Key Takeaways

- Guadeloupe operates under the French Code de commerce, with all business entities registered through the Greffe du Tribunal de Commerce via the Registre du Commerce et des Sociétés (RCS).

- The SAS is the most commonly incorporated structure in Guadeloupe due to its flexible governance rules and absence of minimum share capital requirements.

- Foreign companies can establish a presence in Guadeloupe through a branch or liaison office without incorporating a separate legal entity under French law.

- Tax obligations in Guadeloupe broadly mirror metropolitan France under the Code général des impôts, with certain regional adaptations that include specific overseas tax incentives.

Introduction to Entity Types in Guadeloupe

Guadeloupe is an archipelago in the Lesser Antilles, situated in the eastern Caribbean Sea between Antigua and Dominica. As an overseas department and region of France, it operates under French law — the Code de Commerce governs corporate formation, and businesses register through the Greffe du Tribunal de Commerce, which maintains the Registre du Commerce et des Sociétés (RCS).

Because Guadeloupe is an integral part of the French Republic, its tax regime broadly mirrors metropolitan France, subject to certain regional adaptations under the Code Général des Impôts, including specific overseas tax incentives.

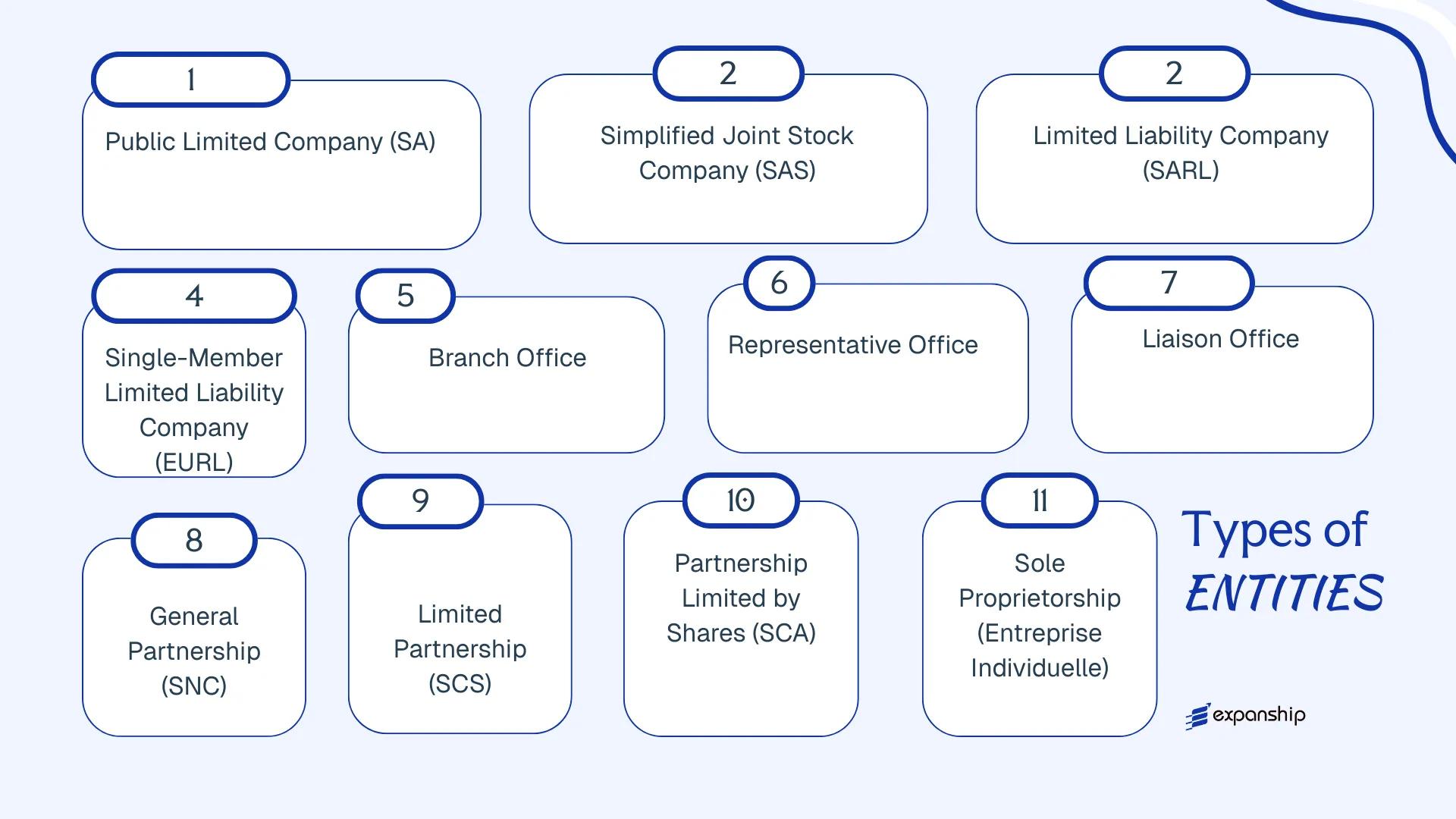

Understanding the available business entity types in Guadeloupe is essential before committing to any structure. The legal forms available include the Société Anonyme (SA), Société par Actions Simplifiée (SAS), Société à Responsabilité Limitée (SARL), Entreprise Unipersonnelle à Responsabilité Limitée (EURL), Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA), the Entreprise Individuelle, and foreign business structures such as branch offices and representative offices.

Each form carries distinct requirements around capital, governance, liability, and taxation — all of which this article examines in turn.

