Key Takeaways

- Gabon's legal entity framework is governed by the OHADA Uniform Acts, providing a regionally harmonized regulatory foundation for all business structures including the SA, SARL, SAS, and partnership forms.

- The Société à Responsabilité Limitée (SARL) is the most commonly registered entity in Gabon, favored by small and medium-sized businesses for its straightforward governance requirements.

- Company formation in Gabon is processed through the Centre de Développement des Entreprises (CDE), which operates as the one-stop shop in coordination with the Tribunal de Commerce and the Direction Générale des Impôts.

- Foreign firms may enter the Gabonese market through a branch or representative office before committing to full incorporation, offering a lower-commitment pathway to establishing a local presence.

Introduction to Entity Types in Gabon

Gabon is a Central African nation bordering Cameroon, Equatorial Guinea, the Republic of the Congo, and the Atlantic Ocean. It is an independent republic and a member of the Economic Community of Central African States (ECCAS). Business registration falls under the jurisdiction of the Centre de Développement des Entreprises (CDE), which operates as the one-stop shop for company formation, working in coordination with the Tribunal de Commerce for commercial registration and the Direction Générale des Impôts for tax enrollment.

The country operates a territorial tax system, meaning resident companies are taxed on Gabon-sourced income, and various rates apply depending on entity type and sector.

