Key Takeaways

- Under Law 1258 of 2008, the Sociedad por Acciones Simplificada (SAS) is the predominant vehicle for entity formation in Colombia, and registration must be completed through the Cámara de Comercio before any formal business activity can commence.

- Beneficial ownership disclosure is a continuing compliance obligation under SAGRILAFT, requiring companies to identify and report controlling parties to the Superintendencia de Sociedades beyond the point of initial incorporation.

- Every registered entity must maintain a physical municipal address on public record as its registered office, and failure to satisfy this condition prevents the entity from completing its registration with the Cámara de Comercio.

- Tax registration with the DIAN is a mandatory post-incorporation step that must be completed before the entity can operate within Colombia's formal commercial framework.

Entity formation in Colombia is governed by the Commercial Code and supplemented by Law 1258 of 2008, which regulates the most widely used business structure, the Sociedad por Acciones Simplificada (SAS). The Superintendencia de Sociedades and the Cámara de Comercio oversee corporate registration and ongoing compliance.

Meeting the incorporation requirements in Colombia is not optional. Failure to satisfy the prescribed conditions results in rejection of the registration application or, in certain cases, the inability to operate under a legally recognised structure.

This article covers the structural, documentary, and governance requirements applicable to entity formation. Specific obligations vary depending on the chosen entity type, the industry sector, and whether the investor is a foreign national or a locally domiciled party.

Foreign entrepreneurs, multinational subsidiaries, and non-resident investors exploring company registration requirements in Colombia will find this article directly relevant to their planning process.