An Overview of Business Structures in Guadeloupe

As a French overseas department, Guadeloupe operates under the same company law framework as metropolitan France, governed primarily by the Code de commerce. Several distinct entity types are available to investors and entrepreneurs, each structured to serve different commercial, liability, and ownership requirements. The sections that follow examine each structure in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| SA | Corporate | Limited | Corporate tax | Permitted | 2 shareholders | Greffe du Tribunal de Commerce | Code de commerce |

| SAS | Corporate | Limited | Corporate tax | Permitted | 1 shareholder | Greffe du Tribunal de Commerce | Code de commerce |

| SARL | Corporate | Limited | Corporate tax | Permitted | 1–100 associates | Greffe du Tribunal de Commerce | Code de commerce |

| EURL | Corporate | Limited | Corporate or income tax | Permitted | 1 associate | Greffe du Tribunal de Commerce | Code de commerce |

| SNC | Partnership | Unlimited | Income tax | Permitted | 2 partners | Greffe du Tribunal de Commerce | Code de commerce |

| SCS | Partnership | Mixed | Income tax | Permitted | 2 partners | Greffe du Tribunal de Commerce | Code de commerce |

| SCA | Corporate/Partnership | Mixed | Corporate tax | Permitted | 4 members | Greffe du Tribunal de Commerce | Code de commerce |

| Branch Office | Non-incorporated | Parent liable | Corporate tax | Permitted | Parent company | Greffe du Tribunal de Commerce | Code de commerce |

| Representative Office | Non-incorporated | Parent liable | Generally exempt | Restricted | Parent company | Greffe du Tribunal de Commerce | Code de commerce |

| Entreprise Individuelle | Sole proprietorship | Personal | Income tax | Permitted | 1 individual | Greffe du Tribunal de Commerce | Code de commerce |

Each of these structures is examined in full in the sections below.

Société Anonyme (SA)

The Société Anonyme SA Guadeloupe operates under the same legal framework as metropolitan France, governed by the French Commercial Code (Code de commerce), consolidated under Law No. 66-537 of 24 July 1966 and its subsequent revisions. As an overseas department (département d'outre-mer), Guadeloupe applies French corporate law in full, with no separate territorial legislation.

The SA carries separate legal personality, meaning it exists as a distinct legal entity from its shareholders. Liability is limited to each shareholder's capital contribution, and the structure accommodates both private placement and public offerings of shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Governed by the French Code de commerce |

| Members | Shareholders (actionnaires); minimum 2, no maximum (unless listed) | Minimum 7 shareholders if shares are offered to the public |

| Governance | Board of Directors (Conseil d'administration, 3–18 members) or Supervisory Board + Management Board | Two governance structures available under the same legal form |

| Local Presence | Registered office (siège social) in Guadeloupe required | No mandatory local director, but registered address is compulsory |

| Share Capital | Minimum EUR 37,000 (private); EUR 225,000 if shares are publicly offered | Must be at least half paid up at incorporation |

| Privacy | Shareholder identities filed with the Registre du Commerce et des Sociétés (RCS) | Beneficial ownership declarations required under French anti-money laundering rules |

Focus Points

- Taxation: Subject to French corporate income tax (impôt sur les sociétés) at the standard 25% rate; VAT applies at standard French rates with certain local variations under the octroi de mer regime; withholding tax may apply on dividends distributed to non-resident shareholders under applicable tax treaties.

- Annual Compliance: Annual accounts must be approved by shareholders, audited by a statutory auditor (commissaire aux comptes) — mandatory for all SAs — and filed with the RCS.

- Audit Obligation: Unlike smaller entities, the SA has no threshold exemption; a commissaire aux comptes is required regardless of size.

- Treaty Access: As a French-domiciled entity, the SA benefits from France's extensive double tax treaty network and EU directives, including the Parent-Subsidiary Directive.

- Conversion: An SA may be converted into an SAS by unanimous shareholder vote without dissolution, under Article L. 227-3 of the Code de commerce.

Sub-Types

SA with Board of Directors (Conseil d'administration)

This is the classical governance model, where a single board handles both strategic oversight and executive management, with a Chairman (Président) who may also serve as CEO (Directeur Général). It suits larger organisations with consolidated decision-making structures.

SA with Supervisory Board (Conseil de surveillance) and Management Board (Directoire)

Here, executive management is separated from oversight — the directoire runs the company while the conseil de surveillance supervises it. This structure is typically adopted by entities with institutional investors or complex ownership arrangements requiring clear separation of powers.

When to Use an SA

The SA suits businesses seeking to raise capital from multiple investors, operate at scale, or prepare for a future public listing. The mandatory audit requirement adds credibility with institutional counterparties, though it also increases annual compliance costs considerably compared to simpler structures.

Best suited for large enterprises, joint ventures with institutional investors, or businesses with a realistic path toward public capital markets.

Company Incorporation in Guadeloupe

Incorporate your business in Guadeloupe with end-to-end support from entity selection through to RCS registration.

Société par Actions Simplifiée (SAS)

The Société par Actions Simplifiée SAS Guadeloupe operates under French corporate law, specifically the provisions of the Code de commerce governing simplified joint-stock companies, introduced through legislation effective since 1994 and significantly amended in 1999 to allow single-shareholder formation. As an overseas department of France, Guadeloupe applies metropolitan French law directly, meaning no separate territorial corporate statute governs this entity type.

A SAS carries full legal personality distinct from its shareholders, with liability limited to capital contributions. Its defining characteristic is contractual flexibility: the articles of association (statuts) govern most internal arrangements, including governance structures, share transfer conditions, and decision-making thresholds, within boundaries set by the Code de commerce.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société par Actions Simplifiée | Hybrid between corporate rigidity and contractual freedom |

| Members | Shareholders (associés) | Minimum 1, no maximum; can be natural or legal persons |

| Governance | President (Président) mandatory | Additional governance bodies defined freely in statuts |

| Registered Office | Required in Guadeloupe or French territory | Must be declared with the Greffe du Tribunal de Commerce |

| Share Capital | No statutory minimum | Must be specified in statuts; contributions in cash or kind permitted |

| Privacy | Shareholder identity filed with Registre du Commerce et des Sociétés (RCS) | Beneficial ownership reported to FIBEN/FICOBA frameworks where applicable |

Focus Points

- Taxation: Subject to standard French corporate income tax (impôt sur les sociétés) at 25%; VAT applies under French rules; withholding tax on dividends paid to non-residents depends on applicable tax treaties or EU directives.

- Annual Compliance: Annual accounts must be filed with the Greffe; statutory audit required once two of three thresholds (turnover, balance sheet, headcount) are exceeded.

- Treaty Access: Benefits from France's extensive double tax treaty network, covering over 120 jurisdictions.

- Conversion: Can be converted into an SA or SARL by shareholder decision, subject to Code de commerce procedural requirements.

- Restrictions: Cannot make public offerings of securities; capital-raising from the public requires conversion to an SA.

Sub-Types

Société par Actions Simplifiée Unipersonnelle (SASU)

A SASU is a single-shareholder variant of the SAS, governed by the same provisions but structured for sole ownership. It suits individual entrepreneurs or parent companies establishing a wholly owned subsidiary while retaining the SAS governance flexibility.

