Key Takeaways

- Ghana's primary corporate legislation, the Companies Act, 2019 (Act 992), governs all incorporated business entities and replaced the Companies Act, 1963 (Act 179) with structural reforms to the registration framework.

- All business entities in Ghana must be registered with the Registrar General's Department, which maintains incorporation records across the country's full range of available structures.

- The Private Limited Company is the most commonly registered entity form in Ghana, favored by both resident and foreign investors for its liability protection and manageable compliance obligations.

- Unincorporated arrangements such as general and limited partnerships fall outside Act 992 and are instead governed by the Incorporated Private Partnerships Act, 1962 (Act 152).

Introduction to Entity Types in Ghana

Ghana is a sovereign republic in West Africa, bordered by Côte d'Ivoire to the west, Burkina Faso to the north, and Togo to the east. Company registration falls under the jurisdiction of the Registrar General's Department, the body responsible for incorporating and maintaining records of all business entities operating in the country. The governing legislation for corporate entities is the Companies Act, 2019 (Act 992), which replaced the earlier Companies Act, 1963 (Act 179) and introduced several structural reforms to the registration framework.

Ghana operates a territorial-based tax system, with corporate income tax applicable to resident companies on their worldwide income and to non-resident entities on income sourced within the country.

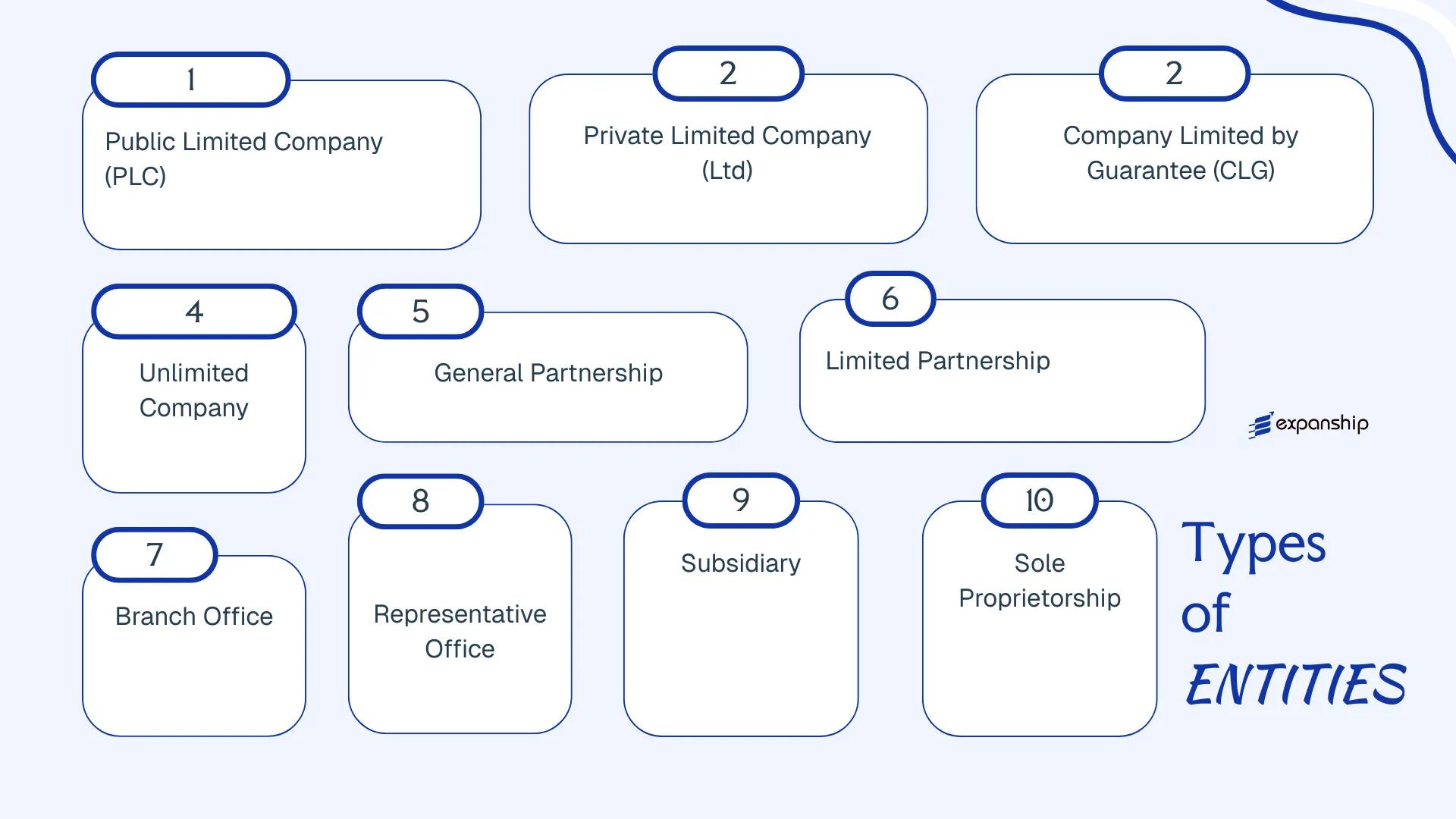

The types of business entities in Ghana available under current law include the Public Limited Company, Private Limited Company, Company Limited by Guarantee, Unlimited Company, General Partnership, Limited Partnership, Branch Office, Representative Office, Subsidiary, and Sole Proprietorship. Each structure carries distinct liability provisions, ownership requirements, and compliance obligations. This article examines each entity type in detail, drawing directly from Act 992 and related regulatory requirements.

