Key Takeaways

- The Ministry of Commerce and Industry (MOCI) maintains the Commercial Register and serves as the primary authority for business registration across most entity forms in Qatar.

- Qatar's territorial corporate tax system has historically exempted Qatari and GCC national-owned entities under the Income Tax Law, while domestically operating foreign-owned businesses remain subject to corporate income tax.

- The Limited Liability Company (W.L.L.) is the most frequently registered structure among foreign investors due to its combination of operational flexibility and defined liability boundaries.

- Amendments to Qatar's Commercial Companies Law have expanded 100% foreign ownership permissions in qualifying sectors, reflecting a broader regulatory trend toward greater market openness.

Introduction to Entity Types in Qatar

Qatar is a sovereign state on the northeastern coast of the Arabian Peninsula, bordered by Saudi Arabia and sharing maritime boundaries with Bahrain, the United Arab Emirates, and Iran. Structurally, it operates as a constitutional monarchy under the Al Thani family. Company registration falls under the authority of the Ministry of Commerce and Industry (MOCI), which maintains the Commercial Register and oversees business licensing across most entity forms. Certain activities — particularly those within the Qatar Financial Centre — are governed by a separate regulatory framework entirely.

For corporate tax purposes, Qatar operates a territorial system, with domestic businesses generally subject to corporate income tax while Qatari and GCC national-owned entities have historically benefited from exemptions under the Income Tax Law.