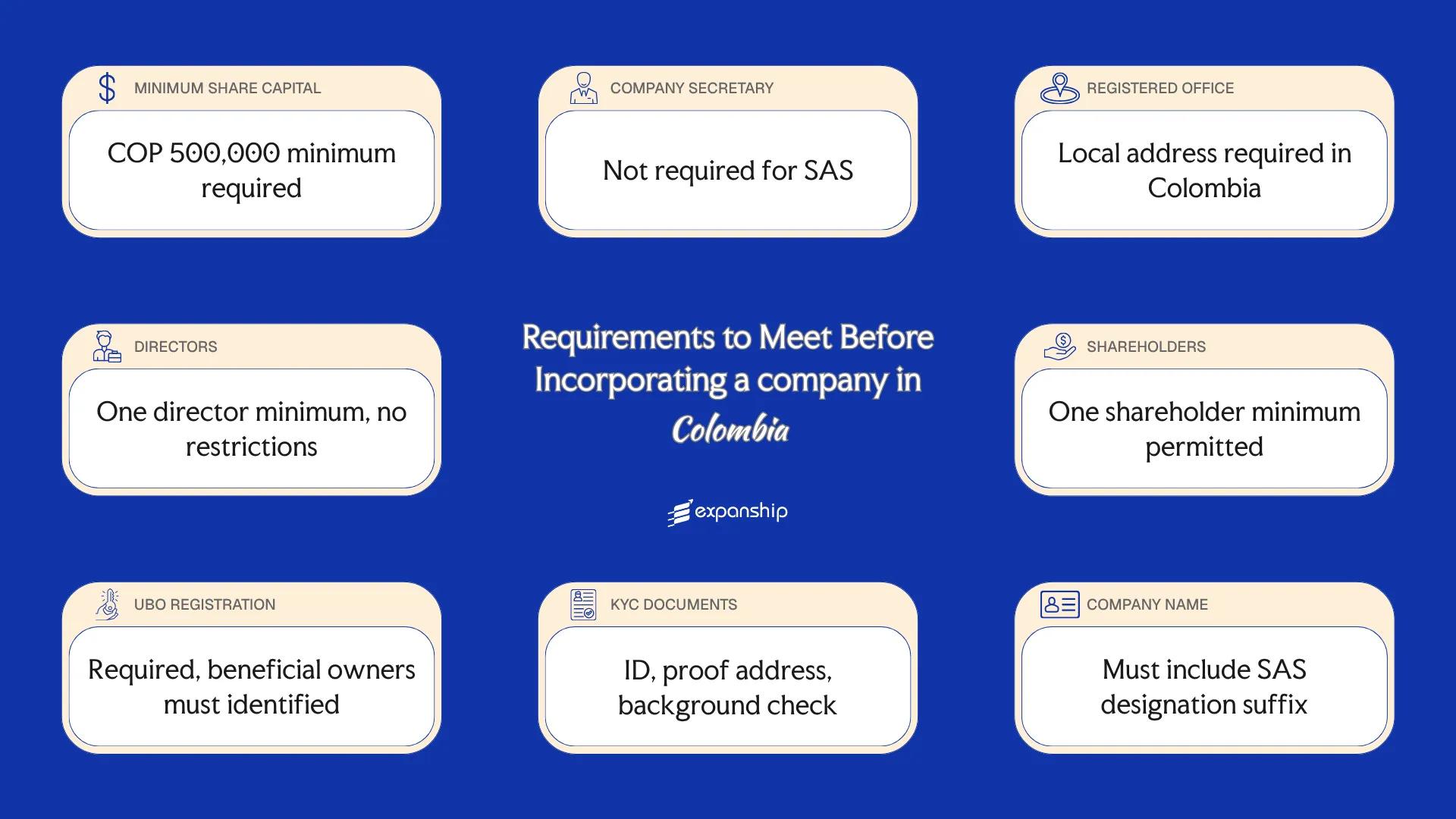

Minimum Share Capital Requirements in Colombia

Under Colombia's corporate framework, there are no minimum share capital requirements for the most widely used entity type, the Sociedad por Acciones Simplificada (SAS), established under Law 1258 of 2008. Capital is defined in the company's articles of incorporation and registered with the Cámara de Comercio (Chamber of Commerce) of the relevant city.

Shares in a SAS are issued under a par value system, meaning each share carries a nominal value stated in Colombian pesos. The Chamber of Commerce verifies the authorized capital structure at the point of registration, though it does not require prior bank deposit confirmation. Capital obligations are set at incorporation and do not trigger recurring statutory minimums thereafter.

| Parameter | Detail |

|---|---|

| Minimum Authorized Share Capital | No statutory minimum |

| Maximum Authorized Share Capital | No statutory maximum |

| Minimum Paid-Up Capital | No statutory minimum |

| Paid-Up Requirement at Incorporation | No statutory requirement |

| Accepted Currency | Colombian Peso (COP) |

| Accepted Forms of Contribution | Cash and non-cash contributions (including assets), subject to valuation rules under Law 1258 of 2008 |

| Timeframe to Deposit Capital | No mandatory deposit deadline under Law 1258 of 2008 |

A SAS still requires a defined authorized capital in its articles of incorporation. Leaving capital undefined or inconsistently stated can cause the Cámara de Comercio to reject the registration filing.

Company Secretary Requirements in Colombia

Under Colombian corporate law, there is no statutory requirement for a dedicated company secretary role in the same form as common law jurisdictions. However, certain entities — particularly corporations (sociedades anónimas) and simplified joint-stock companies (sociedades por acciones simplificadas, or SAS) — are required to appoint a revisor fiscal, an independent statutory auditor whose obligations are defined under the Código de Comercio.

The revisor fiscal is not equivalent to a secretary but carries formal compliance duties. These include certifying financial statements, reporting irregularities to the Superintendencia de Sociedades, and verifying that corporate acts conform to the entity's bylaws and applicable law.

Qualification criteria for serving as revisor fiscal in Colombia:

- Must be a certified public accountant (contador público titulado) registered with the Junta Central de Contadores

- Cannot be a shareholder, employee, or relative within the fourth degree of consanguinity of any director or officer of the firm

- Must be independent of the entity being audited

- Legal persons (firms) providing audit services must hold valid professional registration

Incorporate a Company in Colombia

Set up your legal entity in Colombia with guidance on structure selection, statutory filings, and regulatory compliance.

