Key Takeaways

- Palau recognizes eight distinct business entity types, ranging from C Corporations and S Corporations under the Business Corporation Act to sole proprietorships, each governed by separate legislative frameworks.

- The Office of the Registrar of Corporations under the Republic of Palau's Ministry of Finance administers company registration across all entity types.

- Foreign entities can establish a presence in Palau without creating a separate legal person by registering as a branch office, representative office, or foreign corporation.

- Palau's territorial tax system means foreign-sourced income is generally not subject to domestic taxation, a consideration that directly affects entity selection for internationally oriented businesses.

Introduction to Entity Types in Palau

Palau is an archipelago nation in the western Pacific Ocean, situated east of the Philippines and north of Indonesia, and a member of the Compact of Free Association with the United States. As a sovereign republic, it maintains its own legal and commercial framework, with company registration administered by the Office of the Registrar of Corporations under the Republic of Palau's Ministry of Finance. The country operates a territorial tax system, meaning foreign-sourced income is generally not subject to domestic taxation.

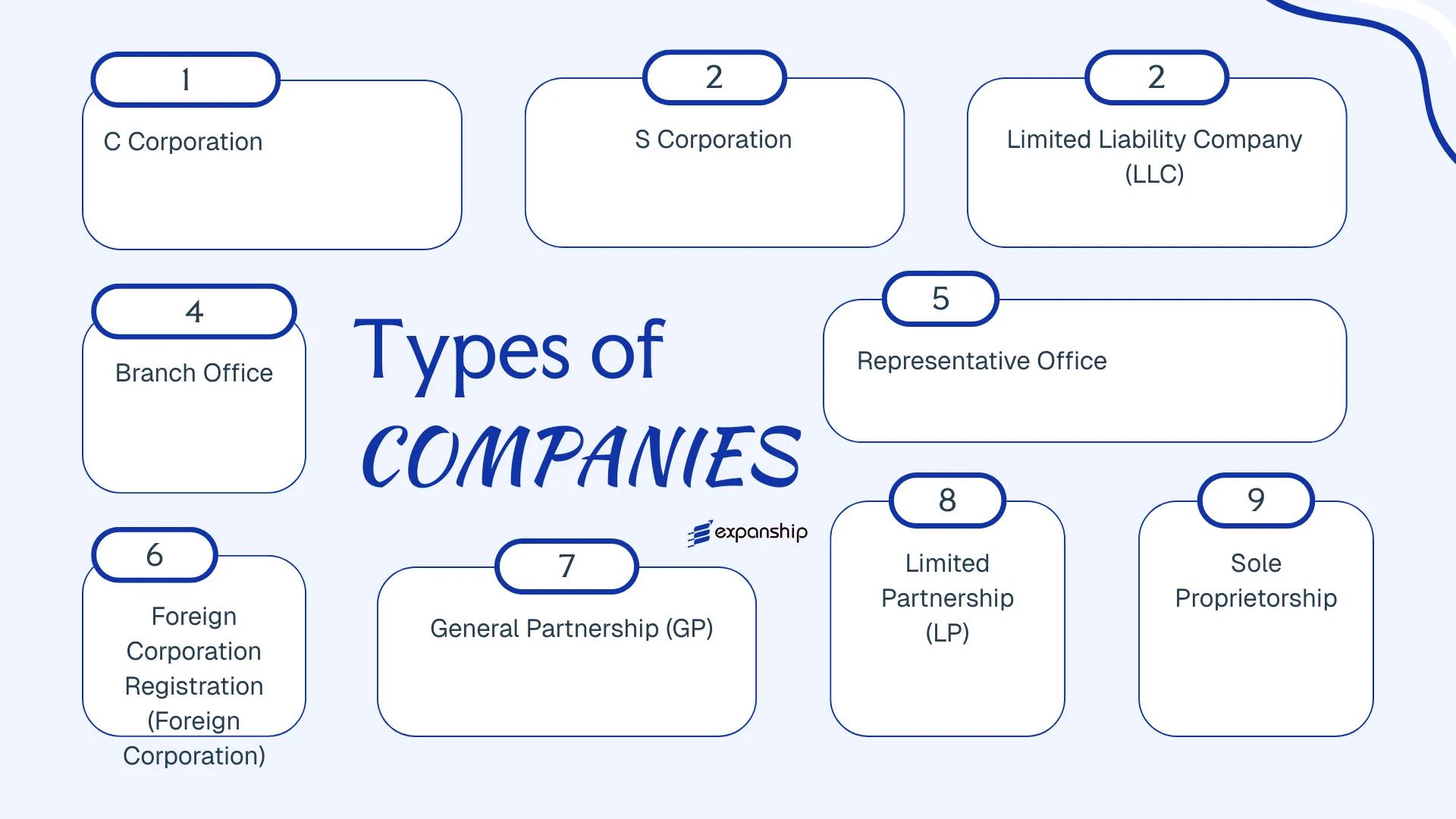

Several distinct business entity types in Palau are available to both resident and foreign investors. These include:

- C Corporation and S Corporation (under the Business Corporation Act)

- Limited Liability Company (LLC)

- General Partnership

- Limited Partnership

- Sole Proprietorship

- Branch Office

- Representative Office

- Foreign Corporation Registration

Each structure carries its own formation requirements, liability treatment, and operational implications. This article examines each option in detail to help you determine which structure aligns with your business objectives.

