Key Takeaways

- The Companies Act 2013 governs all corporate registrations in Gambia, with the Private Limited Company being the most frequently chosen structure due to its closed ownership model and restricted share transfer rules.

- Foreign businesses entering Gambia can establish a branch office, representative office, or subsidiary, each carrying different operational permissions and levels of local activity.

- Gambia applies a territorial tax system, meaning resident companies are generally liable for tax only on income sourced within the jurisdiction.

- Partnership structures in Gambia accommodate professional collaborations but expose general partners to personal liability, making entity selection a decision with direct legal consequences.

Introduction to Entity Types in Gambia

Gambia is a small West African nation bordered by Senegal on three sides and the Atlantic Ocean to the west. It operates as an independent republic, and company registration falls under the authority of the Registrar of Companies, which administers corporate filings in accordance with the Companies Act 2013.

The country applies a territorial tax system, meaning resident companies are generally taxed on income sourced within the jurisdiction.

Several types of business entities in Gambia are available to both local and foreign investors. These include the Public Limited Company, Private Limited Company, General Partnership, Limited Partnership, Sole Proprietorship, Branch Office, Representative Office, and Subsidiary. Each structure carries distinct implications for liability, ownership, governance, and tax treatment. Your choice of entity will shape how the business operates from day one.

This article examines each of these Gambia company types in detail — covering formation requirements, legal obligations, and the regulatory conditions that apply to each.

An Overview of Business Structures in Gambia

Gambian company law recognises several distinct legal forms for conducting business, each governed primarily by the Companies Act 2013 and, for unincorporated structures, the relevant partnership legislation. A separate registration regime applies to foreign entities seeking a commercial presence through branches or representative offices. Each legal form carries different implications for liability, ownership, and permissible activities.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (PLC) | Incorporated company | Limited | Taxed | Permitted | 7 shareholders | Registrar General | Companies Act 2013 |

| Private Limited Company (Ltd) | Incorporated company | Limited | Taxed | Permitted | 1 shareholder | Registrar General | Companies Act 2013 |

| General Partnership | Unincorporated | Unlimited | Taxed | Permitted | 2 partners | Registrar General | Partnership Act |

| Limited Partnership | Unincorporated | Mixed | Taxed | Permitted | 2 partners | Registrar General | Partnership Act |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed | Permitted | 1 owner | Registrar General | Business Registration Act |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Permitted | N/A | Registrar General | Companies Act 2013 |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | Not permitted | N/A | Registrar General | Companies Act 2013 |

| Subsidiary | Incorporated company | Limited | Taxed | Permitted | 1 shareholder | Registrar General | Companies Act 2013 |

Each of these structures is examined in full in the sections below.

