Key Takeaways

- Djibouti's business registration framework is governed by the OHADA Uniform Act on Commercial Companies and administered through the Centre de Formalités des Entreprises (CFE) as the single administrative window.

- The SARL is the most commonly registered entity for small and medium enterprises in Djibouti due to its lower capital threshold and simplified governance structure compared to the SA.

- Foreign companies can enter the Djibouti market through a Branch or Representative Office without establishing a separate legal entity, offering a lower-commitment alternative to full incorporation.

- Djibouti operates a territorial tax system under which income sourced outside the country is generally not subject to domestic corporate tax.

Introduction to Entity Types in Djibouti

Djibouti is a small sovereign republic in the Horn of Africa, bordered by Eritrea, Ethiopia, and Somalia, with coastline along the Red Sea and the Gulf of Aden. Its geographic position at one of the world's busiest maritime chokepoints has shaped its economy around trade, logistics, and port services. Understanding the types of business entities in Djibouti begins with the regulatory framework: company registration falls under the jurisdiction of the Centre de Formalités des Entreprises (CFE), which operates as the single administrative window for business formation.

Djibouti applies a territorial tax system, meaning income sourced outside the country is generally not subject to domestic corporate tax.

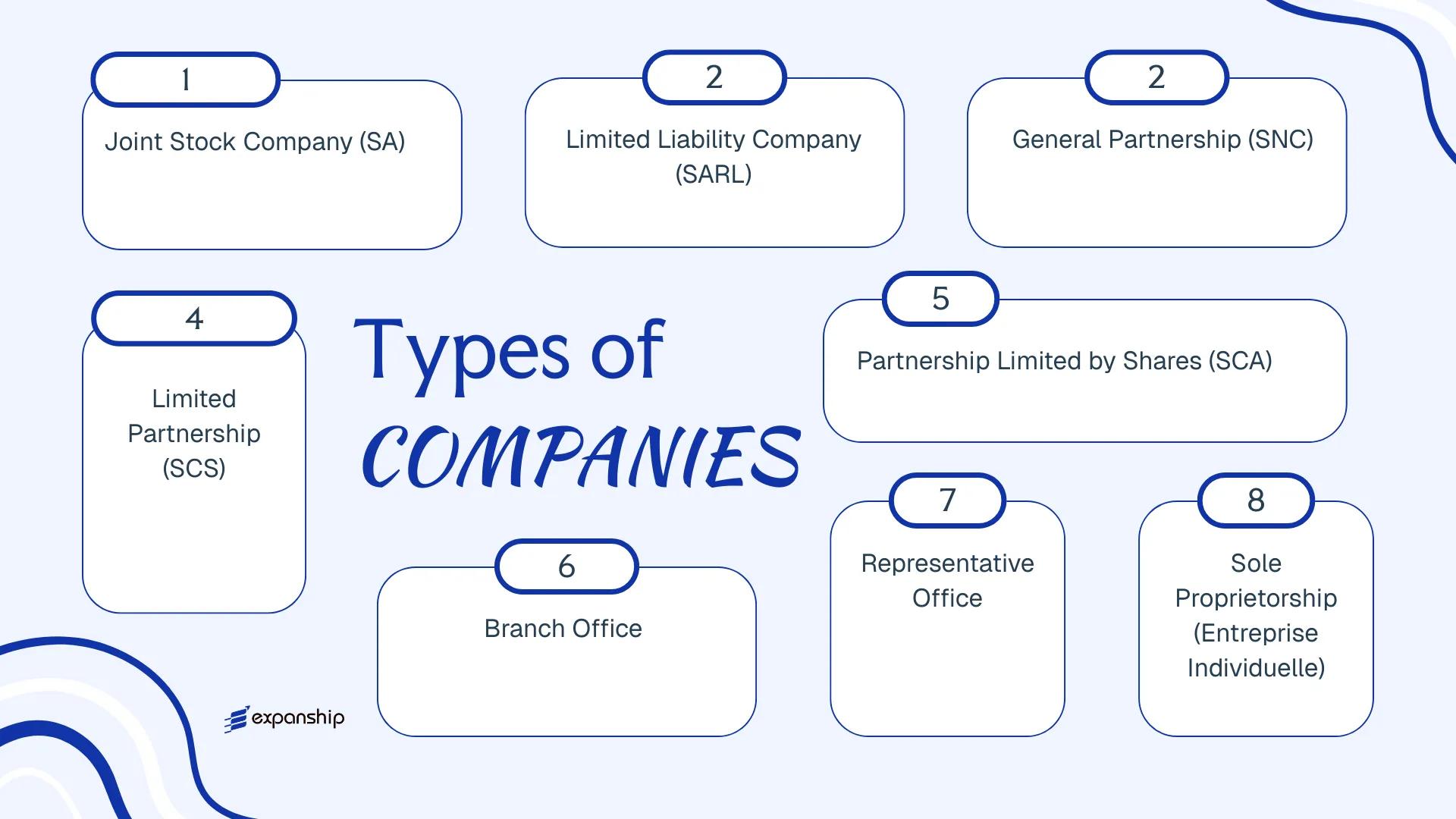

Businesses incorporating there can choose from several legal forms, each governed primarily by the OHADA Uniform Act on Commercial Companies, which Djibouti adopted as part of its membership in the Organisation pour l'Harmonisation en Afrique du Droit des Affaires. Available structures include the Société Anonyme (SA), Société à Responsabilité Limitée (SARL), Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA), Branch Office, Representative Office, and the Entreprise Individuelle. Each of these Djibouti company types carries distinct requirements around capital, liability, and governance, all of which this article examines in detail.

An Overview of Business Structures in Djibouti

Djibouti's company law framework provides several distinct entity types for businesses operating within or from the country. The primary legislation governing these structures is the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, which Djibouti adopted as a member state of the Organisation for the Harmonisation of Business Law in Africa. Each entity type carries different implications for liability, governance, and capital requirements.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Société Anonyme (SA) | Corporation | Limited to share capital | Taxed | Yes | 1 shareholder | CEPEX / RCCM | OHADA Uniform Act |