An Overview of Business Structures in Ghana

Ghana's company law framework provides six principal business structures available to resident and foreign investors. The Companies Act, 2019 (Act 992), administered by the Registrar General's Department, is the primary legislation governing corporate formation and operation, while the Registration of Business Names Act, 2020 (Act 1043) covers unincorporated forms such as sole proprietorships and general partnerships. Each structure carries distinct liability, ownership, and tax implications suited to different commercial purposes.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (PLC) | Incorporated company | Limited to shares | Taxed | Yes | 7 shareholders | Registrar General's Department | Act 992 |

| Private Limited Company (Ltd) | Incorporated company | Limited to shares | Taxed | Yes | 1 shareholder | Registrar General's Department | Act 992 |

| Company Limited by Guarantee | Incorporated company | Limited to guarantee | Taxed / Exempt | Restricted | 1 member | Registrar General's Department | Act 992 |

| Unlimited Company | Incorporated company | Unlimited | Taxed | Yes | 1 shareholder | Registrar General's Department | Act 992 |

| General Partnership | Unincorporated firm | Unlimited | Taxed (pass-through) | Yes | 2 partners | Registrar General's Department | Act 1043 |

| Limited Partnership | Unincorporated firm | Mixed (general/limited) | Taxed (pass-through) | Yes | 2 partners | Registrar General's Department | Act 1043 |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Yes | N/A | Ghana Investment Promotion Centre | Act 992 |

| Representative Office | Foreign entity extension | Parent liable | Exempt from trading income | No | N/A | Ghana Investment Promotion Centre | Act 992 |

| Subsidiary | Incorporated company | Limited to shares | Taxed | Yes | 1 shareholder | Registrar General's Department | Act 992 |

| Sole Proprietorship | Unincorporated business | Unlimited | Taxed | Yes | 1 owner | Registrar General's Department | Act 1043 |

Each of these structures is examined in full in the sections below.

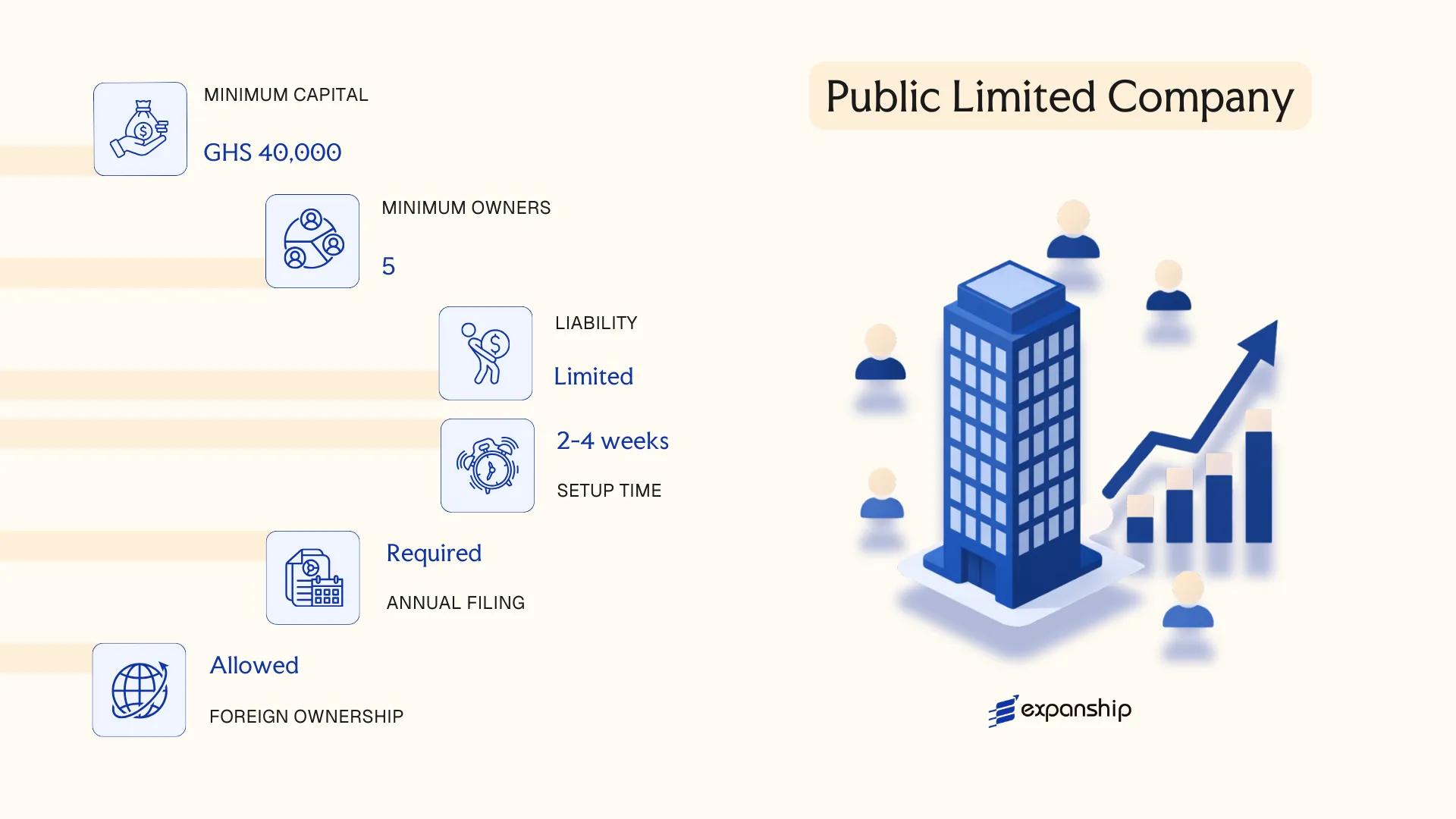

Public Limited Company (PLC) under the Companies Act, 2019 (Act 992)

A public limited company Ghana Act 992 governs is formally incorporated under the Companies Act, 2019 (Act 992), which replaced the earlier Companies Act, 1963 (Act 179). The entity holds a separate legal personality distinct from its shareholders, meaning it can own assets, enter contracts, and incur liabilities in its own name.

