Key Takeaways

- The Naamloze Vennootschap (NV) and Besloten Vennootschap (BV) are the two primary limited liability structures in Curaçao, with the BV serving as the most commonly chosen vehicle for both resident and non-resident private investors.

- Curaçao operates a territorial tax system under which foreign-sourced income may be excluded from local taxation under certain conditions, a feature that directly influences entity selection for internationally oriented businesses.

- Partnerships such as the Vennootschap onder Firma (VOF) and Maatschap expose general partners to unlimited personal liability, limiting their commercial appeal for ventures seeking external investment.

- All business entities in Curaçao must register with the Kamer van Koophandel, while those operating in financial services face additional regulatory oversight from the Central Bank of Curaçao and Sint Maarten (CBCS).

Introduction to Entity Types in Curaçao

Curaçao is an island in the southern Caribbean Sea, situated approximately 65 kilometres off the northern coast of Venezuela and forming part of the ABC islands alongside Aruba and Bonaire. Since 2010, it has functioned as an autonomous country within the Kingdom of the Netherlands, operating under its own civil and commercial legal framework derived from Dutch law.

Company registration and maintenance fall under the jurisdiction of the Curaçao Chamber of Commerce and Industry (Kamer van Koophandel), which administers the commercial registry. Entities operating in financial services are additionally subject to oversight by the Central Bank of Curaçao and Sint Maarten (CBCS). The territory operates a territorial tax system, meaning foreign-sourced income may be excluded from local taxation under certain conditions.

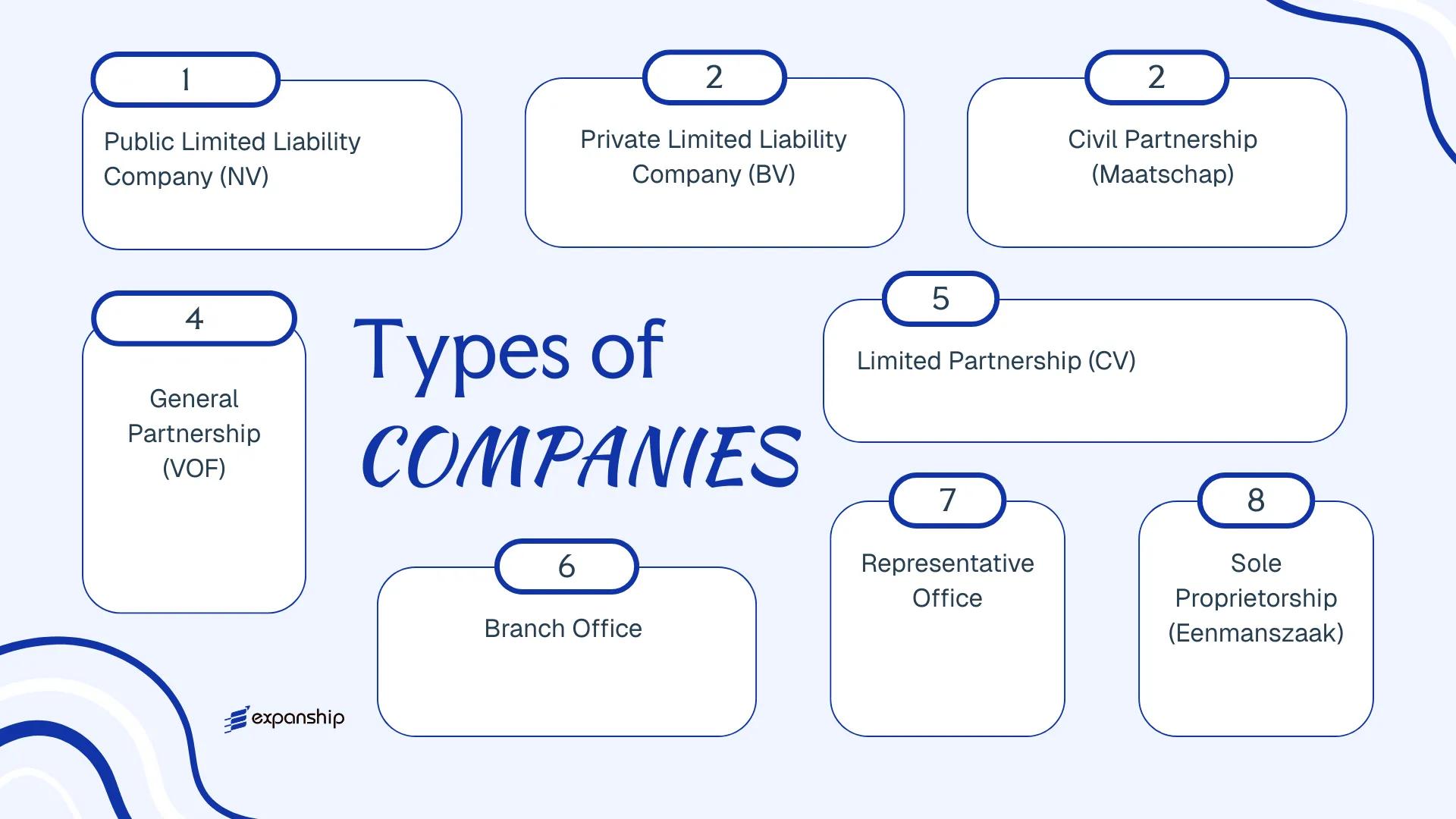

The types of business entities in Curaçao available to local and foreign investors include the Naamloze Vennootschap (NV), Besloten Vennootschap (BV), Maatschap, Vennootschap onder Firma (VOF), Commanditaire Vennootschap (CV), branch office, representative office, and sole proprietorship (Eenmanszaak). Each structure carries distinct liability, governance, and tax treatment characteristics that this article examines in detail.

