Key Takeaways

- Ecuador's business entities are governed by the Ley de Compañías and registered through the Superintendencia de Compañías, Valores y Seguros (SCVS), which serves as the national authority for incorporation and regulatory oversight.

- The Compañía de Responsabilidad Limitada (Cía. Ltda.) is the most widely registered entity type among small and medium-sized businesses in Ecuador.

- Foreign companies operating in Ecuador can establish either a Branch Office, which permits direct commercial activity, or a Representative Office, which is restricted to non-commercial functions.

- Among the newer structures available, the Sociedad por Acciones Simplificada (SAS) offers a more flexible formation process with reduced statutory formalities compared to the S.A. or Cía. Ltda.

Introduction to Entity Types in Ecuador

Ecuador sits on the northwestern coast of South America, bordered by Colombia to the north and Peru to the south and east. It is an independent republic, and company registration falls under the jurisdiction of the Superintendencia de Compañías, Valores y Seguros (SCVS), the national authority responsible for incorporating, supervising, and regulating legal entities operating within the country.

Ecuador operates a territorial-based tax system, meaning resident companies are taxed on worldwide income while certain foreign-sourced income may receive differential treatment under domestic rules.

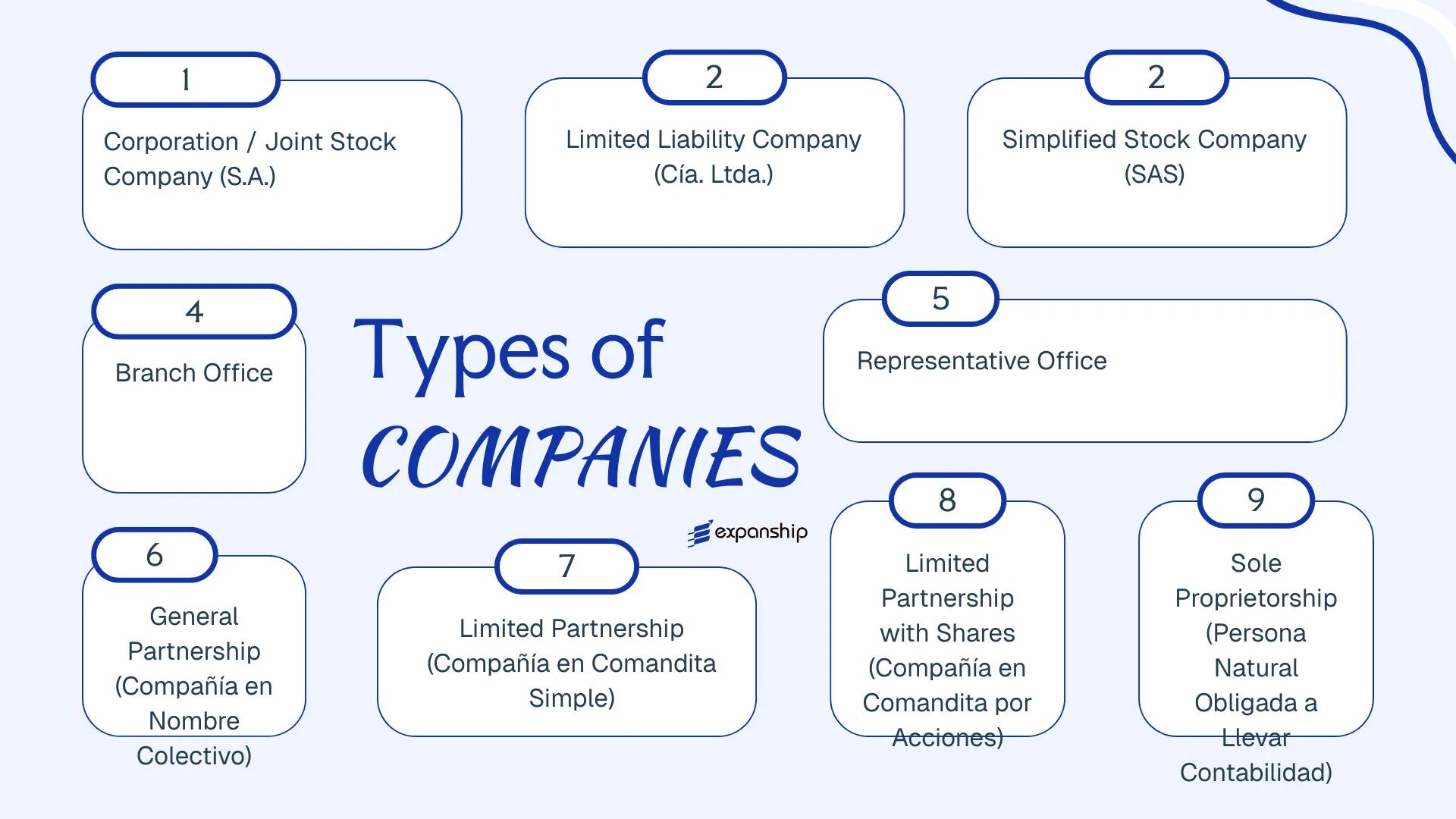

Understanding the types of business entities in Ecuador is a prerequisite before selecting a structure — each carries distinct liability, capital, and governance requirements under the Ley de Compañías. The available legal forms include the Sociedad Anónima (S.A.), Compañía de Responsabilidad Limitada (Cía. Ltda.), Sociedad por Acciones Simplificada (SAS), Compañía en Nombre Colectivo, Compañía en Comandita Simple, Compañía en Comandita por Acciones, Branch Office, Representative Office, and the Persona Natural Obligada a Llevar Contabilidad. Each of these structures is examined in detail across the sections that follow.