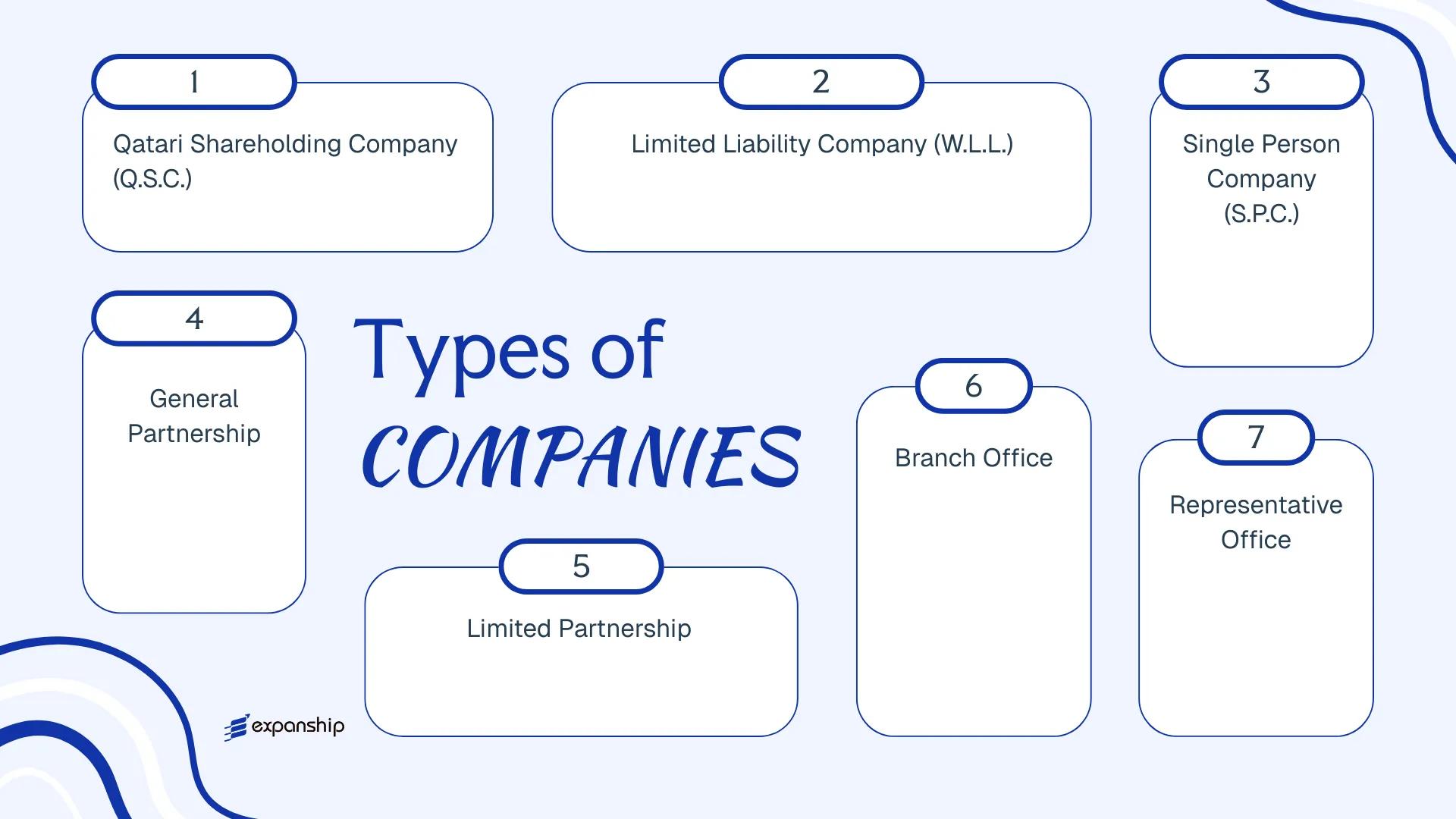

The types of business entities in Qatar available to local and foreign investors include the Qatari Shareholding Company (Q.S.C.), the Limited Liability Company (W.L.L.), the Single Person Company (S.P.C.), General and Limited Partnerships, Branch Offices, and Representative Offices. Each structure carries distinct ownership requirements, liability rules, and operational constraints. This article examines each entity in detail to support an informed Qatar corporate structures comparison.

An Overview of Business Structures in Qatar

Qatar's commercial company law framework, governed primarily by Law No. 11 of 2015 (the Commercial Companies Law) and its subsequent amendments, recognises several distinct entity types for businesses operating in or from the country. Free zone establishments fall under separate legislation administered by their respective authorities, such as the Qatar Financial Centre (QFC) Authority and the Qatar Free Zones Authority (QFZA). Each structure carries different rules on ownership, liability, and permitted activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Qatari Shareholding Company (Q.S.C.) | Public or Closed Joint Stock | Limited to shares | Taxable | Yes | 5 shareholders | Ministry of Commerce & Industry | Law No. 11 of 2015 |

| Limited Liability Company (W.L.L.) | Private LLC | Limited to capital | Taxable | Yes | 2 shareholders | Ministry of Commerce & Industry | Law No. 11 of 2015 |

| Single Person Company (S.P.C.) | Sole-owned LLC | Limited to capital | Taxable | Yes | 1 shareholder | Ministry of Commerce & Industry | Law No. 11 of 2015 |

| General Partnership | Partnership | Unlimited | Taxable | Yes | 2 partners | Ministry of Commerce & Industry | Law No. 11 of 2015 |

| Limited Partnership | Partnership | Mixed | Taxable | Yes | 2 partners | Ministry of Commerce & Industry | Law No. 11 of 2015 |

| Branch Office | Branch | Parent liable | Taxable | Yes | N/A | Ministry of Commerce & Industry | Law No. 11 of 2015 |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | No | N/A | Ministry of Commerce & Industry | Law No. 11 of 2015 |

Each of these structures is examined in full in the sections below.

