Key Takeaways

- Foreign investors establishing a d.o.o. must meet a minimum share capital requirement that imposes an upfront financial threshold before operations can begin.

- Under the Zakon o trgovačkim društvima, the incorporation process routes through court registration and mandatory notarization, adding procedural layers and delays that are uncommon in more streamlined EU jurisdictions.

- Croatia's rigid labour framework, including statutory dismissal protections and associated severance obligations, constrains workforce flexibility in ways that increase the cost of workforce adjustments.

- Official regulatory filings and court communications are conducted exclusively in Croatian, requiring foreign investors without local language capacity to incur ongoing translation and local representation costs throughout the company's lifecycle.

Croatia operates under a heavily regulated corporate framework, shaped significantly by its EU membership obligations and domestic commercial legislation. The disadvantages of incorporating in Croatia span procedural, financial, and operational dimensions — all of which this article examines in detail.

Not every obstacle will apply equally to your business. The challenges you encounter will depend considerably on your chosen legal entity, industry sector, and whether you are entering as a sole foreign investor or through a joint venture structure.

This article is most relevant to non-EU foreign investors and internationally mobile entrepreneurs setting up a private limited liability company, the društvo s ograničenom odgovornošću, for the first time. Primary obligations for company formation are governed by the Companies Act, the Zakon o trgovačkim društvima.

The drawbacks of company formation here affect businesses across registration, tax compliance, labour relations, and access to capital.

