Key Takeaways

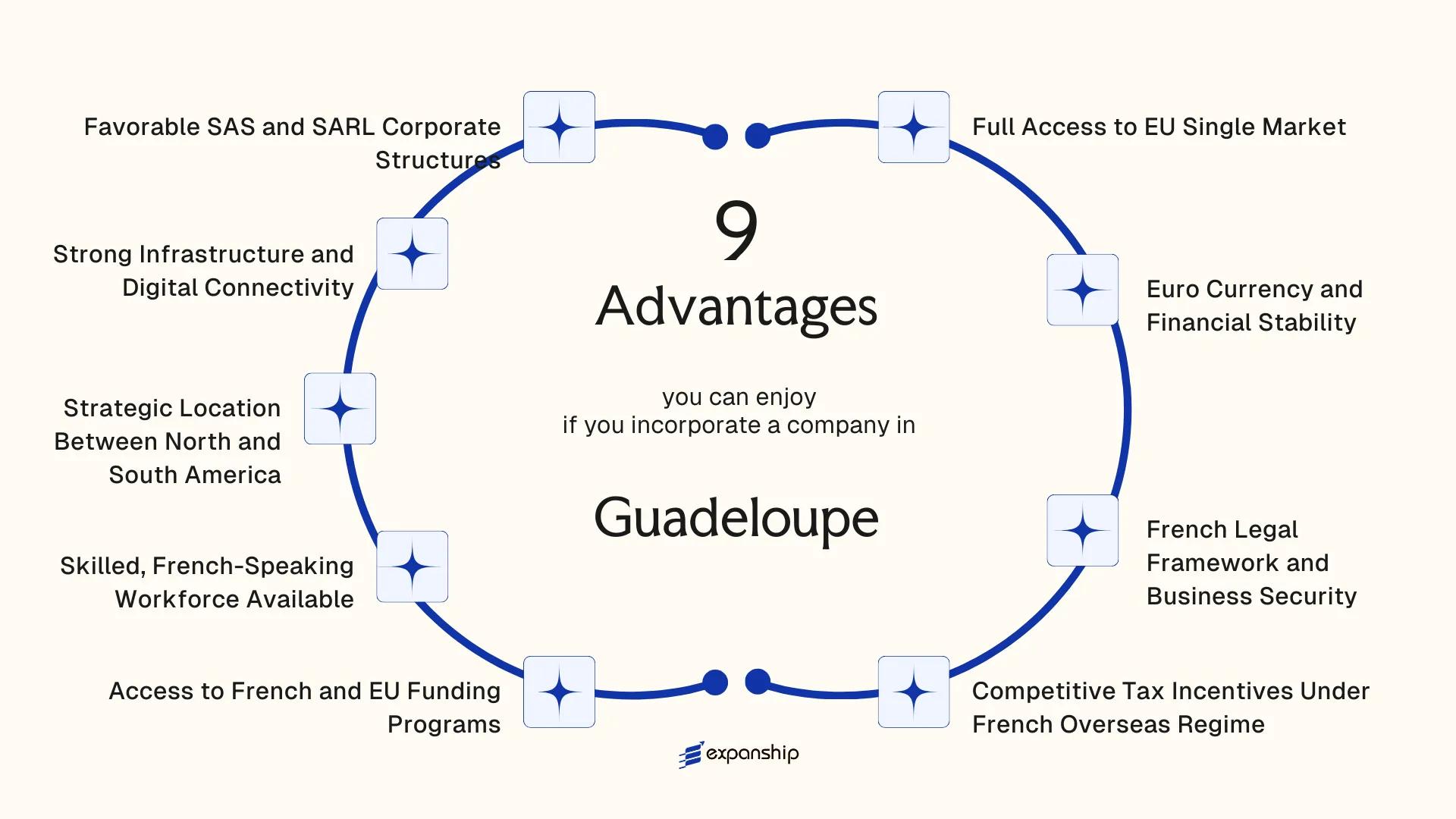

- As a French overseas department, Guadeloupe sits within the EU single market, giving registered businesses the unrestricted right to trade across all EU member states without the customs barriers or regulatory divergence that affect independent Caribbean jurisdictions.