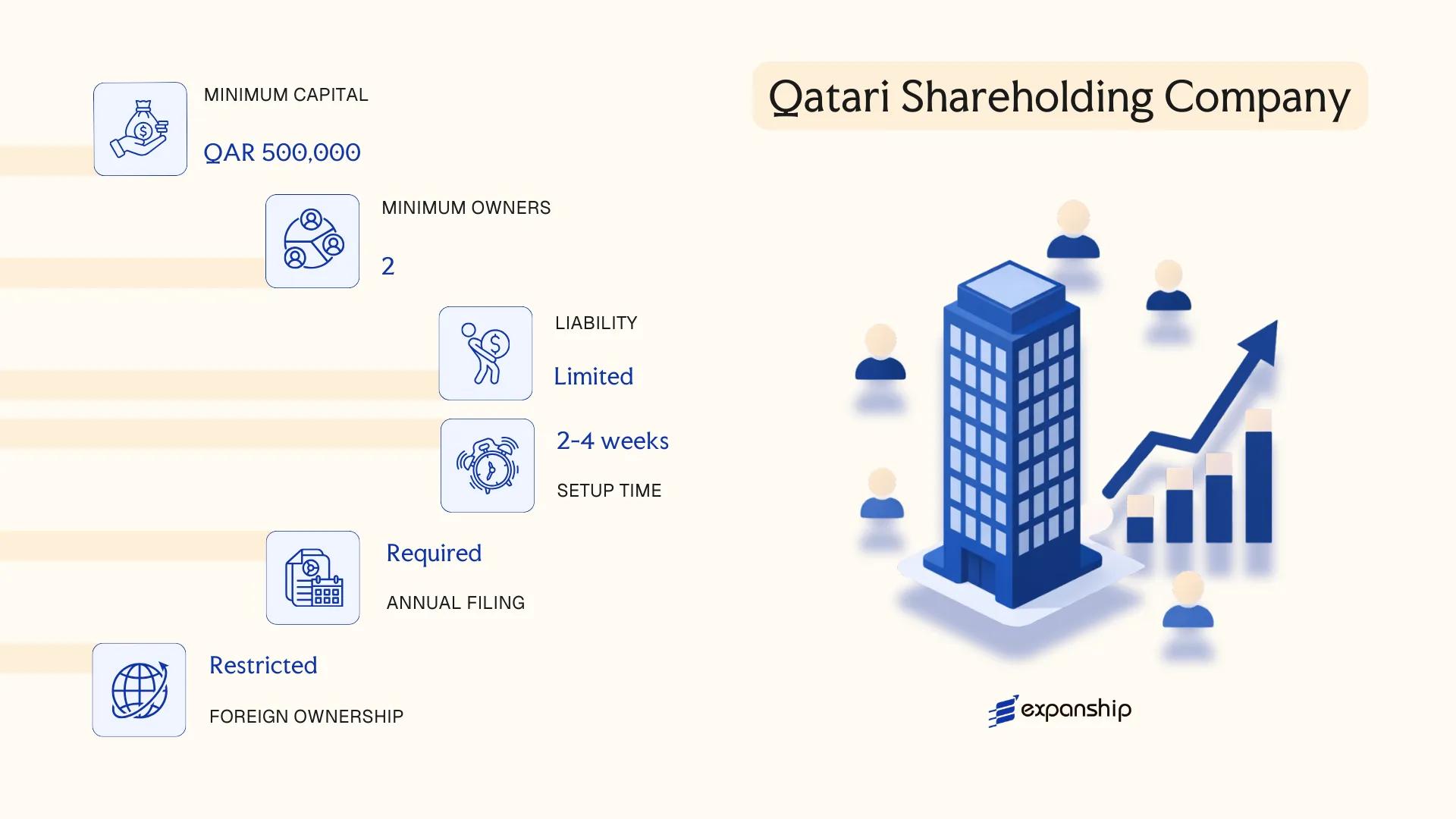

Qatari Shareholding Company (Q.S.C.)

Governed by Law No. 11 of 2015 (the Commercial Companies Law) and its subsequent amendments, the Qatar shareholding company QSC formation process is one of the more demanding incorporation pathways available in the jurisdiction. The structure carries separate legal personality, meaning the entity's obligations are distinct from those of its shareholders.

Shareholders hold limited liability, confined to their subscribed share capital. This makes the Q.S.C. the closest Qatari equivalent to a public company under common law systems, capable of offering shares to the public when licensed to do so.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Qatari Shareholding Company (Q.S.C.) | Governed by Law No. 11 of 2015 |

| Members | Shareholders; minimum 5 founders | No statutory maximum on shareholders |

| Management | Board of Directors; minimum 3, maximum 11 members | Board elected by shareholders at general assembly |

| Local Presence | Registered office in Qatar required | Physical address; no registered agent requirement per se |

| Capital | QAR 10,000,000 minimum for private Q.S.C.; QAR 40,000,000 for public listing | Must be fully subscribed at incorporation; at least 25% paid up |

| Foreign Ownership | Up to 100% in sectors permitted under Investment Law No. 1 of 2019 | Restricted sectors require Qatari majority |

| Privacy | Shareholder register maintained; public companies subject to disclosure requirements | Private Q.S.C. has comparatively greater confidentiality |

Focus Points

- Taxation: Subject to Qatar's 10% corporate income tax on locally sourced profits; VAT is not currently applied in Qatar; no withholding tax on dividends distributed to foreign shareholders under general rules; no stamp duty on share transfers.

- Economic Substance: Qatar does not impose OECD-style economic substance regulations, though regulated activities require genuine operational presence.

- Annual Compliance: Mandatory audited financial statements, annual general assembly, and filing with the Ministry of Commerce and Industry.

- Treaty Access: Qatar has an active double tax treaty network; Q.S.C. entities are generally eligible as tax residents for treaty purposes.

- Conversion: A W.L.L. may be converted into a Q.S.C. subject to Ministry approval and meeting capital thresholds.

Sub-Types

Private Shareholding Company

Shares are not offered to the public and cannot be listed on the Qatar Stock Exchange. This structure suits large family-owned enterprises or joint ventures requiring a share-based ownership model without public market exposure.

Public Shareholding Company

Authorised to list shares on the Qatar Stock Exchange (QSE) following approval from the Qatar Financial Markets Authority (QFMA). This sub-type is subject to continuous disclosure obligations, prospectus requirements, and QFMA regulatory oversight.

Closing

The Q.S.C. suits large-scale commercial operations, joint ventures with institutional partners, and businesses seeking eventual access to public capital markets. The share-based structure facilitates equity transfers more cleanly than member-based entities, though the high minimum capital requirement and ongoing governance obligations make it disproportionate for small or early-stage businesses.