Shareholders' exposure is capped at the nominal value of their shares. This structure allows the firm to raise capital from the general public, including through a listing on the Ghana Stock Exchange (GSE), making it the standard vehicle for large-scale, publicly traded enterprises.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Governed by the Companies Act, 2019 (Act 992); registered with the Registrar-General's Department (RGD) |

| Governing Members | Shareholders (owners), Directors (management), Company Secretary (mandatory) | Minimum 2 directors; at least one Company Secretary required |

| Membership | Minimum 7 shareholders; no upper limit | Shares may be offered to the general public |

| Local Presence | Registered office address in Ghana required | Must maintain a physical registered address; a registered agent is not a statutory requirement but is common in practice |

| Share Capital | No statutory minimum share capital prescribed under Act 992 | Capital denominated in Ghanaian Cedi (GHS); must state authorised capital in the constitution |

| Privacy | Shareholder and director details filed on public record at the RGD | Annual returns and financial statements accessible to the public |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate of 25%; VAT applies to taxable supplies; withholding tax obligations apply to dividends, interest, and service payments; stamp duty is payable on certain instruments and share transfers.

- Annual Compliance: Must file annual returns and audited financial statements with the RGD; a statutory audit is mandatory regardless of size.

- Exchange Listing: A PLC may apply to list shares on the Ghana Stock Exchange, subject to GSE listing rules and Securities and Exchange Commission (SEC) Ghana regulations.

- Restrictions: Cannot commence business until the RGD issues a certificate to commence business; public share offerings require SEC approval.

- Conversion: May convert to a private limited company under Act 992, subject to shareholder approval and RGD filings.

Closing

A PLC suits large enterprises seeking public capital through equity markets, but the mandatory audit requirement, SEC oversight for public offerings, and the disclosure obligations on the public register create a compliance burden that smaller businesses may find disproportionate.

This structure is best suited for established businesses with significant capital requirements seeking to list on the Ghana Stock Exchange or raise funds from the general public.

Company Incorporation in Ghana

Expanship assists with the end-to-end registration of companies in Ghana, including PLCs, through the Registrar-General's Department.

Private Limited Company (Ltd) under the Companies Act, 2019 (Act 992)

The private limited company Ghana Ltd registration process is governed by the Companies Act, 2019 (Act 992), which replaced the earlier Companies Act, 1963 (Act 179). Under Act 992, a private limited company exists as a separate legal entity, meaning it can own property, enter contracts, and incur liabilities in its own name.

Liability exposure for shareholders is capped at the amount unpaid on their shares. This hybrid structure — combining corporate personality with restricted transferability of shares — makes it the most commonly registered business form for both domestic entrepreneurs and foreign investors operating through a local subsidiary.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by shares | Incorporated under Act 992; separate legal personality |

| Members | Shareholders: min. 1, max. 50 | Excludes employees holding shares; directors: min. 2 |

| Local Presence | Registered office address in Ghana required | Must be a physical address; P.O. Box alone not sufficient |

| Capital | No statutory minimum share capital; currency typically GHS | Foreign-owned entities may face sector-specific capital thresholds under the Ghana Investment Promotion Centre Act, 2013 (Act 865) |

| Share Transfer | Restricted by Articles of Association | Public offering of shares is prohibited |

| Privacy | Beneficial ownership disclosure required | Filed with the Registrar General's Department |

Focus Points

- Taxation: Subject to corporate income tax at 25% (standard rate); VAT registration required once annual turnover exceeds the statutory threshold; withholding tax applies to dividends, interest, and service fees at rates ranging from 8% to 20% depending on residency and transaction type.

- Annual Compliance: Annual returns must be filed with the Registrar General's Department; audited financial statements required for most private companies under Act 992.

- Foreign Ownership: Foreign nationals may hold shares, but businesses in certain reserved sectors are restricted to Ghanaian citizens under the Ghana Investment Promotion Centre Act, 2013 (Act 865) and the Ghana Enterprise Development Commission Act.

- Conversion: A private limited company may be re-registered as a public limited company by special resolution and compliance with the additional requirements under Act 992.

- Treaty Access: Ghana has signed double taxation agreements with several countries; treaty benefits are accessible to tax-resident companies incorporated locally.

Closing

A private limited company suits trading operations, foreign subsidiaries, joint ventures, and holding structures requiring clear liability separation. The restricted share transfer mechanism offers ownership control, though the 50-shareholder cap limits equity fundraising from the public.

Foreign investors and local entrepreneurs seeking a formally structured, liability-protected entity for commercial operations with controlled ownership.

Company Limited by Guarantee

A company limited by guarantee Ghana represents a distinct corporate form governed by the Companies Act, 2019 (Act 992). Unlike share-based companies, this entity has no share capital; members commit to contributing a fixed amount toward the company's debts upon winding up, rather than purchasing equity. The structure carries separate legal personality, meaning it can sue, hold assets, and enter contracts in its own name.

Registered under the Registrar General's Department, this entity is typically formed for non-profit purposes such as professional associations, charities, educational bodies, and regulatory organisations. Surplus income is applied toward stated objectives rather than distributed to members.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company Limited by Guarantee (CLG) | Incorporated under Act 992; separate legal personality |

| Members | Minimum 1; no maximum | Members provide a guarantee amount, not share capital |

| Directors | Minimum 2 | At least one must be resident in Ghana |

| Registered Office | Physical address in Ghana required | Must be maintained throughout the company's existence |

| Guarantee Amount | Specified in constitution | Each member's liability capped at their declared guarantee sum |

| Privacy | Constitutive documents publicly filed | Beneficial ownership disclosure required under AML regulations |

Focus Points

- Taxation: Exempt from corporate income tax if registered as a charity or non-profit with the Ghana Revenue Authority; however, commercial activities may attract the standard 25% corporate tax rate, VAT at 15%, and applicable withholding taxes.

- Annual Compliance: Annual returns must be filed with the Registrar General's Department; audited financial statements are required.

- Economic Substance: No formal economic substance regime applies, but operational activities must align with stated non-commercial objectives.

- Conversion: A CLG can be converted to a company limited by shares under Act 992, subject to regulatory approval and constitutional amendment.

- Restrictions: Cannot distribute profits or assets to members during operation or upon dissolution without regulatory scrutiny.

Closing

This structure suits non-governmental organisations, professional bodies, and industry associations that require corporate standing without a profit-distribution mandate. The principal advantage is liability protection for members; the key limitation is the prohibition on profit distribution, which makes this form unsuitable for any revenue-generating venture where investor returns are expected.

A company limited by guarantee is most appropriate for non-profit organisations, trade associations, and foundations requiring legal personality without share capital.