An Overview of Business Structures in Palau

Palau's company law framework accommodates several distinct entity types, each governed by separate legislation. The primary statutes include the Business Corporation Act, the Palau LLC Act, and general partnership law, among others. Each structure carries different implications for liability, ownership, and tax treatment.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| C Corporation | Separate legal entity | Limited to shareholding | Taxable | Permitted | 1 shareholder | Ministry of Finance | Business Corporation Act |

| S Corporation | Separate legal entity | Limited to shareholding | Pass-through taxation | Permitted | 1 shareholder | Ministry of Finance | Business Corporation Act |

| LLC | Separate legal entity | Limited to membership interest | Taxable / flexible | Permitted | 1 member | Ministry of Finance | Palau LLC Act |

| General Partnership | Not separate | Unlimited, joint | Taxable | Permitted | 2 partners | Ministry of Finance | Partnership law |

| Limited Partnership | Separate legal entity | Limited for LPs; unlimited for GP | Taxable | Permitted | 1 GP, 1 LP | Ministry of Finance | Partnership law |

| Foreign Corporation | Branch of foreign entity | Parent liable | Taxable | Permitted | 1 (parent entity) | Ministry of Finance | Business Corporation Act |

| Sole Proprietorship | No separate entity | Unlimited, personal | Taxable | Permitted | 1 owner | Ministry of Finance | General business law |

Each of these structures is examined in full in the sections below.

