Key Takeaways

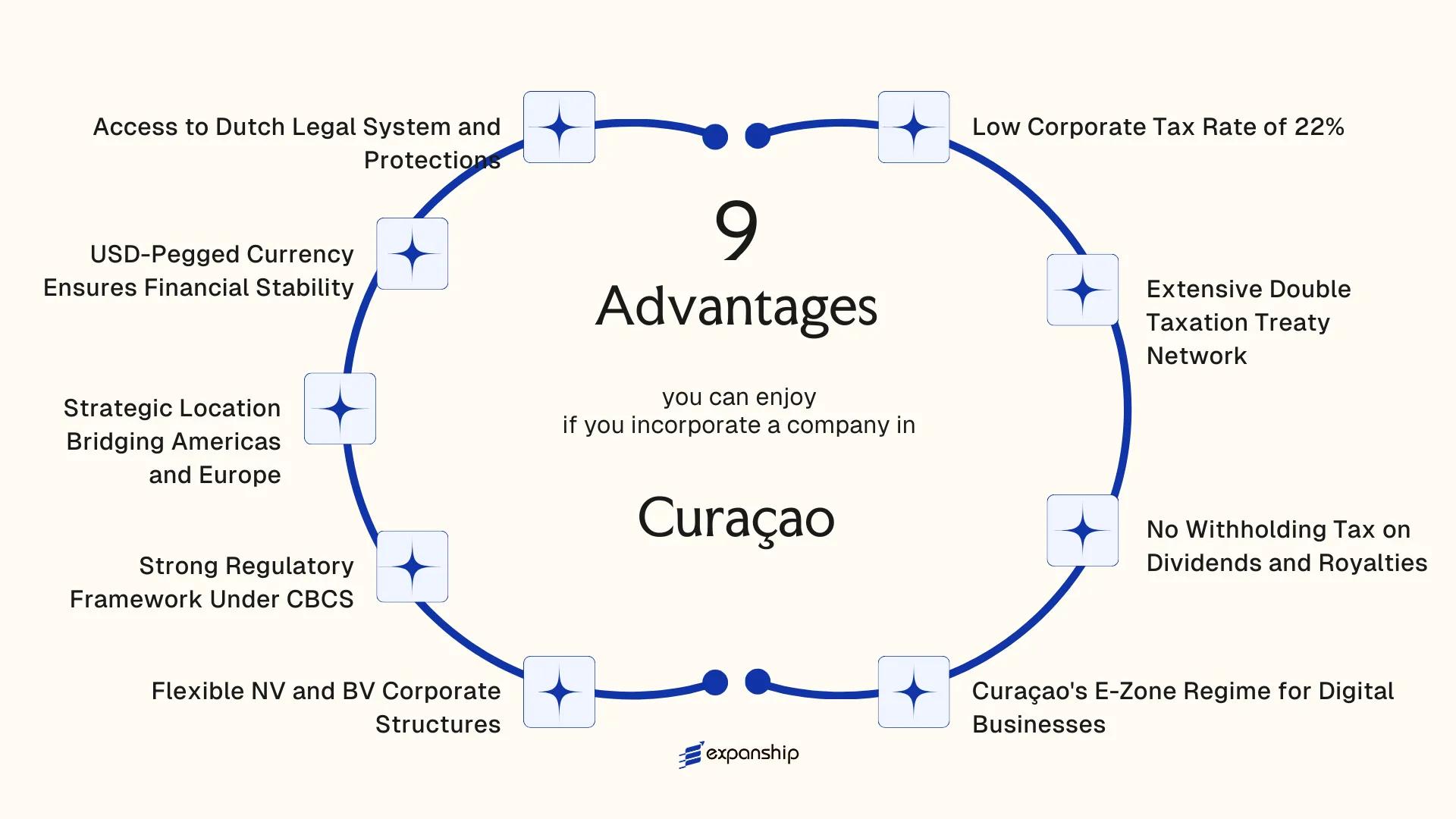

- Curaçao's corporate tax rate of 22% under the Landsverordening op de Winstbelasting, combined with no withholding tax on outbound dividends, allows foreign shareholders to extract profits without the layered tax costs common in higher-rate jurisdictions.

