Key Takeaways

- All legal entities in Georgia must register with the National Agency of Public Registry (NAPR) under the Ministry of Justice before commencing commercial activity.

- The LLC (ShPS — Shezghuduli Pasukhmgeblobis Sazogadoeba) is the most commonly registered entity in Georgia, distinguished by minimal capital requirements and administrative simplicity.

- Georgia's territorial tax system means that foreign-sourced income of Georgian-registered entities is generally not subject to local taxation, a feature reinforced by the country's expanding tax treaty network.

- Foreign businesses may establish a Branch Office or Representative Office in Georgia without forming a separate legal entity, operating instead as an extension of the parent company under the Law of Georgia on Entrepreneurs.

Introduction to Entity Types in Georgia (GE)

Located in the South Caucasus, Georgia borders Russia to the north, Turkey and Armenia to the south, and Azerbaijan to the east, with the Black Sea forming its western boundary. It is an independent republic and a member of the United Nations, the Council of Europe, and the World Trade Organization.

Company registration and ongoing compliance fall under the authority of the National Agency of Public Registry (NAPR), which operates under the Ministry of Justice. All legal entities must register with the NAPR before commencing commercial activity.

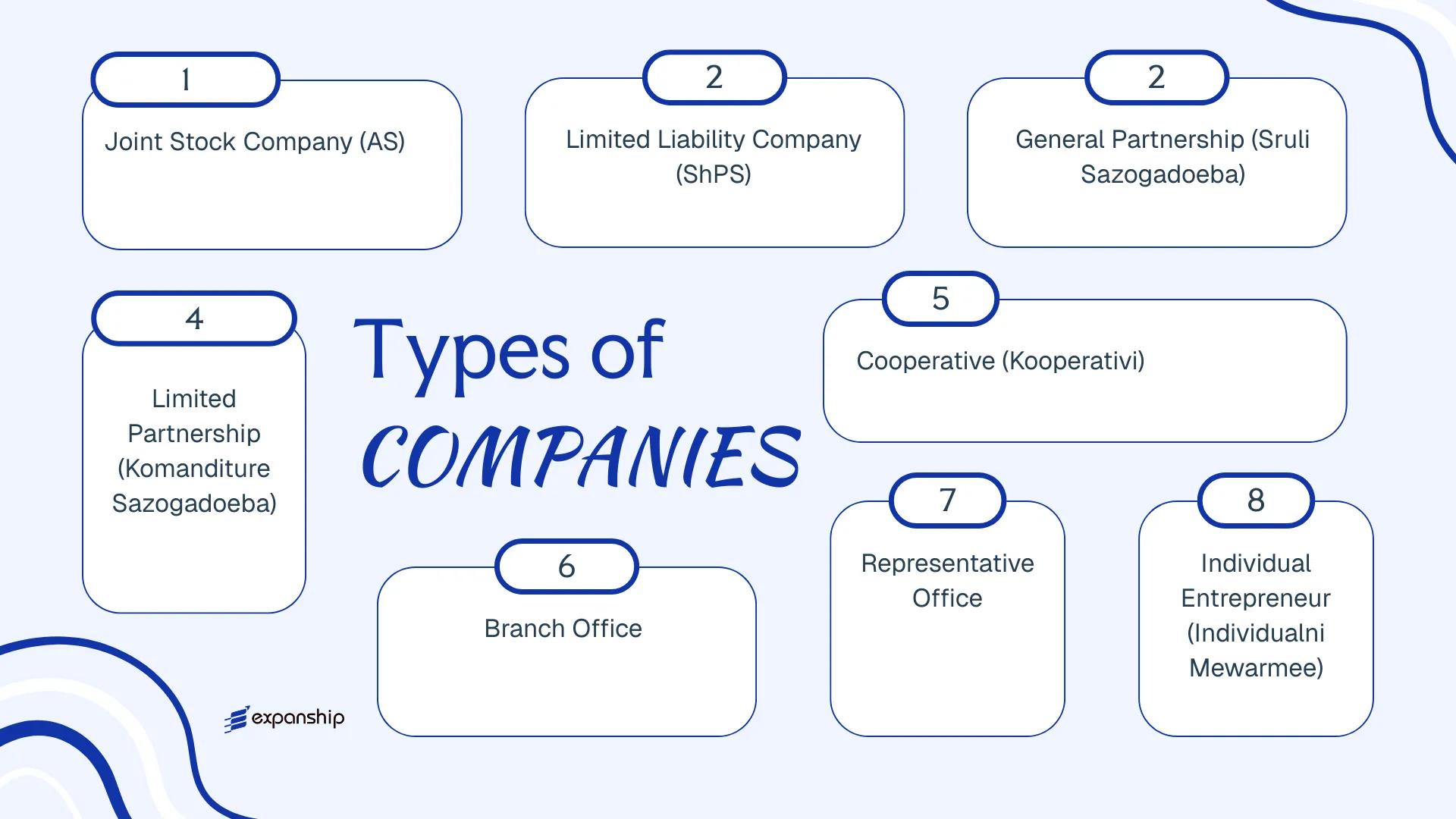

Georgia operates a territorial tax system, meaning that foreign-sourced income of Georgian-registered entities is generally not subject to local taxation. The types of business entities in Georgia available under the Law of Georgia on Entrepreneurs include the Joint Stock Company, the Limited Liability Company, the General Partnership, the Limited Partnership, the Cooperative, and the Individual Entrepreneur. Foreign businesses may also establish a Branch Office or Representative Office without forming a separate legal entity.

Each of these Georgian legal entity structures carries distinct implications for liability, governance, minimum capital, and tax treatment — all of which this article examines in turn.

An Overview of Business Structures in Georgia (GE)

Georgian company law recognises six principal business structures in Georgia country, each governed primarily by the Law of Georgia on Entrepreneurs (consolidated and significantly amended in 2021). These structures range from sole trader arrangements to capital-based corporate forms, and each is designed to serve a distinct commercial function.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Joint Stock Company (AS) | Corporate | Limited to shares | Standard CIT applies | Permitted | 1 shareholder | National Agency of Public Registry | Law on Entrepreneurs |

| Limited Liability Company (ShPS) | Corporate | Limited to contribution | Standard CIT applies | Permitted | 1 member | National Agency of Public Registry | Law on Entrepreneurs |

| General Partnership (Sruli Sazogadoeba) | Partnership | Unlimited, joint | Standard CIT applies | Permitted | 2 partners | National Agency of Public Registry | Law on Entrepreneurs |

