Key Takeaways

- Honduras operates a territorial tax system, meaning corporate income generated outside the country is generally exempt from local income tax regardless of entity type.

- The Sociedad Anónima (S.A.) is the most commonly registered entity in Honduras, preferred by domestic and foreign investors for its transferable share structure and broad sectoral acceptance.

- Foreign companies entering Honduras can establish either a branch office, which retains the parent's legal identity, or a representative office restricted to non-commercial functions.

- All business entity registrations in Honduras fall under the jurisdiction of the Registro Mercantil, operating within the framework of the Código de Comercio.

Introduction to Entity Types in Honduras

Honduras is a Central American republic bordered by Guatemala, El Salvador, and Nicaragua, with coastlines on both the Caribbean Sea and the Pacific Ocean. Understanding the types of business entities in Honduras is the starting point for any foreign investor or local entrepreneur planning to establish a formal commercial presence in the country.

Company registration falls under the jurisdiction of the Registro Mercantil, the commercial registry that operates within the framework of Honduras's Código de Comercio (Commercial Code). Oversight of corporate compliance and certain sector-specific activities involves additional government bodies depending on the nature of the business.

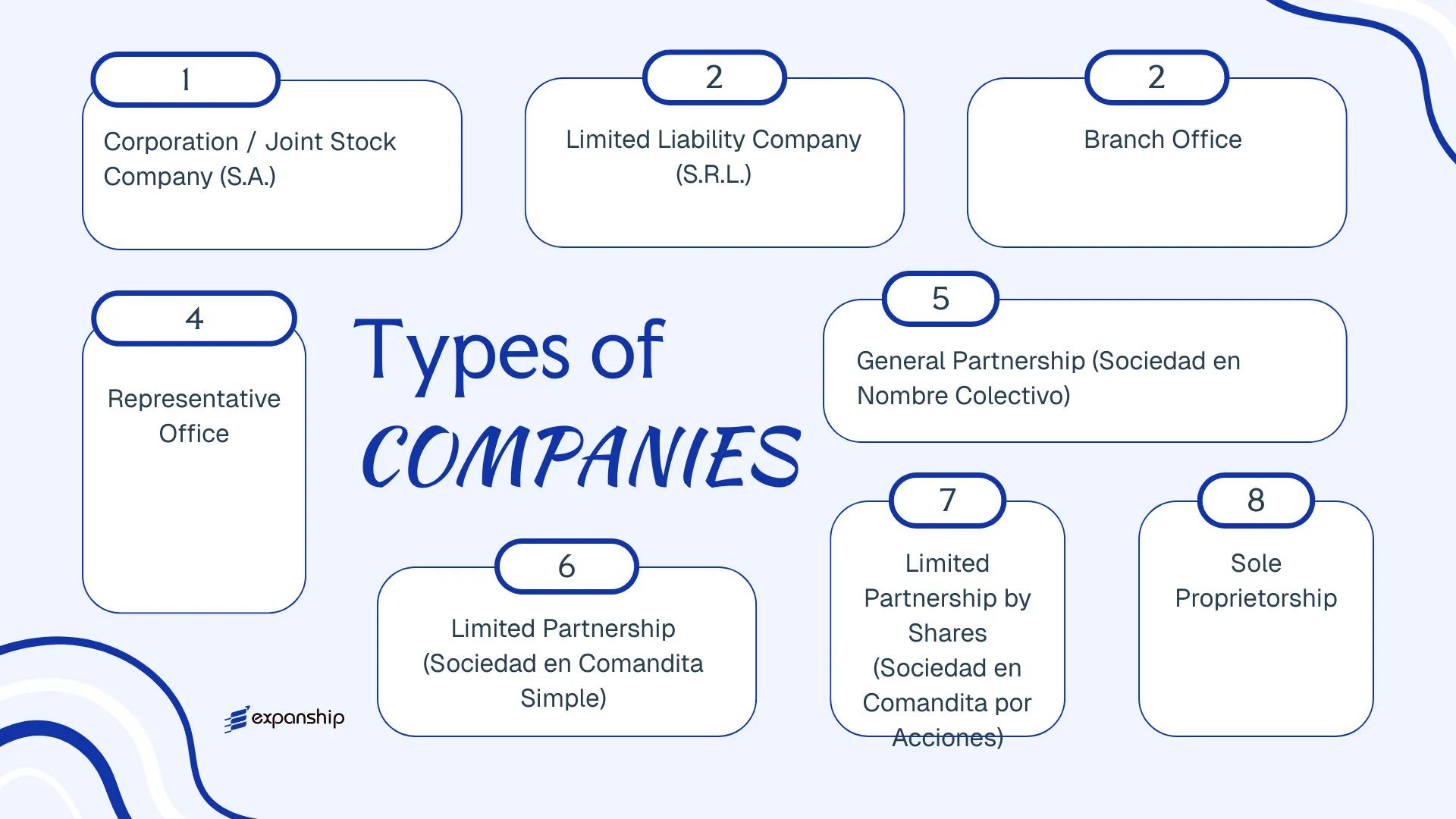

Honduras operates a territorial tax system, meaning income generated outside the country is generally not subject to local income tax. The available corporate structures include the Sociedad Anónima (S.A.), Sociedad de Responsabilidad Limitada (S.R.L.), Sociedad en Nombre Colectivo, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones, sole proprietorship, and foreign entity options such as branch and representative offices. Each structure carries distinct liability, governance, and compliance requirements that this article examines in detail.