| Société à Responsabilité Limitée (SARL) | Private limited company | Limited to contribution | Taxed | Yes | 1 member | RCCM | OHADA Uniform Act |

| Société en Nom Collectif (SNC) | General partnership | Unlimited, joint | Taxed | Yes | 2 partners | RCCM | OHADA Uniform Act |

| Société en Commandite Simple (SCS) | Limited partnership | Mixed | Taxed | Yes | 2 partners | RCCM | OHADA Uniform Act |

| Société en Commandite par Actions (SCA) | Partnership limited by shares | Mixed | Taxed | Yes | 4 members | RCCM | OHADA Uniform Act |

| Branch Office | Foreign extension | Parent liable | Taxed | Yes | N/A | RCCM | OHADA / Local regulation |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | No | N/A | RCCM | Local regulation |

| Entreprise Individuelle | Sole proprietorship | Unlimited, personal | Taxed | Yes | 1 person | RCCM | OHADA / Local law |

Each of these structures is examined in full in the sections below.

Société Anonyme (SA)

Société Anonyme SA Djibouti formation is governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups (AUDSCGIE), which Djibouti adopted as a member state of the Organisation pour l'Harmonisation en Afrique du Droit des Affaires. The SA carries full separate legal personality, meaning the entity itself holds rights and obligations distinct from its shareholders.

Liability is capped at each shareholder's capital contribution. This structure suits larger operations or those seeking to raise capital through share issuance, and it allows for a tiered governance model with a board of directors or an administrative board, depending on the elected structure.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (Joint Stock Company) | Incorporated under the OHADA AUDSCGIE |

| Members | Minimum 1 shareholder; no maximum | Shareholders may be natural or legal persons, resident or foreign |

| Governance | Board of Directors (min. 3, max. 12) or single Administrator if sole shareholder | Board members need not be Djiboutian nationals |

| Local Presence | Registered office in Djibouti required | No mandatory local director, but a registered address is compulsory |

| Share Capital | Minimum DJF 1,000,000 (approx. USD 5,600) | At least 50% paid up on incorporation; remainder within two years |

| Privacy | Shareholder register is not publicly filed, but articles and directors are registered with the RCCM | Beneficial ownership disclosure requirements may apply |

Focus Points

- Taxation: Corporate income tax applies at the standard rate; VAT is levied on taxable supplies; no withholding tax framework comparable to OECD countries exists, though dividend distributions may attract local levies under domestic rules.

