Key Takeaways

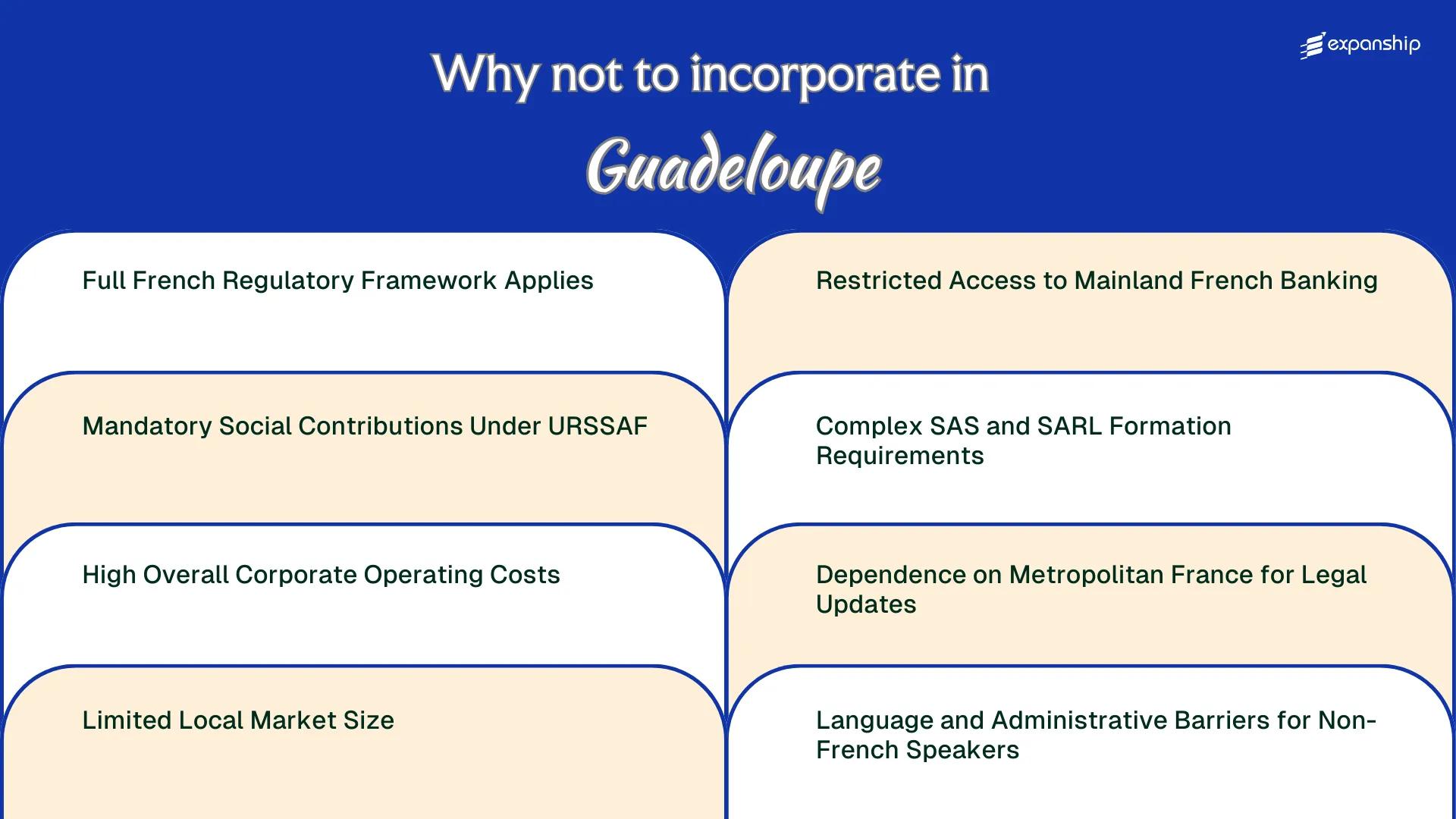

- Businesses incorporated in Guadeloupe are bound by the full provisions of the Code de commerce and French tax legislation, leaving no scope for the lighter regulatory frameworks common to other Caribbean jurisdictions.

- Mandatory social contribution obligations administered through URSSAF apply at the same rates as mainland France, creating a payroll cost burden that can be disproportionate relative to the size of the local market.