An Overview of Business Structures in Ecuador

Ecuador business structures overview falls under a framework that recognises six principal entity types, each defined under the Ley de Compañías and supervised by the Superintendencia de Compañías, Valores y Seguros (SCVS). Complementing these, the Código de Comercio governs certain commercial activities carried out by individuals and foreign operators. Each structure carries distinct rules on liability, membership, and permitted activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima (S.A.) | Corporation | Limited to shares | Taxed | Yes | 2 shareholders | SCVS | Ley de Compañías |

| Cía. Ltda. | LLC | Limited to stake | Taxed | Yes | 2 partners | SCVS | Ley de Compañías |

| Sociedad por Acciones Simplificada (SAS) | Simplified corp | Limited to shares | Taxed | Yes | 1 shareholder | SCVS | Ley de Compañías |

| Branch Office | Foreign branch | Parent liable | Taxed | Yes | N/A | SCVS | Ley de Compañías |

| Representative Office | Foreign presence | Parent liable | Generally exempt | No | N/A | SCVS | Ley de Compañías |

| Compañía en Nombre Colectivo | General partnership | Unlimited | Taxed | Yes | 2 partners | SCVS | Ley de Compañías |

| Compañía en Comandita Simple | Limited partnership | Mixed | Taxed | Yes | 2 partners | SCVS | Ley de Compañías |

| Compañía en Comandita por Acciones | LP with shares | Mixed | Taxed | Yes | 2 partners | SCVS | Ley de Compañías |

| Persona Natural (Obligada a Llevar Contabilidad) | Sole proprietorship | Unlimited | Taxed | Yes | 1 person | SRI / SCVS | Código de Comercio |

Each of these structures is examined in full in the sections below.

Sociedad Anónima (S.A.)

