Key Takeaways

- The Sociedade por Quotas (Lda.) is the most registered business form in Portugal, valued for its flexible capital structure and manageable governance requirements under the Código das Sociedades Comerciais.

- Corporate tax in Portugal is governed by the Código do Imposto sobre o Rendimento das Pessoas Coletivas (IRC), with rates that differ based on company size and profit level.

- Foreign entities entering Portugal face a structural choice between a branch office and a subsidiary, each carrying different liability exposure and fiscal treatment under Portuguese law.

- Sole traders operating as Empresários em Nome Individual accept unlimited personal liability, distinguishing this structure from limited liability vehicles such as the Sociedade Unipessoal por Quotas.

Introduction to Entity Types in Portugal

Portugal sits on the Iberian Peninsula in southwestern Europe, bordered by Spain to the north and east and the Atlantic Ocean to the west and south. It is an independent republic and a member of the European Union, which means companies registered here operate within the EU's single market framework. Company registration falls under the jurisdiction of the Conservatória do Registo Comercial, Portugal's commercial registry, with additional oversight from the Autoridade Tributária e Aduaneira for tax compliance.

The country operates a standard corporate tax system under the Código do Imposto sobre o Rendimento das Pessoas Coletivas (IRC), with rates that vary by company size and profit level.

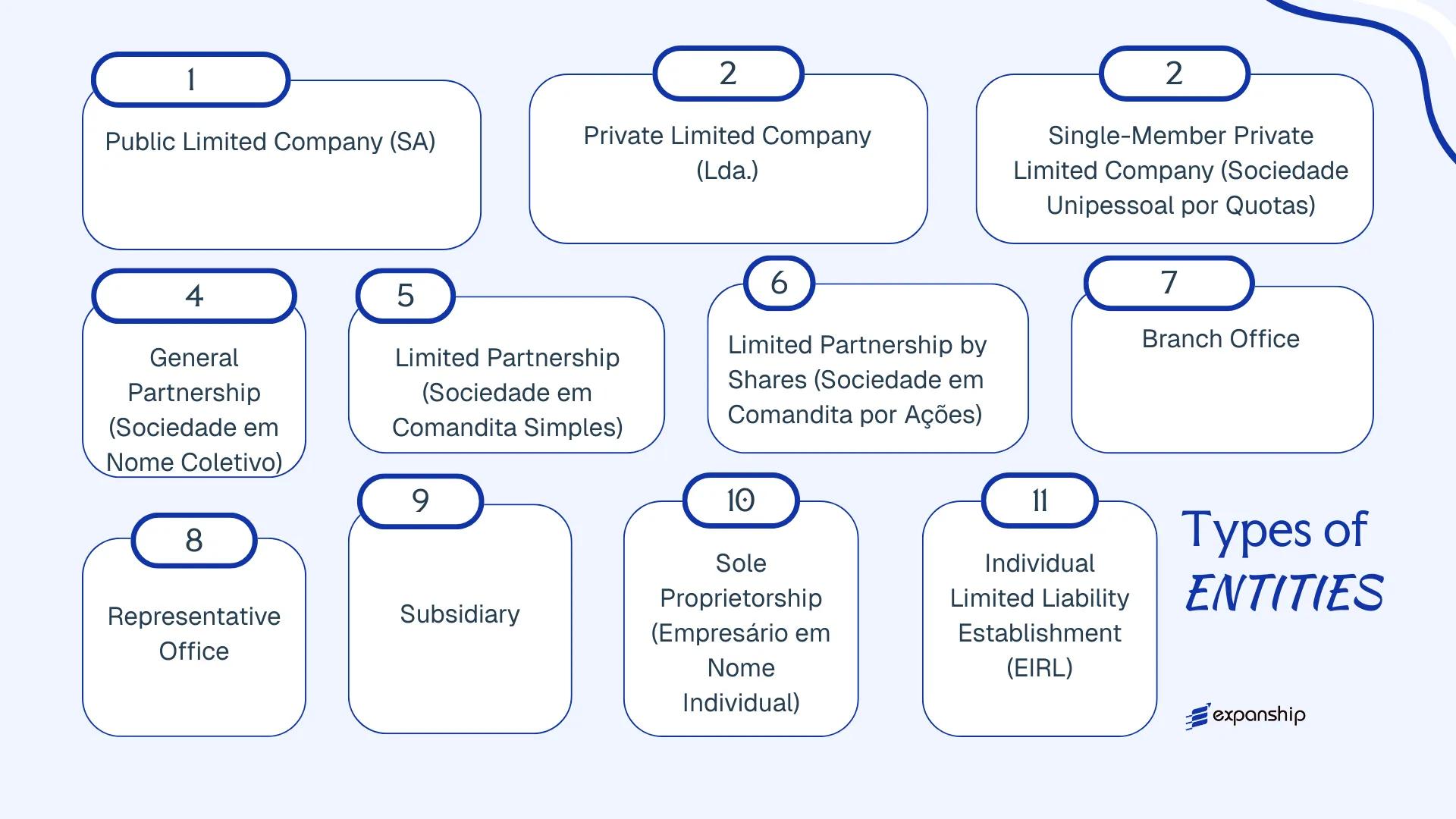

Understanding the types of business entities in Portugal is a prerequisite for any incorporation decision. The main Portuguese legal business structures available include the Sociedade Anónima (SA), Sociedade por Quotas (Lda.), Sociedade Unipessoal por Quotas, Sociedade em Nome Coletivo, Sociedade em Comandita Simples, Sociedade em Comandita por Ações, branch offices, representative offices, subsidiaries, and sole proprietorship forms such as the Empresário em Nome Individual and the Estabelecimento Individual de Responsabilidade Limitada (EIRL). Each entity type carries distinct liability, governance, and tax implications that this article examines in detail.