- Foreign entrepreneurs without prior exposure to French civil law face compounding administrative complexity when navigating SAS or SARL formation requirements, including documentation standards and registration procedures conducted entirely in French.

- Guadeloupe's limited domestic consumer base constrains the revenue potential available to locally incorporated entities, making the fixed costs of French regulatory compliance harder to absorb than in larger markets.

Guadeloupe operates under the full weight of French metropolitan law, making it one of the more heavily regulated environments for business formation among Caribbean jurisdictions. As an overseas region of France, the entity is subject to the same commercial code, tax legislation, and administrative procedures that govern firms on the French mainland.

The disadvantages of incorporating in Guadeloupe span regulatory, financial, operational, and administrative categories, each examined separately across this article. Not all drawbacks will apply equally — the burden shifts considerably depending on whether you are forming a SAS, a SARL, or another recognized structure, and on the sector your business operates in.

This article is most relevant to foreign investors and non-EU entrepreneurs who have no prior exposure to French civil law or the French administrative system. The governing legal framework, including business entity rules, is codified under the Code de commerce.

Full French Regulatory Framework Applies

Incorporating in Guadeloupe means operating under the full French regulatory framework, with no special dispensations for foreign investors seeking a lighter compliance structure.

No Separate Regulatory Tier for Overseas Businesses

As a French overseas department, Guadeloupe falls under the jurisdiction of French national law, including the Code de commerce and Code du travail, administered through local extensions of mainland institutions. Your firm must meet the same regulatory standards imposed on businesses in Paris or Lyon, regardless of the smaller operating environment.

French law compliance burdens apply in full, from mandatory company registration with the Registre du Commerce et des Sociétés to ongoing obligations under the Autorité des marchés financiers for regulated activities. A foreign business owner cannot opt into a simplified or offshore equivalent.

Regulatory Density Creates Structural Cost

Overseas department French regulations carry no reduced filing thresholds or foreign investor carve-outs. Every substantive legal change enacted at the national level applies automatically, requiring your entity to monitor and adapt without a local buffer.

Any regulatory update passed by the French legislature applies to your Guadeloupe entity with immediate effect, meaning legal compliance costs are tied directly to metropolitan France's legislative pace, not local business conditions.

Mandatory Social Contributions Under URSSAF

URSSAF contributions in Guadeloupe follow the same rate structure applied across metropolitan France, meaning your payroll costs carry some of the heaviest employer burdens in the world. Total employer social charges can reach approximately 40 to 45 percent on top of gross salary, administered through URSSAF (Union de Recouvrement des cotisations de Sécurité Sociale et d'Allocations Familiales).

For a foreign business owner unfamiliar with French payroll mechanics, this structure creates immediate friction across several dimensions:

- Each new hire triggers mandatory registration with URSSAF, requiring declarations through the DSN (Déclaration Sociale Nominative) system, which demands French-language payroll software and compliance knowledge that most non-French firms lack from day one.

- Contribution rates are recalculated periodically, meaning your cost projections can shift without any change in local conditions.

- Late or incorrect DSN filings generate automatic penalties, which disproportionately affect foreign firms still building administrative capacity.

Certain exemptions under the LODEOM law (Loi pour le Développement Économique des Outre-Mer) reduce employer charges in specific sectors and wage bands. However, qualifying for these exemptions requires meeting defined conditions, and misclassifying your eligibility exposes your firm to back payments with interest.

Company Incorporation in Guadeloupe

Set up your business entity in Guadeloupe with full compliance across French overseas territory requirements, including URSSAF registration and DSN obligations.

High Overall Corporate Operating Costs

High overall corporate operating costs in Guadeloupe business stem from the territory's status as a French overseas region, which ties it to one of the costlier regulatory environments in the EU. As a département and région d'outre-mer (DROM), the firm you register there operates under the full French Commercial Code, meaning cost structures mirror those of metropolitan France rather than competing Caribbean jurisdictions.

