Key Takeaways

- Paraguay's company registrations are processed through the Registro Público de Comercio under the Poder Judicial, governed by the Código Civil Paraguayo and Ley Nº 1034/83 (Código de Comercio).

- The Sociedad de Responsabilidad Limitada (S.R.L.) is the most commonly registered entity in Paraguay, favored by small to medium-sized businesses for its manageable compliance obligations.

- Under Paraguay's territorial tax system, income generated outside the country is generally not subject to local taxation, making it a notable factor for foreign registrants evaluating jurisdiction.

- Branch offices expose a foreign parent company to direct liability for local operations, whereas a representative office is restricted from conducting commercial activity by definition.

Introduction to Entity Types in Paraguay

Paraguay is a landlocked country in central South America, bordered by Argentina, Brazil, and Bolivia. It is an independent republic, and company registration falls under the jurisdiction of the Registro Público de Comercio, which operates under the Poder Judicial (Judicial Branch). Incorporation filings and commercial registrations are processed through this body in accordance with the Código Civil Paraguayo and the Ley Nº 1034/83 (Código de Comercio).

Paraguay operates a territorial tax system, meaning income generated outside the country is generally not subject to local taxation.

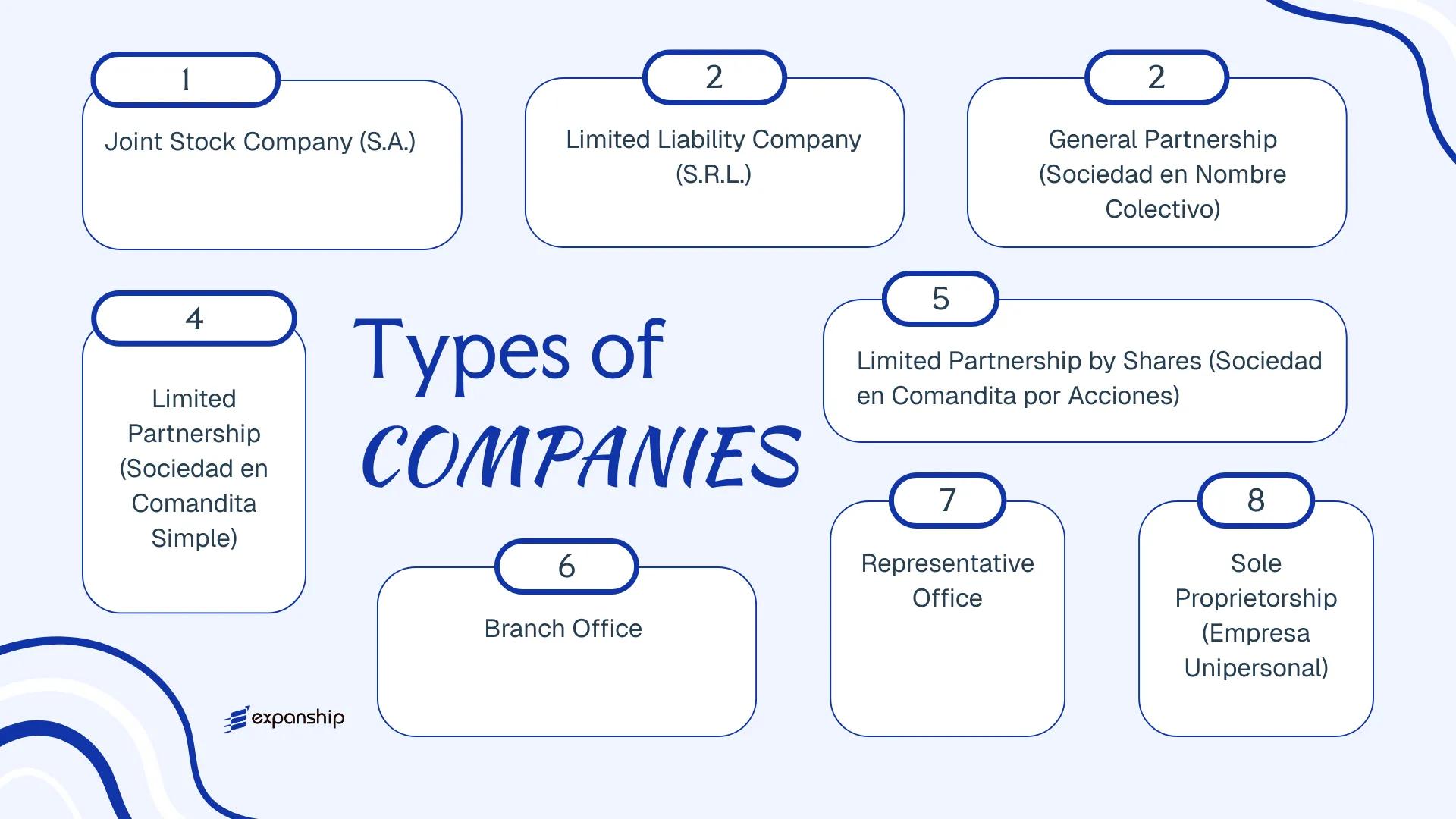

The available business entity types in Paraguay include the Sociedad Anónima (S.A.), the Sociedad de Responsabilidad Limitada (S.R.L.), the Sociedad en Nombre Colectivo, the Sociedad en Comandita Simple, the Sociedad en Comandita por Acciones, the Branch Office, the Representative Office, and the Empresa Unipersonal. Each structure carries distinct requirements around capital, liability, governance, and shareholder composition. This article examines each of these Paraguay company structures in turn, covering formation requirements, ownership rules, and compliance obligations to help you assess which option suits your business objectives.