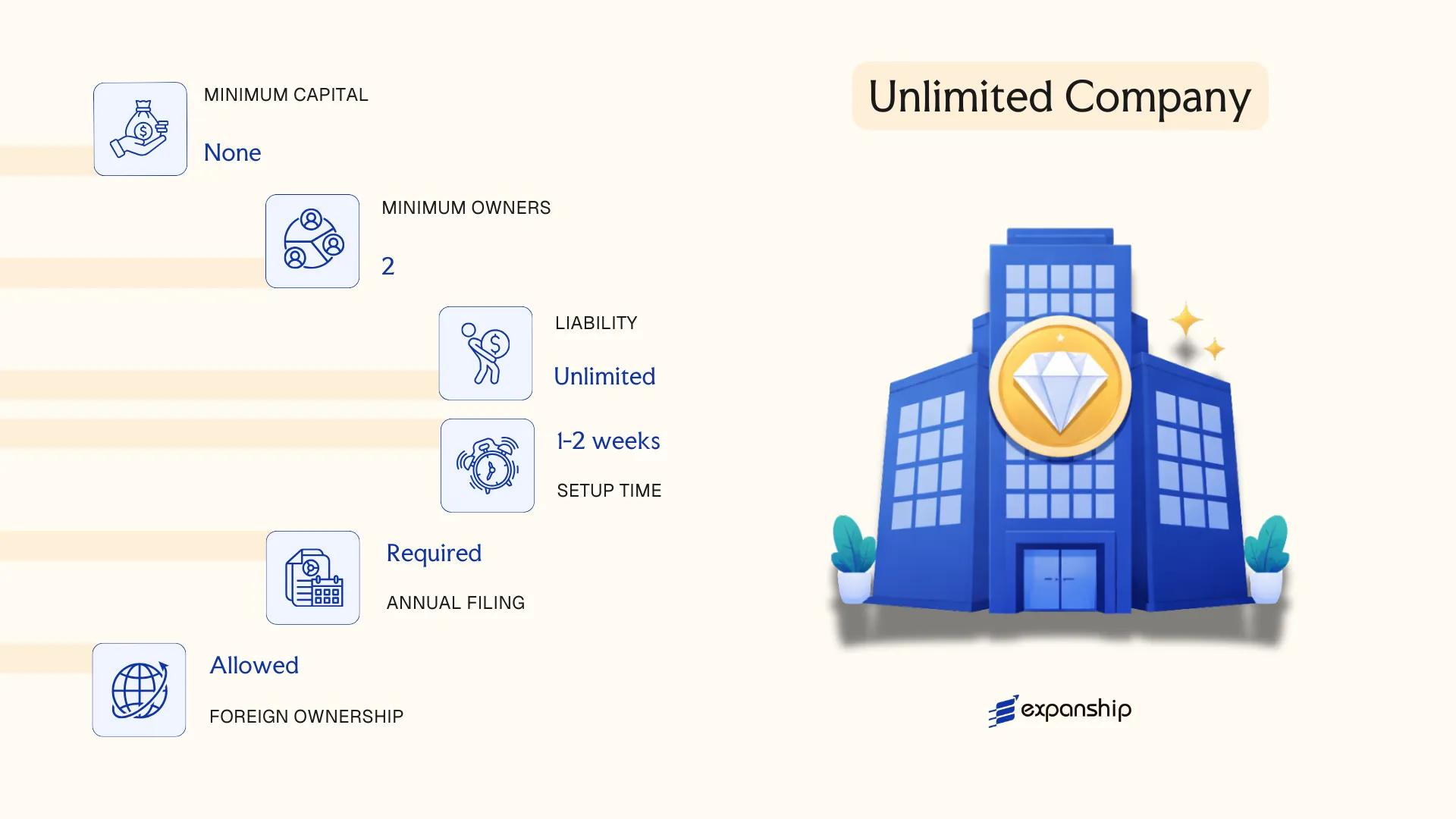

Unlimited Company

Unlimited company registration in Ghana is governed by the Companies Act, 2019 (Act 992), which formally recognises this structure as a distinct legal form. Unlike the more common limited liability variants, an unlimited company does not cap members' liability — shareholders remain personally liable for the debts and obligations of the entity without restriction.

Separate legal personality is retained, meaning the firm exists independently of its members and can own property, enter contracts, and sue or be sued in its own name. This combination of corporate personality with unlimited personal exposure is uncommon in practice, but Act 992 provides the framework for it.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unlimited Company | Recognised under Act 992; members bear unrestricted personal liability for company debts |

| Members | Minimum 1 member; no statutory maximum | Members may be individuals or corporate bodies |

| Directors | Minimum 1 director | At least one director must be resident in Ghana |

| Registered Office | Must maintain a registered address in Ghana | Required for service of legal notices and official correspondence |

| Share Capital | No statutory minimum; shares may or may not be issued | The entity may be structured with or without share capital |

| Privacy | Financial statements may have reduced disclosure obligations | Act 992 allows unlimited companies certain exemptions from full public filing of accounts |

Focus Points

- Taxation: Subject to the standard corporate income tax rate of 25% under the Income Tax Act, 2015 (Act 896); VAT, withholding tax, and stamp duty obligations apply on the same basis as other resident companies.

- Annual Compliance: Must file annual returns with the Registrar General's Department; reduced financial disclosure obligations may apply relative to public companies.

- Conversion: Act 992 permits conversion between company types, including from unlimited to limited form, subject to prescribed procedures and member approval.

- Treaty Access: As a Ghana-resident entity, access to Ghana's double taxation agreements is available, subject to beneficial ownership and substance requirements.

- Restrictions: Not permitted to offer shares to the general public; unsuitable for businesses seeking external investment through public markets.

Closing

An unlimited company suits closely held businesses where members prefer reduced disclosure requirements and accept full personal liability in exchange. The principal advantage is the potential exemption from public filing of financial statements; the corresponding drawback is that personal assets of all members remain exposed to company creditors without limit.

This structure is most appropriate for private family-held businesses or professional firms that prioritise financial confidentiality over liability protection.

