Key Takeaways

- Palestine's company registration framework is governed primarily by Companies Law No. 12 of 1964 and administered by the Companies Controller Department within the Ministry of National Economy.

- The Limited Liability Company is the most commonly registered entity in Palestine, favored for its combination of limited liability protection and relatively low capital requirements.

- Foreign businesses entering Palestine can establish a presence through branch offices or representative offices rather than incorporating a standalone local entity.

- Public Shareholding Companies (Al-Sharika Al-Mosahamah Al-Aama) are structured for large-scale capital raises with broad investor participation, while Private Shareholding Companies suit closely held ventures requiring formal governance.

Introduction to Entity Types in Palestine

Located in the Middle East along the eastern coast of the Mediterranean Sea, the Palestinian territories — comprising the West Bank and the Gaza Strip — share borders with Israel, Jordan, and Egypt. Palestine operates under a distinct political framework as a partially recognized state, with the Palestinian Authority exercising administrative and legislative authority over civil and commercial matters in designated areas.

Company registration and commercial licensing fall under the jurisdiction of the Palestinian Ministry of National Economy, which oversees business formation through its Companies Controller Department. The tax regime is territorial in nature, with corporate income tax applicable to profits generated within the territories.

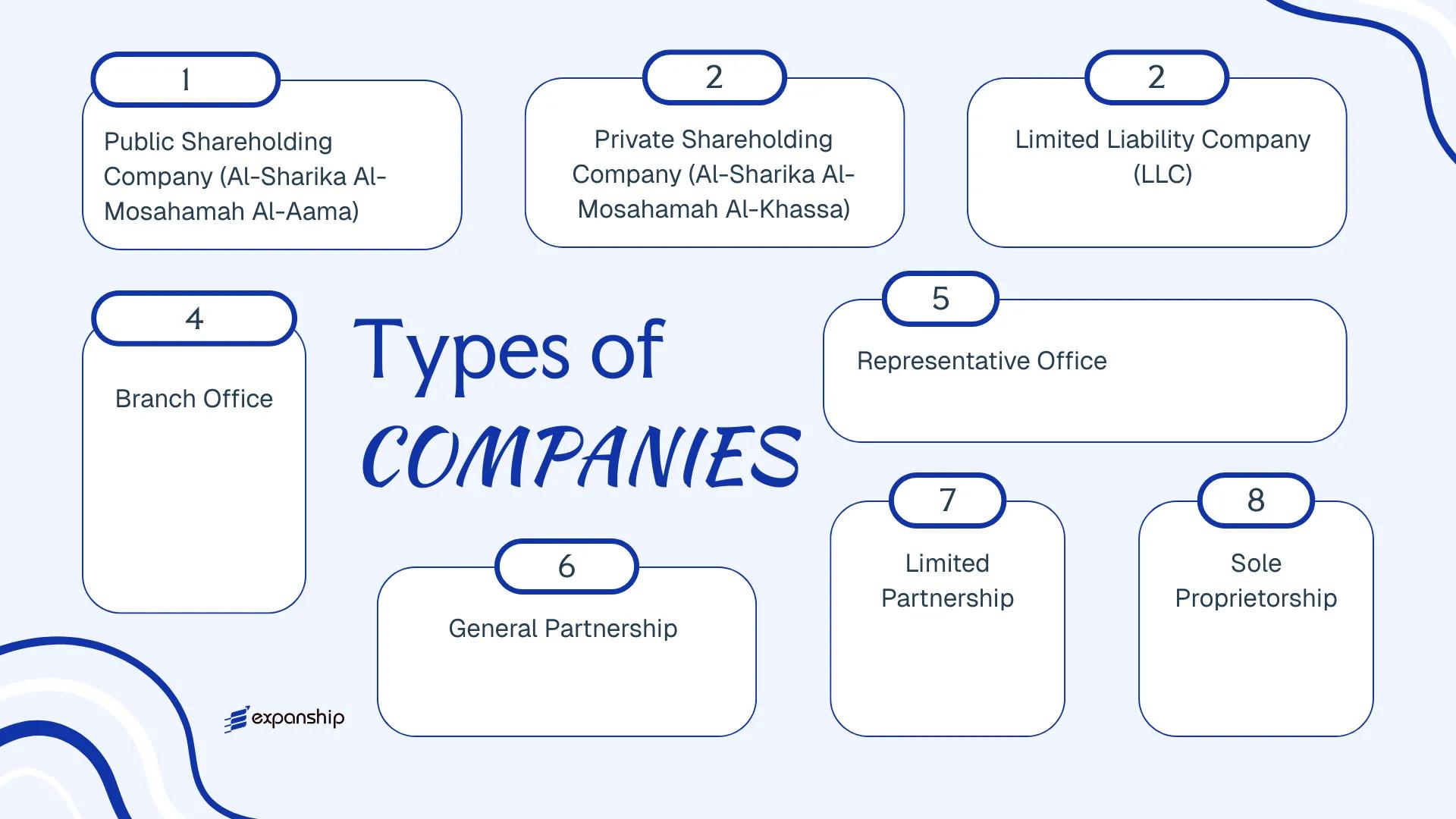

Businesses registering under Palestinian commercial law can choose from several legal structures: the Public Shareholding Company, the Private Shareholding Company, the Limited Liability Company, the General Partnership, the Limited Partnership, the Sole Proprietorship, and foreign-entry vehicles such as branch offices and representative offices. Each structure carries distinct requirements around capital, liability, governance, and ownership that will affect how your business operates locally.