An Overview of Business Structures in Curaçao

Curaçao company law recognises several distinct legal forms, each governed primarily by the Civil Code of Curaçao (Burgerlijk Wetboek van Curaçao) and, for corporate entities, the National Ordinance on Formal Requirements (Landsverordening op de Formeel Vereisten). The business structures available in Curaçao range from incorporated companies with limited liability to unincorporated partnerships and sole traders. Each form carries different implications for liability, taxation, governance, and permitted activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Naamloze Vennootschap (NV) | Corporation | Limited | Taxed (profit tax) | Permitted | 1 shareholder | Chamber of Commerce (KvK) | Civil Code of Curaçao |

| Besloten Vennootschap (BV) | Private company | Limited | Taxed (profit tax) | Permitted | 1 shareholder | Chamber of Commerce (KvK) | Civil Code of Curaçao |

| Maatschap | Civil partnership | Unlimited | Pass-through | Restricted | 2 partners | Chamber of Commerce (KvK) | Civil Code of Curaçao |

| Vennootschap onder Firma (VOF) | General partnership | Unlimited | Pass-through | Permitted | 2 partners | Chamber of Commerce (KvK) | Civil Code of Curaçao |

| Commanditaire Vennootschap (CV) | Limited partnership | Mixed | Pass-through | Permitted | 2 partners | Chamber of Commerce (KvK) | Civil Code of Curaçao |

| Branch Office | Foreign entity extension | Parent liable | Taxed on local income | Permitted | N/A | Chamber of Commerce (KvK) | Civil Code of Curaçao |

| Representative Office | Foreign entity extension | Parent liable | Generally exempt | Not permitted | N/A | Chamber of Commerce (KvK) | Civil Code of Curaçao |

| Eenmanszaak | Sole proprietorship | Unlimited | Personal income tax | Permitted | 1 owner | Chamber of Commerce (KvK) | Civil Code of Curaçao |

Each of these structures is examined in full in the sections below.