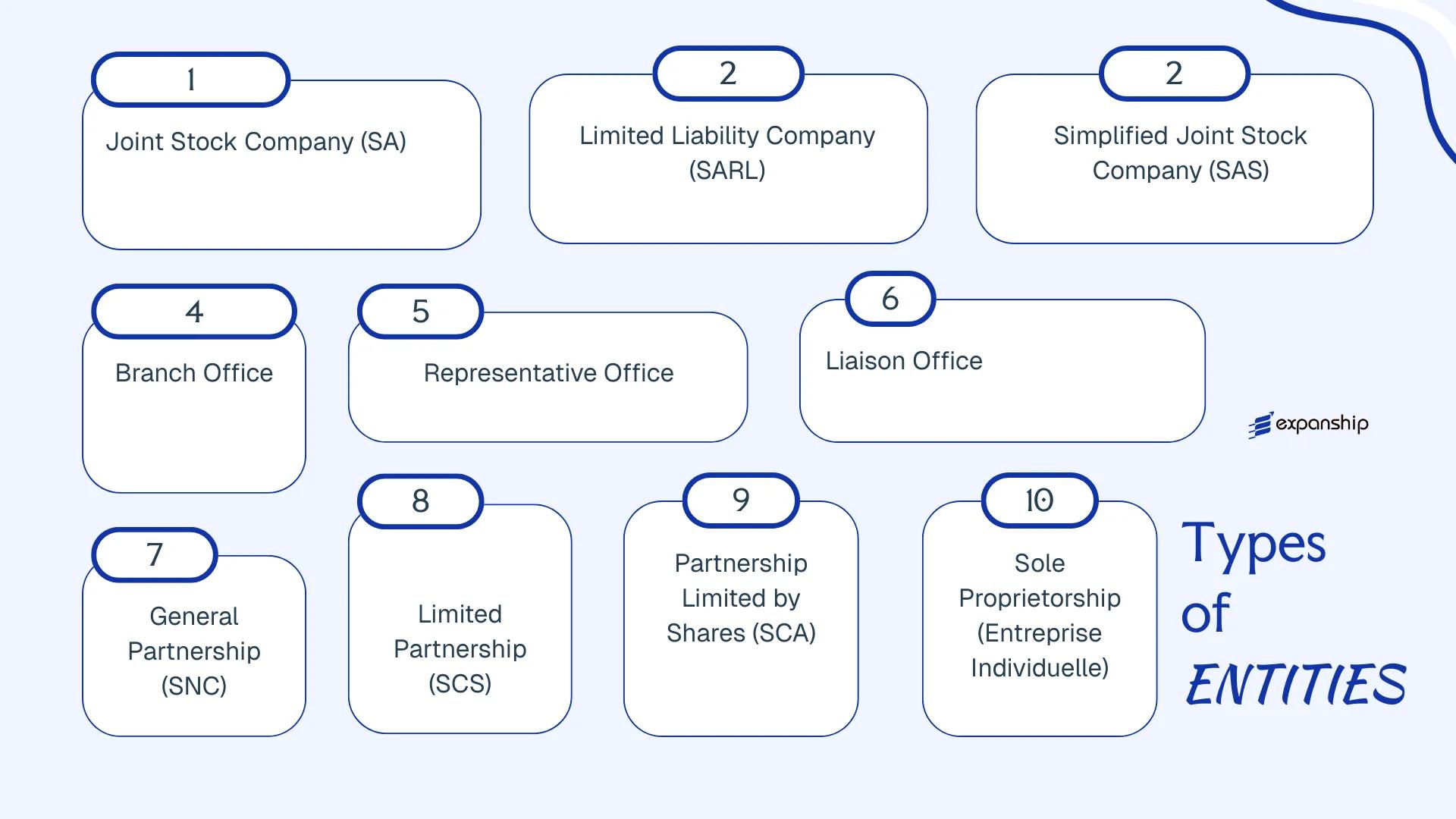

Several legal entity structures are available to both resident and foreign investors. These include the Société Anonyme (SA), Société à Responsabilité Limitée (SARL), Société par Actions Simplifiée (SAS), Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA), Branch Office, Representative Office, and Entreprise Individuelle.

Each structure carries distinct requirements around capital, governance, liability, and taxation. This article examines each option in turn to help your business identify the most appropriate formation path.

An Overview of Business Structures in Gabon

Under the OHADA Uniform Act on Commercial Companies and Economic Interest Groups (Acte Uniforme relatif au droit des sociétés commerciales et du groupement d'intérêt économique), Gabon recognises several distinct corporate forms available to both domestic and foreign investors. Each structure carries different rules on liability, governance, capital requirements, and permitted commercial activity.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| SA | Share company | Limited to shares | Taxed | Yes | 1 shareholder | CENAP / DGI | OHADA Uniform Act |

| SARL | Private limited company | Limited to contribution | Taxed | Yes | 1 shareholder | CENAP / DGI | OHADA Uniform Act |

| SAS | Simplified share company | Limited to shares | Taxed | Yes | 1 shareholder | CENAP / DGI | OHADA Uniform Act |

| SNC | General partnership | Unlimited, joint | Taxed | Yes | 2 partners | CENAP / DGI | OHADA Uniform Act |

| SCS | Limited partnership | Mixed liability | Taxed | Yes | 2 partners | CENAP / DGI | OHADA Uniform Act |

| SCA | Partnership limited by shares | Mixed liability | Taxed | Yes | 4 members | CENAP / DGI | OHADA Uniform Act |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Yes | N/A | CENAP / DGI | OHADA Uniform Act |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | No | N/A | CENAP / DGI | Gabonese Commercial Law |

| Sole Proprietorship | Individual trader | Unlimited personal | Taxed | Yes | 1 individual | DGI / CNAMGS | Gabonese Commercial Code |

Each of these structures is examined in full in the sections below.

Société Anonyme (SA)

The Société Anonyme (SA) is the primary vehicle for large-scale Société Anonyme SA Gabon formation, governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups (originally adopted in 1997, revised in 2014). As a joint stock company, the SA carries full separate legal personality and confers limited liability on its shareholders, capping each member's exposure at their capital contribution.

Ownership is divided into transferable shares, which allows the business to raise capital from a broad investor base, including through public markets where applicable. This structure is common among enterprises seeking external financing or planning eventual stock exchange listing.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (Joint Stock Company) | Separate legal personality; limited liability |

| Members | Minimum 1 shareholder; no maximum | OHADA 2014 revision permits single-shareholder SA |

| Governance | Board of Directors (minimum 3 directors) or single Administrator | Two governance models available under OHADA |

| Local Presence | Registered office address in Gabon required | No mandatory local director under OHADA, but local registration is required |

| Share Capital | Minimum XAF 10,000,000 (approx. USD 16,500) | Gabon SA minimum share capital; fully subscribed at formation |

| Privacy | Shareholder register maintained; beneficial ownership disclosure required | Public companies face additional disclosure obligations |

Focus Points

- Taxation: Subject to Gabonese corporate income tax (30%), VAT (18%) on applicable supplies, withholding taxes on dividends, royalties, and service fees paid abroad, and registration duties on share transfers; details are administered by the Direction Générale des Impôts.

- Annual Compliance: Annual general meeting required; audited financial statements mandatory when thresholds under OHADA are met; annual filings with the Centre de Formalités des Entreprises (CFE).

- Statutory Auditor: At least one commissaire aux comptes (statutory auditor) must be appointed; this is a firm-level obligation, not optional.