Corporation (C Corporation, S Corporation) under the Business Corporation Act

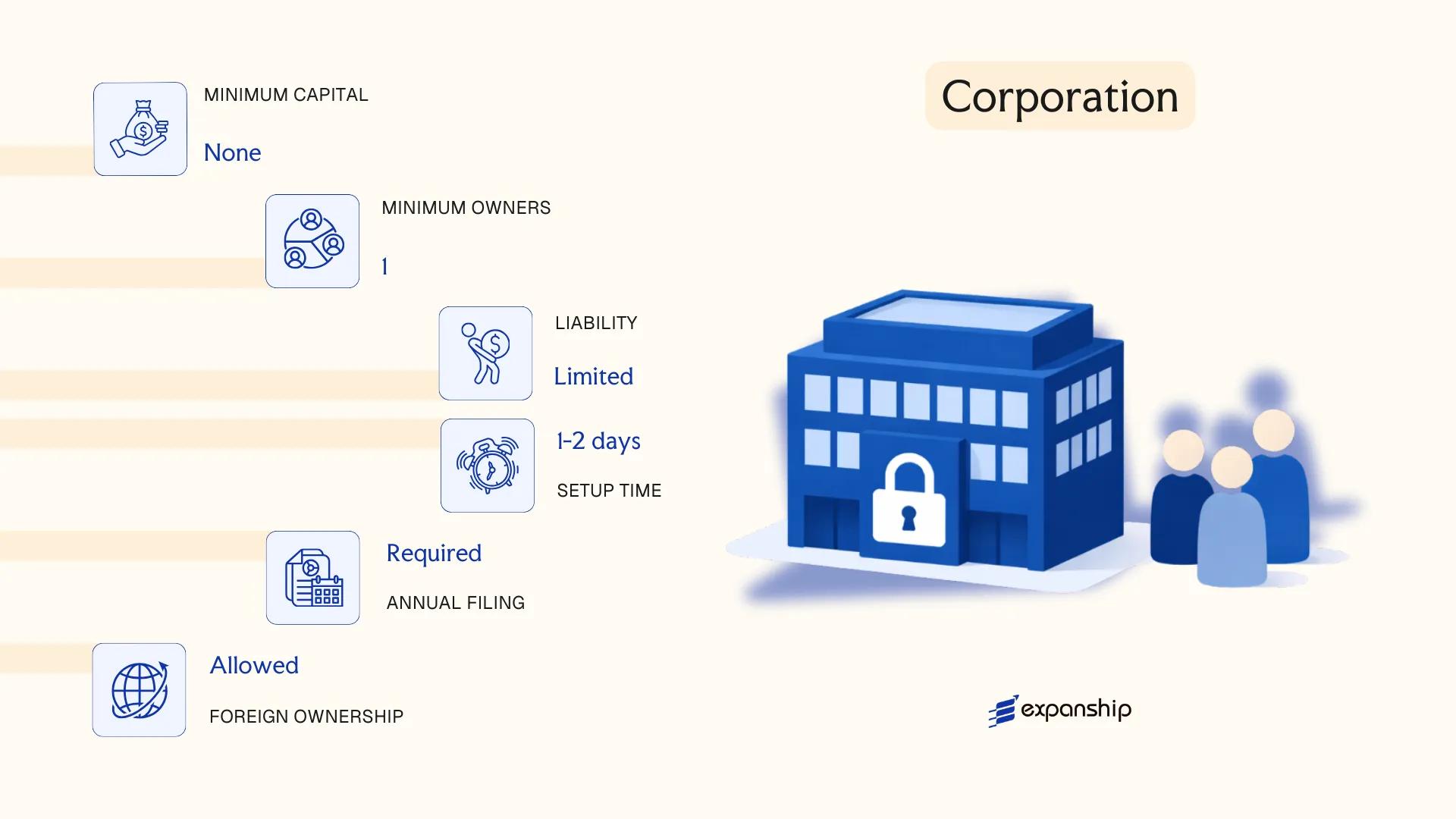

Palau Business Corporation Act registration follows the framework established under the Business Corporation Act of 1990, which governs the formation and operation of domestic corporations. Under this legislation, a corporation exists as a separate legal entity from its shareholders, providing limited liability protection and the capacity to hold property, enter contracts, and sue or be sued in its own name.

Structured as a capital-based entity, a corporation in Palau suits businesses seeking formal governance through a board structure and defined shareholder rights. Both resident and non-resident shareholders may participate in ownership, though restrictions apply to certain business activities reserved for Palauan citizens.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation (separate legal entity) | Governed by the Business Corporation Act 1990 |

| Members | Shareholders, Directors, Officers | Minimum 1 shareholder; no statutory maximum; Directors manage the board |

| Local Presence | Registered Agent required; registered office in Palau | Agent must be a resident or licensed entity |

| Capital | No statutory minimum paid-up capital; USD is standard currency | Authorized share capital defined in Articles of Incorporation |

| Privacy | Shareholder details filed with the Registrar of Corporations | Director information also on public record |

Focus Points

- Taxation: Palau does not levy a corporate income tax, capital gains tax, VAT, or withholding tax on dividends; a gross revenue tax applies to business receipts at graduated rates.

- Annual Compliance: Annual reports and fees are due to the Registrar of Corporations; financial records must be maintained but public filing of accounts is not generally required.

- Economic Substance: No formal economic substance regime is currently enacted, though this may evolve as international standards develop.

- Restrictions: Foreign nationals are restricted from owning corporations engaged in activities reserved for Palauan citizens under the Foreign Investment Act.

- Conversion: A corporation may generally convert to another entity form through formal amendment procedures under applicable statute.

Sub-Types

C Corporation

A C Corporation is the default corporate classification under the Business Corporation Act, with no restrictions on the number or nationality of shareholders. It is commonly used for trading companies, joint ventures, and larger commercial operations requiring a tiered ownership structure.

S Corporation

An S Corporation designation typically refers to a pass-through tax classification used in U.S. federal tax law, where corporate income flows to shareholders' individual tax returns. Because Palau operates outside the U.S. federal tax system, the S Corporation distinction carries limited domestic tax relevance; however, U.S.-connected shareholders may still elect S status for U.S. federal reporting purposes.

Closing

A Palauan corporation suits holding structures, trading entities, and joint ventures where formal governance and limited liability are priorities; the absence of corporate income tax is a material advantage, though foreign ownership restrictions in reserved sectors represent a meaningful constraint on certain business models.

Corporations under the Business Corporation Act are best suited for foreign investors and U.S.-linked entities establishing a formal commercial or holding presence in Palau.

Company Incorporation in Palau

Incorporate a corporation in Palau with support from Expanship across registration, compliance, and ongoing maintenance.