The Q.S.C. is best suited for large enterprises, institutional joint ventures, or businesses with a credible pathway to public listing on the Qatar Stock Exchange.

Company Incorporation in Qatar

Expanship supports Q.S.C. and other entity formations in Qatar, including regulatory liaison and post-incorporation compliance setup.

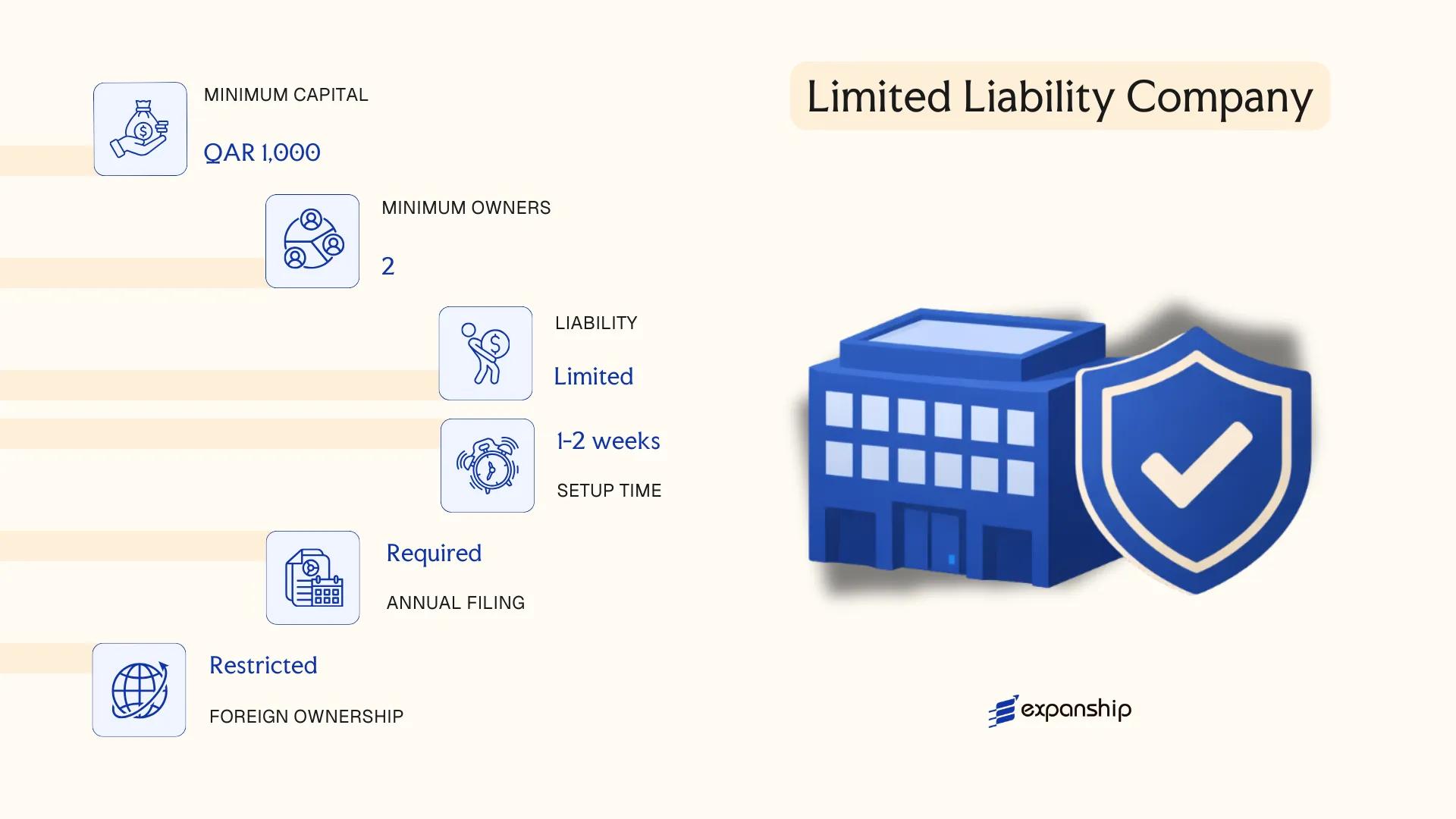

Limited Liability Company (W.L.L.)

Governed by Law No. 11 of 2015 (the Commercial Companies Law), the Qatar limited liability company WLL setup is one of the most widely used structures for commercial activity in the country. The entity carries separate legal personality, meaning liabilities do not pass through to members beyond their capital contributions.