An Overview of Business Structures in Palestine

Palestinian commercial law recognises several distinct entity types, each governed primarily by the Companies Law No. 12 of 1964 and its subsequent amendments, along with sector-specific regulations administered by the Palestinian Ministry of National Economy. An overview of business structures in Palestine shows that available forms range from sole proprietorships to public shareholding companies, each suited to a different scale and purpose of commercial activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Shareholding Company | Corporate | Limited to shares | Taxed | Permitted | 3 founders | Ministry of National Economy | Companies Law No. 12/1964 |

| Private Shareholding Company | Corporate | Limited to shares | Taxed | Permitted | 2 shareholders | Ministry of National Economy | Companies Law No. 12/1964 |

| Limited Liability Company | Corporate | Limited to capital | Taxed | Permitted | 1 member | Ministry of National Economy | Companies Law No. 12/1964 |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Permitted | N/A | Ministry of National Economy | Companies Law No. 12/1964 |

| Representative Office | Non-trading foreign presence | Parent liable | Generally exempt | Not permitted | N/A | Ministry of National Economy | Companies Law No. 12/1964 |

| General Partnership | Unincorporated | Unlimited, joint | Taxed | Permitted | 2 partners | Ministry of National Economy | Companies Law No. 12/1964 |

| Limited Partnership | Unincorporated | Mixed | Taxed | Permitted | 2 partners | Ministry of National Economy | Companies Law No. 12/1964 |

| Sole Proprietorship | Individual trader | Unlimited | Taxed | Permitted | 1 individual | Ministry of National Economy | Companies Law No. 12/1964 |

Each of these structures is examined in full in the sections below.