An Overview of Business Structures in Portugal

Portuguese company law provides several distinct entity types that accommodate different ownership models, liability preferences, and operational scales. The primary legislation governing commercial entities is the Código das Sociedades Comerciais (CSC), established by Decree-Law No. 262/86, with subsequent amendments incorporating EU directives and domestic reforms. Each structure carries different implications for liability, governance, and tax treatment.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedade Anónima (SA) | Public Limited Company | Limited to share capital | Subject to IRC | Permitted | 1 shareholder | IRN / Conservatória | CSC, DL 262/86 |

| Sociedade por Quotas (Lda.) | Private Limited Company | Limited to share capital | Subject to IRC | Permitted | 2 shareholders | IRN / Conservatória | CSC, DL 262/86 |

| Sociedade Unipessoal por Quotas | Single-Member Lda. | Limited to share capital | Subject to IRC | Permitted | 1 shareholder | IRN / Conservatória | CSC, DL 262/86 |

| Sociedade em Nome Coletivo | General Partnership | Unlimited, joint | Subject to IRC | Permitted | 2 partners | IRN / Conservatória | CSC, DL 262/86 |

| Sociedade em Comandita Simples | Limited Partnership | Mixed liability | Subject to IRC | Permitted | 2 partners | IRN / Conservatória | CSC, DL 262/86 |

| Sociedade em Comandita por Ações | Partnership by Shares | Mixed liability | Subject to IRC | Permitted | 2 partners | IRN / Conservatória | CSC, DL 262/86 |

| Branch Office | Foreign Branch | Parent bears liability | Subject to IRC | Permitted | N/A (parent entity) | IRN / AT | CSC; CIRC |

| Representative Office | Non-trading presence | Parent bears liability | Generally exempt | Not permitted | N/A (parent entity) | AT / IRN | CSC; CIRC |

| Empresário em Nome Individual | Sole Trader | Unlimited, personal | Subject to IRS | Permitted | 1 individual | AT / IRN | CSC; CIRS |

| EIRL | Limited Sole Proprietorship | Limited to registered assets | Subject to IRS/IRC | Permitted | 1 individual | IRN / Conservatória | DL 248/86 |

Each of these structures is examined in full in the sections below.

