Key Takeaways

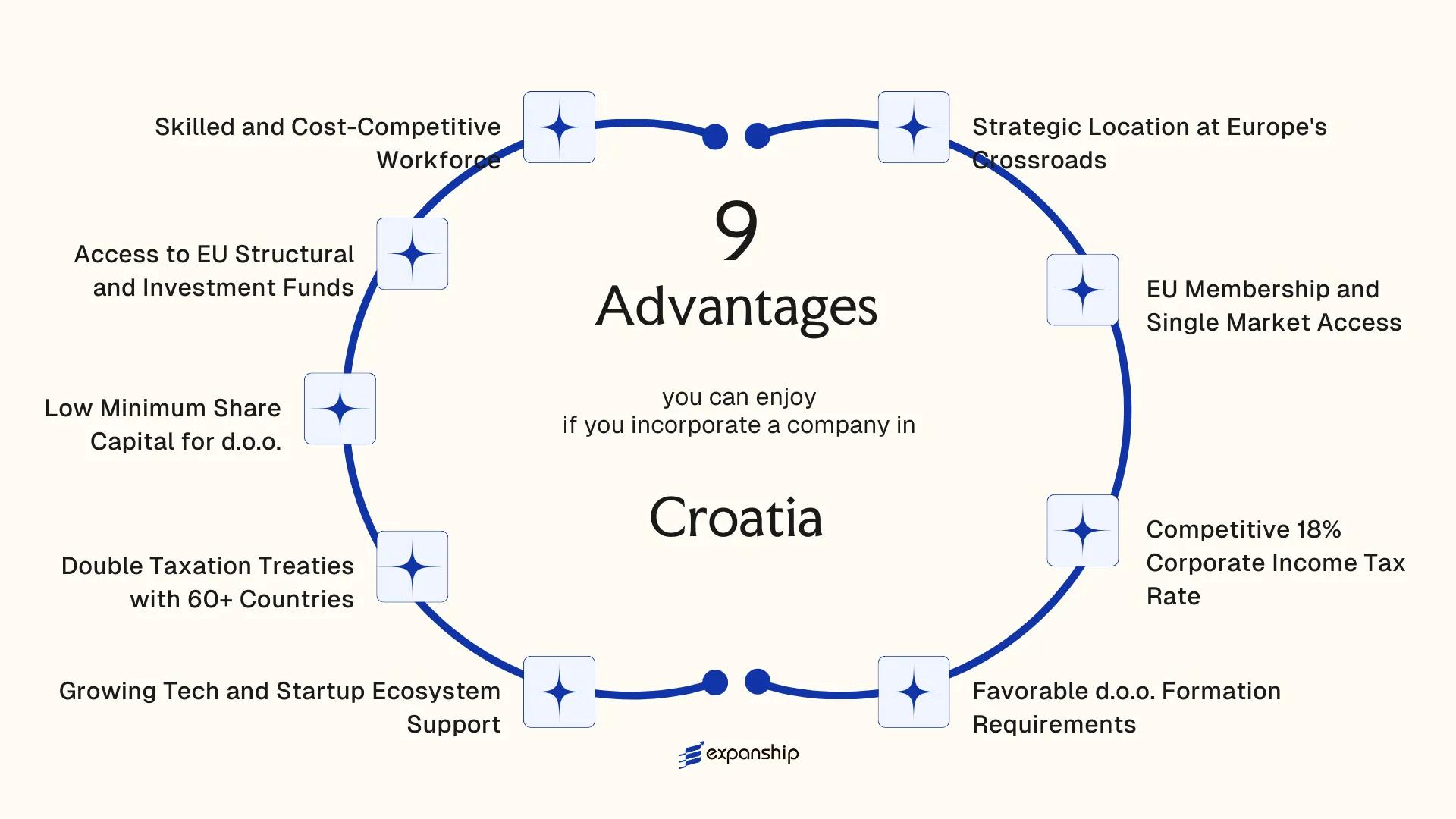

- Croatia's 18% corporate income tax rate, set under the Zakon o porezu na dobit, places resident companies below the EU average and applies uniformly to foreign-owned d.o.o. entities without additional levies tied to non-resident ownership.