- Companies operating in eligible sectors can access tax relief under the Girardin scheme, a French Overseas Law mechanism that reduces the fiscal burden below standard metropolitan France rates on a euro-denominated basis.

- Registration through the Greffe du Tribunal Mixte de Commerce de Pointe-à-Pitre follows established French commercial law, providing foreign investors with a legal framework backed by EU regulatory standards rather than the less predictable systems common to many offshore Caribbean territories.

- Businesses incorporated in Guadeloupe may qualify for EU structural funds and French overseas development programs, funding channels that are categorically unavailable to companies formed in non-EU Caribbean jurisdictions.

Guadeloupe is an overseas region and department of France, situated in the Lesser Antilles between the Atlantic Ocean and the Caribbean Sea. That political status places it within the European Union, meaning businesses registered here operate under French law and EU regulatory frameworks rather than the independent legal systems typical of many Caribbean jurisdictions. Company registration falls under the authority of the Greffe du Tribunal Mixte de Commerce de Pointe-à-Pitre, which handles commercial filings for the territory. Foreign investors most commonly establish a Société par Actions Simplifiée when entering this market.

On taxation, the territory follows the French fiscal system while benefiting from specific overseas department allowances that reduce the standard rates applicable in metropolitan France. Foreign ownership faces no categorical restrictions, and the jurisdiction maintains a generally open posture toward foreign direct investment across most sectors.

This article examines the concrete advantages that incorporating a company in Guadeloupe offers to international businesses and entrepreneurs evaluating the territory as a base of operations.

Full Access to EU Single Market

As an outermost region (OMR) of the European Union under Article 349 of the Treaty on the Functioning of the European Union, Guadeloupe sits fully within the EU's internal market. A company registered here holds the same right to trade goods and services across all 27 member states as a firm incorporated in France, Germany, or the Netherlands.

What Single Market Membership Actually Confers

Guadeloupe EU single market access benefits extend beyond tariff-free movement of goods. A business established here can invoice clients in Berlin or Barcelona without customs declarations, VAT complications at borders, or import duties that would apply to a company operating from outside the EU.

Regulatory Standing Within the EU Framework

Your entity is subject to EU regulations directly, meaning contracts, intellectual property protections, and financial instruments are governed under the same legal architecture that covers Paris or Amsterdam. EU market access through a Guadeloupe company also means your firm can participate in EU public procurement procedures, which are unavailable to third-country businesses.

Your Guadeloupe-registered entity holds full EU operational standing, giving you direct access to a market of over 440 million consumers without third-country trade barriers.

Euro Currency and Financial Stability

Guadeloupe euro currency stability for businesses is not incidental — it is structural. As an overseas region of France under Article 349 of the Treaty on the Functioning of the European Union, the territory uses the euro as its official currency, placing your company within the European Central Bank's monetary framework from day one.

For a foreign business owner, this removes a category of risk entirely. Currency conversion costs, exchange rate exposure, and the volatility common across other Caribbean jurisdictions simply do not apply when transacting with European clients, suppliers, or investors.

Pricing contracts in euros, holding euro-denominated accounts, and repatriating profits without currency conversion friction are practical outcomes of this arrangement — not theoretical ones.

The eurozone advantages for incorporation here are particularly relevant for firms with European parent companies or clients, since intercompany transfers, invoicing, and financial reporting all operate within a single currency environment.

Conditions that reinforce this stability include:

- ECB monetary policy applies directly, shielding the entity from local central bank decisions that could devalue a domestic currency

- No bilateral currency agreements are needed to move funds between the territory and continental France

- Banking institutions operating locally fall under French prudential supervision via the Autorité de Contrôle Prudentiel et de Résolution (ACPR)

- Euro-denominated financing from French or EU lenders is accessible without cross-currency structuring

Company Incorporation in Guadeloupe

Set up a legally compliant business entity in Guadeloupe under the French regulatory framework, with full euro currency access and EU market connectivity.