An Overview of Business Structures in Honduras

Honduras recognizes several distinct legal forms for conducting business, all governed primarily by the Código de Comercio (Commercial Code) of 1950 and its subsequent amendments. Each structure carries different implications for liability, governance, and taxation, and each is designed to serve a specific type of commercial activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima (S.A.) | Corporation | Limited to shares | Taxable | Permitted | 2 shareholders | SAR / Registro Mercantil | Código de Comercio |

| Sociedad de Responsabilidad Limitada (S.R.L.) | Limited liability company | Limited to quota | Taxable | Permitted | 2 partners | SAR / Registro Mercantil | Código de Comercio |

| Sociedad en Nombre Colectivo | General partnership | Unlimited, joint | Taxable | Permitted | 2 partners | Registro Mercantil | Código de Comercio |

| Sociedad en Comandita Simple | Limited partnership | Mixed | Taxable | Permitted | 2 partners | Registro Mercantil | Código de Comercio |

| Sociedad en Comandita por Acciones | Share-based limited partnership | Mixed | Taxable | Permitted | 2 partners | Registro Mercantil | Código de Comercio |

| Branch Office | Foreign branch | Parent liable | Taxable | Permitted | 1 foreign entity | SAR / Registro Mercantil | Código de Comercio |

| Representative Office | Non-trading presence | Parent liable | Limited scope | Not permitted | 1 foreign entity | Registro Mercantil | Código de Comercio |

| Sole Proprietorship | Individual trader | Unlimited | Taxable | Permitted | 1 individual | SAR / Registro Mercantil | Código de Comercio |

Each of these structures is examined in full in the sections below.