Historically, foreign ownership in a W.L.L. was capped at 49%, with a Qatari national or entity holding the majority. Law No. 1 of 2019 and subsequent decisions under the Investment Promotion Agency Qatar (IPA Qatar) have opened select sectors to full foreign ownership, though restrictions remain in others.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (W.L.L.) | Separate legal personality; hybrid of partnership and corporate form |

| Members | 2–50 shareholders | Single-member structures use the S.P.C. form instead |

| Management | One or more managers (not a board) | Managers need not be shareholders; appointed by members |

| Share Capital | Minimum QAR 200,000 | No public offering permitted; shares not freely transferable |

| Local Presence | Registered office address in Qatar required | Physical or virtual office depending on licensing authority |

| Privacy | Shareholder names filed with Ministry of Commerce and Industry | Not publicly searchable in a central online registry |

Focus Points

- Taxation: Subject to Qatar's 10% corporate income tax on profits attributable to foreign ownership; Qatari and GCC-national-owned portions are generally exempt. No withholding tax on dividends, and VAT is currently not imposed in Qatar.

- Annual Compliance: Audited financial statements required annually; accounts filed with the Ministry of Commerce and Industry.

- Economic Substance: No formal economic substance regime equivalent to offshore jurisdictions; physical presence requirements arise through licensing conditions.

- Treaty Access: Qatar's tax treaty network may apply to foreign-owned W.L.L. entities, subject to beneficial ownership conditions.

- Ownership Restrictions: Certain sectors (media, real estate, insurance) retain foreign ownership caps regardless of IPA Qatar exemptions.

Closing

A W.L.L. suits foreign investors entering Qatar for trading, services, or project-based activity where a locally licensed operational presence is required. The structure offers clear liability separation, but the share transfer restrictions and sector-specific ownership caps can limit flexibility for investors seeking exit or restructuring options.

Best suited for foreign companies establishing an operational subsidiary in Qatar with a defined commercial activity and a long-term presence commitment.