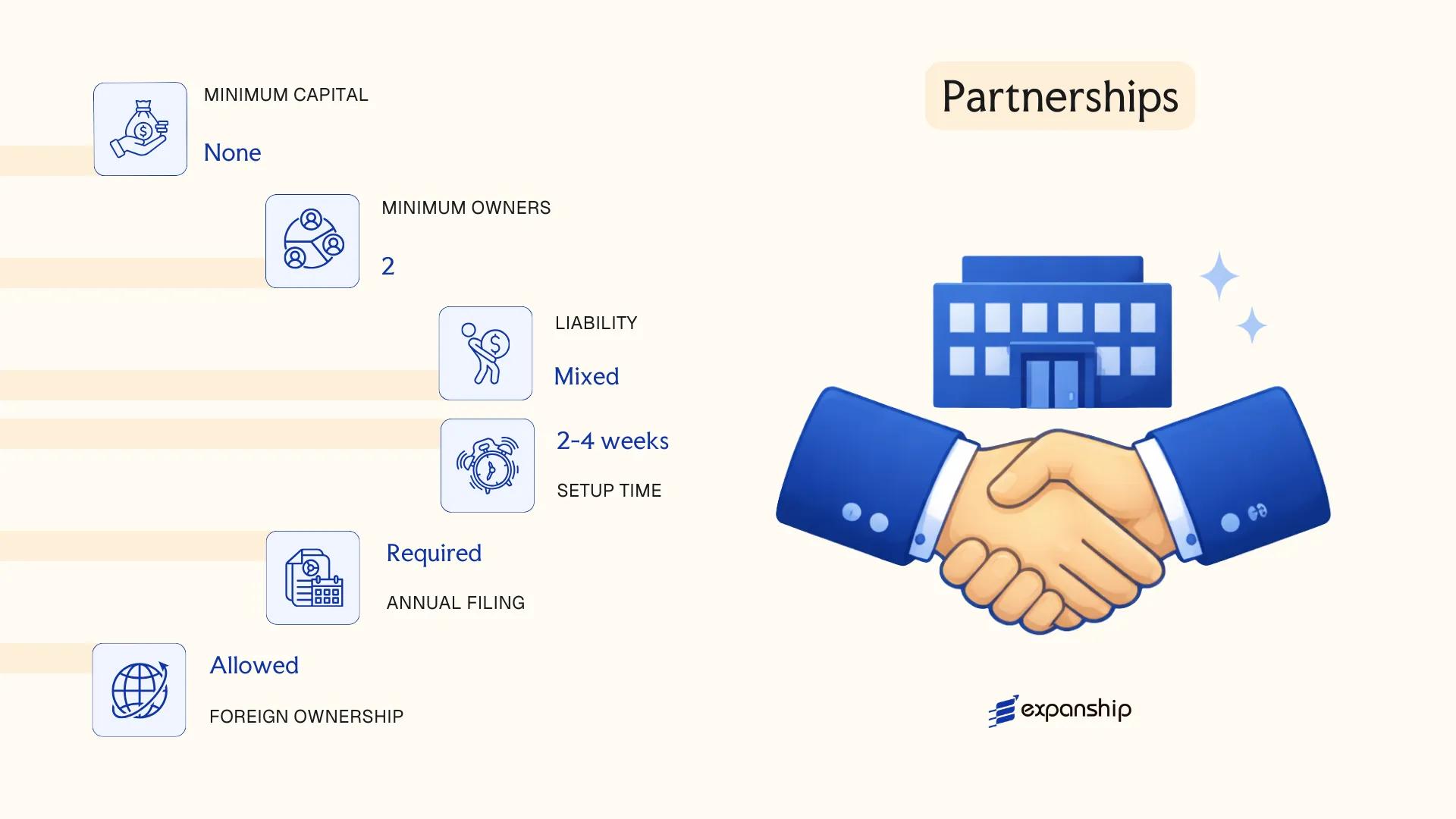

Partnerships [General Partnership, Limited Partnership]

Partnership registration in Ghana is governed by the Incorporated Private Partnerships Act, 1962 (Act 152), which provides the legislative framework for both general and limited partnerships. Unlike a company, a partnership does not possess separate legal personality under Act 152, meaning partners bear direct legal responsibility for the obligations of the firm. The structure suits businesses where personal involvement and shared management are central to operations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business association | No separate legal personality from its partners |

| Members | Partners (minimum 2, maximum 20) | Exceeding 20 requires incorporation as a company |

| Liability | General: unlimited; Limited: mixed | Limited partners' liability is capped at capital contribution |

| Local Presence | Registered business address in Ghana | Required for official correspondence and filing |

| Capital | No statutory minimum; contributions by agreement | Denominated in Ghanaian Cedi (GHS) |

| Registration Body | Registrar General's Department (RGD) | Partnership deed submitted at point of registration |

Focus Points

- Taxation: Partnerships are treated as pass-through entities; profits are taxed at the individual partner level under the Income Tax Act, 2015 (Act 896), with applicable personal income tax rates; VAT registration is required if turnover exceeds the statutory threshold.

- Annual Compliance: Partners must file annual returns with the RGD and maintain proper accounting records.

- Restrictions: Foreign nationals may face ownership restrictions under the Ghana Investment Promotion Centre Act, 2013 (Act 865), particularly in sectors reserved for Ghanaian citizens.

- Conversion: A partnership may be converted to a limited liability company by re-registering under the Companies Act, 2019 (Act 992).

Sub-Types

General Partnership

All partners share equal management authority and carry unlimited personal liability for the debts of the firm. This structure is common among professional service providers such as law firms and accounting practices.

Limited Partnership

At least one general partner retains unlimited liability and management control, while one or more limited partners contribute capital without participating in daily management. Limited partners' liability is confined to their agreed capital contribution, making this form suitable for investment arrangements where passive investors are involved.

Closing

A partnership structure suits small to medium-sized professional or trading businesses where the owners prefer a straightforward setup without the formalities of company incorporation, though the absence of limited liability for general partners exposes personal assets to business risk.

Partnerships in Ghana are most appropriate for small professional firms or joint ventures between known parties who require a low-cost, operationally simple structure with shared management.