Imported goods, equipment, and materials carry freight premiums that mainland-based competitors simply do not face. Your entity absorbs these logistics costs as baseline overhead, not as exceptional expenses.

| Cost Category | Approximate Burden | Why It Compounds the Disadvantage |

|---|---|---|

| Corporate income tax (IS) rate | 25% standard rate | Aligns with French mainland rate, above many Caribbean alternatives |

| Minimum share capital (SARL) | €1 (statutory), but notarial and registration fees apply | Low entry threshold masks significant setup and compliance costs |

| Employer social contribution rate | ~40–45% on top of gross salary | Applies fully under URSSAF Guadeloupe, compressing hiring capacity |

| Freight and logistics surcharge | Typically 15–30% above metropolitan costs | Structural island premium with no statutory relief mechanism |

Accounting, legal, and payroll services priced at metropolitan French rates apply to a market that generates far lower revenue density than Paris or Lyon. That mismatch squeezes operating margins for foreign-owned businesses that cannot spread fixed professional fees across a large client base.

Certain tax credits under the LODEOM framework (Loi pour le Développement Économique des Outre-Mer) offer partial relief in qualifying sectors, but eligibility is sector-specific and administratively demanding to substantiate.

Limited Local Market Size

Guadeloupe's population sits at approximately 400,000 residents, and that ceiling creates real Guadeloupe limited market size risks for any foreign business projecting meaningful revenue from domestic sales alone. A firm that depends on local consumer demand will find the addressable base structurally insufficient to justify the operational costs that incorporation there imposes.

Purchasing power is further constrained by above-average unemployment rates relative to mainland France, which compounds the restricted consumer base beyond what raw population figures suggest. Your unit economics must account for a market where volume-driven growth is not a realistic path.

Most goods consumed locally are imported, meaning domestic production competes against established supply chains from metropolitan France and the wider EU. A foreign-incorporated entity cannot easily undercut those channels on price without absorbing logistics costs that erode margins.

- Revenue projections must be built on export or regional Caribbean reach, not local absorption alone

- INSEE categorizes Guadeloupe as an overseas region, which affects how market size statistics are measured and reported

- Sectoral concentration in tourism and agriculture limits the range of viable industries for new entrants

- Any business model requiring repeat-purchase volume faces structural limits tied to the resident population count

Despite being an EU territory, Guadeloupe is excluded from the EU VAT area, which means intra-EU trade simplifications that typically reduce costs for mainland French businesses do not apply to transactions routed through a locally incorporated entity.

Restricted Access to Mainland French Banking

Guadeloupe banking access restrictions affect foreign-incorporated entities in ways that differ meaningfully from businesses registered in metropolitan France.

Structural Limits on Account Access

French overseas collectivities operate within the French banking system, but branches of major French banks in Guadeloupe often require that parent companies or foreign shareholders hold an established credit history within France itself. Without that history, opening a professional business account for a newly formed SARL or SAS can take considerably longer than on the mainland, and some institutions redirect applicants entirely to their metropolitan branches, creating a disconnect between where the entity is registered and where financial operations are actually managed.

Practical Consequences for Foreign Operators

For a non-resident director or foreign shareholder, mainland French banking limitations in Guadeloupe translate directly into delayed operational timelines. A firm cannot invoice clients, pay URSSAF contributions, or execute payroll until a compliant business account is active, meaning banking delays compound into broader compliance exposure. This structural gap is less pronounced for entities with existing ties to the French financial system, which effectively excludes most first-time entrants from a faster path.

Overcoming Banking and Setup Challenges in Guadeloupe

Get guidance on structuring your entity and banking approach to reduce delays when establishing a business presence in Guadeloupe.

Complex SAS and SARL Formation Requirements

Guadeloupe SAS SARL formation challenges begin before you trade a single euro, as both structures require compliance with French metropolitan corporate law rather than any simplified overseas regime.

- Forming an SAS requires drafting statuts constitutifs that satisfy the requirements of the French Code de commerce, a document-heavy process that typically demands a local avocat or notaire and adds professional fees before registration is even filed.

- SARL registration through the Centre de Formalités des Entreprises (CFE) or its successor, the guichet unique, requires submitting certified documentation that non-French-speaking founders cannot practically prepare without paid translation and legal support.

- Both entity types require a minimum share capital deposit in a French-regulated bank account before incorporation is finalised, creating a capital lock-up period that delays operational start dates.