Registered Office Requirements in Colombia

Registered office requirements in Colombia are governed by the Commercial Code and enforced through the Cámara de Comercio, which registers the domicilio social as part of the company's public record. Using a non-compliant or fictitious address can result in registration rejection, administrative sanctions, or the nullification of legal notices served to the entity.

- A physical address within Colombia is required; virtual office addresses are not universally accepted and their validity depends on the Cámara de Comercio of the relevant jurisdiction.

- The registered address must be located in Colombia, corresponding to the municipality where the company is incorporated.

- Proof of a lease agreement or property title is not always mandatory at registration, but the address must be verifiable and functional.

- The domicilio social is publicly listed in the Registro Mercantil and accessible through the Cámara de Comercio's public database.

- Any change to the registered address must be formally reported to the Cámara de Comercio through an amendment filing, with updated entries reflected in the Registro Mercantil.

- Failure to maintain an accurate registered address can affect the valid service of legal notices and regulatory correspondence, potentially exposing your business to default judgments or missed compliance deadlines.

Director Requirements in Colombia

Upon appointment, directors of a Colombian company assume statutory duties under the Código de Comercio (Commercial Code), including the obligation to act in the firm's best interest and to manage affairs with the diligence of a prudent businessperson. Liability can extend to personal assets where directors breach these duties or act outside the scope of their authority.

| Parameter | Detail |

|---|---|

| Minimum Number of Directors | One director is required. |

| Maximum Number of Directors | No statutory maximum is prescribed. |

| Local/Resident Director Required | No residency requirement exists under Colombian law. |

| Nationality Restrictions | No nationality restrictions apply to directors. |

| Minimum Age Requirement | Directors must be of legal age, which is 18 years under Colombian law. |

| Corporate Directors Permitted | Corporate directors are generally not permitted; directors must be natural persons. |

| Director Must Be a Shareholder | No statutory requirement for directors to hold shares in the entity. |

| Publicly Listed on Registry | Directors are registered with the Cámara de Comercio (Chamber of Commerce) and are publicly accessible. |

| Disqualification Conditions | Persons convicted of certain criminal offences or declared commercially insolvent may be disqualified from serving as directors. |

Despite having no residency requirement, directors registered with the Cámara de Comercio appear on a publicly searchable national registry, meaning their appointment is fully transparent to any third party without a formal disclosure request.

Shareholder Requirements in Colombia

Under Colombian law, a Sociedad por Acciones Simplificada (SAS) requires a minimum of one shareholder, making sole-shareholder structures fully permissible. There is no statutory maximum on the number of shareholders in a SAS.

Nationality and Residency Restrictions

Meeting the shareholder requirements Colombia company formation demands does not require shareholders to be Colombian nationals or residents. Foreign individuals and entities may hold 100% of the shares without restriction under the general foreign investment framework governed by Decree 2080 of 2000 and its successors.

Corporate Shareholders

Legal entities, both domestic and foreign, may act as shareholders in a SAS. No additional conditions specific to corporate shareholders are imposed beyond standard registration and documentation requirements.

Shareholder Liability

In a SAS, accionista liability is limited to the amount each shareholder has contributed or agreed to contribute to the firm's capital. Courts may pierce the corporate veil in cases of fraud or abuse of the legal entity.

Register of Shareholders

A SAS must maintain an internal register of shareholders, which records transfers and ownership changes. This register is not filed with a public authority but must be available for inspection by competent authorities when required.

Shareholder Structuring Support for Your Colombian Entity

Get guidance on meeting shareholder obligations when setting up a business in Colombia, from ownership structuring to register maintenance.