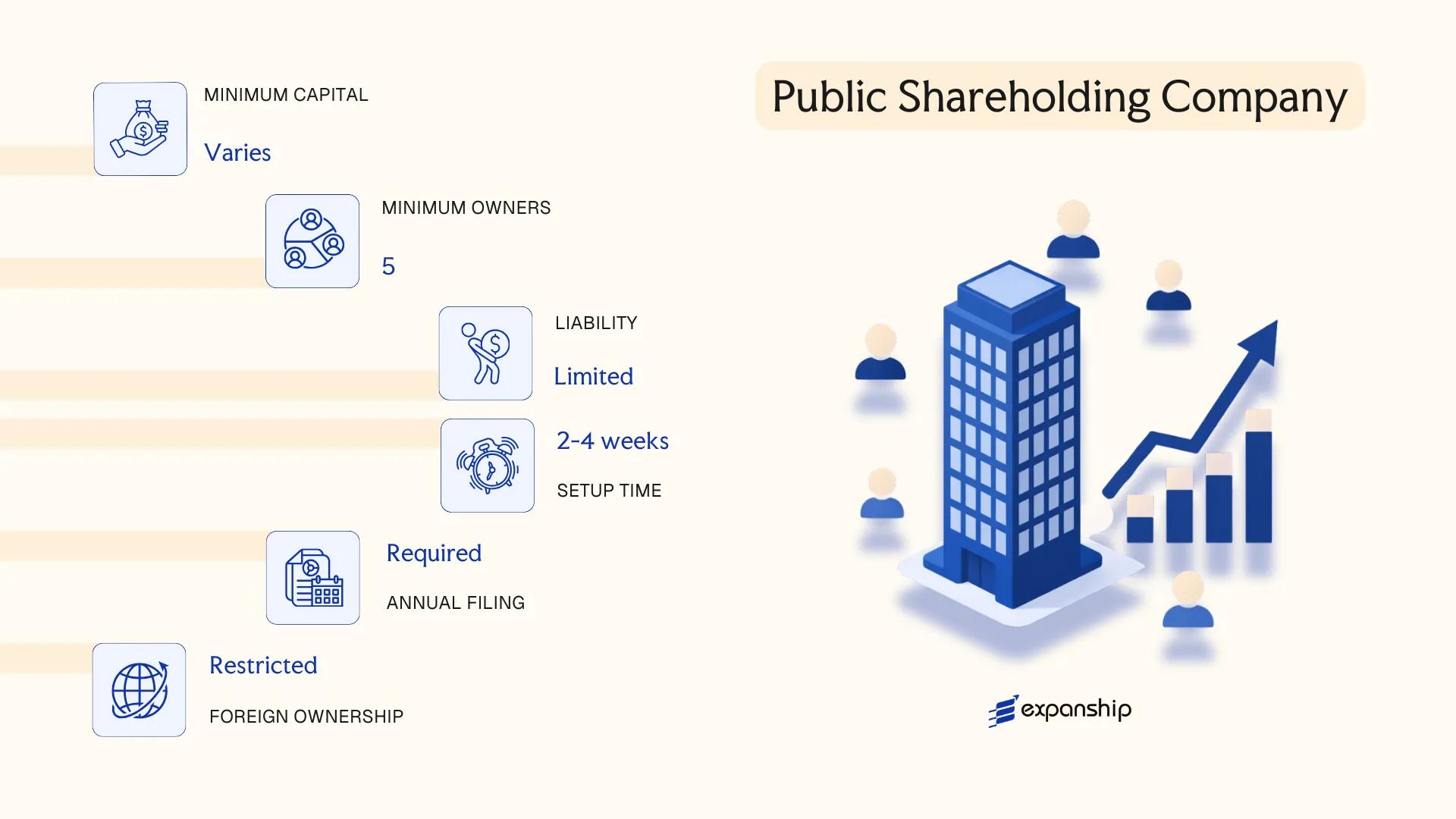

Public Shareholding Company (Al-Sharika Al-Mosahamah Al-Aama)

The Al-Sharika Al-Mosahamah Al-Aama Palestine structure is the most capital-intensive corporate form available under Palestinian law, governed primarily by the Companies Law No. 12 of 1964 (as amended) and regulated by the Companies Controller within the Palestinian Ministry of National Economy. It carries a distinct legal personality, separate from its shareholders, and imposes liability limited to the value of subscribed shares.

Shares in this entity are transferable on the Palestine Exchange (PEX), making it the applicable structure for businesses seeking public capital markets access. Regulatory oversight extends beyond registration to include ongoing supervision by the Palestinian Capital Market Authority (PCMA).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Joint Stock Company | Separate legal personality; shareholders bear no personal liability beyond share value |

| Members | Shareholders | Minimum 7 founding shareholders; no statutory maximum |

| Governance | Board of Directors (minimum 3, maximum 13 members) | Board elected by General Assembly; independent director requirements apply for listed firms |

| Local Presence | Registered office in Palestinian territory required | Must maintain operational headquarters; PEX listing requires PCMA-approved prospectus |

| Capital | Minimum paid-up capital typically set by PCMA; denominated in ILS or USD | Exact threshold varies by sector; financial institutions face higher minimums |

| Privacy | Shareholder register and financial statements are publicly disclosed | Listed companies must file periodic disclosures with PCMA |

Focus Points

- Taxation: Corporate income subject to Palestinian Income Tax Authority rates; VAT obligations apply to taxable supplies; dividends may attract withholding tax depending on recipient residency; no general capital gains exemption exists for share disposals.

- Annual Compliance: Audited financial statements, annual general assembly, and periodic PCMA filings are mandatory for listed entities.

- Economic Substance: No formal economic substance regime exists under current Palestinian legislation, though physical presence is inherent to this structure.