Limited Liability Company (LLC) under the Palau LLC Act

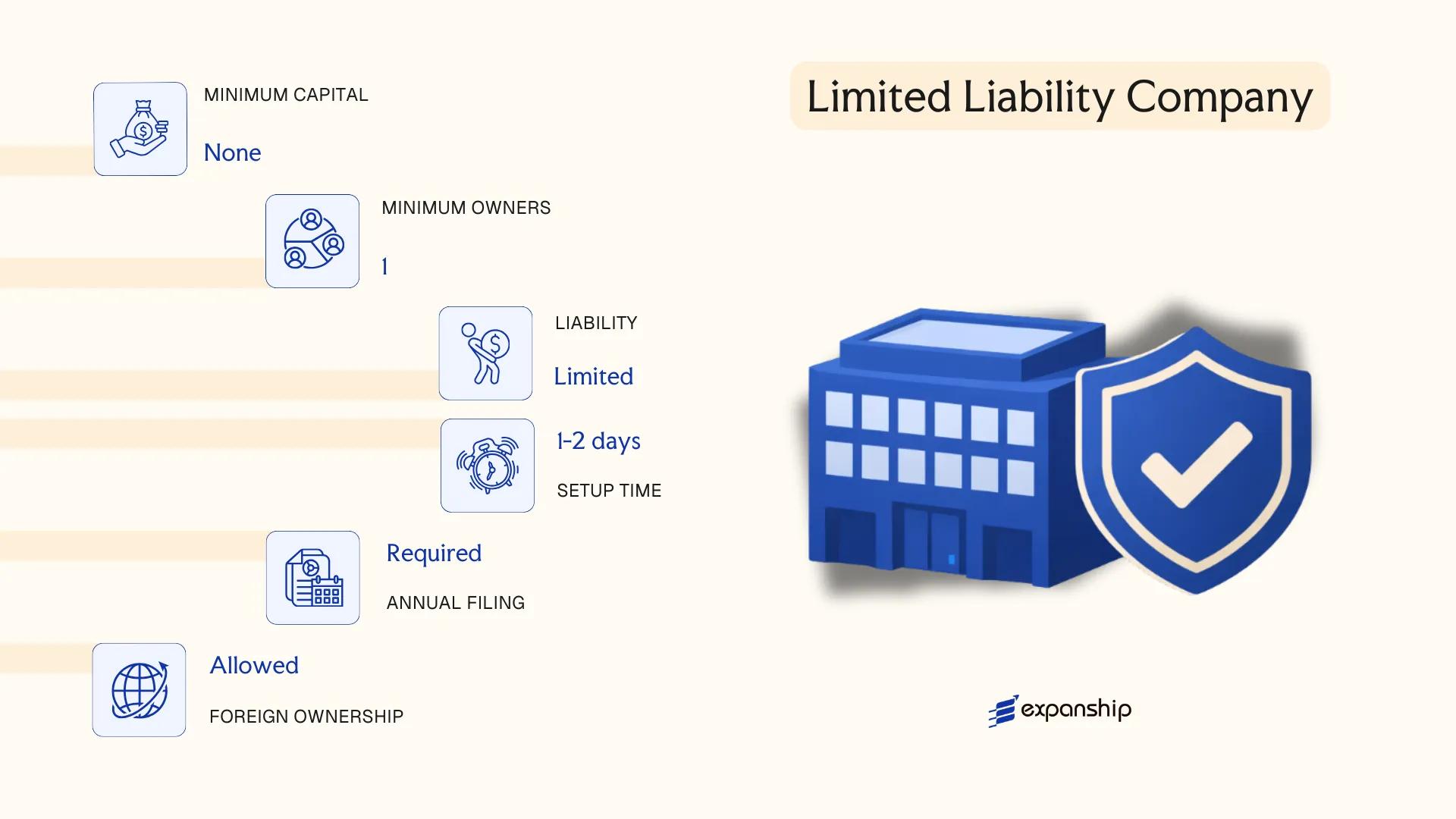

Governed by the Palau Limited Liability Company Act, an LLC is a hybrid structure combining the liability protection of a corporation with the operational flexibility of a partnership. Meeting the Palau LLC formation requirements establishes a separate legal entity, shielding members from personal liability for the company's debts and obligations.

Ownership interests and management responsibilities are defined through an operating agreement, which governs internal affairs where the Act permits private ordering. The Palau LLC operating agreement is not required to be filed publicly, which offers a degree of structural confidentiality.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Separate legal personality; members not personally liable |

| Members | Referred to as Members; minimum 1, no statutory maximum | Single-member LLCs are permitted |

| Management | Member-managed or Manager-managed | Managers need not be members |

| Local Presence | Registered Agent required; registered office in Palau | Agent must be resident or licensed in-country |

| Capital | No statutory minimum; USD is standard | Contributions may be cash, property, or services |

| Privacy | Operating agreement and member details not on public register | Articles of Organization are filed publicly |

Focus Points

- Taxation: Palau does not impose a corporate income tax on foreign-sourced income; local trading activities may attract gross revenue tax obligations, and there is no VAT or general withholding tax regime.

- Annual Compliance: Annual report filing with the relevant registry is generally required to maintain good standing.

- Economic Substance: Substance requirements may apply depending on the nature of activities conducted; professional advice should be sought for specific business types.

- Treaty Access: Palau has a limited tax treaty network, which may restrict access to treaty benefits for cross-border structures.

- Conversion: The LLC Act generally permits conversion to or from other entity types, subject to regulatory approval.

Closing

The LLC suits holding structures, IP ownership arrangements, and trading operations where pass-through flexibility is preferred over a fully capitalized corporate form. Its principal limitation is Palau's narrow treaty network, which can constrain international tax planning.

Foreign investors and small-to-mid-sized businesses seeking limited liability with flexible internal governance and minimal capital requirements.