UBO / Beneficial Ownership Disclosure Requirements in Colombia

Beneficial ownership disclosure Colombia is governed primarily by Resolution 314 of 2021 issued by the Superintendencia de Sociedades, which operationalises the SAGRILAFT framework and defines a beneficial owner as any natural person who, directly or indirectly, holds 5% or more of the capital or voting rights of an entity, or exercises effective control over it.

- Identify all natural persons meeting the 5% ownership or effective control threshold before or at the time of company registration.

- Record beneficial ownership information in your firm's internal SAGRILAFT compliance system.

- Report UBO data to the Superintendencia de Sociedades through the designated Virtual Business Portal (Portal Empresarial Virtual) within the statutory reporting cycle.

- Update the register whenever a change in beneficial ownership occurs.

| Parameter | Detail |

|---|---|

| Ownership Threshold for UBO Status | 5% of capital or voting rights, or effective control |

| Filing Authority | Superintendencia de Sociedades |

| Disclosure Deadline at Incorporation | Within the annual SAGRILAFT reporting cycle |

| Publicly Accessible Register | No |

| Penalties for Non-Disclosure | Administrative sanctions under the SAGRILAFT regime, including fines |

| Ongoing Update Obligation | Yes; updates required upon any change in ownership or control |

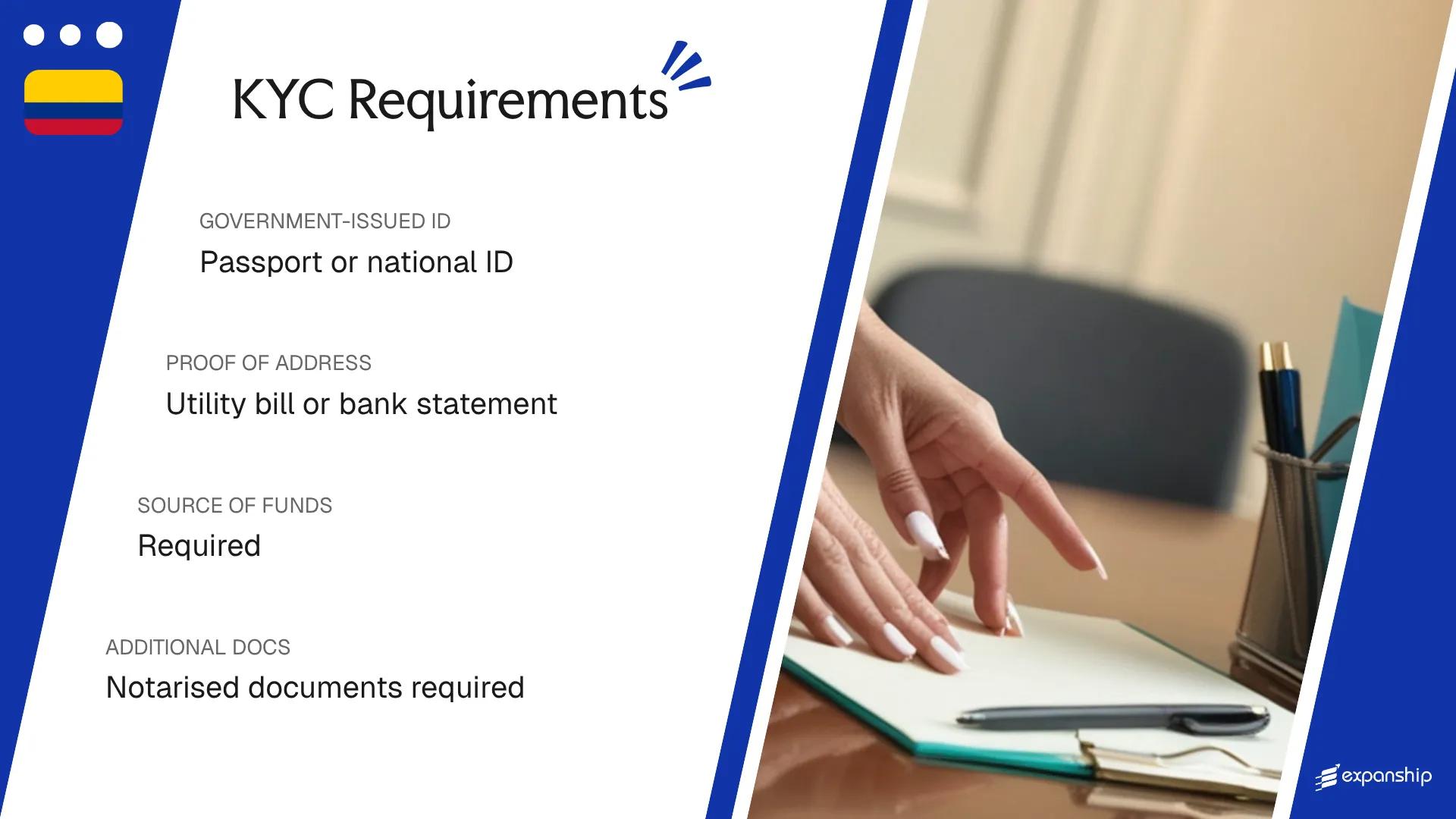

KYC / Document Requirements in Colombia

KYC document requirements in Colombia are governed primarily by Law 1762 of 2015 and the anti-money laundering framework administered by the UIAF, Colombia's Financial Intelligence Unit, which sets the due diligence standards applied during the incorporation process.

Individual / Personal Documents

- Valid government-issued photo identification (cedula de ciudadania for Colombian nationals or passport for foreign nationals)

- Proof of residential address dated within the last three months, such as a utility bill or bank statement

- Completed SAGRILAFT self-declaration form where required by the incorporating entity's compliance programme

- Tax identification number (NIT or equivalent foreign tax ID)

Corporate Documents

- Certificate of incorporation or equivalent formation document from the entity's home jurisdiction

- Constitutional documents, including articles of association or bylaws