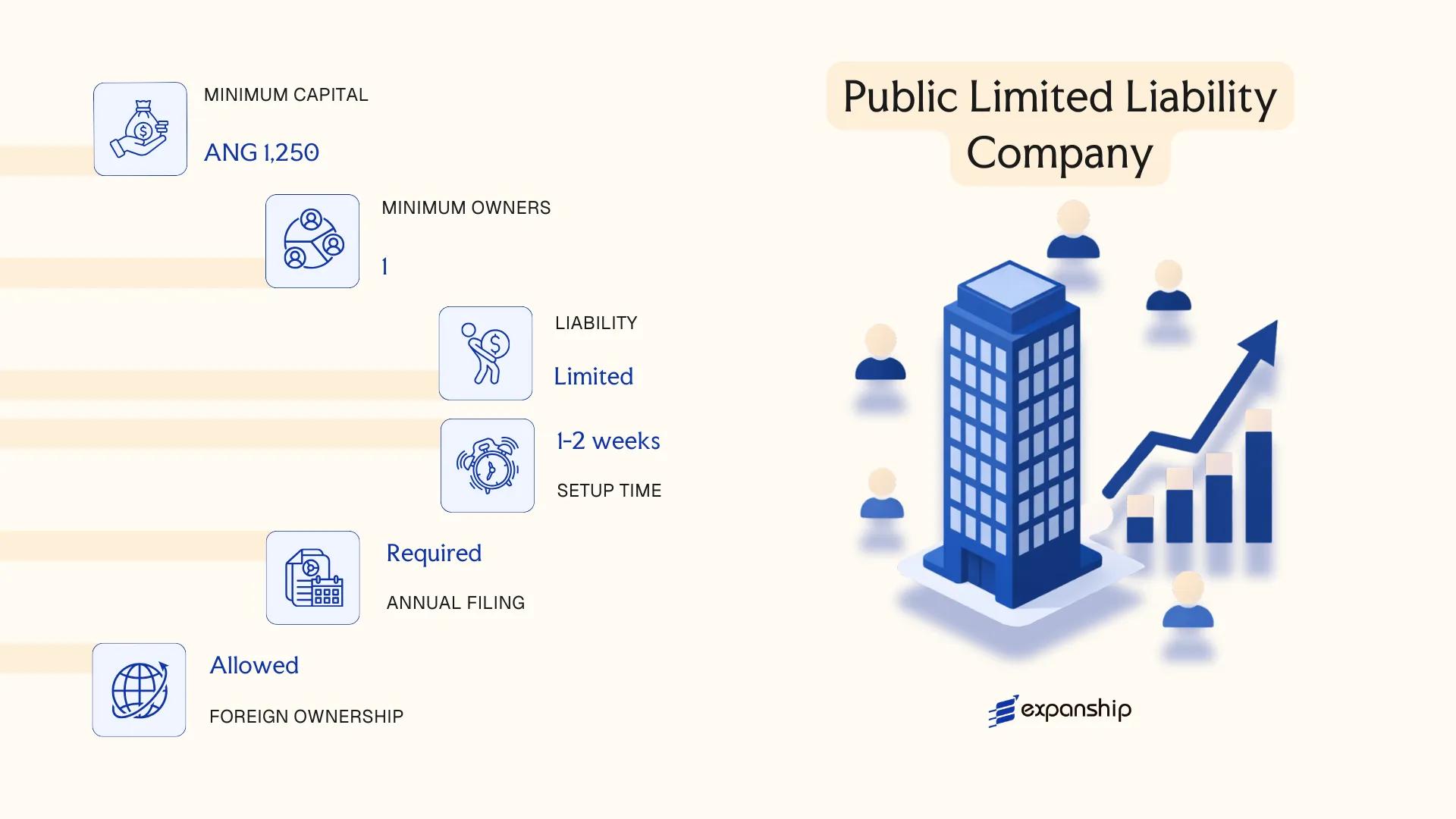

Naamloze Vennootschap (NV) — Public Limited Liability Company

Governed by the Curaçao Civil Code and the National Ordinance on Corporations, the Naamloze Vennootschap is the foundational corporate form for Curaçao NV naamloze vennootschap formation. It holds separate legal personality, meaning the entity itself — not its shareholders — bears legal and financial obligations.

Shares in an NV can be issued to the public and are freely transferable by default, which distinguishes it structurally from its private counterpart. This transferability, combined with limited liability, makes the NV a versatile vehicle for both domestic operations and cross-border structures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Naamloze Vennootschap (NV) | Separate legal personality; limited liability applies |

| Members | Shareholders (min. 1); Directors (min. 1) | No maximum shareholder cap; corporate directors permitted |

| Local Presence | Registered office in Curaçao required | Registered agent not mandatory by statute, but a local address must be maintained |

| Share Capital | ANG 40,000 minimum authorized capital; 20% must be paid-up at incorporation | Shares may be issued in multiple classes |

| Privacy | Shareholders not disclosed in public registry | Directors appear in the Chamber of Commerce register |

Focus Points

- Taxation: Subject to corporate profit tax at a standard rate of 22%; dividend withholding tax applies at 0–15% depending on structure; no capital gains tax in most cases; VAT (turnover tax) applies to local supplies.

- Economic Substance: NVs conducting relevant activities must meet substance requirements under the National Ordinance on Economic Substance.

- Annual Compliance: Annual accounts must be filed; financial statements may require an audit depending on size thresholds.

- Treaty Access: Curaçao maintains a Tax Information Exchange Agreement (TIEA) network and a limited tax treaty framework; treaty benefits are structure-dependent.

- Conversion: An NV can be converted into a BV without liquidation under Curaçao corporate law.

Closing

The NV suits holding structures, publicly offered investment vehicles, and businesses requiring freely transferable shares across multiple investor classes. Its primary advantage is unrestricted share transferability; the main drawback is a comparatively higher administrative and compliance burden relative to a private entity.

The NV is most appropriate for institutional investors, multi-shareholder group holding structures, or businesses intending to raise capital from more than one class of external investor.

Company Incorporation in Curaçao

Incorporate your Naamloze Vennootschap (NV) or other business entity in Curaçao with end-to-end support from Expanship.