- Annual Compliance: Audited financial statements are mandatory; at least one statutory auditor (commissaire aux comptes) must be appointed and cannot be a company insider.

- Economic Substance: No formal substance legislation equivalent to Gulf jurisdictions, but physical presence implied by registered office requirements and OHADA governance obligations.

- Treaty Access: Djibouti's double tax treaty network is limited; SA status does not automatically confer treaty benefits without reviewing bilateral agreements in force.

- Conversion: An SA may be converted to a SARL or other OHADA-recognised form by shareholder resolution, subject to compliance with applicable capital and membership thresholds.

Closing

The SA suits holding structures, larger trading entities, and businesses intending to attract institutional investment or multiple shareholders. The mandatory statutory auditor and higher minimum capital set a compliance floor that smaller ventures may find disproportionate.

The SA is most appropriate for mid-to-large enterprises, joint ventures with institutional partners, or businesses planning future capital raises requiring a recognised share structure.

Company Incorporation in Djibouti

Incorporate your Société Anonyme or other entity type in Djibouti with end-to-end support from Expanship.

Société à Responsabilité Limitée (SARL)

The Société à Responsabilité Limitée (SARL) in Djibouti is governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, which Djibouti adopted as part of its integration into the OHADA legal framework. The entity carries separate legal personality, meaning it is legally distinct from its members, whose financial exposure is confined to their capital contributions.

This hybrid structure sits between a partnership and a fully public company. Its governance is less formal than a Société Anonyme, making it a practical option for closely held businesses, family-owned enterprises, and small to medium commercial operations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Governed under OHADA Uniform Act |

| Members | 1 to 50 associés (shareholders) | A single-member variant is permitted |

| Management | One or more gérants (managers) | Need not be a shareholder; no nationality restriction specified under OHADA |

| Registered Office | Physical address required in Djibouti | Must be maintained for official correspondence |

| Share Capital | No statutory minimum under revised OHADA rules | Capital must be fully subscribed at formation |

| Privacy | Shareholder details filed with the RCCM | Not publicly searchable in the same manner as listed entities |

Focus Points

- Taxation: Subject to corporate income tax; VAT applies to taxable supplies; withholding tax applies to dividends and certain service payments to non-residents; no specific SARL-level exemptions under general tax law.

- Annual Compliance: Financial statements must be filed with the Registre du Commerce et du Crédit Mobilier (RCCM); general assembly of members required annually.

- Economic Substance: No formal substance regime modelled on offshore frameworks, but a registered office and operational presence are expected.

- Treaty Access: Djibouti's limited tax treaty network means treaty benefits are not broadly available to SARL entities.

- Conversion: A SARL may be converted to an SA if shareholder thresholds or capital requirements make that structure more appropriate.

Closing

The SARL suits trading companies, service businesses, and local subsidiaries of foreign groups seeking limited liability without the administrative burden of a full SA structure. Its principal constraint is the 50-member cap, which limits its utility for entities anticipating broad equity participation.

The SARL is best suited for small to medium-sized businesses, including foreign-owned local subsidiaries, that require limited liability and a straightforward governance structure without the formalities of a public company.

Partnerships in Djibouti [Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA)]

Partnership structures in Djibouti — SNC, SCS, and SCA — are governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups (Acte Uniforme relatif au droit des sociétés commerciales et du groupement d'intérêt économique), which Djibouti adopted as part of its integration into the OHADA legal framework. Each form carries distinct liability profiles and membership configurations.