Public Limited Company (PLC) under the Companies Act 2013

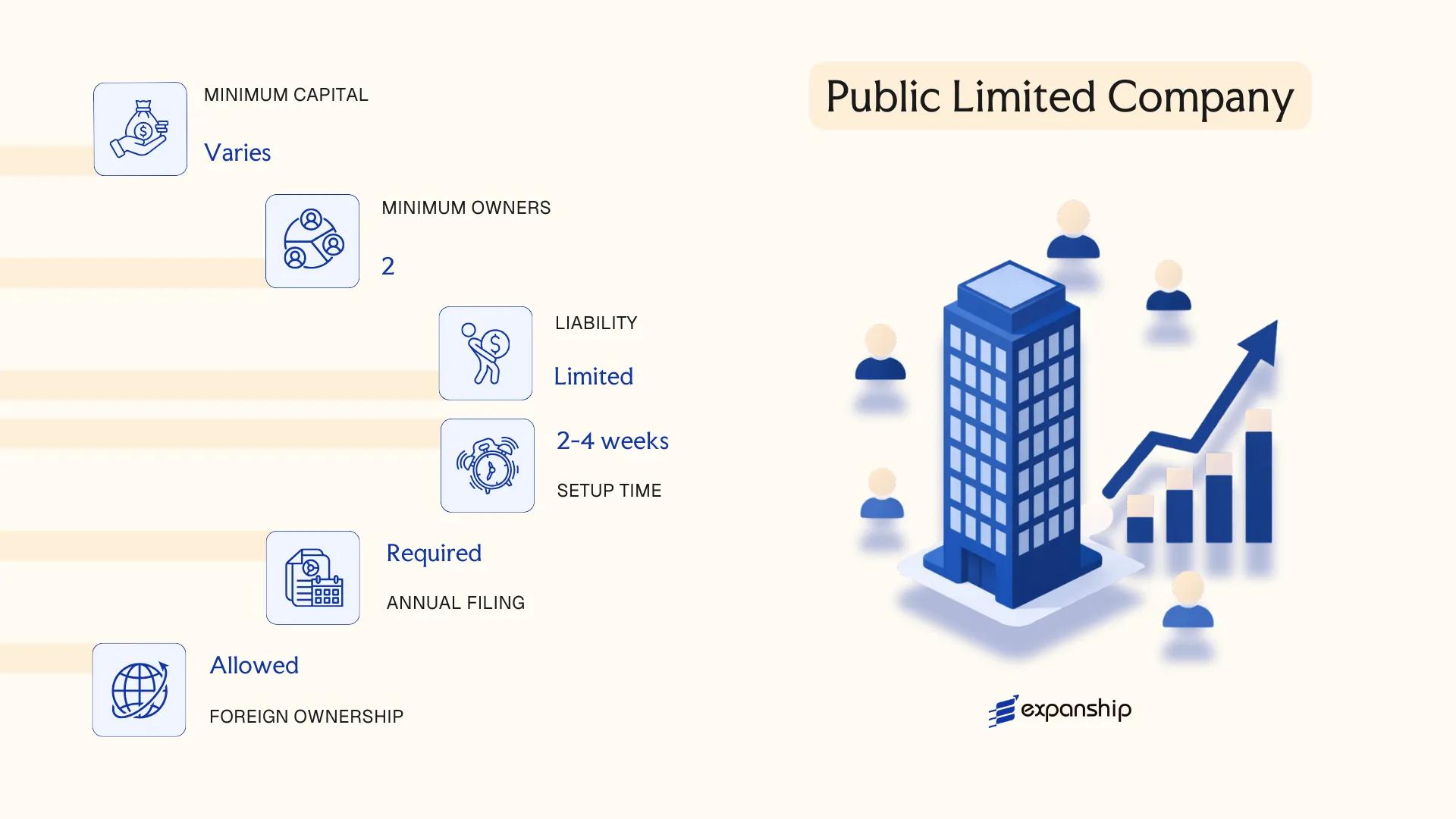

A Gambia public limited company PLC formation is governed by the Companies Act 2013, which replaced the earlier Companies Act and modernised the statutory framework for corporate entities. A PLC carries separate legal personality, meaning the company's obligations are distinct from those of its shareholders, and liability is limited to the amount unpaid on shares held.

Shares in a PLC may be offered to the public and listed on a recognised exchange, which distinguishes this structure from its private counterpart. The entity is capable of raising capital from a broad investor base, though this comes with correspondingly higher disclosure and governance obligations under the Act.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Incorporated under the Companies Act 2013 |

| Members | Shareholders (minimum 7, no statutory maximum) | Directors: minimum 2; at least one must be ordinarily resident |

| Local Presence | Registered office in Gambia required | Must maintain a physical address on record with the registrar |

| Capital | Gambian Dalasi (GMD); minimum authorised capital applies | Shares may be offered to the public; listing requires additional regulatory approval |

| Privacy | Director and shareholder details filed on public record | Beneficial ownership disclosure required under AML regulations |

Focus Points

- Taxation: Corporate income tax applies to profits; VAT registration is required once turnover thresholds are met; withholding tax applies to dividends, interest, and royalties paid to non-residents — administered by the Gambia Revenue Authority.