Recommendations

The SAS suits holding structures, joint ventures, and foreign-owned subsidiaries where bespoke governance arrangements are a priority. Its contractual flexibility is a genuine structural advantage, though the absence of a minimum capital requirement places greater responsibility on founders to ensure adequate capitalisation from the outset.

The SAS in Guadeloupe is best suited for foreign investors and multi-party ventures requiring tailored governance without the statutory rigidity of an SA.

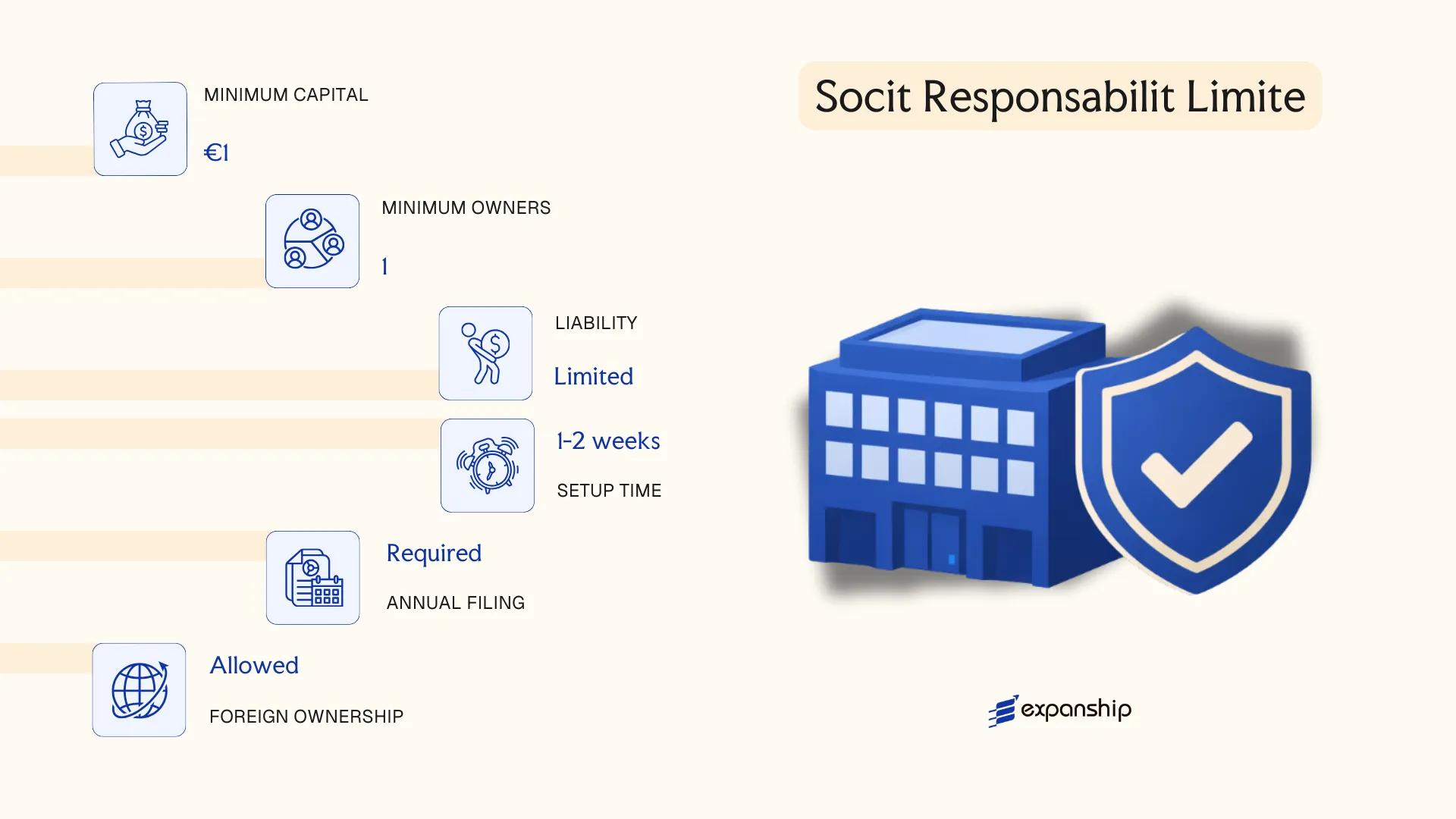

Société à Responsabilité Limitée (SARL)

The Société à Responsabilité Limitée SARL Guadeloupe operates under the same legislative framework as metropolitan France, governed by the French Commercial Code (Code de commerce), principally Articles L223-1 through L223-43. As an overseas department, Guadeloupe applies French law directly, with no separate territorial corporate statute.

The SARL is a separate legal entity, meaning the company holds rights and obligations in its own name. Shareholders' personal liability is capped at their capital contributions, making this a hybrid structure that combines corporate liability protection with the operational flexibility typically associated with smaller, closely held firms.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société à Responsabilité Limitée (Limited Liability Company) | Separate legal personality; governed by Code de commerce |

| Members | 1 to 100 shareholders (associés) | Single-member variant is the EURL; exceeding 100 requires conversion to SA |

| Management | One or more gérants (managers) | Gérant need not be a shareholder; can be a natural person only |

| Capital | No statutory minimum (€1 symbolic minimum in practice) | Must be defined in articles; cash contributions require deposit at a credit institution |

| Local Presence | Registered office (siège social) in Guadeloupe required | No mandatory local director requirement under French law |

| Privacy | Shareholder identity filed with the Registre du Commerce et des Sociétés (RCS) | Beneficial ownership disclosed to the Registre des bénéficiaires effectifs |

Focus Points

- Taxation: Subject to French corporate income tax (IS) at the standard 25% rate; VAT applies at standard French rates; profits distributed to non-resident shareholders attract withholding tax, potentially reduced under applicable French tax treaties; no separate local Guadeloupe corporate tax surcharge.

- Annual Compliance: Annual accounts must be filed with the Greffe du Tribunal de Commerce; approval by shareholders required within six months of the financial year-end.

- Economic Substance: No specific economic substance regime distinct from French mainland rules; genuine business activity and registered office must be maintained.

- Conversion: An SARL may be converted to an SAS or SA by shareholder resolution, subject to statutory conditions under the Code de commerce.

- Transfer Restrictions: Share transfers to third parties outside the shareholder group require prior approval (agrément) from existing shareholders.