- A minimum share capital requirement of just €2,650 allows foreign founders to establish a d.o.o. through the Sudski registar without committing significant capital at the point of incorporation.

- With double taxation treaties covering more than 60 jurisdictions, Croatian-registered entities can reduce withholding tax obligations on dividends, royalties, and interest across a broad range of cross-border structures.

- Non-resident founders and directors face no general ownership restrictions or prior approval requirements under Croatian company law, giving foreign investors full structural control from the outset.

Sitting at the intersection of Central and Southeastern Europe, Croatia is an independent EU member state with a well-defined legal framework for foreign business activity. Company registration is overseen by the court registry (Sudski registar), which operates under the jurisdiction of the commercial courts and serves as the official public register for legal entities. Foreign investors most commonly establish a d.o.o. when entering the Croatian market. The country operates a standard corporate tax system with treaty-based relief mechanisms that reduce withholding obligations across a broad network of bilateral agreements.

The benefits of incorporating in Croatia attract attention from businesses across the EU and beyond, in part because the legal framework places no general restrictions on foreign ownership of Croatian companies. Whether you're a sole founder or a multinational parent entity, the rules governing share acquisition and directorship are largely open to non-residents without prior approval requirements.

This article examines the concrete advantages that Croatia company formation offers to foreign investors and business owners considering a presence in the region.

Strategic Location at Europe's Crossroads

Croatia's geographic position gives your business direct physical access to three distinct regional markets: the EU's single market, the Western Balkans, and Central Europe. That convergence is a structural fact with real commercial consequences for supply chains, distribution, and regional headquarters decisions.

A Gateway Anchored by Infrastructure

Croatia shares land borders with Slovenia, Hungary, Bosnia and Herzegovina, Serbia, and Montenegro. Its Adriatic coastline connects to Italian ports via established maritime routes, while the Pan-European Transport Corridors Vb and X pass through Croatian territory, linking Central Europe to the Adriatic and Southeast Europe to Western Europe.

Access to Non-EU Markets Without Leaving the EU

Registering a Croatian entity gives your firm EU legal standing while placing it within practical reach of Western Balkan markets that sit outside the bloc. Trade relationships between Croatia and neighboring non-EU states are governed by the CEFTA agreement and bilateral arrangements, meaning regional commercial activity is not purely ad hoc.

A Croatian-registered company can serve both EU member states and Western Balkan markets from a single legal entity, reducing the need for parallel corporate structures across multiple jurisdictions.

EU Membership and Single Market Access

As an EU member state since 2004, Croatia grants incorporated entities full access to the single market — covering the free movement of goods, services, capital, and people across all 27 member states. For a foreign business owner, this means your Croatian company operates under the same market access rights as firms based in Germany or France, without requiring separate registrations or bilateral approvals in each country.

Membership in the EU customs union eliminates tariffs on intra-EU trade entirely. A firm incorporated in Croatia can export products to any EU member state without customs duties, and import inputs from across the bloc under the same terms. This directly reduces the cost structure for businesses using Croatia as a base for European distribution or manufacturing.

The practical advantages of EU-incorporated company status in Croatia extend to regulatory recognition:

- EU product certifications and CE markings obtained in Croatia are valid across all member states, removing the need for country-by-country compliance processes

- VAT registration in Croatia enables use of the EU's One Stop Shop (OSS) scheme for cross-border digital and e-commerce sales

- Financial services firms may access EU passporting rights under applicable directives, subject to sector-specific licensing conditions

- Public procurement markets across the EU are open to Croatian-registered entities on equal terms with domestic bidders

Croatia adopted the euro on 1 January 2023, which eliminates currency conversion costs and exchange rate risk on transactions settled within the eurozone.

Incorporate a Company in Croatia

Set up a Croatian d.o.o. with full EU single market access. Expanship manages the incorporation process across all required registrations.