| Limited Partnership (Komanditure Sazogadoeba) | Partnership | Mixed (general/limited) | Standard CIT applies | Permitted | 2 partners | National Agency of Public Registry | Law on Entrepreneurs |

| Cooperative (Kooperativi) | Cooperative | Limited | Standard CIT applies | Permitted | 2 members | National Agency of Public Registry | Law on Cooperatives |

| Branch Office | Non-legal entity | Parent liable | Standard CIT applies | Permitted | N/A (parent company) | National Agency of Public Registry | Law on Entrepreneurs |

| Representative Office | Non-legal entity | Parent liable | Generally non-trading | Restricted | N/A (parent company) | National Agency of Public Registry | Law on Entrepreneurs |

| Individual Entrepreneur (Individualni Mewarmee) | Sole trader | Unlimited personal | Tiered / turnover-based | Permitted | 1 individual | Revenue Service of Georgia | Tax Code of Georgia |

Each of these structures is examined in full in the sections below.

Joint Stock Company (JSC) — Akcioneruli Sazogadoeba (AS)

Governed by the Law of Georgia on Entrepreneurs (2021), the Joint Stock Company Georgia AS registration framework establishes a corporate structure with full separate legal personality and shareholder liability capped at each member's subscribed capital contribution. The entity is suited to capital-intensive operations, institutional investors, and businesses intending to issue publicly traded or privately held shares.

Akcioneruli Sazogadoeba formation produces a hybrid structure: equity is divided into transferable shares, yet the entity retains the governance depth of a classical corporation, including a mandatory supervisory board under certain thresholds.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (AS) | Separate legal personality; shareholders not liable beyond subscribed capital |

| Governing Members | Shareholders, Board of Directors, Supervisory Board | Supervisory board mandatory if shareholder count or assets exceed statutory thresholds |

| Members | Min. 1 shareholder (natural or legal person); no maximum | Single-shareholder JSC is permissible |

| Local Presence | Registered legal address in Georgia required | No mandatory local director requirement under current law |

| Share Capital | Minimum GEL 100,000 for public JSCs; private JSCs have no statutory minimum under general rules | Shares must be registered; bearer shares are not permitted |

| Privacy | Shareholder data filed with the National Agency of Public Registry (NAPR) | Beneficial ownership disclosure required under AML regulations |

Focus Points

- Taxation: Corporate income tax applies at 15% on distributed profits under Georgia's Estonian-model CIT; VAT at 18% applies to taxable supplies; dividends paid to non-residents are subject to 5% withholding tax; no stamp duty on share issuance.

- Annual Compliance: Financial statements must be prepared; audit is mandatory for entities meeting size criteria under the Law on Accounting, Reporting, and Auditing (2016).

- Treaty Access: Georgia has concluded 60+ double tax treaties; a JSC structured with genuine economic substance may access treaty-reduced withholding rates.

- Conversion: An AS may be reorganised into an LLC (ShPS) or other entity form through a statutory merger, division, or transformation procedure under the Law on Entrepreneurs.