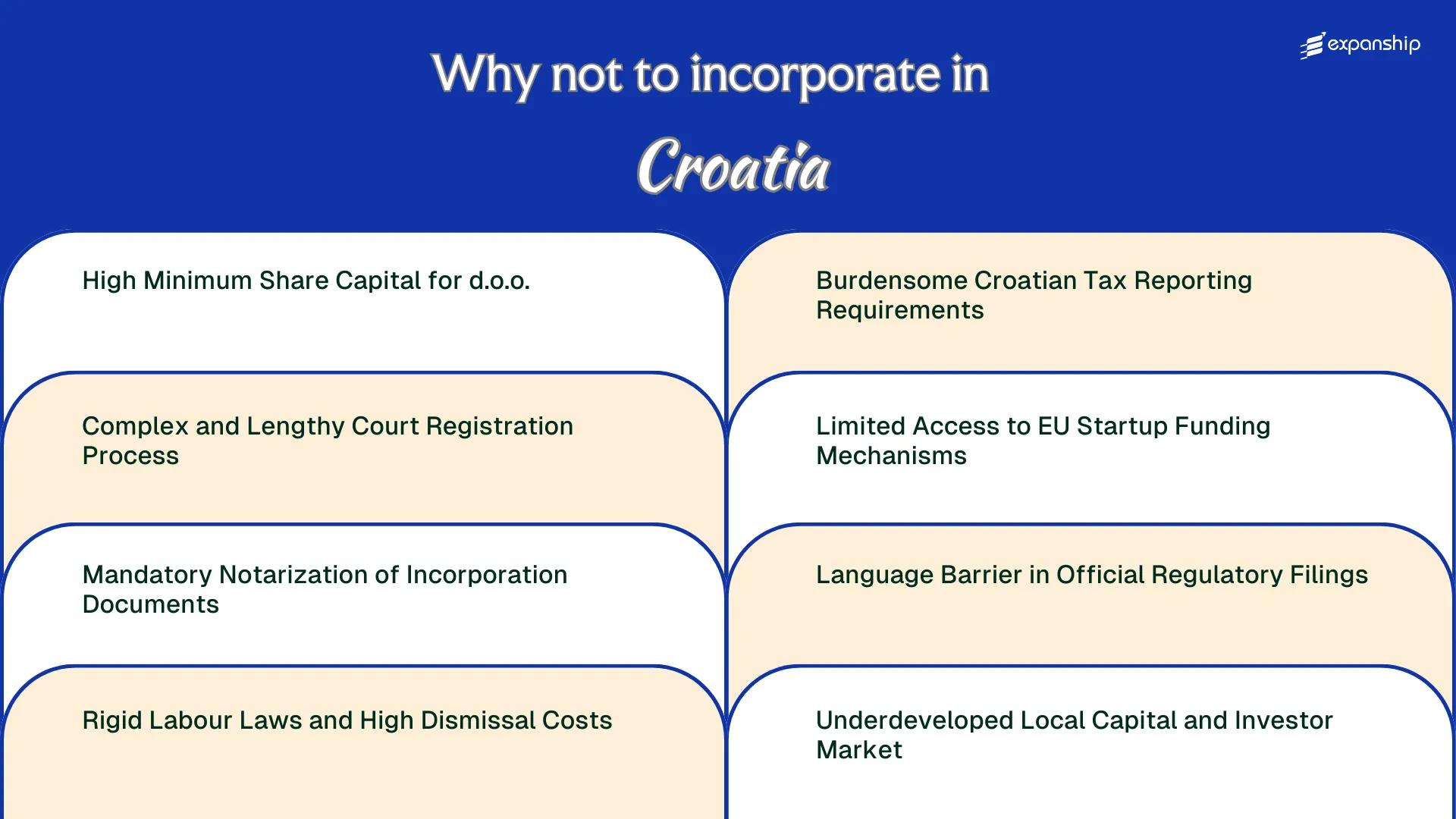

High Minimum Share Capital for d.o.o.

Croatia d.o.o. minimum share capital problems affect foreign founders before the business generates a single euro. Under the Companies Act (Zakon o trgovačkim društvima), forming a društvo s ograničenom odgovornošću requires a minimum share capital of HRK 20,000, now expressed as approximately EUR 2,654 following Croatia's euro adoption in January 2023.

Capital Must Be Committed Upfront

At least half of this amount must be paid in before registration is complete. For a foreign entrepreneur testing a new market, this represents real capital locked into a legal structure with no guarantee of commercial return.

Each member's individual contribution cannot fall below EUR 200, which further constrains how equity is divided among co-founders in early-stage ventures.

The Comparative Burden for Foreign Entrants

Several EU member states permit single-euro symbolic share capital for private limited companies, making Croatia's threshold a meaningful relative obstacle for lean market-entry strategies. The capital does not fund operations; it sits as a structural requirement under company formation capital restrictions in Croatia.

The minimum capital requirement must be deposited into a designated temporary bank account before the court registry accepts your incorporation application, creating a cash commitment that precedes any legal confirmation that your entity will be approved.

Complex and Lengthy Court Registration Process

The Croatia court registration process runs through the commercial courts, not a centralised business registry agency. Your application for a d.o.o. must be submitted to the relevant Commercial Court (Trgovački sud), which means registration timelines are subject to court scheduling, not administrative processing windows. That dependency alone separates Croatia from jurisdictions with dedicated, digitally-driven company registries.

Processing times can extend from several days to several weeks, depending on the court's caseload. Unlike online-first systems in Estonia or Slovenia, procedural gaps and document deficiencies trigger formal rejections that restart the clock entirely.

For a foreign business owner, this structure creates friction at multiple points:

- Waiting on court-controlled timelines delays your ability to open a corporate bank account, which is required before operations can begin.

- Any document correction requires re-submission through the same court queue, compounding delays without a fast-track alternative.

- Coordinating with local legal representatives across time zones extends internal turnaround time beyond the court's own processing period.

- Errors in the founding act or articles of association identified post-submission result in formal court rejection, not a simple amendment request.

Sole traders and branches face separate registration pathways, each with distinct documentary requirements, which adds further complexity if your intended structure evolves during setup.

Company Incorporation in Croatia

Set up your Croatian d.o.o. with accurate documentation prepared from the start, reducing the risk of court rejection and registration delays.

Mandatory Notarization of Incorporation Documents

Forming a d.o.o. in Croatia requires that the founding act — the articles of association — be executed as a notarial deed before a licensed Croatian civil law notary (javni bilježnik). This is not an optional formality. The requirement is anchored in the Companies Act (Zakon o trgovačkim društvima), and without a certified notarial deed, the Commercial Court registry will not accept the registration application.

| Requirement | Detail | Burden for Foreign Founders |

|---|---|---|

| Document requiring notarization | Articles of association (founding act) | Mandatory notarial deed; no digital-only alternative for standard formation |

| Notary fee basis | Calculated on registered share capital value | Higher capital = higher notary fee, compounding the minimum capital burden |

| Personal appearance requirement | Founder or authorized attorney must appear in person | Remote or postal execution not accepted; proxy requires separately notarized power of attorney |

| Language of notarial deed | Croatian only | Foreign-language founders need certified translation before notarization |

The cost of notarization is not a flat administrative fee. Notary charges scale with the registered share capital of the entity, meaning a business that meets the statutory minimum of HRK 20,000 (approximately EUR 2,650) still faces a proportionate fee before any registration costs are added.

Foreign founders who cannot attend in person must grant a power of attorney — itself a document requiring notarization, often in the founder's home country and subject to apostille certification. This creates a two-stage authentication chain that extends timelines and adds fees before the Croatian registration process even begins.