- Annual compliance: Mandatory annual returns, audited financial statements, and AGM requirements under the Companies Act 2013.

- Economic substance: No formal economic substance regime equivalent to offshore jurisdictions, but local directorship and registered office requirements apply.

- Conversion: A PLC may be re-registered as a private limited company subject to shareholder approval and filing with the Companies Registry.

- Public offering restrictions: Any public issuance of securities requires compliance with applicable capital markets regulations overseen by the relevant regulatory authority.

Closing

A PLC suits businesses seeking public investment, large-scale trading operations, or eventual exchange listing, but the mandatory public disclosure requirements and higher governance obligations make it less practical for closely held or confidential structures.

This structure is most appropriate for large enterprises or joint ventures intending to raise capital from the public or pursue a future stock exchange listing.

Company Incorporation in Gambia

Incorporate your business entity in Gambia with end-to-end support from Expanship.

Private Limited Company (Ltd) under the Companies Act 2013

A Gambia private limited company Ltd registration is governed by the Companies Act 2013, the primary legislation regulating corporate entities in the country. The private limited company holds separate legal personality, meaning it exists independently from its shareholders, and liability is capped at the amount unpaid on each member's shares.

Structurally, the private limited company sits between a sole proprietorship and a public company. It restricts the right to transfer shares, prohibits any public offering of its securities, and limits membership to a defined ceiling — making it the default choice for closely held businesses and foreign investors seeking a controlled ownership structure.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company (Ltd) | Incorporated under the Companies Act 2013; separate legal personality |

| Members | Shareholders: min. 1, max. 50 | Directors: min. 1; no statutory requirement for a local director |

| Local Presence | Registered office address required in Gambia | Must be a physical address; a P.O. box is generally not sufficient |

| Share Capital | GMD-denominated; no statutory minimum capital prescribed | Capital structure defined in the memorandum and articles of association |

| Share Transfer | Restricted by the articles of association | Shares cannot be offered to the public |

| Privacy | Shareholder and director details filed with the Registrar of Companies | Records are accessible; beneficial ownership disclosures may apply |

Focus Points

- Taxation: Corporate income tax applies to resident companies on worldwide income; non-resident entities are taxed on Gambia-source income only. VAT, withholding tax on dividends and service payments, and stamp duty on share transfers and instruments are also applicable.

- Annual Compliance: Companies must file annual returns and audited financial statements with the Registrar of Companies under the Companies Act 2013.

- Economic Substance: No formal economic substance regime currently applies to domestic private limited companies, though general tax residency rules require demonstrable management and control.

- Treaty Access: Gambia has a limited network of double taxation agreements; treaty benefits should be verified before structuring cross-border income flows.

- Conversion: A private limited company may be re-registered as a public limited company by satisfying the relevant requirements under the Companies Act 2013 and obtaining Registrar approval.

Closing Paragraph

The private limited company is well-suited to trading operations, holding structures, and joint ventures where ownership needs to remain within a defined group. Its limited liability protection is a clear advantage, though the restriction on public share issuance limits its utility as a vehicle for large-scale capital raising.

Foreign investors and local entrepreneurs seeking a scalable, liability-protected entity for trading, holding, or operational business activities with controlled shareholding.

Partnerships in Gambia [General Partnership, Limited Partnership]

Partnership registration in Gambia is governed primarily by the Partnership Act, with general and limited partnerships operating as distinct structural forms under Gambian commercial law. Unlike a private limited company, a general partnership does not possess separate legal personality — the partners themselves bear direct liability for the firm's obligations. A limited partnership introduces a tiered liability structure, distinguishing between general partners who manage the business and limited partners whose exposure is capped at their capital contribution.