French Legal Framework and Business Security

French legal framework advantages in Guadeloupe derive directly from the territory's status as a French overseas department. As a full department of France under Article 73 of the French Constitution, the entire body of French law applies without modification. The Code de Commerce, which governs commercial activity across metropolitan France, applies in full to entities registered here. For foreign investors, this removes the uncertainty that typically accompanies incorporation in jurisdictions with untested or evolving legal systems.

| Legal Instrument | Governing Body | Relevance to Incorporated Entities |

|---|---|---|

| Code de Commerce | French Parliament | Commercial contracts, company formation, insolvency |

| Code Civil | French Parliament | Property rights, contractual obligations |

| Tribunal de Commerce | French judiciary | Commercial dispute resolution |

| BODACC | Direction de l'information légale et administrative | Official publication of corporate acts |

Contract enforcement follows French civil procedure, and commercial disputes are adjudicated by the Tribunal de Commerce under the same rules applied throughout France. Judgments carry the same legal weight as any French court ruling, which is directly enforceable across EU member states under EU Regulation No. 1215/2012 on jurisdiction and the recognition of judgments. Your contracts, shareholder agreements, and corporate documents operate within a codified, predictable framework that courts in Europe and beyond recognize without requiring additional authentication.

Regulatory oversight is provided by established French institutions, including the Greffe du Tribunal de Commerce, which handles corporate registration and maintains public records. This institutional continuity means your entity's legal standing is not subject to local political variability.

Competitive Tax Incentives Under French Overseas Regime

Guadeloupe overseas tax incentives for businesses are grounded in a statutory framework, not discretionary policy. As a French overseas region classified under Article 349 of the Treaty on the Functioning of the European Union, the territory benefits from specific fiscal derogations that mainland France does not offer.

The corporate income tax rate can be reduced significantly through investment-linked mechanisms under the Girardin law, formally Loi n° 2003-660, which allows qualifying capital investments in productive assets to generate substantial tax reductions. For investors structuring operations through a French entity, this creates a direct cost advantage that standard metropolitan French tax treatment does not replicate.

Reduced VAT rates also apply in Guadeloupe. The standard rate is capped at 8.5%, compared to the 20% rate applicable in mainland France. For businesses with high transactional volume, this differential has meaningful impact on cash flow and pricing structures.

Keep these points in mind:

- Girardin tax reductions apply to new productive investments, not all asset classes

- Benefits are subject to a minimum holding period for qualifying assets

- Tax filings remain subject to French Direction Générale des Finances Publiques oversight

- Some incentives require advance approval or structured compliance through a certified intermediary

The reduced VAT rate in Guadeloupe is a permanent structural feature of French outremer fiscal law, not a temporary relief measure, meaning your firm can plan around it with long-term certainty.

Access to French and EU Funding Programs

Guadeloupe's status as a French Overseas Region and an EU Outermost Region (ORs) creates direct access to EU and French funding programs that are simply not available to businesses incorporated elsewhere in the Caribbean. Companies registered here qualify under the same structural fund frameworks as those in metropolitan France, with additional provisions specifically calibrated for outermost regions.

EU Structural and Investment Funds

Under the European Regional Development Fund (ERDF, known in French as FEDER), businesses operating in the territory can access co-financing for investment in innovation, digital infrastructure, and economic development. The 2021-2027 programming period allocated significant FEDER resources to French Overseas Regions under the cohesion policy framework, with higher co-financing rates applying to outermost regions than to standard EU regions. For your business, this means capital expenditure and R&D projects may attract partial EU grant funding that reduces upfront investment requirements in ways that mainland European jurisdictions at standard development status do not offer.

Beyond ERDF, the European Social Fund Plus (ESF+) covers workforce development and training costs. French state aid schemes administered through BPI France, the public investment bank, also extend to firms established in Guadeloupe, covering innovation grants and export financing.