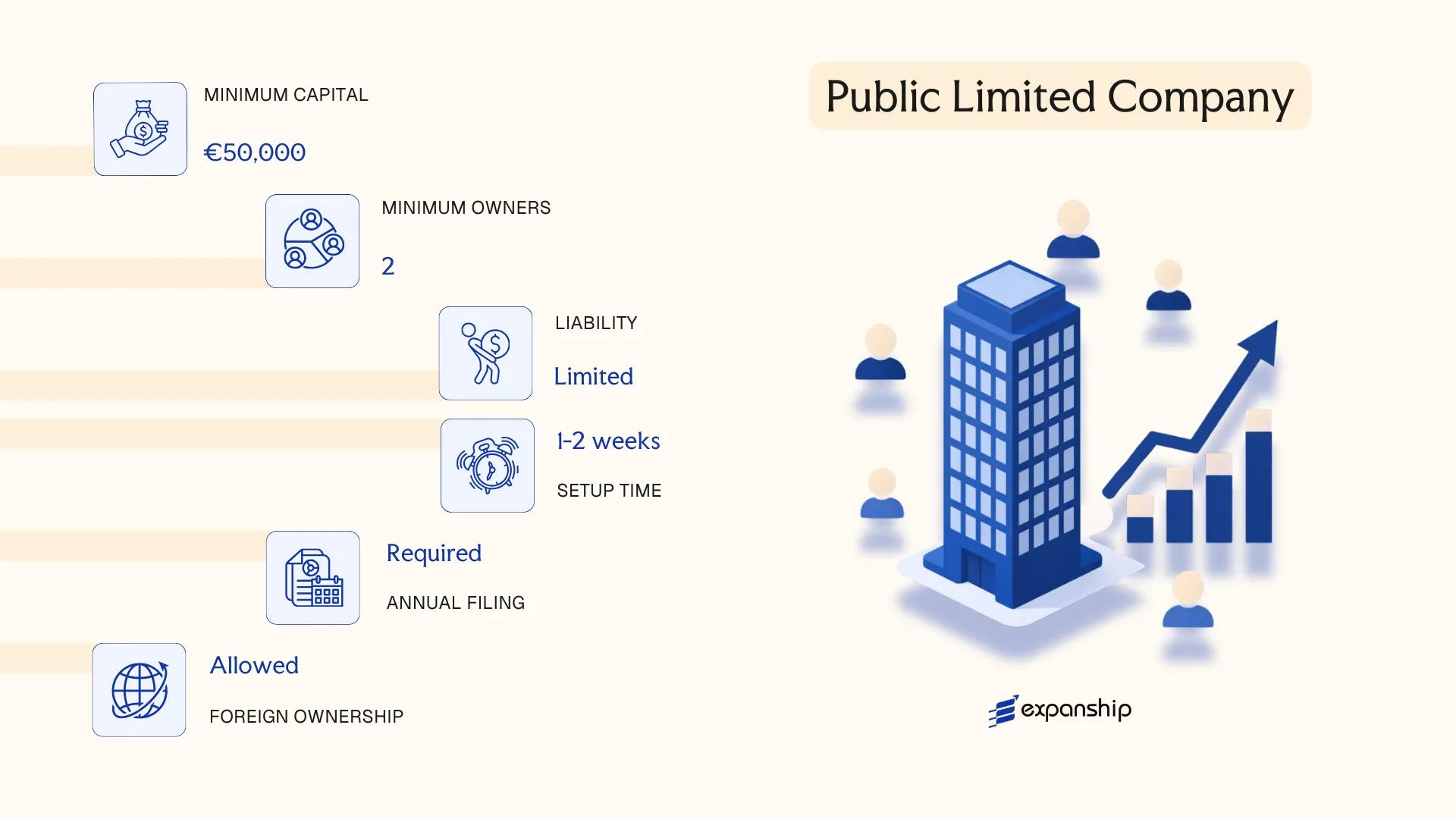

Sociedade Anónima (SA) – Public Limited Company

The Sociedade Anónima Portugal SA company structure is governed by the Portuguese Companies Code (Código das Sociedades Comerciais, Decree-Law No. 262/86), which establishes the foundational rules on formation, governance, and capital. It carries separate legal personality and confers limited liability on its shareholders.

Structurally, the SA sits closer to a capital-markets-oriented entity than most private corporate forms. Shares are freely transferable by default, which makes this structure adaptable for businesses anticipating future public listings or complex ownership arrangements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedade Anónima (SA) | Separate legal personality; limited liability |

| Members | Shareholders (minimum 5; minimum 1 if sole shareholder is the Portuguese State or a public entity) | No statutory maximum on shareholders |

| Governance | Board of Directors (Conselho de Administração) or sole administrator; Supervisory Board (Conselho Fiscal) required above certain thresholds | Three governance model options permitted under the Companies Code |

| Registered Office | Must maintain a registered address in Portugal | No mandatory resident director, but a tax representative may be required for non-EU controllers |

| Share Capital | Minimum EUR 50,000; must be at least 30% paid up at incorporation | Shares may be nominative or bearer (bearer shares now effectively restricted under AML rules) |

| Privacy | Shareholder and director information is publicly registered at the Conservatória do Registo Comercial | Beneficial ownership must be declared in the Registo Central do Beneficiário Efetivo (RCBE) |

Focus Points

- Taxation: Subject to Corporate Income Tax (*IRC*) at the standard rate of 21% (reduced rates apply in Madeira and Azores); VAT (IVA) at the standard rate of 23%; withholding tax applies to dividends, interest, and royalties paid to non-residents at rates typically between 25% and 35%, subject to applicable tax treaties; Stamp Duty (Imposto do Selo) may apply to certain capital transactions.

- Annual Compliance: Annual accounts must be filed with the Informação Empresarial Simplificada (IES) portal; statutory audit required once the entity exceeds two of three thresholds (total assets EUR 1.5M, turnover EUR 3M, 50 employees).

- Treaty Access: Portugal's tax treaty network covers 80+ jurisdictions, making SA entities eligible for reduced withholding rates on cross-border income flows.

- Share Transferability: Shares are freely transferable unless the articles of association impose restrictions; no prior shareholder approval is required by default.

- Conversion: An SA may be converted into a Sociedade por Quotas (Lda.) through a shareholder resolution, subject to compliance with the Companies Code conversion procedure.

Closing

The SA suits holding structures, joint ventures with multiple institutional investors, and businesses planning eventual public market access. Its primary advantage is the free transferability of shares; the principal drawback is the higher minimum capital requirement and more demanding governance obligations relative to private limited forms.

The SA structure is best suited for larger enterprises, institutional joint ventures, or businesses with medium-to-long-term plans for external investment or public listing.

Company Incorporation in Portugal

Incorporate a Sociedade Anónima or other entity type in Portugal with end-to-end support from registration through compliance.