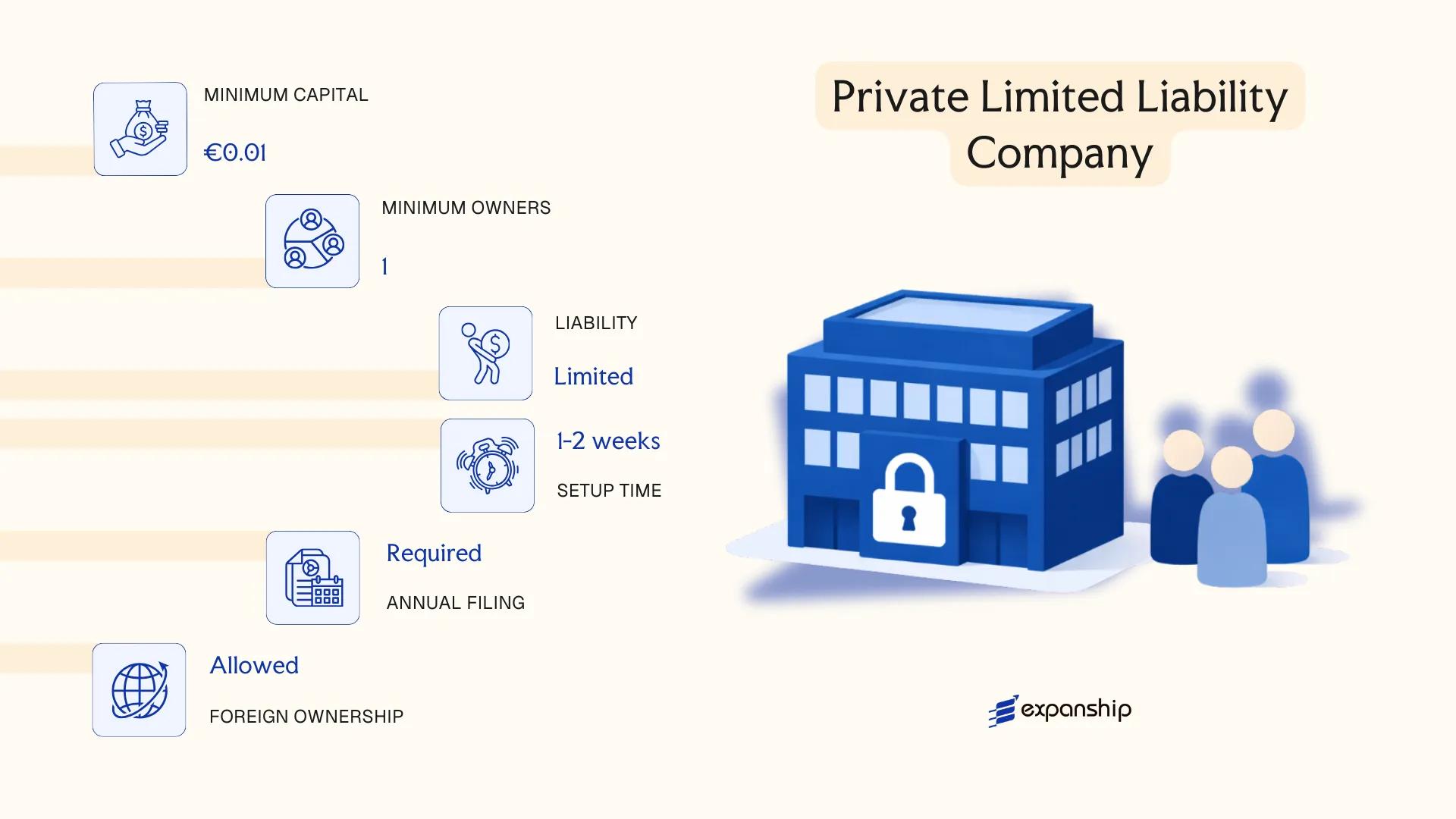

Besloten Vennootschap (BV) — Private Limited Liability Company

Curaçao BV besloten vennootschap registration is governed by the Curaçao Civil Code (Burgerlijk Wetboek van Curaçao), which came into force following the island's constitutional separation from the Netherlands Antilles in 2010. The BV carries separate legal personality, meaning the entity bears its own rights and obligations distinct from those of its shareholders.

Liability is limited to each shareholder's capital contribution. This structure suits closely held businesses, family-owned enterprises, and international holding arrangements where privacy and control over share transfers are priorities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited liability company | Shares are not publicly tradeable |

| Members | Shareholders (min. 1, no maximum); min. 1 Director | Director may be a legal entity; no nationality requirement |

| Local Presence | Registered office address in Curaçao required | Registered agent not legally mandated but standard in practice |

| Share Capital | No statutory minimum; denominated in any currency | Shares may have no par value under the Civil Code |

| Share Transfer | Restricted by deed; subject to approval clauses in articles | Transfer restrictions must be specified in the deed of incorporation |

| Privacy | Shareholder register not publicly disclosed | Directors appear in the Chamber of Commerce (KvK) registration |

Focus Points

- Taxation: Subject to 22% corporate income tax; profit tax exemptions may apply under the participation exemption regime; dividends to foreign shareholders attract a 0% or reduced withholding tax depending on applicable arrangements; no VAT on most financial and holding activities, though a turnover tax (OB) applies to local trading activities.

- Economic Substance: BVs engaged in qualifying activities must meet substance requirements under the National Ordinance on Economic Substance, including local management, qualified staff, and adequate operating expenditure.

- Annual Compliance: Annual financial statements required; audit obligations depend on size thresholds; annual profit tax return filed with the Tax Authority (Inspectie der Belastingen).

- Treaty Access: Curaçao maintains a Tax Information Exchange Agreement (TIEA) network and a tax arrangement with the Netherlands (BRK), which governs dividend, interest, and royalty flows between the two jurisdictions.

Closing

The BV is commonly used for holding structures, intra-group financing, and IP ownership, benefiting from the participation exemption on qualifying dividend income. Its primary limitation is that share transfers require a notarial deed, which adds time and cost compared to more flexible structures.

The Curaçao private limited company BV structure is most appropriate for closely held businesses, international holding companies, and entrepreneurs seeking liability protection with controlled share transferability.

Partnerships in Curaçao [Maatschap (Civil Partnership), Vennootschap onder Firma/VOF (General Partnership), Commanditaire Vennootschap/CV (Limited Partnership)]

Curaçao recognises three partnership structures, each governed by the Civil Code of Curaçao (Burgerlijk Wetboek van Curaçao): the Maatschap (civil partnership), the Vennootschap onder Firma (VOF, general partnership), and the Commanditaire Vennootschap (CV). None of these forms possess separate legal personality under Dutch Caribbean civil law, meaning partners bear personal exposure to the entity's obligations to varying degrees depending on the structure.