- Complex SARL registration procedures in Guadeloupe include mandatory publication of a legal notice in a journal d'annonces légales, an obligation that generates recurring costs even at the formation stage.

- SAS incorporation requirements impose no statutory minimum capital, yet lender and counterparty expectations in the local market frequently make undercapitalised SAS structures commercially unviable from the outset.

Dependence on Metropolitan France for Legal Updates

Guadeloupe legal update dependence risks stem from a structural reality: as an overseas department under Article 73 of the French Constitution, the territory has no independent legislative authority. Laws enacted by the French Parliament in Paris apply automatically, and your business has no local legislative channel to influence or anticipate those changes.

When France amends corporate law, tax codes, or labour regulations, those reforms take effect in Guadeloupe through the same national instruments — ordinances, décrets, and lois — without any local parliamentary filter. A regulatory change passed in the Assemblée nationale can alter your compliance obligations with little lead time for businesses operating remotely from mainland France.

This dependency creates a specific operational exposure: foreign business owners monitoring French regulatory developments must track sources like Légifrance and Journal Officiel de la République Française, both published in French, with no translated or locally adapted guidance issued by Guadeloupe's regional council.

The Conseil Régional de Guadeloupe holds economic development powers but cannot legislate on matters of company law or taxation, which remain exclusively national competencies.

A foreign-owned SARL incorporated in Guadeloupe in early 2023 that did not monitor France's loi de finances for 2024 could have missed changes to the IS (impôt sur les sociétés) rate structure and applicable thresholds, resulting in incorrect quarterly tax provisioning and potential penalties under the Code général des impôts.

Language and Administrative Barriers for Non-French Speakers

Guadeloupe language barrier business risks are immediate and structural. All official documentation, regulatory filings, and correspondence with bodies such as the Centre de Formalités des Entreprises (CFE) and the Greffe du Tribunal de Commerce must be submitted exclusively in French.

Contracts, articles of association, and statutory documents that are drafted or notarized in any other language carry no legal standing until formally translated. This creates a direct dependency on sworn translators (traducteurs assermentés) and French-qualified legal professionals, adding cost and delay to every procedural step.

French administrative requirements in Guadeloupe are not simplified for foreign applicants. The CERFA forms used for business registration, tax enrollment, and social declaration follow metropolitan French administrative conventions, with no official English-language equivalents provided at the territorial level.

Non-French speaker incorporation challenges extend past setup. Ongoing obligations, including annual filings with the Greffe and correspondence with the Direction Générale des Finances Publiques (DGFiP), require continued access to French-language legal support throughout the life of the entity.

Any legal document submitted to a French territorial authority in a language other than French will be rejected outright, regardless of its content or the applicant's business standing.

Mitigating These Incorporation Challenges

Mitigating these incorporation challenges in Guadeloupe requires structural preparation rather than reactive adjustments after formation.

- Register your SAS or SARL statutes with the Greffe du Tribunal de Commerce before commencing operations to ensure legal standing under French commercial law.

- Enroll with URSSAF at the point of incorporation to establish your social contribution obligations from the outset and avoid penalties for late registration.

- Open a dedicated professional account with a French metropolitan bank or an EU-licensed institution that accepts overseas department entities before depositing share capital.

- Appoint a locally registered legal representative fluent in French to manage filings with the Centre de Formalités des Entreprises and official correspondence.

- Monitor the Journal Officiel de la République Française for regulatory updates, given the jurisdiction's dependence on metropolitan France for legislative changes.

Because Guadeloupe operates under the full French legal order, mitigation steps that work in comparable overseas departments do not always translate identically here. The Code de Commerce governs the structural foundations, and compliance obligations apply without regional modification.

Guadeloupe's Overall Business Viability

Guadeloupe business viability risks are real and measurable, but they do not disqualify the territory as an incorporation destination. For businesses that require a legal foothold within the EU and French regulatory system, the overhead costs and administrative complexity may be an acceptable trade-off.

| Pro | Con |

|---|---|

| Full EU market access through French overseas department status | French regulatory framework applies in full, including URSSAF obligations |

| Corporate entities such as SAS and SARL provide recognised legal structures under French law | SAS and SARL formation requirements carry significant procedural and notarial complexity |

| Access to French and EU trade agreements | Local market is small, limiting domestic revenue potential |

| Legal stability under the French Civil Code | Non-French-speaking founders face material administrative and language barriers |

| Eligible for certain French overseas incentive programmes | Operating costs, including social contributions, are high relative to comparable offshore jurisdictions |

Dependence on Metropolitan France for legislative updates means your compliance obligations can shift without local legislative process. Banking access also remains constrained for foreign-owned entities without an established presence on the French mainland.