The SNC (Société en Nom Collectif) is a general partnership where all partners bear unlimited, joint, and several liability for the firm's debts. The SCS and SCA are commandite structures that split membership into general partners with unlimited liability and limited partners whose exposure is capped at their capital contribution.

Key Characteristics

| Requirement | SNC | SCS | SCA |

|---|---|---|---|

| Legal Form | General Partnership | Limited Partnership (simple) | Limited Partnership with Shares |

| Members | 2+ associés (no maximum); all are general partners | 2+ members: at least 1 general partner (commandité), 1 limited partner (commanditaire) | 4+ members: at least 1 general partner, 3 limited shareholders |

| Liability | Unlimited for all partners | Unlimited for commandités; limited for commanditaires | Unlimited for commandités; limited for commanditaires |

| Capital | No statutory minimum under OHADA; denominated in DJF | No statutory minimum | Minimum share capital required; shares freely transferable among commanditaires |

| Local Presence | Registered office in Djibouti required | Registered office in Djibouti required | Registered office in Djibouti required |

| Privacy | Partner names appear in public registry filings | General partner names disclosed; limited partners may have reduced exposure | General partner names disclosed publicly |

Focus Points

- Taxation: Partnerships are generally treated as fiscally transparent or subject to corporate income tax depending on structure; consult the Direction Générale des Impôts for applicable rates on business income, and note that VAT obligations apply to taxable commercial activities.

- Annual Compliance: Entities must file annual accounts with the Registre du Commerce et des Sociétés (RCRCS) and hold partner meetings in accordance with the OHADA Uniform Act.

- Conversion: An SNC may be converted into an SARL or SA subject to unanimous partner consent and compliance with OHADA conversion procedures.

- Restrictions: Non-OHADA foreign nationals acting as general partners must verify local licensing and residency requirements under Djiboutian commercial law.

- Treaty Access: Access to Djibouti's bilateral investment and tax treaties depends on the entity's tax residency status and whether the structure is treated as opaque or transparent for treaty purposes.

Sub-Types

Société en Nom Collectif (SNC)

The SNC is the baseline general partnership form under OHADA, used primarily by small professional or family-run businesses where all parties are willing to accept joint unlimited liability. No shares are issued; ownership interests are transferred only with unanimous partner consent.

Société en Commandite Simple (SCS)

The SCS separates active management (vested in commandités) from passive investment (commanditaires), making it suitable for arrangements where investors want limited exposure without taking on managerial responsibility.

Société en Commandite par Actions (SCA)

The SCA functions similarly to the SCS but issues negotiable shares to limited partners, allowing for broader capital-raising among commanditaires while keeping control with the general partner group. It is structurally closer to a public-facing vehicle.

Closing

Partnership structures suit closely-held commercial ventures, family businesses, and investment arrangements where tiered liability is a deliberate structural choice — though the unlimited liability carried by general partners in all three forms remains a significant exposure that requires careful consideration before formation.

These structures are best suited for closely-held businesses or joint ventures where the partners have established trust and are prepared to accept the liability consequences of the general partner role.

Foreign Business Establishments in Djibouti [Branch Office, Representative Office]