- Digital and e-commerce businesses structured under Curaçao's E-Zone regime can reduce their effective tax rate to 2% on qualifying export-oriented revenue, a meaningful advantage over standard Caribbean incorporation.

- Incorporation within a constituent country of the Kingdom of the Netherlands gives entities access to a Dutch-derived legal system and oversight by the Centrale Bank van Curaçao en Sint Maarten, providing institutional credibility that affects how banks, counterparties, and foreign regulators assess the entity.

- Holding companies benefit materially from Curaçao's dividend exemption provisions, which shield passive income distributions from additional taxation at the entity level before remittance to foreign shareholders.

Curaçao is a constituent country within the Kingdom of the Netherlands, situated in the southern Caribbean Sea. This political arrangement gives incorporated entities access to a Dutch-derived legal system while operating under a distinct fiscal and regulatory framework administered locally. Company registration falls under the oversight of the Curaçao Chamber of Commerce, which maintains the official commercial register for all entities established on the island.

Foreign businesses typically incorporate through a Naamloze Vennootschap or Besloten Vennootschap structure, depending on their ownership and capital preferences. The jurisdiction operates a low-tax regime with select territorial elements, making it attractive to holding companies, trading firms, and digital service providers. Foreign ownership is broadly permitted across most sectors, and the government has historically maintained an open posture toward foreign direct investment without imposing general restrictions on offshore shareholding.

Incorporating here offers a combination of tax efficiency, legal familiarity, and geographic positioning that merits structured examination. This article covers the key advantages relevant to any business evaluating the benefits of incorporating in Curaçao as part of an international structuring strategy.

Low Corporate Tax Rate of 22%

Curaçao applies a standard corporate income tax rate of 22% under the National Ordinance on Profit Tax (Landsverordening op de Winstbelasting 1940, as amended). This positions the jurisdiction notably below the OECD average corporate rate of approximately 23.6% and well under the EU average, which exceeds 21% but with many member states ranging into the mid-to-high 20s.

What the Rate Means in Practice

For a foreign-owned entity generating profits through a Curaçao-registered company, the 22% rate applies to net taxable profit after allowable deductions. Your business retains a larger share of earnings compared to operating through jurisdictions such as France (25%) or Germany (circa 30% combined trade and corporate tax).

Conditions That Shape Your Tax Position

Taxable presence and residency status determine whether your firm falls within the full scope of the profit tax ordinance. A company incorporated locally is generally treated as a tax resident and subject to tax on worldwide income, making the structure of your operations a relevant factor in calculating the effective rate.

A 22% corporate tax rate allows your Curaçao entity to retain more after-tax profit than it would under most Western European or North American tax regimes.

Extensive Double Taxation Treaty Network

Curaçao's double taxation treaty network benefits stem from its constitutional position within the Kingdom of the Netherlands. Under the Kingdom's tax treaty framework, a number of bilateral tax agreements extend to Curaçao as a constituent country, reducing or eliminating the risk of the same income being taxed twice across jurisdictions.

For a foreign business owner, this translates to measurable cost reduction. Dividend flows, interest payments, and royalties moving between your entity and counterparts in treaty countries are subject to reduced withholding rates rather than the full domestic rates applied in the absence of a treaty.

The network is particularly relevant because of the treaty partners involved:

- Agreements with Netherlands, Norway, and other OECD-aligned economies mean your firm operates within a recognised international tax framework, not an offshore grey zone.

- Treaty access can reduce withholding taxes on cross-border payments to rates as low as 0% to 15%, depending on the specific treaty and payment type.

- The legal basis for these treaties sits at the Kingdom level, giving them a constitutional footing that adds stability for long-term tax planning.

Treaty eligibility typically requires that your company maintain genuine economic substance in the jurisdiction, consistent with OECD anti-avoidance principles now embedded in most modern treaty provisions.