Competitive 18% Corporate Income Tax Rate

Croatia's standard corporate income tax (porez na dobit) rate is 18%, governed by the Corporate Income Tax Act (Zakon o porezu na dobit). For companies with annual revenues below HRK 7.5 million (approximately EUR 995,000), a reduced rate of 10% applies. This tiered structure means smaller foreign-owned entities pay a materially lower rate during their early operating years, which directly reduces the tax burden while revenue is still scaling.

The 18% Croatia corporate income tax rate advantage becomes clearer when measured against the EU weighted average corporate tax rate, which has consistently exceeded 21%. For a foreign business generating taxable profit above the reduced-rate threshold, the standard rate still sits below that average, preserving more after-tax capital for reinvestment or repatriation.

| Annual Revenue Threshold | Applicable Tax Rate | Legal Basis |

|---|---|---|

| Up to ~EUR 995,000 | 10% | Zakon o porezu na dobit |

| Above ~EUR 995,000 | 18% | Zakon o porezu na dobit |

| EU Weighted Average (approx.) | 21%+ | European Commission data |

Tax liability is calculated on net profit, with allowable deductions reducing the taxable base under rules administered by the Porezna uprava (Tax Administration). Foreign investors benefit from the same rate structure as domestic entities, so there is no separate, less favorable regime applied to non-resident shareholders owning a Croatian company.

Favorable d.o.o. Formation Requirements

Forming a drustvo s ogranicenom odgovornoscu carries several structural advantages that directly reduce friction for foreign investors pursuing Croatia d.o.o. formation. The process is governed by the Companies Act (Zakon o trgovačkim društvima), which sets out a registration pathway through the court-administered commercial register.

Registration is handled through the Commercial Court Registry (Trgovački sud), and submissions can be filed digitally via the HITRO.HR one-stop-shop system. This means your entity can be established without requiring a physical presence in the country at each stage of the process.

A d.o.o. requires only one founder, who can be a foreign national or a foreign legal entity. No local director or resident shareholder is mandated under Croatian corporate law, which preserves full ownership control for the foreign investor.

The entity type itself limits shareholder liability to the value of their capital contribution. For a foreign business owner, this separation between personal and business liability is structurally enforced by statute, not just conventional practice.

Keep these points in mind:

- A d.o.o. can be formed with a single shareholder (natural or legal person)

- The Companies Act governs formation requirements

- Foreign nationals may hold 100% ownership with no local partner requirement

- Liability is limited to each member's contribution to share capital

- Digital registration is available through HITRO.HR

A d.o.o. can be incorporated with as few as one founder and no mandatory supervisory board, a structural simplicity that many EU jurisdictions with comparable entity types do not permit.

Growing Tech and Startup Ecosystem Support

Croatia's startup ecosystem has developed measurable institutional backing, making the country a credible base for tech-oriented foreign businesses. Under the Science and Innovation Investment Project and instruments tied to the Croatian Agency for SMEs, Innovations and Investments (HAMAG-BICRO), early-stage tech firms can access co-financing, grant schemes, and proof-of-concept funding that reduce initial capital exposure for foreign founders.

State-Backed Innovation Infrastructure

HAMAG-BICRO administers programs such as PoC (Proof of Concept) grants and ESIF equity instruments funded through EU cohesion mechanisms, giving qualifying tech startups access to non-dilutive capital at early development stages. For a foreign business owner, this means your entity can compete for public innovation funding on the same basis as domestic firms once incorporated under Croatian law.

The broader ecosystem includes technology parks and business incubators operating in Zagreb, Split, and Rijeka, providing affordable office infrastructure and peer networks. These facilities lower the fixed-cost burden during the market-entry phase without requiring long-term real estate commitments.

Digital Economy Positioning

Croatia's National Development Strategy 2030 identifies digital transformation as a priority, which has translated into structured public investment in digital infrastructure and skills programs. Tech companies incorporated locally can position themselves within this policy framework, accessing procurement opportunities and partnership programs tied to national digitalization initiatives.