- Conversion: Conversion from a private shareholding company or LLC is permissible under the Companies Law, subject to regulatory approval and capital verification.

- Restrictions: Foreign ownership restrictions may apply in certain sectors; all share issuances require PCMA approval prior to public offering.

Closing

This structure suits large-scale commercial operations, infrastructure ventures, and businesses requiring broad equity distribution or eventual public listing. The primary advantage is unrestricted access to public capital markets; the principal limitation is the administrative burden of continuous regulatory disclosure and PCMA supervision.

Best suited for large enterprises or joint ventures seeking to raise capital from the public through the Palestine Exchange.

Company Incorporation in Palestine

Incorporate a public or private company in Palestine with guidance on regulatory filings, capital requirements, and PCMA compliance.

Private Shareholding Company (Al-Sharika Al-Mosahamah Al-Khassa)

The Al-Sharika Al-Mosahamah Al-Khassa Palestine framework originates from the Palestinian Companies Law No. 12 of 1964, as amended, which remains the primary legislation governing corporate structures in the West Bank. This entity is a private shareholding company — a closed joint stock company whose shares cannot be offered to the public or listed on a stock exchange.

As a distinct legal person, the private JSC carries its own rights and obligations separate from its shareholders. Liability is confined to each shareholder's capital contribution, making it a preferred structure for family-owned groups and closely held businesses.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Closed Joint Stock Company | Separate legal personality; shares are non-publicly tradable |

| Members | Shareholders and a Board of Directors | Minimum 3 shareholders; maximum 50 shareholders |

| Local Presence | Registered office address required | Must be maintained within the registration jurisdiction |

| Capital | Palestinian Pound (ILS widely used); minimum capital applies under law | Capital divided into equal-value registered shares |

| Share Transfer | Restricted; subject to shareholder approval or pre-emption rights | Articles of Association govern transfer conditions |

| Privacy | Shareholder register maintained with the Companies Controller | Register may be inspected; limited public disclosure |

Focus Points

- Taxation: Subject to corporate income tax under Palestinian Income Tax Law; VAT registration obligations apply to qualifying revenue thresholds; withholding tax applies to dividends and certain payments.

- Annual Compliance: Mandatory submission of audited financial statements to the Companies Controller; annual general meeting required.

- Economic Substance: No formal substance regime currently legislated, though registered office and operational presence are required in practice.

- Conversion: Can be converted to a public shareholding company upon meeting minimum shareholder and capital thresholds under the Companies Law.

- Restrictions: Shares may not be publicly offered or listed; shareholder count cannot exceed 50.

Closing

The private JSC formation in Palestine suits family businesses, joint ventures, and mid-size trading or holding operations where ownership control must remain with a defined group of shareholders. The capped membership and restricted share transfer provisions offer governance predictability, though they equally limit the entity's ability to raise capital from outside investors.

Best suited for closely held businesses or family groups seeking corporate structure with limited liability and controlled ownership.