Foreign Business Entities [Branch Office, Representative Office, Foreign Corporation Registration]

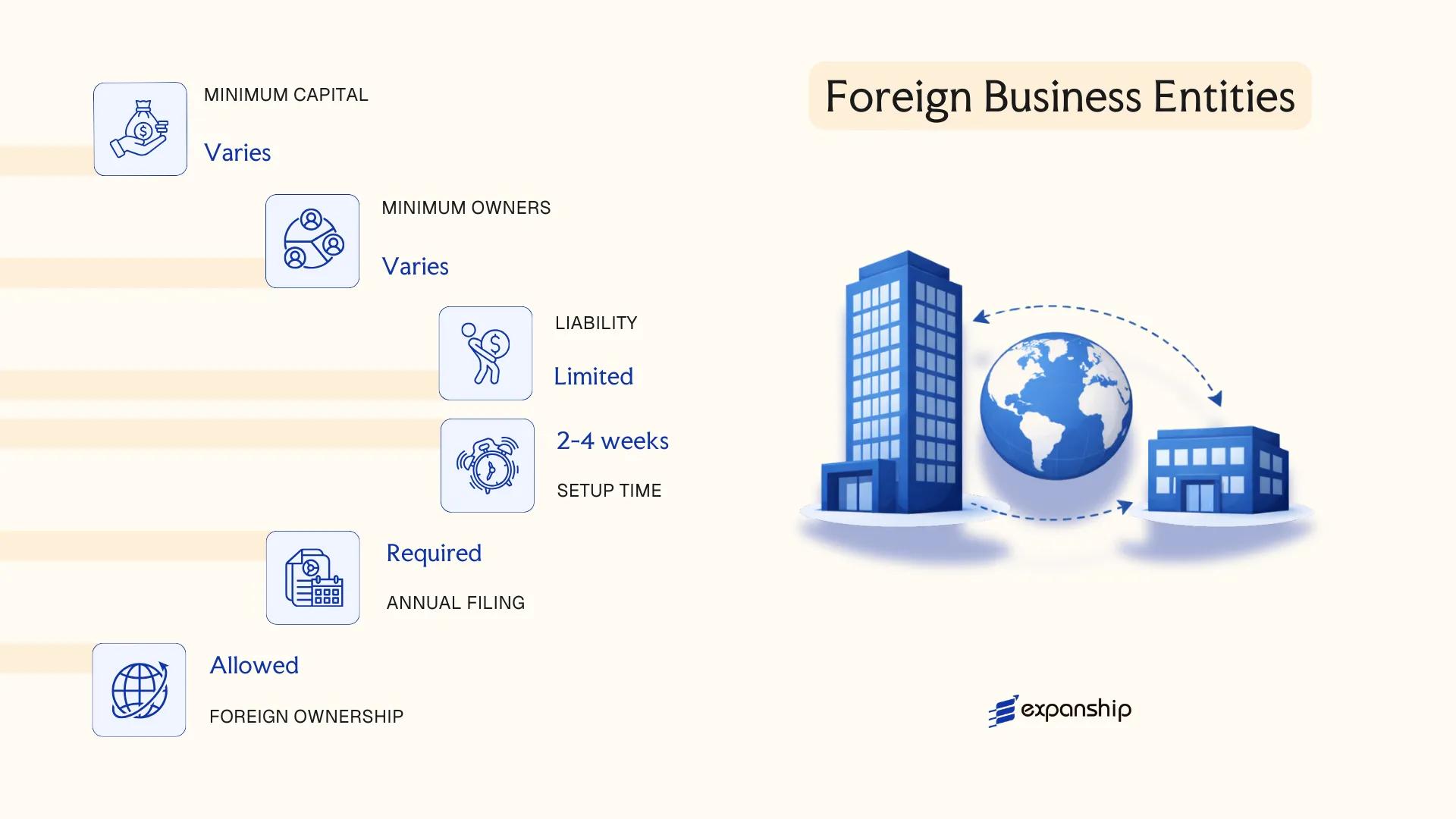

Foreign companies seeking a presence without forming a new domestic entity may pursue foreign corporation registration in Palau under the Foreign Investment Act and related provisions administered by the Foreign Investment Board (FIB). Registration does not create a separate legal person; the foreign parent remains fully liable for the obligations of its registered presence.

Permitted structures include a registered branch, which conducts active commercial operations, and a representative office, limited to liaison and promotional activities without revenue generation. Both require prior FIB approval, and certain sectors remain restricted or closed to foreign participation under Palau's Restricted Business List.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Parent entity bears full liability |

| Authorised Representatives | Resident or appointed local agent | Must be named in FIB application |

| Local Presence | Registered local agent; physical office address required | FIB may verify operational address |

| Capital | No statutory minimum specified | FIB may assess financial capacity during review |

| Privacy | Parent company details disclosed in public registration | Home-jurisdiction documents required |

| Restricted Sectors | Fishing, tourism, retail, and others on Restricted Business List | FIB clearance mandatory before operations |

Focus Points

- Taxation: Palau does not impose corporate income tax, VAT, or withholding tax at the national level; gross revenue tax may apply to certain business activities.