Sociedade por Quotas (Lda.) – Private Limited Company

The Sociedade por Quotas Lda Portugal structure is governed by the Código das Sociedades Comerciais (CSC), enacted in 1986 under Decree-Law No. 262/86. It carries separate legal personality, meaning the entity holds rights and obligations independently of its members.

Liability is capped at the value of each member's subscribed quota, though the CSC permits the articles of association to establish joint and several liability among all members for the total share capital. This hybrid characteristic makes the Lda. a flexible vehicle for both domestic and foreign-owned commercial operations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedade por Quotas (Lda.) | Private limited company with quota-based capital |

| Members | Referred to as quotaholders (sócios); minimum 2, maximum unlimited | Single-member variant exists as a separate legal form |

| Management | One or more gerentes (managers); no board requirement | Managers need not be members or Portuguese residents |

| Local Presence | Registered office (sede social) in Portugal required | No statutory requirement for a resident company secretary |

| Capital | EUR 1 minimum share capital; each quota minimum EUR 1 | No paid-up requirement at a fixed percentage prior to registration |

| Privacy | Quotaholders and managers disclosed in the Registo Comercial | Beneficial ownership registered with the Registo Central do Beneficiário Efetivo (RCBE) |

Focus Points

- Taxation: Subject to IRC (corporate income tax) at the standard rate of 21%, with municipal surtax (derrama) up to 1.5%; VAT applies at standard 23%; dividends paid to non-residents attract 25% withholding tax, reducible under applicable double tax treaties.

- Annual Compliance: Mandatory filing of annual accounts (IES/DA) with the Tax and Customs Authority (AT) and the Registo Comercial; statutory audit not required unless two of three size thresholds are exceeded.

- Economic Substance: No standalone economic substance law, but tax residency and PE rules under the IRC apply; management and control location affects treaty access.

- Conversion: An Lda. may be converted into a Sociedade Anónima (SA) or other commercial form through shareholder resolution and notarial deed under CSC Article 130.

- Transfer Restrictions: Quota transfers to third parties are subject to the right of pre-emption held by existing sócios unless the articles of association waive this right.

Closing Paragraph

The Portugal Lda. private limited company suits trading operations, holding structures, and SME activity where owners prefer simplified governance over public capital markets access. Its principal advantage is low entry capital combined with straightforward management requirements; the primary limitation is that quota transferability to outside parties is restricted by default under the CSC.

Best suited for foreign entrepreneurs and SMEs seeking a cost-effective, privately held operating or holding entity in Portugal without the governance complexity of a public company.