The Curaçao CV commanditaire vennootschap structure is the most commercially significant of the three, particularly for international holding and investment arrangements. Registration is handled through the Kamer van Koophandel (Chamber of Commerce), and the partnership agreement governs internal relations between partners.

Key Characteristics

| Requirement | Maatschap | VOF | CV |

|---|---|---|---|

| Legal Form | Civil partnership; no separate legal personality | Commercial general partnership; no separate legal personality | Limited partnership; no separate legal personality |

| Members | Partners (minimum 2, no maximum) | Partners (minimum 2, no maximum) | General partner (min. 1) + limited partner (min. 1); no maximum |

| Liability | All partners: unlimited, joint liability | All partners: unlimited, joint and several liability | General partner: unlimited; limited partner: capped at contribution |

| Local Presence | Registration with Chamber of Commerce required | Registered office address required | Registered office address required |

| Capital | No statutory minimum; contributions may be cash, labour, or assets | No statutory minimum | No statutory minimum; limited partner's contribution defines liability cap |

| Privacy | Partnership agreement is private; partner names appear in Chamber of Commerce register | Partner names publicly registered | General partner publicly registered; limited partner details may remain private |

Focus Points

- Taxation: CVs and VOFs are fiscally transparent; income passes through to partners and is taxed at partner level. Curaçao does not impose withholding tax on profit distributions from transparent entities. VAT (OB) obligations depend on whether the partnership conducts taxable activities locally.

- Economic Substance: Substance requirements under the National Ordinance on Economic Zones do not directly target transparent partnerships, but arrangements involving passive income may attract scrutiny.

- Annual Compliance: Annual registration renewal with the Chamber of Commerce is required; financial statements are not mandatorily filed for partnerships.

- Treaty Access: Transparent partnerships generally do not access Curaçao's tax treaties in their own name; treaty eligibility falls to the resident partners.

- Conversion: A CV or VOF may be converted into a BV or NV, subject to compliance with the Civil Code requirements governing transformation.

Sub-Types

Maatschap (Civil Partnership)

Used for professional collaborations such as law firms or medical practices, the Maatschap does not carry on trade under a collective firm name and is not registered as a commercial entity unless commercially active.

Vennootschap onder Firma — VOF (General Partnership)

The VOF operates under a shared firm name and is intended for commercial trade. All partners face joint and several liability for the firm's debts, with no liability cap available to any partner.

Commanditaire Vennootschap — CV (Limited Partnership)

The CV separates management from investment: the general partner manages and bears unlimited liability, while the limited partner contributes capital and remains passive. A limited partner who participates in management loses liability protection under the Civil Code.

The CV is frequently used for private equity structures, family holding arrangements, and investment vehicles where one party manages assets and others contribute capital passively. The primary advantage is structural flexibility without mandatory minimum capital; the main limitation is the absence of separate legal personality, which exposes the general partner to unlimited personal liability.

The CV suits investors seeking a tax-transparent holding or fund vehicle with a clear separation between management and capital contribution, provided the general partner is a liability-shielded entity such as a BV or NV.