- Restrictions: Public JSCs intending to offer shares to the public must register with and comply with the National Bank of Georgia as the securities regulator.

Closing

A JSC is commonly used for large trading operations, holding structures, and businesses seeking future capital raises through share issuance. The transferable share structure supports investor entry and exit, though the supervisory board requirement and mandatory audit for qualifying entities add governance overhead compared to lighter corporate forms.

A JSC is most appropriate for businesses anticipating external investment, multiple shareholders, or eventual public listings on the Georgian Stock Exchange.

Company Incorporation in Georgia

Incorporate a Joint Stock Company or other entity type in Georgia with end-to-end support from registration through to compliance setup.

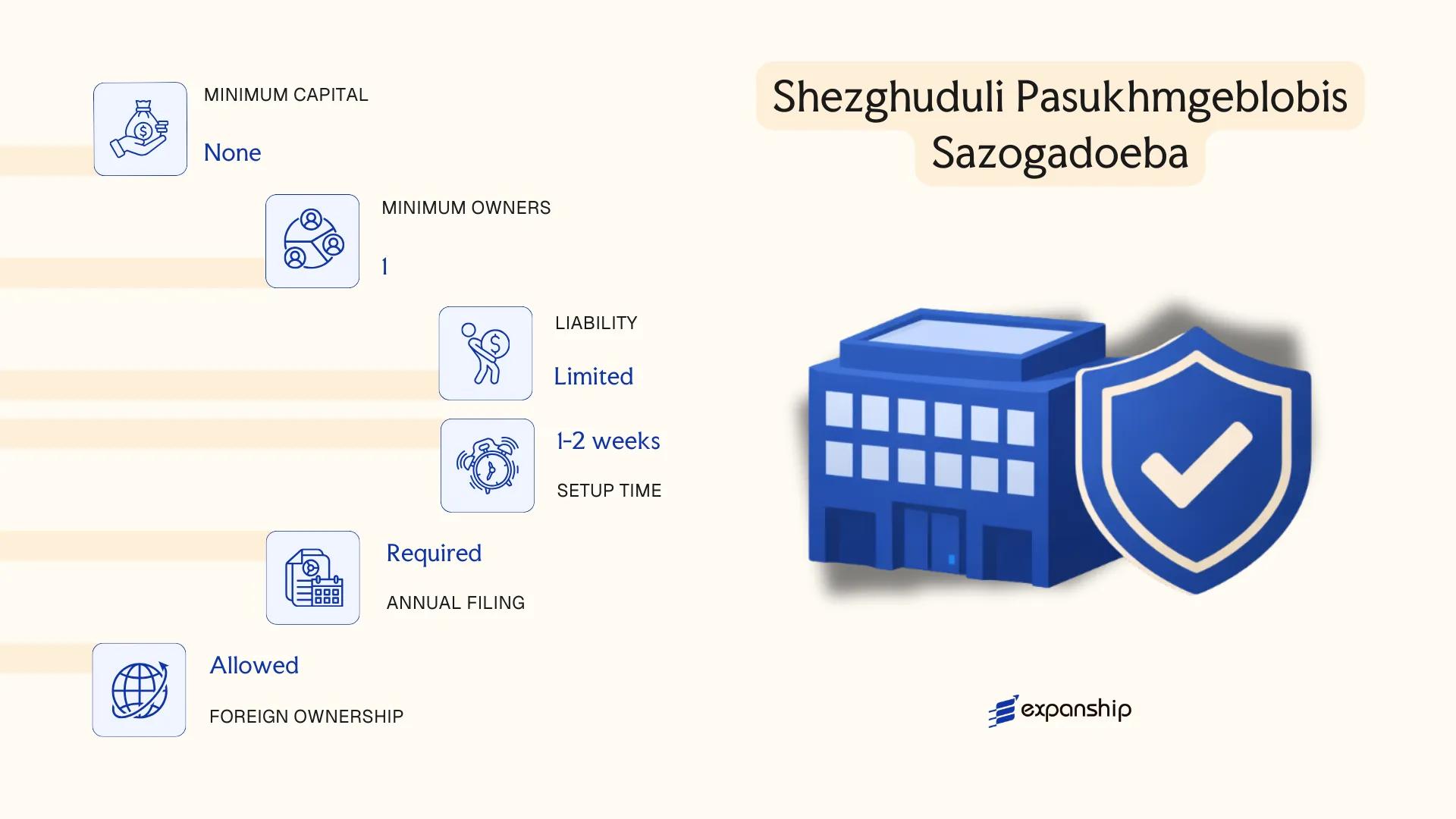

Limited Liability Company (LLC) — Shezghuduli Pasukhmgeblobis Sazogadoeba (ShPS)

Governed by the Law of Georgia on Entrepreneurs (2021), the ShPS is the most widely used commercial structure for LLC formation in Georgia. It carries separate legal personality, meaning the entity's obligations are distinct from those of its members.