Registered businesses in qualifying sectors may also benefit from R&D tax incentives under the Croatian Income Tax Act, which permits deductions on eligible research and development expenditure.

Maximize Croatia's Startup and Innovation Benefits for Your Business

Connect with Expanship to understand which innovation programs, R&D incentives, and ecosystem instruments your Croatian entity may qualify for.

Double Taxation Treaties with 60+ Countries

Croatia's double taxation treaty benefits extend across more than 60 bilateral agreements, covering major trading partners including Germany, the United States, the Netherlands, China, and most EU member states. These treaties are negotiated under the OECD Model Tax Convention framework and directly reduce or eliminate withholding taxes on dividends, interest, and royalties paid between a Croatian entity and a foreign counterpart.

- Withholding tax on dividends paid to non-resident shareholders can be reduced from the domestic rate to as low as 5% or 0% under specific treaty provisions, depending on the ownership threshold and the counterparty jurisdiction.

- Interest payments to foreign lenders are similarly capped under most treaties, reducing the tax cost of cross-border debt financing for your Croatian subsidiary.

- Royalty flows, which are common in IP-holding structures, benefit from reduced withholding rates that protect the economics of licensing arrangements between a Croatian firm and related foreign entities.

- Permanent establishment definitions within these treaties determine when your foreign business activity triggers a Croatian tax presence, giving you clearer planning boundaries.

- Tie-breaker and residency provisions prevent double taxation of corporate profits, meaning income is not taxed twice when funds move between Croatia and a treaty partner.

Treaty eligibility generally requires that the entity receiving income qualifies as a tax resident of the counterparty state under that treaty's terms.

Low Minimum Share Capital for d.o.o.

The Croatia d.o.o. low minimum share capital benefit is one of the more practical structural advantages available to foreign founders. Under the Companies Act (Zakon o trgovačkim društvima), the minimum share capital required to form a društvo s ograničenom odgovornošću is just €2,500. That threshold is low enough that a foreign investor can establish a fully operational, limited-liability entity without committing substantial capital before the business generates revenue.

By comparison, jurisdictions such as Austria require a minimum of €35,000 for an equivalent GmbH structure. Your initial outlay remains modest while still achieving the legal separation between personal and business liability that creditors and commercial partners expect.

The registered capital can be contributed in cash or in kind, and shares need not all be issued to a single member. This means a multi-founder structure is achievable from day one without additional capitalization pressure on any single party.

A foreign investor establishing a d.o.o. with the minimum €2,500 temeljni kapital retains the remaining capital for operational expenditure, hiring, or market entry costs, rather than holding it as a statutory reserve with no immediate commercial function.

Access to EU Structural and Investment Funds

Croatia EU structural funds access for businesses represents one of the more tangible financial advantages of incorporating locally. As a member state, Croatia receives allocations through the European Structural and Investment Funds (ESIF), which include the European Regional Development Fund (ERDF), the Cohesion Fund, and the European Social Fund Plus (ESF+). For the 2021-2027 programming period, Croatia is allocated approximately EUR 10 billion across these instruments.

Companies registered in Croatia can apply for co-financing through these mechanisms, which cover capital investment, R&D activity, workforce development, and digital transformation projects. The Ministry of Regional Development and EU Funds serves as the national coordinating body, while sector-specific intermediary bodies manage calls under their respective operational programmes.

Key funding instruments available to incorporated entities include:

- ERDF grants for SME competitiveness and innovation projects

- ESF+ co-financing for training and employment programmes

- Cohesion Fund support for infrastructure-linked business activity

- European Investment Fund (EIF) instruments, including guarantees and equity for growth-stage companies

Access requires a registered legal entity in Croatia, meaning foreign owners operating through a local d.o.o. are fully eligible to apply on equal terms with domestic firms.

Most EU-funded calls under Croatian operational programmes require the applicant company to have been registered and operational for a minimum period, often 12 to 24 months, before the application date.