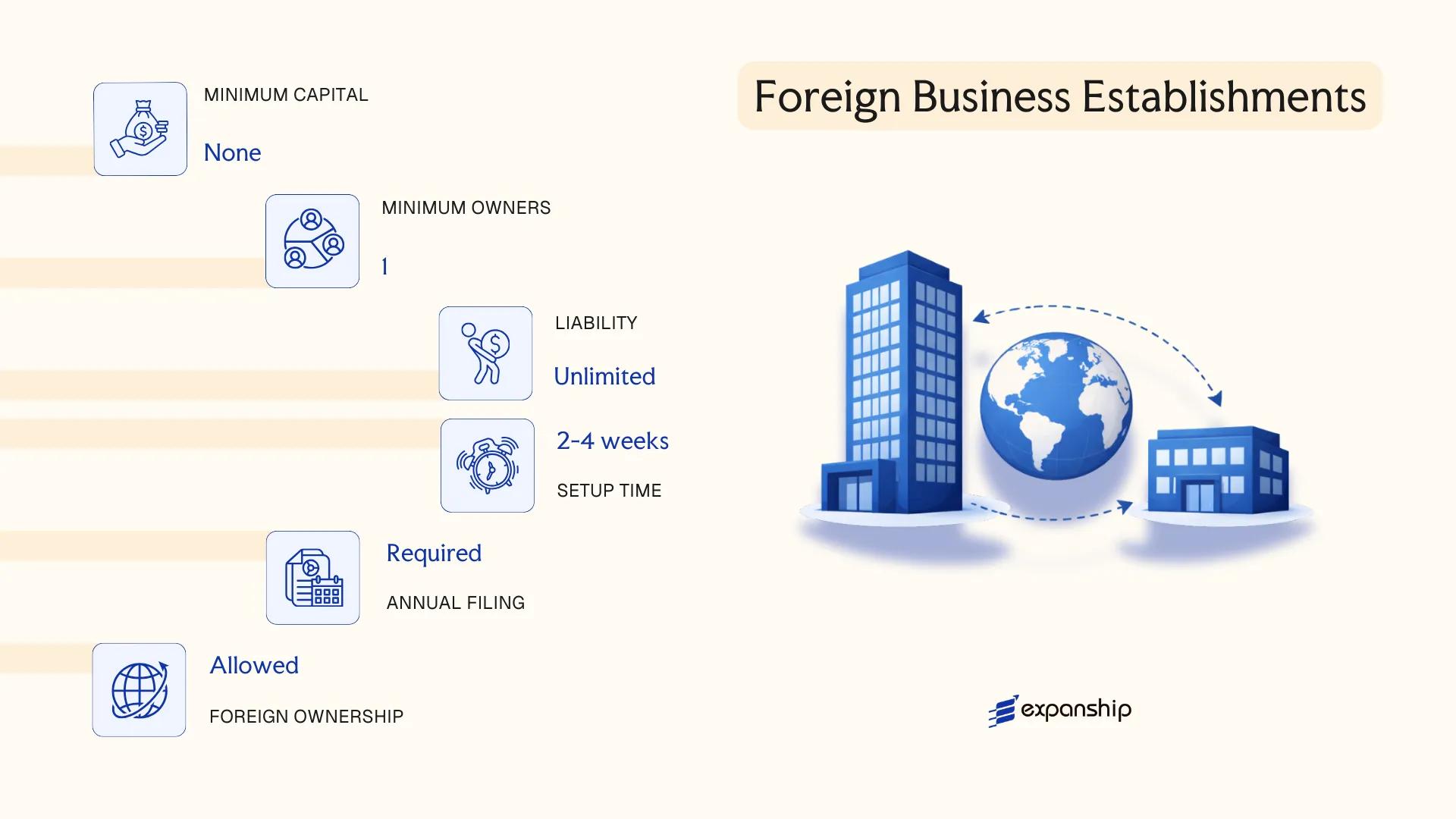

A foreign company branch office in Djibouti allows an overseas parent to conduct commercial activities directly, without forming a separate legal entity. Governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, a branch carries no independent legal personality — liability flows back to the parent company. Registration is processed through the Djibouti One Stop Shop (Guichet Unique), which coordinates approvals across the relevant ministries.

A representative office operates under a more limited mandate. It may carry out market research, liaison, and promotional activities on behalf of the parent, but cannot generate revenue or enter into commercial contracts in its own name.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Commercial Activity | Permitted | Not permitted |

| Personnel | Resident manager required | Liaison staff only |

| Local Presence | Registered address in Djibouti required | Registered address required |

| Capital Requirement | No minimum; parent's capital applies | None |

| Liability | Parent bears full liability | Parent bears full liability |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at the standard rate; VAT obligations apply where taxable supplies are made; withholding tax may apply on remittances to the parent depending on treaty status.

- Treaty access: Access to Djibouti's double tax treaties, where applicable, may be limited since neither structure is a separate resident entity.