Liability is capped at each member's contribution to the charter capital. This hybrid character, combining partnership-style flexibility in internal governance with corporate liability protection, makes the ShPS suitable for a broad range of commercial purposes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (ShPS) | Separate legal personality; governed by the 2021 Law on Entrepreneurs |

| Members | Partners referred to as members; minimum 1, no statutory maximum | A single-member ShPS is permitted |

| Directors | At least 1 director (managing partner); no residency requirement | Director details are publicly registered |

| Local Presence | Registered legal address in Georgia required | No mandatory resident agent under the 2021 law, but a local address must be on file with the National Agency of Public Registry (NAPR) |

| Charter Capital | No statutory minimum; denominated in Georgian Lari (GEL) | Contributions may be cash or in-kind assets |

| Privacy | Member and director details are publicly accessible via NAPR | No bearer interests permitted |

Focus Points

- Taxation: Subject to 15% corporate income tax on distributed profits (Estonian model); standard VAT rate of 18% applies above the GEL 100,000 registration threshold; withholding tax of 5% applies to dividends paid to non-residents.

- Annual Compliance: Financial statements must be prepared; audit obligations depend on entity size classification under Georgian accounting law.

- Treaty Access: Georgia's tax treaty network may reduce withholding tax rates for qualifying non-resident members.

- Conversion: An ShPS may be reorganised into a Joint Stock Company (AS) through a formal restructuring procedure under the 2021 Law on Entrepreneurs.

Closing

The ShPS suits trading operations, holding structures, and service businesses where members require liability protection without the administrative burden of a public company. Its primary constraint is that member information remains publicly accessible through NAPR, limiting structural privacy.

Best suited for foreign investors and small-to-medium enterprises seeking a flexible, cost-efficient operating entity with full liability separation and no minimum capital requirement.

Partnerships in Georgia [General Partnership (Sruli Sazogadoeba), Limited Partnership (Komanditure Sazogadoeba)]

Under the Law of Georgia on Entrepreneurs (2021), partnerships are recognised as distinct legal entities with separate legal personality from their members. Both the general partnership Georgia Sruli Sazogadoeba and the Komanditure Sazogadoeba limited partnership Georgia carry unlimited liability for at least one category of partner, which differentiates them structurally from capital companies such as the LLC or JSC.

Partnerships are registered through the National Agency of Public Registry (NAPR), the same body that oversees all commercial entity registrations in the country. The register partnership company Georgia process requires submission of a partnership agreement, partner identification documents, and a registered address.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Separate legal entity | Distinct from its partners under the 2021 Law on Entrepreneurs |

| Members | General Partnership: min. 2 general partners, no maximum. Limited Partnership: min. 1 general partner + min. 1 limited partner | General partners bear unlimited liability; limited partners liable only to the extent of their contribution |

| Local Presence | Registered legal address in Georgia required | No mandatory local director or resident agent requirement under general rules |

| Capital | No statutory minimum capital; contributions defined in the partnership agreement | Contributions may be monetary or in-kind |

| Privacy | Partner details filed with NAPR and publicly accessible | No nominee partner framework exists |

Focus Points

- Taxation: Partnerships are subject to Georgia's Estonian-model CIT (15% on distributed profit); VAT applies at 18% on taxable turnover above GEL 100,000; no withholding tax on profit distributions to Georgian-resident partners under standard rules.

- Annual Compliance: Annual financial statements must be filed; audit requirements depend on the entity's classification under Georgian accounting law.

- Treaty Access: Georgia has an active double tax treaty network; partnership treaty access depends on how the counterpart jurisdiction classifies the entity for tax purposes.

- Restrictions: General partners in both structures bear unlimited personal liability for the entity's obligations, which limits the Georgian partnership business structure's appeal for high-risk commercial activities.

Sub-Types

General Partnership (Sruli Sazogadoeba)

All partners hold equal management rights and bear joint and unlimited liability for the firm's debts, unless the partnership agreement restricts management to designated partners.

Limited Partnership (Komanditure Sazogadoeba)

Limited partners contribute capital but are excluded from management and hold liability capped at their contribution amount; only general partners retain unlimited liability and management authority.

Closing Paragraph

Partnerships suit professional service arrangements, family-held businesses, or joint ventures where partners accept personal liability in exchange for structural simplicity. The absence of minimum capital is an advantage, but unlimited liability for general partners remains a significant constraint.

Partnerships are best suited for closely-held businesses or professional firms where all principals are actively involved and accept personal liability exposure.