Incorporate a Company in Curaçao

Set up your Curaçao entity and access the Kingdom of the Netherlands treaty network with proper legal structure and substance requirements in place.

No Withholding Tax on Dividends and Royalties

Curaçao imposes no withholding tax on dividends paid to foreign shareholders. That single rule has a direct effect on how much of your company's distributed profit actually reaches you. In jurisdictions that do apply dividend withholding, rates commonly range from 5% to 25%, meaning a meaningful portion of distributions is withheld before remittance. No such deduction applies here.

The same principle extends to royalty payments. Fees paid from a Curaçao-registered entity to a foreign licensor for intellectual property rights are not subject to withholding tax at the source. For holding structures or IP-holding companies that routinely transfer royalty income across borders, this eliminates a layer of cost that would otherwise require treaty planning or credit mechanisms to recover.

| Payment Type | Withholding Tax Rate | Condition |

|---|---|---|

| Dividends to foreign shareholders | 0% | No minimum shareholding threshold required |

| Royalties to foreign licensors | 0% | Payment must originate from a registered local entity |

| Interest payments | Subject to general rules | Confirm current position under local tax law |

Under the National Ordinance on Profit Tax, these zero-rate provisions are embedded in domestic law, not dependent on a tax treaty being in place. Your business retains the full distributed amount regardless of the recipient's country of residence. This makes the structure predictable: there is no treaty shopping required, no reclaim process, and no dependency on bilateral agreements to achieve a clean outbound payment.

Curaçao's E-Zone Regime for Digital Businesses

The Curaçao E-Zone regime digital business benefits are grounded in a specific legislative framework designed to attract foreign-owned digital enterprises. Established under the E-Zone regulations, this regime allows qualifying companies to operate within a designated economic zone and supply digital goods or services exclusively to clients outside the island. That export-only requirement is what unlocks the tax advantage.

Profits derived from qualifying E-Zone activities are subject to a reduced corporate profit tax rate of 2%, compared to the standard 22% rate that applies to ordinary resident companies. For a digital firm generating significant margin, that differential directly reduces the effective tax cost of operating through this structure.

Eligible activities typically include software development, e-commerce, and digital content services. The company must be physically established within an approved E-Zone facility, and services must be delivered to non-resident customers.

Keep these points in mind:

- E-Zone status requires physical presence within a licensed zone facility

- Revenue must derive from services or goods delivered outside the island

- The 2% rate applies only to qualifying E-Zone income; non-qualifying income is taxed at the standard rate

- Annual compliance with zone operator requirements is necessary to maintain status

For the official regulatory framework, refer to the E-Zone rules.

An E-Zone company can be 100% foreign-owned with no local shareholder requirement, which is uncommon among low-tax digital business regimes globally.

Flexible NV and BV Corporate Structures

Both the Naamloze Vennootschap (NV) and the Besloten Vennootschap (BV) are governed by the Civil Code of Curaçao, which was revised to permit considerable structural flexibility. For foreign business owners, the Curaçao NV BV corporate structure advantages begin with the degree of customization available at the articles-of-incorporation stage — well before operations commence.

Share Capital and Governance Flexibility

The BV has no statutory minimum share capital requirement, which reduces the upfront financial commitment when establishing a new entity. Voting rights, profit entitlements, and transfer restrictions can all be configured through the articles of association, allowing shareholders to tailor governance to the specific needs of their business rather than conforming to a rigid statutory model.

The NV permits the issuance of bearer shares under regulated conditions, which is useful for structures requiring tradeable equity. Both entity types allow a single director and a sole shareholder, so your business can be established and maintained without assembling a full board or a dispersed ownership group.

Flexibility for Foreign Investors

A foreign national can serve as sole director without a residency requirement, giving foreign investors direct control over the entity. This is a practical distinction from many EU jurisdictions where local director mandates add administrative overhead and third-party dependence.

Profit distributions can be structured through multiple share classes, enabling tax-efficient allocations among shareholders without requiring a formal corporate restructuring.