French National Programs

The French government supplements EU instruments with national schemes under the Plan de Relance and sector-specific programs managed by the DREETS (Direction régionale de l'économie, de l'emploi, du travail et des solidarités). Eligibility generally requires a registered legal entity in France, which an incorporated firm in the territory satisfies automatically.

Access Every Funding Advantage Available to Your Guadeloupe Entity

Our team can guide you through EU and French funding programs applicable to your business structure and sector, from FEDER grants to BPI France instruments.

Skilled, French-Speaking Workforce Available

Guadeloupe's labor pool carries a distinct advantage rooted in the French national education system. As a French overseas region under Article 73 of the French Constitution, the territory applies the same educational standards as metropolitan France, producing graduates trained under the same curricula and professional certification frameworks used in Paris or Lyon.

- French as the primary business language eliminates translation friction for firms operating across francophone markets in Africa, Canada, or Europe, reducing operational overhead from the start.

- Vocational and higher education institutions on the island are governed by French national standards, meaning professional qualifications hold the same legal recognition as those issued in mainland France.

- Workers employed through a local entity are subject to the French Labour Code (Code du travail), which your business applies in a familiar, codified form rather than navigating an unfamiliar national system.

- For foreign investors targeting Latin American and Caribbean markets, a workforce fluent in French and often in Caribbean Spanish or English provides a practical communication asset at no additional recruitment cost.

- Social contributions and employment contracts follow French metropolitan rules, so HR processes mirror what multinational firms already manage across their European operations.

Strategic Location Between North and South America

Guadeloupe sits at the northeastern edge of the Caribbean Sea, roughly equidistant between Florida and the northern coast of South America. This geographic position gives companies registered there a physical anchor in a region that connects two of the world's largest consumer markets.

As a French overseas region, the territory operates under EU customs rules, which means goods processed or shipped through a firm here can move within the EU single market without additional customs procedures. For businesses trading with both North American and Latin American partners, this dual access is not easily replicated from a purely domestic US, Brazilian, or Colombian entity.

The time zone (UTC-4, with no daylight saving shifts) aligns working hours with both the US East Coast and much of South America simultaneously, reducing scheduling friction for firms managing cross-regional operations.

A distribution company registered in Guadeloupe can ship to Martinique, mainland France, and other EU member states under intra-EU rules, while maintaining commercial relationships with Caribbean neighbors and Latin American markets outside the EU customs union, all from a single legal entity operating under French commercial law.

Strong Infrastructure and Digital Connectivity

Guadeloupe's infrastructure operates under French national standards, which means road networks, port facilities, and air connections are maintained to the same technical and regulatory benchmarks applied across metropolitan France. For a foreign business owner, this removes uncertainty about basic operational conditions that might otherwise require due diligence in other Caribbean markets.

The archipelago is served by Pointe-à-Pitre International Airport (Pôle Caraïbes), a fully equipped international hub, and by the Port of Pointe-à-Pitre, which handles both container cargo and passenger traffic. These two facilities position your business to move goods and personnel efficiently across the Caribbean basin and toward North and South American ports.

On the digital side, fiber-optic submarine cable systems connect the territory to mainland France and onward to international networks. Broadband connectivity meets EU technical benchmarks, which matters practically because your company can operate cloud-based systems, conduct cross-border transactions, and maintain compliant digital recordkeeping without investing in alternative infrastructure.

- Fixed and mobile telecommunications fall under French regulatory authority, specifically ARCEP (Autorité de Régulation des Communications Électroniques et des Postes), ensuring the same consumer and operator standards as in mainland France.

- Public digital infrastructure investments are eligible under EU cohesion funding frameworks, supporting continued network expansion.

Connectivity quality can vary between the main island and the outer islands of the archipelago, so confirm available infrastructure at your specific intended operating location before finalizing any site-related business decisions.