Cooperative — Kooperativi

A cooperative company in Georgia (Kooperativi) is governed by the Law of Georgia on Cooperatives, which establishes it as a distinct legal entity with separate legal personality from its members. Liability is generally limited to each member's contribution, giving it a hybrid character that sits between a capital company and a membership organisation.

Registered as a cooperative business structure in Georgia, the entity operates on the principle of mutual benefit rather than capital return, meaning surplus distribution follows member activity rather than ownership share.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative (Kooperativi) | Separate legal personality; governed by the Law of Georgia on Cooperatives |

| Members | Referred to as Members; minimum 2 | No statutory maximum; open membership principle applies |

| Governance | General Meeting (supreme body); Board of Directors for management | Supervisory Board required when membership exceeds a statutory threshold |

| Local Presence | Registered legal address in Georgia required | No requirement for a local resident director by default |

| Capital | No fixed statutory minimum capital | Contributions defined in the cooperative's charter |

| Privacy | Member register maintained internally | Not fully public, but founding members appear in registration records |

Focus Points

- Taxation: Subject to standard Georgian corporate income tax at 15% on distributed profit (Estonian-model); VAT applies at 18% if turnover exceeds the registration threshold; no special cooperative tax exemption exists under general rules.

- Annual Compliance: Annual financial statements must be filed; general meeting of members required at least once per year.

- Economic Substance: No specific substance regime targets cooperatives, but actual activity must align with the registered purpose.

- Treaty Access: Access to Georgia's double tax treaties is available, subject to beneficial ownership and residency conditions.

- Restrictions: Cooperatives may not freely transfer membership interests in the manner a shareholder transfers shares; exit is governed by the charter and the Law on Cooperatives.

Closing

The Kooperativi suits agricultural associations, producer groups, and consumer collectives where shared economic activity matters more than investor returns. Its main advantage is democratic governance tied to member participation; its principal limitation is that it is poorly suited to attracting external investment or venture capital.

Best suited for agricultural producers, artisan groups, or community-based enterprises where members jointly own and use the entity's services rather than seeking capital gains.