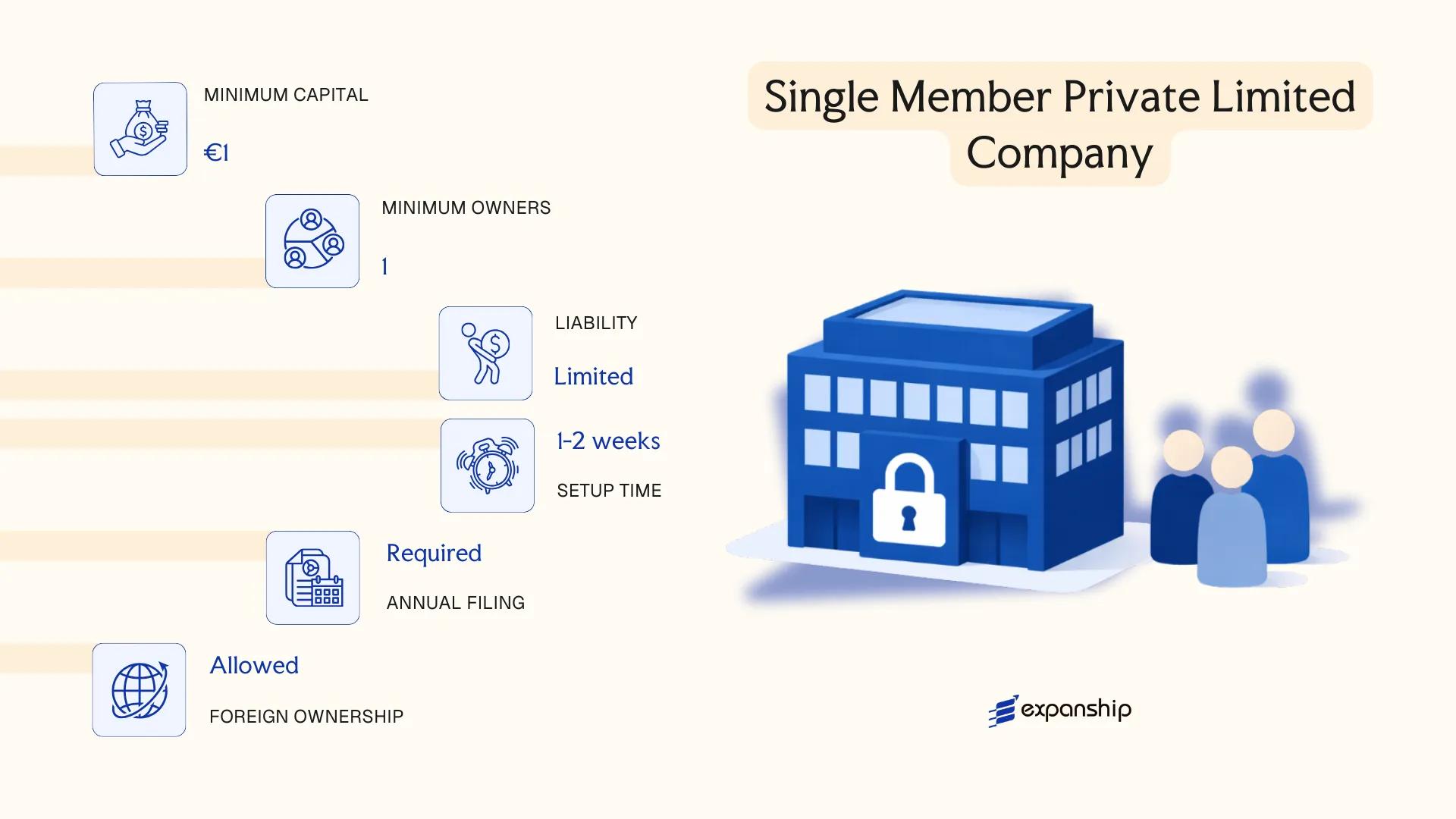

Sociedade Unipessoal por Quotas – Single-Member Private Limited Company

The Sociedade Unipessoal por Quotas Portugal framework derives from the Código das Sociedades Comerciais (CSC), specifically through provisions that permit a single natural person or legal entity to form a private limited company. Unlike a standard Lda., this structure requires exactly one member, making it the default choice for solo entrepreneurs seeking a corporate vehicle with full limited liability.

Legally, the entity holds separate legal personality from its founder. The sole member's exposure is confined to their subscribed capital contribution, and personal assets remain shielded from business liabilities under ordinary circumstances.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedade Unipessoal por Quotas | Regulated under the CSC |

| Members | 1 (sole member only) | Can be a natural person or legal entity; must remain single-member |

| Management | Manager (Gerente) | Sole member may also act as Gerente |

| Registered Office | Required in Portugal | Physical or c/o address accepted |

| Share Capital | No statutory minimum (€1 technically sufficient) | Capital divided into quotas, not shares |

| Privacy | Member details filed with the Conservatória do Registo Comercial | Publicly accessible via the business register |

Focus Points

- Taxation: Subject to IRC (corporate income tax) at 21% standard rate, with reduced rates for SMEs on the first €50,000 of taxable income; VAT registration required once turnover thresholds are met; withholding tax applies to dividends distributed to the sole member.

- Annual Compliance: Annual accounts must be submitted via the IES (Informação Empresarial Simplificada) portal; statutory audit not generally required unless size thresholds are exceeded.

- Economic Substance: No specific substance regime beyond maintaining a registered office and conducting genuine business activity.

- Conversion: Can be converted into a standard Lda. by admitting a second member, without dissolving the entity.

- Restrictions: The sole member cannot simultaneously be the sole member of another Unipessoal por Quotas, per CSC rules.

Closing

A single-member private limited company suits holding structures, freelance professionals, and small trading operations where one founder wants corporate liability protection without partnership complexity. The absence of a minimum capital requirement lowers the entry barrier, though the public disclosure of the sole member's identity offers no confidentiality.

This entity type is best suited for individual entrepreneurs and solo operators who require limited liability and a formal corporate structure without co-founders.

Partnerships in Portugal [Sociedade em Nome Coletivo, Sociedade em Comandita Simples, Sociedade em Comandita por Ações]

Partnership structures in Portugal are governed by the Código das Sociedades Comerciais (Companies Code), established by Decree-Law No. 262/86 of 2 September 1986. Three distinct forms exist: the Sociedade em Nome Coletivo (general partnership), the Sociedade em Comandita Simples (limited partnership), and the Sociedade em Comandita por Ações (partnership limited by shares).

Each form carries separate legal personality upon registration with the Conservatória do Registo Comercial. Liability exposure varies significantly across the three structures, ranging from unlimited personal liability for all partners to hybrid models where only certain partner classes bear unlimited exposure.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedade em Nome Coletivo / Sociedade em Comandita Simples / Sociedade em Comandita por Ações | All registered under the Código das Sociedades Comerciais |

| Members | Partners (general and/or limited depending on form) | Minimum 2 partners; no statutory maximum; Comandita por Ações requires at least one general partner and shareholders |

| Liability | General partners: unlimited; Limited partners / shareholders: limited to contribution | Sociedade em Nome Coletivo — all partners carry unlimited liability |

| Registered Office | Physical address in Portugal required | Maintained on public record at the Conservatória do Registo Comercial |

| Capital | No statutory minimum for general partnership or Comandita Simples; Comandita por Ações requires share capital | Capital divided into shares (ações) only in Comandita por Ações |

| Privacy | Partner names appear in public commercial registry | Limited confidentiality for general partners across all forms |

Focus Points

- Taxation: Partnerships are subject to IRC (corporate income tax) at the standard 21% rate; VAT, withholding taxes, and municipal surtax (derrama) apply where relevant thresholds are met.