Compliance Services for Companies in Guadeloupe

Maintain your Guadeloupe entity in good standing with French regulatory requirements, including URSSAF filings, corporate reporting, and ongoing statutory obligations.

Conclusion

The Guadeloupe incorporation drawbacks summary is straightforward: operating through a French overseas department means accepting the full weight of metropolitan French corporate law, URSSAF contribution obligations, and a local consumer base too small to sustain most business models on its own. These structural factors are not peripheral concerns. For businesses without the administrative capacity to manage French-language compliance requirements or the financial position to absorb high payroll costs, the formation challenges present real operational constraints. Specialist guidance covering both French regulatory requirements and the department's specific administrative environment becomes a practical necessity before committing to formation.

Expanship's Support for Your Guadeloupe Expansion

Expanship Guadeloupe incorporation support is designed to reduce the operational burden that comes with establishing a company under the full French legal and administrative system. From managing URSSAF registration and social contribution filings to coordinating with the Greffe du Tribunal Mixte de Commerce, your business will have a specialist handling the procedural weight of Guadeloupe's compliance framework on your behalf.

Our services cover the practical requirements of setting up and maintaining a legal presence in the territory:

- Your company registration and all supporting document preparation are handled from the outset.

- We provide a registered agent and local office address for your entity.

- Our team liaises directly with government offices and regulatory bodies on your behalf.

- Post-incorporation compliance obligations are tracked and managed on an ongoing basis.

- We facilitate introductions to banking institutions suited to your business structure.

- Tax registration and coordination with local fiscal authorities are included in our scope.

To discuss your specific requirements, contact Expanship Guadeloupe.

Frequently Asked Questions (FAQ)

Yes, both the SAS and SARL are governed by French company law as codified in the Code de commerce, and there are no local carve-outs or simplified rules for entities registered in Guadeloupe. This means formation requirements, ongoing governance obligations, and statutory filing deadlines mirror those enforced in mainland France. Foreign founders cannot expect a lighter regulatory touch simply because the entity is based in an overseas territory.

Guadeloupe-incorporated businesses frequently face additional scrutiny when opening accounts with major French banks, particularly when the beneficial owners are non-residents. Banks may request extended due diligence documentation and some institutions decline to service overseas department entities remotely. This creates practical delays in capitalising your business at the point of formation.

Late filings with the Greffe can result in court-ordered financial penalties and, in some cases, personal liability for directors who fail to comply with mandatory deposit deadlines for annual accounts. The Tribunal Mixte de Commerce in Basse-Terre handles commercial matters for the territory and applies the same enforcement standards as commercial courts in France. Persistent non-compliance can also affect a company's standing in the Registre du Commerce et des Sociétés, which is publicly visible to creditors and counterparties.

Operating costs in Guadeloupe are generally higher than in jurisdictions such as Saint-Barthélemy, which has its own fiscal regime and is not subject to standard French VAT or the same social contribution rates. In Guadeloupe, employer social charges under the French system apply in full, and while there are some partial exemptions under the LODEOM (Loi pour le Développement Économique des Outre-Mer) for certain sectors, these are conditional and sector-specific. A business that does not qualify for LODEOM relief faces the full weight of French payroll and operating costs.

Managing compliance without French-language capability is not realistic. All filings with the Greffe, correspondence with URSSAF, and interactions with the Direction des Finances Publiques are conducted exclusively in French, and there is no official English-language process available. Errors in formal documents submitted to these bodies can result in rejected applications, delayed registrations, or financial penalties that compound quickly.

Because Guadeloupe is an integral part of France and subject to French law, changes to the Code de commerce, tax legislation, or labour law apply automatically unless explicitly excluded. A company that fails to track and implement these updates risks operating outside current legal requirements, which can expose directors to personal liability. There is no local legislative buffer that gives businesses additional time to adapt after a change takes effect in metropolitan France.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.