Rigid Labour Laws and High Dismissal Costs

Croatia labour law restrictions for employers represent one of the more significant structural costs of operating a local entity. The Labour Act (Zakon o radu), administered in conjunction with sector-level collective agreements, sets binding obligations on notice periods, severance calculations, and procedural requirements for termination that directly increase the cost of workforce adjustments.

Dismissing an employee is not simply an administrative act. Under the Labour Act, redundancy dismissals require a formal business justification, defined consultation periods, and in many cases, coordination with works councils where they exist, adding weeks to any workforce reduction process.

Severance entitlements accrue based on years of service, and for long-tenured employees the cumulative liability can be substantial. This creates a financial exposure that foreign firms frequently underestimate when modelling operational costs at the point of entry.

Fixed-term contracts offer limited flexibility, as Croatian law restricts repeated renewals and imposes conversion to indefinite employment after defined periods. Each extension or renewal requires careful documentation to avoid automatic contract reclassification.

- Severance pay is a statutory entitlement, not a negotiable term

- Redundancy procedures require documented business justification before notice is issued

- Works councils must be consulted in firms meeting the applicable employee threshold

- Fixed-term contracts convert to indefinite-term contracts if renewal conditions are breached

- Collective agreements in certain sectors impose obligations beyond the Labour Act's baseline

Croatia's Labour Act grants employees the right to challenge dismissal before a court for up to two years after termination, exposing employers to reinstatement orders rather than just monetary compensation.

Burdensome Croatian Tax Reporting Requirements

Corporate tax compliance challenges in Croatia extend well beyond the standard EU filings that foreign business owners may expect.

Frequency and Volume of Reporting Obligations

The Porezna uprava (Tax Administration) requires companies to file monthly VAT returns, monthly income tax prepayments, and separate annual corporate income tax returns under the Zakon o porezu na dobit (Corporate Income Tax Act). For a foreign-owned d.o.o. without a dedicated local accounting team, maintaining that monthly cadence across multiple parallel obligations generates recurring administrative costs that many jurisdictions do not impose at the same frequency.

Statistical and earnings reports must also be submitted to the Financijska agencija (FINA), Croatia's financial agency, which operates independently from the Tax Administration. Coordinating compliance across two separate bodies doubles the administrative touchpoints your business must manage year-round.

Practical Cost Implications for Foreign Entities

The burdensome Croatia tax reporting requirements translate directly into sustained professional fees, since local certified accountants are effectively a structural necessity rather than an optional service. Errors or late submissions carry penalty provisions under the Opći porezni zakon (General Tax Act), adding financial exposure on top of routine compliance costs.

Businesses registered for EU cross-border trade must additionally submit EC Sales Lists and Intrastat declarations once thresholds are met, compounding the overall reporting volume. For smaller foreign-owned firms with lean back-office operations, this accumulation of obligations absorbs a disproportionate share of operational capacity.

Managing Tax Compliance Obligations in Croatia

Understand the full scope of Croatian tax reporting requirements before you incorporate, and get guidance on structuring your compliance operations from day one.

Limited Access to EU Startup Funding Mechanisms

Croatia's limited EU startup funding access stems from a structural reality: most EU-backed instruments prioritize entities with established local operational histories or specific national eligibility criteria that newly incorporated foreign-owned companies often cannot satisfy.

- Under the European Structural and Investment Funds (ESIF) framework, Croatia's operational programmes are administered domestically through the Ministry of Regional Development and EU Funds, and grant eligibility frequently requires demonstrated prior business activity within the country, which excludes recently registered entities.

- Horizon Europe funding is technically open to Croatian-registered companies, but the administrative burden of preparing competitive applications without local institutional partnerships significantly reduces practical access for small foreign-owned firms.

- The Croatian Agency for SMEs, Innovation and Investments (HAMAG-BICRO) manages several co-financing instruments, but many schemes impose sector-specific restrictions or require co-financing ratios that early-stage foreign-owned subsidiaries cannot meet.

- Foreign companies incorporated solely as holding or intermediary structures face outright exclusion from startup-oriented grant schemes that mandate active commercial operations in Croatia.

Language Barrier in Official Regulatory Filings

The Croatia language barrier in regulatory filings is a structural constraint, not an administrative formality. All submissions to the Commercial Court Registry (Trgovački sud), the Croatian Financial Services Supervisory Agency (HANFA), and the Tax Administration (Porezna uprava) must be prepared exclusively in Croatian.