- Annual Compliance: Annual renewal of FIB registration and business licence required; failure to renew results in lapse of operating authority.

- Economic Substance: No formal economic substance regime currently legislated for foreign entities.

- Restrictions: Foreign ownership caps apply in designated sectors; a branch cannot operate outside its approved activity scope.

- Treaty Access: Palau has limited double tax treaty coverage, reducing the relevance of treaty-based structuring for most foreign entities.

Sub-Types

Branch Office

A branch conducts revenue-generating commercial activities directly on behalf of the foreign parent. It is suited to companies needing an operational footprint without the administrative burden of incorporating a separate local entity.

Representative Office

A representative office is restricted to non-commercial functions such as market research, sourcing coordination, and liaison work. It cannot invoice clients, conclude contracts, or repatriate profits, making it unsuitable for active trading.

Closing Note

Foreign entity registration suits multinational firms testing the market or maintaining a regional liaison function, with the principal advantage being speed of establishment relative to full incorporation. The primary limitation is unlimited parental liability, which exposes the home entity to all local obligations.

Foreign corporations exploring market entry or maintaining a non-revenue liaison function before committing to full local incorporation.

Partnerships [General Partnership, Limited Partnership]

Palau recognizes two principal partnership structures under its domestic business legislation: the general partnership and the limited partnership. Limited partnership registration in Palau follows the procedural requirements set out under the Palau Business Corporation Act and related enabling statutes, with formation completed through the Bureau of Revenue, Customs and Taxation (BRCT) of the Ministry of Finance.

Neither form carries separate legal personality in the manner of a corporation. Liability exposure and management authority differ substantially between the two structures, making the choice of form a consequential one for founders.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Members | Partners (minimum 2, no statutory maximum) | At least 1 general partner and 1 limited partner |

| Liability | Unlimited personal liability for all partners | General partner: unlimited; limited partner: capped at capital contribution |

| Local Presence | Registered agent and registered office in Palau required | Registered agent and registered office in Palau required |

| Partnership Agreement | Recommended in writing; governs internal affairs | Written agreement required; filed or referenced at registration |

| Capital | No minimum capital; denominated in USD | No minimum capital; denominated in USD |

| Privacy | Partner details generally on public record at BRCT | General partner details on public record; limited partner details may have limited disclosure |

Focus Points

- Taxation: Palau does not impose a federal corporate income tax or VAT; partnerships are treated as pass-through entities, with partners subject to gross revenue tax on business income derived within Palau.

- Annual Compliance: Annual renewal filings and applicable fees are due to the BRCT; failure to renew risks administrative dissolution.

- Treaty Access: Palau has a limited tax treaty network, which restricts treaty-based withholding tax relief for partnership income distributed to foreign partners.

- Restrictions: Foreign nationals face ownership restrictions in certain sectors under Palauan foreign investment law, regardless of the partnership structure chosen.

- Conversion: Conversion from a general to a limited partnership, or to a corporate form, is permissible but requires amended filings with the BRCT.

Sub-Types

General Partnership

All partners hold equal management rights and bear joint and several liability for the firm's obligations. This structure suits small, domestically focused operations where co-founders intend to share both control and risk without a formal separation of roles.

Limited Partnership

One or more general partners manage the business and carry unlimited liability, while limited partners contribute capital and are shielded from personal liability beyond their investment. This arrangement is commonly used for investment vehicles or project-specific ventures where passive investors require defined exposure.

When to Consider a Partnership

Partnership structures in Palau suit small domestic ventures and joint ventures where pass-through taxation is preferred. The absence of a minimum capital requirement lowers the entry threshold, though the unlimited liability of general partners represents a significant structural risk for high-exposure commercial activities.

Partnerships are most appropriate for small domestic co-ventures and locally active traders where two or more founders seek a simple, low-cost structure with pass-through tax treatment.