Skilled and Cost-Competitive Workforce

Croatia skilled workforce advantages for businesses are grounded in measurable structural factors, not general claims. The country's tertiary education enrollment rate consistently exceeds the EU average, producing graduates in engineering, information technology, economics, and natural sciences who enter the labor market at wage levels well below those in Western Europe.

Average gross monthly wages in Croatia sit considerably lower than in Germany, Austria, or the Netherlands, while the workforce operates under EU employment law standards. For a foreign-owned d.o.o., this means your payroll costs can remain a fraction of what comparable roles would command in higher-cost member states, without sacrificing the legal protections and contractual predictability that come with operating inside the EU regulatory framework.

Employment relationships in Croatia are governed by the Labor Act (Zakon o radu), which sets out clear rules on contracts, termination procedures, and working time. The Act distinguishes between fixed-term and indefinite contracts, giving your business defined options for workforce planning from day one.

The workforce also carries strong multilingual capacity. English proficiency is high among younger professionals, particularly in urban centers such as Zagreb and Split. Several Croatian universities offer degree programs conducted in English, which affects the practical communication capacity your business can rely on.

- IT and tech professionals are among the most cost-competitive in the EU relative to their skill level

- Zagreb's universities supply a consistent pipeline of STEM graduates annually

- Social contribution rates for employers are defined under the Contributions Act (Zakon o doprinosima), providing cost predictability

Why Croatia Stands Out Among European Jurisdictions

Three jurisdictions consistently appear in the same investor conversations as Croatia: Slovenia, Hungary, and Bulgaria. All four are EU members targeting foreign-owned entities, share overlapping treaty networks, and compete for similar inbound investment. The comparison below focuses on parameters where Croatia holds a neutral or favourable position, based on publicly available regulatory data.

What the table reflects, but cannot fully convey, is the cumulative effect of these parameters. An 18% corporate income tax rate, codified under the Corporate Income Tax Act, sits two percentage points below Hungary's standard rate for larger entities and four points below Slovenia's. Combined with a minimum share capital threshold that imposes no meaningful barrier to entry for a foreign-owned d.o.o., the structural conditions for establishing a presence here require less initial capital commitment than several comparable EU jurisdictions. For your business, that means fewer administrative prerequisites before trading can begin.

| Parameter | Croatia | Slovenia | Hungary | Bulgaria |

|---|---|---|---|---|

| Corporate Income Tax Rate | 18% (10% for small companies) | 19% | 9% (above threshold: 15%) | 10% |

| Minimum Share Capital (LLC equivalent) | EUR 2,500 | EUR 7,500 | HUF 3,000,000 (~EUR 7,500) | BGN 2 (~EUR 1) |

| EU Member | Yes | Yes | Yes | Yes |

| Double Tax Treaties | 60+ | 60+ | 90+ | 70+ |

| Official Language Requirement for Registration | Croatian | Slovenian | Hungarian | Bulgarian |

Compliance Services for Companies in Croatia

Maintain your Croatian d.o.o. in good standing with Expanship's ongoing compliance support, covering annual filings, tax obligations, and regulatory reporting under Croatian law.

Conclusion

Croatia offers a structurally coherent case for foreign incorporation: EU market access through a member state with a sub-20% corporate rate, a d.o.o. formation framework requiring just €2,650 in minimum share capital, and an active treaty network covering more than 60 jurisdictions that directly reduces withholding tax exposure on cross-border income.

Among the benefits of incorporating in Croatia, two factors carry particular weight for foreign business owners. The 18% corporate income tax rate, governed by the Zakon o porezu na dobit, applies uniformly to resident entities, and the d.o.o. structure allows non-resident directors and shareholders without requiring local equity participation. Together, these features give foreign-owned firms meaningful cost and structural control from the outset.

Whether your business operates in manufacturing, digital services, or trade, the advantages of Croatia business registration are not universally applicable. A holding company may prioritize the treaty network; a tech firm may place greater value on EU fund eligibility and the growing startup infrastructure centred in Zagreb. Identifying which factors align with your specific structure and tax position determines how much of the available advantage you can actually capture. For businesses that meet those criteria, the regulatory and fiscal framework in place supports a clear path to operational and tax efficiency within the EU.