Registration is administered through the Gambia Revenue Authority (GRA) and the relevant business registration bodies. Both structures require registration before commencing commercial activity.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Form | Unincorporated; no separate legal personality | Unincorporated; no separate legal personality |

| Members | Partners (minimum 2; no statutory maximum) | Minimum 1 general partner + 1 limited partner |

| Liability | Unlimited for all partners | Unlimited for general partners; capped for limited partners |

| Local Presence | Registered business address required | Registered business address required |

| Capital | No statutory minimum; contributions in GMD | No statutory minimum; limited partner liability tied to contribution amount |

| Privacy | Partner names typically appear on public record | General partner names publicly disclosed; limited partners may have reduced exposure |

Focus Points

- Taxation: Partnerships are generally taxed on a pass-through basis; individual partners are subject to personal income tax on their share of profits, with applicable rates under the GRA's income tax framework — VAT registration applies where turnover thresholds are met.

- Annual Compliance: Annual renewal of business registration and filing of applicable returns with the GRA are required to maintain good standing.

- Restrictions: Foreign nationals may face ownership or sector-specific restrictions under Gambian investment regulations; confirmation through the Gambia Investment and Export Promotion Agency (GIEPA) is advisable.

- Conversion: Converting a partnership to a limited liability structure requires a fresh incorporation process rather than a direct statutory conversion.

Sub-Types

General Partnership

All partners hold equal management authority and bear joint and several liability for the firm's debts. This structure is commonly used by professional services firms or small trading operations where partners actively participate in day-to-day management.

Limited Partnership

Limited partners contribute capital but are prohibited from participating in management; exercising management control risks forfeiting their liability protection. This form is used where passive investors wish to fund a business without assuming operational responsibility.

Partnerships suit trading operations, professional practices, and small-scale joint ventures where simplified governance is preferred over corporate formality. The main advantage is low setup cost and administrative simplicity; the primary drawback is unlimited personal liability for at least one partner, which poses material risk in commercial disputes or insolvency.

This structure is best suited for small businesses or professional operators seeking a low-cost entry point with a known co-venturer, where personal liability exposure is considered manageable.

Sole Proprietorship

Sole proprietorship registration in Gambia is governed primarily by the Business Names Act, which requires any individual trading under a name other than their own to register that name with the Registrar General's Department. Unlike a private limited company, this structure carries no separate legal personality — the business and its owner are legally the same person, meaning personal assets are fully exposed to business liabilities.

Registration is straightforward. You submit the prescribed forms to the Registrar General's Department, pay the applicable fee, and obtain a certificate of registration. No minimum capital is required, and there is no requirement to file audited accounts with the Registrar.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Owner Title | Sole Proprietor | Single individual only; no co-owners |

| Membership | 1 person (maximum 1) | Cannot admit partners without converting to partnership |

| Local Presence | Registered business address required | Must be a physical address within The Gambia |

| Capital | No minimum capital requirement | Operates on personal funds; no share structure |

| Privacy | Owner's name on public register | Business name registration is publicly searchable |

Focus Points

- Taxation: Subject to personal income tax on business profits under the Income and Value Added Tax Act; VAT registration is required once turnover exceeds the statutory threshold; no separate corporate income tax applies.

- Annual Compliance: No mandatory annual filing with the Registrar General, but renewal of the business name registration is required periodically.

- Treaty Access: As an unincorporated entity, a sole proprietorship does not access double tax treaties independently; any treaty relief applies at the individual owner's level.

- Conversion: Can be converted to a private limited company by incorporating a new entity and transferring business assets; there is no automatic conversion mechanism.

- Restrictions: Cannot raise equity capital from third parties, issue shares, or limit personal liability without restructuring into a separate legal entity.

Closing Paragraph

A sole proprietorship suits low-capital, owner-operated trading or service activities where administrative simplicity outweighs the need for liability protection. The principal advantage is minimal registration cost and no ongoing statutory filing burden; the clear limitation is unlimited personal liability, which exposes the owner's private assets to any business debt or legal claim.

This structure is best suited for individual residents or self-employed professionals testing a local market before committing to formal incorporation.

Foreign Business Presence in Gambia [Branch Office, Representative Office, Subsidiary]

Foreign company setup in Gambia is governed primarily by the Companies Act 2013, administered by the Registrar General's Department. The Act sets out the conditions under which overseas entities may conduct business within the country, requiring registration before commencing any commercial activity.

