formation stage. Banking access remains narrower than in larger financial centres. Professional guidance specific to Isle of Man company formation can reduce the risk of compliance gaps, particularly as regulatory expectations across filing, substance, and residency continue to evolve.

Expanship's Isle of Man Incorporation Support

From managing substance requirements under the Income Tax Act 1970 to maintaining ongoing filings with the Isle of Man Companies Registry, the compliance obligations here are real and ongoing. Expanship Isle of Man company incorporation support is designed to reduce the operational weight of these requirements, so you spend less time on administrative coordination and more time running your business. Our role is to help your entity stay on track, not to make the obligations disappear.

Our services cover the full scope of setting up and maintaining a company on the island:

- Preparing and submitting company registration documentation on your behalf

- Providing a compliant registered agent and registered office address

- Handling government filings and liaising directly with the Companies Registry

- Managing post-incorporation compliance obligations on an ongoing basis

- Making introductions to suitable banking partners for your firm's needs

- Registering your business for tax purposes and coordinating with local authorities

To discuss your specific situation, contact Expanship Isle of Man.

Frequently Asked Questions (FAQ)

The substance requirements apply specifically to companies that are tax resident in the Isle of Man and derive income from certain designated activities, such as banking, insurance, fund management, and intellectual property holding. A company engaged in activities outside those categories is not subject to the same directed management and control tests. However, tax residency itself still requires genuine central management on the island, so even non-designated businesses cannot be entirely passive.

Failure to file annual returns with the Isle of Man Companies Registry can result in the company being struck off the register, which effectively dissolves the entity and strips it of legal standing. Restoration is possible but involves a formal application, associated fees, and potential penalties for the period of non-compliance. The disruption to ongoing contracts and bank accounts during a strike-off period can be commercially damaging.

Registered agent and registered office fees vary by provider, but annual costs generally range from several hundred to over a thousand pounds depending on the level of service included. This is a non-negotiable statutory requirement under Isle of Man company law, so there is no way to avoid it by using a virtual address or a foreign contact. Factoring this into your annual operating budget is essential, as it is a recurring fixed cost regardless of whether the company trades actively.

Banking access is noticeably more constrained for an Isle of Man entity than for companies in EU member states like Ireland or the Netherlands. EU-based firms benefit from passporting rights and established relationships with a broad network of European clearing banks, whereas Isle of Man companies must approach a more limited set of institutions willing to onboard offshore-structured clients. Due diligence requirements are also typically more intensive, which can extend account opening timelines significantly.

An Isle of Man company itself has no rights under EU single market rules, but you can establish a subsidiary incorporated in an EU member state that does. That subsidiary would need to meet the local substance and incorporation requirements of the chosen EU jurisdiction, adding cost and administrative overhead. The Isle of Man parent entity does not automatically confer any EU market access to the group.

Non-compliance with Isle of Man substance requirements can result in financial penalties issued by the Isle of Man Assessor of Income Tax, and persistent or serious failures can be reported to relevant foreign tax authorities under automatic exchange of information frameworks. The initial penalty tiers escalate with continued non-compliance, and the information sharing element means that exposure is not limited to the Isle of Man alone. A company found lacking substance may also have its claimed tax residency challenged, which creates retrospective tax liability risk.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.