- Annual Compliance: Annual accounts must be filed with the Informação Empresarial Simplificada (IES) system; statutory audit requirements depend on entity size thresholds.

- Treaty Access: Portugal's tax treaty network extends to partnerships, though treaty eligibility may depend on how the partner's home jurisdiction classifies the entity for tax purposes.

- Restrictions: General partners in all three forms cannot transfer their participation without unanimous partner consent unless the articles expressly permit otherwise.

Sub-Types

Sociedade em Nome Coletivo

All partners hold unlimited, joint and several liability for the firm's obligations. This structure is rarely used commercially due to the personal exposure it creates for every partner.

Sociedade em Comandita Simples

Two partner classes exist: general partners (comanditados) with unlimited liability and limited partners (comanditários) whose liability is capped at their agreed contribution. Limited partners may not manage the business or act externally on its behalf.

Sociedade em Comandita por Ações

The limited partners' interests are represented by transferable shares (ações), making this form closer structurally to a public company while retaining at least one general partner with unlimited liability. It is governed partly by rules applicable to the Sociedade Anónima.

When to Consider a Partnership

Partnership forms in Portugal are most commonly used for professional service firms or family-owned businesses where partners prefer direct operational involvement over a corporate management structure. The principal limitation across all three forms is the unlimited liability exposure carried by at least one partner class.

These structures are best suited to professional firms or closely held family businesses where partners are willing to accept personal liability in exchange for simplified governance.

Foreign Business Presence in Portugal [Branch Office, Representative Office, Subsidiary]

Establishing a foreign company presence in Portugal is primarily governed by the Código das Sociedades Comerciais (CSC), the Commercial Companies Code, alongside Decree-Law No. 76-A/2006, which introduced procedural modernisation for business registration. Foreign entities operating through a branch or representative office do not create a new legal person under Portuguese law — the parent company retains full liability. A subsidiary, by contrast, is incorporated as a distinct legal entity, most commonly as a Sociedade por Quotas or Sociedade Anónima, and carries its own legal personality.

Registration of all commercial presences is handled through the Conservatória do Registo Comercial (Commercial Registry) and is subject to the Instituto dos Registos e do Notariado (IRN).

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary |

|---|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality | Independent legal entity (Lda. or SA) |

| Liability | Parent bears full liability | Parent bears full liability | Limited to subsidiary's own assets |

| Members / Management | Resident representative (procurador) required | Resident representative required | Directors / managers per chosen entity form |

| Local Presence | Registered address in Portugal; must appoint a legal representative | Registered address required | Registered office required |

| Capital | No minimum capital requirement | No minimum capital requirement | Follows Lda. or SA minimums |

| Tax Registration | Subject to Portuguese IRC (corporate tax) on local income | Generally not subject to IRC if no commercial activity | Full taxpayer; subject to IRC, VAT, and withholding obligations |

Focus Points

- Taxation: Branch profits are subject to IRC at 21% (plus municipal surtax); representative offices conducting no commercial activity fall outside IRC scope; subsidiaries are fully taxable on worldwide income sourced in Portugal, with VAT at 23% standard rate and withholding tax applying to dividends, interest, and royalties paid abroad.

- Tax Treaties: Portugal's network of double taxation agreements (DTAs) applies to subsidiaries and branches; representative offices with no taxable presence may not qualify as a permanent establishment under treaty definitions.

- Annual Compliance: Branches must file annual accounts with the Conservatória do Registo Comercial and submit IRC returns to the Autoridade Tributária e Aduaneira (AT); subsidiaries follow full statutory filing obligations.

- Conversion: A branch can be converted into a subsidiary, though this requires a new incorporation process rather than a simple structural change.

- Activity Restrictions: Representative offices are restricted to promotional, liaison, or market-research activities — conducting commercial transactions through one creates an undeclared permanent establishment risk.

Sub-Types

Branch Office (Sucursal)

A branch, or sucursal, is the standard vehicle for foreign firms conducting active commercial operations without incorporating locally. It must be registered with the Conservatória do Registo Comercial and appoint a resident representative with authority to bind the parent.

Representative Office (Escritório de Representação)

Used for non-commercial activities such as market research, liaison, or promotional functions. No revenue-generating activity is permitted; exceeding this scope may trigger permanent establishment classification by the AT.

Subsidiary

Incorporated as a standalone Portuguese entity, typically an Lda. or SA, the subsidiary is legally and financially separate from its foreign parent. This structure is chosen when the foreign firm requires full operational autonomy, local contracting capacity, or access to EU-specific regulatory frameworks.