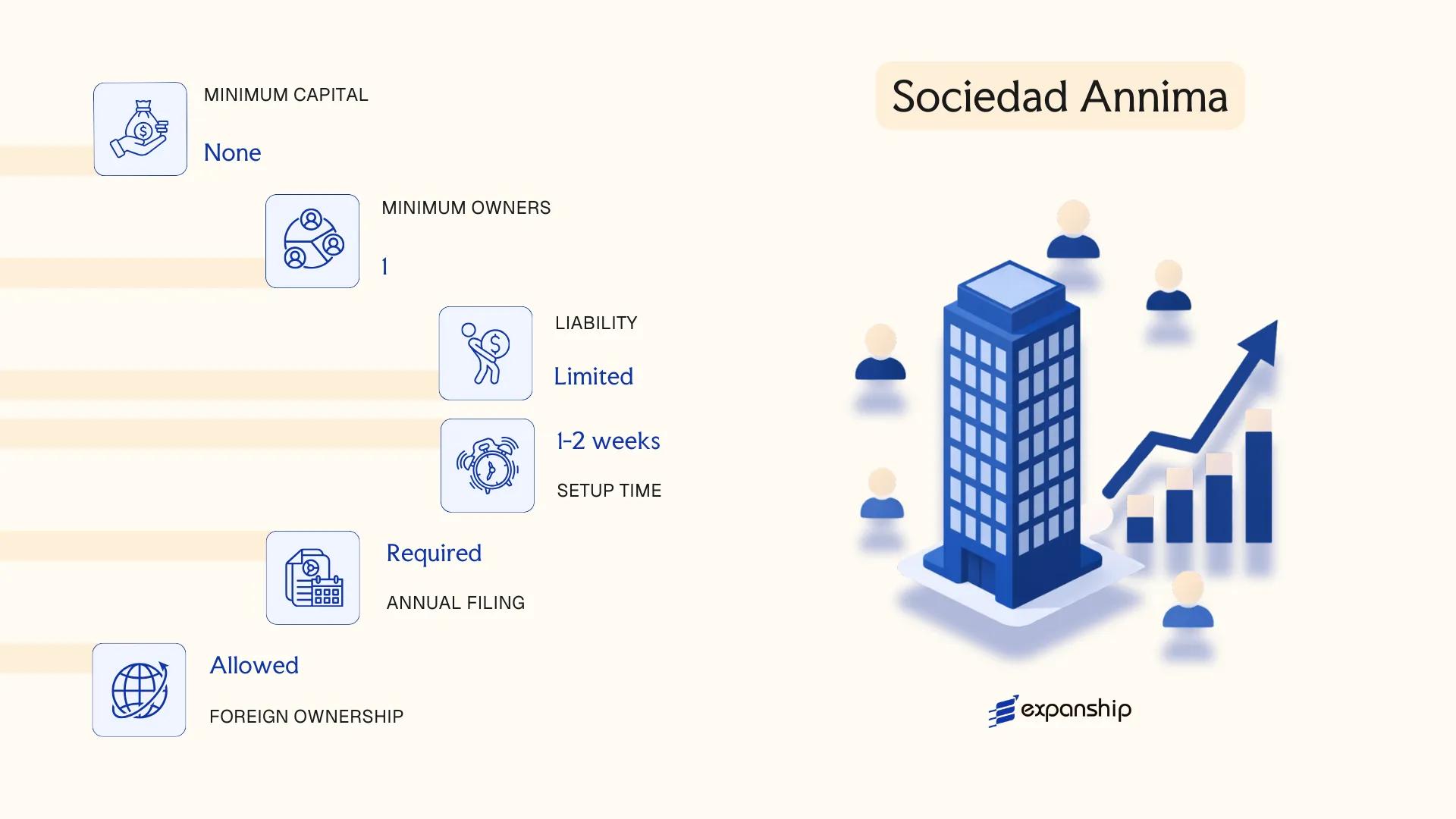

Sociedad Anónima (S.A.)

Honduras Sociedad Anónima formation is governed primarily by the Código de Comercio de Honduras (Decree No. 73-1950), which establishes the S.A. as a capital-based company with full separate legal personality. Shareholders hold no personal liability for corporate obligations beyond their capital contributions.

Ownership is divided into transferable shares, making the structure suitable for mid-to-large enterprises, joint ventures, and foreign direct investment. Share transfers do not require unanimous shareholder approval unless the bylaws restrict them.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima (S.A.) | Capital company; separate legal personality |

| Members | Shareholders (minimum 2, no statutory maximum) | No residency requirement for shareholders |

| Governing Body | Board of Directors (minimum 3 directors) or a sole administrator permitted in some structures | Directors need not be Honduran residents |

| Local Presence | Registered legal address in Honduras required | A registered agent is not a statutory requirement but a local address must be maintained |

| Capital | Minimum paid-in capital of L 25,000 (Honduran Lempira); no foreign currency restriction | Capital divided into nominative or bearer shares (bearer shares now restricted in practice) |

| Privacy | Shareholder and director names appear in public registry filings | Honduras has a public Registro Mercantil; beneficial ownership disclosure rules apply |

Focus Points

- Taxation: Corporate income tax is levied at 19% on net taxable income; VAT (Impuesto Sobre Ventas) applies at 15% (18% on certain goods); a 10% withholding tax applies to dividends paid to non-residents; a 1.5% solidarity contribution (Aportación Solidaria Temporal) may apply to firms with higher net income.

- Annual Compliance: Annual financial statements must be filed with the Registro Mercantil; accounting records must be maintained in accordance with the Código de Comercio.

- Economic Substance: No dedicated economic substance regime, but tax residency and permanent establishment rules under domestic law and applicable treaties determine where income is taxed.

- Treaty Access: Honduras has a limited tax treaty network; access to withholding tax reductions depends on the counterparty jurisdiction.

- Conversion: An S.A. may be converted into an S.R.L. or other commercial form through a notarized public deed and Registro Mercantil re-registration.

Closing

The S.A. is the standard vehicle for foreign investors, holding structures, and trading operations that require freely transferable shares and a scalable governance framework. Its key advantage is capital flexibility; the principal drawback is the public disclosure of shareholders and directors through mandatory Registro Mercantil filings.

Foreign investors and multi-shareholder ventures seeking a scalable, capital-based structure with unrestricted share transferability.

Company Incorporation in Honduras

Incorporate a Sociedad Anónima or other business entity in Honduras with end-to-end support from registration through post-incorporation compliance.