- Treaty Access: Gabon is a member of CEMAC and has limited bilateral tax treaties; SA entities can access available treaty benefits subject to substance requirements.

- Conversion: An SA may be converted into an SAS or SARL under OHADA provisions, subject to shareholder approval and regulatory filing.

Closing

The SA suits holding structures, large trading operations, and businesses that anticipate institutional investment or eventual public listing; its principal limitation is the higher administrative burden relative to simpler OHADA entities, including mandatory auditor appointment and more formal governance requirements.

The SA is most appropriate for large enterprises, joint ventures with institutional partners, or businesses intending to access capital markets.

Company Incorporation in Gabon

Incorporate your business in Gabon with end-to-end support across entity selection, registration, and ongoing compliance.

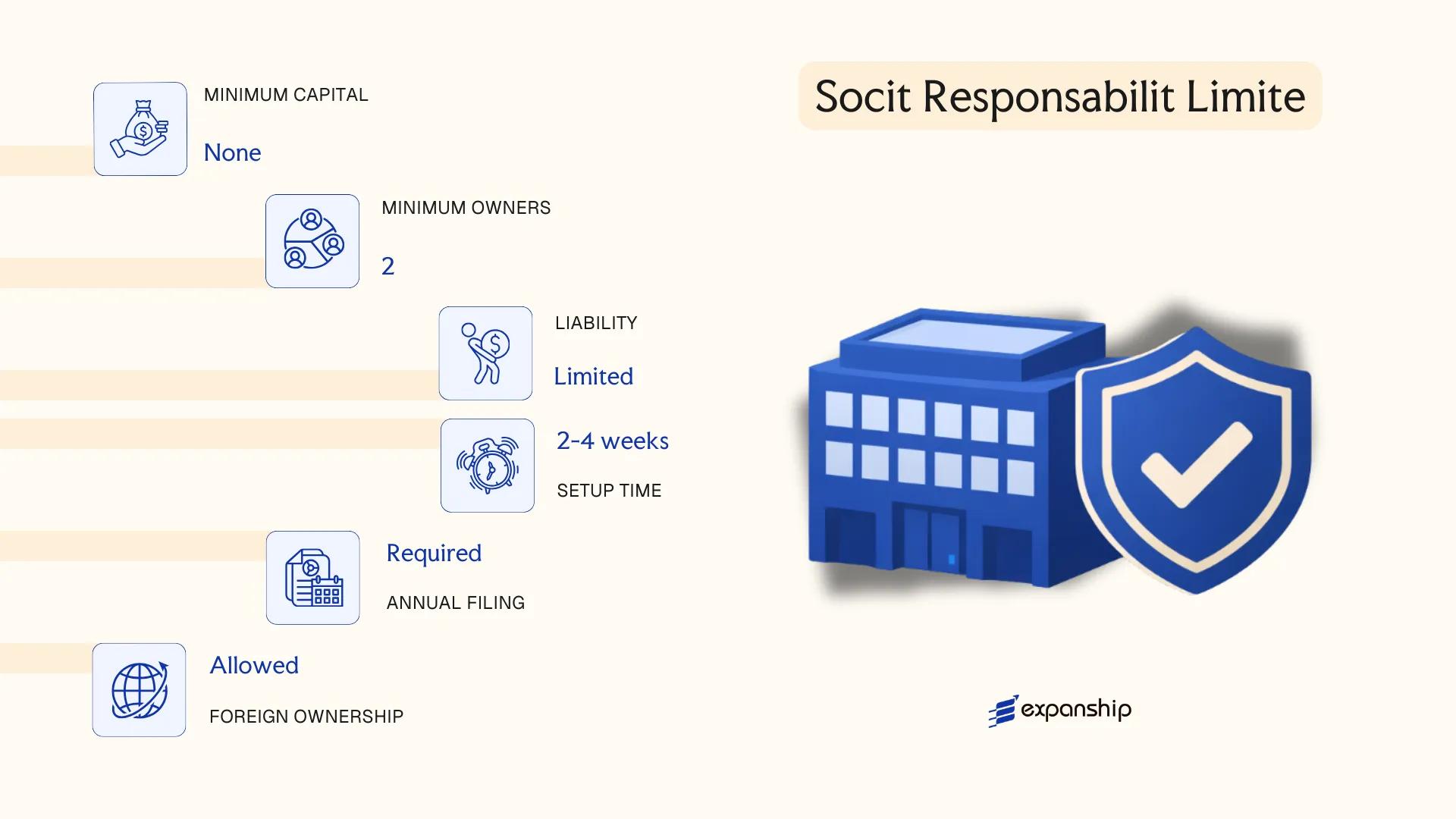

Société à Responsabilité Limitée (SARL)

The Société à Responsabilité Limitée SARL Gabon is governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups (AUDSCGIE), originally adopted in 1997 and revised in 2014. It is the most widely used commercial structure for small and mid-sized businesses operating in the country.