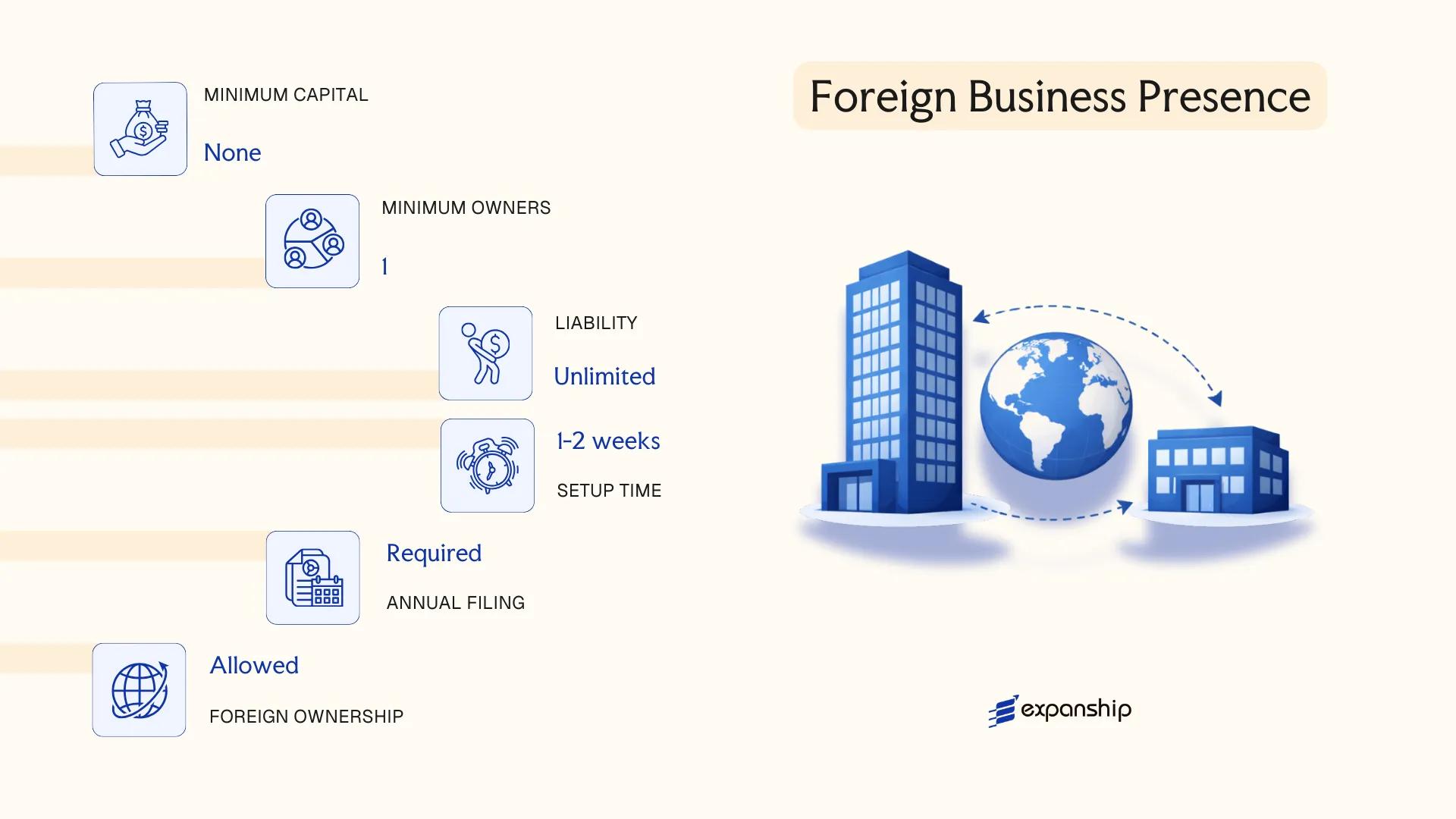

Foreign Business Presence in Curaçao [Branch Office, Representative Office]

Opening a branch office in Curaçao allows a foreign company to conduct business activities on the island without incorporating a separate local entity. The branch is not a distinct legal person — it remains part of the parent company, which bears full liability for the branch's obligations. Registration is governed by the Curaçao Commercial Register, and the foreign entity must file its constitutional documents, translated into Dutch where required, with the Chamber of Commerce (Kamer van Koophandel).

A representative office operates under more restricted conditions. It may not generate revenue or enter into commercial contracts locally; its activities are limited to market research, promotion, and liaison functions on behalf of the parent firm.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Parent Liability | Unlimited | Unlimited |

| Commercial Activity | Permitted | Not permitted |

| Local Representative | Required (resident authorized representative) | Required |

| Registered Address | Required in Curaçao | Required |

| KvK Registration | Mandatory | Mandatory |

Focus Points

- Taxation: Branch profits are subject to Curaçao's corporate income tax at the standard rate; transfer pricing rules apply to transactions with the parent, and no separate withholding tax exemptions attach by default.

- Economic Substance: Branches performing relevant activities must satisfy the substance requirements under the National Ordinance on Economic Substance.

- Annual Compliance: Annual financial statements of the parent must be filed with the Chamber of Commerce; local accounting records for branch activities are also required.

- Treaty Access: Access to tax treaties depends on the parent's jurisdiction of incorporation, not the branch's location.

- Restrictions: A representative office cannot invoice clients or earn local revenue; operating beyond these limits risks reclassification.

Closing

A branch structure suits foreign firms testing the market or managing regional operations without committing to a standalone subsidiary, though the absence of liability separation means the parent carries full exposure for all local obligations.

Foreign companies seeking a direct operational presence without a separately incorporated entity — particularly those with centralized group structures that can absorb the associated liability exposure.