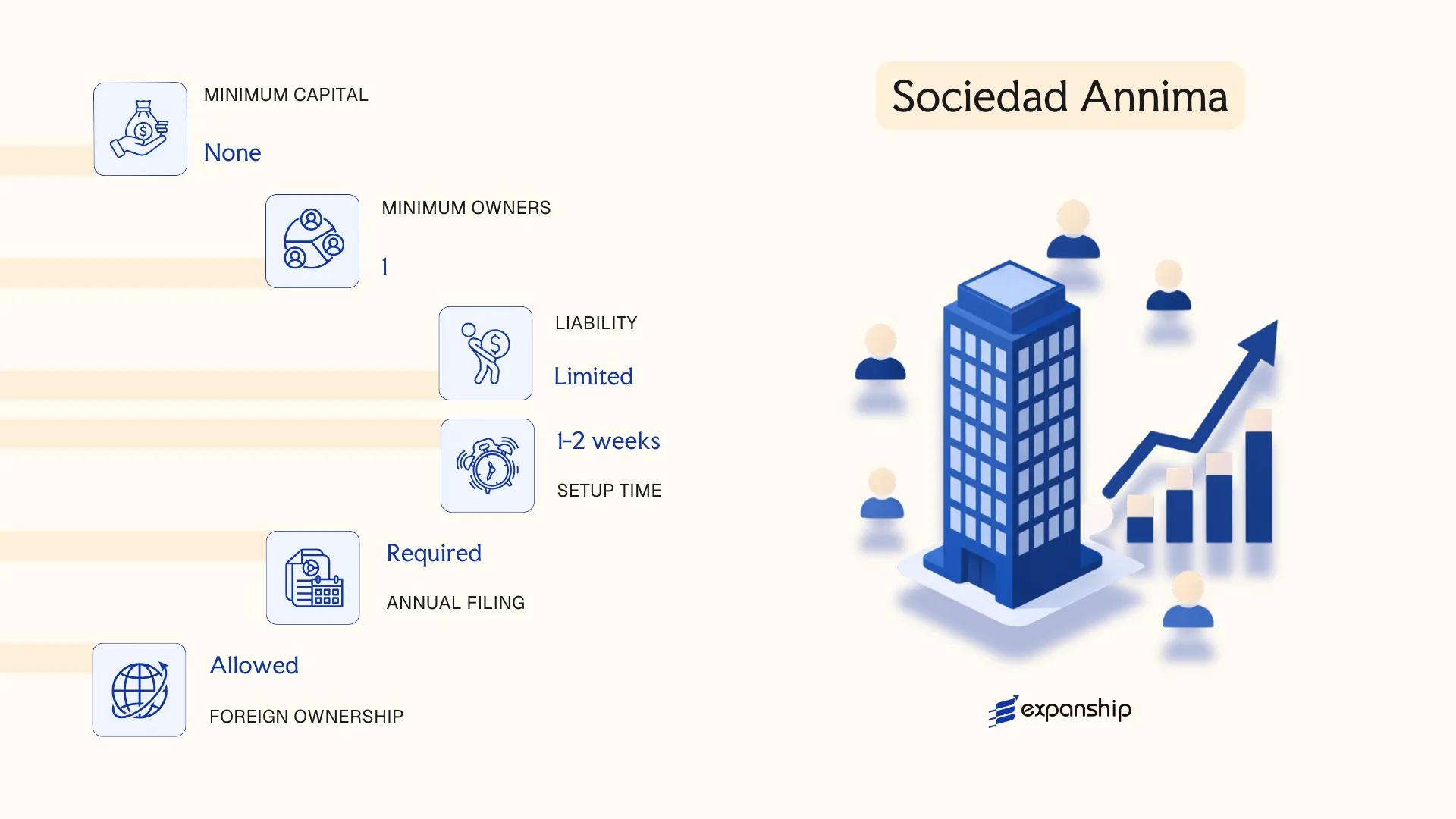

Governed by the Ley de Compañías of 1999 and overseen by the Superintendencia de Compañías, Valores y Seguros (SCVS), the Sociedad Anónima Ecuador formation process produces a fully separate legal entity with limited liability. Shareholders bear no personal responsibility for corporate obligations beyond their subscribed capital contribution.

Capital is divided into negotiable shares, which can be transferred without requiring approval from other shareholders. This free transferability distinguishes the S.A. from more restrictive structures and makes it the standard choice for businesses that anticipate investor participation or eventual equity transactions.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima (S.A.) | Registered and regulated by the SCVS |

| Members | Shareholders; minimum 2, no statutory maximum | Shareholders can be individuals or legal entities, domestic or foreign |

| Capital | Minimum USD 800 fully subscribed; at least 25% paid in at incorporation | Denominated in U.S. dollars; balance payable within 2 years |

| Local Presence | Registered domicile in Ecuador required; a legal representative (who must be resident) is mandatory | No requirement for a resident director beyond the legal representative |

| Share Transferability | Shares are freely transferable unless restricted by company statutes | Restrictions must be written into the articles of incorporation |

| Privacy | Shareholder information filed with the SCVS; not fully private | Beneficial ownership data reportable under anti-money-laundering obligations |

Focus Points

- Taxation: Subject to a standard corporate income tax rate of 25% (22% for compliant entities meeting reinvestment conditions); VAT at 15% applies to taxable supplies; dividends distributed to non-residents attract a 10% withholding tax; no stamp duty on share transfers.

- Annual Compliance: Audited financial statements required if assets or revenue exceed statutory thresholds set by the SCVS; annual reports and shareholder meeting minutes must be filed.

- Treaty Access: Ecuador maintains a limited network of double taxation agreements; S.A. entities qualify as residents for treaty purposes where treaties are in force.

- Conversion: An S.A. may be converted into another company type permitted under the Ley de Compañías through a formal transformation process approved by the SCVS.

- Foreign Ownership: No restriction on 100% foreign shareholding, though certain regulated sectors apply ownership caps independently.

Closing

The S.A. suits trading operations, holding structures, and businesses seeking to raise capital from multiple investors, with free share transferability being its principal structural advantage. The mandatory residency requirement for the legal representative and the relatively higher administrative compliance burden compared to simpler structures are practical constraints to account for during planning.

The S.A. is best suited for medium-to-large enterprises, joint ventures with multiple investors, or any business where future equity transfers or external investment are anticipated.