As a separate legal entity, the SARL shields its members from personal liability beyond their capital contributions. This hybrid character, combining the flexibility of a partnership with the liability protection of a corporation, makes SARL formation requirements in Gabon relatively accessible for both resident and foreign investors.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Governed by OHADA AUDSCGIE (revised 2014) |

| Members | 1 to 50 associates | A single-member SARL is permitted (SARL unipersonnelle) |

| Management | One or more gérants (managers) | Gérant need not be a member or a national resident |

| Share Capital | No statutory minimum under revised OHADA rules | Capital must be fully subscribed at incorporation |

| Local Presence | Registered office in Gabon required | No mandatory local director, but a registered address is compulsory |

| Privacy | Member names filed in the RCCM | Records are publicly accessible at the trade registry |

Focus Points

- Taxation: Subject to corporate income tax (standard rate of 30%), VAT at 18%, and withholding taxes on dividends, interest, and royalties paid to non-residents; stamp duty applies on certain instruments.

- Annual Compliance: Filing of audited financial statements with the RCCM and tax authorities; statutory audit is mandatory once the entity exceeds applicable OHADA thresholds.

- Treaty Access: Gabon is a member of CEMAC and party to select double taxation agreements; treaty eligibility depends on the beneficial ownership structure.

- Conversion: An SARL may be converted into an SA or SAS once member and capital thresholds are met, subject to member resolution and regulatory filings.

- Restrictions: Shares in an SARL are not freely transferable to third parties; transfers require approval from members holding a specified majority.

Closing Paragraph

The Gabon limited liability company SARL suits trading companies, locally embedded service businesses, and joint ventures where partners prefer a defined governance structure without the administrative burden of a full SA. Its primary constraint is the restriction on share transferability, which limits liquidity for investors seeking an eventual exit.

Best suited for small to mid-sized businesses, resident entrepreneurs, and foreign investors entering Gabon through a locally registered operating entity with defined liability boundaries.

Société par Actions Simplifiée (SAS)

The Société par Actions Simplifiée SAS Gabon framework is governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, most recently revised in 2014. As a distinct legal entity, the SAS carries its own rights, obligations, and liabilities, separate from those of its shareholders. This structure sits between the rigidity of the SA and the scale limitations of the SARL, making it a hybrid vehicle suited to joint ventures, holding arrangements, and subsidiaries of foreign groups.

Statutory rules for the SAS are less prescriptive than those applying to the SA, particularly around governance. Shareholders have broad contractual freedom to define voting rights, share transfer conditions, and management authority through the articles of association.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société par Actions Simplifiée | Separate legal personality; limited liability for shareholders |

| Members | Shareholders; minimum 1, no statutory maximum | A single-shareholder SAS is designated SASU |

| Management | President (mandatory); other officers optional | President can be a natural person or legal entity; nationality restrictions may apply |

| Registered Office | Physical address required in Gabon | Must be maintained for official correspondence and RCCM registration |

| Share Capital | No statutory minimum under OHADA 2014 reforms | Capital must be fully subscribed; amount set in the articles |

| Privacy | Shareholders not publicly disclosed by default | Articles and certain filings registered with the RCCM are accessible |

Focus Points

- Taxation: Subject to corporate income tax at the standard OHADA-member rate applicable in Gabon, VAT obligations where applicable, and withholding tax on dividends, royalties, and service fees paid to non-residents.

- Annual Compliance: Financial statements must be filed with the RCCM; statutory audit requirements depend on size thresholds set under OHADA rules.

- Conversion: An SAS may be converted into another OHADA-recognized form, such as an SA or SARL, subject to shareholder approval and regulatory filings.

- Transfer Restrictions: Share transfers are governed entirely by the articles; statutory pre-emption rights do not apply unless expressly included.

- Treaty Access: As a Gabonese-resident entity, the SAS can access bilateral tax treaties to which Gabon is a party, subject to beneficial ownership conditions.

Closing

The SAS suits foreign investors establishing local subsidiaries, joint ventures with defined governance arrangements, or holding structures where contractual flexibility over share rights is a priority. Its open capital rules and permissive governance framework reduce structural friction at incorporation, though the absence of statutory default protections means the articles of association must be carefully drafted to prevent disputes.