An Overview of Business Structures in Paraguay

Governed primarily by the Código Civil Paraguayo (Law No. 1183/1985) and supplemented by the Ley de Sociedades Comerciales, the overview of business structures Paraguay offers spans several distinct legal forms, each regulated under a coherent statutory framework. The Registro Público de Comercio, administered through the Dirección General de los Registros Públicos, serves as the central registry for most commercial entities. Each structure carries different implications for liability, ownership, taxation, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima (S.A.) | Joint Stock Company | Limited to share capital | Taxed | Yes | 2 shareholders | Registro Público de Comercio | Código Civil / Ley de Sociedades |

| Sociedad de Responsabilidad Limitada (S.R.L.) | Limited Liability Company | Limited to quota contribution | Taxed | Yes | 2 members (max 25) | Registro Público de Comercio | Código Civil / Ley de Sociedades |

| Sociedad en Nombre Colectivo | General Partnership | Unlimited, joint | Taxed | Yes | 2 partners | Registro Público de Comercio | Código Civil |

| Sociedad en Comandita Simple | Limited Partnership | Mixed (general/limited) | Taxed | Yes | 2 partners | Registro Público de Comercio | Código Civil |

| Sociedad en Comandita por Acciones | Partnership by Shares | Mixed (general/limited) | Taxed | Yes | 2 partners | Registro Público de Comercio | Código Civil |

| Branch Office (Sucursal) | Foreign Branch | Parent bears liability | Taxed on local income | Yes | 1 foreign parent | Registro Público de Comercio | Ley de Sociedades |

| Representative Office | Non-trading presence | Parent bears liability | Generally exempt | No | 1 foreign parent | Ministerio de Industria y Comercio | Ley de Sociedades |

| Empresa Unipersonal | Sole Proprietorship | Limited (if registered) | Taxed | Yes | 1 individual | Registro Público de Comercio | Law No. 1034/1983 |

Each of these structures is examined in full in the sections below.