Company Incorporation in Ecuador

Incorporate a Sociedad Anónima or other entity type in Ecuador with full regulatory support from the SCVS registration through to post-incorporation compliance.

Compañía de Responsabilidad Limitada (Cía. Ltda.)

The Compañía de Responsabilidad Limitada Ecuador framework is governed by the Ley de Compañías, originally enacted in 1999 and administered by the Superintendencia de Compañías, Valores y Seguros (SCVS). It constitutes a separate legal entity, meaning the company holds rights and obligations independently of its members.

Liability is capped at each member's capital contribution. The structure occupies a middle ground between a closely held partnership and a corporation, making it a common choice for small to medium-sized businesses seeking legal separation without the formalities of a Sociedad Anónima.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (Sociedad de Responsabilidad Limitada) | Separate legal personality; governed by the Ley de Compañías |

| Members | Referred to as socios; minimum 2, maximum 15 | Exceeding 15 socios requires conversion to an S.A. |

| Capital | Minimum USD 400, divided into participaciones (not shares) | Participaciones are not freely transferable without member consent |

| Local Presence | Registered legal address in Ecuador required | A domicilio fiscal must be registered with the SCVS |

| Management | Managed by a gerente (general manager) appointed by socios | The gerente acts as legal representative |

| Privacy | Member names appear in public SCVS registry | No bearer participaciones permitted |

Focus Points

- Taxation: Subject to 25% corporate income tax; 12% VAT applies to taxable supplies; dividends remitted abroad attract withholding tax, generally 10%, subject to applicable double tax treaties.

- Annual Compliance: Annual financial statements must be filed with the SCVS; tax returns submitted to the Servicio de Rentas Internas (SRI).

- Transfer Restrictions: Transfer of participaciones requires approval from the remaining socios and formal notarisation, limiting investor exit flexibility.

- Treaty Access: Ecuador maintains a limited tax treaty network; treaty benefits depend on the residency status of the foreign shareholder.

- Conversion: A Cía. Ltda. exceeding 15 members is legally required to convert to an S.A. under Article 92 of the Ley de Compañías.

Closing

The Cía. Ltda. suits owner-operated trading businesses, family-held firms, and local service companies where ownership is intended to remain closely held. The member cap of 15 socios, however, limits scalability for ventures anticipating broader equity participation.

Small to medium-sized businesses with a defined, stable group of local or foreign investors who require limited liability without the administrative overhead of a full share company structure.

Sociedad por Acciones Simplificada (SAS)

Introduced under the Ley de Compañías through amendments that took effect in 2020, the Sociedad por Acciones Simplificada Ecuador represents a deliberately flexible corporate form designed to reduce the procedural burden of traditional incorporation. It carries separate legal personality, meaning the entity holds rights and obligations distinct from those of its shareholders.

Liability is limited to each shareholder's capital contribution. The SAS is classified as a hybrid structure — it draws from share-based corporate models while allowing statutes to be tailored extensively, giving founders significant latitude in defining governance, profit distribution, and transfer restrictions.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Simplified Joint Stock Company | Governed by the Ley de Compañías; registered with the Superintendencia de Compañías, Valores y Seguros (SCVS) |

| Members | Shareholders; minimum 1, maximum unlimited | Single-shareholder formation is permitted — a notable departure from older Ecuadorian corporate forms |

| Local Presence | Registered domicile required within Ecuador | A legal address must be declared before the SCVS; a registered agent is not a statutory requirement |

| Capital | USD; no fixed statutory minimum | Contributions may be in cash or in kind; capital is divided into shares with values set in the articles |

| Privacy | Shareholder information filed with the SCVS | Beneficial ownership disclosure requirements apply under anti-money laundering regulations |

| Governance | Flexible; defined by the company's estatutos | No mandatory board structure; a single administrator can suffice |

Focus Points

- Taxation: Subject to corporate income tax at 25% (or 28% where a foreign fiscal haven is involved), VAT at 15% on taxable supplies, withholding tax on payments to non-residents at rates varying by payment type, and no stamp duty on share transfers.

- Annual compliance: Obligated to file audited or reviewed financial statements with the SCVS annually; income tax returns filed with the Servicio de Rentas Internas (SRI).

- Economic substance: No formal substance test under Ecuadorian law, though transfer pricing rules apply to transactions with related parties across borders.

- Conversion: An SAS may be converted into another company type recognised under the Ley de Compañías, subject to SCVS approval and compliance with conversion procedures.

- Restrictions: Foreign nationals may hold shares, but activities in strategic sectors may require prior authorisation from relevant sector regulators.