Closing

The SARL suits small-to-medium trading operations, family-owned businesses, and local service firms where ownership control and liability protection are priorities; its primary limitation is the 100-shareholder cap, which restricts scalability for businesses anticipating broad investor participation.

The SARL is most appropriate for resident entrepreneurs and small joint ventures seeking a straightforward liability shield without the administrative burden of a public company structure.

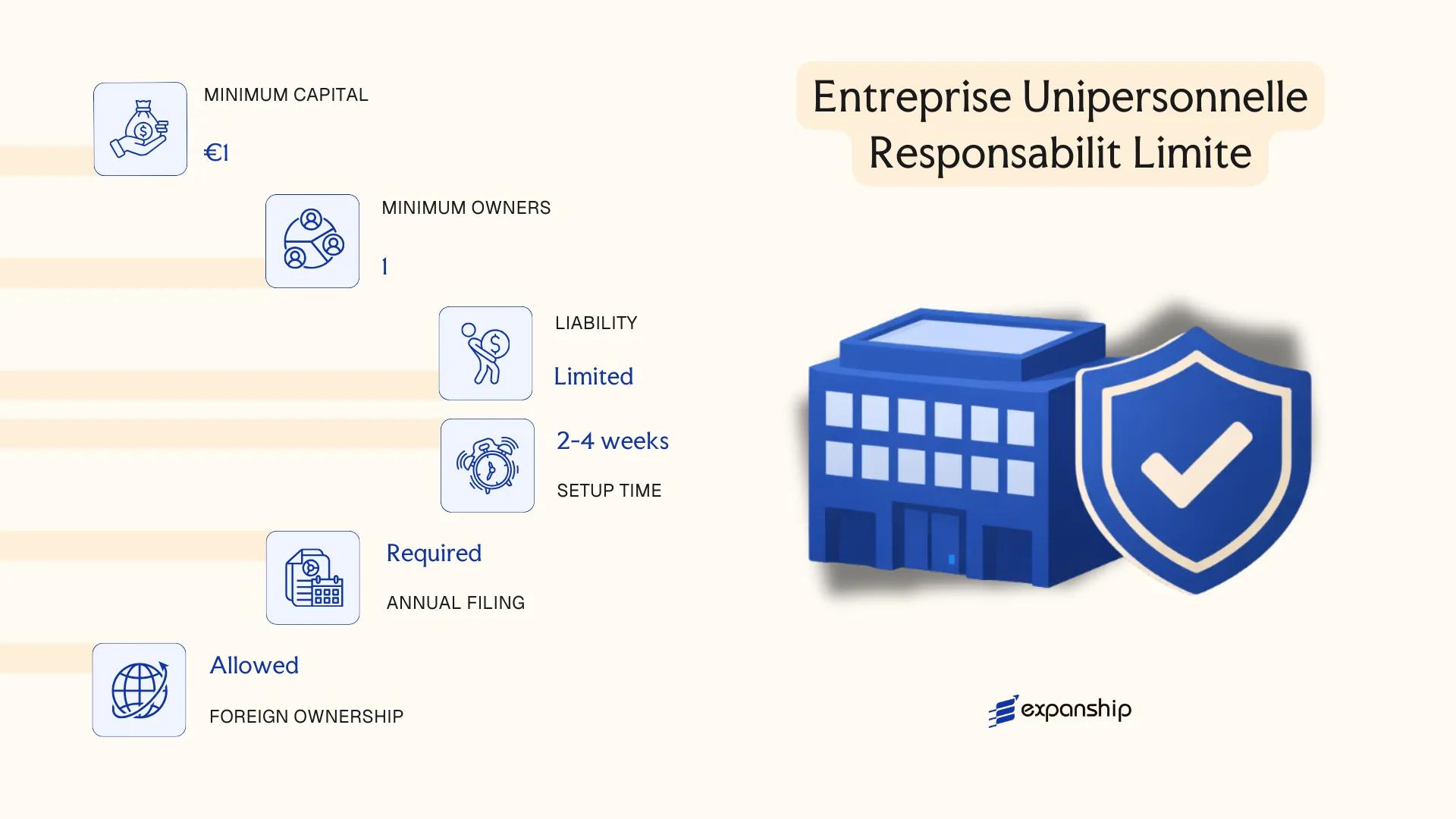

Entreprise Unipersonnelle à Responsabilité Limitée (EURL)

The EURL single member company Guadeloupe founders typically choose operates as a one-person variant of the SARL, governed by French commercial law as extended to Guadeloupe under the principle of legislative assimilation. Like its multi-member counterpart, it carries separate legal personality, meaning the entity's assets and liabilities are distinct from those of its sole shareholder.

Liability is capped at the amount contributed to share capital. This structure suits individuals who require the protections of a corporate form without involving additional shareholders, effectively creating a hybrid between a sole proprietorship and a limited liability company.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Single-member SARL variant | Governed by French commercial law as applied in Guadeloupe |

| Members | 1 sole shareholder (natural or legal person) | A legal entity acting as sole shareholder converts the EURL to a standard SARL if a second member joins |

| Management | Single gérant (manager); may be the shareholder | The gérant can be a non-shareholder third party |

| Capital | No statutory minimum; €1 minimum in practice | Capital divided into parts sociales; must be stated in the articles |

| Local Presence | Registered office address in Guadeloupe required | Registered with the Registre du Commerce et des Sociétés (RCS) via the guichet unique |

| Privacy | Shareholder identity disclosed in public registry | Financial statements filed with the greffe du tribunal de commerce |

Focus Points

- Taxation: Subject to French corporate income tax (IS) at standard rates; however, if the sole shareholder is an individual, the entity may opt for personal income tax (IR) treatment for up to five years. VAT rules, social contributions, and withholding tax obligations follow the standard French metropolitan framework applicable in Guadeloupe.

- Annual Compliance: Annual accounts must be approved and filed with the greffe; a statutory audit is not mandatory below certain thresholds.

- Conversion: Automatic conversion to a SARL occurs upon admission of a second shareholder; no separate dissolution is required.

- Treaty Access: As a French overseas department, Guadeloupe falls within France's tax treaty network, giving the EURL access to applicable double taxation agreements.

Closing

The EURL suits individual entrepreneurs and foreign investors seeking a single-person corporate vehicle for trading, consulting, or holding activities, with the primary limitation being that social charges on the gérant-shareholder can be substantial compared to a salaried employee arrangement.