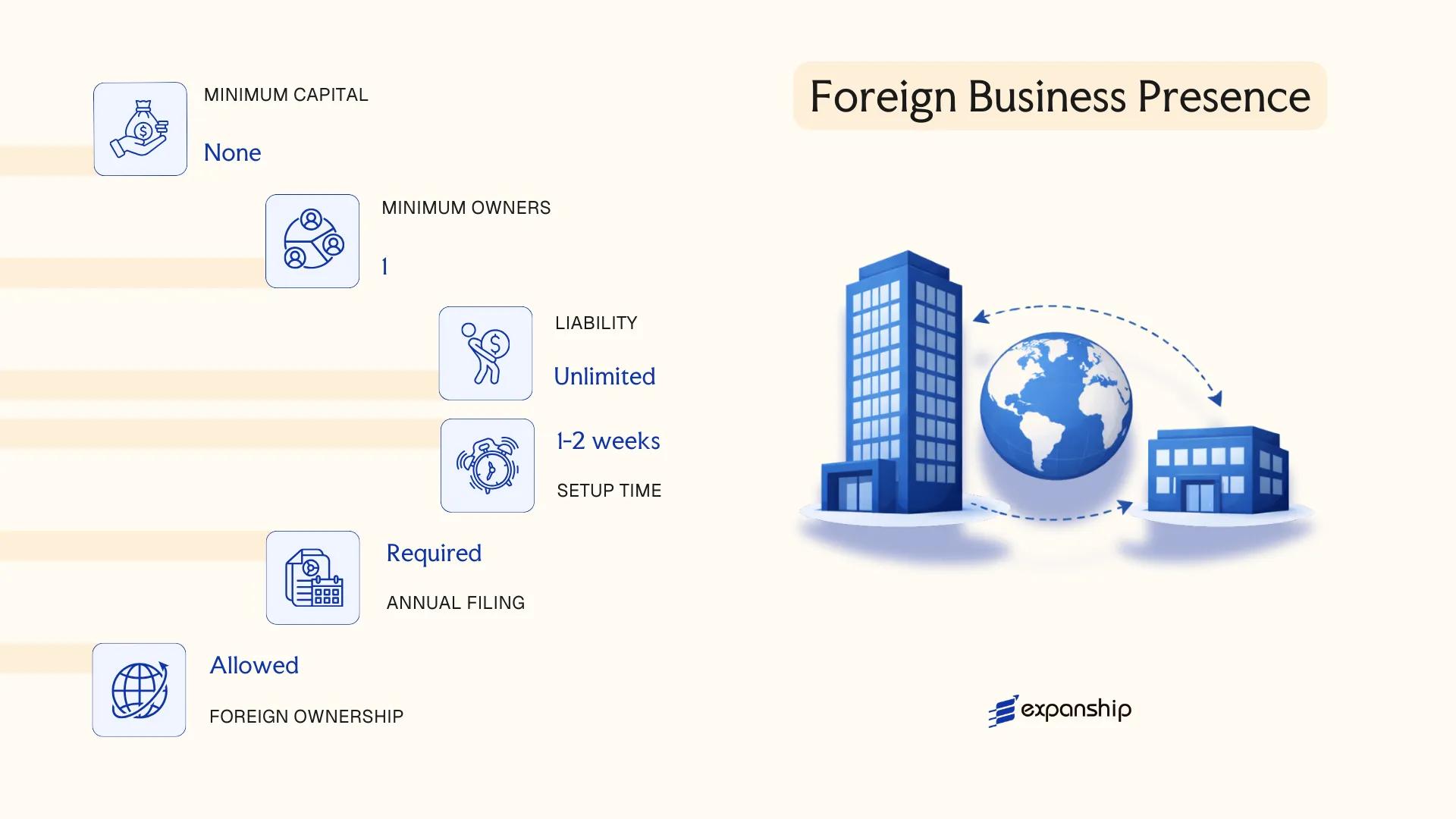

Foreign Business Presence in Georgia [Branch Office, Representative Office]

Foreign companies seeking a physical presence without forming a new local entity can establish either a foreign company branch office Georgia or a representative office. Both forms are governed by the Law of Georgia on Entrepreneurs (2021). Neither structure constitutes a separate legal entity — each operates as an extension of the parent company, which retains full liability for its Georgian operations.

Registration is handled through the National Agency of Public Registry (NAPR). A certified extract from the parent company's home jurisdiction, translated into Georgian and apostilled, is required as part of the application package.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Permitted Activities | Full commercial and trading activities | Non-commercial only (marketing, liaison, research) |

| Head | Director / Authorised Representative | Authorised Representative |

| Local Office | Required registered address in Georgia | Required registered address in Georgia |

| Capital Requirement | None prescribed | None prescribed |

| Registration Body | NAPR | NAPR |

Focus Points

- Taxation: Branch profits are subject to the standard 15% corporate income tax; VAT registration is required if taxable turnover exceeds GEL 100,000 annually; representative offices with no revenue-generating activity generally fall outside corporate tax scope, though specific analysis is advised.

- Economic Substance: No formal substance test is legislated for branches, but the parent's liability exposure makes operational reality relevant.

- Annual Compliance: Both forms must file updates with NAPR upon any change to the parent company's details; branches with taxable activity file returns with the Revenue Service of Georgia.

- Treaty Access: As extensions of the parent, treaty eligibility depends on the parent entity's residence and the applicable double tax agreement between Georgia and the home jurisdiction.

- Restrictions: Representative offices are prohibited from generating revenue directly; conducting commercial transactions through a representative office structure creates compliance and tax exposure risk.

Closing

A branch suits foreign firms that need operational activity in the country without a full subsidiary, while a representative office fits market-entry, liaison, or pre-operational purposes where no direct revenue is anticipated. The primary limitation of both forms is the absence of liability separation from the parent company.

A branch office is best suited for established foreign companies that want direct commercial activity in Georgia without the administrative burden of incorporating a new legal entity.