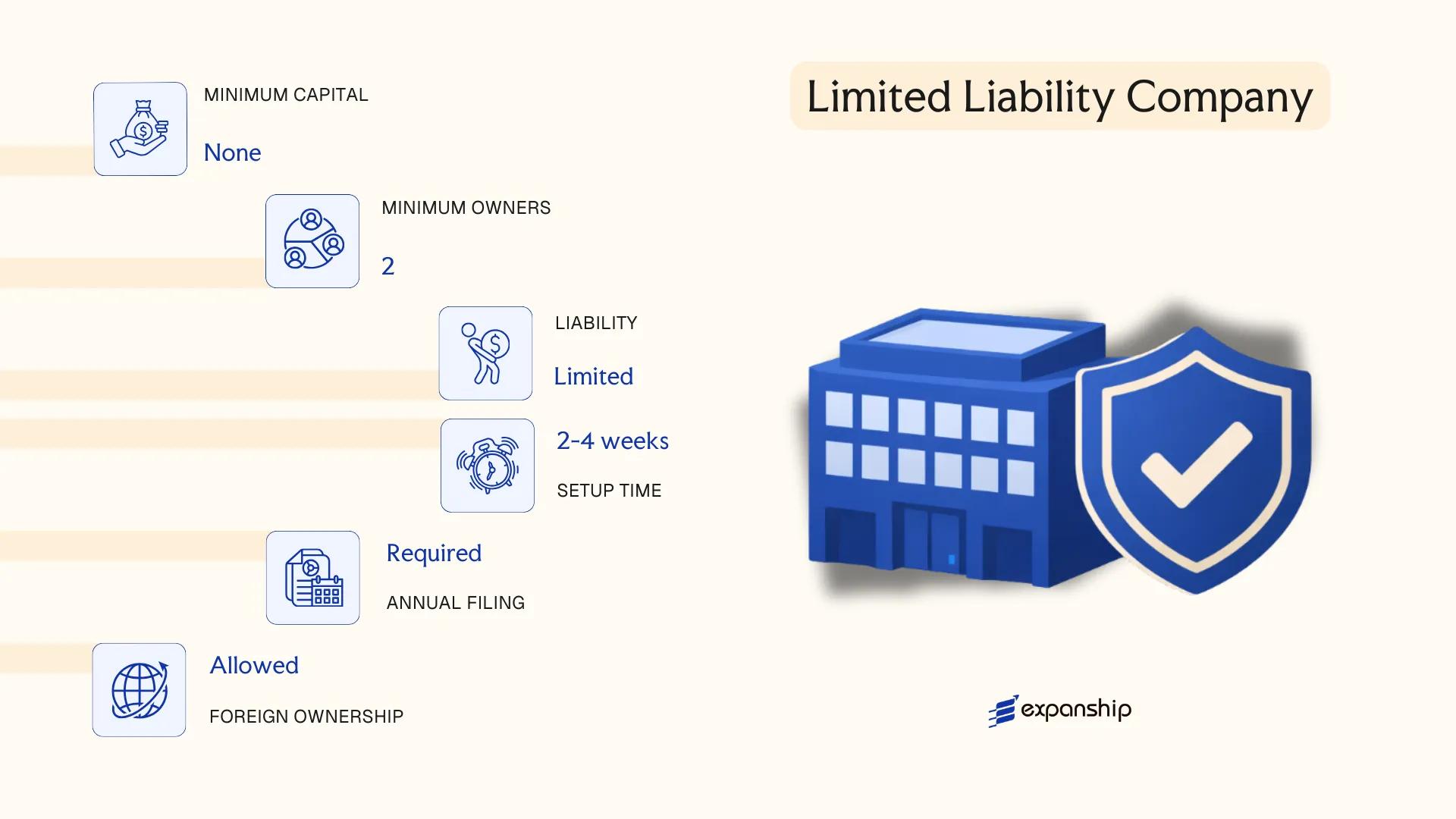

Limited Liability Company (LLC)

Limited liability company formation Palestine is governed by the Companies Law No. 12 of 1964, as amended, which remains the primary legislative framework administered by the Palestinian Companies Controller. The LLC is structured as a hybrid entity — it carries a separate legal personality distinct from its members, while capping member liability at the value of their subscribed shares.

Registration is handled through the Companies Controller at the Ministry of National Economy, and the firm must be incorporated with a memorandum of association authenticated before a licensed notary.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (Sharika Zat Mas'ouliya Mahdouda) | Separate legal personality; governed by Companies Law No. 12 of 1964 |

| Members | 2–50 members | Cannot issue shares to the public; membership transfer subject to existing member approval |

| Management | One or more managers (not a board) | Managers appointed by members; need not be Palestinian nationals |

| Local Presence | Registered office address required within the Palestinian territories | No mandatory resident agent requirement, but a local address is obligatory |

| Capital | No statutory minimum under general provisions; denominated in Jordanian Dinars or USD in practice | Capital divided into equal quotas, not publicly tradeable shares |

| Privacy | Member names disclosed in the Companies Registry | Registry records are publicly accessible |

Focus Points

- Taxation: Corporate income tax applies at a flat 15% rate under the Palestinian Income Tax Law; VAT is levied at 16% on taxable supplies; no separate withholding tax regime specific to LLCs, though dividend distributions may attract income tax obligations at the member level.

- Annual Compliance: Annual financial statements must be filed with the Companies Controller; audited accounts are required where member count or capital thresholds trigger the obligation.

- Restrictions: An LLC cannot offer its quotas to the general public or list on a stock exchange; membership transfer requires consent of other members unless the memorandum provides otherwise.

- Conversion: An LLC may be converted to a shareholding company structure through a formal resolution and re-registration process with the Companies Controller.