- Annual compliance: Branches must file audited accounts and renew their registration annually with the Guichet Unique.

- Restrictions: Representative offices cannot invoice clients or sign commercial contracts; any revenue-generating activity requires conversion to a branch or locally incorporated entity.

- Conversion: Upgrading a representative office to a branch, or a branch to a locally incorporated company, requires a fresh registration process rather than a structural amendment.

Closing

Both structures suit firms testing market entry or maintaining a controlled operational footprint without committing to full local incorporation. The branch offers genuine commercial capacity, while the representative office's inability to generate revenue limits its utility to preliminary or support functions.

Established foreign firms seeking a direct, revenue-generating presence without a locally incorporated subsidiary — particularly those in trading, logistics, or services — will find the branch structure the more practical of the two options.

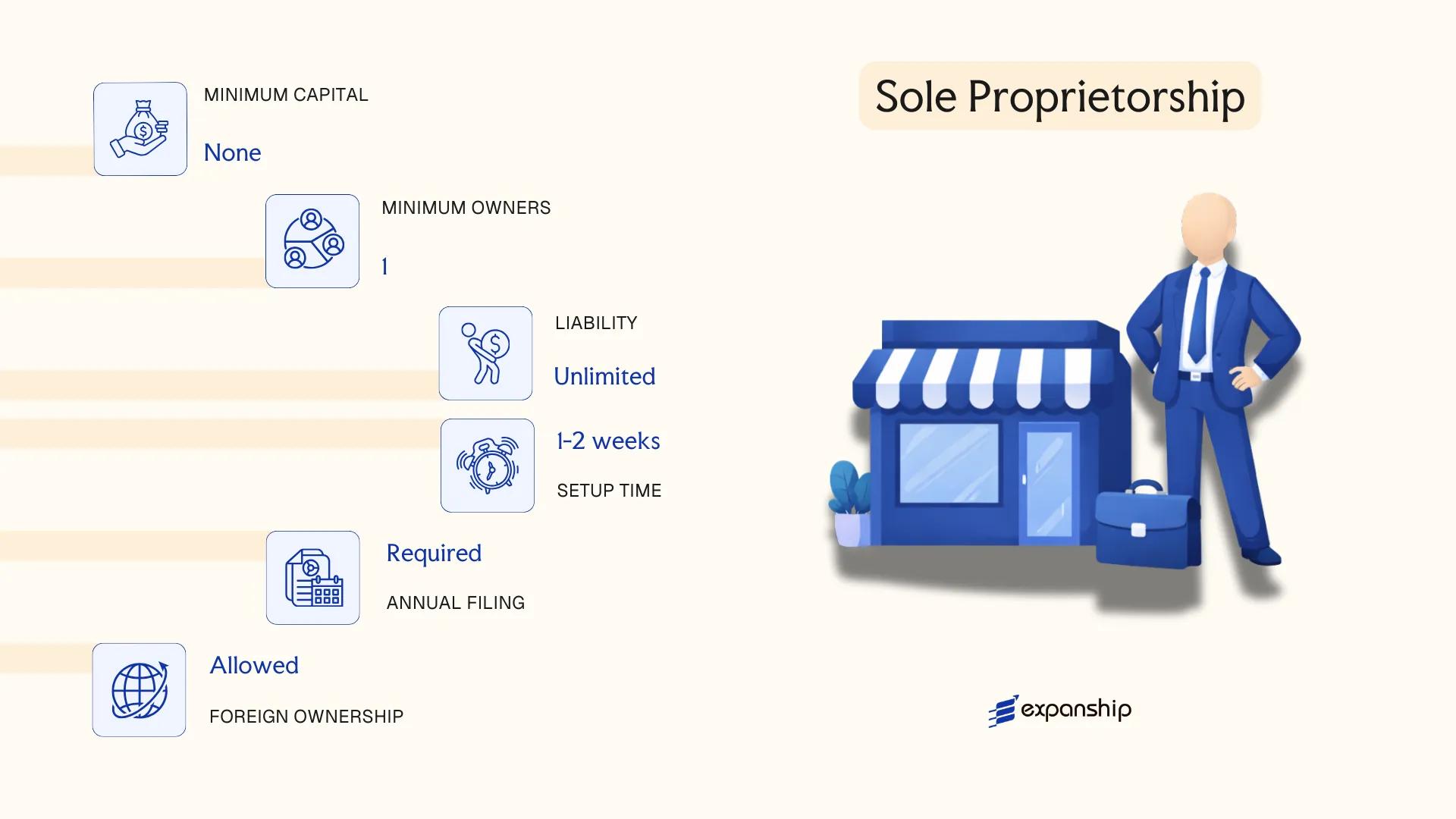

Sole Proprietorship (Entreprise Individuelle)

The sole proprietorship Djibouti Entreprise Individuelle is governed by the OHADA Uniform Act relating to General Commercial Law, which Djibouti adopted as part of its integration into the Organisation pour l'Harmonisation en Afrique du Droit des Affaires legal framework. Under this structure, the business has no separate legal personality from its owner — the individual and the enterprise are treated as a single legal unit.

Liability is unlimited, meaning personal assets are exposed to business debts and obligations. Registration is handled through the Centre de Formalités des Entreprises (CFE), which serves as the single administrative window for Djibouti self-employed business registration.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Entreprise Individuelle) | No separate legal personality |

| Member Designation | Proprietor | Single individual only; no partners or shareholders |

| Membership | 1 proprietor (minimum and maximum) | Natural persons only; legal entities cannot be proprietors |

| Local Presence | Registered business address required | Must be declared at CFE registration |

| Capital | No statutory minimum capital | Francs Djiboutiens (DJF); proprietor's own assets constitute operational capital |

| Liability | Unlimited personal liability | Personal and business assets are legally indistinct |

Focus Points

- Taxation: Subject to the Impôt sur le Revenu des Personnes Physiques (IRPP) on net business income; VAT registration applies once turnover exceeds the applicable threshold under Djiboutian tax law; no corporate income tax applies.