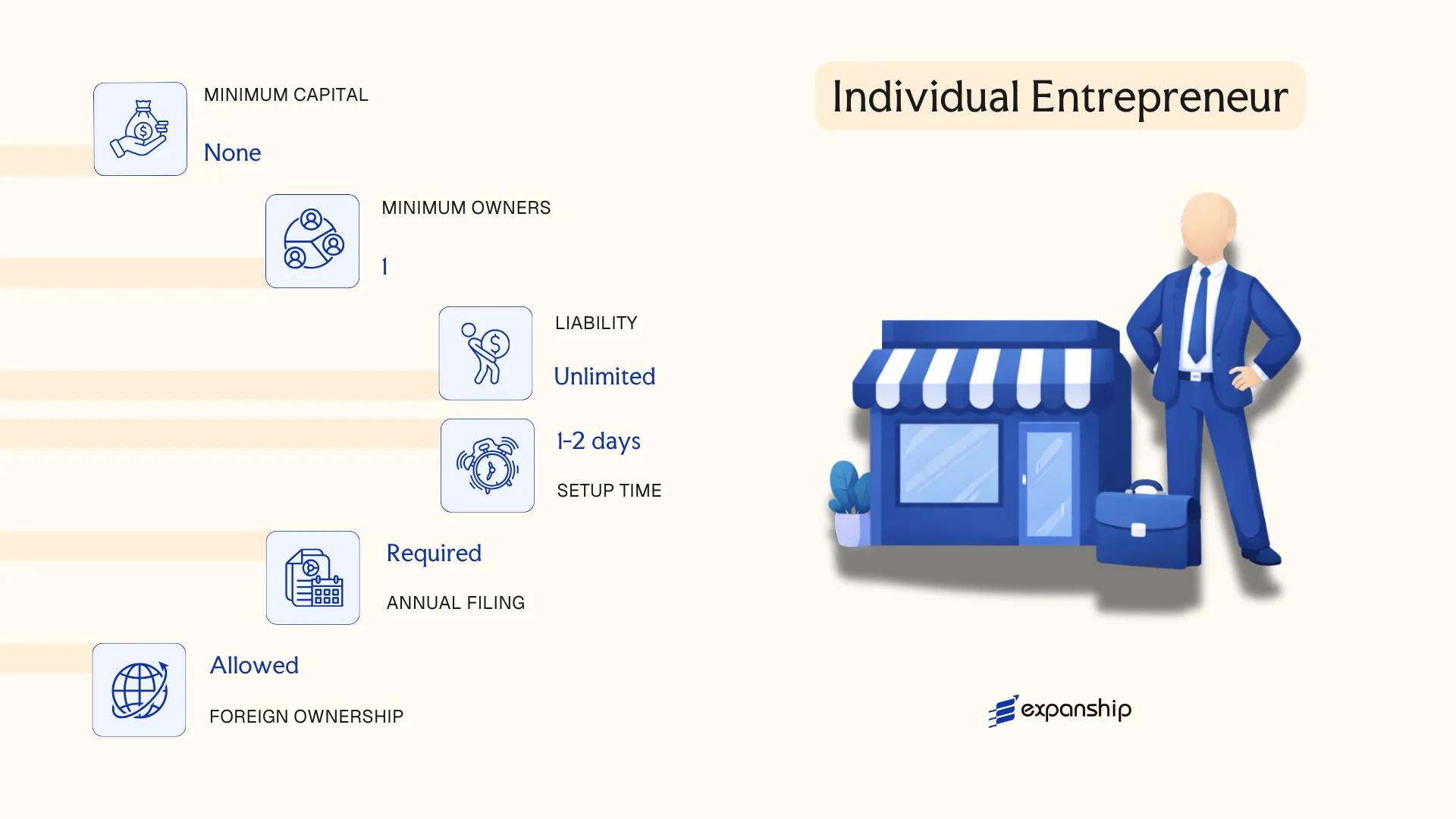

Sole Trader — Individual Entrepreneur (Individualni Mewarmee)

Sole trader registration in Georgia under the designation Individualni Mewarmee is governed by the Law of Georgia on Entrepreneurs (2021), which replaced the earlier 1994 framework and modernised the rules for individual business activity. Unlike capital companies, this structure carries no separate legal personality — the individual and the business are treated as one and the same for both legal and liability purposes.

Registration is conducted through the National Agency of Public Registry (NAPR), which maintains the unified business register. Because the proprietor bears unlimited personal liability, all business debts and obligations are recoverable against personal assets.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Member Type | Sole proprietor | One natural person only; no co-ownership permitted |

| Local Presence | Registered address in Georgia required | Must be maintained with NAPR |

| Capital | No minimum capital requirement | Contributions are informal; no share structure |

| Liability | Unlimited personal liability | Personal assets exposed to business creditors |

| Privacy | Name and registration data publicly accessible via NAPR register | No beneficial ownership concealment |

Focus Points

- Taxation: Subject to personal income tax at progressive rates; VAT registration mandatory once annual turnover exceeds GEL 100,000; small business status available under certain thresholds with a flat 1% rate on turnover.

- Annual Compliance: No statutory audit requirement; annual income declaration filed with the Revenue Service of Georgia.

- Treaty Access: As an unincorporated individual, treaty benefits under Georgia's double tax agreements depend on residency status, not entity classification.

- Conversion: Can be converted into a capital company (typically an LLC) through NAPR without ceasing operations, subject to re-registration.

- Restrictions: Cannot issue shares or admit partners; unsuitable for raising external equity investment.

Closing

This structure suits freelancers, sole traders, and micro-business operators conducting low-risk, low-revenue activity where administrative simplicity outweighs liability exposure. The absence of a minimum capital threshold is a practical advantage, though unlimited personal liability remains a significant constraint for anyone operating in sectors with material financial or legal risk.

Best suited for Georgian residents or tax residents running a one-person service or trading business who qualify for the small business tax regime.

How to Choose the Right Entity Type in Georgia (GE)

Selecting the right entity type is a structural decision that affects your tax position, liability exposure, and regulatory obligations for the life of the business. Understanding how to choose a business entity in Georgia requires more than a general comparison — it requires matching your specific operational profile to what each structure legally permits.