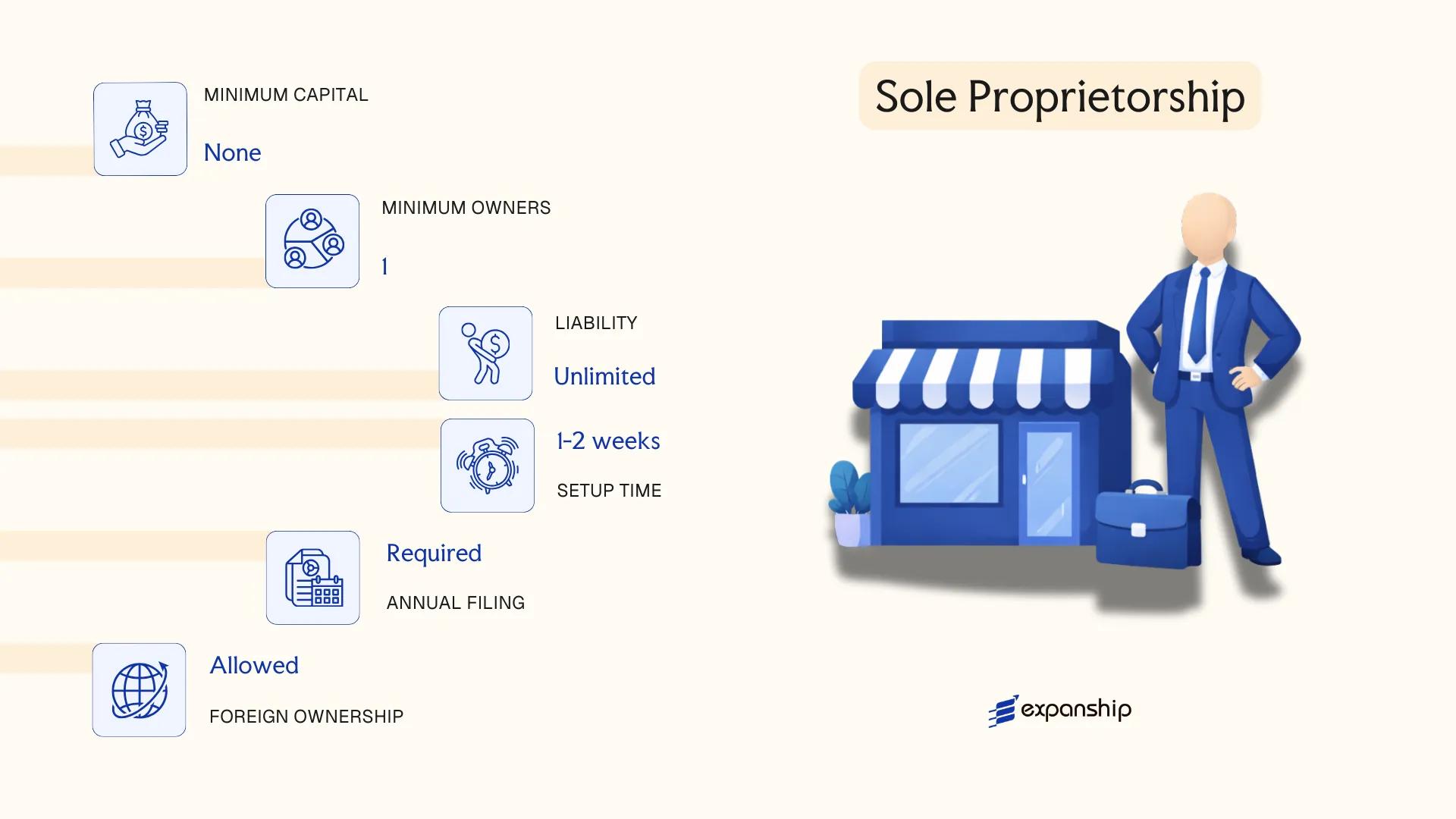

Sole Proprietorship

Sole proprietorship registration in Palau falls under the general business licensing framework administered by the Bureau of Revenue and Taxation, as there is no dedicated sole proprietorship statute separate from the general business registration requirements. This structure carries no separate legal personality — the owner and the business are treated as a single legal unit, meaning personal assets are directly exposed to any business liabilities.

Registration typically involves obtaining a business license from the relevant authority and, where the business operates under a trade name, registering that name separately. Foreign nationals should note that Palauan law restricts certain business activities to citizens or entities with qualifying local ownership.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Owner Title | Proprietor | Single individual only; no co-owners |

| Membership | 1 proprietor (minimum and maximum) | Cannot have partners or co-owners without changing structure |

| Local Presence | Business license; registered trade name if applicable | Physical address in Palau required for licensing |

| Capital | No statutory minimum; Palauan Dollar (USD) | USD is the functional currency in Palau |

| Privacy | Owner's name linked to business registration | No structural confidentiality available |

Focus Points

- Taxation: Subject to Palau's gross revenue tax; no separate corporate income tax applies, but the proprietor is personally liable for all tax obligations on business income.

- Annual Compliance: Business license must be renewed annually with the Bureau of Revenue and Taxation.

- Foreign Ownership Restrictions: Certain sectors are reserved for Palauan citizens under the Foreign Investment Act; foreign nationals may face activity limitations.

- Conversion: Can be converted into a corporation or LLC if the business outgrows the sole proprietorship structure, though this requires full re-registration.

Closing

A sole proprietorship suits local residents or Palauan citizens operating small-scale service or trading businesses where administrative simplicity outweighs the need for liability protection. The primary limitation is unlimited personal liability, which exposes the proprietor's personal assets to all business debts and claims.

Local Palauan citizens or residents running low-risk, single-owner businesses who prioritize minimal setup costs and administrative overhead over liability protection.

How to Choose the Right Entity Type in Palau

Choosing the right business entity in Palau is a structural decision with binding legal and financial consequences — not a preference to revisit casually.