The EURL is best suited for individual entrepreneurs or sole foreign investors who require limited liability and a recognised corporate structure without bringing in additional shareholders.

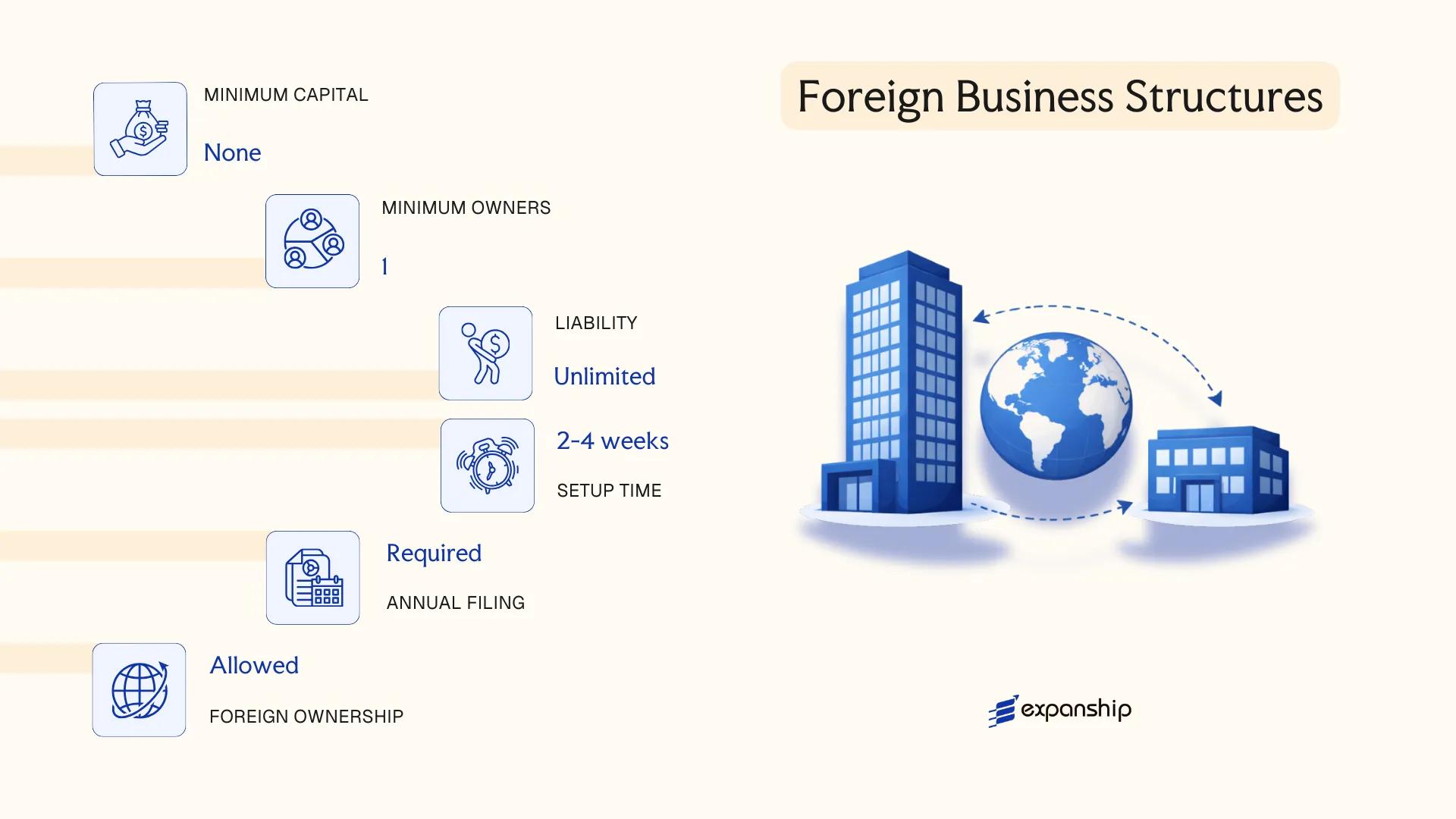

Foreign Business Structures in Guadeloupe [Branch Office, Representative Office, Liaison Office]

As an overseas region of France, Guadeloupe applies French commercial law in full, meaning a foreign company branch office Guadeloupe follows the same legal framework as mainland France under the Code de Commerce. Foreign entities operating here do not form a new legal person — the branch, representative office, or liaison office remains an extension of the parent company abroad.

Registration is handled through the Greffe du Tribunal de Commerce, which maintains the Registre du Commerce et des Sociétés (RCS). The parent company bears full legal and financial liability for the activities of its foreign presence here.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Parent entity remains fully liable |

| Representatives | Appointed representative (mandataire) resident in France | Must be formally designated at registration |

| Local Presence | Registered address in Guadeloupe; RCS filing mandatory for branches | Liaison offices have lighter registration obligations |

| Capital | No minimum capital requirement | Parent company's capital governs |

| Privacy | Parent company details disclosed in RCS filing | Public record |

Focus Points

- Taxation: Branches are subject to French corporate income tax (IS) at 25% on profits attributable to French territory; VAT applies at standard French rates; withholding tax may apply on profit remittances depending on the parent's home jurisdiction and applicable tax treaties.

- Treaty Access: France's tax treaty network covers the branch as French-sourced income is treated under French domestic rules; treaty benefits depend on the parent entity's residence.

- Economic Substance: No formal economic substance regime applies, but genuine commercial activity must be demonstrable to avoid recharacterisation by French tax authorities.

- Annual Compliance: Branches must file annual accounts with the Greffe and submit French tax returns; the parent's financial statements must also be deposited.

- Restrictions: Certain regulated sectors (finance, insurance, healthcare) require prior authorisation from sector-specific French regulatory bodies before commencing operations.

Sub-Types

Branch Office (Succursale)

A branch conducts full commercial activity in Guadeloupe and generates taxable income locally. It must register with the RCS and is subject to the complete French tax and accounting obligations.

Representative Office

A representative office is permitted to carry out market research, promotional activities, and liaison functions, but cannot conclude contracts or generate revenue directly. Lighter registration requirements apply.

Liaison Office (Bureau de Liaison)

Functionally similar to a representative office, a liaison office is restricted to non-commercial, preparatory, or auxiliary activities. It is not registered on the RCS as a commercial entity, though a local address and appointment of a representative remain necessary.