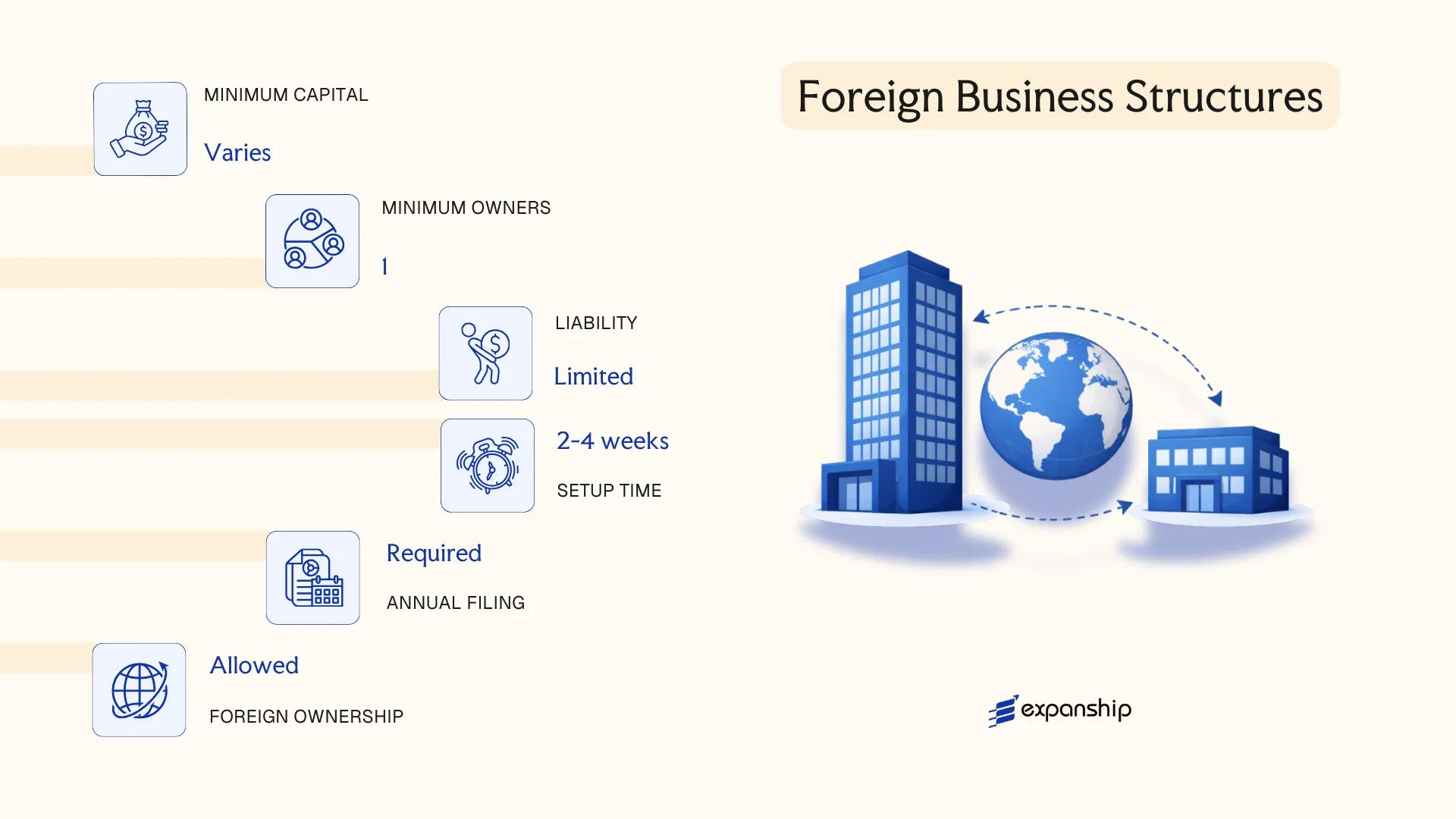

Foreign Business Structures [Branch Office, Representative Office, Subsidiary]

A foreign company branch office in Ghana must be registered with the Registrar General's Department under the Companies Act, 2019 (Act 992) and, in most cases, with the Ghana Investment Promotion Centre (GIPC) under the GIPC Act, 2013 (Act 865). Unlike a subsidiary, a branch has no separate legal personality — it is a direct extension of the parent company, which remains fully liable for its obligations.

Registration requirements vary by structure. A subsidiary is incorporated as a distinct Ghanaian entity, typically as a private limited company, and carries liability independent of the foreign parent.

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary |

|---|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality | Separate legal entity incorporated under Act 992 |

| Governing Members | Directors of parent company | Designated resident representative | Directors and shareholders |

| Local Presence | Registered office address in Ghana required | Registered office address required | Registered office address required |

| Minimum Capital | USD 500,000 (foreign-owned trading entity per GIPC Act) | Not applicable — no commercial activity permitted | USD 200,000 (joint venture) or USD 500,000 (wholly foreign-owned, per GIPC Act) |

| Liability | Parent bears full liability | Parent bears full liability | Limited to subsidiary's own assets |

| Privacy | Parent company details are publicly disclosed on registration | Parent company details disclosed | Shareholder and director details filed with Registrar |

Focus Points

- Taxation: Branch profits are subject to the standard corporate income tax rate of 25%; a 10% branch profits remittance tax applies on after-tax profits sent to the parent. Subsidiaries are taxed as resident entities at 25% corporate tax, with VAT at 15% (plus applicable levies) and withholding taxes on dividends, interest, and royalties applying to both structures.

- GIPC Compliance: Most foreign-owned entities must register with the GIPC and meet sector-specific local equity requirements; certain sectors are wholly reserved for Ghanaians.

- Annual Compliance: Both branches and subsidiaries must file annual returns with the Registrar General's Department and maintain audited financial statements.

- Employment: Foreign entities must meet GIPC-mandated minimum local employment thresholds; at least one Ghana-citizen employee is required at the entry level.

- Conversion: A branch may not automatically convert to a subsidiary; a new incorporation process is required.

Sub-Types

Branch Office

A branch conducts revenue-generating commercial activity on behalf of the foreign parent. It cannot hold assets in its own name and is not a separate taxpayer from the parent for liability purposes, though it files tax returns independently in Ghana.