Three structural options are available to foreign firms: a branch office, a representative office, or a locally incorporated subsidiary. Each carries a distinct legal character and operational scope, and the choice affects liability exposure, tax treatment, and permitted activities.

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary |

|---|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; limited operational scope | Locally incorporated private limited company; separate legal entity |

| Governing Instrument | Certificate of Compliance issued by Registrar General's Department | Registration with Registrar General's Department | Memorandum and Articles of Association |

| Directors / Officers | Local representative required | Local representative required | Minimum 2 directors |

| Local Presence | Registered office in Gambia | Registered office in Gambia | Registered office; resident director recommended |

| Capital | No statutory minimum; parent's capital backs operations | No statutory minimum | Subject to Companies Act 2013 requirements for private companies |

| Privacy | Parent company details disclosed on registration | Parent company details disclosed | Director and shareholder details filed with Registrar |

Focus Points

- Taxation: Branch offices are taxed on Gambia-sourced income under the Income and Value Added Tax Act; subsidiaries are subject to corporate income tax as resident entities, and both may attract withholding tax on dividends, interest, and royalties remitted abroad.

- Permitted Activities: Representative offices are restricted to liaison, market research, and promotional activities — they may not generate revenue or enter into commercial contracts directly.

- Economic Substance: No formal economic substance regime equivalent to those in certain offshore centres currently applies, though genuine local activity is expected for tax residency purposes.

- Treaty Access: Gambia has a limited network of double taxation agreements; subsidiaries, as resident entities, are better positioned to access any applicable treaty benefits than branch offices.

- Repatriation: Profit remittances by branches and subsidiaries are subject to applicable withholding tax rates under domestic law; no specific exchange control legislation restricts repatriation, though Central Bank of The Gambia approval may be required for large transfers.

Sub-Types

Branch Office

A branch carries no separate legal personality, meaning the foreign parent retains full liability for its obligations. It is suited to firms that want direct operational presence without establishing an independent local entity.

Representative Office

This structure permits only non-revenue-generating activities, such as market research or coordination functions. Because it cannot contract commercially, it carries lower compliance overhead but significant operational restrictions.

Subsidiary

Incorporated as a private limited company under the Companies Act 2013, a subsidiary is a distinct legal entity from its foreign parent. This separation limits parental liability and makes the subsidiary the structure of choice for full commercial operations.

Closing

A foreign subsidiary is most appropriate for businesses intending to trade actively, hold assets, or enter long-term contracts within the jurisdiction, while branch registration suits firms requiring an operational foothold without a standalone corporate structure. The principal drawback of a branch is the unrestricted liability it imposes on the parent entity.

Foreign subsidiaries incorporated under the Companies Act 2013 are best suited to multinational firms seeking full commercial operations with liability separation from their parent entity.

How to Choose the Right Entity Type in Gambia

Selecting how to structure your business presence is one of the few decisions that reshapes every operational, tax, and compliance obligation that follows — understanding how to choose a business structure in Gambia before incorporation prevents costly restructuring later.

Why Your Entity Choice Matters

The structure you register determines your legal exposure from day one. Selecting the wrong form carries concrete consequences:

- Registering a branch or representative office when your activity qualifies as active local trade may constitute a breach of the Companies Act 2013, exposing the entity to deregistration or financial penalties by the Registrar General's Department.

- Forming a private limited company when your primary objective is asset protection or succession planning binds you to annual shareholder obligations, filing requirements, and directorship duties that would not apply under a trust arrangement.

- Choosing a structure that mandates audited financial statements for a single-person consultancy introduces recurring professional costs that a sole proprietorship or simple partnership would not trigger.

- Selecting an entity without adequate substance capacity, where substance requirements apply, can result in reporting failures and potential regulatory action under applicable anti-avoidance provisions.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as banking or insurance, and passive asset-holding each point toward distinct entity forms under Gambian company law.