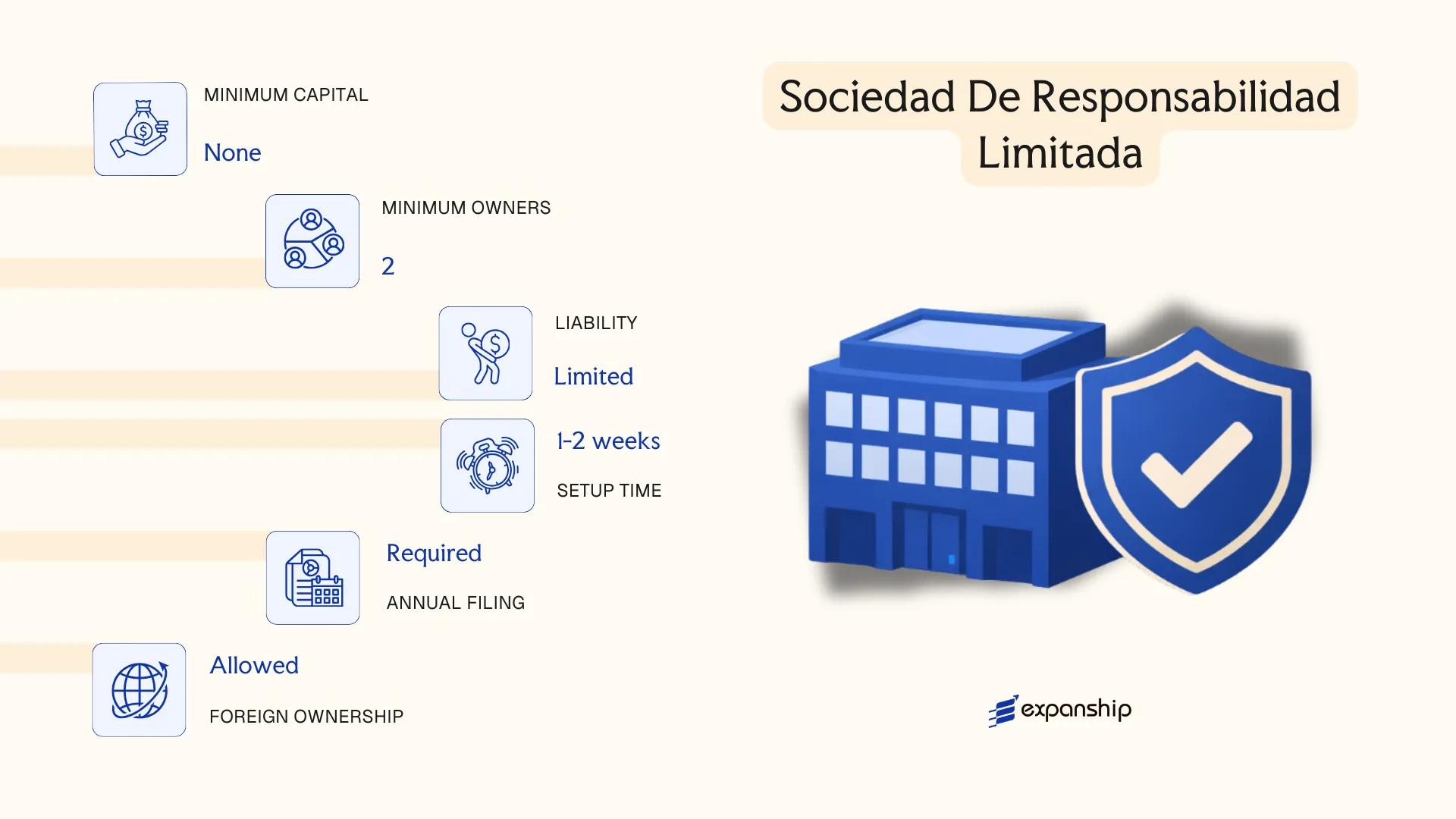

Sociedad de Responsabilidad Limitada (S.R.L.)

The Honduras Sociedad de Responsabilidad Limitada is governed by the Honduran Commercial Code (Código de Comercio, Decree No. 73-1950) and its subsequent amendments. It carries separate legal personality, meaning the entity's obligations are distinct from those of its members.

Structurally, the S.R.L. sits between a corporation and a partnership. Liability is capped at each member's capital contribution, yet the firm retains a more closed, private character than a Sociedad Anónima — ownership transfers are restricted and require member consent.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad de Responsabilidad Limitada (S.R.L.) | Registered with the Honduran Mercantile Registry (Registro Mercantil) |

| Members | Minimum 2, maximum 20 | Members (socios); no public shareholding permitted |

| Management | One or more managers (gerentes) | Can be members or third parties |

| Local Presence | Registered address in Honduras required | Registered agent not mandated by statute but a local address is obligatory |

| Capital | No statutory minimum; denominated in Honduran Lempira (HNL) | Divided into quotas (cuotas), not freely transferable shares |

| Privacy | Member names appear in public registry | Less disclosure than an S.A. in practice; no share certificates issued |

Focus Points

- Taxation: Subject to corporate income tax at 25% on net profits; VAT applies at 15% on taxable supplies; dividend withholding tax applies to distributions; stamp duty applies on certain instruments.

- Annual Compliance: Annual financial statements and tax filings required; registration with the Servicio de Administración de Rentas (SAR) is mandatory.

- Quota Transfers: Transfer of quotas to non-members requires prior consent from the majority of existing socios, as stipulated in the Commercial Code.

- Treaty Access: Honduras has a limited tax treaty network; S.R.L. entities can access treaties where in force, subject to beneficial ownership requirements.

- Conversion: Conversion to a Sociedad Anónima is legally permissible but requires notarial deed, SAR notification, and re-registration with the Registro Mercantil.

Closing

The S.R.L. suits closely held trading businesses and family-owned enterprises where ownership control and privacy of internal governance are priorities; the 20-member cap, however, makes it unsuitable for ventures requiring broad investor participation.

Small to mid-size closely held businesses and family enterprises seeking limited liability without the administrative overhead of a full Sociedad Anónima structure.