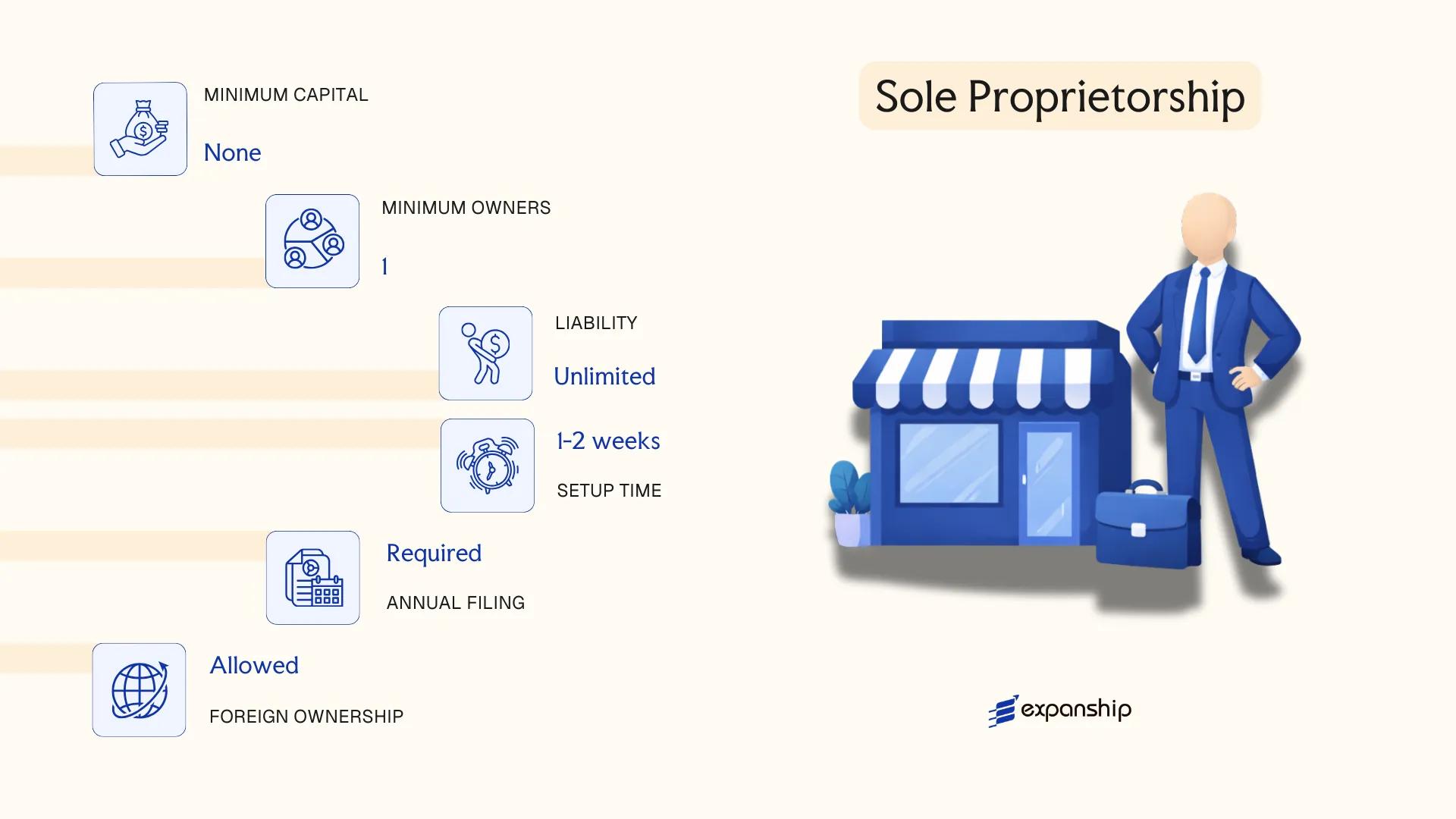

Sole Proprietorship (Eenmanszaak)

Curaçao eenmanszaak sole proprietorship registration is governed by the general civil and commercial law framework applicable in Curaçao, drawing from the Civil Code of Curaçao (Burgerlijk Wetboek van Curaçao). Unlike a Naamloze Vennootschap or Besloten Vennootschap, the eenmanszaak carries no separate legal personality — the proprietor and the business are treated as a single legal unit.

All business debts and obligations fall directly on the individual owner. There is no liability shield, meaning personal assets remain fully exposed to creditors of the business.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole proprietorship (unincorporated) | Not a separate legal entity from its owner |

| Members | Single proprietor | No shareholders, directors, or members; one individual owns and operates the business |

| Local Presence | Registered business address in Curaçao; registration with the Kamer van Koophandel (Chamber of Commerce) | Physical presence of the owner or an appointed local contact may be required |

| Capital | No statutory minimum capital | Owner contributes personal funds; no formal paid-up capital requirement |

| Privacy | Owner's name is publicly registered | The Handelsregister (Trade Register) records are accessible to third parties |

Focus Points

- Taxation: Subject to personal income tax (inkomstenbelasting) on business profits; turnover tax (omzetbelasting) obligations may apply depending on revenue thresholds; no corporate profit tax applies at the entity level.

- Annual Compliance: Required to maintain updated registration with the Kamer van Koophandel; annual financial records must be kept, though formal audit requirements do not apply at this level.

- Economic Substance: Substance obligations applicable to certain legal entities under Curaçao's economic substance legislation do not extend to sole proprietorships.

- Conversion: Can be converted into a BV or NV, though this requires formal incorporation of a new legal entity and transfer of business assets and liabilities.

- Restrictions: Cannot issue shares, admit partners, or raise equity capital; unsuitable for businesses requiring institutional investment or multiple ownership stakes.

Closing Paragraph

Self-employed business registration in Curaçao through the eenmanszaak structure suits freelancers, individual traders, and small service providers operating without partners or outside investors. The primary advantage is minimal setup cost and administrative simplicity; the significant drawback is unlimited personal liability for all business obligations.

Best suited for individual residents or locally operating self-employed professionals running low-risk, small-scale businesses who do not require limited liability protection.

How to Choose the Right Entity Type in Curaçao

Choosing the right company type in Curaçao is a structural decision with direct legal, tax, and operational consequences — not a matter of preference.

Why Your Entity Choice Matters

Misalignment between your intended activity and your registered entity can produce concrete and costly outcomes:

- Registering a tax-exempt entity when your business needs access to Curaçao's tax treaties means withholding tax reductions in counterpart countries are unavailable to you.