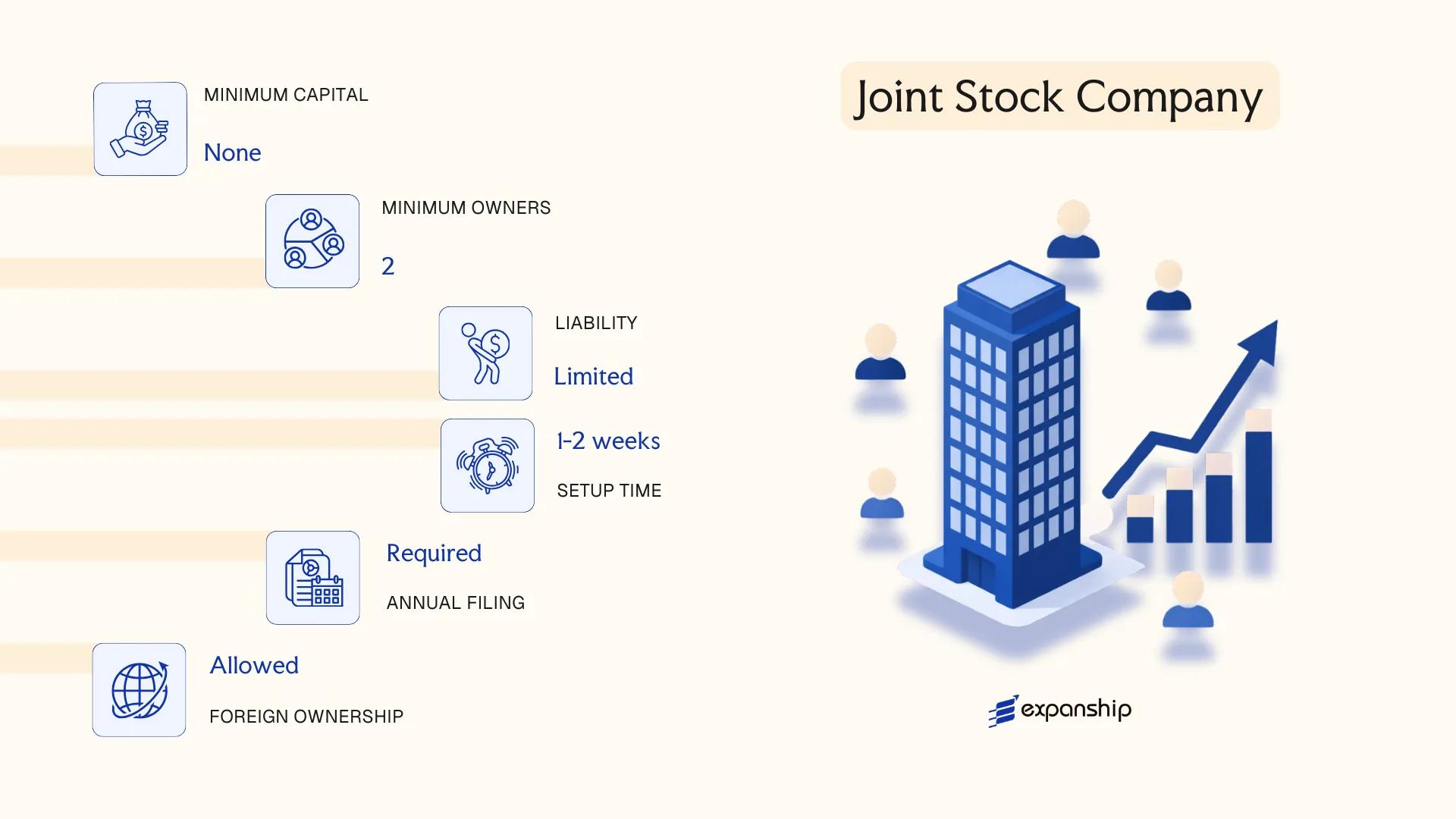

Sociedad Anónima (S.A.) — Joint Stock Company

Paraguay Sociedad Anónima SA formation is governed by the Código Civil Paraguayo (Law No. 1183/1985), which establishes the S.A. as a separate legal entity with full juridical personality distinct from its shareholders. Liability is limited to each shareholder's capital contribution.

Shares are freely transferable by default, which makes this structure suitable for businesses anticipating changes in ownership or future investment rounds. The entity can issue multiple share classes, and share capital is divided into negotiable instruments rather than quotas.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima (S.A.) | Governed by Law No. 1183/1985 |

| Members | Shareholders; minimum 2, no statutory maximum | No nationality restrictions on shareholders |

| Management | Board of Directors; minimum 3 directors | Directors need not be residents |

| Local Presence | Registered legal address in Paraguay required | No mandatory resident director, but a fiscal domicile is needed |

| Capital | Minimum share capital set by the SUACE registration process; denominated in Paraguayan Guaraní (PYG) | No paid-up minimum prescribed by the Civil Code; capital must be fully subscribed at incorporation |

| Privacy | Bearer shares are prohibited; registered shares required | Shareholder information filed with SUACE and Abogacía del Tesoro |

Focus Points

- Taxation: Subject to Impuesto a la Renta Empresarial (IRE) at 10% on net income; VAT applies at 10% (5% on certain goods); dividend distributions to non-residents attract a 15% withholding tax; no stamp duty on share transfers.