- Current register of directors issued by the relevant authority in the home jurisdiction

- Proof of the corporate entity's registered address

Source of Funds Documentation

- Recent bank statements covering a minimum of three to six months

- Audited financial statements or accountant-certified accounts where bank statements are insufficient

- Written declaration of the origin of capital to be introduced into the Colombian entity

Notarisation and Apostille Requirements

- Foreign public documents must be apostilled under the Hague Convention or, for non-member countries, legalised through the Colombian consulate

- Official Spanish translations must be prepared by a certified translator recognised in Colombia

- Notarised copies of identity documents are required when originals cannot be presented directly

Unsigned or uncertified translations of foreign corporate documents are the most common cause of incorporation delays with the Cámara de Comercio.

Company Name Requirements in Colombia

Proposed company name requirements Colombia are assessed by the local chamber of commerce, the Cámara de Comercio, before registration is confirmed. Names must be unique within the commercial registry and cannot duplicate or closely resemble an already-registered entity.

All business names must be written in Spanish or include a Spanish translation where a foreign-language term is used. The firm's legal suffix must reflect its corporate form, such as S.A.S., S.A., or Ltda., and this suffix is mandatory in all formal references to the entity.

Certain words are outright prohibited if they imply a government affiliation the business does not hold, or suggest a regulated activity, such as banking or insurance, without the corresponding authorization. Words referencing the Colombian state or national institutions fall into a restricted category requiring prior approval from the relevant supervisory authority.

Name reservation is available through the Cámara de Comercio and is typically granted for a defined period before formal registration, allowing your business to secure the chosen name while incorporation documents are prepared. The reservation must be applied for directly with the chamber in the jurisdiction where the registered office will be located.

Compliance Services for Companies in Colombia

Manage your ongoing corporate compliance obligations in Colombia, from annual filings to regulatory reporting with the Cámara de Comercio.