Foreign groups, joint venture partners, and investors requiring a flexible, scalable Gabonese entity with contractually defined governance and no minimum capital constraint.

Foreign Business Entities in Gabon [Branch Office, Representative Office, Liaison Office]

Operating as a foreign company branch office Gabon requires compliance with the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, which governs how non-resident entities may establish a presence within the country. Foreign firms do not automatically acquire separate legal personality through a branch; the parent company retains full liability for the branch's obligations.

Registration is handled through the Centre de Formalités des Entreprises (CFCE) and requires submission of the parent company's constitutional documents, duly apostilled and translated into French where necessary.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch, Representative Office, or Liaison Office | No separate legal personality in any form |

| Management | Appointed resident or non-resident representative | Must hold valid power of attorney from parent |

| Local Presence | Registered address in Gabon required | Physical office generally required for branches |

| Capital | No minimum capital for branch or liaison office | Branch may need working funds per sector regulations |

| Liability | Parent company bears full liability | No liability shield between branch and parent |

| Privacy | Parent company details disclosed upon registration | Public filings required at CFCE |

Focus Points

- Taxation: Branches are subject to corporate income tax at the standard rate; VAT obligations apply to taxable activities; withholding tax on remitted profits may apply under applicable double tax treaties.

- Economic Substance: Branches conducting active business must demonstrate genuine operational presence; purely passive structures face scrutiny.

- Annual Compliance: Annual financial statements and renewal of registration with the CFCE are required.

- Treaty Access: Access to double tax treaty benefits depends on the parent entity's residence and treaty terms; liaison offices generating no revenue generally fall outside treaty scope.

- Restrictions: Representative and liaison offices are prohibited from engaging in direct commercial or revenue-generating activities.

Sub-Types

Branch Office

A branch conducts active commercial operations on behalf of the parent company and is fully subject to Gabonese tax law on locally sourced income. It is the appropriate structure when a foreign firm intends to execute contracts, employ staff, or generate revenue locally.

Representative Office

A representative office is limited to market research, promotion, and liaison activities. It cannot sign commercial contracts or invoice clients, and its permissible scope is narrower than a branch.

Liaison Office

Functionally similar to a representative office, a liaison office is used primarily for administrative coordination between the parent entity and local partners or authorities, with no commercial mandate whatsoever.

Closing

Foreign entities that require operational capacity without incorporating a local subsidiary typically use a branch, while those conducting preliminary market activities opt for a representative or liaison office. The primary advantage is avoiding full local incorporation; the corresponding limitation is that the parent bears unlimited liability for all branch obligations.

A branch office suits established foreign companies with confirmed commercial activity in Gabon; a liaison or representative office is more appropriate during exploratory or pre-market phases.