- Annual Compliance: Annual financial statements must be submitted to the Ministerio de Hacienda; larger entities may require external audit.

- Economic Substance: No formal economic substance legislation currently in force, though a registered fiscal address and operational records are standard requirements.

- Treaty Access: Paraguay has a limited tax treaty network; S.A. entities are generally eligible for any applicable bilateral agreements.

- Conversion: An S.A. may be converted into an S.R.L. or other recognised form through a notarial deed and re-registration with SUACE.

Closing

The S.A. suits holding structures, larger trading operations, and businesses requiring transferable share capital or multiple investor classes. Its primary advantage is unrestricted share transferability; the principal limitation is the three-director minimum, which adds administrative overhead for small operations.

This entity type is most appropriate for medium-to-large businesses, joint ventures, or foreign investors seeking a scalable ownership structure with freely transferable shares.

Company Incorporation in Paraguay

Incorporate a Sociedad Anónima or other legal entity in Paraguay with end-to-end support from registration through compliance.

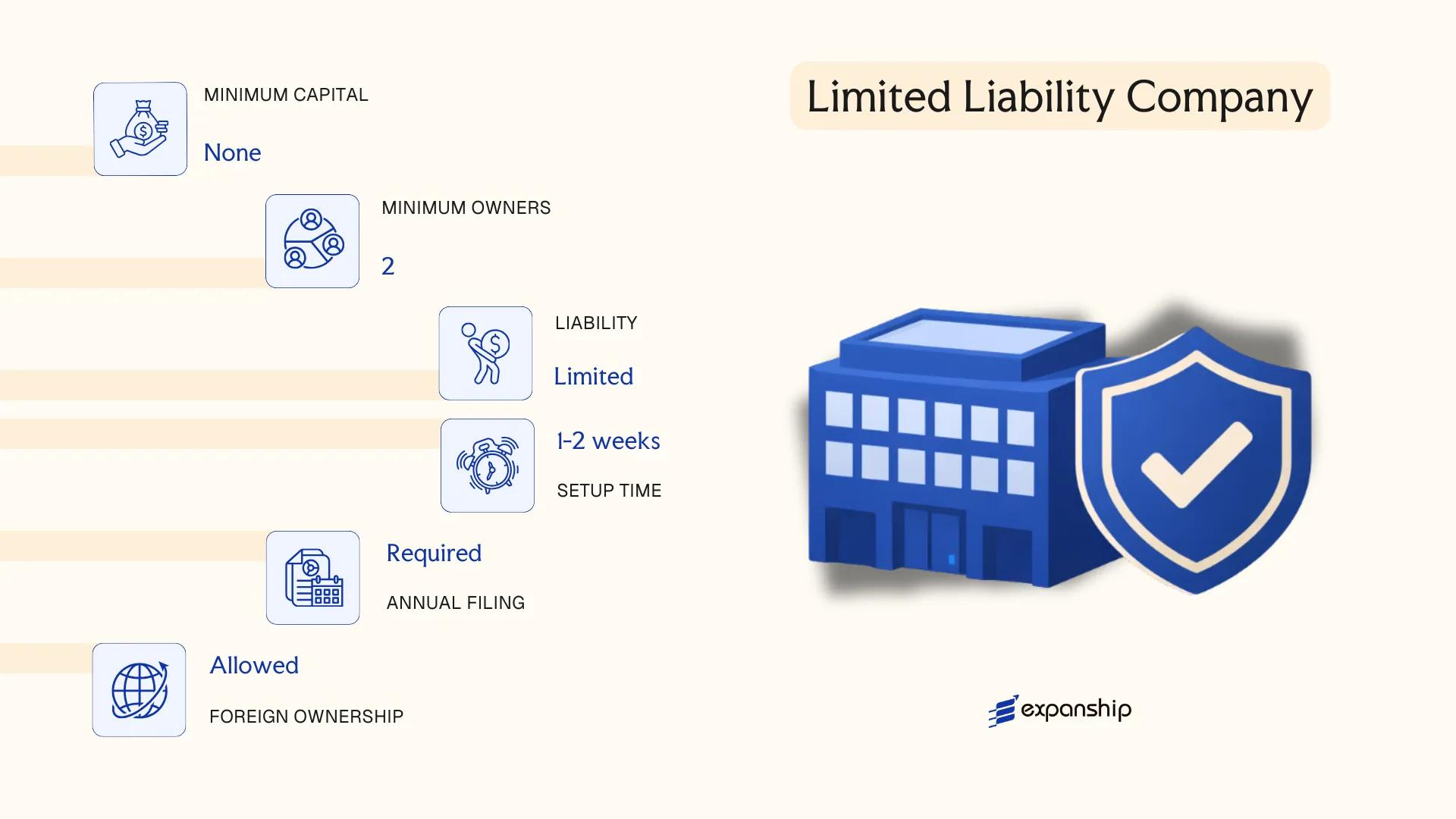

Sociedad de Responsabilidad Limitada (S.R.L.) — Limited Liability Company

The Paraguay SRL limited liability company is governed by the Civil and Commercial Code (Law No. 1183/1985), specifically the provisions covering commercial companies. It holds separate legal personality from its members, meaning the entity bears its own rights and obligations independently of the individuals behind it.

Liability is capped at each member's capital contribution. This hybrid structure combines elements of a partnership-style management with the liability protections of a share-based company, making it a widely used vehicle for small to medium-scale operations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad de Responsabilidad Limitada | Separate legal personality; governed by Law No. 1183/1985 |