Closing

The SAS suits early-stage ventures, startups, and domestic holding structures where founders require governance flexibility and a simplified formation process without the shareholder minimums imposed on older corporate forms. Its primary limitation is that it lacks the established track record and international recognition of the Sociedad Anónima, which can occasionally affect banking relationships or foreign investor due diligence.

Best suited for resident or non-resident entrepreneurs forming a single-founder or small-team operating company in Ecuador who prioritise flexible governance over conventional corporate familiarity.

Foreign Business Structures in Ecuador [Branch Office, Representative Office]

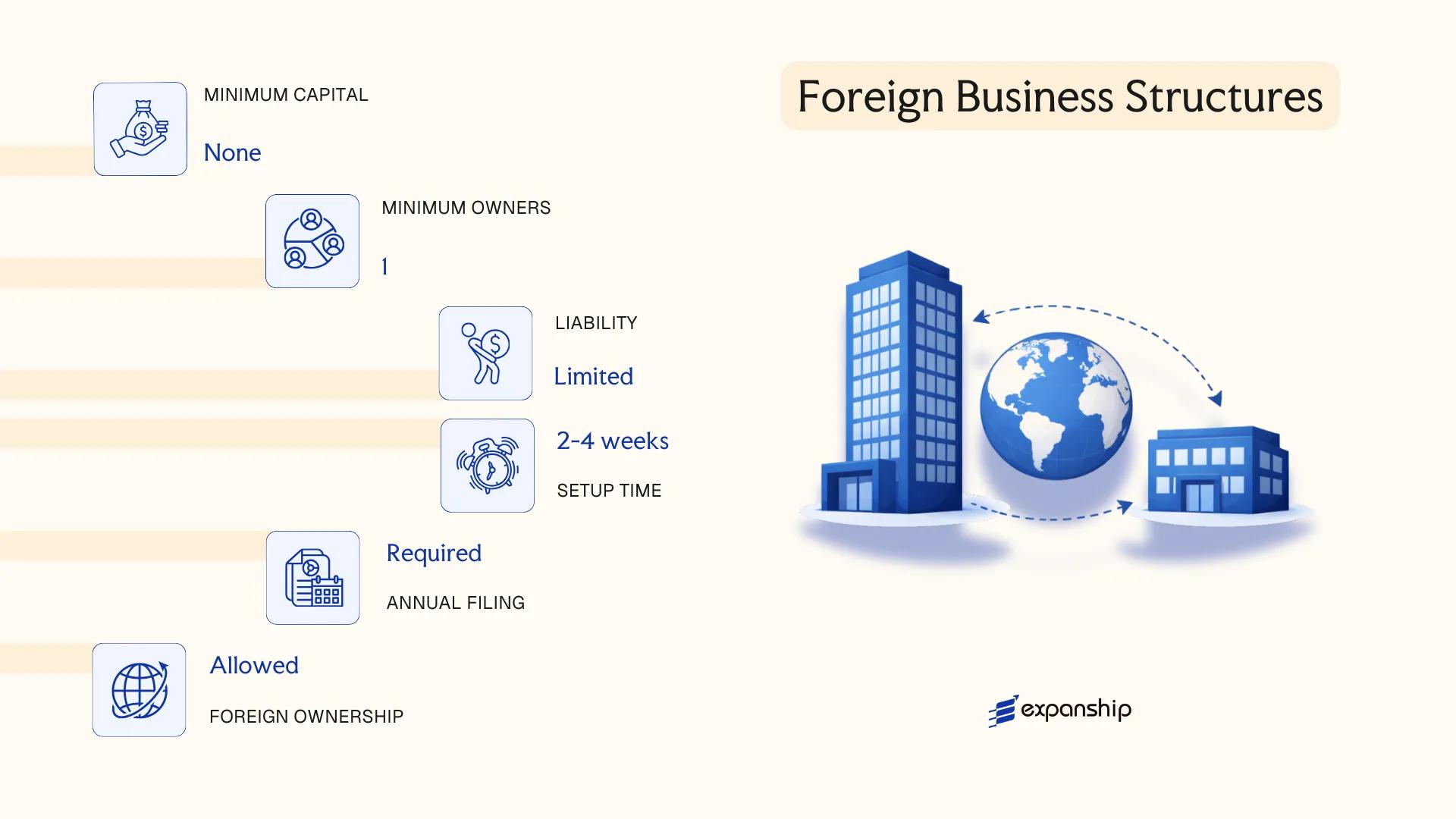

Establishing a foreign company branch office in Ecuador is governed by the Ley de Compañías, administered by the Superintendencia de Compañías, Valores y Seguros (SCVS). A branch (sucursal) does not constitute a separate legal entity; it remains an extension of the parent company, which bears full liability for the branch's obligations. Registration requires a notarized resolution from the parent company authorizing the branch's establishment, along with authenticated copies of the parent's constitutive documents.