- Annual Compliance: Must maintain accounting records per OHADA standards and file annual income declarations with the Direction des Impôts.

- Treaty Access: As an unincorporated structure, the enterprise does not independently access double taxation treaties; relief depends on the proprietor's personal tax residency status.

- Conversion: Can be converted into a SARL or SA if the business grows, though this requires a formal dissolution and re-registration process.

- Restrictions: Foreign nationals face additional administrative requirements and may require a professional card (carte de commerçant étranger) to operate legally.

Closing

The Entreprise Individuelle suits low-volume trading, freelance services, and small-scale retail activities where administrative simplicity outweighs the need for liability protection. Its primary advantage is ease and speed of registration through the CFE; its core drawback is full personal exposure to business liabilities with no legal separation.

This structure is most appropriate for individual residents or qualified foreign nationals operating a small, low-risk commercial or service-based activity with limited external financing needs.

How to Choose the Right Entity Type in Djibouti

Choosing the right company structure in Djibouti has direct legal and financial consequences — the decision affects your tax position, liability exposure, compliance obligations, and operational permissions from day one.

Why Your Entity Choice Matters

Selecting the wrong structure is not merely an administrative inconvenience. Concrete outcomes include:

- Registering as a foreign branch when you intend to conduct standalone commercial activity can result in regulatory non-compliance under the OHADA Uniform Act on Commercial Companies, exposing the business to administrative penalties or forced dissolution.

- Choosing a structure ineligible for treaty benefits means withholding taxes levied by counterpart jurisdictions cannot be reduced, increasing the effective cost of cross-border payments.

- Forming a capital company such as an SA when your activity is a single-person consultancy creates mandatory governance obligations — including a board and statutory auditor — that generate recurring costs disproportionate to your scale.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each correspond to distinct legal structures under the OHADA Uniform Act on Commercial Companies and Economic Interest Groups.

- Ownership Structure: A sole owner operating with minimal capital requirements is better served by an SARL, while multi-investor ventures expecting public capital raises require an SA.