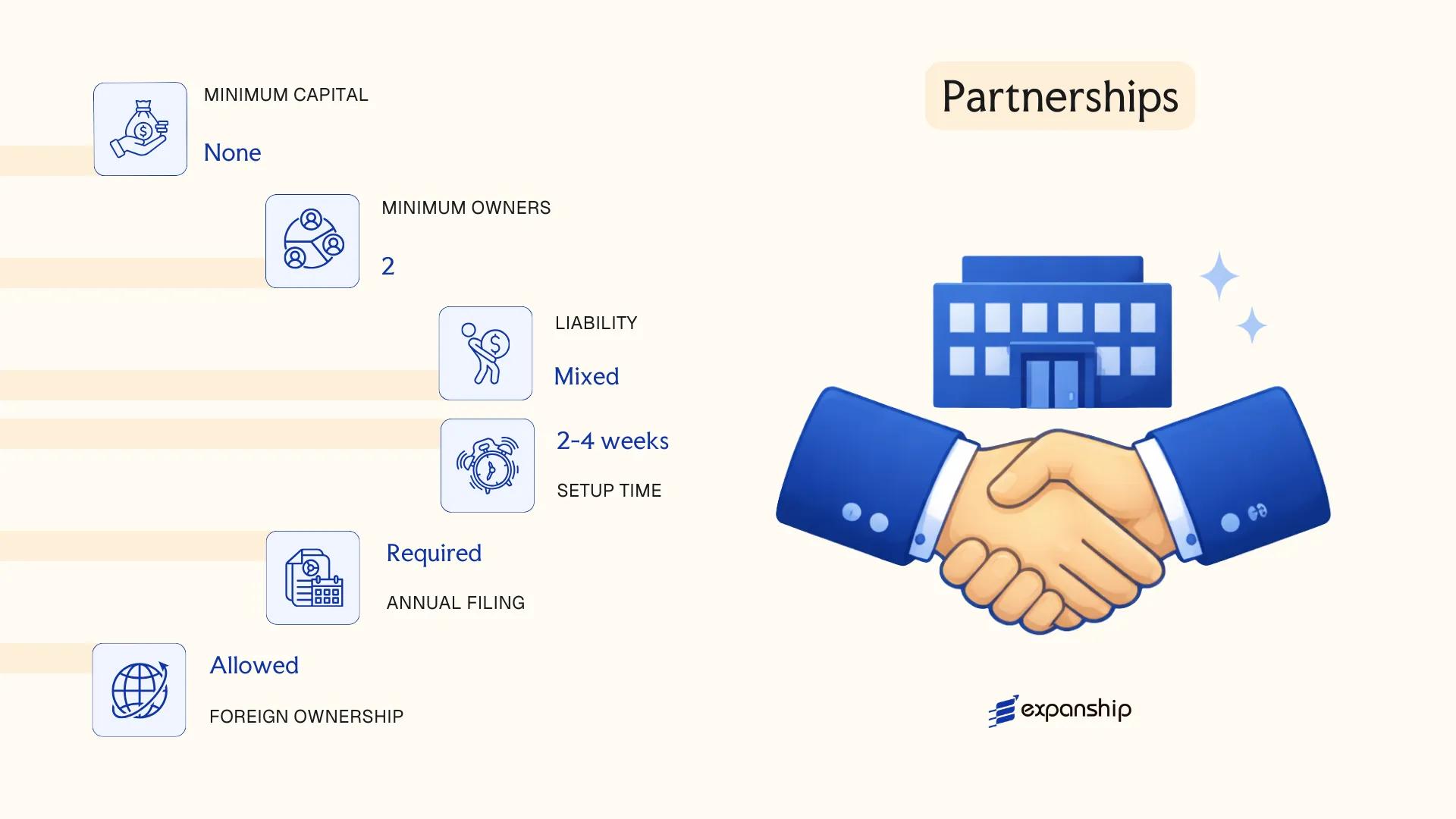

Partnerships in Gabon [Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA)]

Gabon's partnership structures in Gabon SNC SCS and related forms are governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups (Acte Uniforme relatif aux Sociétés Commerciales et au Groupement d'Intérêt Économique), which Gabon adopted as a member state of the Organisation pour l'Harmonisation en Afrique du Droit des Affaires. This framework defines three distinct partnership vehicles: the Société en Nom Collectif (SNC), the Société en Commandite Simple (SCS), and the Société en Commandite par Actions (SCA).

Each structure carries separate legal personality upon registration with the Centre de Formalités des Entreprises (CFE). Liability treatment differs across the three forms, ranging from unlimited joint liability for all partners in an SNC to a hybrid model in the SCA where some investors hold limited liability through transferable shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Three distinct types: SNC, SCS, SCA | All carry separate legal personality under OHADA |

| Members | SNC: minimum 2 associés (all general partners, unlimited); SCS: minimum 1 general partner (commandité) + 1 limited partner (commanditaire); SCA: minimum 1 general partner + 3 shareholders (actionnaires commanditaires) | No statutory maximum for any form |

| Liability | SNC: unlimited joint liability for all; SCS: unlimited for commandités, limited to contribution for commanditaires; SCA: same split as SCS | General partners in SCS and SCA are personally exposed |

| Capital | No statutory minimum for SNC or SCS; SCA requires share capital divided into negotiable shares | Capital denominated in CFA Franc (XAF) |

| Local Presence | Registered office in Gabon required for all three forms | A physical address within the country is mandatory |

| Privacy | Partner identities disclosed in the RCCM (Registre du Commerce et du Crédit Mobilier) | No confidentiality provisions under OHADA for partnerships |

Focus Points

- Taxation: Partnerships are generally subject to corporate income tax at the standard rate applicable in Gabon; VAT obligations apply to commercial activities, and withholding tax rules under domestic law govern distributions to foreign partners.

- Annual Compliance: All three forms must file annual financial statements and maintain accounting records in accordance with the OHADA Uniform Act on Accounting Law (SYSCOHADA).