Why Your Entity Choice Matters

The wrong structure creates concrete, legal consequences:

- An Individual Entrepreneur cannot issue equity or bring in shareholders, which blocks growth strategies that require capital raises or investor participation.

- Choosing an entity that triggers mandatory audit requirements under Georgian law when your firm has minimal turnover adds recurring professional costs without regulatory benefit.

- A Representative Office cannot generate revenue or enter commercial contracts; operating commercially through one places you in breach of its registered purpose and risks administrative action by the National Agency of Public Registry.

- If your business qualifies for Georgia's Virtual Zone or International Company status, forming a standard LLC without applying for the relevant status forfeits a 0% corporate tax rate that would otherwise apply.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each fall under different legal and licensing frameworks under the Law of Georgia on Entrepreneurs.

- Ownership and Management: A single-owner consultancy has no structural need for a supervisory board, making an LLC more appropriate than a JSC.

- Tax Objectives: If treaty access or a specific preferential regime is your goal, the entity type and its registration status must both align with the qualifying criteria.

- Liability Exposure: Partnerships in Georgia do not limit personal liability for general partners, which is material if the business carries contractual or operational risk.

- Substance Capacity: If you cannot maintain a physical presence, employees, or local decision-making, certain preferential tax statuses may not be available or sustainable.

- Exit Strategy: JSCs permit share transfers and potential public listings; LLCs offer simpler wind-up procedures but fewer structural options for complex exits.

Compliance Services for Companies in Georgia

Ongoing compliance support for Georgian entities, including annual filings, statutory reporting, and regulatory correspondence with the National Agency of Public Registry.

Conclusion

Incorporating a company in Georgia GE means choosing from a clearly defined set of structures, each suited to a different operational profile. The LLC (ShPS) is the most commonly registered entity, favored for its minimal capital requirements and administrative simplicity. JSCs serve businesses that require share capital structures and broader investor participation. General and limited partnerships carry unlimited or tiered liability and are less common in practice. Cooperatives address member-based economic activity, while individual entrepreneurs suit sole operators with straightforward business models. Branch and representative offices allow foreign entities to establish a presence without forming a separate legal person.

Registered under the Law of Georgia on Entrepreneurs and overseen by the National Agency of Public Registry, the country's corporate framework has been modernized steadily. Georgia's expanding tax treaty network and its virtual zone and free industrial zone regimes continue to attract cross-border business activity, signaling an ongoing trajectory toward greater international integration. Selecting the right structure is best done with jurisdiction-specific legal and tax advice before registration.

How Expanship Can Assist You

Expanship company registration Georgia services are built around the specific requirements of the Georgian legal framework — from selecting between a ShPS and an AS, to satisfying the registration obligations set by the National Agency of Public Registry (NAPR). Every entity type discussed in this blog carries distinct compliance obligations, and your choices at incorporation have lasting consequences.

Expanship handles the full process on your behalf:

- Document preparation and notarization

- Registered agent and legal address provision

- Filing with the National Agency of Public Registry

- Post-incorporation compliance management

- Banking introduction assistance

From initial structuring through to ongoing regulatory obligations, your business has a single point of contact throughout.

Ready to move forward? Reach out to Expanship Georgia to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The Limited Liability Company (ShPS) is the most frequently registered structure. Its combination of limited liability, a single-member option, and comparatively straightforward NAPR registration procedures makes it the default choice for both resident and non-resident founders.

A ShPS suits closely held businesses with fewer compliance burdens, while a JSC (AS) is structured for entities seeking external investment through share issuance. JSCs carry heavier reporting obligations, including audited financial statements, whereas an ShPS may operate with lighter ongoing requirements depending on its size classification.

An ShPS can appoint nominee directors, and beneficial ownership details are not displayed prominently in public NAPR records under standard filings. Shareholder registers are maintained but are not always publicly searchable in the same manner as directorship data.

A ShPS and a JSC can each be formed by one person. Partnerships, by legal definition under the Law on Entrepreneurs, require at least two partners, so an Individual Entrepreneur (Individualni Mewarmee) or single-member ShPS is the only route for a sole founder.

Foreign individuals and legal entities may register a ShPS, JSC, Branch Office, or Representative Office without residency requirements. Georgia imposes no nationality restrictions on company founders or directors, and NAPR accepts applications from non-residents supported by apostilled identification documents.

Reorganisation between entity types is addressed under the Law of Georgia on Entrepreneurs, which permits transformation, merger, and division procedures. A ShPS may be converted to a JSC, subject to NAPR re-registration and updated charter documentation.

A ShPS, JSC, Cooperative, and both partnership forms hold separate legal personality under Georgian law. An Individual Entrepreneur does not — the founder and the business remain the same legal subject, meaning personal assets are exposed to business liabilities without limitation.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.