Foreign-language documents are not accepted unless accompanied by a certified translation produced by a court-sworn interpreter. Each translation adds cost and delays, and for a filing-heavy first year, those costs compound quickly.

- Annual financial statements, articles of association, and shareholder resolutions must all be translated before submission

- Contracts with public authorities require Croatian-language versions

- Any amendment to company documents triggers a new round of certified translations

This requirement stems from the Official Use of the Croatian Language Act, which mandates Croatian as the sole language of public administration and legal proceedings.

If your firm operates across multiple jurisdictions, language compliance in Croatia demands a dedicated local resource or a standing arrangement with a certified translator, neither of which is a one-time expense.

A foreign founder filing three rounds of document amendments in year one, each requiring certified translation of five pages, could realistically spend between €600 and €1,200 on translation fees alone, before accounting for any legal review costs.

Underdeveloped Local Capital and Investor Market

Croatia underdeveloped investor market risks are a structural concern for any foreign business owner expecting to raise capital locally after incorporation. The domestic venture capital ecosystem remains thin compared to Western European peers, with few institutional investors actively deploying early-stage or growth funding.

The Croatian Private Equity and Venture Capital Association (CVCA) represents a small community of active funds. Deal volume and fund sizes are considerably lower than markets such as Austria or Slovenia, meaning your firm cannot realistically depend on local capital rounds to sustain post-incorporation growth.

HAMAG-BICRO, the state agency for SME support, administers grant schemes and subsidised loan instruments, but these programmes are government-backed rather than market-driven. Eligibility criteria, sectoral restrictions, and documentation requirements limit their practical accessibility for foreign-owned entities.

- Equity investment culture among private Croatian investors remains underdeveloped, with limited appetite for minority stakes in foreign-controlled companies.

- Secondary market liquidity on the Zagreb Stock Exchange (ZSE) is low, restricting exit options for investors.

- Angel investor networks exist but operate at a scale that rarely meets the capital needs of scaling businesses.

Foreign-owned d.o.o. entities may face additional scrutiny or outright ineligibility under certain HAMAG-BICRO and EU co-funded programmes that prioritise domestically controlled SMEs, which directly narrows the funding options you might otherwise assume are available to your entity.

Mitigating These Incorporation Challenges

Mitigating these incorporation challenges requires a structured approach rather than reactive fixes. Specific legal and administrative choices made at the formation stage can reduce exposure to several of the procedural and compliance burdens described throughout this blog.

- Elect the simplified d.o.o. formation procedure under the Companies Act to reduce notarization costs where eligible.

- Pre-clear your share capital deposit with FINA, the Financial Agency, to avoid delays during court registration at the commercial court.

- Structure employment contracts within the boundaries set by the Labour Act (Zakon o radu) to limit future dismissal liability.

- Engage a certified Croatian tax advisor before filing with the Tax Administration (Porezna uprava) to ensure VAT and corporate tax compliance from inception.

- File all incorporation documents with certified Croatian translations to satisfy the official language requirements of the commercial court registry.

These steps address structural friction points within Croatia's regulatory system, not workarounds. The effectiveness of each measure depends on how consistently your business applies them across its ongoing compliance obligations.

Croatia's Overall Appeal for Foreign Investors

Croatia's overall appeal for foreign investors exists alongside a documented set of structural friction points. EU membership, euro adoption in January 2023, and access to the Schengen Area give the country a credible foundation that few regional peers can match. That said, the incorporation and compliance environment carries real costs that a foreign business owner should weigh before committing.

| Pros | Cons |

|---|---|

| Euro-denominated economy reduces currency conversion costs and simplifies cross-border EU transactions | The d.o.o. requires a minimum share capital of HRK 20,000 (approx. €2,654), a hard threshold before operations begin |

| EU membership grants access to the single market, freedom of establishment, and standardised contract enforcement | Court registration through the commercial courts can extend the formation timeline beyond typical EU norms |

| Schengen membership simplifies travel and logistics for founders managing operations across multiple European countries | Notarisation of incorporation documents adds a mandatory procedural layer and associated costs to every formation |

| Croatia's Adriatic geography and tourism infrastructure support certain service-based and logistics-oriented business models | Labour dismissal procedures are governed by strict statutory rules, making workforce adjustments legally complex and costly |

| Bilateral tax treaties with numerous countries reduce withholding tax exposure for qualifying foreign shareholders | Tax reporting obligations are administered through the ePorezna system, with filings required in Croatian only |

Access to EU structural funds exists in principle, but the administrative channels through which those funds flow remain difficult for smaller foreign-owned entities to access without local institutional relationships. Official filings with the Croatian Financial Agency (FINA) and the Tax Administration are conducted exclusively in Croatian, which creates an ongoing operational dependency on local professional support.