| Members | 2 to 25 cuotapartistas (quota holders) | No distinction between voting and non-voting classes |

| Management | One or more gerentes (managers) | Need not be members; no board requirement |

| Local Presence | Registered address in Paraguay required | A registered agent is not mandated but a local domicile is |

| Capital | No statutory minimum; denominated in Paraguayan Guaraní (PYG) | Divided into cuotas (quotas), not shares |

| Privacy | Member names filed with SUNAT/SET and public registry | No public share register equivalent, but member identity is disclosed |

Focus Points

- Taxation: Subject to corporate income tax (IRACIS) at 10%, VAT at 10% on applicable transactions, and dividend withholding tax of 15% on distributions to non-residents; no stamp duty on routine transactions.

- Annual Compliance: Annual financial statements and tax filings required with the Subsecretaría de Estado de Tributación (SET); no mandatory audit unless thresholds are met.

- Transfer Restrictions: Quota transfers require consent of members holding at least 75% of capital, per the Civil and Commercial Code.

- Treaty Access: Paraguay has a limited tax treaty network; SRLs may not benefit from reduced withholding rates in most cross-border structures.

- Conversion: An SRL can be converted into an S.A. through a formal restructuring process recorded before a Paraguayan notary and registered with the public registry.

Closing

The SRL suits trading operations, family-owned businesses, and joint ventures where the number of participants is limited and close management control is preferred. The 25-member cap, however, restricts scalability if the ownership base is expected to grow.

Small to medium businesses with a defined group of investors who require liability protection without the administrative overhead of a full joint-stock structure.

Partnerships [Sociedad en Nombre Colectivo, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones]

Paraguay partnership business structures are governed by the Código Civil paraguayo (Law No. 1183/1985) and the Código de Comercio, which collectively define the formation, liability, and operational rules for each partnership form.