- Selecting an entity without the capacity to meet substance requirements triggers reporting failures under the National Ordinance on Profit Tax and can result in penalties.

- Incorporating a standard company when a foundation would serve asset protection or estate planning purposes binds you to ongoing shareholder obligations, annual general meeting requirements, and share register maintenance that foundations do not carry.

- Choosing an entity that mandates audited financial statements for a single-person consultancy adds recurring professional costs that serve no regulatory purpose at your scale.

Key Factors to Consider

- Business Activity: Passive asset-holding, active trading, and regulated sectors such as banking or funds management each correspond to a distinct entity form under Curaçao law.

- Local vs. Offshore Operations: Transacting with Curaçao residents requires a locally licensed and registered structure, whereas purely offshore activity may qualify for different fiscal treatment.

- Tax Objectives: Your choice should align with whether you require full profit tax exemption, eligibility for the e-zone regime, or access to the Kingdom of the Netherlands treaty network.

- Ownership and Management: Single-owner operations and multi-party ventures have different governance requirements; partnerships offer flexible internal arrangements that a rigid board structure does not.

- Substance Capacity: If your firm cannot realistically maintain personnel, office space, and management decisions within the jurisdiction, your entity choice must reflect that constraint from the outset.

- Exit Strategy: Redomiciliation, conversion, and voluntary winding-up are not uniformly available across all entity forms under the Civil Code of Curaçao — confirm these options before registering.

Corporate Compliance Services in Curaçao

Maintain good standing with local regulatory requirements, including annual filings, substance documentation, and statutory obligations.

Conclusion

Incorporating a company in Curaçao draws on a small set of well-defined legal structures, each suited to a distinct operational profile. The NV serves larger enterprises or those seeking public share issuance, while the BV functions as the standard vehicle for private, closely held businesses. Partnerships carry unlimited liability for general partners, making them less common for commercial ventures with external investors. Branch offices and representative offices extend a foreign firm's presence without creating a separate legal entity. The sole proprietorship suits individual operators running small, local businesses.

Among registered entities, the BV is the most frequently chosen structure for both resident and non-resident investors. Curaçao's regulatory framework, administered under the Civil Code of Curaçao and overseen by the Kamer van Koophandel, continues to evolve. Ongoing treaty negotiations and alignment with international tax transparency standards signal a maturing compliance environment that shapes how new businesses approach the Curaçao incorporation process overview.

How Expanship Can Assist You

Expanship company formation services Curaçao cover the full process of registering your business with the Curaçao Chamber of Commerce (Kamer van Koophandel), from selecting the right structure — an NV, BV, CV, or branch — to meeting the ongoing compliance requirements that apply after incorporation. Each entity type carries distinct obligations, and the registration requirements differ accordingly.

From initial document preparation to post-incorporation maintenance, Expanship supports your business at every stage:

- Document preparation and notarial deed legalization

- Registered agent and registered office provision

- Government filing and Kamer van Koophandel liaison

- Post-incorporation compliance management

- Corporate secretarial support

- Banking introduction assistance

Reach out to Expanship Curaçao to discuss which structure fits your business objectives and what the setup process involves for your specific situation.

Frequently Asked Questions (FAQ)

The Besloten Vennootschap (BV) is the most frequently incorporated entity. Its flexible share structure, single-shareholder eligibility, and limited liability make it the default choice for both resident entrepreneurs and foreign investors establishing a local or holding presence.

Both the BV and the NV are subject to profit tax under the Landsverordening op de Winstbelasting, but the NV carries heavier compliance obligations, including public disclosure requirements and a minimum share capital of ANG 40,000. The BV does not have a statutory minimum share capital requirement and is not required to offer shares to the public, making its administrative burden comparatively lighter.

The BV offers the strongest privacy profile among Curaçaoan business structures. Shareholder information is not publicly accessible through the Curaçao Chamber of Commerce (Kamer van Koophandel), and nominee shareholder arrangements are permissible under local practice. Beneficial ownership registration requirements do apply, however, under AML/CFT obligations.

A sole proprietorship (Eenmanszaak) and both the BV and NV can be formed by one person. Partnerships — the Maatschap, VOF, and CV — each require at least two parties by definition, as their legal basis rests on a contractual agreement between multiple persons.

Foreign nationals may incorporate any entity type, including the BV, NV, or a branch office, without a requirement for local resident shareholders or directors under general company law. Certain regulated sectors may impose additional conditions, but the Civil Code of Curaçao does not restrict entity formation by nationality.

Conversion from a BV to an NV, or the reverse, is legally recognized under Curaçaoan company law through a formal deed of amendment before a civil law notary. The process requires shareholder resolution and updated registration with the Kamer van Koophandel. Cross-type conversions involving partnerships are more complex and may require dissolution and re-incorporation.

The NV and BV both have full legal personality, meaning they can hold assets, enter contracts, and bear liabilities independently of their shareholders. Partnerships such as the VOF and Maatschap do not have separate legal personality under Curaçaoan civil law, which means partners remain personally exposed to the firm's obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.