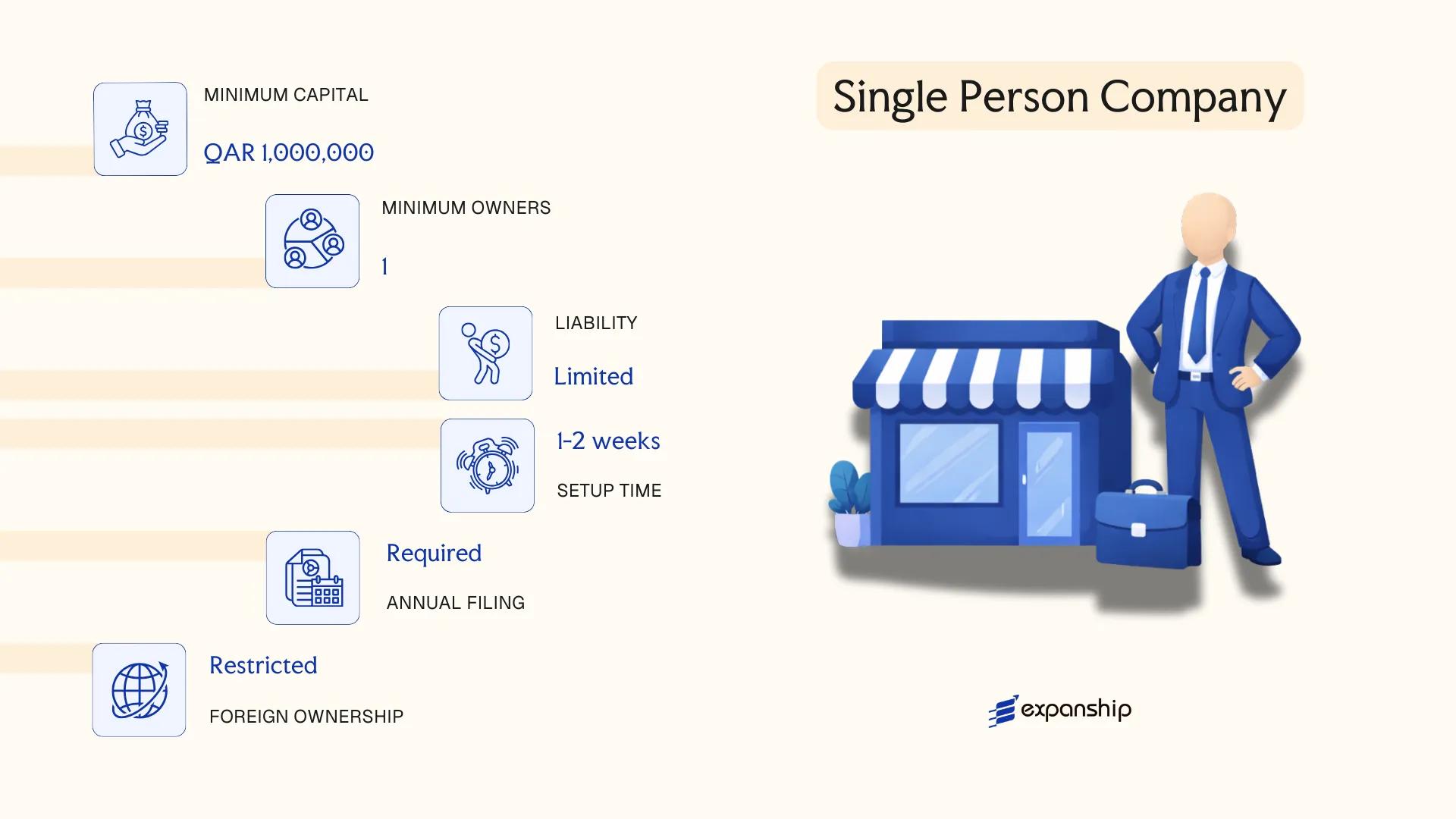

Single Person Company (S.P.C.)

Qatar single person company SPC registration is governed by Law No. 11 of 2015 (the Commercial Companies Law), which formally introduced the S.P.C. as a distinct legal structure. The entity carries its own legal personality, separate from its sole owner, and offers limited liability protection.

Structurally, the S.P.C. functions as a hybrid: it retains the operational simplicity of sole ownership while adopting the legal standing of a corporate body. Sole owner company Qatar formations under this structure are administered and licensed through the Ministry of Commerce and Industry (MoCI).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Single Person Company (S.P.C.) | Separate legal personality; limited liability |

| Members | 1 Sole Owner (individual or corporate entity) | No minimum share count mandated beyond capital requirement |

| Management | Manager(s) appointed by the sole owner | Owner may self-appoint as manager |

| Local Presence | Registered office address in Qatar required | Physical or registered address; virtual offices not universally accepted |

| Share Capital | No statutory minimum under the CCL | MoCI may impose sector-specific minimums during licensing |

| Ownership | 100% foreign ownership permissible in approved activities | Subject to the Positive List under Qatar's foreign investment framework |

Focus Points

- Taxation: Subject to Qatar's 10% corporate income tax on taxable profits; VAT is not currently imposed; no withholding tax on dividends distributed to the sole owner; no stamp duty on share transfers.

- Economic Substance: No formal economic substance regime currently in force, though physical presence and genuine activity are assessed during licence renewals.

- Annual Compliance: Annual financial statements required; audit obligations apply regardless of revenue size.

- Conversion: An S.P.C. may be converted to a W.L.L. or Q.S.C. by admitting additional shareholders, subject to MoCI approval.

- Restrictions: Certain regulated sectors, including banking, insurance, and legal services, remain closed or subject to additional licensing conditions.

Closing Paragraph

The S.P.C. suits sole founders, holding structures, and consultancy-oriented businesses seeking full ownership with corporate liability protection. Its primary limitation is the dependency on a single decision-maker, which can create governance or operational continuity risks.

Best suited for individual entrepreneurs or parent companies seeking full ownership and operational control without a co-shareholder requirement.

Partnerships [General Partnership, Limited Partnership]

Qatar general and limited partnership formation is governed by the Commercial Companies Law, Law No. 11 of 2015, along with its subsequent amendments. Both partnership structures carry unlimited joint liability for at least one class of partner, which distinguishes them from limited liability entities under the same legislation. Registration is administered through the Ministry of Commerce and Industry (MoCI).

Unlike corporations, partnerships do not have shares traded or transferred freely. Ownership interests are governed by the partnership agreement, and partner changes require formal amendment procedures through MoCI.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (General or Limited) | Governed under Law No. 11 of 2015 |

| Members | Partners (General: minimum 2, no maximum; Limited: minimum 1 general + 1 limited partner) | General partners bear unlimited liability; limited partners are liable only to the extent of their capital contribution |

| Local Presence | Registered office address in Qatar required | Must maintain a physical or registered address on file with MoCI |

| Capital | QAR; no statutory minimum | Capital amount is defined in the partnership agreement |

| Liability | General partners: unlimited personal liability; Limited partners: capped at contribution | A limited partner who participates in management may lose liability protection |

| Privacy | Partner names appear in the commercial register | No confidentiality mechanism for partner identity |

Focus Points

- Taxation: Subject to Qatar's corporate income tax at 10% on Qatar-sourced profits for non-Qatari partners; Qatari partners' shares are generally exempt. VAT is applicable at the standard rate where turnover thresholds are met; no withholding tax on dividends, and no stamp duty on incorporation.

- Economic Substance: Partnerships conducting relevant activities may be subject to economic substance requirements under Qatar Financial Centre or mainland regulations.