Compliance Services for Companies in Croatia

Ongoing compliance for Croatian companies covers FINA reporting, corporate tax filings through the ePorezna system, and statutory record-keeping obligations under Croatian company law.

Conclusion

The Croatia company incorporation cons summary points to a jurisdiction with genuine structural friction for foreign businesses. Court registration through the Commercial Court registry, mandatory notarization under Croatian law, and the HRK-denominated minimum share capital requirement each create measurable delays and upfront costs that affect early-stage planning. Labour regulations under the Labour Act further constrain operational flexibility once the entity is active. These are fixed features of the current legal framework, not incidental procedural hurdles. Professional guidance specific to Croatian regulatory and compliance requirements remains the most direct way to reduce the risk of missteps during formation and beyond.

Expanship's Support for Your Croatia Expansion

Expanship Croatia company formation support is built around the specific friction points this jurisdiction presents. From coordinating mandatory notarization of your founding act under the Croatian Companies Act to liaising with HITRO.HR and the commercial courts for registration, Expanship handles the procedural weight so your team can focus on the business itself.

Beyond registration, the firm offers a broader scope of practical support across your Croatian setup:

- Your company documents are prepared and submitted through the correct registration channels.

- A registered agent and local office address are provided to satisfy statutory presence requirements.

- Filings with the Croatian Financial Agency (FINA) and other regulatory bodies are managed on your behalf.

- Ongoing compliance obligations are tracked and handled after your entity is active.

- Introductions to local banking institutions are facilitated to support account opening.

- Tax registration with the Tax Administration (Porezna uprava) and local authority liaison are coordinated for you.

Reach out to Expanship Croatia to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

Notarization through a Croatian public notary is required for the founding act (društveni ugovor) and statements of founders, without exception for a d.o.o. This applies regardless of whether the founders are domestic or foreign nationals, and remote or electronic notarization options remain limited compared to jurisdictions like Estonia or the Netherlands. The practical consequence is that foreign founders frequently need to be physically present in Croatia or grant a notarized power of attorney to a local representative.

The Croatian Tax Administration (Porezna uprava) can impose fines for late filing or inaccurate submissions under the General Tax Act (Opći porezni zakon). Penalties vary depending on the violation but can reach tens of thousands of euros for legal entities in serious cases of non-compliance. Repeated or deliberate breaches can also trigger audits that disrupt normal business operations for extended periods.

Yes, Croatia's commercial court registration process (conducted through the sudski registar) takes materially longer than in digital-first jurisdictions. While Estonia or Ireland can complete company registration within one to two business days online, Croatian registrations often take several weeks due to court queue times and document verification procedures. Delays are common even when all documents are correctly submitted.

All official filings with Croatian regulatory bodies must be submitted in Croatian, and errors caused by mistranslation or misunderstanding of legal terminology can result in rejected applications or compliance failures. The Croatian Financial Agency (FINA), which handles certain financial disclosures, does not accept submissions in foreign languages. Engaging a qualified local lawyer or certified translator is not optional in practice, and that cost is recurring, not a one-time expense.

Access is structurally limited. Most EU-backed early-stage funding disbursed through Croatian intermediaries, including programs channeled via the Croatian Bank for Reconstruction and Development (HBOR), is designed with domestic economic development criteria that disadvantage newly formed foreign-owned entities. A d.o.o. with no Croatian operational track record and no local co-founders will find it difficult to meet eligibility requirements. This is distinct from the EU funds themselves being unavailable; the bottleneck lies in how Croatia allocates and administers those funds domestically.

Croatia's Labour Act (Zakon o radu) mandates severance pay for employees dismissed after two years of continuous service, with entitlements increasing incrementally with tenure. Combined with mandatory notice periods and restrictions on termination grounds, the total cost of workforce reduction in Croatia is higher than in jurisdictions like Poland or the Czech Republic, where employer flexibility is comparatively greater. For a foreign company scaling cautiously, this makes Croatia's labour framework a genuine financial risk in the event of restructuring.

A company incorporated in Croatia will find limited domestic options for equity financing beyond bank credit, as the Zagreb Stock Exchange (ZSE) handles relatively low trading volumes and private venture capital activity is thin compared to regional peers like Poland or Romania. For businesses that anticipate needing follow-on investment rounds, reliance on the local market creates a structural funding constraint. Foreign investment can still be attracted, but the infrastructure supporting it, including fund managers, angel networks, and secondary market liquidity, is materially less developed.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.