- Tax Objectives: Your eligibility for Djibouti's free zone tax exemptions or the standard corporate tax regime depends partly on entity type and registered location.

- Management Flexibility: Partnerships such as the SNC allow contractual management arrangements, whereas capital companies impose statutory governance frameworks.

- Exit Strategy: Not all structures permit redomiciliation or conversion; confirm whether your chosen form allows dissolution, merger, or transformation under applicable OHADA provisions.

Compliance Services for Companies in Djibouti

Maintain good standing and meet ongoing regulatory obligations for your Djibouti entity.

Conclusion

Djibouti's legal framework for business registration draws from French civil law traditions and is administered under the OHADA treaty framework, which gives the jurisdiction a degree of predictability for foreign investors familiar with Francophone commercial law.

Each entity serves a distinct function. The SA suits larger operations requiring share capital structures and institutional investment. The SARL remains the most commonly registered form for small and medium enterprises, given its lower capital threshold and simpler governance requirements. Partnerships such as the SNC and SCS are reserved for operators who accept personal liability in exchange for structural flexibility. A Branch or Representative Office addresses foreign firms testing the market without establishing a separate legal entity. The Entreprise Individuelle is suited to individual traders operating without partners.

Djibouti's ongoing positioning as a Horn of Africa trade hub continues to shape its regulatory approach, with gradual alignment to international compliance standards influencing how businesses incorporating here are structured and reported.

How Expanship Can Assist You

Expanship company registration services Djibouti cover the full process of forming an SA, SARL, branch office, or any other structure discussed in this guide. From preparing your founding documents to filing with the Centre de Formalités des Entreprises (CFE) and satisfying the requirements of the Tribunal de Commerce de Djibouti, your incorporation is handled with accuracy and accountability.

Beyond initial registration, our scope as a Djibouti corporate services provider extends to the ongoing obligations your entity will face once operational:

- Document preparation, notarization, and legalization

- Registered agent and local office address provision

- Government filing and registrar liaison

- Post-incorporation compliance management

- Banking introduction assistance

Professional company formation in Djibouti requires local knowledge that goes beyond a checklist. Expanship Djibouti incorporation support gives you direct access to that knowledge at every stage.

Contact Expanship Djibouti to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is the most frequently registered business structure. Its lower minimum capital requirement and simpler governance rules make it accessible to small and medium-sized businesses compared to the Société Anonyme (SA).

A branch office has no separate legal personality and its foreign parent bears full liability for its Djiboutian operations, whereas a SARL is an independent legal entity that limits liability to contributed capital. From a tax standpoint, both are subject to local corporate tax on Djibouti-sourced income, but a SARL can trade freely with local residents while a branch's permitted activities are typically tied to the parent's scope.

Among available structures, the SARL generally involves fewer public disclosure requirements than the SA, whose shareholder register and board composition are subject to broader reporting obligations. Nominee arrangements are not formally regulated under Djiboutian corporate law, so their practical availability depends on service provider terms rather than a statutory framework.

No. Partnerships — the Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), and Société en Commandite par Actions (SCA) — require at least two partners by definition under OHADA rules. A sole individual can form a SARL or an Entreprise Individuelle, but cannot satisfy the multi-party requirement for any partnership form.

Foreign investors may form an SA, SARL, or establish a branch or representative office. The Centre de Formalités des Entreprises (CFE) processes registrations for foreign-owned entities, and there is no statutory requirement for a local shareholder in an SA or SARL. A representative office, however, cannot generate local revenue.

Conversion is generally permitted under OHADA principles, most commonly from a SARL to an SA when a business grows and requires access to equity capital markets or a larger shareholder base. The process requires a formal resolution, updated constitutional documents, and re-registration with the relevant commercial registry.

Not all. The SA, SARL, SCA, and SCS (in its commandite structure) hold separate legal personality, whereas the SNC does not create a liability shield — partners remain personally and jointly liable for firm debts. The Entreprise Individuelle is not a separate legal entity at all; the owner and the business are legally the same person.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.