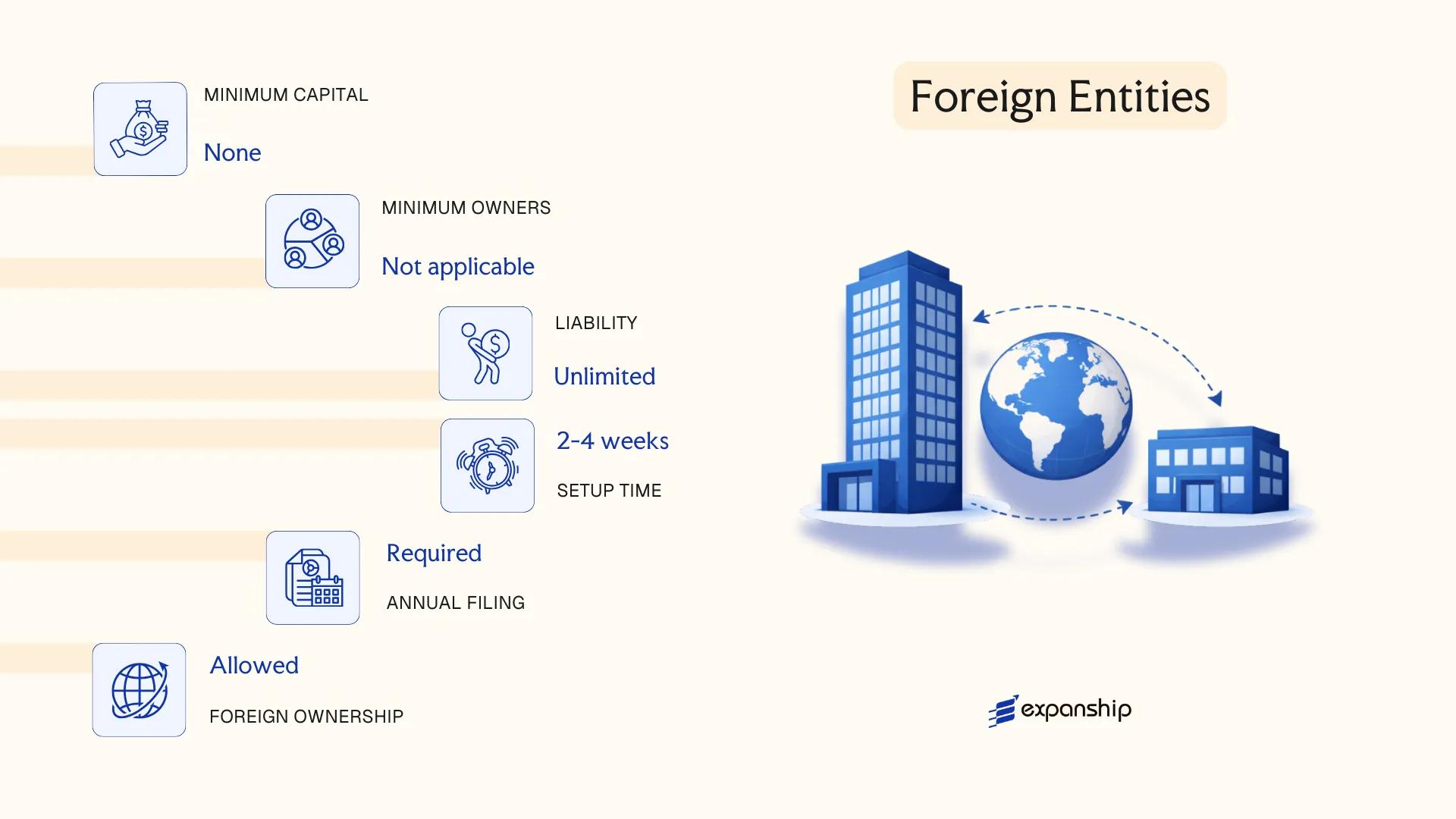

Foreign Entities in Honduras [Branch Office, Representative Office]

Establishing a foreign company branch office Honduras operates under the Commerce Code of Honduras (Decreto No. 73-1950) and its subsequent amendments, which govern how foreign entities may conduct business activities within the country. A branch office is not a separate legal entity — it remains an extension of its parent company, which retains full legal and financial liability for the branch's obligations.

A representative office, by contrast, is restricted to promotional and liaison activities; it cannot generate revenue or enter into commercial contracts in its own right. Both structures require registration with the Honduran Chamber of Commerce and Industry and must appoint a legal representative domiciled in Honduras.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None (extension of parent) | None (extension of parent) |

| Liability | Parent bears full liability | Parent bears full liability |

| Commercial Activity | Permitted | Not permitted |

| Legal Representative | Required (Honduras-resident) | Required (Honduras-resident) |

| Registered Address | Required in Honduras | Required in Honduras |

| Capital Requirement | No statutory minimum; parent's capital applies | None |

| Privacy | Parent company documents become public record upon registration | Parent company documents become public record upon registration |

Focus Points

- Taxation: Branch profits are subject to the standard corporate income tax rate of 25%; remittances to the parent may attract withholding tax, and the branch is subject to VAT at 15% on taxable transactions.

- Economic Substance: The branch must demonstrate genuine operational presence; a nominal address without actual activity may attract scrutiny from the Servicio de Administración de Rentas (SAR).

- Annual Compliance: Annual financial statements must be filed with the Honduran tax authority, and the appointed legal representative must remain active and duly registered.

- Treaty Access: Honduras has a limited tax treaty network; access to double taxation agreements depends on the parent's jurisdiction of incorporation.