- Treaty Access: Tax treaty eligibility depends on whether the entity is treated as a resident taxpayer; general partners' personal tax exposure may affect treaty application.

- Restrictions: General partners in an SNC and commandités in an SCS and SCA cannot limit their liability by agreement — this is fixed by statute under the OHADA framework.

- Conversion: An SNC or SCS may be converted into a SARL or SA through a formal restructuring process subject to OHADA procedures and creditor notification requirements.

Sub-Types

Société en Nom Collectif (SNC)

All partners hold the status of merchant (commerçant) and bear unlimited, joint, and several liability for the firm's debts. The SNC is most commonly used by small professional or family-operated businesses where personal accountability among partners is accepted.

Société en Commandite Simple (SCS)

This form separates active management (commandités, with unlimited liability) from passive investors (commanditaires, liable only to the extent of their contribution). The Société en Commandite Gabon SCS structure suits arrangements where a managing partner operates the business while silent investors provide capital without operational involvement.

Société en Commandite par Actions (SCA)

The Gabon SCA limited partnership introduces transferable shares for the limited partners, making it the most structurally complex of the three. It is used in cases where capital needs to be raised from multiple investors while control is retained by one or more general partners with unlimited liability.

Closing

Partnership structures are used most often for family businesses, professional firms, and arrangements requiring a clear separation between active managers and passive capital contributors. The principal advantage is structural flexibility in allocating control and risk; the central limitation is that general partners in all three forms face personal, unlimited liability for entity obligations.

These structures are most appropriate for closely held businesses or arrangements where at least one party is willing to accept unlimited personal liability in exchange for full operational control.

Sole Proprietorship (Entreprise Individuelle)

The sole proprietorship Gabon Entreprise Individuelle is the simplest business form available to individual operators under Gabonese commercial law, governed by the OHADA Uniform Act on General Commercial Law (Acte Uniforme relatif au Droit Commercial Général), as revised in 2010. Unlike capital companies, this structure carries no separate legal personality — the business and its owner are legally indistinguishable.

Because personal and business assets are not separated, the proprietor bears unlimited personal liability for all commercial obligations. Registration is handled through the Centre de Formalités des Entreprises (CFE), and the business must be entered in the Registre du Commerce et du Crédit Mobilier (RCCM).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Entreprise Individuelle) | No separate legal personality from the owner |

| Members | Single proprietor | No minimum capital requirement |

| Local Presence | Registered business address required | Must be declared at CFE and RCCM |

| Capital | No statutory minimum | Gabon CFA Franc (XAF); owner contributes as needed |

| Liability | Unlimited personal liability | Personal assets exposed to business debts |

| Privacy | Owner's identity publicly registered via RCCM | No shareholding structure to obscure ownership |

Focus Points

- Taxation: Subject to income tax (Impôt sur le Revenu) on business profits rather than corporate income tax; VAT registration is required once turnover thresholds are met; no withholding tax structure applies at the entity level.

- Annual Compliance: Must file annual income tax returns and maintain accounting records in line with the OHADA Uniform Act on Accounting Law (Acte Uniforme relatif au Droit Comptable).

- Conversion: Can be converted into a capital company such as a SARL, but requires a formal incorporation process and RCCM re-registration.

- Treaty Access: As a pass-through structure without separate legal personality, access to Gabon's tax treaties is generally limited or unavailable at the entity level.

- Restrictions: Foreign nationals face additional conditions under Gabonese law before operating as a sole trader; local licensing requirements vary by activity sector.

Closing Paragraph

The Entreprise Individuelle suits resident individuals conducting low-volume trade, artisanal activities, or consulting services where administrative simplicity outweighs the need for liability protection. The primary advantage is minimal setup cost and administrative burden; the significant drawback is unrestricted personal exposure to business debts.

This structure is best suited for Gabonese residents or qualifying individuals operating small-scale, low-risk commercial or professional activities who do not require external investment or corporate liability protection.

How to Choose the Right Entity Type in Gabon

Knowing how to choose a company type in Gabon requires more than a general preference for simplicity or cost — the wrong choice produces concrete legal and financial consequences.

Why Your Entity Choice Matters

- Registering a foreign branch to conduct local commercial trade without meeting the registration requirements under the OHADA Uniform Act on Commercial Companies exposes the business to deregistration and administrative penalties.

- Selecting a structure without legal personality — such as an SNC — when your contracts require a distinct legal counterparty creates enforceability problems at the point of dispute.