Representative Office

A representative office is restricted to non-commercial functions such as market research, liaison, and promotional activities. It cannot enter into contracts or generate local revenue, making it unsuitable for active trading operations.

Subsidiary

Incorporated as a Ghanaian company under Act 992, the subsidiary is the only foreign business structure that achieves full legal and financial separation from the parent. It qualifies as a resident entity for tax treaty purposes and can access Ghana's network of Double Taxation Agreements.

Closing

Foreign subsidiaries are the preferred structure for long-term market entry involving significant local operations, while branches suit firms seeking a lighter administrative footprint with direct parent control. The primary limitation of a branch is the parent's unlimited exposure to Ghanaian liabilities.

Foreign subsidiaries are best suited for multinationals committing to sustained commercial activity in Ghana who require liability separation and treaty access; branches work for firms testing the market under direct parent oversight.

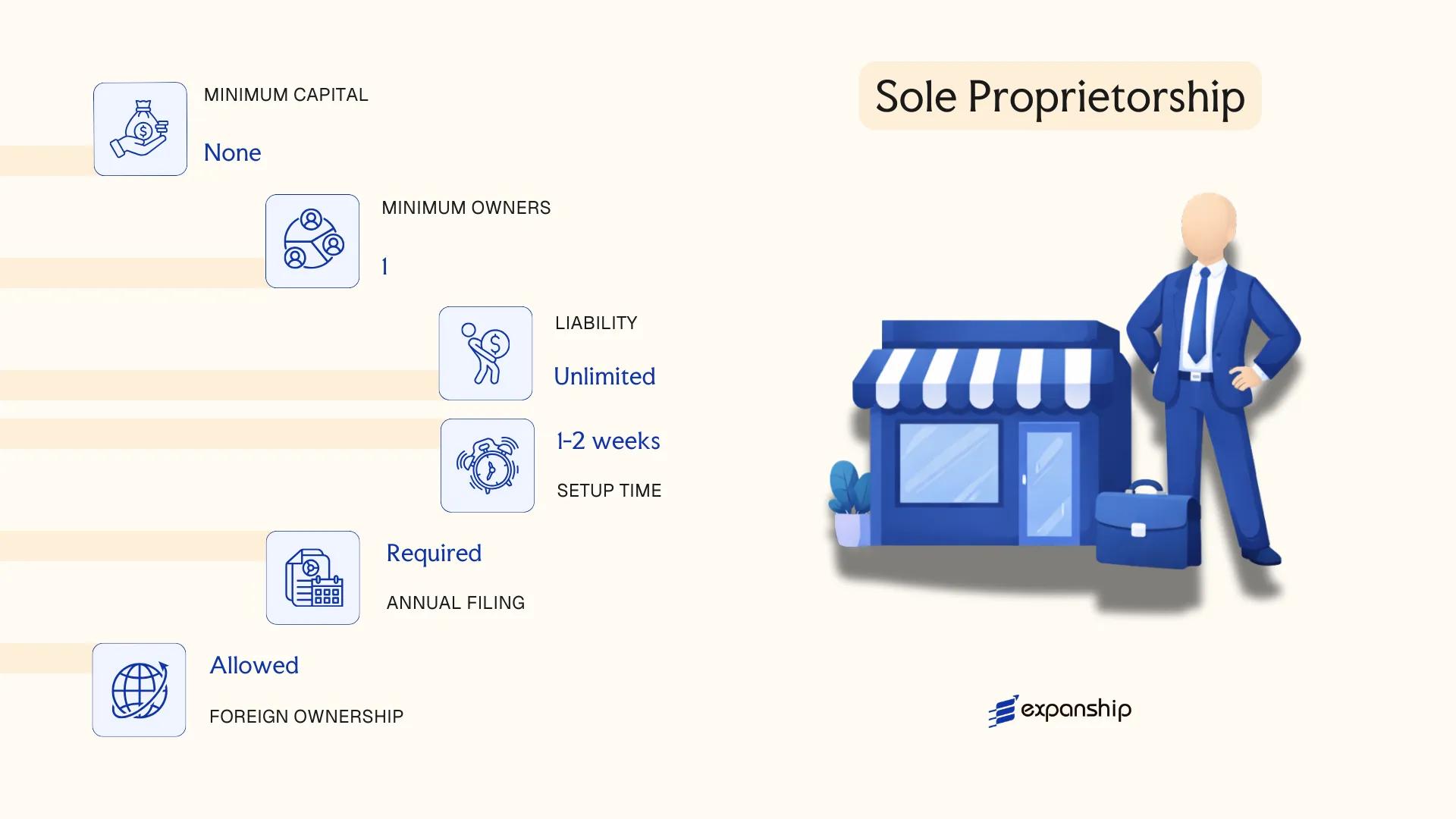

Sole Proprietorship

Sole proprietorship registration in Ghana is governed by the Registration of Business Names Act, 1962 (Act 151), which requires any individual trading under a business name to register with the Registrar-General's Department (RGD). Unlike a limited company, this structure confers no separate legal personality — the business and its owner are legally indistinguishable.

Because no liability shield exists, the proprietor bears unlimited personal responsibility for all debts and obligations incurred by the business. Registration is relatively straightforward, and the RGD issues a Certificate of Registration upon successful filing.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Members | One individual proprietor | Cannot have co-owners; remains solely owned |

| Local Presence | Registered business address required | Must maintain a physical or postal address in Ghana |

| Capital | No statutory minimum | Funded entirely by the proprietor |

| Privacy | Business name and owner details on public register | Filed with the RGD and accessible publicly |

| Registration Body | Registrar-General's Department | Registration under Act 151 |

Focus Points

- Taxation: Subject to personal income tax under the Income Tax Act, 2015 (Act 896) at progressive rates up to 35%; VAT registration required if annual turnover exceeds the prescribed threshold; withholding tax applies on certain payments received.

- Annual Compliance: Business name registration must be renewed periodically with the RGD; no audited accounts requirement.

- Treaty Access: No access to double taxation treaties, which apply to corporate entities only.

- Conversion: Can be converted to a limited liability company by incorporating a new entity and transferring assets; no direct statutory conversion mechanism.