Start Your Croatian Company with Expanship Today

Incorporating a d.o.o. through Expanship connects you to the full range of advantages this blog has outlined, from the 18% corporate tax rate and EU Single Market access to the double taxation treaty network and structural fund eligibility. Expanship manages the end-to-end formation process with the Croatian court registry known as the trgovački sud, handling every procedural and documentary requirement on your behalf.

The service scope covers the practical steps that carry the most friction for foreign principals:

- Preparation and legalization of incorporation documents, including the articles of association

- Registered agent and registered office provision to satisfy the mandatory Croatian address requirement

- Filing and liaison with the Commercial Court Registry and the Croatian Financial Agency (FINA) for OIB tax number registration

- Post-incorporation compliance management, including annual financial reporting obligations under the Accounting Act

- Banking introduction assistance to support corporate account opening with a Croatian financial institution

Croatia company formation services through Expanship are structured to match the specific regulatory sequence the local system requires, not a generic offshore template applied indiscriminately. Each engagement reflects the actual obligations imposed by the Zakon o trgovačkim društvima, the Companies Act that governs d.o.o. formation and ongoing operation.

To discuss your requirements, contact Expanship Croatia.

Frequently Asked Questions (FAQ)

The standard corporate income tax rate is 18%, applied under the Corporate Income Tax Act (Zakon o porezu na dobit). Entities with annual revenues below HRK 7.5 million (approximately EUR 995,000) are taxed at a reduced rate of 10%. This threshold-based structure means the applicable rate depends directly on your firm's revenue in the preceding tax year.

Registration through the Commercial Court Registry (Sudski registar) typically takes between five and ten business days once all required documentation has been submitted in proper order. The process involves notarization of the founding act and submission to the relevant commercial court. Delays generally occur when documentation is incomplete or requires apostille certification for foreign-issued documents.

Croatia's tax treaties, of which there are over 60 in force, generally cover multiple income categories including dividends, interest, royalties, and capital gains, not solely business profits. The exact withholding tax rates on dividends and royalties vary by treaty and are defined in the bilateral agreement with each signatory country. You should consult the specific treaty text for the counterparty jurisdiction, as rates and exemption thresholds differ materially between agreements.

A d.o.o. must have a registered seat (sjedište) in Croatia, as required under the Companies Act. A physical or virtual registered address that satisfies the legal seat requirement is acceptable, provided it appears in the Commercial Court Registry. The address serves as the official point of contact for regulatory correspondence from bodies such as the Croatian Financial Agency (FINA) and the Tax Administration (Porezna uprava).

The minimum share capital for a d.o.o. is HRK 20,000 (approximately EUR 2,650), and this amount must be registered at the time of incorporation, though it does not need to be maintained as a permanent liquid reserve in all circumstances. If the company's net assets fall below the registered share capital due to accumulated losses, the directors are required under the Companies Act to convene a general meeting to address the situation. Failure to act on a capital deficiency can expose directors to personal liability and, in serious cases, trigger compulsory dissolution proceedings.

Yes, a qualifying Croatian company can apply for EU Structural and Investment Funds, including the European Regional Development Fund and the European Social Fund. In Croatia, these programs are administered through the Ministry of Regional Development and EU Funds (Ministarstvo regionalnoga razvoja i fondova Europske unije), which publishes calls for applications under the national operational programs. Eligibility conditions vary by program and typically include criteria related to company size, sector, and project location within designated development regions.

Croatia's 18% corporate income tax rate and participation exemption provisions make it a mid-range option within the EU, less tax-efficient than jurisdictions such as Ireland (12.5%) or Hungary (9%), but more favorable than Germany or France for certain structures. The reduced 10% rate for smaller entities and the treaty network of 60+ agreements add planning value, particularly for investors routing income from Central and Southeast European operations. The suitability of Croatia as a holding location depends on the investor's specific income flows, residency position, and the treaty coverage between Croatia and their home jurisdiction.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.