A representative office (oficina de representación) operates under a more restricted mandate. It cannot engage in direct commercial transactions or generate local revenue — its activities are limited to promotion, liaison, and market research on behalf of the foreign parent.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Commercial Activity | Permitted | Not permitted |

| Legal Representative | Mandatory local appointed agent | Mandatory local appointed agent |

| Registered Address | Required in Ecuador | Required in Ecuador |

| Minimum Capital Assignment | Required (amount set by SCVS) | Not applicable |

| Liability | Parent company bears full liability | Parent company bears full liability |

Focus Points

- Taxation: Branch profits are subject to the standard 25% corporate income tax; a 10% additional withholding applies on remittances to the foreign parent; VAT at 15% applies to taxable supplies.

- Economic Substance: No formal substance regime exists, but the branch must maintain demonstrable local operations to sustain its registration.

- Annual Compliance: Annual financial statements must be filed with the SCVS; the appointed legal representative must remain current with the public registry.

- Treaty Access: Ecuador's double taxation treaties may apply to branch profits, depending on the parent's jurisdiction of residence.

- Restrictions: Representative offices are strictly prohibited from invoicing, signing commercial contracts, or earning revenue locally.

Sub-Types

Branch Office (Sucursal)

A sucursal is the standard mechanism for foreign firms seeking operational presence and the ability to contract, invoice, and conduct trade. It requires a capital assignment registered with the SCVS and is the appropriate structure when the foreign parent intends to generate revenue directly.

Representative Office (Oficina de Representación)

This structure suits foreign companies that need a local foothold for promotional or informational purposes only. Because it cannot generate income, it carries lower compliance obligations but offers no path to commercial activity without converting to a branch or local entity.

A branch office is commonly used by foreign firms in sectors such as construction, services, and trading that require direct contracting capacity but prefer to avoid incorporating a separate local entity. The primary limitation is that the parent assumes unlimited liability for all branch obligations without the liability shield available through a locally incorporated subsidiary.

Foreign companies seeking temporary or sector-specific operational presence in Ecuador without establishing a standalone local entity.

Partnerships in Ecuador [General Partnership (Compañía en Nombre Colectivo), Limited Partnership (Compañía en Comandita Simple), Limited Partnership with Shares (Compañía en Comandita por Acciones)]

Partnership structures in Ecuador are governed by the Ley de Compañías, codified under Codification No. 000, administered by the Superintendencia de Compañías, Valores y Seguros (SCVS). Three distinct partnership forms exist under this legislation: the Compañía en Nombre Colectivo, the Compañía en Comandita Simple, and the Compañía en Comandita por Acciones.

All three structures carry full legal personality upon registration with the SCVS. Each differs primarily in how liability is distributed among partner classes and whether capital is divided into transferable shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Forms | Compañía en Nombre Colectivo / Compañía en Comandita Simple / Compañía en Comandita por Acciones | Three distinct partnership forms under the Ley de Compañías |

| Members | Partners (socios); Comandita forms have general (gestores) and limited (comanditarios) partners | Nombre Colectivo: min. 2, no statutory max; Comandita Simple: min. 2; Comandita por Acciones: min. 2 per class |

| Liability | Nombre Colectivo: unlimited for all partners; Comandita Simple: unlimited for gestores, limited for comanditarios; Comandita por Acciones: same class split | Unlimited liability partners are personally exposed to business debts |

| Capital | No statutory minimum across all three forms; Comandita por Acciones divides capital into shares | Shares in Comandita por Acciones are transferable; interests in the other two are generally not freely transferable |

| Local Presence | Registered domicile in Ecuador required; registered agent not separately mandated but a legal representative must be appointed | Legal representative must be domiciled locally |

| Privacy | Partner names appear in public registration records with the SCVS | No meaningful privacy for general partners |

Focus Points

- Taxation: Subject to Ecuadorian corporate income tax at the standard rate (currently 25%); VAT obligations at 15% apply to commercial activities; profit distributions to foreign partners may attract withholding tax under domestic rules or applicable double tax treaties.

- Annual Compliance: Annual financial statements must be filed with the SCVS; failure to file triggers administrative sanctions including potential dissolution.

- Treaty Access: Access to Ecuador's double tax treaty network depends on partner residency and the structure's qualification as a resident entity under each treaty.

- Restrictions: Foreign nationals may participate as partners, but sectors subject to foreign investment restrictions apply equally to partnership structures.