- Choosing an entity that mandates statutory audit (the SA requires a commissaire aux comptes) for a single-person consultancy adds recurring compliance costs that a SARL or Entreprise Individuelle would not trigger.

- Forming an SA when flexible, bilateral governance between two founders is the actual need locks you into a mandatory board structure and capital requirements that do not apply to a SAS or SARL.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors (banking, insurance), and passive asset-holding each point to different structures under OHADA rules.

- Ownership Structure: A sole founder has no reason to form an SA; multi-investor firms requiring transferable share classes are poorly served by an SARL.

- Governance Preferences: If you need a simplified, contractually defined management framework, a SAS offers statutory flexibility that an SA does not.

- Liability Exposure: Activities carrying high third-party risk call for limited liability structures rather than general partnerships, where personal assets remain exposed.

- Substance Capacity: If you cannot maintain a physical presence or local management, certain structures will face scrutiny from the Direction Générale des Impôts regarding tax residency.

- Exit and Transferability: SARL share transfers require shareholder approval under the OHADA framework; SA and SAS shares transfer more freely, which matters if investor exit is anticipated.

For the governing statutory text, consult the OHADA Uniform Act on Commercial Companies and Economic Interest Groups.

Compliance Services for Companies in Gabon

Maintain good standing with Gabon's regulatory requirements — from annual filings to statutory record-keeping.

Conclusion

Gabon offers a defined set of legal structures governed primarily by the OHADA Uniform Acts, giving your incorporating a company in Gabon guide a consistent regulatory foundation to work from. The SA suits larger enterprises requiring capital market access or institutional investment. SARLs remain the most commonly registered entity in the country, favored by small and medium-sized businesses for their straightforward governance requirements. The SAS provides contractual flexibility for joint ventures and holding arrangements. Branch and representative offices serve foreign firms testing the market before committing to full incorporation. Partnerships and the sole proprietorship address more specific operational or personal liability considerations.

Gabon's continued membership in OHADA and its engagement with regional economic frameworks suggest a gradual trajectory toward greater regulatory harmonization across Central Africa. For businesses evaluating Gabon company formation, understanding which structure aligns with your ownership model and operational scope is the first practical step.

How Expanship Can Assist You

Setting up a corporate services company registration in Gabon involves working within the OHADA legal framework, registering with the Centre de Formalités des Entreprises (CFCE), and meeting the specific capital and governance requirements tied to your chosen entity — whether an SA, SARL, or SAS. Expanship works directly with these processes, helping your business move from entity selection to operational status without unnecessary delays.

From document preparation to post-incorporation filing, our services cover the full scope of what incorporation in Gabon requires:

- Document preparation and notarization

- Registered agent and legal address provision

- CFCE filing and government registrar liaison

- Post-incorporation compliance management

- Banking introduction assistance

Every engagement is handled by professionals who understand Gabon's regulatory requirements firsthand, not generalists working from templates.

Ready to take the next step? Reach out to Expanship Gabon to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is the most frequently registered structure. Its lower capital requirements and simplified governance make it accessible to both domestic entrepreneurs and foreign investors operating at the SME level.

A SARL is suited to closely held businesses with fewer shareholders, while an SA accommodates larger enterprises that may seek external capital. Both structures are subject to OHADA Uniform Act regulations, though the SA carries heavier compliance obligations, including mandatory statutory auditors once certain thresholds are met.

The Société par Actions Simplifiée (SAS) provides the greatest structural flexibility regarding internal governance, and its shareholder arrangements are not always fully disclosed in public registries. Nominee arrangements are permissible under Gabonese law, though beneficial ownership obligations under CEMAC anti-money laundering directives still apply.

Not all structures permit sole formation. A SARL can be formed by one shareholder, and a SAS similarly accommodates a single founder, but partnerships such as the Société en Nom Collectif (SNC) require at least two partners by definition under the OHADA Uniform Act on Commercial Companies.

Foreigners may register a SARL, SA, or SAS without a local partner requirement, subject to obtaining the necessary authorizations under Gabonese investment law. A Branch Office or Representative Office provides an alternative for foreign companies testing the market before committing to full incorporation.

Conversion is permitted under the OHADA framework. A SARL can be converted to an SA once it meets the requisite capital and shareholder conditions, and the process generally requires a shareholder resolution and filing with the Centre de Formalités des Entreprises (CFE).

The SARL, SA, and SAS each hold distinct legal personality separate from their shareholders. Partnerships such as the SNC do not fully separate personal liability from the entity, and a Representative Office carries no independent legal personality whatsoever.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.