Conclusion

Colombia company incorporation requirements span several distinct obligations governed primarily by the Código de Comercio and supervised by the Superintendencia de Sociedades and the Cámara de Comercio. Among the most significant are the beneficial ownership disclosure rules under SAGRILAFT, which impose ongoing due diligence duties beyond the initial registration, and the registered office requirement tied to a specific municipal address on public record. Once these obligations are understood, a foreign investor can move toward entity formation, tax registration with the DIAN, and building the operational structure needed to conduct business formally.

Expanship's Corporate Services for Colombia Expansion

Registering a business in Colombia involves engaging with the Cámara de Comercio, obtaining a tax identification number (NIT) from the DIAN, and meeting the SAS's specific formation requirements. Expanship's Colombia corporate services incorporation support is structured around these actual procedural steps, reducing the time and coordination your team would otherwise spend managing multiple government bodies. Our role is to carry the administrative weight, not to change what Colombian law requires of your entity.

From document preparation through to post-incorporation obligations, Expanship supports your business across the full formation cycle:

- We prepare and file all company registration documentation with the relevant Cámara de Comercio.

- Our team provides registered agent and office address services compliant with Colombian requirements.

- We handle direct liaison with government bodies including the DIAN and Superintendencia de Sociedades.

- Ongoing compliance management is available to keep your entity in good standing after formation.

- Banking introduction assistance is available to help you establish a local or international account.

- We manage tax registration with the DIAN and coordinate with local municipal authorities where applicable.

Reach out to Expanship Colombia to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

A foreign national can serve as the sole legal representative (director) of a Colombian SAS without requiring a local co-director. That said, the individual must obtain a valid Colombian tax identification number (NIT) and, in most cases, a cedula de extranjería to execute binding acts before the Cámara de Comercio. Failure to hold these identifiers prevents the company from completing key registration and tax enrollment steps with the DIAN.

The registered office address recorded with the Cámara de Comercio must remain valid and current at all times, as official notifications, regulatory correspondence, and judicial communications are served to that address. If the address lapses, the entity risks missing legally binding notices, which can result in unanswered claims proceeding by default. You are required to update the registered address through a formal amendment filed with the relevant Cámara de Comercio before vacating the premises.

All Colombian legal entities, including those with foreign shareholders, must register their beneficial owners in the SAGRILAFT system and report to the UIAF (Unidad de Información y Análisis Financiero) under the anti-money laundering framework established by Superintendencia de Sociedades. A natural person who ultimately owns or controls 25% or more of the equity or voting rights qualifies as a UBO and must be disclosed. Non-compliance with SAGRILAFT reporting obligations can trigger administrative sanctions and suspension of operations.

The Cámara de Comercio requires that your proposed company name be distinguishable from all names already registered in its database, and it will reject any name that is identical or confusingly similar to an existing entity. Foreign-language words are permitted, but the name cannot imply a state affiliation or use terms restricted by law, such as "banco" or "seguro," without the corresponding regulatory authorization. A name availability search through the Cámara de Comercio's online portal is the recommended first step before drafting the articles of incorporation.

A foreign corporate shareholder must submit a Certificate of Existence or equivalent public registry document from its home jurisdiction, translated into Spanish by a certified translator and apostilled or consularized depending on whether the issuing country is a signatory to the Hague Convention. This differs from an individual foreign shareholder, who primarily needs a valid passport and proof of address. Both document sets must be current, typically issued within the prior three to six months, to be accepted during the registration process.

Yes, a single individual can simultaneously act as the sole shareholder and legal representative of a SAS under Law 1258 of 2008, which explicitly permits one-person ownership and management. This structure is valid from incorporation and does not require a supervisory board (junta directiva) unless the articles of incorporation specifically establish one. The unipersonal SAS structure is regularly used by foreign entrepreneurs who want full operational control without the obligation to bring in additional partners.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.