- Conversion: Conversion to a Sociedad Anónima or Compañía de Responsabilidad Limitada is permitted under the Ley de Compañías through a formal restructuring process before the SCVS.

Sub-Types

Compañía en Nombre Colectivo

All partners bear unlimited, joint, and several liability for the firm's obligations. This structure is typically used by small professional or family-run businesses where partners are closely known to one another and trust-based governance is acceptable.

Compañía en Comandita Simple

This form separates gestores, who manage the business and carry unlimited liability, from comanditarios, whose exposure is capped at their capital contribution. It suits arrangements where passive investors wish to participate financially without operational involvement.

Compañía en Comandita por Acciones

The comanditario interest is divided into transferable shares, making this form closer in capital structure to a corporation. It is used when a partnership arrangement is preferred but some degree of capital transferability is required.

Partnership structures are used primarily by family businesses, professional service providers, and closely held commercial ventures where the partners have existing relationships and accept the associated liability exposure. The principal advantage of these forms is structural simplicity with minimal capital requirements; the significant drawback is the unlimited personal liability borne by general partners, which creates meaningful financial risk.

These structures are best suited for small, closely held businesses where all partners are known to one another and the liability exposure of general partnership status is commercially acceptable.

Sole Proprietorship (Persona Natural Obligada a Llevar Contabilidad)

Operating as a sole proprietorship Ecuador Persona Natural structure means doing business under your own name as an individual, without forming a separate legal entity. This form is governed by the Código de Comercio and regulated by the Servicio de Rentas Internas (SRI), Ecuador's tax authority, which determines when an individual crosses the threshold requiring formal accounting obligations.

Once your gross income, costs, or assets exceed the thresholds set by the SRI, you become classified as a Persona Natural Obligada a Llevar Contabilidad. At that point, you must maintain full double-entry bookkeeping records and file financial statements accordingly. No separate legal personality is conferred; your personal assets remain exposed to business liabilities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated individual business | No separate legal personality from the owner |

| Owner Title | Proprietor (Persona Natural) | Single individual; no partners or shareholders |

| Liability | Unlimited personal liability | Personal assets are fully exposed to business debts |

| Local Presence | RUC registration with SRI; physical address required | Registro Único de Contribuyentes (RUC) is mandatory |

| Capital | No minimum capital requirement | No paid-up capital rules apply |

| Accounting Threshold | Set by SRI (reviewed periodically) | Triggers full bookkeeping obligations when exceeded |

Focus Points

- Taxation: Subject to personal income tax (Impuesto a la Renta) under progressive rates up to 37%; VAT obligations apply at 15% on taxable supplies; no separate corporate income tax applies.

- Compliance: Annual income tax return required; monthly or semi-monthly VAT declarations depending on activity; full double-entry accounting records must be maintained.

- Treaty Access: As an individual, access to Ecuador's double tax treaties is limited compared to corporate entities; treaty benefits depend on specific agreement terms.

- Conversion: Transition to a Cía. Ltda. or S.A. is possible but requires formal incorporation proceedings rather than a simple structural conversion.

- Restrictions: Cannot issue shares, admit partners, or raise equity capital; growth financing options are substantially narrower than for incorporated entities.

Closing

This structure suits freelancers, consultants, and small-scale traders whose operations remain owner-managed and whose liability exposure is manageable. The absence of minimum capital requirements reduces the entry barrier, but unlimited personal liability makes it unsuitable for activities carrying significant financial or legal risk.

Individuals operating small, low-risk businesses in Ecuador who require a straightforward registration without the administrative overhead of full incorporation.

How to Choose the Right Entity Type in Ecuador

Selecting how to choose business entity Ecuador structures correctly from the outset prevents costly restructuring later. Choosing the wrong form carries concrete legal and financial consequences.

Why Your Entity Choice Matters

The Ley de Compañías, administered by the Superintendencia de Compañías, Valores y Seguros (SCVS), governs which structures may lawfully conduct each category of activity.

- Registering a foreign branch while conducting activities that require local incorporation exposes the business to SCVS sanctions and potential cancellation of operating permissions.

- Selecting a structure ineligible under Ecuador's double taxation agreements means withholding tax reductions available to qualifying residents cannot be claimed.

- Forming an S.A. or Cía. Ltda. when your purpose is purely asset holding may impose annual shareholder meeting obligations and audited financial reporting requirements that a simpler arrangement would not.

- Choosing a SAS with a single shareholder when your investor base later expands may trigger mandatory conversion proceedings under SCVS regulations.