- Treaty Access: Access to double taxation treaties depends on the member's tax residency, as Palestine has a limited treaty network; professional advice on treaty applicability is necessary before structuring.

Closing Paragraph

The LLC structure suits trading operations, professional services firms, and family-owned businesses seeking operational flexibility without public disclosure of internal financials beyond what the registry requires. The principal advantage is liability limitation without the governance burden of a full shareholding company; the corresponding drawback is the restriction on capital-raising, since quotas cannot be offered publicly.

Best suited for small to mid-sized private businesses, joint ventures between two or more parties, and foreign investors seeking a locally incorporated entity with contained liability and direct management control.

Foreign Business Structures in Palestine [Branch Office, Representative Office]

Establishing a foreign company branch office in Palestine is governed primarily by the Companies Law No. 12 of 1964, as applied and administered through the Palestinian Ministry of National Economy. A branch office operates as an extension of its parent company rather than a distinct legal entity, meaning the parent bears full liability for the branch's obligations incurred within the Palestinian territories.

A representative office serves a narrower function, restricted to promotional and liaison activities without the authority to generate revenue or enter into commercial contracts directly. Both structures require registration with the Companies Controller at the Ministry of National Economy, and foreign firms must appoint a local authorised representative during the registration process.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Liable Party | Parent company bears full liability | Parent company bears full liability |

| Permitted Activities | Full commercial and trading operations | Liaison, marketing, and research only — no revenue generation |

| Local Presence | Registered local address; appointed authorised representative required | Registered local address; appointed authorised representative required |

| Capital Requirement | No statutory minimum; parent's capital referenced in registration | No statutory minimum |

| Privacy | Parent company details disclosed on public register | Parent company details disclosed on public register |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at the standard rate applicable to Palestinian-registered entities; VAT registration obligations apply if turnover thresholds are met, and withholding tax may apply on remittances to the foreign parent.

- Economic Substance: No formal substance regime equivalent to offshore jurisdictions; however, the branch must demonstrably operate from a registered address with an active local representative.

- Annual Compliance: Branches are required to file audited financial statements and renew their registration annually with the Companies Controller.

- Treaty Access: Palestine has a limited network of bilateral investment and tax treaties; treaty benefits available to the parent entity may not automatically extend to the branch.

- Restrictions: Representative offices are expressly prohibited from invoicing clients or signing commercial contracts; breach of this boundary can result in deregistration.

Sub-Types

Branch Office

A branch conducts the full scope of the parent company's business activities within the Palestinian territories and can enter contracts, employ staff, and generate revenue in its own operational name, though all legal accountability flows to the parent entity.

Representative Office

Permitted only for non-commercial functions such as market research, promoting the parent's services, and maintaining client relationships. Registration of a representative office in Palestine follows a separate, lighter-touch process, but the operational restrictions are strictly enforced.

Closing

Both structures suit foreign firms seeking a foreign business presence in Palestine without incorporating a standalone local entity, with the branch being appropriate for active trading and the representative office for pre-market or exploratory activities. The principal limitation for both is the absence of limited liability protection, as all obligations remain with the parent company.

Foreign companies opening a branch in Palestinian territories that already operate established entities abroad and require an operational presence without the administrative burden of a separately capitalised local company.

Partnership-Based Structures [General Partnership, Limited Partnership]

General partnership registration in Palestine is governed by the Companies Law No. 12 of 1964, which remains the primary legislative framework for partnership-based entities. Both general and limited partnerships carry distinct liability profiles and are registered with the Companies Registration Directorate under the Palestinian Ministry of National Economy.

Under Palestinian law, a general partnership does not confer separate legal personality distinct from its partners — each partner bears unlimited, joint liability for the firm's obligations. A limited partnership introduces a hybrid structure, separating actively managing general partners from passive limited partners whose liability is capped at their contributed capital.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Partners | Minimum 2; no statutory maximum | Minimum 1 general partner + 1 limited partner |

| Liability | Unlimited for all partners | Unlimited for general partners; limited for passive partners |

| Management | All partners may manage | Only general partners manage |

| Capital | No statutory minimum | No statutory minimum |

| Local Presence | Registered office in Palestinian territory required | Registered office in Palestinian territory required |

| Privacy | Partner names appear in public registration records | Partner names appear in public registration records |

Focus Points

- Taxation: Partnerships are generally taxed at the partner level under Palestinian income tax rules; no separate corporate income tax applies at the entity level, though professional advice should confirm current VAT and withholding treatment.