Structure Your Curaçao Entity the Right Way

Speak with our team about configuring an NV or BV that fits your ownership, governance, and distribution requirements from day one.

Strong Regulatory Framework Under CBCS

Financial services operating out of Curaçao fall under the oversight of the Centrale Bank van Curaçao en Sint Maarten (CBCS), the joint central bank established under the Kingdom of the Netherlands following the 2010 dissolution of the Netherlands Antilles. For foreign business owners, the Curaçao CBCS regulatory framework advantages are meaningful precisely because they are grounded in Dutch legal tradition rather than improvised local legislation.

- Licensing requirements under the CBCS are defined by specific legislation, including the National Ordinance on the Supervision of Banking and Credit Institutions (NOSSBI) and the National Ordinance on the Supervision of Investment Institutions and Administrators (NOSII). These statutes give your business a clearly mapped compliance path rather than discretionary enforcement.

- The CBCS applies internationally recognized standards aligned with Basel III and FATF recommendations. Counterparties and institutional partners in Europe and North America are familiar with these frameworks, which reduces friction in correspondent banking relationships.

- Regulatory oversight from a central bank with a statutory mandate creates a credible supervisory structure. This matters when your entity needs to demonstrate to auditors, lenders, or partners that it operates within an accountable system.

- The CBCS publishes supervisory guidelines and maintains transparency in its regulatory decisions, which allows your compliance team to plan around known requirements rather than ambiguous regulatory expectations.

Strategic Location Bridging Americas and Europe

Curaçao sits at 12 degrees north latitude in the southern Caribbean, approximately 65 kilometers off the Venezuelan coast. That position places it within a four-hour flight radius of Miami, Bogotá, São Paulo, and several major European connecting hubs, giving companies incorporated there direct operational proximity to both Latin American and North Atlantic markets without maintaining separate regional entities.

Atlantic Standard Time (UTC-4, observed year-round without daylight saving shifts) means your working hours overlap simultaneously with European mornings and North American afternoons. For firms managing cross-continental deal flow, treasury operations, or client relationships, that time zone alignment reduces the coordination friction that typically forces businesses to choose one region over the other.

The island's port infrastructure, handled through the Curaçao Ports Authority, supports transshipment between the Americas and Europe. For businesses with physical goods moving between these trade corridors, this creates a functional logistical anchor rather than a purely nominal registration address.

A company incorporated in Curaçao operating in UTC-4 shares a 4-hour business day overlap with London (GMT) and a 5-hour overlap with Amsterdam (CET during winter), while simultaneously covering the full New York business day. No single continental jurisdiction offers equivalent dual-corridor coverage without a secondary establishment.

USD-Pegged Currency Ensures Financial Stability

The Curaçao USD-pegged currency stability benefit stems from the Netherlands Antillean guilder (ANG), which has maintained a fixed exchange rate of 1.79 ANG per US dollar since 1971. This peg is administered by the Centrale Bank van Curaçao en Sint Maarten (CBCS) and has remained unchanged for over five decades.

For a foreign business owner, this exchange rate stability advantage translates directly into predictable cost structures. Pricing contracts, forecasting revenues, and repatriating profits all carry significantly less currency risk than in jurisdictions with floating exchange regimes.

Firms that invoice or hold assets in US dollars face minimal conversion friction, since the ANG tracks the dollar at a fixed rate rather than fluctuating against it. This reduces the need for currency hedging instruments, which lowers operational overhead for cross-border entities.

- The fixed rate applies to all commercial transactions conducted in the local currency.

- USD accounts are widely accepted within the local banking system, reducing conversion frequency for foreign investors.

- CBCS monetary policy is structurally aligned with maintaining this peg as a price stability mechanism.

The Antillean guilder peg applies to ANG-denominated transactions; businesses operating primarily in third currencies such as EUR or GBP will not benefit from dollar peg stability by default.