All three types acquire separate legal personality upon registration with the Registro Público de Comercio, distinguishing them from informal business arrangements. Liability treatment varies significantly across the three forms, making the choice of structure a consequential decision.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Commercial partnership with legal personality | Registered under the Código de Comercio |

| Members | Partners (socios or accionistas depending on type); minimum 2, no statutory maximum | General partners bear unlimited liability; limited partners' exposure depends on sub-type |

| Local Presence | Registered domicile in Paraguay required | A local registered address must be maintained with the Registro Público de Comercio |

| Capital | No statutory minimum in Guaraníes (PYG); contributions defined in the partnership deed | Comandita por Acciones issues shares for limited partner capital |

| Privacy | Partner names appear in public registration records | No confidentiality equivalent to nominee arrangements |

Focus Points

- Taxation: Partnerships are generally treated as pass-through or transparent entities for IRACIS (corporate income tax) purposes, though taxable income attribution depends on structure; VAT and withholding tax obligations apply to commercial activities.

- Annual Compliance: Annual financial statements must be filed; general partners remain personally liable for filing defaults.

- Restrictions: Foreign nationals may act as general partners but must comply with residency and documentation requirements under Paraguayan commercial law.

- Conversion: Conversion to an S.A. or S.R.L. is permitted through a formal restructuring process requiring notarial deed and Registro Público de Comercio re-registration.

Sub-Types

Sociedad en Nombre Colectivo

All partners carry unlimited, joint, and several liability for the firm's obligations. This structure is uncommon in modern commercial practice and is typically used only in small, closely held family businesses where partners accept full personal exposure.

Sociedad en Comandita Simple

This form separates general partners (socios gestores), who bear unlimited liability and manage the business, from limited partners (socios comanditarios), whose liability is capped at their agreed capital contribution. The Sociedad en Comandita Paraguay structure suits arrangements where passive investors wish to participate without operational responsibility.

Sociedad en Comandita por Acciones

Limited partner interests are divided into transferable shares (acciones), while general partners retain unlimited liability. This hybrid form bridges partnership and corporate mechanics, making Paraguay limited partnership registration under this sub-type relevant for ventures requiring capital fungibility alongside a defined management layer.

When to Use a Partnership Structure

Partnership forms in Paraguay suit professional firms or family-controlled ventures where the partners are known to one another and governance complexity is to be minimised. The primary advantage is structural flexibility in defining capital contributions and profit distribution. The principal drawback is the unlimited personal liability carried by at least one general partner in all three forms.

These structures are best suited for closely held businesses or joint ventures between identified parties who accept defined liability roles and do not require the full liability shield of a corporate entity.

Foreign Business Structures [Branch Office, Representative Office]

Foreign companies seeking a presence in Paraguay without incorporating a separate local entity have two primary options: the branch office (Sucursal) and the representative office (Oficina de Representación). Both are governed by the Paraguayan Commercial Code (Código de Comercio) and registration is handled through the Public Registry of Commerce (Registro Público de Comercio).

A branch office is not a legally separate entity from its parent company. The foreign firm retains full liability for the branch's obligations. Foreign branch office registration in Paraguay requires submitting authenticated copies of the parent company's constitutive documents, proof of legal existence, and a board resolution authorizing operations in the country.

Key Characteristics

| Requirement | Branch Office (Sucursal) | Representative Office (Oficina de Representación) |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Liability | Parent bears full liability | Parent bears full liability |

| Commercial Activity | Permitted | Not permitted; promotional only |

| Local Representative | Mandatory (resident legal representative) | Mandatory (resident contact person) |

| Minimum Capital | No statutory minimum, but parent's capital documented | No statutory minimum |

| Registration Body | Registro Público de Comercio | Registro Público de Comercio |

| Tax Registration | Required (RUC with SET) | Generally required if any local payments occur |

Focus Points

- Taxation: Branch profits are subject to the standard corporate income tax (IRACIS) at 10%; VAT at 10% applies to taxable supplies; withholding taxes apply on remittances to the parent company abroad.

- Economic Substance: No formal substance regime exists, but the branch must maintain a registered local address and an appointed legal representative.

- Annual Compliance: Annual financial statements must be filed with tax authorities; the branch must maintain accounting records locally under Paraguayan standards.

- Treaty Access: Paraguay has a limited tax treaty network; branch operations may not benefit from double taxation relief in most cases.

- Restrictions: A representative office cannot invoice clients, generate local revenue, or sign commercial contracts on its own behalf.

Sub-Types

Branch Office (Sucursal)

Authorized to conduct full commercial and operational activities in Paraguay, the branch functions as an operational extension of the foreign parent. It is commonly used by firms seeking to trade, contract, or deliver services directly without establishing a separate subsidiary.