Closing

Foreign entities typically use a branch to test the French Caribbean market before committing to a locally incorporated subsidiary; the key advantage is operational simplicity, while the primary drawback is full parental liability exposure with no liability ring-fencing.

Foreign companies seeking a temporary or exploratory commercial presence without incorporating a separate entity are best suited to this structure.

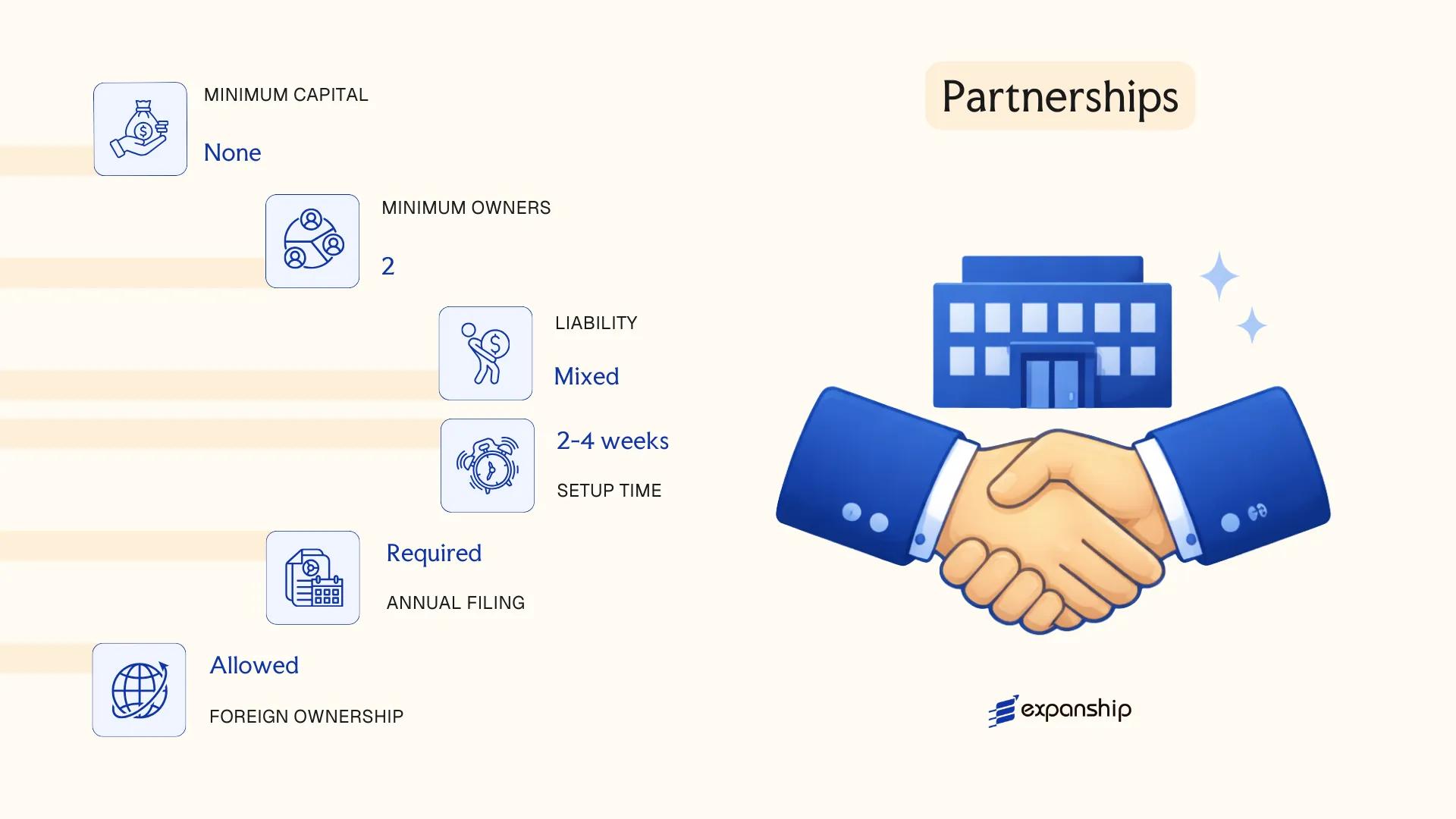

Partnerships in Guadeloupe [Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA)]

As an overseas department of France, Guadeloupe applies the French Commercial Code (Code de commerce) in full, which governs all three partnership structures available: the Société en Nom Collectif (SNC), the Société en Commandite Simple (SCS), and the Société en Commandite par Actions (SCA). These partnership structures in Guadeloupe SNC SCS SCA frameworks share one defining trait — at least one category of partner bears unlimited personal liability for the entity's debts.

Registration of all three forms is handled through the Centre de Formalités des Entreprises (CFE) and recorded in the Registre du Commerce et des Sociétés (RCS). Each structure holds separate legal personality upon registration, meaning the firm can contract, own assets, and litigate in its own name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (société de personnes or hybrid) | SNC = general; SCS = limited/general hybrid; SCA = hybrid with capital |

| Members | SNC: min. 2 general partners (associés); SCS: min. 1 general + 1 limited partner; SCA: min. 1 general partner + 3 shareholders | No statutory maximum for any form |

| Liability | SNC: unlimited for all; SCS: unlimited for general partners, limited for silent partners; SCA: unlimited for gérants, limited for shareholders | Unlimited partners are jointly liable for all debts |

| Local Presence | Registered office (siège social) in Guadeloupe required; no mandatory local director | Registered address must be maintained at all times |

| Share Capital | SNC/SCS: no minimum capital; SCA: minimum €37,000 | SCA capital divided into shares (actions) |

| Privacy | Partner identities disclosed in RCS filings; not publicly listed individually but accessible on request | Beneficial ownership reported to the Registre des bénéficiaires effectifs |

Focus Points

- Taxation: All three structures are generally transparent for tax purposes — profits are taxed at the partner level under personal income tax (impôt sur le revenu), though an election for corporate tax (impôt sur les sociétés) at 25% is available; VAT at 8.5% (reduced rate applicable in Guadeloupe under DOM rules) applies to taxable supplies; withholding taxes follow standard French rules on distributions to non-resident partners.

- Annual Compliance: Annual accounts must be filed with the RCS; the SCA is additionally subject to statutory audit requirements once certain thresholds are met.

- Transfer Restrictions: SNC partner shares (parts sociales) are not freely transferable without unanimous partner consent, making entry and exit structurally rigid.