Favorable SAS and SARL Corporate Structures

As a French overseas territory, Guadeloupe offers access to two well-established legal entities under French commercial law: the Société par Actions Simplifiée (SAS) and the Société à Responsabilité Limitée (SARL). Both are governed by the French Code de Commerce, giving foreign investors a predictable, codified legal foundation rather than a newly developed or untested framework.

SAS: Flexible Governance for Foreign-Owned Entities

The SAS structure imposes no minimum share capital requirement and allows a single shareholder, making it accessible for solo founders or holding structures. Its articles of association can define governance rules with considerable freedom, which means you can structure management, voting rights, and profit distribution in ways that reflect your specific operational needs. This flexibility is particularly relevant for foreign investors who need to align a French-law entity with a parent company abroad.

SARL: Defined Structure With Capped Liability

The SARL suits smaller enterprises and joint ventures where defined shareholder roles matter. Liability is limited to each associate's capital contribution, and the entity can operate with as few as one associate (in which case it becomes an EURL). Profit extraction follows fixed rules under French tax law, which creates consistency for cross-border tax planning.

Key structural features shared by both entities include:

- Separate legal personality from the moment of registration at the Registre du Commerce et des Sociétés (RCS)

- No requirement for a local resident director

- Accounts filed under French GAAP, compatible with EU reporting standards

Why Guadeloupe Stands Out Among Caribbean Business Destinations

Most Caribbean jurisdictions that attract foreign incorporation, such as the British Virgin Islands, the Cayman Islands, and Barbados, operate as independent states with their own currencies, legal systems, and trade arrangements. Guadeloupe occupies a structurally different position: as a French overseas region and an outermost region of the European Union under Article 349 of the Treaty on the Functioning of the European Union, your business operates under French commercial law and within the EU regulatory framework, while remaining geographically in the Caribbean. That combination is uncommon at this latitude.

The comparison below focuses on jurisdictions a foreign investor would realistically evaluate alongside Guadeloupe, chosen for their Caribbean location, their relevance to holding and operational structures, and their standing as incorporation destinations. What the table reveals is that Guadeloupe's EU membership is not simply a symbolic designation, it carries direct legal and commercial consequences, including euro-denominated accounts, access to EU funding mechanisms, and enforceable EU contract standards, that independent Caribbean jurisdictions cannot replicate.

| Parameter | Guadeloupe | British Virgin Islands | Barbados | Cayman Islands |

|---|---|---|---|---|

| EU Membership | Yes, outermost region | No | No | No |

| Currency | Euro (EUR) | US Dollar (USD) | Barbadian Dollar (BBD) | Cayman Islands Dollar (KYD) |

| Legal System | French civil law (Code de commerce) | English common law | English common law | English common law |

| EU Single Market Access | Full | None | None | None |

| Corporate Tax Framework | French overseas tax regime with LODEOM incentives | 0% on offshore profits | 5.5% on international business companies | 0% corporate tax |

| Workforce Regulation | French Labour Code | Independent legislation | Independent legislation | Independent legislation |

| VAT System | Specific local rate (Taxe sur la valeur ajoutée, adapted) | None | 17.5% VAT | None |

Compliance Services for Companies in Guadeloupe

Maintain good standing under French commercial law and French overseas regulatory requirements with structured compliance support tailored to Guadeloupe-registered entities.

Conclusion

Guadeloupe presents a specific and coherent case for foreign business incorporation: a French-law jurisdiction within the EU that offers access to VAT-exempt incentive regimes, EU structural funds, and a euro-denominated financial system, without requiring physical relocation to continental Europe.

The most structurally significant advantages remain the tax relief available under French Overseas Law mechanisms and the unrestricted right to trade across EU member states. For capital-intensive operations or businesses planning to scale across markets, these two factors carry more practical weight than many comparable Caribbean jurisdictions can offer.

That said, the benefits of incorporating in Guadeloupe align most closely with businesses in specific sectors, including export-oriented services, regional distribution, and industries eligible for the Girardin scheme. Your structure, revenue profile, and operational base will determine whether these advantages materialise in practice.