- Annual Compliance: Annual financial reporting and renewal of registration with the Companies Registration Directorate is required.

- Restrictions: Foreign nationals may face limitations on partnership participation depending on the business activity sector.

- Conversion: Conversion to a limited liability company or shareholding company is permissible under the Companies Law with regulatory approval.

Sub-Types

General Partnership

All partners share management authority and bear unlimited personal liability. This structure is most common among professional service providers and small family-run trading businesses.

Limited Partnership

A limited partner contributes capital but takes no role in daily management; doing so risks losing liability protection. This arrangement suits investors seeking participation without operational exposure.

Closing

Palestinian partnership structures serve trading, professional services, and small-scale commercial operations where partners accept direct liability in exchange for simpler formation requirements. The primary advantage is ease of establishment; the key drawback is unlimited personal exposure for general partners.

Partnership structures suit small, closely held businesses or professional practices where partners know each other well and accept personal liability for the firm's obligations.

Sole Proprietorship

Sole proprietorship setup in Palestine is governed by the Companies Law No. 12 of 1964, as amended, alongside the Commercial Registry regulations administered by the Palestinian Ministry of National Economy. Unlike incorporated entities, a sole proprietorship carries no separate legal personality — the owner and the business are legally the same, meaning personal assets are fully exposed to business liabilities.

Registration is handled through the Ministry of National Economy's commercial registry, where the proprietor must register under their own name or a trade name. Individual business registration in Palestine requires submitting identification documents, proof of address, and a description of the intended commercial activity. Foreign nationals face restrictions on operating as sole traders and generally require additional approvals.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated individual business | No separate legal personality from the owner |

| Members | Single proprietor | No shareholders, directors, or partners |

| Local Presence | Registered business address required | Must be a physical address within the Palestinian territories |

| Capital | No statutory minimum | Owner contributes capital at discretion |

| Privacy | Owner's name appears on public registry | Trade name permitted but owner identity disclosed |

| Liability | Unlimited personal liability | Owner's personal assets are fully at risk |

Focus Points

- Taxation: Subject to personal income tax under the Palestinian Income Tax Law; no separate corporate tax applies, though VAT registration may be required depending on turnover thresholds.

- Annual Compliance: Annual renewal of the commercial registration with the Ministry of National Economy is required to maintain active status.

- Conversion: Can be converted into an LLC or other incorporated structure, though this requires a new registration process rather than a simple amendment.

- Restrictions: Foreign nationals are generally prohibited from self-employed registration in Palestine as sole traders without specific regulatory approval.

- Treaty Access: As an unincorporated structure with no separate legal identity, access to double tax treaty provisions is limited or unavailable.

Closing

A sole proprietorship suits Palestinian residents operating small-scale service businesses or local trading activities where administrative simplicity outweighs liability concerns. The primary advantage is low setup cost and minimal formalities; the significant drawback is unlimited personal liability with no legal separation between the owner and the business.

Best suited for individual Palestinian residents running low-risk, small-scale commercial activities who do not require liability protection or external investment.

How to Choose the Right Entity Type in Palestine

Choosing the right company type in Palestine depends on factors that are specific to your operational model, ownership structure, and regulatory obligations under the Palestinian Companies Law No. 12 of 1964 (as amended).

Why Your Entity Choice Matters

The structure you register has binding legal and financial consequences.

- Registering a foreign branch to conduct local commercial activity without meeting the Ministry of National Economy's registration requirements exposes the business to penalties and potential forced closure.

- Selecting a structure that lacks access to the Palestinian tax framework may disqualify your business from applicable exemptions or treaty positions available to properly registered entities.

- Forming a private shareholding company when a limited liability company would suffice imposes minimum capital requirements and governance obligations that increase your annual administrative costs without corresponding benefit.

- Choosing a structure misaligned with your intended exit strategy — particularly if redomiciliation or conversion is anticipated — may require full dissolution and re-registration, as Palestinian law does not provide a straightforward conversion mechanism across all entity types.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as banking or insurance, and passive asset-holding each correspond to distinct permissible structures under Palestinian law.

- Ownership Configuration: A single founder or a multi-party joint venture will face different governance requirements across an LLC versus a shareholding company.