Key Factors to Consider

- Business Activity: Regulated sectors such as banking, insurance, and securities require structures specifically authorized by sectoral superintendencias, not standard SCVS-registered entities.

- Ownership Structure: A sole founder operating a consultancy fits the Persona Natural or SAS framework; multiple international shareholders typically require an S.A.

- Tax Objectives: Your eligibility for Ecuador's tax incentive regimes under the Código Orgánico de la Producción depends on entity type and sector.

- Reporting Obligations: S.A. companies above statutory thresholds must file audited financials; smaller structures carry lighter compliance burdens.

- Exit Strategy: Not all entity types permit redomiciliation or conversion without full dissolution under the Ley de Compañías — verify this before incorporating.

The full text of the Ley de Compañías is available through the SCVS official portal.

Compliance Services for Companies in Ecuador

Ongoing compliance support for Ecuadorian entities, including annual filing, SCVS reporting, and statutory obligation management.

Conclusion

Incorporating a company in Ecuador requires matching your operational model to the right legal structure under the Ley de Compañías, administered by the Superintendencia de Compañías, Valores y Seguros. The Sociedad Anónima suits larger enterprises requiring transferable share capital and broader investor access. A Compañía de Responsabilidad Limitada works for closely held businesses with a defined partner group. The Sociedad por Acciones Simplificada offers a more flexible formation process with fewer statutory formalities. Branch offices serve foreign companies maintaining direct operational presence, while representative offices are limited to non-commercial activity. Partnerships and sole proprietorships address smaller-scale or family-run arrangements.

The Cía. Ltda. remains the most registered entity type among small and medium-sized businesses. Regulatory updates in recent years signal a gradual move toward greater procedural efficiency in company formation. Expanship works directly with these structures across all formation stages.

How Expanship Can Assist You

Expanship's Ecuador company formation services cover every entity type discussed in this guide — from a Sociedad Anónima or Compañía de Responsabilidad Limitada to a Sociedad por Acciones Simplificada. Our team manages filings directly with the Superintendencia de Compañías, Valores y Seguros (SCVS), ensuring your registration follows the procedural requirements set out in the Ley de Compañías.

Beyond initial incorporation, we support the full lifecycle of your business in Ecuador:

- Document preparation, notarization, and apostille legalization

- Registered agent and registered address provision

- Government filing and SCVS liaison throughout the registration process

- Post-incorporation compliance management, including annual reporting obligations

- Tax registration with the Servicio de Rentas Internas (SRI)

- Banking introduction assistance for corporate account opening

Reach out to Expanship Ecuador to discuss your specific structure and timeline.

Frequently Asked Questions (FAQ)

The Compañía de Responsabilidad Limitada (Cía. Ltda.) is the most frequently registered entity, governed by the Ley de Compañías. Its capped shareholder structure and limited liability make it practical for small to medium-sized domestic operations.

The S.A. allows unrestricted share transfers and can access capital markets, while the Cía. Ltda. restricts transfers among participants and suits closely held businesses. Both are subject to Superintendencia de Compañías, Valores y Seguros oversight and carry comparable compliance obligations under Ecuadorian corporate law.

The Sociedad Anónima historically offered more privacy through bearer-adjacent mechanisms, though reforms have increased beneficial ownership disclosure requirements. Shareholder registers are maintained but not always fully public; nominee arrangements are legally permissible in certain structures, subject to disclosure rules under current anti-money laundering regulations.

No. The Cía. Ltda. requires a minimum of two and a maximum of fifteen participants, and partnerships require at least two partners by definition. The Sociedad por Acciones Simplificada (SAS) permits single-shareholder formation, making it the only structure a sole founder can register unilaterally.

Foreign individuals and entities may incorporate an S.A. or SAS without residency requirements, though a local legal representative is typically required for regulatory correspondence. Branch offices of foreign firms must register with the Superintendencia de Compañías and appoint a domestic legal representative under the Ley de Compañías.

The Ley de Compañías permits transformation between entity types, including conversion from a Cía. Ltda. to an S.A., subject to shareholder approval and registration with the Superintendencia de Compañías. Not all conversions follow an identical procedural path; the specific steps depend on the origin and target structure.

The S.A., Cía. Ltda., and SAS each hold separate legal personality distinct from their shareholders. General partnerships (Compañía en Nombre Colectivo) also have legal personality under the Ley de Compañías, though partners remain personally liable for obligations — a fundamental distinction from capital-based structures.

The SAS generally imposes lighter statutory requirements than the S.A. or Cía. Ltda., particularly regarding meeting formalities and capital rules. Sole proprietors registered as Persona Natural Obligada a Llevar Contabilidad face SRI reporting obligations but no corporate governance requirements.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.