For those whose business model fits the framework, the next step is ensuring that the company formation process, from selecting the correct legal entity to fulfilling URSSAF and SIRET registration requirements, is handled with precise attention to French regulatory procedure.

Start Your Guadeloupe Company Formation With Expanship

Expanship Guadeloupe company formation services cover the full incorporation lifecycle for foreign entrepreneurs setting up a Société par Actions Simplifiée or a Société à Responsabilité Limitée under French commercial law. From initial registration with the Greffe du Tribunal de Commerce to post-incorporation compliance under the Code de Commerce, each stage involves procedural requirements that vary depending on your entity type, capital structure, and intended activity. Coordinating those requirements across French overseas administrative channels is where structured support has practical value.

Expanship's service scope for your Guadeloupe entity includes:

- Preparation and legalization of incorporation documents, including statutes and identity verification files

- Registered agent and registered office provision to satisfy the domiciliation requirement

- Government filing and liaison with the Greffe du Tribunal de Commerce de Pointe-à-Pitre

- Post-incorporation compliance management, including annual obligations under French corporate law

- Banking introduction assistance to support your entity's operational setup

Incorporate in Guadeloupe with Expanship to keep your formation process organized and your compliance obligations on track from day one.

Reach out to Expanship Guadeloupe to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

Companies operating in Guadeloupe may qualify for tax reductions under the LODEOM framework (Loi pour le Développement Économique des Outre-Mer), which provides reduced employer social contribution rates and investment tax credits in qualifying sectors. Corporate tax obligations otherwise follow the French Code Général des Impôts, with the standard French corporate tax rate applying unless a specific exemption or reduction applies. Eligibility conditions vary by sector, company size, and the nature of the investment.

Yes. As a French overseas region and a full member of the European Union, a company registered in Guadeloupe holds EU legal status and can trade across EU member states under single market rules. This includes the free movement of goods, services, and capital. The same CE marking requirements and EU regulatory standards apply to products and services offered within the single market.

Registration with the Registre du Commerce et des Sociétés in Guadeloupe generally follows the same procedural timeline as metropolitan France. A straightforward SAS or SARL formation can typically be completed within one to two weeks, assuming all required documents are in order. Delays can occur if foreign-issued documents require apostille certification or certified translation into French.

The choice depends on the intended governance structure and shareholder profile. The SAS (Société par Actions Simplifiée) offers more flexibility in drafting shareholder agreements and imposes fewer statutory constraints on internal governance, making it a common choice for multi-investor or holding structures. The SARL (Société à Responsabilité Limitée) has a more prescriptive legal framework under the French Code de Commerce but is often preferred for smaller, closely held businesses due to its lower administrative complexity.

Failure to file annual accounts with the Greffe du Tribunal de Commerce or meet statutory obligations under the French Code de Commerce can result in administrative penalties, striking off from the RCS, or, in serious cases, personal liability for directors. French commercial courts have jurisdiction over compliance enforcement, and the same sanctions applicable in metropolitan France apply. Maintaining a registered office and a compliant local representative helps ensure ongoing obligations are met on time.

Yes. Guadeloupe is designated as an outermost region under Article 349 of the Treaty on the Functioning of the European Union, which makes businesses operating there eligible for European Structural and Investment Funds, including the ERDF (European Regional Development Fund). Applications are typically managed through the Région Guadeloupe in coordination with national and European administrations. Eligibility criteria are project-specific and generally require the company to demonstrate economic activity and job creation within the territory.

The LODEOM regime applies across several French overseas territories, including Martinique and French Guiana, so the tax incentive framework is not unique to Guadeloupe alone. The practical differentiation lies in sector-specific opportunities, infrastructure, and geographic positioning rather than exclusive tax advantages. Comparing jurisdictions requires assessing the specific investment type, applicable sectoral incentives, and operational costs in each territory.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.