- Minimum Capital: Your available capital at registration directly narrows which entity types are legally accessible.

- Liability Exposure: The degree to which you require personal liability separation from business obligations should guide the choice between partnership-based and corporate structures.

- Public Disclosure Tolerance: Shareholding companies have greater public filing obligations than LLCs; if ownership privacy matters, this distinction is material.

- Operational Substance: If your business will maintain physical premises and employees locally, a fully registered Palestinian entity is appropriate; purely representative functions warrant a representative office.

The full text of the Palestinian Companies Law should be reviewed alongside current Ministry of National Economy registration requirements before making a structural decision.

Corporate Compliance Services in Palestine

Maintain your Palestinian entity in good standing with ongoing compliance support across filing, reporting, and regulatory obligations.

Conclusion

Incorporating a company in Palestine guide readers through a framework shaped primarily by the Companies Law No. 12 of 1964, as amended, and overseen by the Companies Controller at the Ministry of National Economy. Each structure registered under this framework carries a distinct profile: the Public Shareholding Company suits large-scale capital raises with broad investor participation; the Private Shareholding Company fits closely held ventures requiring structured governance; the LLC remains the most commonly registered entity, favored for its combination of limited liability and relatively low capital requirements. General and Limited Partnerships apply where personal relationships between founders drive the business model, while a Sole Proprietorship serves individual traders operating without partners.

Palestine's regulatory environment continues to develop, with ongoing efforts to modernize commercial registration procedures and expand bilateral investment treaty coverage. Professional guidance aligned with current Ministry of National Economy requirements will help your business structure hold up as that framework continues to evolve.

How Expanship Can Assist You

As a dedicated corporate services provider Palestine businesses and foreign investors rely on, Expanship works directly with the requirements set by the Palestinian Companies Controller at the Ministry of National Economy. From selecting between an LLC, a Private Shareholding Company, or a Branch Office, through to completing registration filings, our work is grounded in the specific procedural and documentary requirements of Palestinian company law.

Expanship's Palestine company formation assistance covers the full scope of what your business needs from day one through ongoing compliance.

- Document preparation and official legalization

- Registered agent and registered office provision

- Filing liaison with the Companies Controller

- Post-incorporation compliance management

- Banking introduction assistance

For a detailed conversation about your specific situation, reach out to Expanship Palestine.

Frequently Asked Questions (FAQ)

The Limited Liability Company (LLC) is the most frequently formed structure under Palestinian corporate law. Its combination of capped shareholder liability, a comparatively modest minimum capital requirement, and flexible internal governance makes it the default choice for small to mid-sized domestic and foreign-owned ventures.

A branch office is a direct extension of its foreign parent, carries no separate legal personality, and is restricted in the scope of commercial activity it may undertake locally. An LLC, by contrast, is an independent legal entity under Palestinian law and may conduct the full range of permitted commercial activities. From a compliance standpoint, the LLC faces more extensive ongoing filing obligations, while the branch remains liable through its parent.

The Private Shareholding Company does not require public disclosure of its shareholder register to the same degree as a Public Shareholding Company, whose ownership structure is subject to broader regulatory reporting. Nominee arrangements are not formally prohibited, though their use must align with Palestinian beneficial ownership disclosure requirements.

A sole proprietorship is, by definition, a one-person structure, and an LLC can be formed with a single member under applicable regulations. Partnerships — both general and limited — require a minimum of two partners, so a sole individual cannot form those structures unilaterally.

Foreigners may register an LLC, a Private Shareholding Company, or a Public Shareholding Company, subject to any sector-specific restrictions under Palestinian investment law. A foreign company may also establish a branch or representative office rather than incorporating a new local entity. Foreign ownership ceilings can apply in certain regulated industries, so sector verification is necessary before proceeding.

Palestinian company law permits structural conversions, most commonly from an LLC to a shareholding company as a business scales. The process requires approval from the Companies Controller and involves updated constitutional documents, re-registration, and capital adjustments where applicable. Not all conversion pathways are equally straightforward; a partnership converting to a corporate form, for example, involves more complex procedural steps.

No. Sole proprietorships and general partnerships do not confer separate legal personality, meaning owners bear direct personal liability for business obligations. The LLC, Private Shareholding Company, and Public Shareholding Company each constitute distinct legal persons under Palestinian law, and liability is generally contained within the entity.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.