- Restrictions: Foreign nationals face restrictions on operating sole proprietorships in sectors reserved for Ghanaian citizens under the Ghana Investment Promotion Centre Act, 2013 (Act 865).

Recommendations

A sole proprietorship suits small-scale, locally owned businesses where administrative simplicity outweighs the need for liability protection — common among traders, artisans, and individual service providers. The absence of incorporation requirements reduces setup costs, but unlimited personal liability remains a significant structural drawback for any business carrying financial or operational risk.

This structure is most appropriate for Ghanaian nationals running low-risk, owner-operated micro or small businesses with no plans for external investment.

How to Choose the Right Entity Type in Ghana

Selecting the correct legal structure at the outset determines your tax exposure, liability, and regulatory obligations — and getting it wrong creates concrete problems that are costly to unwind.

Why Your Entity Choice Matters

The Companies Act, 2019 (Act 992) governs company formation and imposes distinct requirements depending on the structure you register. Choosing the wrong one carries real consequences:

- Registering a structure intended for passive holding when you intend to trade actively with Ghanaian residents may result in non-compliance with the Registrar General's Department requirements, exposing your business to penalties or administrative striking off.

- Selecting an entity without the capacity to support local substance — employees, a registered office, resident management — can trigger reporting failures under applicable tax rules administered by the Ghana Revenue Authority.

- Forming a private limited company when your objectives are purely non-commercial or charitable locks you into annual shareholder obligations, filing requirements, and audit thresholds that a company limited by guarantee avoids.

- Choosing a structure that mandates audited financial statements for a single-person consultancy adds annual compliance costs that a sole proprietorship registration does not require.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or insurance each point to a structurally distinct entity under Ghanaian law.

- Ownership and Management: Single-owner operations suit a sole proprietorship or private limited company, while multi-party arrangements may require a partnership deed or a formal board structure.

- Tax Objectives: Your need for treaty access, sector-specific incentives under the Ghana Revenue Authority's administered regimes, or full exemption will narrow your structural options significantly.

- Liability Exposure: The degree to which you need to separate personal assets from business liabilities should directly inform whether an incorporated or unincorporated structure is appropriate.

- Exit and Conversion: Not all structures permit redomiciliation or conversion — confirm whether your chosen entity type supports your long-term exit or restructuring plans before registering.

Corporate Compliance Services in Ghana

Maintain good standing with the Registrar General's Department and Ghana Revenue Authority — annual filings, statutory updates, and ongoing compliance management.

Conclusion

Incorporating a company in Ghana requires choosing from a well-defined set of structures, each governed primarily by the Companies Act, 2019 (Act 992) or, for unincorporated arrangements, the Incorporated Private Partnerships Act, 1962 (Act 152). The Private Limited Company remains the most registered entity form, favored by resident and foreign investors alike for its liability protection and straightforward compliance obligations. A Public Limited Company suits businesses seeking public capital; a Company Limited by Guarantee serves non-profit purposes; an Unlimited Company fits situations where full liability is acceptable. Branch and representative offices address foreign entities testing or operating in-country without separate incorporation. Sole proprietorships and partnerships remain accessible entry points for smaller-scale operations.

Registered with the Registrar General's Department, each structure carries distinct obligations. Ghana's continued expansion of its double taxation treaty network and its ongoing Companies Act implementation signal a maturing regulatory environment. Expanship's team works directly within this framework to support your registration process from start to finish.

How Expanship Can Assist You

Expanship Ghana company incorporation services cover the full process of registering a business with the Registrar General's Department — from selecting the right entity type under the Companies Act, 2019 (Act 992) to meeting the post-incorporation obligations that apply to your specific structure.

From the outset, your Expanship team handles the practical work so your attention stays on building the business itself:

- Preparation and legalization of incorporation documents

- Registered office and resident agent provision

- Filing and liaison with the Registrar General's Department

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance for newly incorporated entities

Ghana business setup assistance through Expanship is built around your entity type, whether that is a private limited company, a branch office, or any other structure discussed above.

Reach out directly to discuss your situation: Expanship Ghana

Frequently Asked Questions (FAQ)

The Private Limited Company (Ltd) is the most frequently incorporated structure under Act 992. Its liability protection, relatively low minimum share capital, and permission to have a sole director and shareholder make it accessible for both resident and foreign entrepreneurs.

A Branch Office is an extension of the foreign parent and carries no separate legal personality, whereas a Private Limited Company is an independent legal entity. Both must register with the Registrar General's Department, but the Branch's tax obligations in Ghana are tied to the activities it conducts locally, while the Ltd is taxed on its own income. Compliance requirements for a Branch typically involve additional filings relating to the parent entity.

The Company Limited by Guarantee does not issue shares, so there are no shareholders listed on the public register. Directors remain on file with the Registrar General's Department, but beneficial ownership details are less exposed than in a share-based structure. Nominee arrangements are permissible under Ghanaian law, subject to disclosure requirements.

A sole proprietorship and a Private Limited Company can each be formed by one individual. A General Partnership requires at least two partners, and a Limited Partnership equally demands a minimum of one general and one limited partner. The Public Limited Company requires a minimum of seven shareholders under Act 992.

Foreign individuals and entities may incorporate a Private Limited Company, a Public Limited Company, or establish a Branch or Representative Office. However, businesses with foreign participation must comply with the Ghana Investment Promotion Centre Act, 2013 (Act 865), which sets minimum foreign equity thresholds and restricts certain sectors to Ghanaian nationals exclusively.

Act 992 provides for re-registration, allowing a Private Limited Company to convert to a Public Limited Company and vice versa, subject to meeting the applicable conditions. Conversion between fundamentally different structures, such as from a partnership to a limited company, generally requires dissolving the existing entity and forming a new one. The Registrar General's Department oversees all re-registration procedures.

A Private Limited Company, Public Limited Company, Company Limited by Guarantee, and Unlimited Company all obtain separate legal personality upon incorporation under Act 992. Partnerships and sole proprietorships do not, meaning owners bear personal liability for obligations incurred. This distinction directly affects how creditors may pursue claims against the business.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.