- Annual Compliance: Annual financial statements and commercial registration renewal are required through MoCI; audit requirements depend on partnership size and structure.

- Treaty Access: Access to Qatar's double tax treaties is available, subject to the partnership being treated as a tax resident entity.

- Restrictions: Foreign nationals cannot be general partners in a mainland partnership without meeting foreign ownership regulations; certain sectors remain restricted.

Sub-Types

General Partnership (Sharikat al-Tadamun)

All partners hold equal management authority and carry unlimited joint liability for the firm's obligations. This structure is typically used by professionals or family-owned businesses where all participants are actively involved in operations.

Limited Partnership (Sharikat al-Tawsiya al-Basita)

At least one general partner bears unlimited liability while one or more limited partners contribute capital without taking part in management. This arrangement suits investors seeking passive exposure without operational responsibility.

Closing

Partnerships are most suited to closely held businesses, professional services firms, or family enterprises where partners are known to one another and operational control is shared or deliberately divided. The absence of a minimum capital requirement offers flexibility at formation, but unlimited personal liability for general partners represents a significant structural risk for commercial ventures.

Partnerships in Qatar are best suited for small professional firms or family businesses where all active participants are known and trust-based liability arrangements are acceptable.

Foreign Business Presence [Branch Office, Representative Office]

Establishing a foreign company branch office in Qatar is governed primarily by Law No. 1 of 2021 (the Commercial Companies Law) and supplementary regulations issued by the Ministry of Commerce and Industry (MoCI). A branch office does not constitute a separate legal entity; it remains an extension of the parent company, which retains full liability for the branch's obligations.

Registration of either structure requires approval from MoCI, and in certain regulated sectors, additional approvals from sector-specific authorities apply. Both structures must appoint a local manager and maintain a registered address within the country.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Permitted Activities | Commercial and operational activity (subject to sector approvals) | Limited to promotion, market research, and liaison only |

| Local Manager | Mandatory; must be appointed and registered with MoCI | Mandatory |

| Local Sponsor | Required (Qatari agent or sponsor in most cases) | Required |

| Minimum Capital | No statutory minimum, but MoCI may set conditions | None prescribed |

| Registration Authority | Ministry of Commerce and Industry (MoCI) | Ministry of Commerce and Industry (MoCI) |

Focus Points

- Taxation: Branch profits are subject to the standard 10% corporate income tax under Law No. 21 of 2009; representative offices generating no income are generally not taxable, though they may still have filing obligations. No VAT is currently imposed in Qatar, and there is no withholding tax on dividends or interest at the time of writing.

- Economic Substance: Branches conducting income-generating activities must demonstrate genuine operational substance within Qatar.

- Annual Compliance: Both structures must renew their commercial registration annually with MoCI and maintain audited financial records.

- Treaty Access: As an extension of the parent entity, a branch may access Qatar's double taxation agreements, subject to the specific treaty's permanent establishment provisions.

- Restrictions: Representative offices are prohibited from invoicing clients or generating direct revenue; any commercial activity must be conducted through a separately registered entity.

Sub-Types

Branch Office

A branch office may conduct the same commercial activities as the parent company, provided those activities are permitted under Qatari law and any required sector licences are obtained. It is the structure used when a foreign firm intends to execute contracts or deliver services directly within the country.

Representative Office

A representative office is restricted to non-revenue-generating functions such as promoting the parent company's products, conducting market research, or facilitating communications. It carries no authority to sign contracts or collect payments on behalf of the parent.

Closing

Both structures suit foreign firms testing market entry or fulfilling contract-specific obligations, with the branch offering operational capacity and the representative office serving a purely promotional function. The principal limitation of both is the absence of liability separation from the parent entity.

Foreign companies with existing contracts in Qatar or those conducting preliminary market assessments before committing to a locally incorporated entity.

How to Choose the Right Entity Type in Qatar

Selecting how to structure your business in Qatar shapes everything from your tax position and liability exposure to your ability to hire staff and sign local contracts.

Why Your Entity Choice Matters

The consequences of choosing an unsuitable structure are concrete, not theoretical.

- Forming a branch office when you intend to conduct independent commercial activity — rather than extending an existing foreign parent's operations — places the entity outside its permitted scope under the Commercial Companies Law (Law No. 11 of 2015), which can result in regulatory penalties or forced dissolution.

- Selecting a structure that does not qualify under Qatar's tax treaty network means your business cannot claim withholding tax reductions available to treaty-resident entities in counterpart jurisdictions.

- Registering a Qatari Shareholding Company when a single-person consultancy is all you require introduces mandatory audited financial statements and governance obligations that add material annual cost without operational benefit.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as banking or insurance, and passive asset-holding each point toward different structures under the Commercial Companies Law.