Representative Office (Oficina de Representación)

Restricted to liaison, marketing, and promotional activities, this structure cannot generate local revenue. It suits foreign companies conducting market research or coordinating regional operations before committing to a fuller commercial presence.

Closing

Branch offices serve foreign firms that require direct operational capacity without the administrative overhead of a locally incorporated subsidiary; the representative office suits preparatory or non-commercial mandates where revenue generation is not intended. The primary limitation of either structure is that the parent company remains fully exposed to local liabilities.

Foreign companies testing the Paraguayan market or managing regional operations centrally, where a separate legal entity is not operationally necessary.

Sole Proprietorship [Empresa Unipersonal]

The Paraguay Empresa Unipersonal sole proprietorship is governed by Law No. 1034/1983 (Código del Comerciante) and subsequent regulatory provisions that formalized single-owner commercial activity. Unlike a partnership or corporation, this structure involves no separation between the owner's personal assets and business liabilities under the traditional framework.

Registration is handled through the Registro Público de Comercio, and the proprietor operates under their own name or a trade name, bearing full personal liability for all obligations incurred by the business.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Empresa Unipersonal) | No separate legal personality from the owner |

| Owner Reference | Proprietor (Titular) | Single natural person only; legal entities may not form this structure |

| Membership | 1 proprietor (minimum and maximum) | No co-owners permitted |

| Local Presence | Registered business address in Paraguay | Physical or fiscal address required for registration |

| Capital | No statutory minimum capital requirement | Capital is declared at registration but not mandated by law |

| Privacy | Owner's name appears in public commercial registry | Limited privacy; full personal identification is publicly recorded |

Focus Points

- Taxation: Subject to personal income tax (Impuesto a la Renta Personal) on business profits; VAT applies to taxable transactions at 10% (standard) or 5% (reduced); no corporate income tax applies since profits flow directly to the individual.

- Annual Compliance: Annual income declarations must be filed with the Subsecretaría de Estado de Tributación (SET); commercial books must be maintained per the Código del Comerciante.

- Liability: The proprietor bears unlimited personal liability; business debts are recoverable against personal assets.

- Conversion: The structure can be converted into an S.R.L. or S.A., though this requires a formal incorporation process rather than a simple administrative change.

- Treaty Access: Access to Paraguay's tax treaty network is limited for sole proprietors, as most treaties apply to corporate residents rather than individuals operating commercially.

Recommendations

The Empresa Unipersonal suits low-volume domestic trading, freelance service providers, and small-scale commercial activity where administrative simplicity outweighs the need for liability protection. The primary advantage is minimal setup cost and regulatory burden; the significant drawback is unlimited personal liability, which exposes the owner's personal estate to all business creditors.

This structure is best suited for resident individuals conducting small-scale domestic commerce who do not require liability separation or plan to raise external capital.

How to Choose the Right Entity Type in Paraguay

Choosing the right company type in Paraguay has direct legal and financial consequences that extend well beyond the registration stage.

Why Your Entity Choice Matters

The structure you register determines your obligations under Paraguayan law from day one. Selecting the wrong entity type can produce concrete, costly outcomes:

- Operating a branch without registering under the Código Civil (Law No. 1183/1985) exposes a foreign entity to penalties and potential forced closure by the Abogacía del Tesoro.

- Forming an S.A. when a single-person consultancy is all you need subjects you to mandatory board composition requirements and annual assembly obligations that generate recurring administrative costs without operational benefit.

- Registering under a structure that does not qualify for Paraguay's treaty network prevents you from claiming withholding tax reductions in counterpart jurisdictions.

- Choosing an entity with insufficient substance capacity when local tax residency is asserted can trigger reclassification by the Subsecretaría de Estado de Tributación (SET).

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each correspond to distinct structural requirements under Paraguayan commercial law.

- Ownership Configuration: A sole owner operating locally will find the Empresa Unipersonal more proportionate than a multi-shareholder S.A. structure.

- Tax Objectives: Your eligibility for specific regimes under the Ley de Modernización y Simplificación del Sistema Tributario (Law No. 6380/2019) depends on the entity type selected.