- Treaty Access: As a French territory, entities may access France's extensive double tax treaty network, subject to the specific treaty's scope and residency provisions.

- Conversion: An SNC or SCS may be converted to a capital company (SARL, SAS) by unanimous partner vote and compliance with the applicable minimum capital rules.

Sub-Types

Société en Nom Collectif (SNC)

The SNC is the standard general partnership form in which all partners hold the status of commerçant (trader) and bear joint and several unlimited liability. It is typically used for family businesses or professional groupings where all participants wish to retain equal governance control.

Société en Commandite Simple (SCS)

The SCS introduces a two-tier membership structure: associés commandités (general partners) manage the business and carry unlimited liability, while associés commanditaires (silent partners) contribute capital and bear liability only to the extent of their contribution. This structure suits arrangements where passive investors fund an actively managed business.

Société en Commandite par Actions (SCA)

Distinct from the SCS, the SCA's passive investors hold transferable shares (actions) rather than non-transferable interests, and the entity is subject to rules closer to those governing capital companies, including potential audit obligations. The SCA is used in private equity structures and family holding arrangements requiring transferable investor interests alongside a stable management tier.

Closing

Partnership structures suit closely held businesses, family-controlled enterprises, and arrangements where tax transparency is a deliberate objective rather than a secondary concern. The principal limitation across all three forms is the unlimited personal exposure of at least one partner class, which raises the personal risk profile of active managers considerably.

These structures are best suited for professional groupings, family-controlled businesses, or investment arrangements where partners accept personal liability in exchange for operational control and pass-through taxation.

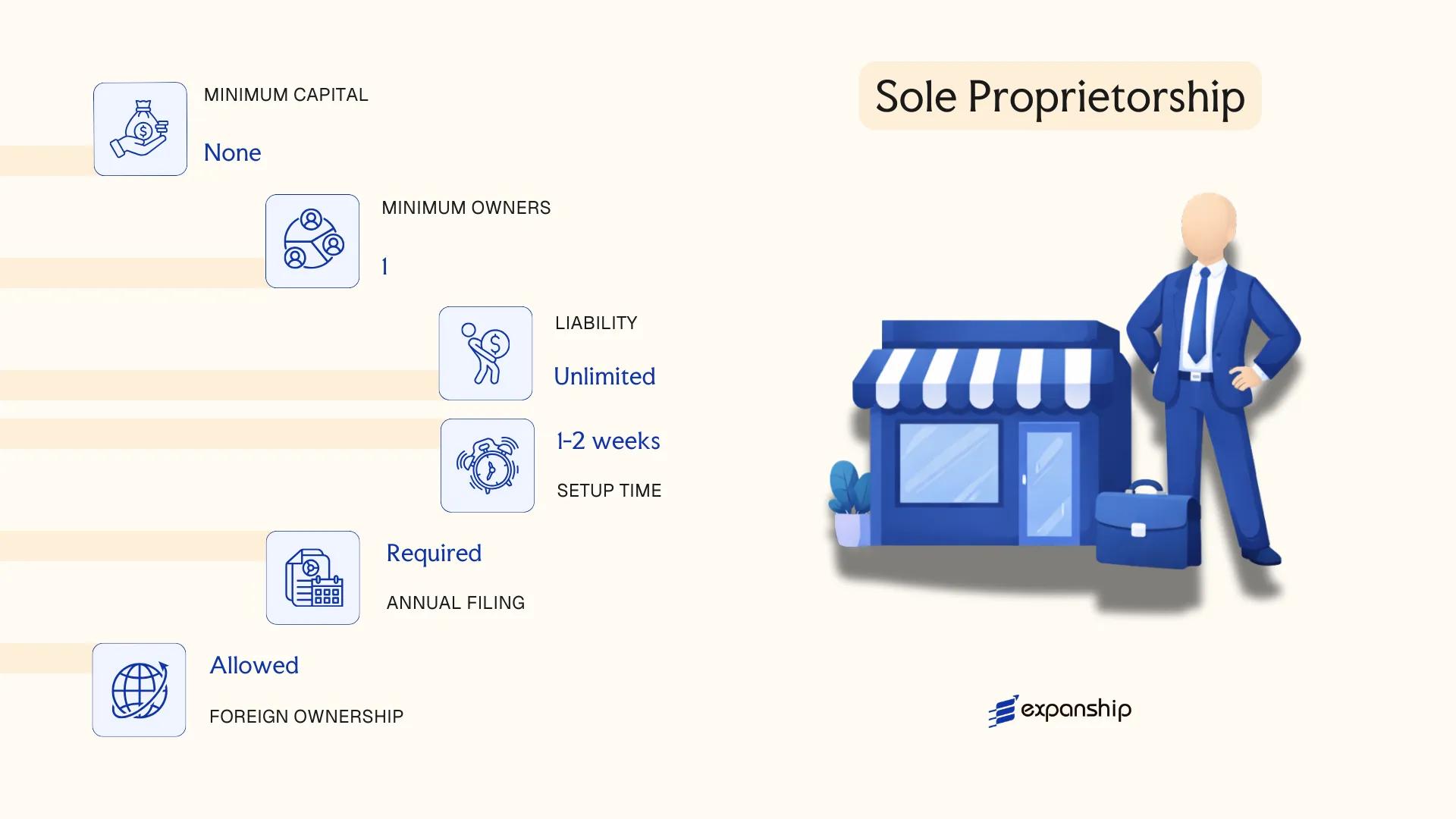

Sole Proprietorship (Entreprise Individuelle)

The sole proprietorship Entreprise Individuelle in Guadeloupe is governed by French law, specifically the reforms introduced under the Loi n° 2022-172 du 14 février 2022, which fundamentally altered the structure of individual enterprise in France and its overseas departments. Prior to this legislation, sole traders operated without any separation between personal and professional assets.

Under the 2022 reform, a statutory separation now exists between the professional patrimony and the personal patrimony of the sole trader by default, without requiring incorporation. This does not create a separate legal personality — the Entreprise Individuelle remains a non-corporate form — but it does provide a structural asset-protection mechanism that creditors must respect unless personal guarantees have been given.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality; single-patrimony rule replaced by dual-patrimony since 2022 |

| Members | One proprietor (exploitant individuel) | No minimum capital; no shareholders or directors |

| Local Presence | Registered business address in Guadeloupe required | Registration via the Guichet Unique (INPI platform) |

| Capital | None required | No minimum capital threshold |

| Liability | Limited to professional patrimony by default | Personal assets protected unless voluntary guarantee extended to creditors |

| Privacy | Proprietor's name forms part of the business identity | No shareholder register; minimal public disclosure |

Focus Points

- Taxation: Subject to income tax (impôt sur le revenu) under the BIC or BNC regime depending on activity; VAT applies above applicable turnover thresholds; option to elect corporate tax (IS) treatment available under the 2022 reform.