- Restrictions: A representative office cannot invoice, collect revenue, or sign commercial contracts — any deviation from this scope requires conversion to a branch or locally incorporated entity.

Closing

A branch office suits foreign firms seeking direct operational activity without incorporating a separate subsidiary, though the parent company's unlimited liability exposure is a material drawback for risk-conscious businesses. Representative offices are used primarily for market research or pre-sales activity where no immediate revenue generation is planned.

A branch office is best suited for established foreign corporations that require a direct operational presence and are prepared to assume full parental liability for Honduras-based activities.

Partnerships in Honduras [Sociedad en Nombre Colectivo, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones]

Partnership structures in Honduras are governed by the Código de Comercio (Commercial Code), enacted in 1950 and subsequently amended. Three distinct partnership forms exist under this framework, each carrying separate legal personality upon registration with the Registro Mercantil: the Sociedad en Nombre Colectivo, the Sociedad en Comandita Simple, and the Sociedad en Comandita por Acciones.

Each form differs primarily in how liability is distributed among partners. Unlimited personal liability for all partners characterises the general partnership, while the comandita structures introduce a split between active managing partners and passive investors whose exposure is capped.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Separate legal entity | Registered with the Registro Mercantil |

| Members | Partners (socios); minimum 2, no statutory maximum | General partners bear unlimited liability |

| Local Presence | Registered office in Honduras required | No statutory resident agent requirement, but a fiscal address is mandatory |

| Capital | No statutory minimum; denominated in Honduran Lempira (HNL) | Comandita por Acciones divides passive partner capital into shares |

| Privacy | Partner names disclosed in public registry | Limited confidentiality available |

Focus Points

- Taxation: Subject to corporate income tax at 25%, plus a 1.5% solidarity contribution on net taxable income exceeding HNL 1 million; VAT at 15% applies to commercial activity; profit distributions to foreign partners attract withholding tax.

- Annual Compliance: Obligatory filing of financial statements and tax returns with the Servicio de Administración de Rentas (SAR); annual renewal with the Registro Mercantil required.

- Treaty Access: Honduras has a limited tax treaty network; partnership entities generally do not benefit from reduced withholding rates.

- Conversion: Partnership forms may be converted to a Sociedad Anónima or S.R.L. through a notarial deed and re-registration, subject to creditor notification requirements.

- Restrictions: General partners in all three forms cannot transfer their partnership interest without unanimous consent of remaining partners.

Sub-Types

Sociedad en Nombre Colectivo

All partners carry joint and unlimited liability for the firm's obligations. This structure is uncommon in commercial practice and is used primarily among closely-knit professional groups where mutual trust among partners is the principal operating control.

Sociedad en Comandita Simple

Two classes of partners coexist: general partners (socios gestores) with unlimited liability who manage the business, and limited partners (socios comanditarios) whose liability is capped at their agreed capital contribution. Capital is not divided into transferable shares.

Sociedad en Comandita por Acciones

The passive partners' capital is divided into shares (acciones), making this the most transferable of the three forms. General partners retain unlimited liability, while shareholders hold limited liability proportional to their shareholding, giving this structure a hybrid character closer to a corporation.

Closing

These partnership forms are used occasionally for family-owned trading operations or professional service arrangements where relational accountability is valued over structural complexity. The ability to admit passive investors through the comandita por acciones structure offers flexibility, though unlimited personal liability for managing partners remains a significant legal exposure that discourages broader commercial adoption.

Partnership structures in Honduras are best suited for small, closely-held businesses or professional partnerships where the partners have an established relationship and accept the liability implications of shared management.