Why Your Entity Choice Matters

Selecting the wrong structure from the outset produces specific, avoidable problems:

- Registering a foreign corporation when you intend to conduct local trade without complying with the Business Corporation Act constitutes unlawful operation and may result in administrative penalties or involuntary dissolution.

- Choosing a tax-exempt entity when your business requires access to withholding tax reductions under a bilateral agreement disqualifies your firm from claiming those reductions in counterpart jurisdictions.

- Forming a corporation when your purpose is asset protection or succession planning locks your structure into annual shareholder meeting obligations and capital requirements that do not apply to trust arrangements.

- Selecting an entity that mandates audited financial statements for a single-person consulting operation introduces recurring professional costs that serve no regulatory purpose at that scale.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each correspond to a distinct entity type under Palauan law.

- Local vs. Offshore Operations: If your business will transact with Palauan residents, a locally registered corporation or LLC is required rather than a foreign entity registration.

- Ownership and Management: Single-owner operations and those requiring flexible governance structures are better served by the LLC form, while multi-party ventures with formal board requirements point toward a corporation.

- Tax Objectives: Your need for full exemption, a specific territorial treatment, or eligibility under a particular regime should determine the entity before other factors are considered.

- Substance Capacity: If you cannot realistically maintain personnel or decision-making functions within the jurisdiction, your entity choice must account for any applicable substance thresholds.

- Exit Strategy: Not all entity types in Palau permit redomiciliation or conversion; confirm the available exit mechanisms before committing to a structure.

Compliance Services for Companies in Palau

Ongoing compliance support for Palauan corporations, LLCs, and foreign-registered entities, including annual filings and regulatory obligations.

Conclusion

Palau company incorporation concludes with a relatively contained menu of structures, each governed by distinct legislation. Corporations formed under the Business Corporation Act suit ventures requiring shareholder investment and formal governance, while the LLC Act offers a more flexible arrangement for smaller or domestically focused operations. General and limited partnerships work for businesses where profit-sharing arrangements between known parties take precedence over liability separation. Branch offices and representative offices serve foreign entities testing or maintaining a market presence without establishing a separate legal person. Sole proprietorships remain accessible but carry unlimited personal liability.

Domestic corporations and LLCs account for the majority of registered entities, reflecting the typical preference for limited liability structures. Regulatory oversight by the relevant government ministries has trended toward greater documentation requirements, consistent with broader Pacific region compliance standards. Your choice of entity will ultimately rest on ownership structure, liability tolerance, and the nature of intended operations — factors that Expanship's advisors routinely work through with clients entering this jurisdiction.

How Expanship Can Assist You

Expanship Palau company registration services cover every entity structure discussed in this guide — from domestic corporations formed under the Business Corporation Act to LLCs governed by the Palau LLC Act and foreign entities registering with the Office of the Attorney General. Each structure carries distinct filing obligations, and Expanship works with you to meet them accurately from the outset.

Our services span the full setup and maintenance cycle:

- Document preparation, notarization, and legalization

- Registered agent and local office provision

- Government filing and liaison with the Palau registrar

- Post-incorporation compliance management

- Banking introduction assistance

From initial incorporation to ongoing annual reporting, your business has a single point of contact for all regulatory requirements in the jurisdiction.

Ready to move forward? Reach out to Expanship Palau to discuss your setup.

Frequently Asked Questions (FAQ)

The corporation formed under the Business Corporation Act is the most frequently registered structure, largely because it offers familiar governance mechanics, clear liability separation, and eligibility for foreign ownership without restrictions on share structures.

A corporation is subject to Palau's standard corporate tax regime and carries more formal compliance obligations, including board requirements and annual reporting. An LLC formed under the Palau LLC Act offers pass-through tax treatment and greater operational flexibility. Local trading rights are available to both, though each requires a business license from the relevant authority.

The LLC generally provides more privacy, as member details may not be fully disclosed in public filings depending on the operating agreement structure. Nominee arrangements are available for both corporations and LLCs, though their legal recognition depends on applicable provisions under each governing act.

A sole proprietorship and an LLC can each be formed by one individual. Partnerships, by definition, require a minimum of two partners, and corporations require at least one director and one shareholder, which may be the same person.

Corporations and LLCs are both accessible to foreign nationals under Palau law. Branch offices and representative offices of foreign corporations are also permitted, subject to registration with the relevant government authority. General and limited partnerships may involve foreign partners, though local licensing requirements still apply.

Palau law does not have a widely documented statutory conversion procedure equivalent to those in larger common law jurisdictions. Restructuring typically involves dissolving one entity and forming another, though legal counsel should confirm current procedural options under the Business Corporation Act or Palau LLC Act before proceeding.

Corporations and LLCs hold separate legal personality distinct from their owners. General partnerships do not — partners remain personally liable for the firm's obligations. Limited partnerships provide partial separation, protecting limited partners while general partners retain full personal exposure.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.