Closing

A branch suits foreign firms testing the Portuguese market or managing projects of defined duration, while a subsidiary is the standard choice for sustained commercial operations requiring full contractual and regulatory standing. The principal limitation of the branch structure is that parent-company liability is unlimited and directly exposed.

This structure is best suited to multinational companies entering the Portuguese market as part of a broader European expansion, where the choice between a branch and a subsidiary hinges on liability exposure and anticipated operational scale.

Sole Proprietorship in Portugal [Empresário em Nome Individual, Estabelecimento Individual de Responsabilidade Limitada (EIRL)]

Portugal recognises two primary sole proprietorship structures for individual business operators. The Empresário em Nome Individual (sole proprietorship Portugal Empresário em Nome Individual) is the simpler of the two: it carries no separate legal personality, meaning the owner's personal assets remain fully exposed to business liabilities. Registration is handled through the Registo Nacional de Pessoas Coletivas (RNPC) and the Balcão do Empreendedor portal.

The Estabelecimento Individual de Responsabilidade Limitada (EIRL) introduced a degree of asset segregation without creating a distinct legal person. Under Decree-Law No. 248/86, the proprietor ring-fences a designated pool of assets for business purposes, limiting creditor claims to that defined patrimony — provided accounting records are properly maintained and the two estates remain distinct.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Empresário em Nome Individual / EIRL | EIRL offers patrimony separation; neither form is a legal person |

| Proprietor | Single individual | No partners or shareholders permitted |

| Minimum Capital | None (ENI) / Defined asset pool (EIRL) | EIRL capital must be formally declared and registered |

| Local Presence | Registered business address in Portugal required | Must be declared at registration |

| Liability | Unlimited (ENI) / Limited to declared assets (EIRL) | EIRL liability protection lapses if asset segregation is not maintained |

| Privacy | Owner's name appears in public registry | No anonymity available under either structure |

Focus Points

- Taxation: Both structures are taxed under IRS (personal income tax) via Category B income rules; VAT registration is required if annual turnover exceeds the statutory exemption threshold; no separate corporate tax applies.

- Social Security: The proprietor must enrol with Segurança Social as an independent worker; contributions are calculated on declared professional income.

- Annual Compliance: Submission of the annual IRS declaration (Modelo 3) is mandatory; EIRL additionally requires audited accounts if thresholds under the Commercial Companies Code are met.

- Conversion: An ENI can convert to a Sociedade Unipessoal por Quotas without dissolving operations, which is the standard route when limited liability becomes a priority.

- Restrictions: Neither structure permits equity investment or the admission of partners; scaling through external capital requires a formal change of entity type.

Sub-Types

Empresário em Nome Individual (ENI)

The ENI is the baseline form with no asset separation. It suits micro-scale trade, freelance activity, and service provision where personal liability exposure is considered acceptable or where revenue remains below thresholds triggering more complex compliance requirements.

Estabelecimento Individual de Responsabilidade Limitada (EIRL)

The EIRL was introduced specifically to address the liability gap in sole trading. Its distinguishing feature is the formal declaration of a separated business patrimony registered at the conservatória do registo comercial. Liability protection under this structure is conditional, not absolute.

Closing

Both structures suit early-stage or low-revenue individual operators who require minimal formation costs and straightforward administration, though the absence of separate legal personality limits access to institutional financing and creates personal exposure that incorporated forms avoid.

These structures are best suited to individual freelancers and micro-business operators in Portugal who do not anticipate seeking external investment or incurring significant business liabilities.

How to Choose the Right Entity Type in Portugal

Selecting how to choose a company type in Portugal is a structural decision with legal, tax, and operational consequences that are difficult to reverse once incorporation is complete.

Why Your Entity Choice Matters

The wrong entity type produces concrete, documented outcomes under Portuguese law:

- Registering a branch rather than a subsidiary when conducting autonomous commercial activity means the foreign parent retains unlimited liability for Portuguese operations.

- Selecting the Sociedade Unipessoal por Quotas when you later admit a second shareholder requires a formal conversion to an Lda., triggering notarial and registry fees.

- Choosing a structure ineligible for Portugal's participation exemption regime under the Código do IRC can result in double taxation on dividend distributions from subsidiaries.

- Forming a general partnership (Sociedade em Nome Coletivo) when limited liability is required exposes partners personally to business debts with no statutory cap.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each correspond to distinct legal forms under the Código das Sociedades Comerciais.

- Ownership Structure: Single ownership points toward the Unipessoal por Quotas, while multi-party ventures require an Lda. or SA depending on capital and governance needs.

- Tax Objectives: Eligibility for the RETGS group taxation regime or treaty benefits depends on the entity's legal form and residency status.

- Liability Exposure: Unlimited personal liability attaches to general partners by statute; limited structures require minimum capital thresholds.

- Substance Capacity: If you cannot maintain genuine management presence locally, certain structures carry higher transfer pricing and permanent establishment risk.