- Ownership Structure: A sole operator will find the Single Person Company more appropriate than a multi-shareholder W.L.L., which requires a minimum of two partners.

- Foreign Ownership Requirements: Activities outside the Foreign Investment Promotion Law's restricted list may permit 100% foreign ownership, directly determining which entity types are available to your firm.

- Substance Capacity: If your business cannot maintain physical presence, staff, and local decision-making, this limits viable structures under Qatar Financial Centre regulations.

- Exit Strategy: Not all entity types permit straightforward conversion or redomiciliation, so your intended exit route should inform the initial structure selected.

Corporate Compliance Services in Qatar

Maintain good standing with Qatar's regulatory requirements, including annual filings, audits, and Commercial Register renewals.

Conclusion

Selecting the right structure is one of the more consequential decisions in any incorporating a business in Qatar guide, because the choice affects ownership rights, liability exposure, and regulatory obligations from day one. The Limited Liability Company remains the most frequently registered entity among foreign investors, largely due to its balance between operational flexibility and defined liability boundaries. Single Person Companies suit sole proprietors who require a separate legal personality without a partner, while a Qatari Shareholding Company is reserved for businesses intending to raise capital from the public. Branch and representative offices serve distinct purposes for foreign firms without a permanent local establishment.

Qatar's regulatory posture has trended toward greater openness since amendments to the Commercial Companies Law and the expansion of 100% foreign ownership permissions in qualifying sectors. The Ministry of Commerce and Industry continues to refine registration procedures, signaling a sustained effort to align the framework with international standards. Expanship's team works directly within this environment to guide your business through each registration stage.

How Expanship Can Assist You

Expanship's Qatar company formation services cover the full arc of incorporation, from selecting the right entity structure under the Commercial Companies Law (Law No. 11 of 2015) to completing registration with the Ministry of Commerce and Industry. Every entity type discussed in this guide, whether a W.L.L., Q.S.C., or S.P.C., carries distinct filing requirements, and our team handles each accordingly.

Our Qatar entity registration assistance spans the entire process:

- Document preparation and notarization/legalization

- Registered agent and registered office provision

- Government filing and liaison with the Ministry of Commerce and Industry

- Post-incorporation compliance management

- Corporate bank account introduction

Setting up a business in Qatar involves multiple regulatory touchpoints that vary by entity type and ownership structure. Our team coordinates each step so nothing falls through the gaps.

Reach out to Expanship Qatar to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Limited Liability Company (W.L.L.) is the most frequently registered structure. Its flexible minimum capital requirements and relatively straightforward incorporation process under the Ministry of Commerce and Industry make it the default choice for small to mid-sized ventures.

A Branch Office operates as an extension of a foreign parent entity and carries no separate legal personality, while a W.L.L. is a distinct legal entity incorporated under Qatari law. Branch offices are generally restricted to activities tied to a specific government contract, whereas a W.L.L. can pursue broader commercial operations. Compliance obligations are heavier for a W.L.L., which requires annual audited financial statements filed with the relevant authorities.

The Single Person Company (S.P.C.) involves a single shareholder, and while beneficial ownership disclosure is required during registration with the Ministry of Commerce and Industry, there is no public shareholder register in the same format as jurisdictions with open registries. Nominee arrangements are not a recognized mechanism under Qatari corporate law, so privacy is structural rather than nominee-based.

Not all structures permit sole formation. The S.P.C. is specifically designed for single-person ownership, while a W.L.L. requires a minimum of two shareholders. General and limited partnerships both require at least two partners, and a Qatari Shareholding Company (Q.S.C.) mandates a minimum of five founding shareholders.

Under the Foreign Investment Law (Law No. 1 of 2019), foreign nationals may hold up to 100% ownership in many sectors through a W.L.L. or S.P.C., subject to the activities listed in the Ministry of Commerce and Industry's approved sectors. Certain strategic or restricted industries still require a Qatari partner holding a minimum 51% stake. A Branch Office or Representative Office remains available for foreign companies seeking a presence without incorporating a new entity locally.

Conversion between entity types is addressed under the Commercial Companies Law and is permissible in defined circumstances, such as converting a W.L.L. into a Q.S.C. The process requires shareholder approval, regulatory filings with the Ministry of Commerce and Industry, and in some cases, a revised commercial registration. Conversion in the reverse direction is subject to conditions tied to minimum capital thresholds and shareholder count requirements.

A W.L.L., S.P.C., and Q.S.C. each hold separate legal personality upon registration, meaning liabilities are ring-fenced from those of the individual shareholders. A Representative Office does not hold separate legal personality and cannot enter into commercial contracts in its own name. Branch Offices occupy an intermediate position: they are registered locally but remain legally inseparable from the foreign parent company.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.