- Privacy Requirements: Shareholder information in an S.A. is filed with the Registro Público de Comercio, which affects confidentiality planning.

- Exit Strategy: Not all Paraguayan entity types permit redomiciliation or structural conversion without full dissolution and re-registration.

The full text of the primary corporate legislation is available via the official Paraguayan legal database.

Compliance Services for Companies in Paraguay

Ongoing compliance support for Paraguayan entities, including annual filings, SET obligations, and corporate maintenance.

Conclusion

Selecting the right structure is the first binding decision you make when incorporating a company in Paraguay, and each form carries distinct legal and operational consequences. The S.A. suits larger ventures requiring share transferability and capital market access, while the S.R.L. remains the most commonly registered entity, favored by small to medium-sized businesses for its manageable compliance obligations. Partnerships serve operators who accept personal liability in exchange for structural simplicity. Branch offices bind a foreign parent directly to local liabilities, whereas a representative office restricts commercial activity by definition. The Empresa Unipersonal fits sole traders operating without partners.

Paraguay's gradual expansion of bilateral investment treaties and its territorial tax system continue to attract foreign registrants. Your choice of entity will be governed by the Código Civil and administered through the Registro Público de Comercio, making early legal review a practical step before submission.

How Expanship Can Assist You

Expanship's Paraguay company formation services cover the full incorporation process, from selecting the right structure under the Paraguayan Civil and Commercial Code to registering your entity with the Registro Público de Comercio. Having guided clients through S.A. and S.R.L. formations, branch office registrations, and ongoing compliance obligations, we handle the administrative and legal coordination so you can focus on running your business.

Our corporate services in Paraguay include:

- Document preparation, notarization, and apostille legalization

- Registered agent and local office provision

- Government filings and liaison with the Registro Público de Comercio

- Tax identification (RUC) registration with the Subsecretaría de Estado de Tributación

- Post-incorporation compliance management, including annual reporting

- Banking introduction assistance for opening corporate accounts in Paraguay

Reach out to Expanship Paraguay to discuss your specific requirements with our corporate services team.

Frequently Asked Questions (FAQ)

The Sociedad de Responsabilidad Limitada (S.R.L.) is the most frequently formed structure. Its lower capital requirements, simplified governance, and suitability for small-to-medium operations make it the default choice for both resident entrepreneurs and foreign investors entering the market.

An S.A. can issue transferable shares to an unlimited number of shareholders and is subject to more extensive disclosure and auditing obligations under the Commercial Code, while an S.R.L. restricts quota transfers and caps membership at fifty quotaholders. Both entities are subject to the standard corporate income tax rate administered by the Subsecretaría de Estado de Tributación (SET), though the S.A. structure is generally required for public offerings or larger institutional arrangements.

The S.R.L. provides a comparatively higher degree of confidentiality, as quota ownership is recorded in the company's internal registry rather than a fully public shareholder register. Nominee arrangements are legally permissible, though beneficial ownership disclosure requirements have expanded under anti-money laundering regulations in recent years.

No. An S.R.L. requires a minimum of two quotaholders, and all partnership forms — including the Sociedad en Nombre Colectivo and Sociedad en Comandita Simple — require at least two partners by definition. Only the Empresa Unipersonal is structured specifically for a single natural person operating as a sole trader.

Foreigners may form an S.A. or S.R.L. without restrictions on nationality, and they may also establish a Branch Office of a foreign entity registered through the Registro Público de Comercio. A foreign national acting as a director or quotaholder does not require local residency, though a registered legal address within the country is mandatory for all entities.

Conversion between entity types is permitted under the Paraguayan Commercial Code through a formal transformation process, which requires a notarized deed, amendment of the constituent documents, and re-registration with the Registro Público de Comercio. An S.R.L. may be converted into an S.A. provided the statutory requirements for the new form are met, including any minimum capital thresholds.

The S.A., S.R.L., Sociedad en Comandita por Acciones, and Sociedad en Nombre Colectivo all hold separate legal personality distinct from their members. The Empresa Unipersonal does not create a separate legal person — the individual owner and the business remain legally unified, which carries direct implications for personal liability exposure.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.