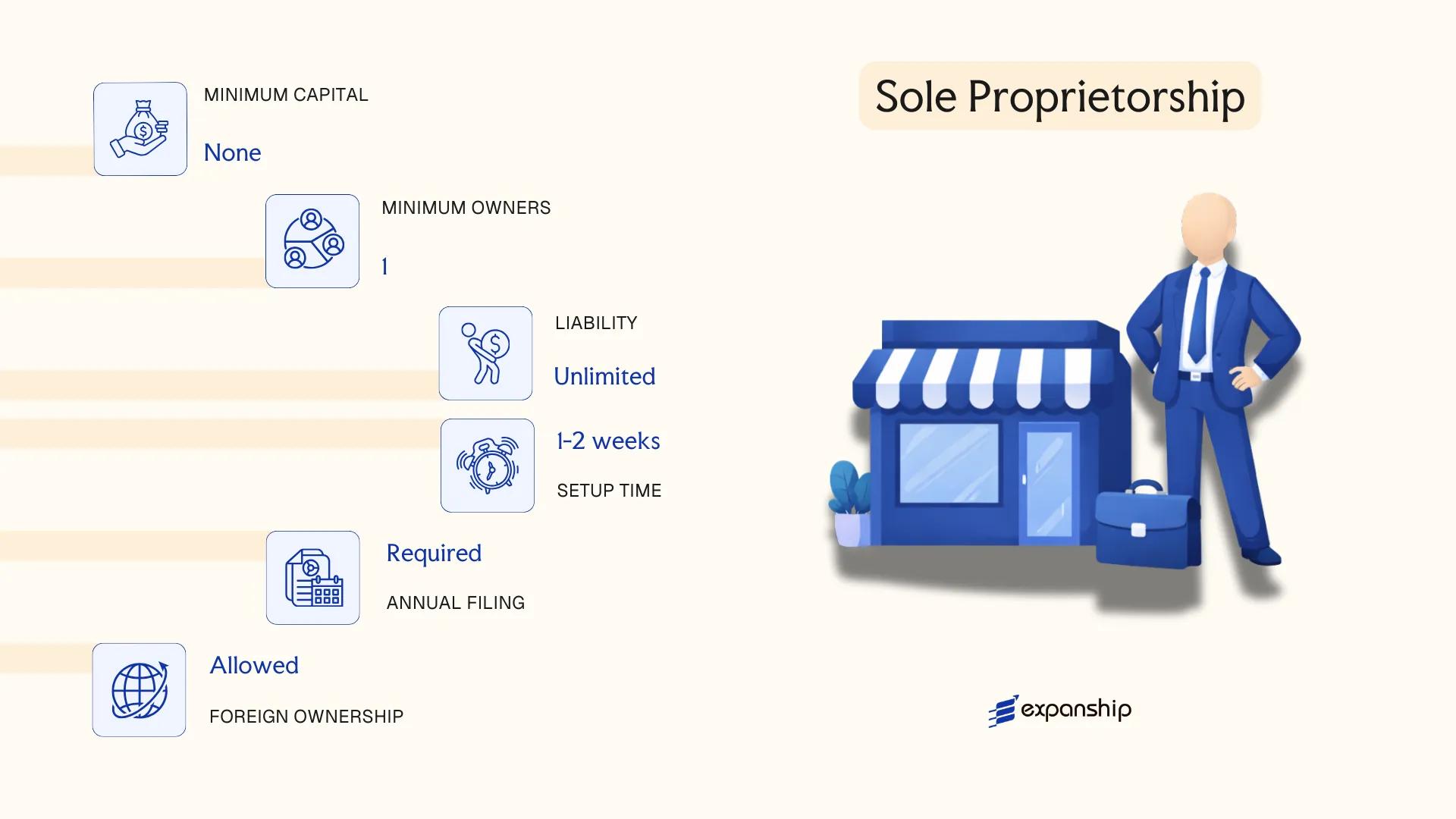

Sole Proprietorship in Honduras

Operating a sole proprietorship in Honduras means conducting business as an individual without forming a separate legal entity. The applicable framework falls under the Código de Comercio (Commercial Code) of Honduras, which permits natural persons to register as individual merchants (comerciantes individuales). Because no distinct legal person is created, the proprietor's personal assets are fully exposed to business liabilities.

Registration is handled through the Registro Mercantil, and depending on the nature of the activity, the Servicio de Administración de Rentas (SAR) will require enrollment for tax purposes. A business trade name may be registered separately, but the legal identity remains that of the individual.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Individual merchant (comerciante individual) | No separate legal personality from the owner |

| Member Title | Proprietor | Single individual only; no co-owners permitted |

| Liability | Unlimited personal liability | Personal assets at risk for all business obligations |

| Local Presence | Physical address required | Must maintain a registerable business address in-country |

| Capital | No statutory minimum | Declared capital is reported at registration but not legally prescribed |

| Privacy | Owner's name is publicly registered | No structural privacy available |

Focus Points

- Taxation: Subject to income tax under SAR's progressive or flat-rate schedules for individuals; VAT (Impuesto Sobre Ventas) at 15% applies to taxable sales; no corporate tax layer exists.

- Annual Compliance: Annual income tax filing required with SAR; municipal business license renewal typically required.

- Treaty Access: As an individual rather than a corporate entity, access to Honduras's double tax treaties is limited and generally unavailable for business income structuring.

- Conversion: Can be converted into a formal entity such as an S.R.L. or S.A. through a separate incorporation process; no automatic conversion mechanism exists.

- Restrictions: Foreign nationals face additional requirements to operate as individual merchants, including residency or work permit conditions.

Closing

This structure suits small-scale local traders, freelancers, and self-employed individuals conducting low-risk domestic activities. The absence of minimum capital requirements reduces the barrier to entry, but unlimited personal liability makes it unsuitable for operations carrying significant financial or legal exposure.

Best suited for Honduran residents or nationals running small, low-liability businesses who need a simple, low-cost registration without corporate governance obligations.

How to Choose the Right Entity Type in Honduras

Selecting the correct legal structure before incorporation is a decision with lasting operational and financial consequences. Knowing how to choose a business entity in Honduras requires matching your commercial objectives against the specific attributes of each available form under the Código de Comercio de Honduras.

Why Your Entity Choice Matters

The structure you register determines what your business can and cannot do legally, financially, and administratively.

- Forming a Sociedad Anónima when your activity falls under a regulated sector — such as banking or insurance — without the corresponding licence from the Comisión Nacional de Bancos y Seguros exposes the entity to administrative sanctions and potential cancellation of its operating permit.