- Ownership and Management: A sole director-shareholder structure suits a private limited company, while multi-party arrangements may be better served by a partnership deed.

- Tax Objectives: Your eligibility for specific tax treatments under the Income and Value Added Tax Act depends on which entity type you register.

- Substance Capacity: If you cannot maintain a physical office or resident management, the entity form you select must be consistent with that operational reality.

- Exit Strategy: Not all Gambian structures permit redomiciliation or straightforward conversion, so your anticipated exit route should inform initial registration decisions.

- Privacy Requirements: The Registrar General's Department maintains a public register; nominee arrangements and their limitations should be factored in where confidentiality is a priority.

Corporate Compliance Services in Gambia

Ongoing compliance support for companies incorporated in Gambia, including annual filings, registered agent maintenance, and regulatory reporting.

Conclusion

Setting up a company in Gambia requires matching the chosen structure to the operational profile, ownership requirements, and long-term objectives of your business. Under the Companies Act 2013, the Private Limited Company remains the most commonly registered entity, favoured for its closed ownership structure and restricted share transfer rules. The Public Limited Company suits ventures seeking broader capital access. Partnerships serve professional collaborations where personal liability is acceptable, while a sole proprietorship fits individual traders operating on a smaller scale. For foreign firms, a subsidiary offers full operational capacity, whereas a branch or representative office limits local activity by design.

Regulated by the Registrar General's Department, the formation framework has been subject to incremental modernisation efforts, and continued alignment with regional ECOWAS standards is expected to shape future compliance requirements. Your choice of structure will determine the reporting obligations, tax treatment, and operational scope that apply from incorporation onward.

How Expanship Can Assist You

Expanship provides company incorporation services in Gambia for foreign investors and local founders registering entities under the Companies Act 2013. From Private Limited Companies to Branch Offices, our team manages filings directly with the Registrar General's Department, the authority responsible for business registration in The Gambia.

From initial document preparation through to post-incorporation compliance, our Gambia business setup support covers every procedural stage:

- Company name reservation and registration with the Registrar General's Department

- Preparation and legalization of constitutional documents

- Registered agent and registered office provision

- Government filing and ongoing registrar liaison

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance for corporate account opening

Your business structure determines which obligations apply and when — getting the formation right from the start avoids unnecessary rework later.

Reach out to Expanship Gambia to discuss your registration requirements.

Frequently Asked Questions (FAQ)

The Private Limited Company (Ltd) is the most frequently registered structure. It limits shareholder liability, permits a single-member setup, and satisfies the requirements of most commercial activities under the Companies Act 2013.

A Branch is not a separate legal entity — it remains an extension of the foreign parent and carries the parent's liability. A Private Limited Company is locally incorporated, taxed as a resident entity, and subject to full annual compliance obligations including audited accounts and annual returns filed with the Registrar.

A Private Limited Company restricts share transfers and is not required to offer shares to the public, limiting disclosure relative to a Public Limited Company. Nominee director and shareholder arrangements are generally permissible under Gambian law, though ultimate beneficial ownership disclosure requirements apply under anti-money laundering regulations.

No. A sole proprietorship and a single-member Private Limited Company can each be formed by one individual. General Partnerships and Limited Partnerships require a minimum of two partners, making solo formation legally impermissible for those structures.

Foreign nationals may incorporate a Private Limited Company, a Public Limited Company, or establish a Branch or Subsidiary. A Representative Office is also available for non-trading purposes. Foreign investors must register with the Gambia Investment and Export Promotion Agency (GIEPA) and may be subject to minimum capital thresholds depending on the sector.

Conversion between entity types is addressed under the Companies Act 2013, which provides mechanisms for re-registration. A Private Limited Company may re-register as a Public Limited Company, subject to meeting the applicable capital and membership requirements at the time of conversion.

No. A sole proprietorship and a general partnership do not confer separate legal personality — the owner or partners remain personally liable for business obligations. Private Limited Companies, Public Limited Companies, and properly registered Limited Partnerships hold distinct legal identities under the Act.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.