Access to Dutch Legal System and Protections

Curaçao's position as a constituent country within the Kingdom of the Netherlands gives businesses incorporated here access to a legal foundation that is grounded in Dutch civil law tradition. This Curaçao Dutch legal system protection benefit is structural, not aspirational: the island's civil code is directly derived from the Dutch Burgerlijk Wetboek, meaning contract law, property rights, and corporate liability rules follow a well-documented, centuries-tested framework.

Civil Law Certainty for Contracts and Disputes

Your contracts and corporate documents are governed by the Curaçaos Burgerlijk Wetboek, which mirrors Dutch civil code principles closely enough that legal precedent from the Netherlands carries interpretive weight in local courts. For foreign investors unfamiliar with offshore legal uncertainty, this translates into a predictable litigation environment where rulings are grounded in codified law rather than administrative discretion.

Judicial Structure and Enforcement

The court system follows a defined hierarchy: the Gerecht in Eerste Aanleg handles first-instance cases, with appeals heard by the Gemeenschappelijk Hof van Justitie, the joint appellate court shared across the Dutch Caribbean territories. Final appeal lies with the Hoge Raad der Nederlanden, the Dutch Supreme Court in The Hague.

This means your firm has access to one of Europe's most respected apex courts as the ultimate arbiter of commercial disputes. The practical consequence for a foreign business owner is meaningful: enforcement of judgments and contractual claims follows a structured, internationally recognised process rather than a local administrative framework with limited external oversight.

Is Curaçao the Right Jurisdiction for You?

Determining whether a jurisdiction suits your business comes down to how its specific features map onto your operating model. The comparisons below focus on jurisdictions that foreign investors evaluating Curaçao realistically consider: Barbados, Panama, and the British Virgin Islands. Each targets a broadly similar investor profile, offers Dutch or common-law legal protections, or sits within the same Atlantic incorporation market. The table isolates parameters where this jurisdiction holds a neutral or favourable position, drawing on features already detailed in this blog.

What the comparison reveals is structural rather than superficial. The combination of a tax-coded income regime, access to the Dutch legal system, CBCS regulatory oversight, and the E-Zone for digital businesses produces a profile that differs meaningfully from Caribbean peers that offer lower headline rates but lack treaty access or regulated financial oversight. For businesses where legal predictability and banking credibility matter as much as tax efficiency, that distinction carries weight.

| Parameter | Curaçao | Barbados | Panama | British Virgin Islands |

|---|---|---|---|---|

| Standard Corporate Tax Rate | 22% | 5.5–9% (sliding scale) | 25% (territorial) | 0% (no income tax) |

| Double Tax Treaties | 10+ active treaties | 40+ active treaties | Limited network | None |

| Withholding Tax on Dividends | 0% (standard) | 0–15% (varies) | 10% | 0% |

| Regulated Financial Supervisor | CBCS | Central Bank of Barbados | SBP | FSC (lighter framework) |

| E-Zone / Special Digital Regime | Yes (E-Zone, 2% effective rate) | No direct equivalent | No direct equivalent | No |

| Legal System | Dutch civil law (Kingdom of the Netherlands) | English common law | Civil law | English common law |

| USD-Pegged Currency | Yes (ANG pegged to USD) | Yes (BBD pegged to USD) | USD is legal tender | No local currency |

| Judicial Appeal Body | Supreme Court of the Netherlands | Caribbean Court of Justice | Panamanian courts | Eastern Caribbean Supreme Court |

Compliance Services for Companies in Curaçao

Maintain good standing under CBCS requirements and the National Ordinance on the Supervision of Company Service Providers with ongoing compliance support tailored to Curaçao-registered entities.

Conclusion

The benefits of incorporating in Curaçao rest on a combination of statutory features that few jurisdictions in the Caribbean or Latin American corridor can replicate within a single regulatory framework. The 22% corporate tax rate, enforced under the Landsverordening op de Winstbelasting, paired with the absence of withholding tax on outbound dividends, creates a tax position that directly reduces the cost of profit distribution to foreign shareholders. For digital and e-commerce businesses, the E-Zone regime takes this further by applying a 2% effective rate on qualifying export-oriented revenue.