- Choosing a structure that requires audited financial statements when your firm operates as a single-person consultancy introduces annual compliance costs that would not apply to a sole proprietorship or a simplified S.R.L.

- Registering a foreign branch to conduct local commercial activity without filing with the Registro Mercantil constitutes an operating violation under Articles 357–362 of the Código de Comercio.

- Selecting a partnership structure when liability segregation is a priority leaves each general partner personally exposed to the entity's obligations with no statutory cap.

Key Factors to Consider

- Business Activity: Active trading, asset holding, or regulated-sector operations each point toward a different entity form under Honduran commercial law.

- Ownership Structure: Single-owner operations can function as a sole proprietorship, while multi-party ventures require a structure with defined capital participation rules.

- Liability Exposure: Your tolerance for personal liability determines whether an S.A. or S.R.L. — both offering limited liability — is more appropriate than a general partnership.

- Management Flexibility: An S.R.L. allows simpler governance without a formal board, whereas an S.A. requires a Junta Directiva with defined officer roles.

- Local vs. Cross-Border Operations: A foreign branch can operate locally but remains an extension of the parent entity with no separate legal personality in Honduras.

- Exit Strategy: Not all Honduran entity types permit redomiciliation or conversion; confirming this before formation avoids costly restructuring later.

Compliance Services for Companies in Honduras

Maintain your Honduran entity in good standing with ongoing compliance support, including annual filings, Registro Mercantil renewals, and regulatory reporting.

Conclusion

Selecting the right structure before Honduras company incorporation determines your compliance obligations, liability exposure, and operational flexibility from day one. The Sociedad Anónima remains the most registered entity type, favored by both domestic and foreign investors for its transferable share structure and broad acceptance across sectors. The S.R.L. suits smaller, closely held businesses where owners prefer direct control with capped membership. For foreign firms testing the market, a branch office maintains the parent's legal identity, while a representative office limits activity to non-commercial functions. Partnerships under the Commercial Code serve specialized arrangements but carry personal liability considerations that make them less common in practice.

Regulatory oversight through the Registro Mercantil and the Comisión Nacional de Bancos y Seguros continues to evolve, with Honduras expanding its bilateral investment treaty network gradually. Understanding where each entity fits within that framework is where structured professional guidance adds practical value.

How Expanship Can Assist You

Expanship Honduras company registration services cover the full process of forming and maintaining a business entity under Honduran law, from selecting between a Sociedad Anónima and a Sociedad de Responsabilidad Limitada to satisfying the filing requirements set by the Registro Mercantil. Your corporate structure choices have direct compliance consequences, and getting the foundation right matters from day one.

Expanship's Honduras incorporation assistance spans the entire setup process and beyond:

- Document preparation, notarization, and apostille legalization

- Registered agent and local office provision

- Filing and liaison with the Registro Mercantil and relevant municipal authorities

- Post-incorporation compliance management, including annual obligations

- Banking introduction assistance for local and international accounts

- Ongoing registered agent maintenance

Get in touch with Expanship Honduras to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Sociedad Anónima (S.A.) is the most frequently formed entity. Its share-based capital structure, transferable ownership, and suitability for both domestic operations and foreign investment make it the default choice across most sectors.

A branch is an extension of its foreign parent and carries no independent legal personality, meaning the parent bears full liability for its obligations in Honduras. An S.A. is a locally incorporated entity with separate legal status, distinct tax registration, and the ability to retain earnings domestically. Compliance obligations for an S.A. are generally broader, but the entity operates with greater structural independence.

The S.A. permits the use of bearer-adjacent nominee arrangements at the shareholder level, though disclosure requirements have tightened under anti-money laundering regulations. Beneficial ownership information is maintained in the Registro Mercantil, but is not uniformly available for public inspection.

No. A Sociedad en Nombre Colectivo and a Sociedad en Comandita Simple each require a minimum of two partners by statute. An S.R.L. requires at least two quota-holders, and an S.A. requires a minimum of two shareholders to incorporate.

Foreign nationals may form an S.A., an S.R.L., or establish a branch or representative office. Certain regulated sectors impose additional licensing requirements regardless of structure. Full foreign ownership is permitted in most industries without a mandatory local partner.

The Código de Comercio permits structural transformation between entity types, though the process requires notarial deed, Registro Mercantil filing, and publication in the official gazette, La Gaceta. Conversion from an S.R.L. to an S.A. is the most common transformation. Not all conversions follow the same procedural path, and tax implications must be assessed separately.

No. A Sole Proprietorship (Empresa Individual) does not create a legal distinction between the owner and the business, leaving personal assets exposed to commercial liabilities. Partnerships under the Sociedad en Nombre Colectivo structure also impose unlimited personal liability on general partners, unlike the S.A. or S.R.L., which maintain full legal separateness.

A representative office carries the lightest compliance burden, as it cannot generate local revenue and is not subject to corporate income tax filing in the same manner as trading entities. However, its operational scope is strictly limited to promotional and liaison activities, making it unsuitable for entities intending to conduct direct commercial transactions.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.