- Annual Compliance: Declaration of revenue through the annual income tax return; accounting obligations vary by turnover category (micro, réel simplifié, réel normal).

- Conversion: Can be converted into an EURL or other corporate form without triggering a full dissolution process under current French commercial law.

- Treaty Access: As a non-corporate entity, access to France's tax treaty network depends on individual residency status, not entity classification.

- Restrictions: Cannot issue shares or raise equity capital; unsuitable for multi-investor structures.

Closing

The Entreprise Individuelle suits freelancers, tradespeople, and consultants operating with low liability exposure and straightforward revenue structures. The dual-patrimony protection introduced in 2022 is a genuine structural benefit, though the absence of legal personality limits access to institutional financing and equity arrangements.

Best suited for resident self-employed individuals in Guadeloupe who operate solo, have no need for external investors, and want minimal administrative overhead with default asset separation.

How to Choose the Right Entity Type in Guadeloupe

Selecting the right business structure in Guadeloupe shapes your tax position, liability exposure, and administrative obligations from day one — getting this wrong carries concrete legal and financial consequences.

Why Your Entity Choice Matters

The French Commercial Code, as applied in Guadeloupe, governs entity formation and conduct. Choosing the wrong structure can result in:

- Selecting a structure without audited financial requirements when your firm scales beyond the SARL statutory thresholds forces a mandatory conversion, adding retroactive compliance costs.

- Choosing a tax-exempt regime when your business needs access to France's tax treaty network means you cannot claim withholding tax reductions in counterpart countries.

- Forming a multi-shareholder company when a sole-operator structure applies locks you into annual general meeting obligations, formal governance requirements, and shareholder documentation that a single-member EURL would not require.

- Selecting an entity without adequate substance capacity when economic substance expectations apply triggers reporting failures and potential regulatory penalties under French fiscal law.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each point toward structurally distinct entities under French commercial law.

- Ownership Structure: A single founder and a multi-investor operation have different governance demands that directly determine whether an EURL, SARL, SAS, or SA fits.

- Tax Objectives: Your need for IS (corporate tax) standard rates, specific territorial regimes, or treaty eligibility narrows the viable options considerably.

- Liability Exposure: The degree of personal liability you can accept determines whether a limited-liability structure or a partnership form is appropriate.

- Exit Strategy: Not all entity types permit straightforward redomiciliation or conversion; your anticipated exit method should factor into the formation decision.

The full text of the French Commercial Code is publicly accessible on Légifrance, the official French government legal database.

Compliance Services for Companies in Guadeloupe

Maintain your legal standing in Guadeloupe with ongoing compliance support, including annual filings, statutory maintenance, and regulatory reporting.

Conclusion

Setting up a company in Guadeloupe means operating within the French legal framework, where the Code de commerce and Code général des impôts govern every registered entity. The SAS is the most frequently incorporated structure, favoured for its flexible governance and minimal share capital requirements. The SA suits larger enterprises requiring formal board governance and public capital access. A SARL fits closely held businesses with a defined group of associates, while the EURL serves a single founder who wants limited liability without partners. Sole proprietorships carry unlimited personal liability, making them appropriate only for low-risk, small-scale activities. Branch and liaison offices allow foreign firms to establish a presence without creating a separate legal entity.

As an outermost region of the EU, the jurisdiction benefits from European single-market access, and ongoing alignment with French regulatory modernisation continues to shape its corporate governance standards. Professional guidance through the Centre de Formalités des Entreprises remains essential for accurate registration and ongoing compliance.

How Expanship Can Assist You

Expanship company formation services Guadeloupe cover the full process of registering your entity with the Greffe du Tribunal de Commerce, from selecting the right structure — an SA, SAS, SARL, or any other form discussed in this guide — to meeting the statutory obligations that apply once your business is active.

From initial documentation through to post-incorporation filings, our team manages each stage on your behalf:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Filing and liaison with the relevant commercial court registry

- Post-incorporation compliance management, including annual reporting

- Corporate secretarial support

- Banking introduction assistance

Every jurisdiction carries its own procedural specifics. Guadeloupe, operating under French law as an overseas region, follows metropolitan French commercial regulations — and our team works within that framework daily.

Reach out to [Expanship Guadeloupe](gp/contact-us) to discuss your incorporation requirements directly.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is the most frequently incorporated structure. Its combination of capped liability, a single-shareholder variant (EURL), and relatively straightforward administrative requirements makes it accessible for small and medium-sized businesses.

The SAS offers considerably more contractual freedom in its governance arrangements, whereas the SA imposes mandatory statutory requirements including a board of directors and minimum share capital of €37,000. For compliance burden, the SA carries heavier ongoing obligations, including statutory audit requirements at lower thresholds.

Among available structures, the SAS provides the most flexibility in keeping internal governance arrangements out of public view, since shareholder agreements are not filed in the Registre du Commerce et des Sociétés. Beneficial ownership disclosure requirements still apply under French anti-money laundering regulations.

Not all structures permit sole formation. The EURL and the SASU (the single-person SAS variant) are designed for sole founders, while the SNC requires at least two partners and the SA requires a minimum of two shareholders.

Foreign nationals may incorporate an SA, SAS, or SARL without restriction on nationality grounds, since Guadeloupe operates under French commercial law. Non-EU nationals may need to obtain a carte de commerçant étranger before conducting commercial activity.

French commercial law permits conversion between certain forms — most commonly from SARL to SAS — provided the conversion meets the conditions set out under the Code de commerce. Conversion requires shareholder approval and re-registration with the Greffe du Tribunal de Commerce.

The SA, SAS, SARL, EURL, SCA, and SCS all carry distinct legal personality separate from their members. The SNC also has legal personality, though its partners remain jointly and severally liable for the firm's debts.

The EURL imposes the lightest administrative requirements among multi-purpose structures, particularly when the sole associate is also the gérant. Statutory audit obligations only apply once the EURL exceeds the thresholds defined under French commercial regulations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.