Not every business structure benefits equally. A holding company with passive income streams will find the dividend exemption provisions particularly material, while an operational entity serving international markets may find greater value in the E-Zone designation. Your industry, the origin of your customers, and the nature of your income all shape which features apply and to what degree.

Curaçao's position within the Kingdom of the Netherlands gives it an institutional foundation that most offshore jurisdictions lack. The legal system, oversight by the Centrale Bank van Curaçao en Sint Maarten, and access to Dutch treaty protections add a layer of credibility that affects how counterparties, banks, and regulators in other countries treat your entity. For businesses that require both tax efficiency and reputational standing, that combination determines whether the jurisdiction is workable in practice. The next step is matching these structural features against your specific corporate circumstances.

Start Your Curaçao Company with Expanship Today

Expanship's Curaçao company formation services cover the full incorporation lifecycle, from selecting between a Naamloze Vennootschap and a Besloten Vennootschap to meeting the filing requirements set by the Curaçao Chamber of Commerce. The blog has covered the material advantages this jurisdiction offers, including the 22% corporate tax rate, the E-Zone regime, CBCS oversight, and treaty access. Translating those structural benefits into an operational entity requires accurate documentation, local regulatory knowledge, and ongoing compliance management.

Expanship handles each stage of that process directly:

- Preparation and notarial legalization of incorporation documents

- Registered agent and registered office provision in Willemstad

- Filing and liaison with the Curaçao Chamber of Commerce

- Post-incorporation compliance management, including statutory obligations under the Civil Code of Curaçao

- Banking introduction assistance for corporate account opening

- Ongoing corporate secretarial and annual reporting support

Reach out to Expanship Curaçao to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The standard corporate income tax rate is 22%, applicable to profits generated within the jurisdiction. Income sourced entirely outside the country may be treated differently depending on the entity structure and whether an E-Zone license or other special regime applies. You should confirm the precise treatment of foreign-sourced income with a qualified local tax adviser familiar with the Landsverordening op de Winstbelasting.

Companies operating under an approved E-Zone license that generate revenue exclusively from clients outside the jurisdiction are subject to a reduced profit tax rate of 2%. This regime is administered under specific E-Zone legislation and requires that services or goods be delivered to foreign recipients. Physical presence within the designated zone and prior government approval are conditions for eligibility.

No withholding tax applies to dividend distributions made to non-resident shareholders under the current tax framework. This treatment extends to royalty payments as well, making the jurisdiction structurally favorable for holding companies that collect and redistribute income across borders. The absence of these withholding obligations is a statutory position, not a discretionary exemption.

The treaty network in force derives largely from the Kingdom of the Netherlands' historical tax conventions, though not all treaties automatically extend to the constituent countries. Coverage depends on whether a specific treaty was extended to or separately negotiated by the island territory. You should verify treaty applicability with reference to the current list maintained by the tax authority, as treaty status can differ from what applied prior to the 2010 constitutional reorganization of the Kingdom.

No statutory requirement mandates that a director be a resident of the island or hold a specific nationality. However, substance requirements tied to tax residency claims and certain regulatory approvals under the CBCS (Centrale Bank van Curaçao en Sint Maarten) may make a local director arrangement commercially advisable in practice. Substance considerations are particularly relevant if your firm is seeking to establish genuine tax residency rather than simply a registered address.

Incorporation timelines vary depending on entity type, the completeness of submitted documentation, and whether the business activity requires a prior license from a regulatory body such as the CBCS. A straightforward BV formation can generally be completed within a few weeks once a notarial deed is executed and filed with the Trade Register of the Chamber of Commerce of Curaçao. Regulated activities, such as financial services, require additional licensing steps that extend this timeline considerably.

The Netherlands Antillean guilder (ANG) is pegged to the US dollar at a fixed rate of 1.79 ANG per USD, a rate maintained under the monetary authority of the CBCS. This peg eliminates exchange rate volatility between the local currency and the dollar, which reduces transactional uncertainty for businesses billing or holding assets in USD. Exposure to other currencies, such as the euro, remains subject to standard market fluctuation.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.