- Exit and Conversion: Not all Portuguese entities permit cross-border redomiciliation; plan for restructuring costs if your strategy may change.

Compliance Services for Companies in Portugal

Ongoing compliance support for Portuguese entities, including statutory filings, annual reporting, and Código das Sociedades Comerciais obligations.

Conclusion

Choosing the right structure is one of the most consequential early decisions in any incorporating a business in Portugal guide. Each entity type carries distinct implications for liability, governance, and tax treatment under the Código das Sociedades Comerciais. The Sociedade por Quotas remains the most registered business form in Portugal, favored for its flexible capital structure and straightforward management requirements. The Sociedade Anónima suits firms with complex shareholder arrangements or capital market ambitions. Single-member operations fit within the Sociedade Unipessoal por Quotas, while sole traders operate under the Empresário em Nome Individual framework, accepting unlimited personal exposure. Partnerships occupy a narrower space, typically used for specific professional or family arrangements. Branches and subsidiaries serve foreign entities entering the market under different liability and fiscal conditions. Portugal's expanding tax treaty network and its status as an EU member state continue to shape how international investors approach entity selection here. Expanship's team works directly within this framework to support your registration and compliance obligations.

How Expanship Can Assist You

Expanship's Portugal company formation services cover the full incorporation process, from choosing between a Sociedade por Quotas, a Sociedade Anónima, or a Unipessoal structure, through to registration with the Conservatória do Registo Comercial and obtaining your NIPC (tax identification number) from the Autoridade Tributária e Aduaneira. Our corporate services Portugal assistance is structured around your specific situation, not a generic workflow.

Expanship handles each operational stage on your behalf:

- Document preparation and notarization or apostille where required

- Registered agent and registered office provision in Portugal

- Filing with the Registo Comercial and coordination with RNPC

- Post-incorporation compliance management, including annual reporting obligations

- Banking introduction assistance with Portuguese financial institutions

- Ongoing statutory maintenance aligned with the Código das Sociedades Comerciais

To discuss your specific requirements, contact Expanship Portugal directly.

Frequently Asked Questions (FAQ)

The Sociedade por Quotas (Lda.) is the most frequently registered entity, governed by the Código das Sociedades Comerciais (CSC). Its relatively low minimum share capital and straightforward governance structure make it the default choice for small and medium-sized businesses.

A branch office is not a separate legal entity — it remains an extension of the foreign parent company, which retains full liability for the branch's obligations. A Lda., by contrast, holds its own legal personality and limits liability to the subscribed share capital. From a compliance standpoint, the Lda. carries heavier standalone reporting obligations, but it also allows the business to operate as a fully independent Portuguese entity under Portuguese law.

Among standard commercial structures, the Sociedade por Quotas offers relatively limited public disclosure compared to the Sociedade Anónima (SA). Shareholder details for an SA are more readily accessible through the Registo Comercial, whereas Lda. quota-holder information, while registered, receives less routine public scrutiny. Nominee arrangements are legally permissible under Portuguese law, though ultimate beneficial ownership must be disclosed to the Registo Central do Beneficiário Efetivo (RCBE).

No. The Sociedade Unipessoal por Quotas is specifically designed for sole ownership and permits a single individual or corporate entity to hold all quotas. Partnerships — including the Sociedade em Nome Coletivo and both forms of Sociedade em Comandita — require a minimum of two partners by definition. The SA requires at least five shareholders, unless structured under single-member rules in specific circumstances permitted by the CSC.

Yes. Foreign nationals face no statutory restriction on forming a Lda., SA, or Sociedade Unipessoal por Quotas. The practical prerequisites are obtaining a Portuguese tax identification number (NIF) through the Autoridade Tributária e Aduaneira and, for non-EU residents, potentially appointing a fiscal representative. The branch and representative office routes are also available specifically for foreign companies seeking a local presence without incorporating a separate entity.

The CSC expressly permits the transformation of commercial companies from one legal form to another — for instance, converting a Lda. into an SA. The process requires a shareholders' resolution, updated articles of association, and re-registration with the Conservatória do Registo Comercial. Not all conversions follow the same procedural path; transformations involving partnerships generally carry additional requirements related to partner liability.

Not all of them. The Sociedade por Quotas, SA, Sociedade Unipessoal por Quotas, and Sociedade em Comandita por Ações each hold separate legal personality under the CSC. The Empresário em Nome Individual (sole trader) does not — the individual and the business are legally the same person, meaning personal assets are exposed to business liabilities without limitation. The EIRL was introduced specifically to address this gap for sole operators, though its use remains limited in practice.

The Empresário em Nome Individual has the most minimal formal compliance footprint, with no requirement for separate audited accounts or corporate governance procedures. However, that simplicity comes without liability protection. Among limited-liability structures, the Sociedade Unipessoal por Quotas generally imposes fewer ongoing obligations than the SA, which is subject to statutory audit requirements and more extensive disclosure obligations under the CSC and applicable securities regulations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.